Should we worry about Government debt?

That was the question recently posed by Ben Carlson who laid out several arguments as to why spiraling Government debt may not matter. To wit:

“Is this debt so unsustainable it’s going to wreck future generations and leave them holding the bag? Are we really screwing the grandkids?

Although absolute debt heading into this crisis was high, you could argue we’ve never been in a better position to add debt to the country’s balance sheet. Generationally low interest rates and subdued inflation make for a perfect opportunity to add debt during this type of crisis.”

The Conundrum

On the surface it certainly seems to be a reasonable argument. However, while everyone is in a hurry to rationalize the need to take on trillions in debt, no one is discussing either the consequences of such actions, or more importantly how, to reverse the process.

Ben’s view on debt is not unique. The WSJ maintains a similar view.

“The usual fear is that high government debt leads to a crisis or excessive inflation. But there’s little risk of the first, and nothing inevitable about the second. It depends on choices to be made by the Federal Reserve and, indirectly, Mr. McConnell, since he has some say in who sits on the Fed.”

“This doesn’t mean all that added debt is necessary or being put to its best possible use. It does mean it’s not doing much harm. ‘Interest rates have been trending down for 30 years,’ said Doug Elmendorf, a former director of the Congressional Budget Office who is now dean of the Harvard Kennedy School.

‘That doesn’t just make it manageable to have more debt. It’s a signal that the economic costs of that debt, in terms of crowding out private borrowers, is particularly low.'”

Debt Isn’t A Solution

I would readily agree with both views had the U.S. been fiscally responsible to start with. As I warned repeatedly in 2019:

“With the economy, and the financial markets, sporting the longest-duration in history, simple logic should suggest time is running out.

Politicians, over the last decade, failed to use $34 trillion in monetary injections, near-zero interest rates, and surging asset prices to refinance the welfare system, balance the budget, and build surpluses for the next downturn.

Instead, they only made the deficits worse, and the U.S. economy will enter the next recession pushing a $2 Trillion deficit, $24 Trillion in debt, and a $6 Trillion pension gap, which will devastate many in their retirement years.”

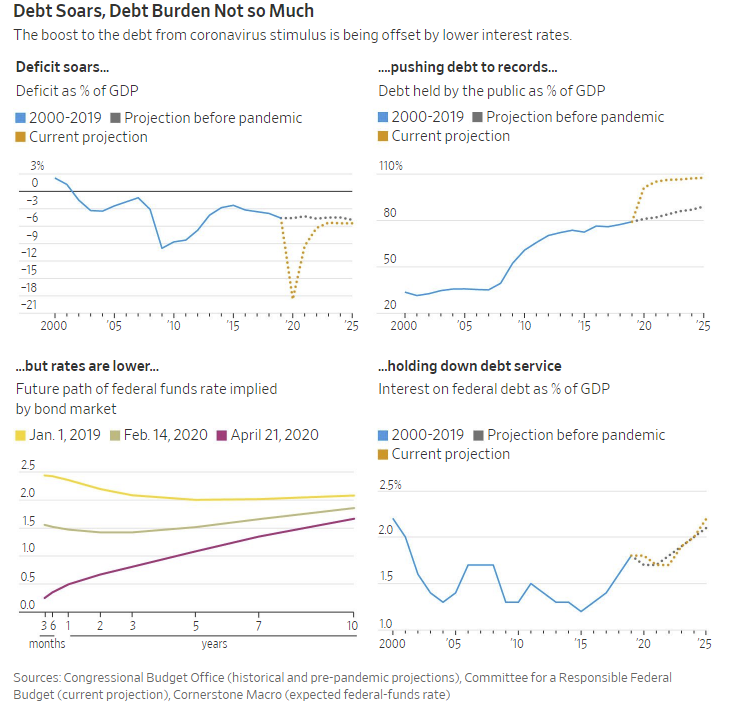

Unfortunately, my forecast proved overly optimistic.

Over the next few quarters, the U.S. will push a $4 trillion deficit as Government debt surges toward $27 trillion.

It’s a bit mind-boggling, considering in:

- 2007, the Senator Barack Obama chastised President George Bush for adding $4.5 trillion to the national debt during is 8-year term.

- 2016, Donald Trump railed on Barack Obama for adding $9 trillion to the debt load during his two terms as President.

- 2020, the media is now making excuses for adding $9 trillion in debt in just 4-years.

