Evergrande- Why Most Analysis Is Dead In The Water

There is a lot more to the failure of China’s Evergrande company than meets the eye. For the last year, China has been taking steps to curb speculation and promote economic productivity.

At $16 billion, (China’s GDP) is no longer that far from that of the U.S. ($22 billion) and nearly three times Japan, the world’s third-largest economy. What China does and how they do it matters a lot, not just to China but for the global economy. To help keep you better informed, we share a must-read commentary of the situation from @INArteCarloDoss. Please give him a follow on Twitter for powerful analysis on China and macroeconomic/market topics worldwide.

The following is from a series of Twitter postings, so please ignore the post’s casualness and any spelling/grammatical errors. All highlights are ours.

Evergrande: why most analysis is dead in water and how best to understand and navigate what’s happening? Both denialists and alarmists are getting it wrong. Let’s start by understanding this: what is happening is the result of a CCP-initiated policy change to curb leverage. (CCP- China’s Communist Party)

It started a while back and has seen other defaults, including SOEs. What are the specific policy changes? Most important is the introduction of the 3 red lines a year ago: – L/A < 70%, net leverage < 100%, cash to ST debt > 1 (SOE= State-owned enterprises)

What’s the point of the 3 red lines? First and foremost, to forestall a systemic crisis that could have brought down the whole financial sector if left unchecked. Real estate amounts to a significant chunk of China GDP with strong linkages upstream and downstream.

And believe it or not, the sector was levered to the gills. The 3 red lines are hardly draconian, yet all the CCC, a large chunk of the B, and a good 1/3 of the BB did not pass them a year ago. Needless to say, it was really not too early. But there is more to it than leverage

One common practice of these construction companies, a game Evergrande excelled at, was to bid land at prices significantly higher than the market. It didn’t matter to them, coz the risk got transferred to flat buyers and banks that financed the purchase.

That model worked well for local governments, banks, and households because house prices were going up. So much so over the last 15 years, that a serious affordability crisis emerged in major cities AND HH debt soared way above disposable income – below HH debt as % GDP (HH= Household)

So, it wasn’t hard to figure out the economic disaster in the making: exponential price rises with explosive HH and Construction leverage. But that’s not all. There is another problem that escapes most China analysts.

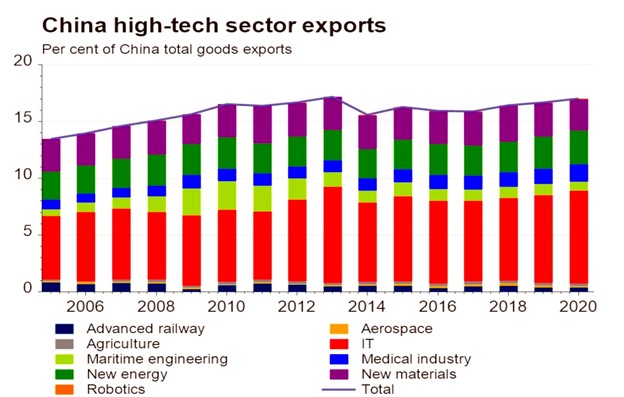

As a result of years of seeking easy growth through construction and leverage, the misallocation of capital was : 1- capital starving more innovative and high tech sectors (see chart) and 2- creating a headwind for a re-balancing towards a more consumption-driven growth.

At some point, reigning in lending to the RE sector became vital in order to address the structural issue of capital misallocation. That also explains the curbs on VC investments in RE and most importantly, a curb on all the irregularities that characterized RE. (RE=real estate)

The issue of irregularities is at the core of what is happening with Evergrande. More on that later. It’s a long introduction, but it seemed important to explain these issues to understand the long-term nature of this problem and why its resolution will be tedious.

So, there is a new paradigm dictated by a set of economic realities that CCP could no longer ignore, and most importantly, they can relax the rules a bit, but can’t reverse course. They can’t allow consumers to be bust nor a rogue unproductive sector to balloon further.

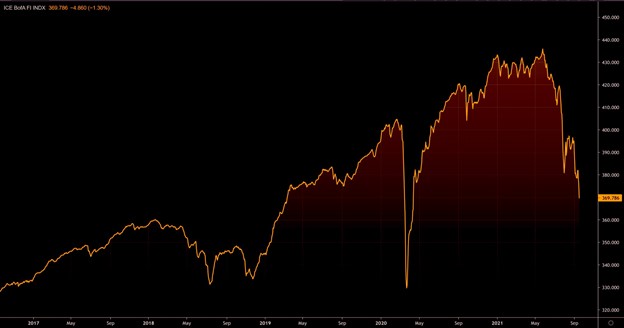

The tail risk emanating from the implementation of this new paradigm is being priced in. It’s not only Evergrande’s credit that is collapsing but the whole HY market. Contagion is AT work. China HY is some 10% away from its March 2020 low….that’s not benign (HY= High yield aka Junk Bonds)

