Fed Governor Christopher Waller was crystal clear in a speech on Thursday that he would like the Fed to cut rates in July. Importantly, consider the first line of his speech at NYU:

My purpose this evening is to explain why I believe that the Federal Open Market Committee (FOMC) should reduce our policy rate by 25 basis points at our next meeting (July 30th).

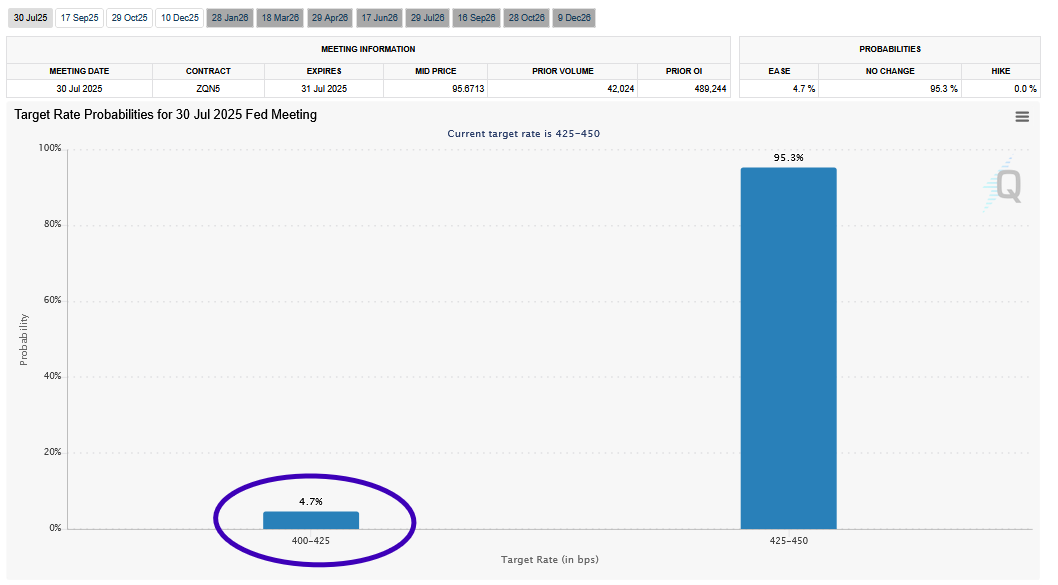

As we share below, investors place the odds of a July rate cut at a mere 4.7%. Moreover, no other Fed members have called for a rate cut in July. Let’s examine Waller’s speech and highlight a few reasons he believes a July rate cut is necessary.

- Tariffs do not cause inflation:

“Tariffs are one-off increases in the price level and do not cause inflation beyond a temporary surge. Standard central banking practice is to “look through” such price-level effects as long as inflation expectations are anchored, which they are.”

- Weakening Labor Market: He thinks the labor market looks “fine on the surface,” but BLS data revisions and non-BLS data point to downside risks. Notably, ADP has shown no growth in the last three months.

- Rates Are Too Restrictive: Real GDP growth is running around 1% and he expects similarly slow activity in the second half. Combined with a weak labor market and transitory tariff-related inflation, he states:

Taken together, the data imply the policy rate should be around neutral, which the median of FOMC participants estimates is 3 percent, and not where we are, 1.25 to 1.50 percentage points above 3 percent.

What To Watch Today

Earnings

Economy

Market Trading Update

As markets close the week after setting fresh all-time highs, the near-term outlook remains cautiously constructive but demands more tactical positioning. Earnings season is ramping up, and early reports from sectors like consumer staples, airlines, and semiconductors have reinforced the bullish narrative, helping propel the S&P 500 to new records. However, technical indicators, including stretched RSI levels and flattening MACD histograms, signal that short-term momentum could reach exhaustion levels, particularly in mega-cap growth stocks.

