In retail investing, do the “blind lead the blind?” Such was a question I asked recently about young investors who are “Long Confidence And Short Experience.” However, a recent survey by MagnifyMoney dug much deeper into the subject.

Our previous article’s gist is that throughout history, markets have a way of separating investors from their money. Such is the reason every great investor in history has one rule in common: “Don’t lose money.” The reason, of course, is that if you lose your capital, you are “out of the game.”

As I noted, the market’s current speculative behavior is not uncommon throughout history.

“Bubbles are characterized by extreme predictions, tend to dominate conversations and induce people to leave their jobs. The warnings of bubble skeptics get invariably met with scorn and derision.” – William Bernstein

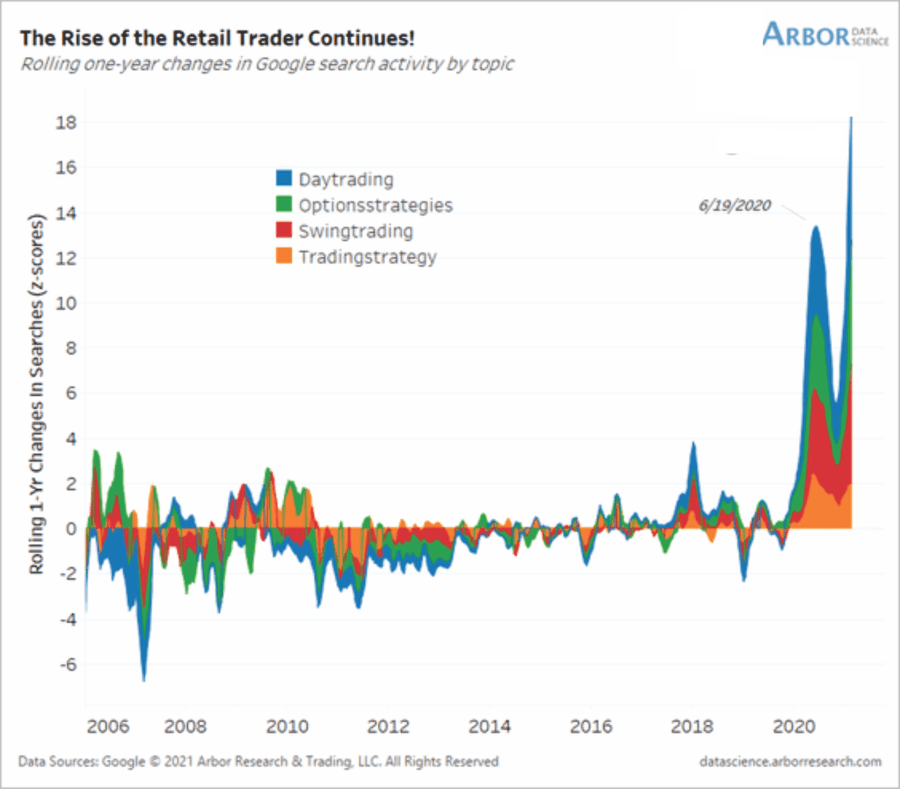

Today, more individuals are searching “google” for how to “trade stocks” than at any point in history. (If data was available back to 1999, I am sure it would be similar.)

Of course, this overconfidence grew from the repeated Federal Reserve interventions. Those interventions lofted asset prices and speculative confidence. Not surprisingly, as noted by CNBC:

“Young retail investors plan to spend almost half of their stimulus checks on stocks, Deutsche survey claims.”

