MMT, or Modern Monetary Theory, offers a new monetary “logic” that allows the government to spend without concern for debts and deficits. Does MMT seem too good to be true or do MMT’s fatal flaws render it troublesome?

On the heels of unprecedented spending and unmanageable deficits, MMT is gaining popularity. Its acceptance is not surprising as its principles justify reckless fiscal behavior. MMT advocates are loud in their support for unlimited spending and mock the thought of “too much debt.” We often fail to hear them highlight the critical governor in their theory designed to limit inflation.

The current bout of inflation exposes MMT’s fatal flaw.

What is MMT

“Free healthcare and higher education, jobs for everyone, living wages and all sorts of other promises are just a few of the benefits that MMT can provide.” –MMT and its Fictional Discipline

Before discussing two inherent flaws with MMT, it’s worth briefly summarizing what the theory entails.

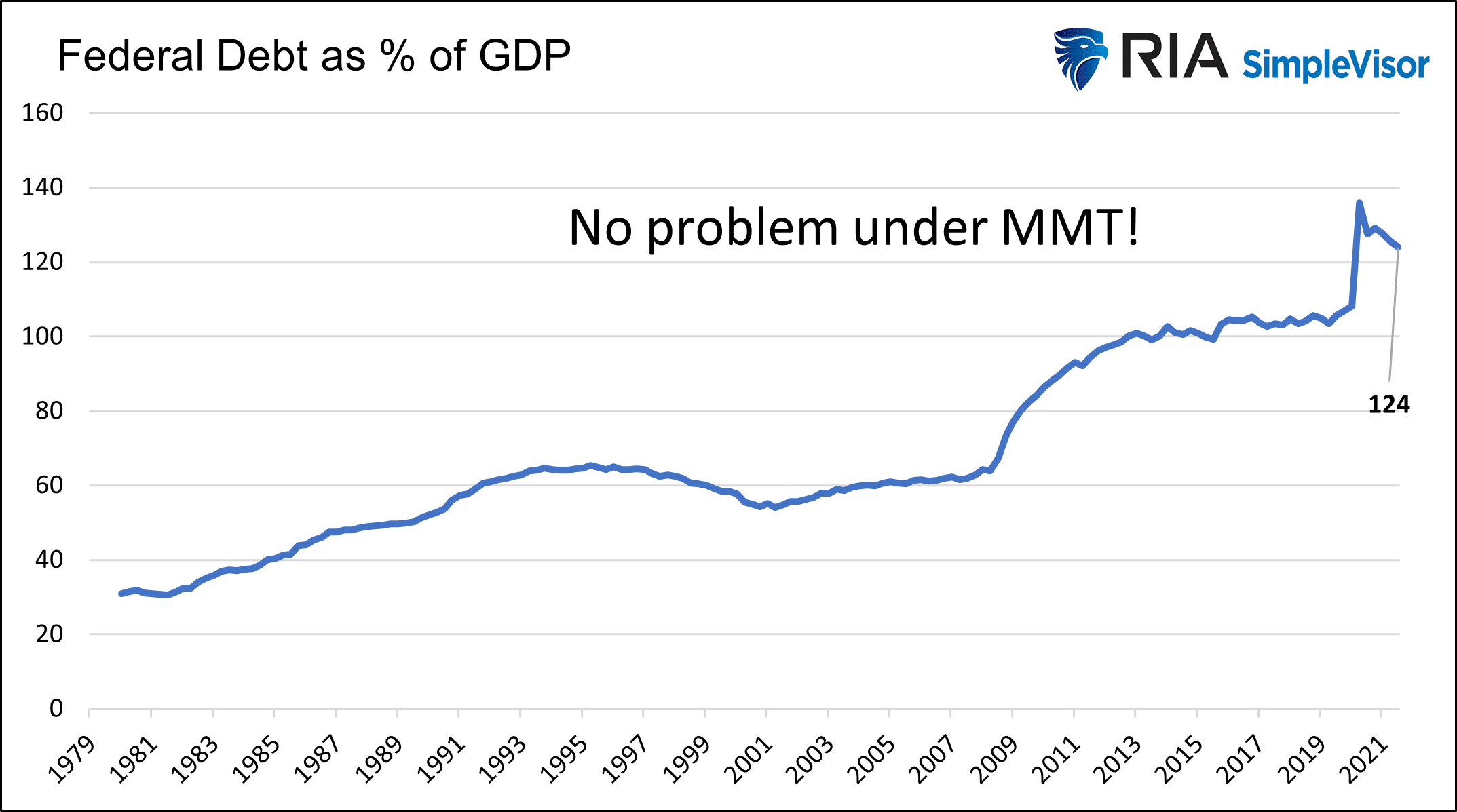

At its core, MMT states government can create money via fiscal policy. Currently, all “new” money is lent into existence by the banks. Under MMT, Congress and the President would get a new printing press and print to their heart’s content. Debt would no longer be needed to fund government shortfalls. The current deficits become irrelevant because the government can print money to satisfy its debt requirements. Accordingly, without debt and deficits, MMT is a dream for politicians.