Investors should be prepared for rotational opportunities as positive earnings momentum starts filtering into under-owned sectors, such as financials, industrials, and select cyclicals, which are still trading below their relative highs. Key earnings reports from large banks dictated this week’s action, as did updated inflation data and ongoing concerns about the current battle between the White House and the Fed.

With these catalysts in play, investors should consider trimming profits in overextended positions, raising modest cash allocations of 5–10%, and tightening stop-loss orders on high-beta trades. Maintaining tactical flexibility will allow investors to capitalize on sector rotation opportunities, particularly if earnings from financials or industrial companies exceed expectations. While the market remains in a confirmed uptrend, narrow breadth and overbought technical conditions suggest a more selective and risk-managed approach is prudent as we head into the last weeks of July.

📈Technical Backdrop

- S&P 500 Index remains nearly 10% above its 50-day moving average and close to 9% above its 200-day moving average. Technical indicators like RSI and MACD point to overbought conditions, with momentum beginning to stall.

- Tech leaders like Nvidia hold strong uptrends and are comfortably above short- and long-term moving averages. However, broader market participation is weakening, and retail involvement is declining.

- A negative divergence occurs when the market tries to push higher, even as momentum and relative strength weaken. Such a divergence is beginning to develop and is worth paying attention to. While this is not an imminent threat, historically, these negative divergences tend to precede short-term corrections.

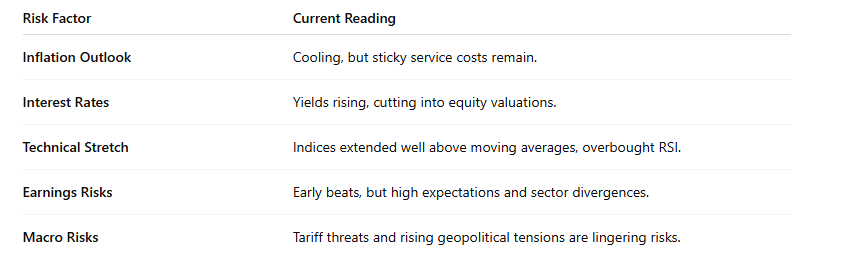

- Risk factors remain mostly the same.

🔑 Key Catalysts Next Week

As markets head into the final stretch of July, several important catalysts will drive market direction next week. The primary focus will be earnings season, which kicks into high gear.

- Earnings season: High-profile reports from major consumer, tech, and industrial names. Companies like Coca-Cola, Verizon, Alphabet, Tesla, Intel, and General Motors will provide crucial insight into consumer demand and corporate profitability. Strong reports could help expand market breadth, while any high-profile misses, particularly from mega-cap tech, could trigger sector rotation.

- Federal Reserve policy signals will remain in focus. The market is split on whether the Fed will cut rates at next week’s meeting. Governor Waller’s recent comments supporting a cut have increased market speculation, but mixed views within the Fed suggest policy uncertainty remains high. Several Fed speakers are scheduled next week, and markets will closely monitor their remarks for clues on rate direction into the fall.

- U.S. Leading Economic Indicators will provide a broad gauge of economic momentum, helping investors assess whether the soft-landing narrative remains intact or if growth concerns are building.

- Fed Chairman Powell will make public remarks that could provide critical clues on the Fed’s evolving stance on rate cuts. Markets will be hyper-sensitive to any shift in tone, especially with the July FOMC meeting approaching.

Next week will be pivotal for balancing economic resilience and softening growth. Stronger data could push yields higher and extend the equity rally, particularly in cyclicals and financials. However, any deterioration in the leading indicators, labor market, or housing data could reignite concerns about economic slowing and trigger defensive rotations.

Central bank commentary, particularly from Powell and the ECB, will be closely monitored for signals on policy direction. Investors should remain tactically flexible, focusing on earnings reactions while keeping an eye on these key data points for broader market cues. High-beta positions may warrant tighter risk controls, while maintaining some dry powder could allow for opportunistic rotation into sectors showing relative strength following the data releases.

