Retirement is a a continuous road; mile markers that represent age may be visualized along the path.

However, if one looks to retire at 67 and in relatively good health, it’s a challenge to comprehend what quality of life may be like at 80. It’s easy to understand how 40 may not look too different from 60 from a quality of health perspective. The stretch from 60 to 90 may be so dramatically different, it’s a challenge to envision.

How does one contemplate their own increasing frailty?

People tend to avoid the topic of long-term care which is defined as financial and caregiver resources required to perform daily activities such as bathing and dressing. Services range from temporary home health services to full-time care through assisted living or memory care. At RIA, we find that investors are hesitant to confront the topic of long-term care. It’s understandable. After all, the mitigation of long-term care risk is expensive. People barely save enough for retirement, overall. Imagine planning for the possible additional six-figure burden of long-term care services.

Also, consumers don’t understand how coverage works, premiums have the ability to skyrocket every few years which can break constrained budgets, and insurance underwriting can be a challenge. It’s reported that over 30% of those who apply for traditional long-term care coverage are rejected for health reasons. Realistically, after age 62, premiums become cost prohibitive for consumers. It’s in their mid-sixties we find people scramble to put together some patchwork plan. We call long-term care the ‘financial elephant in the room.’ You can try to lift it, move it to another area of your financial house however, wherever you go, there it is!

As we lament at workshops, on the radio, to clients at face-to-face meetings – heck, to anybody who’ll listen! – Long-term care expenses are the greatest threat to a secure retirement. Confounding about this specific study is that over 53% of Boomers are confident about managing long-term care costs yet the majority have nothing set aside. The results lead me to conclude there’s a strong and dangerous case of DENIAL going on here. Is there more to the story? Since 50% of middle-income Boomers maintain less than $5,000 in emergency reserves, saving for retirement AND retirement care is most likely too burdensome.

Don’t ignore the elephant. Prepare for it. If traditional long-term care insurance isn’t in your future, hope isn’t lost. Consider these alternatives.

Bankers Life Center for Secure Retirement in a study conducted by Blackstone Group in October 2018, discovered that middle-income Baby Boomers (those with an annual household income between $30 and $100,000 and have less than $1 million in investable assets), are increasingly concerned about staying healthy enough to enjoy retirement (56%). Yet, an astounding 4 in 5 (79%) of Boomers sampled have no money set aside specifically for retirement care needs.

First Step: Don’t Ignore the Elephant!

Your rightful concern, if I got you thinking, is to take a deep breath and find a Certified Financial Planner® who is also a fiduciary. In other words, your interests above all else. Financial plans laud strengths; plans also expose financial vulnerabilities that require remedy.

Per the Center For A Secure Retirement® study, six out of ten Baby Boomers have a plan for how they will fund retirement. Only one-third have a retirement long-term care strategy which leads me to believe this group is not undertaking holistic financial planning which considers every facet of a fiscal life including the possible need for long-term care from custodial to skilled nursing. I’m not surprised that 88% of Boomers who have included a retirement care strategy reported a positive impact to their overall plan.

Second Step: Cover the Spouse Who’ll Most Likely Live Longest.

I’m not going to lie; the mitigation of long-term care risk using insurance isn’t cheap. According to the American Association for Long-Term Care Insurance, the best age to apply is in your mid-fifties. To obtain coverage, the current condition of your health matters or you may not qualify. Only 38% of those age 60-69 make the cut. Even if healthy, at a point in life, especially around the mid-sixties, premiums are known to be household budget nightmare. For example, a couple both age 60 in a preferred health class can wind up paying close to $5,000 a year in premiums and will likely experience premium increases over time.

The number of insurance carriers is shrinking – down to less than 12 from more than 100. Recently, Genworth, one of the heavy hitter providers of long-term care insurance temporarily suspended sales of traditional individual policies and an annuity product designed to provide income to cover long-term costs such as nursing home stays.

If you’re astute enough to plan for retirement care and concerned about the impact of dual premiums on the household budget including saving for other goals, work with a Certified Financial Planner to create a scenario to consider at least partial coverage for the spouse with a greater probability of longevity. For example, on average, women outlive men by 7 years.

If single and do not have a reason to leave a legacy to children or grandchildren, it’s likely that asset liquidation can adequately cover a long-term care event. Again, it’s best to work with a CFP Fiduciary who can help create a liquidation strategy.

Third Step: Take the Kids Out of It.

I’m shocked by parents who assume their adult children will take care of them or ‘take them in’ in the case of a long-term care event. Personally, I find it too painful to interrupt my daughter’s life and impact her physical, emotional and financial health by providing long-term assistance to her dad.

According to www.caregiver.org, 44 million Americans provide $37 billion hours of unpaid informal care for adult family members and friends with chronic illnesses and conditions. Women provide over 75% of caregiving support. Caregiving roles are going to do nothing but blossom in importance as the 65+ age cohort is expected to double by 2030. There will be a tremendous negative impact, financial as well as emotional, on family caregivers who will possibly need to suspend employment, dramatically interrupt their own lives to assist loved ones who require assistance with activities of daily living.

