Following President Trump’s re-election, the S&P 500 has seen an impressive surge, climbing past 6,000 and sparking significant optimism in the financial markets. Unsurprisingly, the rush by perma-bulls to make long-term predictions is remarkable. For example, Economist Ed Yardeni believes this upward momentum will continue and has revised his long-term forecast, projecting that the S&P 500 will reach 10,000 by 2029. His forecast reflects a mix of factors that he believes are reigniting investor confidence, including tax cuts, deregulation, and advancements in technology that could drive productivity growth.

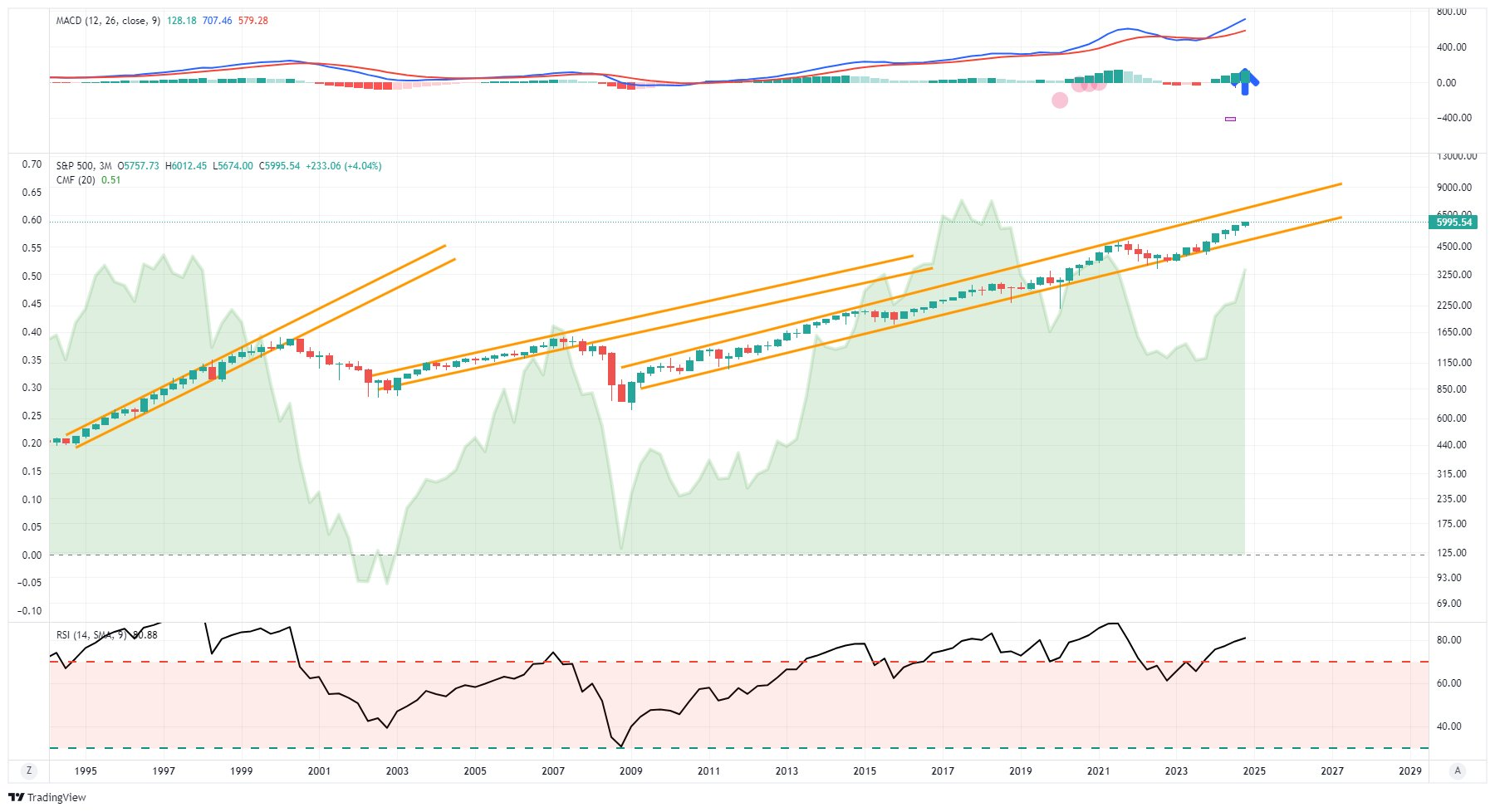

The chart shows the current bull market from the 2009 lows to the present, with a 12-month moving average and a trend channel extension into 2030. While Yardeni’s forecast seems astonishing, it represents a bit more than a 7% annualized rate of return through the end of the decade.

