The A.I. chase is making for a very narrow market. As Bob Farrell once quipped:

“Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.”

Breadth is important. A rally on narrow breadth indicates limited participation, and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small and mid-caps (troops) must also be on board to give the rally credibility. A rally that “lifts all boats” indicates far-reaching strength and increases the chances of further gains.

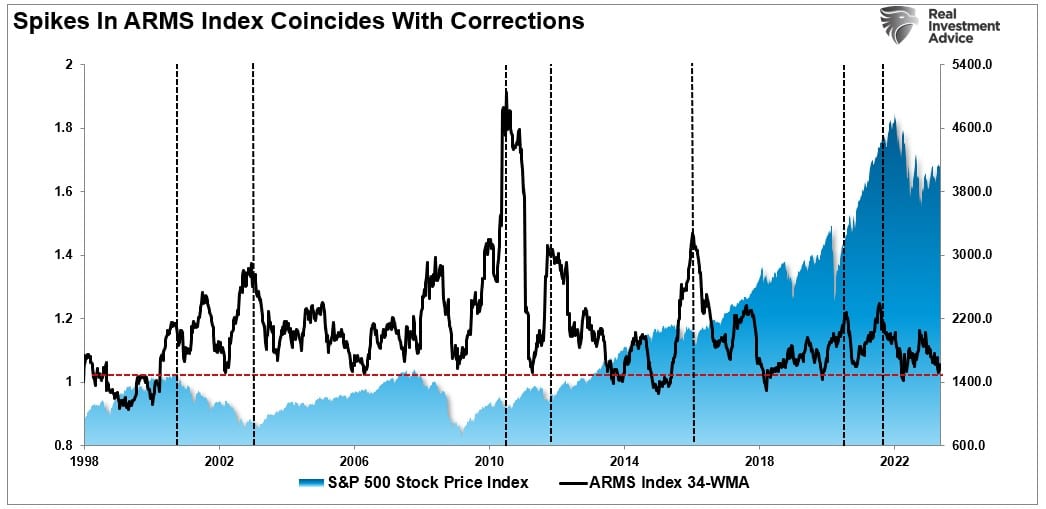

As Bob noted, the chart below shows the ARMS Index. This volume-based indicator, developed by Richard W. Arms in 1967, determines market strength and breadth by analyzing the relationship between advancing and declining issues and their respective volume. It is usually used as a short-term trading measure of market strength. However, when smoothing the index with a 34-week average, extremely low readings often coincide with near-term market peaks. Such is what we are seeing currently.

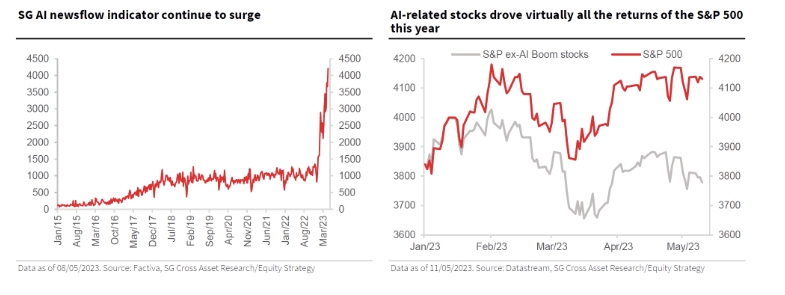

The rally this year has been extremely narrow. As quoted in last week’s article discussing the “A.I. Revolution:”

“The A.I. boom and hype is strong. So strong that without the A.I.-popular stocks, S&P500 would be down 2% this year. Not +8%.” – Societe Generale

We can show this anomaly more clearly by looking at the stocks in the S&P 500 as a “heat map” over the last three months. As you can see, the largest stocks in the index by market capitalization have been holding the index in positive territory.

Unfortunately, the stocks that investors are piling into are also, by far, the most expensive in terms of price-to-sales.

This, of course, elicits two questions.

- Why is this happening?

- What happens next?

