Futures are slightly lower this morning after two strong days of gains as bulls remain in charge but the rebound continues. Treasury bonds and the dollar sold off as the risk-on sentiment took hold. The S&P 500 gained 1.2% to close above its 50-day moving average for the first time since last Friday. The 10-Year Treasury yield rose by roughly 7 bps to 1.41%, and the dollar lost 0.46%. Based solely on the sharp rise in bond yields, it appears the initial reaction to the FOMC meeting is signaling that the Fed may be too late to curb inflationary pressures.

Index futures are pointing slightly down this morning, while the longer end of the yield curve is flat to slightly higher. Cryptocurrencies and crypto-related stocks are struggling in response to a new policy out of the Peoples Bank of China that makes all crypto-related transactions illegal, according to Bloomberg.

[dmc]

What To Watch Today

Economy

- 10:00 a.m. ET: New home sales, month-over-month, August (1.0% expected, 1.0% in July)

Earnings

- No notable reports scheduled for release

Politics

- The Federal Reserve will host a virtual Fed Listens event at 10:00 a.m. ET, called “Perspectives on the Pandemic Recovery.” Chair Jerome Powell will provide opening remarks and other Fed governors will moderate the conversation among leaders in the private sector.

Market Trading For Friday, Sept. 24th.

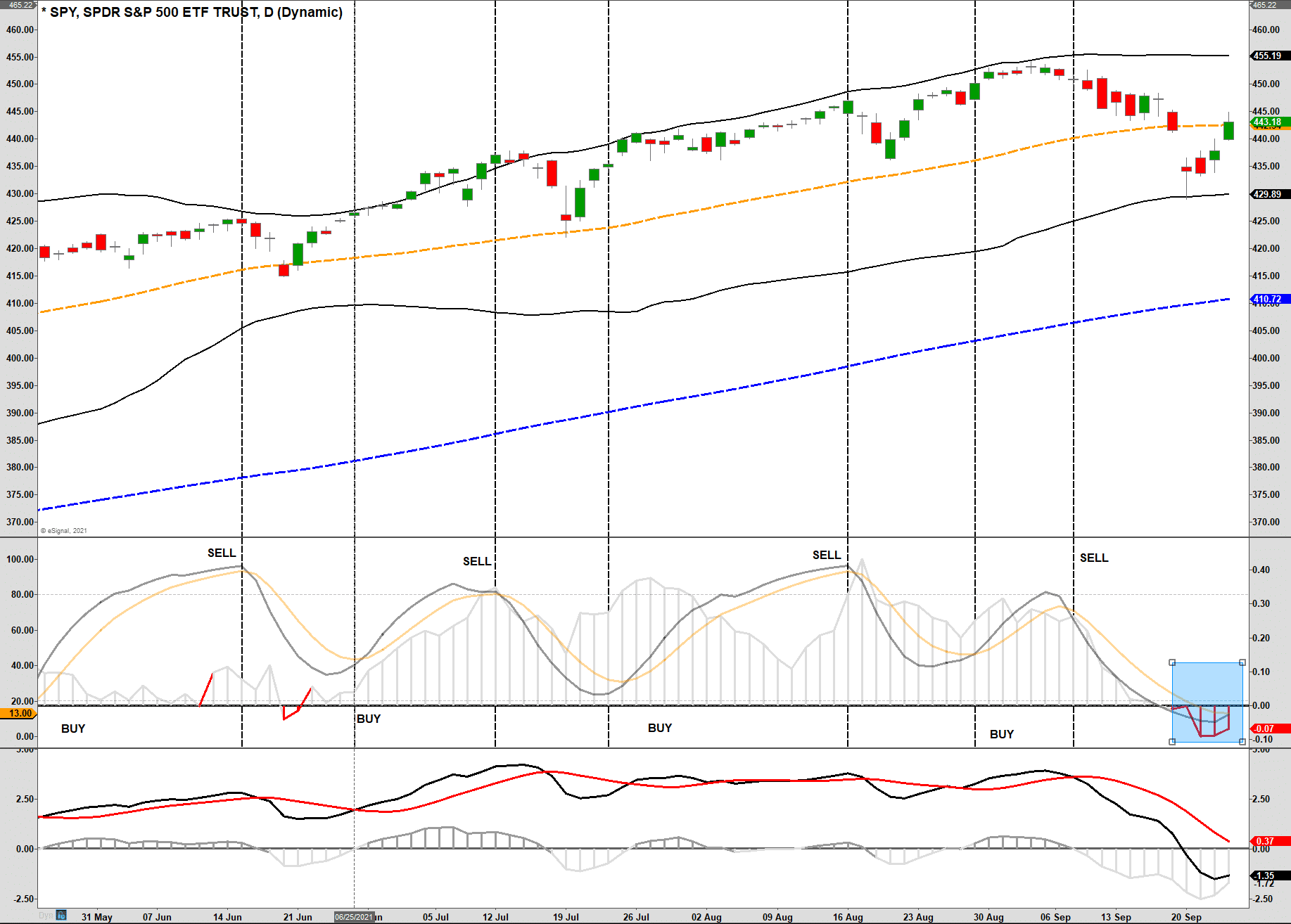

Heading into September, we spilled a lot of ink about us raising cash, increasing bond duration, and rebalancing equity risk. With our previous “sell signal” beginning to reverse, we have spent the last couple of days putting that excess cash back to work.

With the market reclaiming the 50-dma and buy signals close to triggering, the bulls are back in charge. It will be important for the market to hold the 50-dma by the close of trading today. There is still some downside risk short-term with the “debt-ceiling” debate, China, and markets still processing the Fed’s announcement.