Specifically, Yardeni highlights the potential for substantial corporate tax cuts. He suggests that Trump could reduce the corporate tax rate from 21% to as low as 15%, which would significantly boost corporate profitability. Tax cuts and deregulation would help companies expand their margins and grow earnings. As a result, Yardeni predicts a continuation of record-high profit margins for S&P 500 companies, further supporting his bullish outlook on the stock market.

Yardeni’s analysis is equally striking, even in the shorter term. He anticipates the S&P 500 will reach 6,100 by the end of 2024, with additional gains to 7,000 by 2025 and 8,000 by 2026. He believes these targets are achievable in the current environment, bolstered by solid performances from tech giants and the reinvigoration of investor “animal spirits.”

As investors, is such optimism warranted? Are there essential risks to consider with his forecast? That answer would be “yes,” as Yardeni has previously made bullish forecasts that failed to mature. In the late 1990s, he predicted that the S&P 500 could reach 5,000 by 2000, reflecting his optimism during the dot-com boom. However, the market downturn in 2000 prevented the achievement of that target. Then, during the market run-up into 2008, he maintained his bullish outlook, forecasting significant gains derailed by the “Financial Crisis.” As discussed in this past weekend’s Bull Bear Report:

Concerning long-term market outlooks, it is helpful to remember that Wall Street analysts predicted the same in 1999 and 2007. At the time, valuations were elevated, but analysts and economists believed that economic growth would remain strong and support earnings growth well into the future. Unfortunately, despite the rather rosy outlook, economic realities overtook the exuberance, leading to significant market declines. The same assumptions existed in 1972 about the “Nifty Fifty,” Also, let’s not forget 1929 when Irving Fisher proclaimed the market had achieved a “permanently high plateau.”

However, the rise in “animal spirits” continues to support more bullish outlooks. But what exactly does that mean?

The Problem With Animal Spirits

The term Animal Spirits” comes from the Latin term “spiritus animals,” meaning “the breath that awakens the human mind.”

The term can be traced back to 300 BC in human anatomy and physiology. It refers to the fluid, or spirit, responsible for sensory activities and nerves in the brain. Besides the technical meaning in medicine, animal spirits were also used in literary culture. In that form, they referred to states of physical courage, delight, and exuberance.

Its modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money.” He used the term to describe the human emotions driving consumer confidence. Ultimately, the financial markets adopted the “animal spirits” to describe the psychological factors that drive investors to take action. This is why human psychology is essential in understanding the close linkage to short-term valuation measures.

The 2008 financial crisis revived interest in the role that “animal spirits” could play in the economy and financial markets. The Federal Reserve, under the direction of Ben Bernanke, believed it necessary to inject liquidity into the financial system to lift asset prices to “support” consumer confidence. The result would be a self-sustaining environment of economic growth. In 2010, Bernanke made his famous statement as the economy was on the brink of slipping back into a recession. The Fed’s goal was simple: ignite investors “animal spirits.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

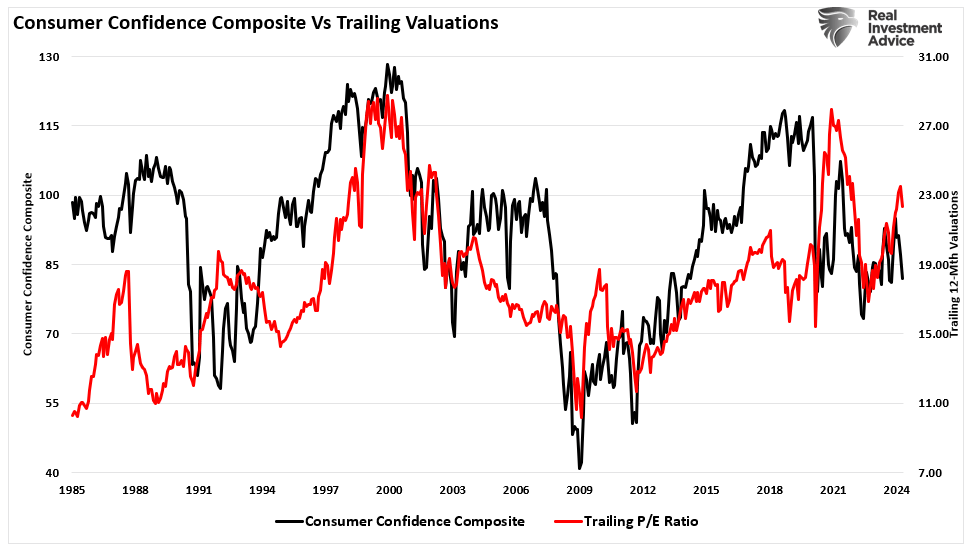

“Bernanke & Co.” successfully fostered a massive lift in equity prices, boosting consumers’ confidence. (The chart below shows the composite index of the University of Michigan and Conference Board surveys. Shaded areas are when the index is above 100)

