Is it 1999 or 2007? Retail investors flood the market as speculation grows rampant with a palpable exuberance and belief of no downside risk. What could go wrong?

Do you remember this commercial?

The Etrade commercial aired during Super Bowl XLI in 2007. The following year, the financial crisis set in, markets plunged, and investors lost 50%, or more, of their wealth.

However, this wasn’t the first time it happened.

The same thing happened in late 1999. This commercial was aired 2-months shy of the beginning of the “Dot.com” bust as investors once again believed “investing was as easy as 1-2-3.”

Why this trip down memory lane? (Other than the fact the commercials are hilarious to watch.) Because this is typical of the exuberance seen at the peaks of bull market cycles.

So, what are the signs we are seeing today.

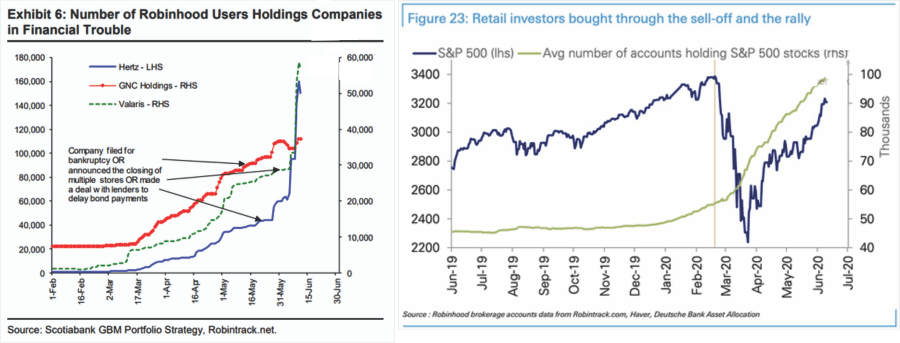

- Retail investors are chasing bankrupt companies like Hertz and Chesapeake Energy

- Hertz, a company in bankruptcy, is issuing stock with a disclaimer the shares are likely worthless.

- Investors chasing companies with extremely poor fundamentals.

- Investing tips coming from individuals with no experience.

https://twitter.com/stoolpresidente/status/1274076383615090688?s=20

Investing is simple. Just pick some letters out of a Srabble bag, buy it, and it goes up.

Its so easy a “baby can do it.”

Or in this case, it like “stealing from the rich to give to the poor.”

Retail Investors Go Robinhood

As Barron’s recently noted:

“Free trading app Robinhood has added more than three million retail accounts in 2020, and now has over 13 million. The median age of its retail customer is 31. The Covid-19 lockdowns and the plunge in markets in March persuaded millions of new investors to open accounts. Some of the action appears to be from people who would otherwise be gambling or betting on sports—both of which were shut down.”

Just like we saw in 1999 and 2008, “day trading” has had a resurgence from “message boards” on AOL to live blogs and video feeds on social media.

“The new generation tends to convene on social media. Beyond TikTok, retail investors chat on forums like Reddit and Twitter, sharing internet memes and jokes about stocks, and even posting self-deprecating charts showing their worst losses.

A former Goldman Sachs partner, Joseph Mauro, joked on Twitter that his son’s friends are never free anymore to play videogames during the day because they’re too busy trading stocks. “He is 10,” Mauro added.”

The irony is that Robinhood really isn’t “stealing from the rich.” In reality, they are “getting rich by stealing from the poor.” As is always the case, there is no “free lunch,” as Robinhood bundles orders and then“sells” the flows to major hedge funds for profit. Those hedge funds then “front run” the “Robinhooders” taking advantage of their trading. (If this wasn’t massively profitable for hedge funds they wouldn’t pay millions for the data.)

Retail Discovers A New “Toy”

These “newbie” retail investors are not trading based on fundamentals, earnings, estimates, products or market values, but rather talking up stocks driven by pure momentum. Robinhood makes the “research” even easier by posting the top holdings of its users.

They are then leveraging what cash they have through option contracts and margin debt to boost their buying power.

