After a bout of relative market tranquility, investors were rudely awakened Friday with a barrage of new tariff actions targeting the EU and Apple. Via Truth Social, Trump recommended a 50% tariff on European Union imports starting June 1, 2025, and a 25% tariff on all iPhones made outside the US.

Regarding the EU, the new 50% tariff replaces the 20% tariff on EU goods set in April. At that time, the EU proposed retaliatory tariffs. Therefore, the new tariff increases the odds of a deeper trade war with the EU nations. The EU as a whole is one of our top trade partners. In 2024, the US exported $370 billion of goods to the EU, while we imported $605 billion, resulting in a US goods trade deficit with the EU of $235 billion. Conversely, we have a trade surplus of $109 billion with the EU in the service sector.

Trump also proposed a 25% tariff on all iPhones manufactured outside the country. If you recall, Apple’s CEO, Tim Cook, negotiated with Trump and secured exemptions from steep Chinese import tariffs in April 2025. The new proposed tariffs could significantly increase iPhone prices if implemented and fully passed through to consumers.

What To Watch Today

Earnings

- No notable earnings reports

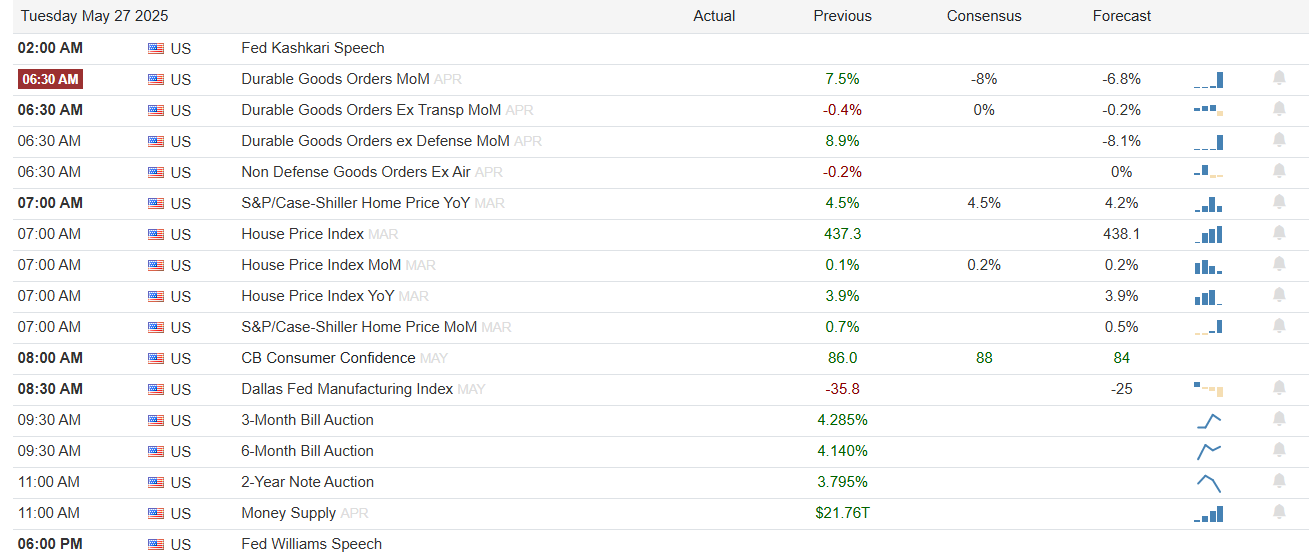

Economy

Market Trading Update

Last week, we discussed how the rally had repaired much of the previous damage following the correction. As we noted:

“This past week, the market continued its advance. There is little reason to be bearish with key overhead resistance levels broken. However, as shown, the markets are reaching decently overbought levels after being extremely oversold. This suggests that at least for now, the “easy money” has been made. With the market above the 200, and above the 50 and 20-DMA, pullbacks should be between 5600 and 5800. Investors can use such a pullback to increase portfolio equity exposures and reduce hedges accordingly. Conversely, 5000 to 5200 becomes the next critical target if those lower supports are violated. Notably, such would require some unexpected event to unfold.”