While it is true that generationally low interest rates seems to make running higher debt levels relatively “risk-free,” this is only because the right question isn’t being asked.

Why Are Interest Rates So Low?

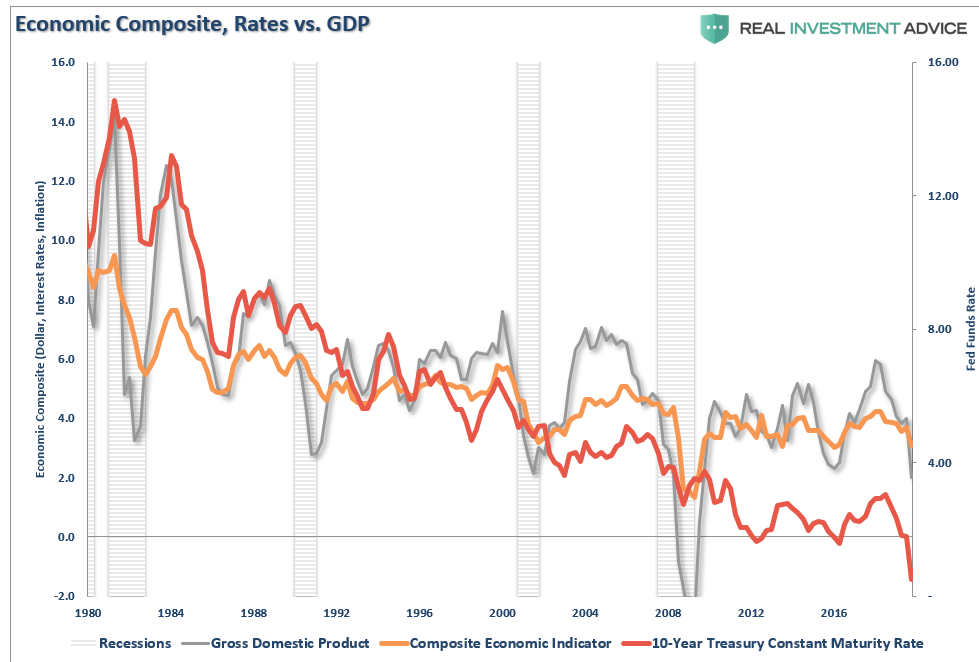

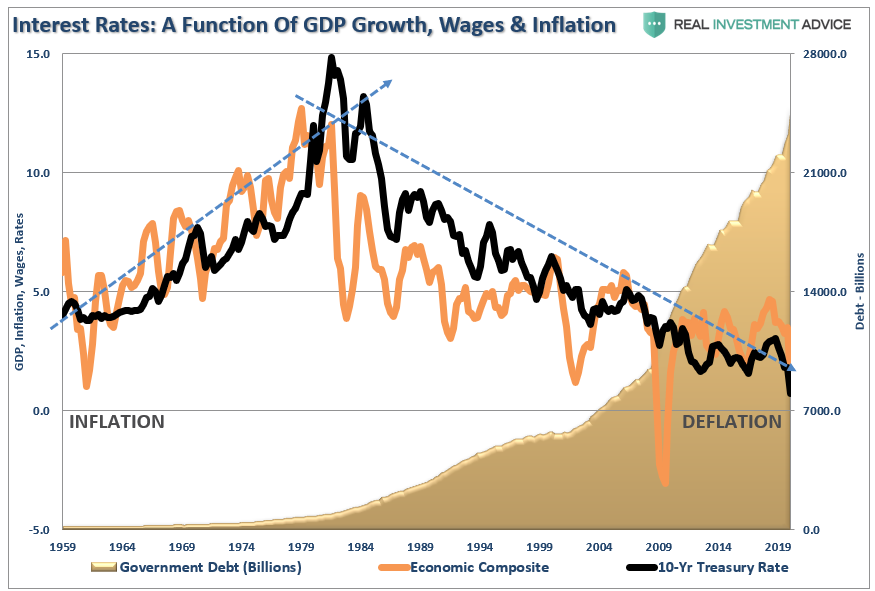

Interest rates don’t operate in isolation.

Rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be seen in the chart below. The composite economic indicator is the composite of the three components.

