Based on early Black Friday sales estimates, sales were strong, but shoppers were much more inclined to take advantage of online sales than go to the malls and stores in person. Mastercard SpendingPulse estimates that in store sales only grew by 0.7% from last year, while online sales rose by nearly 15%. Facteus, another data source, claims that in-store sales fell by 5.4% compared to an increase of 8.5% for online sales. Per ABC News and Adobe Analytics:

Black Friday online shopping this year set a new high, reaching $10.8 billion in sales, according to Adobe Analytics, which tracks U.S. e-commerce data.

That’s more than double what online consumers spent on online shopping in 2017, when sales were just over $5 billion, according to Adobe.

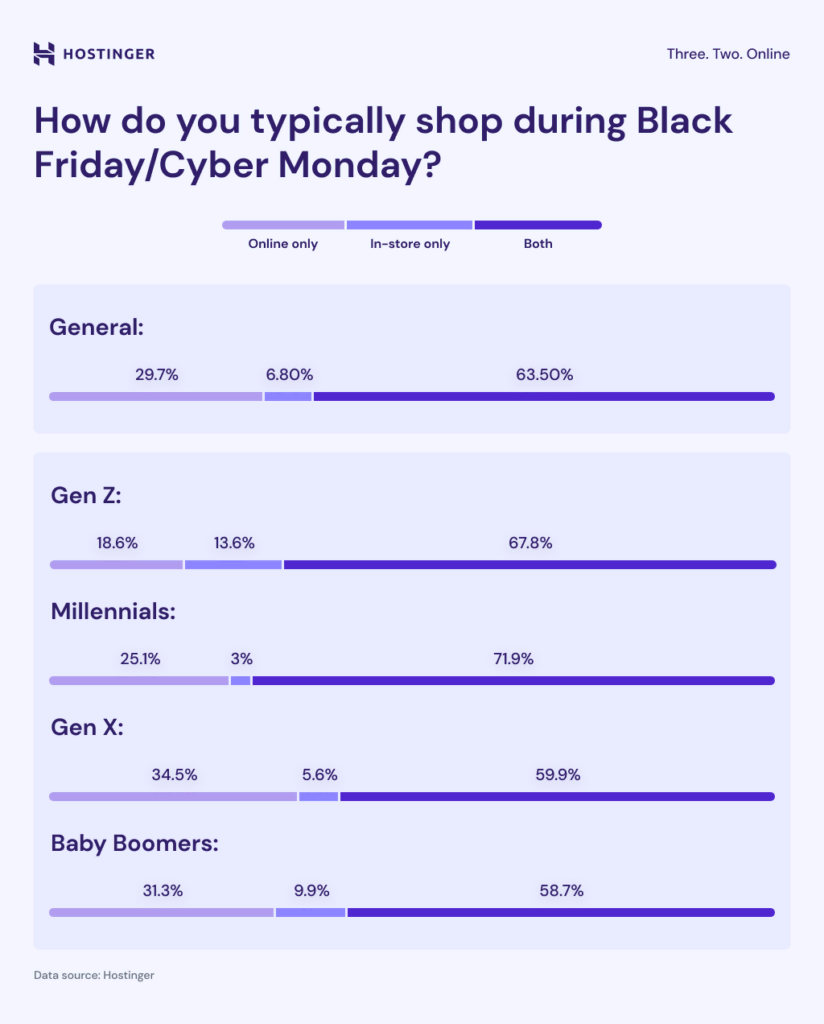

Bear in mind that the data we share does not include inflation. Moreover, it’s hard to make assumptions about the holiday shopping season based solely on Black Friday sales data. Since Black Friday discounts are the largest, more and more consumers elect to purchase on that day. Furthermore, more consumers are shifting their purchases to take advantage of the sales without having to wake up early and brave lines and crowds, as was traditional on Black Friday. Thus, it’s too early to claim that holiday sales were better or worse than last year. However, we have a good inkling that consumers gravitate to online shopping instead of going into stores and malls. The graphic below, courtesy of Hostinger, shows that almost a third of shoppers will rely inclusively on online shopping. While the other two-thirds will shop online and in stores, they clearly prefer digital shopping.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we noted that the recent rally reversed the short-term “sell” signal leading the market to breakout to all-time highs. However, with the market now very overbought, it will be unlikely the market can make further substantial gains without a pullback or consolidation first. We think that will happen over the next two weeks, as noted yesterday:

“The rising trend line from the August lows remains the likely peak to any rally in December, and as noted last week, expect some weakness in the second and third week of December as mutual funds make annual distributions. For now, any corrective action in early December should be bought in anticipation for a rally into year end.”