Over-Confident

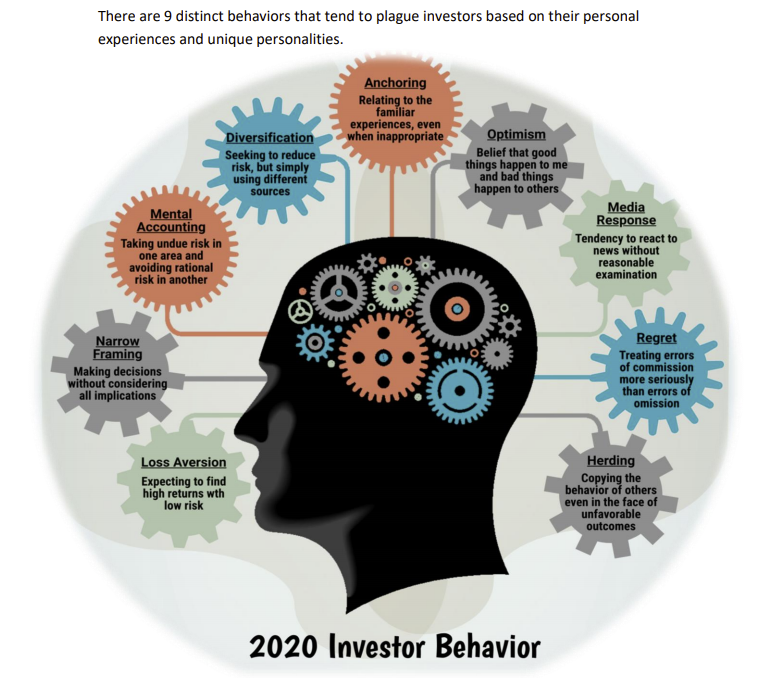

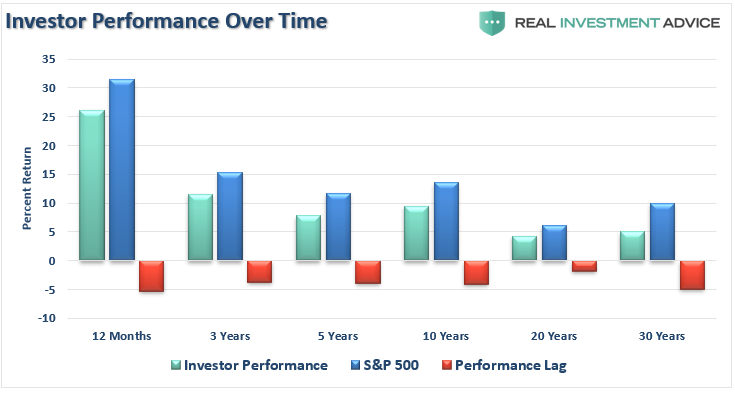

Every year, Dalbar Research does a study of retail investors. The latest study revealed retail investors tend to underperform markets due to a series of “behavioral biases.”

As the study showed, the biases lead equity investors to do worse than the index consistently.

Such is due primarily to the psychological pitfalls that occur from “herding” to “confirmation bias.”

“When discussing investor behavior it is helpful to first understand the specific thoughts and actions that lead to poor decision-making. Investor behavior is not simply buying and selling at the wrong time, it is the psychological traps, triggers and misconceptions that cause investors to act irrationally. That irrationality leads to buying and selling at the wrong time, which leads to underperformance.” – Dalbar

Of course, since individuals don’t operate in a vacuum, where is the information coming from that promulgates these emotionally driven actions?

Blind Leading The Blind

A recent survey from MagnifyMoney, showed the youngest and least experienced investors use social media as the “most important” source of information.

“We found that almost 6 in 10 Gen Z and millennial investors (age 40 and younger) are members of investment communities or forums, such as Reddit, and nearly half have turned to social media in the past month for investing research.” – MagnifyMoney

The findings:

- Nearly 6 in 10 investors are members of investment communities or forums, such as Reddit or a group of like-minded investor friends.

- YouTube is the top source for investing information among young investors, with 41% turning to the site in the past month. Other social media platforms are:

- TikTok (24%),

- Instagram (21%),

- Twitter (17%),

- Facebook groups (16%) and

- Reddit (13%).

- In all, 46% have used social media for investing information in the past month.

- 22% of Gen Z investors say they were younger than 18 when they started investing, versus 8% of millennial investors.

- Only 36% of young investors plan to use that money for retirement. 35% will make additional investments, while 19% will use the funds to pay for a major purchase.

- Nearly two-thirds (64%) of investors who are 40 and younger have withdrawn money from their investment accounts to spend.

Considering that many of these individuals have never seen an actual “bear market,” such is the very definition of the “blind leading the blind.”