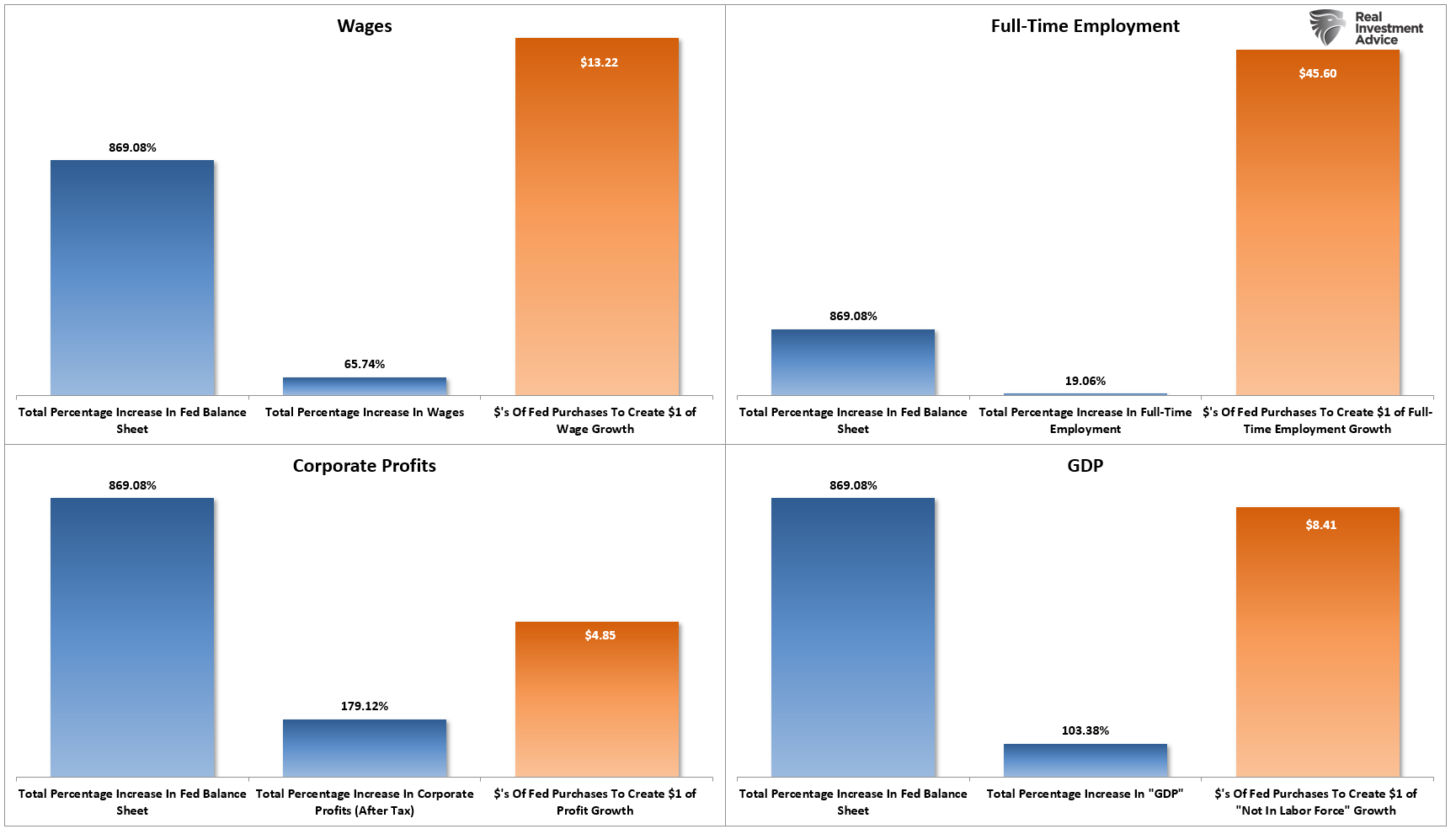

Unfortunately, since 2009, despite the massive expansion of the Fed’s balance sheet and the surge in asset prices, there has been relatively little translation into wages, full-time employment, or corporate profits after tax, which ultimately triggered very little economic growth.