The Week Ahead

Earnings will likely be the predominant driver of stock prices this week. As we share below, courtesy of Earnings Whispers, Tesla, Google, and numerous other large companies will report. We believe that the earnings of consumer-facing companies, such as Tesla, Coca-Cola, Domino’s, and Southwest, will help us better assess consumer spending trends.

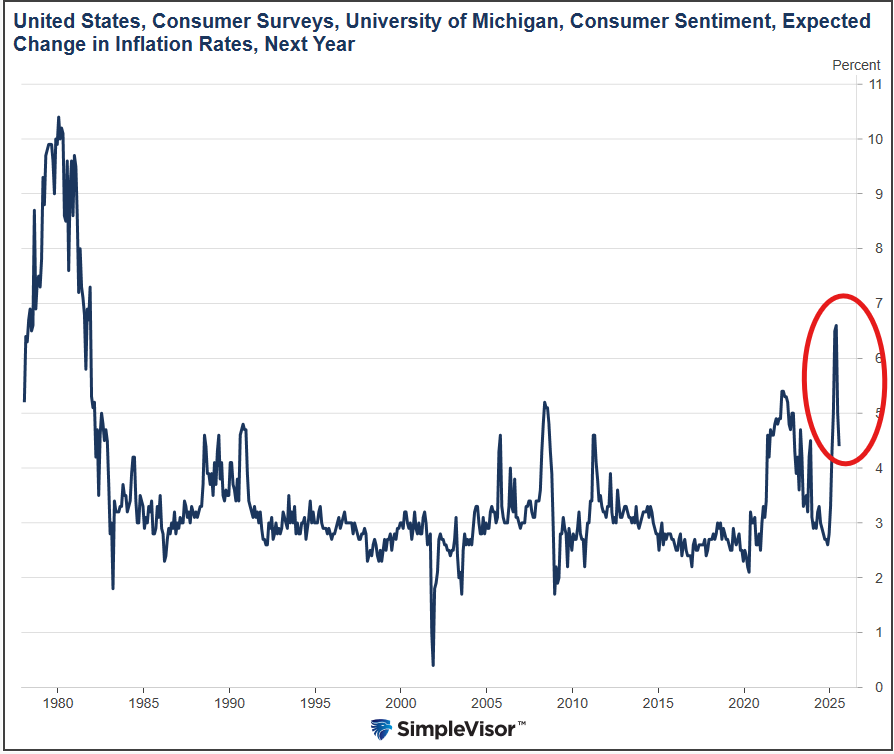

Fed Chair Powell will speak on Tuesday. Given recent inflation data and the reversal of inflation expectations, we will be interested in hearing if he starts to take on a more dovish tilt. For example, consider the decline in Friday’s UM 1-year inflation forecast, which is shown below the earnings graphic. We do not expect him to opine on the prospect of Trump firing him.

China’s Economic Demise And Its Impact On The US

Few are as candid and historically accurate as hedge fund manager Kyle Bass when identifying structural breaks in the global economy. In a recent interview, Bass painted a grim but telling picture of China’s economic condition, warning:

“We are witnessing the largest macroeconomic imbalances the world has ever seen, and they are all coming to a head in China.”

While China has long been touted as the next great economic superpower, its recent trajectory reveals a far different story, one marked by policy missteps, systemic financial rot, and a rapidly eroding growth engine.

Bass didn’t mince words either:

“China’s economy is spiraling with no end in sight.”