The New T.I.N.A. Is Not The Old T.I.N.A.

What is TINA? TINA is an acronym for the phrase “There is no alternative.”

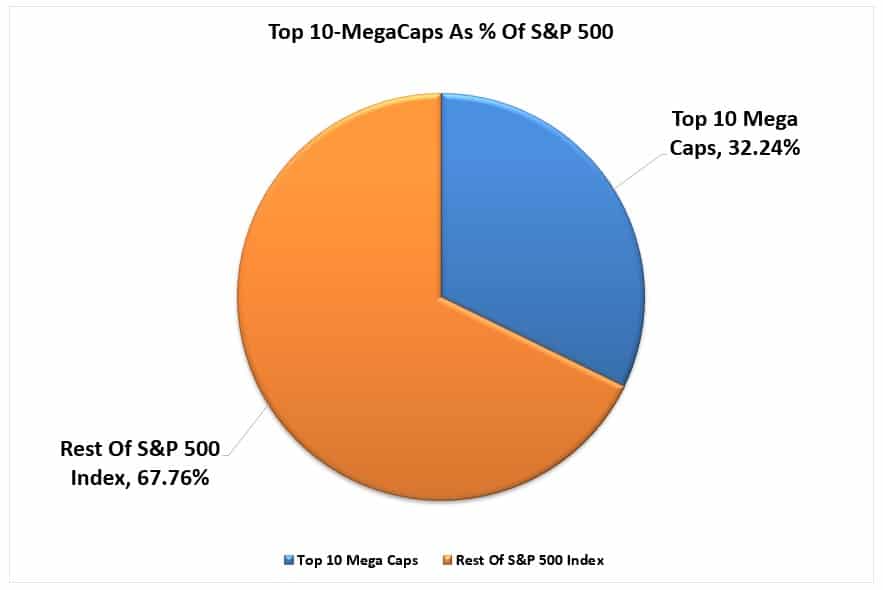

For investment managers, generating performance is necessary to limit “career risk.” If a manager underperforms their relative benchmark index for very long, they most likely won’t have a “career” in the investment management business. Currently, there are two drivers for the mega-capitalization stock chase. First, these stocks are highly liquid, and managers can quickly move money into and out without significant price movements. The second is the passive indexing effect. As investors move money back into the market, it unequally flows into the largest capitalization stocks in the index.

As shown, for each $1 invested in the S&P 500 index, $0.32 flows directly into the top 10 stocks. The remaining $0.68 is divided between the remaining 490 stocks. This “passive indexing effect” has changed the market dynamics over the last decade.

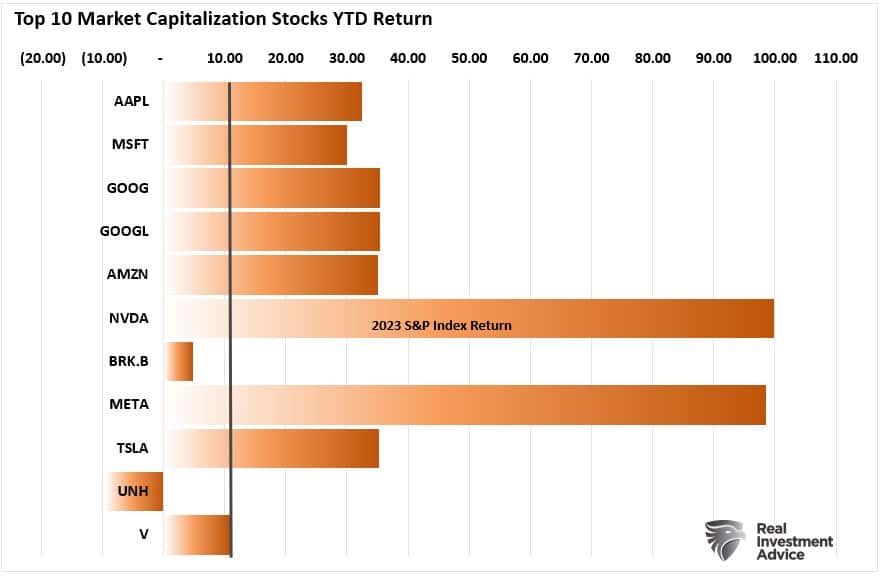

When looking at the year-to-date performance of those top 10 stocks, it is clear where the overall index’s performance is coming from.