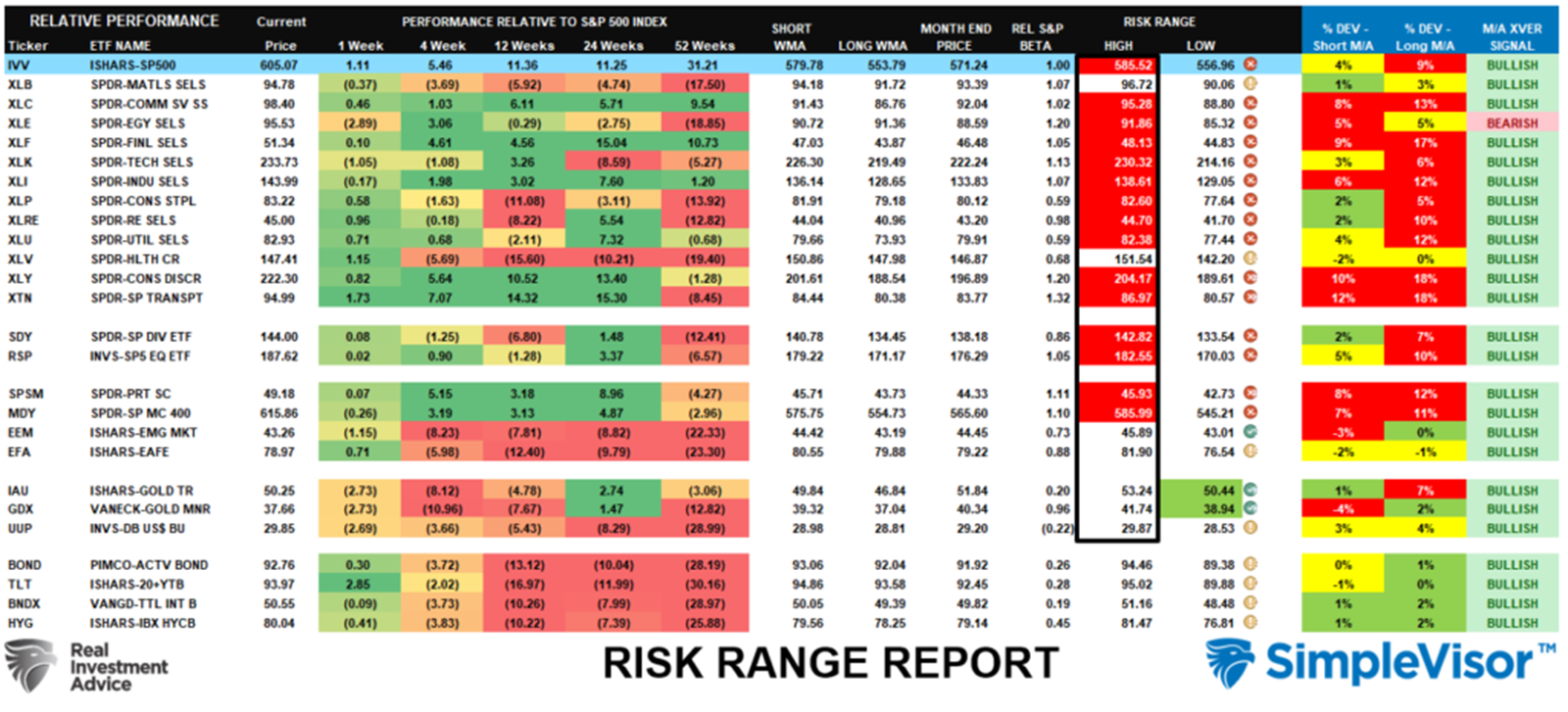

That remains the most likely case over the next two weeks, particularly with most sectors and markets trading well outside their normal risk ranges. Such is shown in the risk range report from last week’s #BullBearReport.

“With that rally behind us, which could continue early next week, it should be noted that most sectors and markets are overbought. Therefore, the upside may remain limited, and a rotation to underperforming market areas, like Bonds, Gold, and Gold Miners, is possible. Overall, the market is very bullish, with every sector and market, except Energy, on a bullish buy signal.”