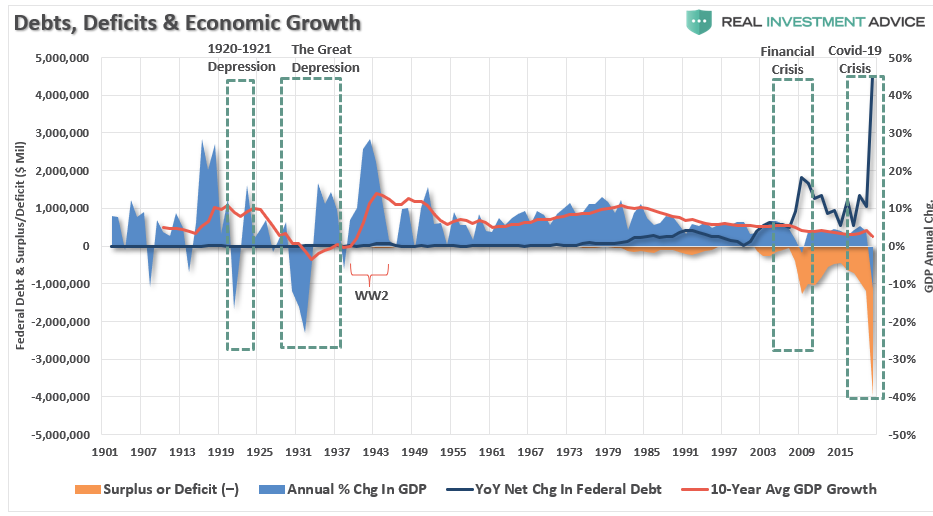

Understanding that interest rates are a reflection of economic growth, we can view the impact of debt on the growth of the economy.