Parents must begin a dialogue with adult children to determine if or how they may become caregivers. Armed with information learned from discussion, I have helped children prepare for some form of caregiving for parents.

A 47-year-old client has added financial support for parents as a specific needs-based goal in her plan; another recently purchased a larger one-story home with an additional and easily accessible bedroom and bath. Yet another has commenced building a granny pod on his property for his elderly (and still independent), mother. All these actions have taken place due to open, continuous dialogue with parents and siblings.

In addition, elder parents have been receptive to allocating financial resources to aid caregiver children. Siblings who reside too far away to provide day-to-day support have been willing to offer financial support as well. However, these initiatives weren’t pushed on children. Children weren’t forced into a situation based on an assumption. If you’re a parent, ask children if they’d be willing to provide care. As an adult child, don’t be afraid to ask parents how they plan to cover long-term care expenses.

Fourth Step: Get Creative.

Three out of every five financial plans I create reflect deficiencies to meet long-term care expenses. Medical insurance like Medicare does not cover long-term care expenses – a common misperception. Close to 56% of people surveyed in the Bankers Life Center study are under the false impression that Medicare covers long-term care expenses.

The Genworth Cost of Care Survey has been tracking long-term care costs across 440 regions across the United States since 2004.

Genworth’s results assume an annual 3% inflation rate. In today’s dollars a home-health aide who assists with cleaning, cooking, and other responsibilities for those who seek to age in place or require temporary assistance with activities of daily living, can cost over $45,000 a year in the Houston area. On average, these services may be required for 3 years – a hefty sum of $137,000. We use a 4.25-4.5% inflation rate for financial planning purposes to reflect recent median annual costs for assisted living and nursing home care.

As I examine long-term care policies issued recently vs. those 10 years or later, it’s glaringly obvious that coverage isn’t as comprehensive and costs more prohibitive. It will require unorthodox thinking to get the job done.

One option is to consider a reverse mortgage, specifically a home equity conversion mortgage. The horror stories about these products are way overblown. The most astute of planners and academics study and understand how for those who seek to age in place, incorporating the equity from a primary residence in a retirement income strategy or as a method to meet long-term care costs can no longer be ignored. Those who talk down these products are speaking out of lack of knowledge and falling easily for overblown, pervasive false narratives.

Reverse mortgages have several layers of costs (nothing like they were in the past), and it pays for consumers to shop around for the best deals. Understand to qualify for a reverse mortgage, the homeowner must be 62, the home must be a primary residence and the debt limited to mortgage debt. There are several ways to receive payouts.

One of the smartest strategies is to establish a reverse mortgage line of credit at age 62, leave it untapped and allowed to grow along with the value of the home. The line may be tapped for long-term care expenses if needed or to mitigate sequence of poor return risk in portfolios. Simply, in years where portfolios are down, the reverse mortgage line can be used for income thus buying time for the portfolio to recover. Once assets do recover, rebalancing proceeds or gains may be used to pay back the reverse mortgage loan consequently restoring the line of credit.

Our planning software allows our team to consider a reverse mortgage in the analysis. Those plans have a high probability of success. We explain that income is as necessary as water when it comes to retirement. For many retirees, converting the glacier of a home into the water of income using a reverse mortgage is going to be required for retirement survival and especially long-term care expenses.

American College Professor Wade Pfau along with Bob French, CFA are thought leaders on reverse mortgage education and have created the best reverse mortgage calculator I’ve studied. To access the calculator and invaluable analysis of reverse mortgages click here.

Insurance companies are currently creating products that have similar benefits of current long-term care policies along with features that allow beneficiaries to receive a policy’s full death benefit equal to or greater than the premiums paid. The long-term care coverage which is linked to a fixed-premium universal life policy, allows for payments to informal caregivers such as family or friends, does not require you to submit monthly bills and receipts, have less stringent underwriting criteria and allow an option to recover premiums paid if services are not rendered (after a specified period).

Unfortunately, to purchase these policies you’ll need to come up with a policy premium of $50,000 either in a lump sum or paid over five to ten years. However, for example, paying monthly for 10 years can be more cost effective than traditional long-term care policies, payments remain fixed throughout the period (a big plus), and there’s an opportunity to have premiums returned to you if long-term care isn’t necessary (usually five years from the time your $50,000 premium is paid in full). Benefit periods can range from 3-7 years and provide two to five times worth of premium paid for qualified long-term care expenses. As a benchmark, keep in mind the average nursing home stay is three years.

I personally went with this hybrid strategy. For a total of $60,000 in premium, I purchased six years of coverage, indexed for inflation, for a total benefit of close to $190,000.

Also, pay closer attention to your employers’ benefits open enrollment. It’s amazing to discover how many people have bypassed or didn’t realize their employers offer long-term care insurance coverage. Those with health issues and possibly ineligible for coverage in the open marketplace will find employer-offered long-term care insurance their best deal.