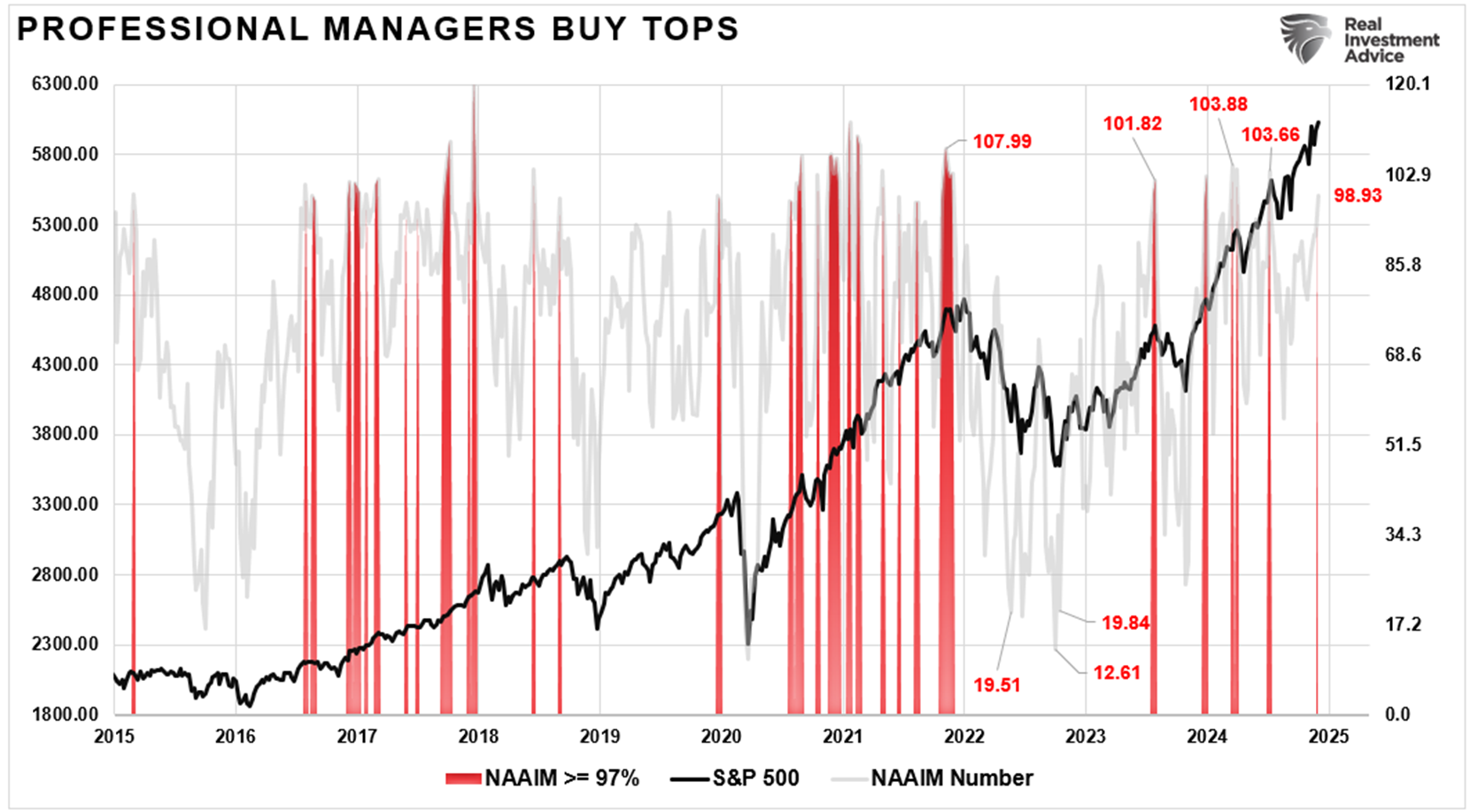

Furthermore, professional managers are extremely bullish with allocations above 97%. As shown by the red shaded areas, when allocations exceed 97% such has historically been close to short-term market peaks or consolidations.

While the levels of bullishness are certainly cause for short-term risk management, December tends to be one of the better performing months of the year. Therefore, with buybacks still in play, investors chasing performance, and year-end portfolio window dressing coming, use any short-term weakness to add equity exposure as needed for trading purposes. However, one theme we will start discussing more in January, is the impact of policies that could undermine corporate profitability next year. But that is a story we will get into in January.