As my colleague Doug Kass recently noted in his consistently excellent daily digest.

“Today, TINA can arguably be associated with a small group of large-cap tech stocks – Microsoft, Meta, Apple, Alphabet, Nvidia, and Amazon. To many, there is no alternative to these six stocks, and their leadership is as conspicuous as the last narrow market advance in history…that of The Nifty Fifty.

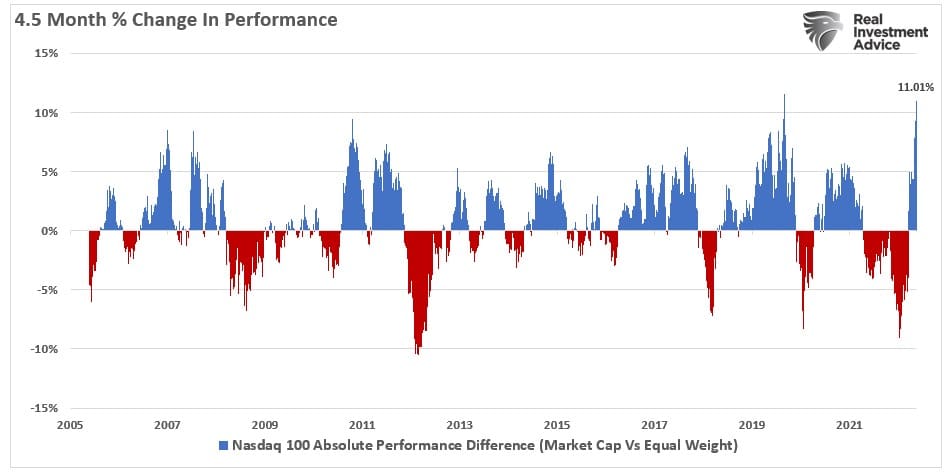

The following chart underscores the remarkable year-to-date outperformance of the unweighted Nasdaq versus the equal-weighted Index. This NDX > NDXE spread is now +11% on the year, by far the widest spread over any 4.5 month period in the last 18 years.”

As Jefferies recently noted, the long technology is now both an extremely overcrowded and overbought trade.

“We have been banging on about the last few days, how the US Tech sector is working on a pretty convincing exhaustion setup. We obviously do not want to go on about the same thing over and over again, but in all fairness, it is the only convincing chart setup right now across pretty much all markets and all assets.

As it is usually with these type of exhaustion outlooks, there is no way to tell, if we get an imminent reaction, or the choppy trading continues. But what can be said with pretty strong confidence is, that upside right now from current levels will be hard to come by.‘

This massive overbought condition of the Technology sector relative to the rest of the market is easily seen in the SimpleVisor Relative Performance Analysis.

It is worth noting that such periods of outperformance were ultimately unsustainable. While such does NOT mean the market must experience a mean-reverting event, it does suggest that, at the minimum, there will be a rotation to other market sectors.

One thing is sure: the old T.I.N.A. of chasing stocks due to zero interest rates is not the new T.I.N.A. of performance chasing.

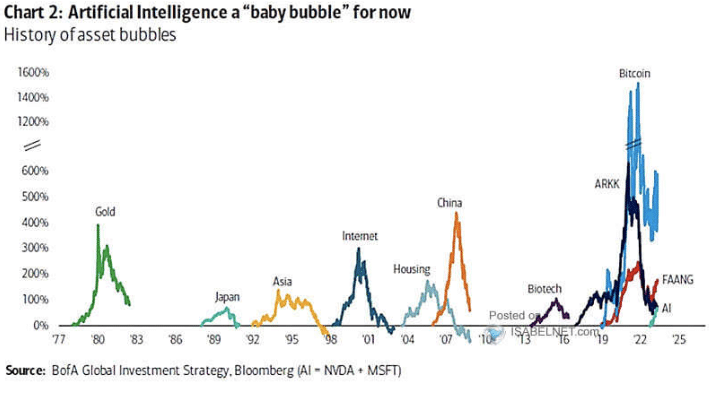

The A.I. Chase Can Last Longer Than You Think

As discussed in “The A.I. Revolution,” these speculative market phases can last up to a decade.