Fifth Step: Formalize a Liquidation/Downsize Plan.

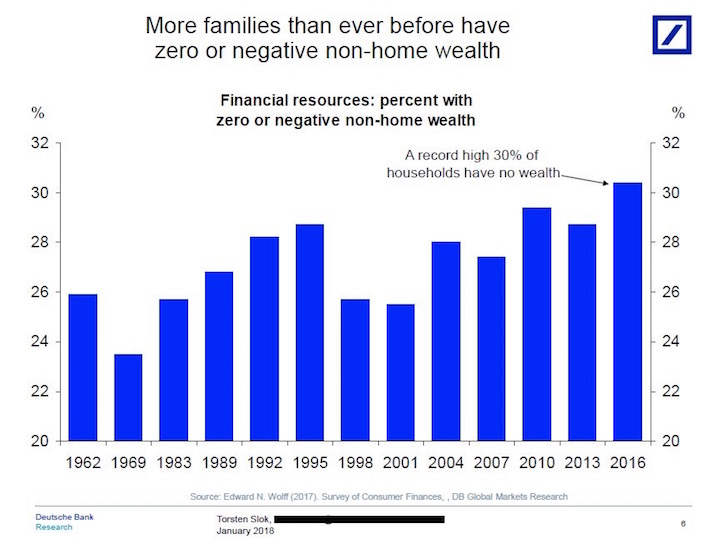

Consider a liquidation/downsizing hierarchy to subsidize long-term care costs. According to a Deutsche Bank report from January 2018 titled US Wealth and Income Inequality, a record high 30% of Americans hold no wealth outside their primary residences which makes me wonder how that group is going to fund retirement, let alone long-term care expenses.

We partner with clients who can’t afford premiums or not able to pass long-term care insurance underwriting with liquidation strategies which look to begin 3-5 years before retirement. Liquidation of a primary residence can be a workable option especially if an individual is widowed or living alone. Empty-nesters can aspire to sell and move into one-story smaller digs early into or before retirement to lower overall fixed costs. They include in their plan home improvements such as ramps, easy access baths, kitchen cabinets and the cost of caregiver services which complement a spouse or life partner’s long-term care responsibilities.

Per the Center for Retirement Research from their analysis dated February 11, 2020, most older Americans prefer to age in their homes. However, it’s important to decide whether a current residence is appropriate for the task. In other words, many older Baby Boomers look to remain in large homes with empty rooms and two stories which is absolutely not practical – Especially in the face of property taxes that increase annually, sometimes dramatically!

The Center’s paper discovered that:

- Seventy percent of households have very stable homeownership patterns, even over several decades. They either stay in the home they own in their 50s (53 percent) or purchase a new home around retirement and stay for the rest of their life (17 percent).

- The 30 percent of households that do move consist of two distinct subgroups. Frequent movers (14 percent) appear to face labor market challenges. Late movers (16 percent) look like a slightly more affluent version of the households that never move, but then face a health shock that forces them out of the home that they owned into a rental unit or a long-term services and supports facility.

- Overall, the findings largely support the narrative from prior research that most people want to age in place and move only in response to a shock.

Sixth Step: Consider Long-Term Care Riders for Permanent Life Insurance.

Permanent life insurance unlike term, builds cash value. Policies can be ‘over funded’ above the cost of insurance to allocate to a fixed interest sleeve and other investment choices attached through various calculations, to stock indexes such as the S&P 500. There is no chance of loss in cash-value accumulation therefore balances have the true opportunity to compound.

A living benefits rider allows the insured to accelerate access to death benefits due to certain conditions such as long-term care needs and terminal illness. There are benefits to utilizing permanent life insurance to subsidize long-term care needs. Premiums remain level (unlike long-term care insurance premiums that tend to increase on a regular basis, sometimes dramatically), second, of course unlike long-term care insurance, at least there’s life insurance or dollars at the end of the road for heirs.

In addition, underwriting for morbidity risk (long-term care) can be draconian compared to mortality risk (life insurance). In other words, medical issues that have potential to affect activities of daily living may not have the same effect on life expectancy; consumers who don’t qualify for long-term care insurance may still qualify for life insurance. There are a couple of drawbacks to these life insurance riders: Funds accessed during a lifetime will inevitably reduce the face value or death benefit of a life insurance policy. Second, riders cost money. So, before adding a living benefits rider, through holistic financial planning be certain you require insurance to mitigate long-term care risk. Through proper planning, we discover that four out of every ten clients have assets to liquidate or are able to self-insure.

Retirement care analysis is a deep dive into the overall retirement planning process. Unlike income planning, retirement care planning requires us to face our inevitable physical limitations and the toll it can have on personal finances along with the negative ripple effects on wealth and health of loved ones.

It’s best to expose vulnerability and plan accordingly while there’s precious time to do so.