The problem with reviving the “animal spirits” is the monetary policy “transmission system” collapsed following the financial crisis.

The Instability Of Borrowing From The Future

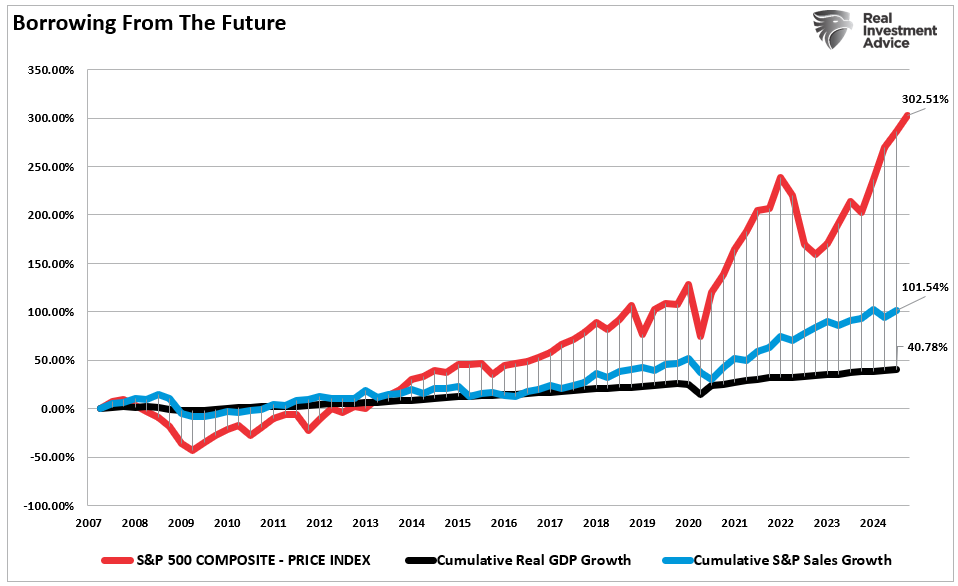

Instead of flowing through the system, liquidity remained bottled up within institutions and the ultra-wealthy, who had “investible wealth.” However, the bottom 90% of Americans continued to live paycheck-to-paycheck. The chart below shows the failure of the flush of liquidity to translate into economic growth. While the stock market returned over 300% since the 2007 peak, that increase in asset prices was more than 7x the growth in real GDP and roughly 3x the growth in corporate revenue. (I have used SALES growth, which is not subject to accounting manipulation.)

Asset prices should reflect economic and revenue growth. Therefore, the deviation is evidence of a more systemic problem. The market has acted as a “wealth transfer” system from the middle class to the rich. Such has not gone unnoticed by the masses as the complaint that “capitalism is broken” continues to rise. However, while capitalism is not broken, there has been a clear shift in the underlying economic dynamics. One of the critical issues is corporate profitability, which we addressed last week:

“Companies have been able to push through profit‑margin‑expanding price increases under the cover of two key events, namely 1) supply constraints in the aftermath of the Covid pandemic and 2) commodity cost-push pressures after Russia’s invasion of Ukraine. But we still emphasise that one of the main sources of the recent surge in profit margins is massive fiscal expansion. In short, the government has been spending more to the benefit of corporates.” – Albert Edwards, Societe Generale

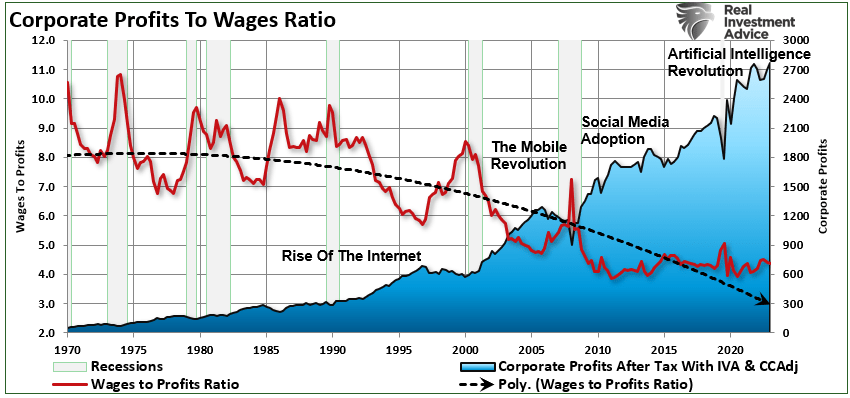

As he notes, U.S. corporate profits are incredibly elevated as a percentage of GDP, well outside historical norms.