“These booms provided great opportunities as the innovations offered great investment opportunities to capitalize on the advances. Each phase led to stellar market returns that lasted a decade or more as investors chased emerging opportunities.

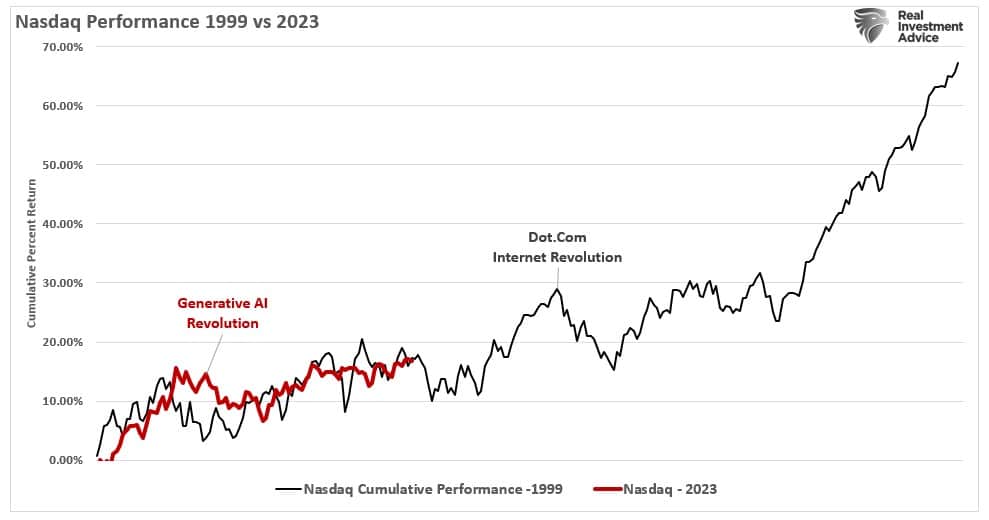

We are experiencing another of these speculative “booms” as “Generative AI” grips investors’ imaginations. The chart below compares the 1999 “Dot.com/Internet Revolution” in the Nasdaq composite versus the 2023 “Generative AI” revolution.

Of course, these speculative periods have recurred repeatedly over the last four decades as investors’ imaginations outpaced the underlying fundamental realities.

Previous investment bubbles like the “Dot.com” resulted in investors chasing a narrow group of stocks hoping for future revenues that failed to materialize. Today, investors are chasing mature companies expecting a massive surge in future revenues to justify exceedingly high starting valuations.