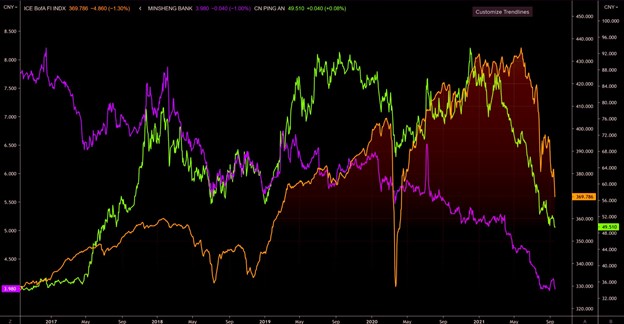

Within construction, many weak operators are seeing their credit collapse: Fantasia, R&F, Suna, China Aoyuan. But that’s not all. The stress is spreading to the banks and financials. Here is Minsheng and Ping An – next level up would be IG starting to show stress

So, we established that we are in the phase of pricing the tail risk. All in all, it’s pretty China-centric for now. How could it create contagion beyond? There are significant losses already for the international holders of China credit and equities. That’s one channel.

Any broader contagion on towards the financial sector in China will prompt temporary policy responses like liquidity injection (done this week). But don’t expect a turnaround. They can’t. How will it resolve itself? Well, it started with leverage as the big issue.

So it will get resolved through asset sales. Idiosyncratic stories will dominate. Stronger balance sheet players will snap land and construction sites. SOEs will snap some assets. State will unwind bad players to help make whole employees and home buyers.

There is a shady side to many of these construction sites, none more so than Evergrande and their Wealth management products sold mostly to employees. They can’t discharge the guarantees on many of these products and there are rumors of insider selling.

Expect more rot to be exposed, trials, accountability, compensation, etc…Stabilizing the onshore property market will be long, arduous, and risky. Evergrande alone has an order book of 1,7 m residential units. Those are down-paid for, yet unfinished.

Uncertainty and volatility will remain elevated. None of the ill-informed « they will bail them out » scenario is possible. One thing is certain, there will be a protracted construction slump in activity and price increases. CCP might not allow for house and land prices to fall.

There’s obviously a read-cross for all commodities, but mostly steel. Dalian Iron Ore started collapsing in July and never looked back. Unsurprisingly, August showed the biggest drop in steel output on record…

And guess who is taking note? The miners are. That’s how contagion works. Aussie miners are the obvious play here: you can see that RIO has established a downtrend and is looking primed for a large move down. $BHP and $FMG looking equally awful.

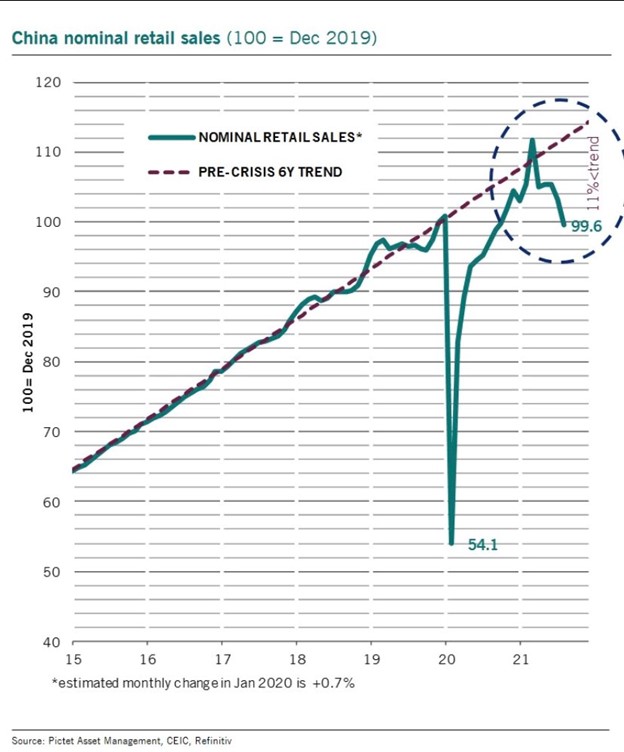

It’s not only a commercial issue. China’s consumers are very levered and while output has been restored to pre-COVID levels, consumers can’t keep up. Retail sales plunged recently to 11% below trend and all high-frequency measures are showing sluggish spending.

And China is looking at a winter of power shortages that is going to challenge its output further. It’s looking pretty dire, and a last level of pernicious contagion will come from the losses all unsuspecting US moms and pops will incur following years of reckless inflows.

While some signs of funding stress are emerging like the Onshore USD/CNY 1y swap rates ticking up, it’s still largely benign. China is a financial system where state and banks are one and liabilities locally dominated and held.

If funding stress signs don’t emerge, don’t conclude that there is no contagion. Contagion is playing out already if you know where to look.

Our Summary

China is trying to pop a massive speculative bubble in real estate. To avoid an uprising or revolution, they must do it to avoid significant losses to the people. Given sizeable real estate holdings by their people, threading this needle will not be easy.

At a minimum, China’s actions will curb their insatiable demand for building commodities. Countries and companies that serve China in this regard are most at risk.

The author alludes that the same reckless speculation plaguing China will eventually occur here. We can debate all day whether China should or shouldn’t pop the real estate bubble. What is not debatable is that China is taking actions that will likely strengthen its economy via more productive investments in the long run.

If you want more background on China’s property bubble, please watch this dated but poignant short 60 Minutes episode- LINK.