Google search trends for "call options" and "day trading" is pretty telling: pic.twitter.com/C3mjoAOEv1

— Jesse Felder (@jessefelder) June 10, 2020

The problem with options is that when you are wrong, you can lose 100% of your investment.

The problem with margin is that when you are wrong, you can lose more than 100% of your investment.

However, given the current belief by “daytraders” that there is no downside risk, then why not leverage up and “get rich quick?”

Speculative Fervor in U.S. Stocks Surges to ‘Stunning’ Levels https://t.co/xv9G5zdSSA pic.twitter.com/GbsLObPuWP

— Jesse Felder (@jessefelder) June 9, 2020

After all, in this “new paradigm” of “no risk” investing there are only two rules:

A lot of people are asking me if Airlines and Cruises will go up tomoroew. My answer is see tenet #1 of the #DDTG playbook

1. Stocks only go up

2. When in doubt whether to buy or sell see Rule #1— Dave Portnoy (@stoolpresidente) June 7, 2020

But this is the nature of what happens in a late-stage bull market cycle.

Still In A Bull Market

“But we had a 35% selloff in March, how can we be in a late stage bull market?”

This was a point I discussed in “Was March A Bear Market?”

“Such brings up an interesting question. After a decade-long bull market, which stretched prices to extremes above long-term trends, is the 20% measure still valid?

To answer that question, let’s clarify the premise.

- A bull market is when the price of the market is trending higher over a long-term period.

- A bear market is when the previous advance breaks, and prices begin to trend lower.

This distinction is important.

- “Corrections” generally occur over very short time frames, do not break the prevailing trend in prices, and are quickly resolved by markets reversing to new highs.

- “Bear Markets” tend to be long-term affairs where prices grind sideways or lower over several months as valuations are reverted.

Given the trend was never broken, valuations were never reversed, and “speculative greed” wasn’t extinguished, the “bull market” remains intact.

Topping Process

The markets quick recovery from the March lows further bolstered the “speculative greed” in the market which has now manifested itself in current behaviors.

The risk, however, is the economic recession which will impair the fundamentals of the markets over the next several quarters making it harder to justify current valuations. As I noted in the chart above, the current rally could be part of a bigger “topping” process which may take young traders by surprise.

I have noted the market may be in the process of a topping pattern. The 2018 and 2020 peaks are currently forming the “left shoulder” and “head” of the topping process. Such would also suggest the “neckline” is the running bull trend from the 2009 lows.

A market peak without setting a new high that violates the bull trend line would define a “bear market.”

What Could Cause The Market To Break?

As noted by Mish Shedlock recently, the Federal Reserve itself has noted six downside risks to the markets and the economy.

“In its semiannual monetary report to the Senate Finance Committee the Fed warns of six downside risks. The risks are not spread evenly. Low wage earners and small businesses are particularly vulnerable.

Please consider the Fed’s Monetary Policy Report to the Senate Committee on Banking, Housing, and Urban Affairs and to the House Committee on Financial Services. The report is 66 pages long and is full of interesting charts and comments.

Let’s start with Powell’s statement on risk: ‘Despite aggressive fiscal and monetary policy actions, risks abroad are skewed to the downside.’

Six Downside Risks

- The future progression of the pandemic remains highly uncertain.

- The collapse in demand may ultimately bankrupt many businesses.

- Unlike past recessions, services activity has dropped more sharply than manufacturing—with restrictions on movement severely curtailing expenditures on travel, tourism, restaurants, and recreation and social-distancing requirements and attitudes may further weigh on the recovery in these sectors.

- Disruptions to global trade may result in a costly reconfiguration of global supply chains.

- Persistently weak consumer and firm demand may push medium- and longer-term inflation expectations well below central bank targets.

- Additional expansionary fiscal policies— possibly in response to future large-scale outbreaks of COVID-19—could significantly increase government debt and add to sovereign risk.”