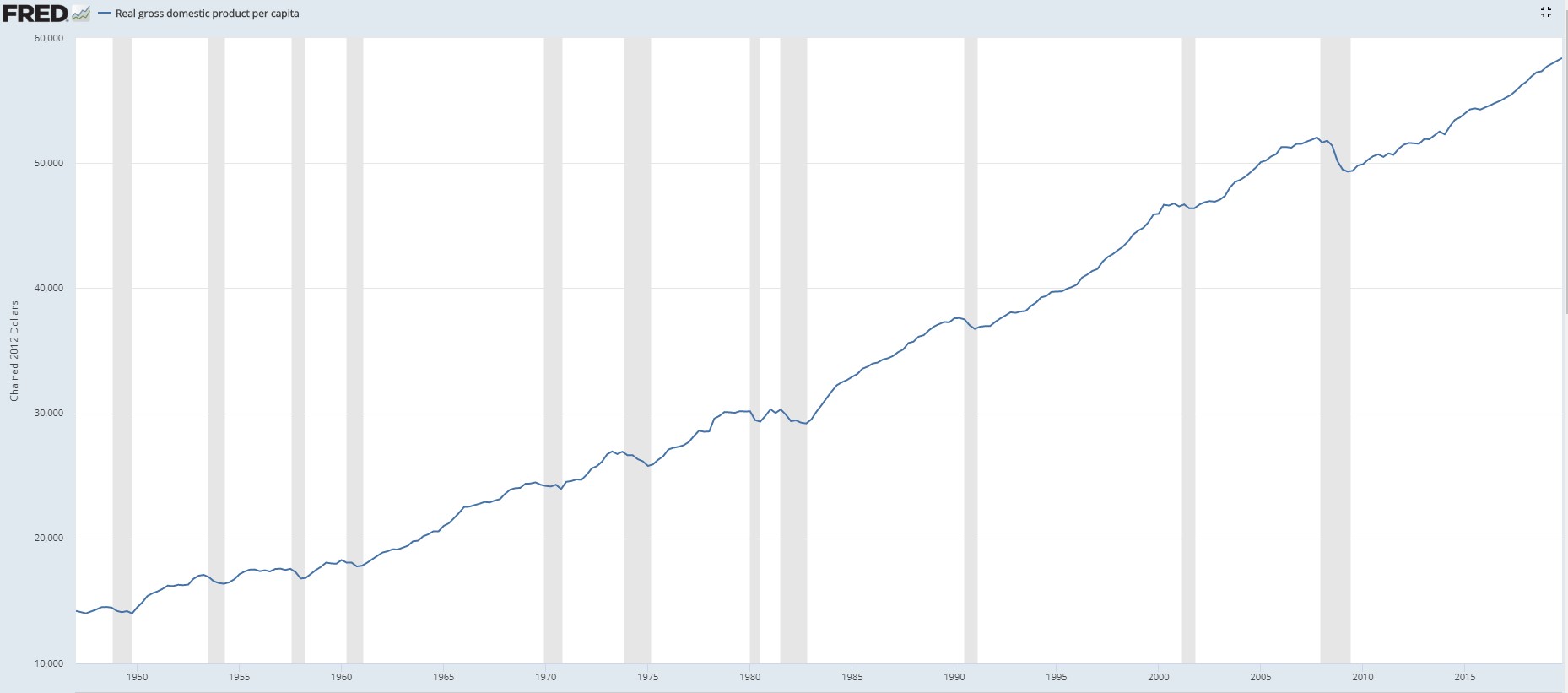

Not surprisingly, prior to 1980, economic growth rates rose as production led to rising incomes and demand. Since debt, and debt to income ratios, were relatively non-existent, savings were reinvested back into economy.

However, beginning in 1980, the view by Government that debt had no consequences, led to 40-years of deflationary pressures, slower economic growth, and ultimately lower interest rates.

Not Just A U.S. Problem

Global economies are currently holding nearly $78 trillion in debt, with nearly 20% of that debt sporting negative interest rates. If the theory “debt has no consequences” and “low interest rates are beneficial,” held true, then those economies should be surging.

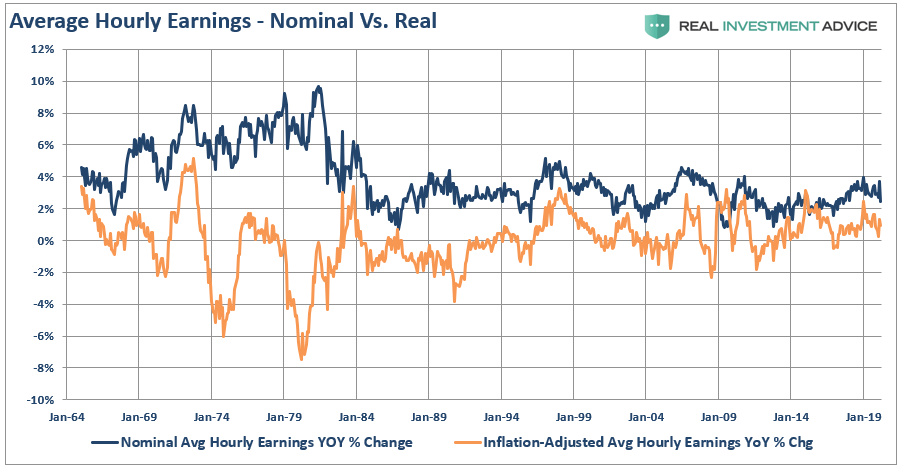

However, that isn’t the case. Over the last decade annual GDP growth has remained weak growing at less than 3% annually. Deflation has remained a constant burden with wage growth almost non-existent.

What has risen rapidly? Wealth inequality.

Not surprisingly, we are caught in a “liquidity trap.” Lower interest rates fail to increase economic growth, and any contraction in monetary accommodation results in an almost immediate economic downturn.

Inflation Isn’t The Answer

“Inflation is one way out of this debt as the purchasing power of the money you’re paying back on the debt gets lower over time. This is the reason inflation is the biggest risk to bondholders over time.

If we have to worry about inflation in a few years I view that as a good problem to have because it means we beat this thing and people are out spending money again and wages are rising.

The second way out of debt is simply growing the economy, something we have been very good at over the long haul.”

Taken out of context, such would certainly seem to be the case.

In an economy driven by debt, a rise in inflationary pressures would also be coincident with an increase in interest rates. As we have repeatedly seen in recent history, even small increases in interest rates leads to rapid declines in economic activity.

Ben is correct that rising inflation does diminish the value of the dollar, which is where inflation comes from. However, inflation also reduces the purchasing power of wages. This is problematic when wages have not grown for workers over the past 20-years.

Since debt does not increase economic growth, but retards it as it diverts dollars away from productive investments into debt service, it is hard to suggest we can “grow our way out of debt.”

Otherwise, we would have done it by now.

Let’s Be Like Japan

What is clear is that years of low interest rates, weak economic growth, low inflation, and ongoing monetary interventions has lead to a massive surge in debt in the U.S. and globally. While many want to suggests that “debt” isn’t a problem, we don’t have to go far to see what ultimately happens.