Maintaining some risk hedges, for now, is logical until the market clears the 50- and 20-dma moving averages successfully.

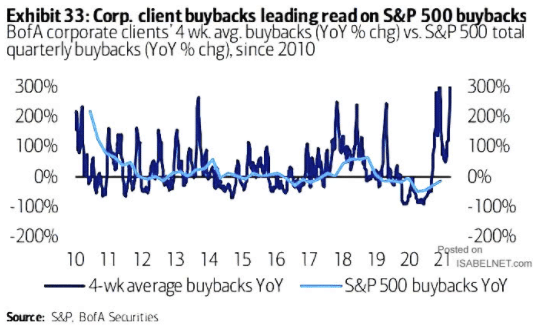

Buybacks Are Surging And That’s Good For Stocks

Buybacks have been a major contributor to stock market returns over the last 5-years. With corporations flush with cash after pandemic-related bailouts, they are putting that cash to work. However, they are doing that in the one area that benefits insiders the most.

As opposed to the mainstream narrative, stock buybacks are NOT a return of capital to shareholders. We dig into the reasons why in this article.

PMI

The PMI composite index fell slightly as growth is “hampered by severe supply chain hold-ups and capacity shortages.” Both manufacturing and services sectors continue to signal solid economic expansion. Inflation however remains a concern. The following paragraph from the report leads to concern the recent stabilization in headline inflation data may not be lasting: “

On the price front, input costs rose at a sharper pace during September. The rate of cost inflation was the quickest for four months, and the second-highest on record, as supply chain disruptions and material shortages pushed prices and transportation costs up. Meanwhile, output charges continued to increase markedly, continuing to rise at a pace far outstripping anything seen in the survey’s history prior to May, as firms sought to pass on higher costs to clients where possible.

The Evergrande Saga

Evergrande is required to pay $83 million of interest on a dollar-denominated bond today. Per Newsquawk, they have a 30-day grace period as part of an existing agreement before the debt is classified as a default. It appears as if Evergrande may give a preference to paying off Yuan-denominated debt and obligations over foreign-held dollar-denominated debt. They have another $47.5 million dollar-denominated interest payment due next week.

Is Now the Time to Buy Stocks?