The biggest problem is the lack of research on investments. In many cases, investments get made on the recommendation of people who have a “large following.” The assumption is since they are “popular,” they are “smart.” Such is not necessarily the case.

Eventually, there will be a time to “sell.” Such is something most won’t learn from “social media” influencers.

Technological Pitfalls

One of the more significant disadvantages to investors today is changing the face of the investing process to gambling. While the speed and convenience of access to financial markets is a modern marvel, it is also problematic by leading to “risky behaviors” by tapping into the “dopamine effect.”

Not surprisingly, the younger the user is, the more gravitated they are towards investing “apps” and other technologies, which turns “investing” into a “game.”

While the advances in technology certainly provide many positives, they also breed behaviors that are an anathema to investor success longer-term.

An article in the Seattle Times noted the same:

“Online traders can experience a certain high when trading that is similar to what people experience when gambling, according to a recent study on excessive trading published in the journal Addictive Behaviors. The study noted that some investors choose short-term trading strategies that involve investing in risky stocks offering the potential for large gains but also significant losses. ‘The structure itself of the two activities (gambling and trading) is very close,’ the study concluded.”

In the current market environment, individuals have been fortunate to garner quick successes, making them overconfident in their actual abilities. Unfortunately, when the cycle turns, the losses mount just as quickly.

There is very little difference in today’s market between “trading” and “gambling.” Both hold the promise of significant financial rewards, but those rewards also come with great risk. That latter tends to get dismissed at the individual’s peril.

Selling Bottoms

No matter how committed people think they are about “buying and holding,” they eventually fall into the same old emotional pattern of “buying high and selling low.”

Investors are human beings. As such, we gravitate towards what feels good, and we seek to avoid pain. When things are euphoric in the market, typically at the top of a long bull market, we buy when we should be selling. When things are painful, we sell when we should be buying.

It’s usually the final capitulation of the last remaining “holders” that sets up the end of the bear market and the start of a new bull market. As Sy Harding says in his excellent book “Riding The Bear,” while people may promise themselves at the top of bull markets, they’ll behave differently:

“No such creature as a ‘buy and hold’ investor ever emerged from the other side of the subsequent bear market.”

Statistics compiled by Ned Davis Research back up Harding’s assertion. Every time the market declines more than 10% (and “real” bear markets don’t even officially begin until the decline is 20%), mutual funds experience net outflows of investor money.

Fear is a stronger emotion than greed.

Most bear markets last for months (the norm), or even years (both the 1929 and 1966 bear markets), and one can see how the torture of losing money week after week, month after month, would wear down even the most determined “buy and hold” investor.

But the average investor’s pain threshold is a lot lower than that. The research shows that it doesn’t matter if the bear market lasts less than 3-months (like the 1990 bear) or less than 3-days (like the 1987 bear). People will still sell out, usually at the very bottom and almost always at a loss.

If You Trade, Have Some Guidelines

Throughout history, individuals repeatedly jump into the more speculative stages of the financial market under the assumption that “this time is different.”

Of course, as we now know, with the benefit of hindsight, 1929, 1972, 1999, 2007, and 2020 were not different – they were just the peak of speculative investing frenzies.

While many young investors are simply following other young investors, who lack the experience, skill, and knowledge to be successful over the long term, a select group of investors is revered for their success. While we idolize these investors for their respective “geniuses,” we can also save ourselves time and money by learning from their wisdom and their experiences.

That wisdom was NOT inherited but birthed out of years of mistakes, miscalculations, and trial-and-error. Most importantly, what separates these individuals from all others was their ability to learn from those mistakes, adapt, and capitalize on that knowledge in the future.

Experience is an expensive commodity to acquire, which is why it is always cheaper to learn from the mistakes of others.

I have compiled a collection of rules, axioms, and wisdom to protect you from repeating mistakes that eventually destroy your wealth.

There is an old WallStreet axiom which states:

“A man with money meets a man with experience. The man with the experience leaves with the money, while the man with money leaves with experience.”

Such is the truth about markets and investing.

Experience tends to be a brutal teacher, but it is only through experience that we learn how to build wealth successfully over the long-term. Many young investors will eventually gain a lot of experience by giving most of their money away to those with experience.

It is one of the oldest stories on Wall Street.