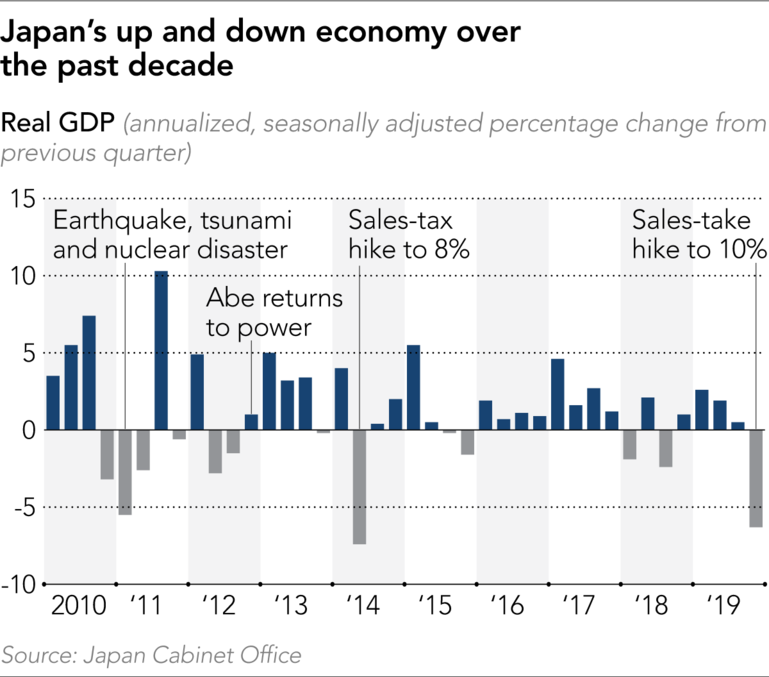

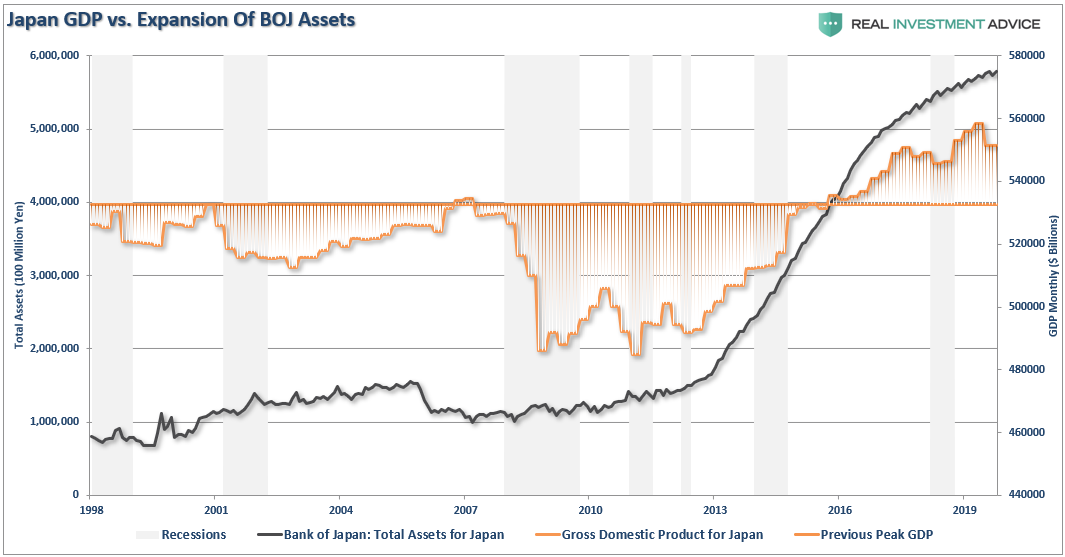

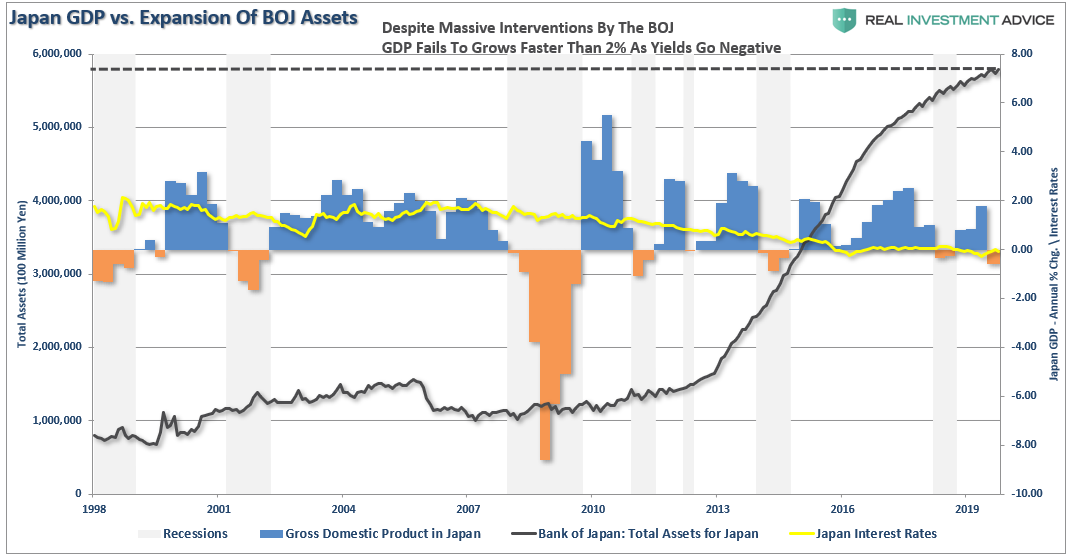

Even before the onset of the COVID-19 virus, Japan has been struggling economically.

There is more to this story.

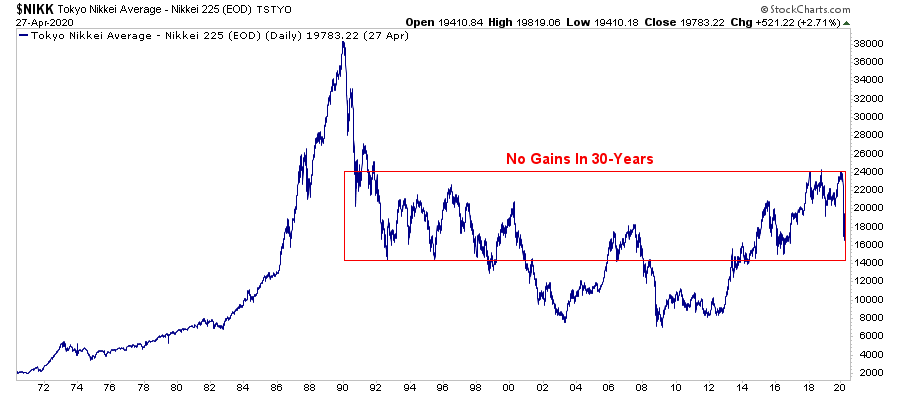

Since 2008, Japan has been running a massive “quantitative easing” program which, on a relative basis, is more than 3-times the size of that in the U.S. However, while stock markets did rise with Central Bank interventions, long-term performance has remained muted.

More importantly, economic prosperity is only slightly higher than it was prior to the turn of century.

Lastly, despite the BOJ’s balance sheet consuming 80% of ETFs, not to mention a sizable chunk of the corporate and government debt market, Japan has been plagued by rolling recessions, low inflation, and low-interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time in recent years.)

The End Game

Why is this important? Because Japan is a microcosm of what is happening in the U.S. As I noted previously:

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.

Most importantly, while there are many calling for an end of the ‘Great Bond Bull Market,’ this is unlikely the case. As shown in the chart below, interest rates are relative globally. Rates can’t increase in one country while a majority of economies are pushing negative rates. As has been the case over the last 30-years, so goes Japan, so goes the U.S.”

Japan Is A Template

Should we worry about the debt? If Japan is indeed an template of what we will eventually face, the simple answer is “yes.”

As global growth continues to slow, the negative impact of debt expands economic instability and wealth inequality. Likewise, hope that Central Bank’s monetary ammunition can foster economic growth or inflation has been sorely misplaced.

“The fact is that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.” – Doug Kass

Japan is a microcosm of what the U.S. will face in coming years as the “3-D’s” of debt, deflation, and the inevitability of demographics continues to widen the wealth gap. What Japan has shown us is that financial engineering doesn’t create prosperity, and over the medium to longer-term, it actually has negative consequences.

This is a key point.

What is missed by those promoting the use of more debt, is the underlying flawed logic of using debt to solve a debt problem.

At some point you simply have to stop digging.