However, that surge in profitability has come at the expense of the employee. We discussed this point in “Does Technology Make Things Better?”

“Monopolistic behavior stifles competition, reduces innovation, and limits consumer choice. Furthermore, corporate profitability soared by reducing labor, which is the most costly expense for any business.”

While the rise in “animal spirits” may foster an appearance of economic growth, especially when combined with monetary and fiscal policy support, the sustainability of that growth is questionable. Pulling forward growth does work in the short term; however, the void it leaves in future consumption continues to grow. As such, without continued, outsized fiscal deficit increases, the reversion risk to corporate profitability seems quite significant.

Which brings us to the risks in Yardeni’s bullish long-term forecast.

Risks To Forecasts

In conclusion, while Yardeni’s optimistic forecast is enticing, several risks could derail this bullish outlook. First, historical precedents remind us that unforeseen economic downturns can reverse market momentum even during seemingly unstoppable growth. As noted, Yardeni made bullish forecasts previously, only for economic realities to undermine those projections. The risk of repeating history remains, especially if overconfidence blinds investors to underlying vulnerabilities.

A significant threat lies in the sustainability of the so-called “animal spirits,” the psychological factors that drive market exuberance. While heightened investor confidence can fuel short-term market gains, it often relies on continuous support from monetary and fiscal policies. The long-term effectiveness of those policies is debatable. If economic growth fails to match rising market valuations, the illusion of stability could shatter, leading to sharp corrections.

Yardeni’s bullish case also hinges on expectations of substantial tax cuts and deregulation. However, such fiscal policies have trade-offs, including potential federal debt and deficit increases. Over time, these imbalances could strain economic growth. Such is especially the case if rising deficits erode economic growth or investor confidence in the government’s fiscal health.

Lastly, corporate profitability also poses a challenge. The elevated profit margins, primarily boosted by fiscal spending and price increases, may be unsustainable. As supply chain constraints ease and cost pressures subside, companies could struggle to maintain margins, particularly if labor costs rise or consumer spending weakens. While the outlook remains positive, investors should remain vigilant. Acknowledging that optimism can quickly give way to economic headwinds and market instability is crucial.

Here are five steps investors can take to position portfolios for potential market gains if Ed Yardeni’s bullish forecast is correct. However, these steps can also hedge against unexpected economic downturns or market volatility:

1. Diversify Across Asset Classes

- Strategy: Spread investments across various asset classes, including equities, bonds, real estate, and alternative assets. Diversification reduces the risk of being overly exposed to a single market downturn.

- Implementation: Consider maintaining a core allocation to broad-market index funds or ETFs that can capture market upside while diversifying into sectors like fixed income and real assets, which tend to perform well in risk-off environments.

2. Maintain a Balanced Equity Portfolio

- Strategy: Balance growth-oriented stocks, which could benefit from continued market gains, with defensive and dividend-paying stocks that provide stability.

- Implementation: Allocate a portion of your portfolio to high-quality, large-cap tech and growth stocks to capture Yardeni’s expected upside. Simultaneously, invest in defensive sectors like utilities, healthcare, and consumer staples to cushion against market corrections.

3. Use Bond Investments as a Hedge

- Strategy: Invest in a mix of short- and long-term bonds to benefit from potential interest rate cuts while providing stability if equities falter.

- Implementation: With the expectation of falling inflation and interest rates, long-term Treasuries could increase in value, serving as a hedge. Short-term bonds and cash equivalents provide liquidity and reduce volatility.

4. Add Exposure to Alternative Investments

- Strategy: Incorporate alternatives such as gold, commodities, or real estate investment trusts (REITs) to diversify risk and hedge against inflation or market disruptions.

- Implementation: Gold and commodities can act as a hedge if inflation unexpectedly rises, while REITs may offer income and stability, benefiting from lower interest rates.

5. Keep Cash Reserves and Stay Flexible

- Strategy: Hold a portion of your portfolio in cash or cash equivalents to capitalize on future market opportunities and mitigate downside risk.

- Implementation: Cash reserves allow you to quickly take advantage of market dips or reallocate to higher-yielding investments if conditions change. Staying flexible ensures you can adapt to evolving economic landscapes without being forced into reactive decisions.

We, nor anyone else, know what the market will do in 5 months, much less 5 years from now. History clearly shows that the most optimistic forecasts are often disappointed by economic realities; however, by taking some action within portfolios, investors can remain well-positioned to benefit from potential market gains while being prepared for unforeseen economic shocks.