The A.I. Darling

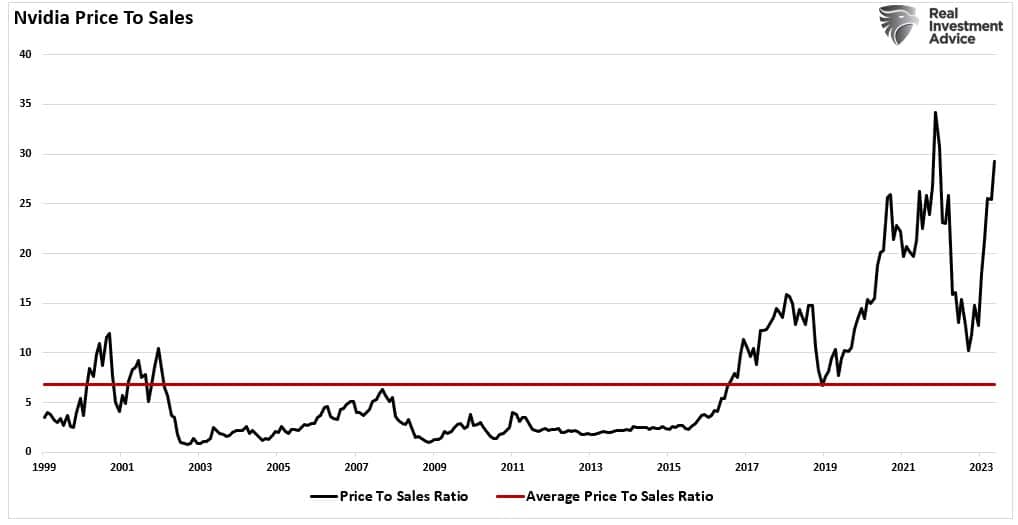

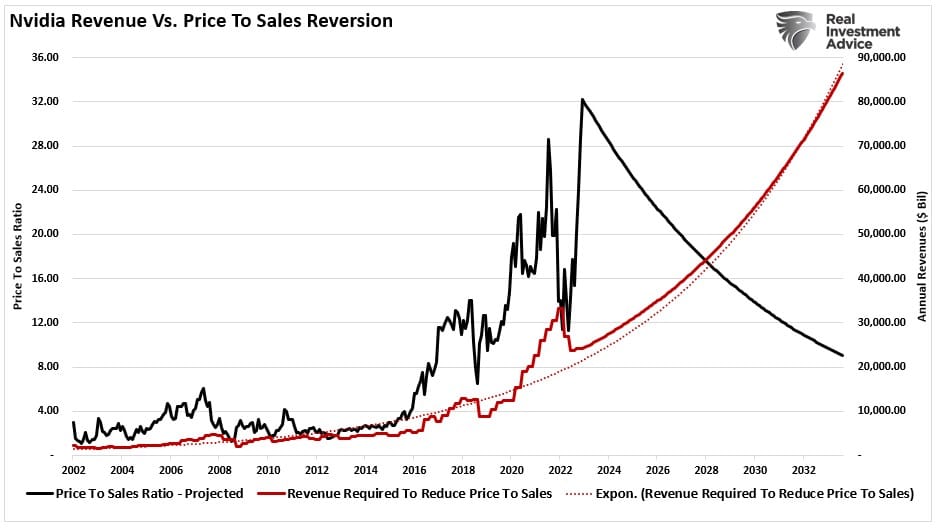

A good example is Nvidia (N.V.D.A.) which is at the heart of the A.I. revolution. Nvidia currently trades at a price-to-sales ratio of 29x. Such is 300% higher than when Scott McNeely suggested investors were stupid to pay 10x sales for Sun Microsystems at the peak of the Dot.com bubble. (Read the entire quote here)

Nvidia has a long history of trading above and below high valuations, with its long-term average running at roughly 9x sales.

The problem with 29x price to sales is that between now and the end of 2033, Nvidia will need to grow sales by 1% every month for the next ten years, and the stock price can not change during that period. There are two problems with this. First, since 2002, Nivida has had a monthly sales growth of just 1.26%. It is far different to grow sales at that pace when sales are $2 billion versus $33 billion today. Secondly, even if Nvidia can maintain that pace of uninterrupted growth, which means Nvidia will own 100% of the GPU market, it would only reduce its valuation to a still expensive 9x sales.

In other words, at 29x sales, an investor must be willing to lock zero returns over the next decade on a fundamental basis. In this light, chasing A.I. stocks seems much less appealing.

While the fundamentals don’t support current investor expectations, the “mania” phase of a “melt-up” can last much longer than you think. However, as with every other bubble period in history, this, too, will end.

As investors, it is essential to participate in these market evolutions. However, it is equally important to remember to sell when expectations exceed fundamental realities.

In other words, in the famous words of legendary investor Bernard Baruch:

“I made my money by selling too soon.”