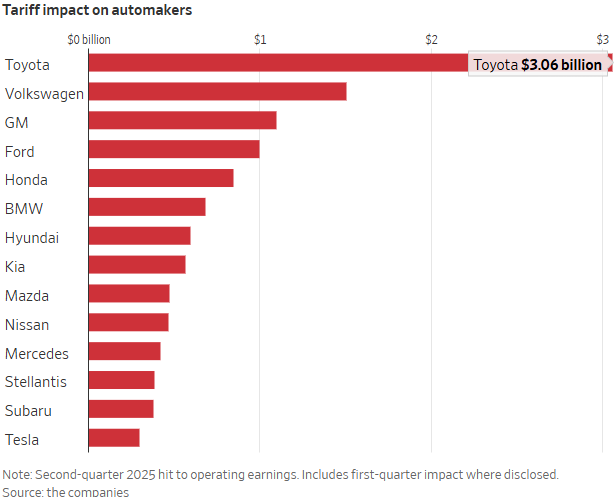

While tariff threats dominate headlines, automakers face a structural shift that could reshape the global auto industry. In response to steep auto import duties, manufacturers are being nudged toward “local for local” production models- an expensive and time-consuming pivot. Per the Wall Street Journal article “Auto Industry Takes $12 Billion Hit From Trade War”:

Beyond the continuing cost of tariffs, automakers in the U.S., Japan, South Korea and Europe face years of retooling and supply-chain tweaks to adjust to the new realities. This comes after they spent heavily to reshape factories for electric vehicles.

The obvious responses to tariffs are to raise prices and move production to the U.S. But both are hard for carmakers to do quickly, potentially saddling them for years to come.

Carmakers like GM, Toyota, and Hyundai are ramping up U.S. production, but not without cost. Toyota alone expects a $9.5 billion hit from tariffs this fiscal year. Meanwhile, the top 10 global automakers are projected to post their lowest profits since the pandemic. This structural shift raises a key question for investors: Will the market continue to reward reshoring narratives, or start penalizing margin compression and increased capital expenditures?

The logic behind “Made in America” is bullish for domestic output, but short-term earnings pain could overshadow long-term benefits. Stock prices reflect not just earnings but the trajectory of those earnings. And right now, that trajectory appears to be bending lower. While regionalized production may benefit U.S. jobs, it poses near-term headwinds for profit growth, and by extension, for stock market sectors tied to global auto trade.

What To Watch Today

Earnings

- No notable earnings releases

Economy

- No notable economic releases.

Market Trading Update

This past week, markets were driven by trade policy shocks, monetary policy developments, and solid corporate earnings, creating a push-and-pull dynamic for investor sentiment. President Trump’s announcement of sweeping “reciprocal” tariffs, doubling duties on Indian imports and imposing broad levies on semiconductors and pharmaceuticals, rekindled trade war concerns and injected fresh geopolitical risk into the outlook. However, that was offset by Apple’s announcement that it would inject $600 billion into building factories in the U.S. to bypass those tariffs. The positive response to Apple’s deal with the White House sent the stock and the Nasdaq higher on the week.

The policy backdrop shifted further when Trump nominated Stephen Miran to the Federal Reserve, a move widely interpreted as signaling a more dovish tilt and raising expectations for possible rate cuts. Overseas, the Bank of England delivered a 25-basis-point cut, dropping its rate to 4%, though its narrow 5–4 split vote underscored internal divisions and the challenges of managing policy amid stagflation pressures.

On the corporate front, earnings season is winding down but has provided pockets of support and disappointment. Earnings beats received a muted reaction. Companies beating estimates only outperformed by 55 bp vs. the 101 bp historical average. That lack of performance was likely due to overly low analyst expectations. Meanwhile, earnings misses are being punished nearly twice as much as usual.

📈Technical Backdrop

After a sharp reversal from record highs last week, the S&P 500 struggled this week with a fragile technical profile, but not yet a broken one. The index’s retreat from the 6,350 area has pulled it back inside the rising channel that has defined advance since May, after testing the bottom of that trend channel last Friday. This week was marked by a choppy, up-and-down advance with money flows remaining weak amid a decline in momentum.

Despite the pullback, the longer-term structure remains constructive. The 50-day moving average (~6,200) is still trending higher above the 200-day (~5,900), confirming the primary uptrend. So far, this correction has been modest, with retail buyers stepping in to buy every dip. So far, the market action is more about digestion than a correction. However, despite this week’s relatively bullish action, a retest of the 50-day remains a possibility over the next few weeks.

As noted, momentum signals have softened, the relative strength Index has rolled down from overbought territory and bounced off the neutral 50 level, and money flows are slowing. These signals suggest short-term risk to the bullish narrative until improvement is evident. Market breadth has also narrowed, as shown, with fewer than 60% of S&P 500 stocks above their 50 and 200-day moving averages, highlighting the reliance on mega-cap technology to prop up index levels.

Outlook: Neutral. The uptrend remains intact, but weakening breadth, fading momentum, and elevated volatility warrant a more selective approach. A decisive break below 6,150 would tilt the outlook bearish, while stabilization above that level could quickly restore the bull trend. For now, patience and disciplined risk management are essential.

🔑 Key Catalysts Next Week

After choppy trading action this past week, traders will focus on the CPI and PPI reports, retail sales, and what that means for the Federal Reserve’s monetary policy outlook.

Overall Risk Outlook: Cautiously Bearish

With CPI and PPI poised to test the Fed’s rate-cut narrative, a packed Friday data slate, and geopolitical tensions from tariff deadlines and U.S.–Russia talks, markets face an elevated risk of a pullback given the weaker underlying technicals and seasonal volatility patterns.

The Week Ahead

This week’s economic data kicks off tomorrow with July’s CPI report. The core inflation rate has remained subdued for several months as tariffs have yet to spark noticeable inflationary pressures. The consensus expects core inflation to increase to 0.3% MoM in July, likely reflecting marginal impacts from tariffs. Headline inflation has remained similarly subdued, with the consensus expecting a decrease to 0.2% MoM in July.

PPI data on Thursday will give us a glimpse into manufacturers’ ability to pass through tariff-related costs to retailers. There was no change in the PPI for June, but the consensus is for both headline and core PPI to rise 0.2% MoM in July. PPI is seen as an early indicator of inflationary pressures in CPI. Thus, a soft reading would further strengthen the case for a September rate cut given the recent revisions to employment data. Finally, Friday will bring July retail sales data and the August University of Michigan consumer sentiment gauge.

The Debt And Deficit Problem Isn’t What You Think

I understand the concerns about rising debt levels. However, the problem of rising debt levels for the U.S. is NOT a default but a continued degradation of economic growth. Let’s start this discussion with a basic fact—without continued increases in debt, there would be very little to no economic growth. This is because all government debt winds up in the economy and the household’s balance sheet through lending, credit, or direct payments. We can view this by looking at the dollars of debt required to create a dollar of economic growth. Since 1980, the increase in debt has usurped the entire economic growth. The problem with the growth in debt is that it diverts tax dollars away from productive investments into debt service and social welfare.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.