Several times this past week, we discussed that the market was due for a corrective pullback after reaching more overbought conditions. On Friday, the market gave way early in the morning on fresh comments by President Trump instituting 25% tariffs on Apple (AAPL) on any product not manufactured in the U.S. and 50% tariffs on the EU, as trade talks are not going well. As is always the case, amid a bull run, sellers are still unwilling to sell over fear of “missing out” on rising asset prices. It takes some “event” to bring sellers into the market, which we saw early on Friday.

However, by late afternoon, markets bounced off the 200-DMA and clawed their way higher as comments from Scott Bessent took the sting out of Trump’s announcements. Most importantly, he made two significant statements to alleviate concerns over the recent yield rise. First, he expects the US budget deficit “to be something with a 3% in front of it by 2028,” with revenue from tariffs to be used to solve the deficit. This is crucial as the CBO projections of never-ending deficits do not consider the effects of policy changes that can lead to economic growth. Tax cuts, deregulation, the coming productivity boost from Artificial Intelligence, or the infrastructure demand for power can significantly impact future growth rates.

Secondly, he specifically mentioned the SLR. The Supplementary Leverage Ratio (SLR) is a rule imposed after the 2008 financial crisis that increased bank capital requirements. This is particularly interesting to the bond market, where reversing that requirement will allow banks to purchase more Treasury Bonds. Bessent noted in his interview that the Treasury is close to “moving the SLR requirement and could see that move by the summer.” That shift in the SLR requirement is very bond-friendly and will work to bring rates lower. (For more, read our Daily Market Commentary from last week.)

Even with Bessent’s comments, that market remains overbought short-term, and a further consolidation process is likely into next week. At the end of this week, we removed our short-market hedge, added to bonds, and reduced equity exposure. If the market is going to consolidate, we can allow cash to act as the primary hedge. However, if the 200-DMA is violated, the 50-DMA will become the next critical support. From a bullish perspective, the 20 and 50-DMAs are now sloping positively, which should provide rising support levels. Overall, we suspect that the market will stabilize. Of course, there are always risks to be aware of, so increased cash levels are essential now.

We are not “bearish” on the market because buybacks remain a powerful market influence over the next month. The recent surge has been the largest since the October 2022 market lows. However, those will begin to fade in the middle of June, which could weigh on markets into the Q2 earnings reports.

For now, this seems to be an “unstoppable” bull market, and investor spirits have become substantially more bullish. However, all rallies eventually end. That doesn’t mean a “crash” is coming, and as noted last week, the market is holding the 200-DMA for now. This suggests the previous correction phase is likely complete with support gathering at slightly lower levels. However, there is never a guarantee, so we have taken some recent gains and raised cash levels. We will be patient for a much better entry point soon.

The Week Ahead

Despite being a holiday-shortened week, we will have a good amount of data and Fed speak to digest. In addition, NVDA’s earnings on Wednesday may generate some equity market volatility. As we share below, NVDA is potentially on the verge of a MACD sell signal.

The FOMC minutes will likely further stress that most members are concerned about tariff-related inflation. It will be interesting to see if they address how the recent bout of higher yields impacts their economic outlook. PCE prices and personal income and spending are due on Friday. Expectations are for a slight decline in spending but an increase in income, which alludes to consumers saving or paying down debt. PCE prices are expected to increase by 0.2%.

The Anchoring Problem And How To Solve It

“Anchoring is a heuristic revealed by behavioral finance that describes the subconscious use of irrelevant information, such as the purchase price of a security, as a fixed reference point (or anchor) for making subsequent decisions about that security.” – Investopedia

“Anchoring,” also known as the “relativity trap,” is the tendency to compare our current situation within the scope of our limited experiences. For example, I would be willing to bet that you could tell me exactly what you paid for your first home and what you eventually sold it for. However, can you tell me exactly what you paid for your first soap bar, hamburger, or pair of shoes? Probably not.

The reason is that the home purchase was a major “life” event. Therefore, we attach particular significance to that event and remember it vividly. If there was a gain between the purchase and sale price of the home, it was a positive event, and therefore, we assume that the next home purchase will have a similar result. We are mentally “anchored” to that event and base our future decisions around very limited data.

Today, investors are trained by the financial media to “anchor” to a fixed point in the market. Such is why investors consistently measure performance, relative to the market, from January 1st to December 31st. Or, worse, we measure performance from the peak of an advance. For example:

- The market is up 140% from the March 2020 lows.

- The market is down 10% from the 2025 peak.

- Or, the market is down 6% for the year.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.