The only flaw with the theory is inflation. If the economy reaches full employment and inflation becomes a risk, the discipline of MMT says taxes should be imposed on individuals and corporations to limit spending and reduce inflationary pressures. Measuring and managing inflation is where MMT will fail.

MMT’s Fatal Flaw #1 – Measuring Inflation

The first flaw is in the measurement of inflation. In the article mentioned above, we state:

“Inflation is impossible to calculate. Inflation is impossible to calculate. No, that is not a typo. For emphasis, let us put it another way. Inflation is impossible to calculate.

The point that inflation is impossible to calculate cannot be overstated.”

Inflation is not measurable in any uniform matter. We can compute general gauges of inflation, but the degree of accuracy is highly questionable. Just consider the difference between inflation for a 45-year-old couple with three kids living in New York City and a retired couple living in New Mexico. MMT requires precision that is not possible.

Making the task even trickier is the conflict of interest between the users and reporters of inflation data. Government agencies report on inflation. Congress and the President control these agencies. As such, those in power manipulate inflation data and have a strong interest in reporting low inflation numbers. MMT increases the need to underreport inflation.

For more, read up on the Boskin Commission in MMT and its Fictional Discipline.

MMT’s Fatal Flaw #2 – Political Willpower

The second and more vexing problem with inflation is politicians’ willpower and vested interests. Should we expect elected officials to reduce spending and raise taxes when inflation is problematic? One needs only to consider the current environment when answering the question.

Current Political Willpower

Inflation is running at 6.8%, over three times higher than the Fed’s stated 2% objective. The media and populace are steadily increasing pressure on the administration and Congress to combat inflation. At the same time, wages are growing but at a lesser rate than inflation. Average hourly earnings are up 4.8%. While historically strong, real wages, factoring in inflation, are down 2%.

With stimulus largely spent, consumers are reducing savings, increasing credit card debt, and withdrawing equity from their houses. These are signs that lower- and middle-income classes are falling behind.

Under MMT, the government should be raising taxes to reduce consumption to fight inflation. Furthermore, they would need to raise taxes on all income classes to be effective. Raising taxes on just the wealthy would barely dent the spending habits of the rich and does not affect a large percentage of total consumption. Demand would not be meaningfully affected unless lower and middle incomes are taxed.

Do you think Joe Biden and the Democrat-controlled Congress would entertain raising taxes on the middle class and poor today? Absolutely not! They know they will lose control of Congress next year if they try.

Our opinion is not biased. There are very few politicians on either side of the aisle willing to raise taxes and lose their power.

As politicians constantly remind us, retaining control tends to trump doing the right thing in Washington. Such a mindset bodes poorly for managing inflation under MMT.

Proof in the Fed

If you seek more evidence of Washington’s lack of willpower to tackle inflation, look at the Fed. Despite red hot inflation and maximum employment, this “politically independent body” runs crisis-level monetary policy. They have dragged their feet for the last nine months as inflation soared well above their objective. The Fed is finally concluding inflation might be a problem as inflation hits 40-year highs.

The Fed can curtail inflation by halting QE and quickly raising rates. Doing so would likely harm the financial markets and slow economic activity. While they appear to be willing to take steps to reduce their stimulus slowly, it will not be at the pace warranted by inflation. The Fed cares more about markets than their mandate. Like politicians, Fed members are fearful of losing their power.

Summary

Inflation is MMT’s fatal flaw. Inflation is the fly in MMT’s ointment.

The current high inflation episode exposes MMT’s fatal flaw. Despite the flaw, we suspect the push for MMT will continue, and the rules around inflation will change, allowing for more inflation. Without stringent inflation guidelines and willpower, MMT is nothing more than a printing press for the government.

Historically, MMT-like schemes have always resulted in default. We do not doubt that the adaption of MMT leads us on that same path.