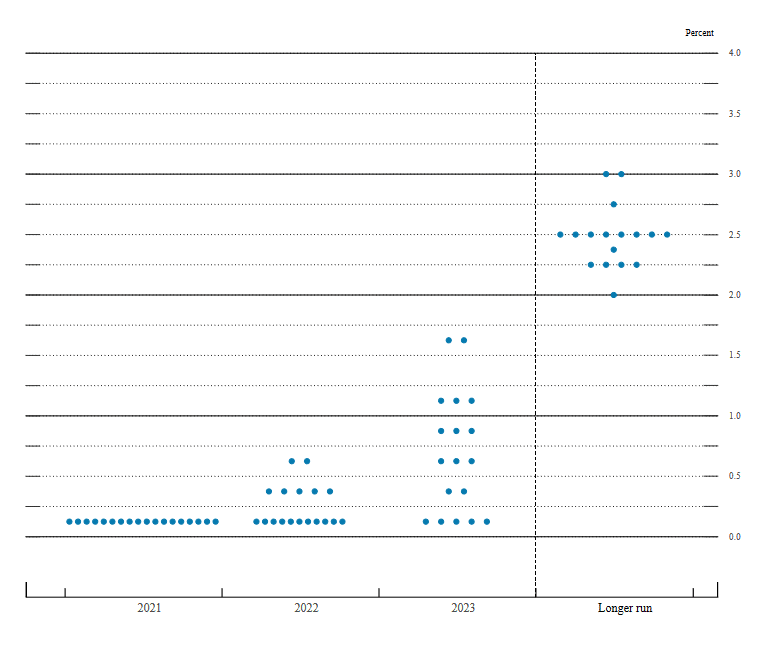

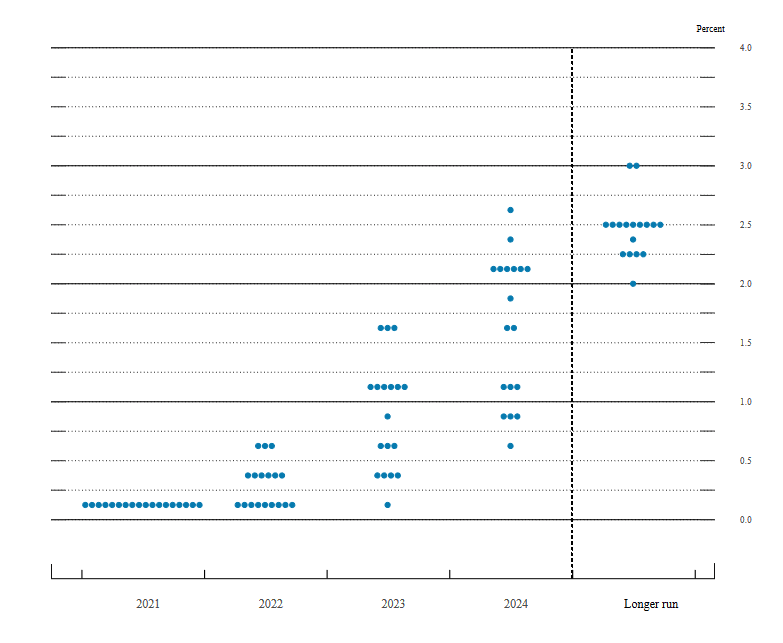

Fed Rate Projections

The two graphs below are the “dot plots” from the Federal Reserve showing Fed member expectations for where the Fed Funds rate will be in the coming years. The graph on top is the set of projections from June. At the time only 5 members thought they would raise rates four times or more by the end of 2023. As shown on the bottom graph, with yesterday’s projections, that number stands at 9. There are also 2 more Fed members that think the Fed will hike rates in 2022 compared to three months ago.

June

September

All Ears on the Fed

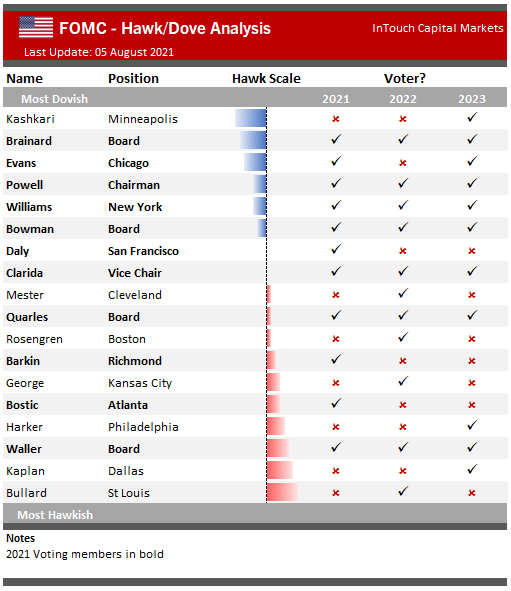

With the Fed meeting behind us, Fed members can now speak publicly. We expect a deluge of speeches and interviews over the coming days as members try to clarify the Fed’s views as well as their personal opinions. We are on the lookout for dissension in the ranks by the members that are overly concerned with higher inflation. While Powell clearly set out a time frame for taper, the Fed might get cold feet if the equity markets turn lower. If that were to happen some of the hawks may become even more vocal about the need to taper and ultimately raise rates. In The Fed Speaks Loudly and Carries a Feather, we decompose the Fed members by their voting status and degree of influence. The chart below and the article provides some context for their latest thoughts on the economy and policy.