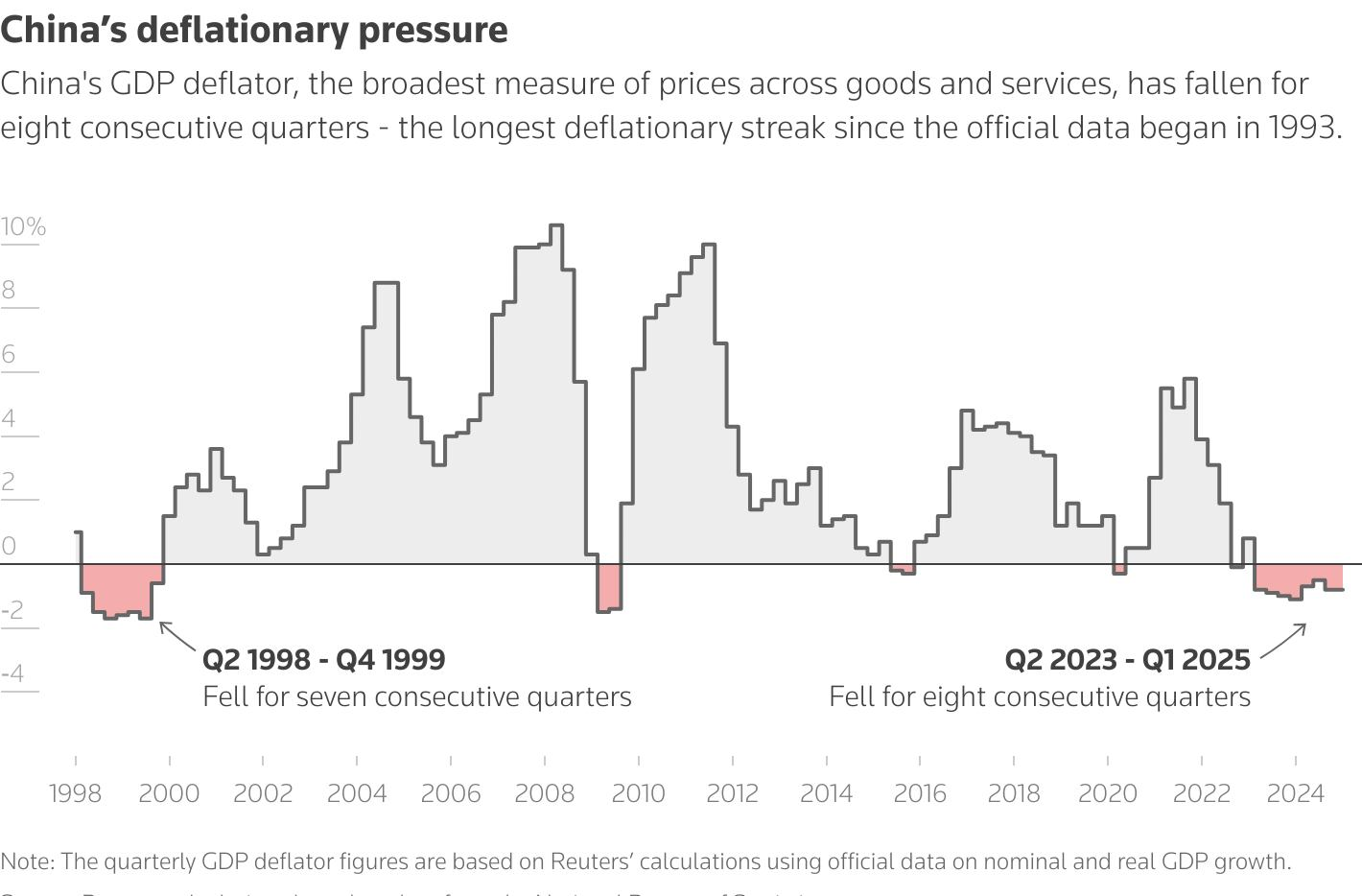

China’s GDP deflator, the broadest measure of prices across goods and services, continues to decline as economic activity erodes.

For investors around the globe, this isn’t just a regional concern; it’s a seismic macroeconomic event that will ripple through capital markets. The implications are significant for U.S. investors because when global economies falter, especially one as large and interconnected as China’s, capital doesn’t just vanish. It moves. That movement will significantly impact U.S. assets as flows transfer back into U.S. dollars and Treasury bonds.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.