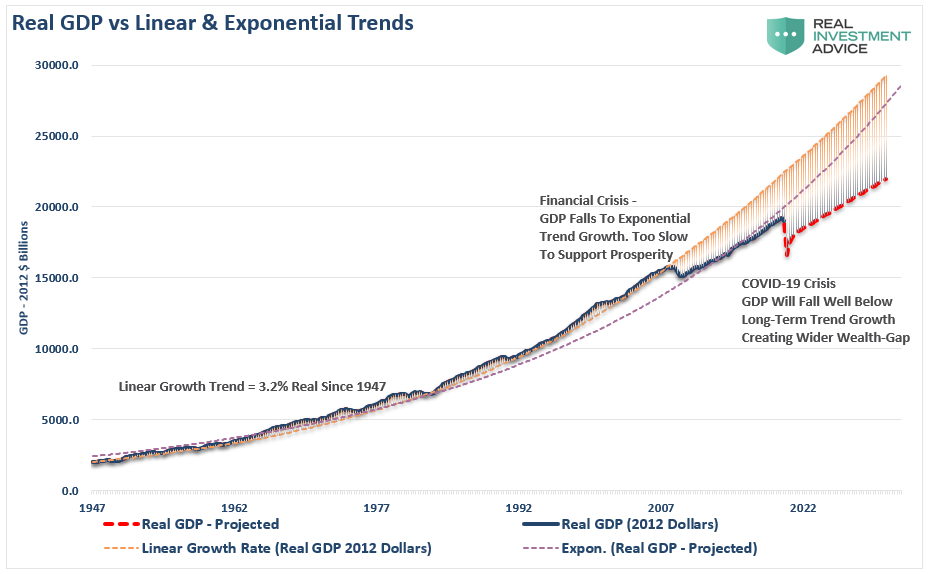

The biggest risk, is the 6th point where massive increases in debts and deficits retard long-term economic growth.

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.”

Retail “Investor” Or “Speculator?”

In today’s market the majority of investors are simply chasing performance.

But, this isn’t “investing,” it’s “speculation.”

Think about it this way.

If you were playing a hand of poker, and were dealt a “pair of deuces,” would you push all your chips to the center of the table?

Of course, not.

The reason is you intuitively understand the other factors “at play.” Even a cursory understanding of the game of poker suggests other players at the table are probably holding better hands which will lead to a rapid reduction of your wealth.

Investing, ultimately, is about managing the risks which will substantially reduce your ability to “stay in the game long enough” to “win.”

Robert Hagstrom, CFA penned a piece discussing the differences between investing and speculation:

“Philip Carret, who wrote The Art of Speculation (1930), believed “motive” was the test for determining the difference between investment and speculation. Carret connected the investor to the economics of the business and the speculator to price. ‘Speculation,’ wrote Carret, ‘may be defined as the purchase or sale of securities or commodities in expectation of profiting by fluctuations in their prices.’”

Chasing markets is the purest form of speculation. It is simply a bet on prices going higher rather than determining if the price being paid for those assets are selling at a discount to fair value.

Graham & Dodd

Benjamin Graham, along with David Dodd, attempted a precise definition of investing and speculation in their seminal work Security Analysis (1934).

“An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

There is also very important passage in Graham’s The Intelligent Investor:

“The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern. We have often said that Wall Street as an institution would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise the stock exchanges may some day be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.”

Surviving The Game

Regardless of whether you believe fundamentals will ever matter again is largely irrelevant. What is important is that periods of excess speculation always end the same way.

For now, Dave Portnoy has garnered a legion of followers. However, Dave’s financial future is quite secure after he sold his company to Penn National for $450 million. So, when things go wrong in the market, he will be just fine financially. However, for the host of inexperienced, over-confident, millennials who follow him, many have the financial livelihoods on the line.

I get it. If you are one of our younger readers, who have never been through an actual “bear market,” I wouldn’t believe what I am telling you either.

However, after living through the Crash of ’87, managing money through 2000 and 2008, and navigating the “Great Crash of 2020,” I can tell you the signs are all there.

A real bear market will happen. When? I don’t have a clue. But it will be an unexpected, exogenous event that triggers the selling.

It always appears easiest at the top.

More importantly, at bottoms, retail investors will not be wanting to buy stocks.