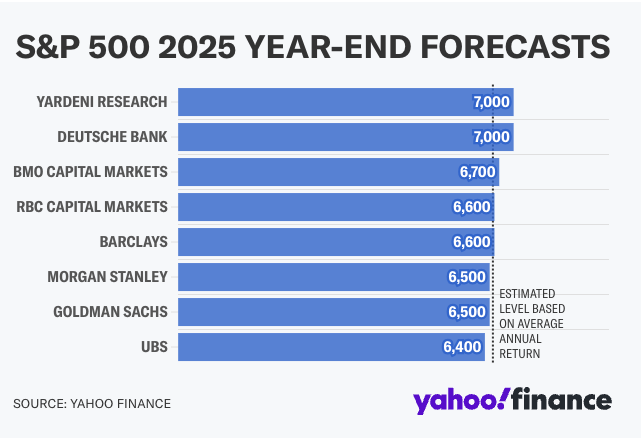

2025 Year-End Forecasts

The graphic below, courtesy of Yahoo Finance, shows some S&P 500 forecasts for the year-end of 2025. The dotted vertical line shows the forecasts hugging the average annual return. Since 1928, the average annual return has been slightly over 8%. The average return over the last two years has been 25.35%, well above the historical average. Interestingly, there have only been five other times during this period when the average two-year return was 25% or greater. The average return over the following two years was 8.82%, not far from the average. Maybe the forecasters are on to something!

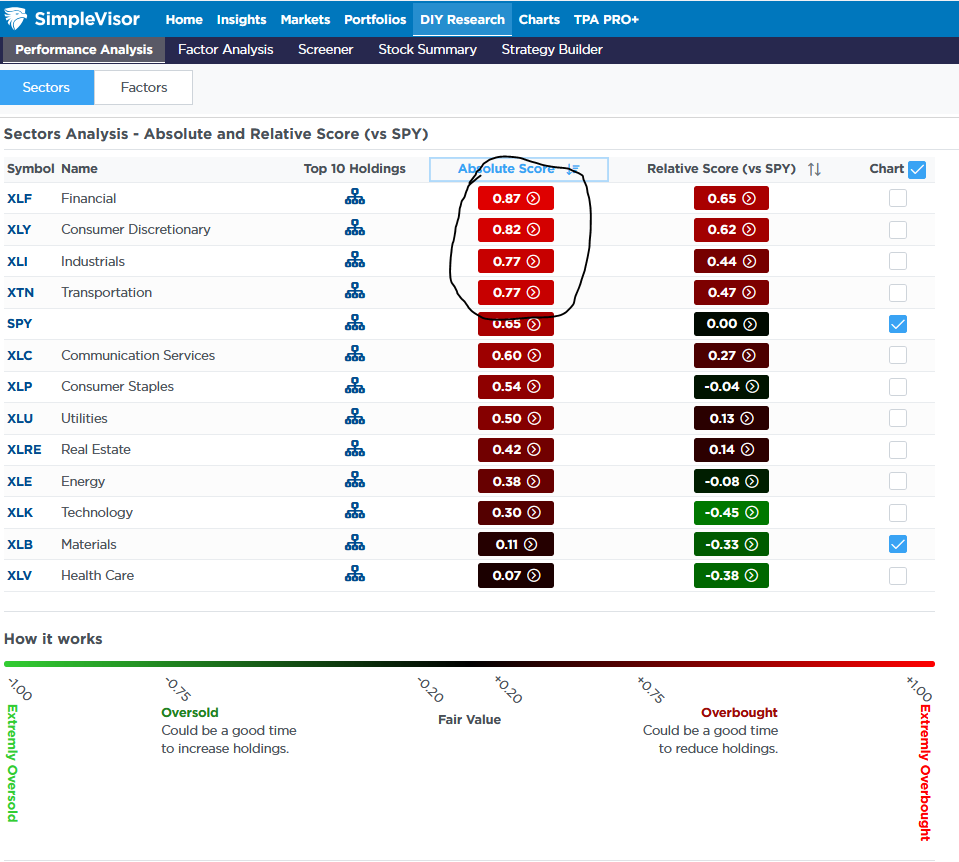

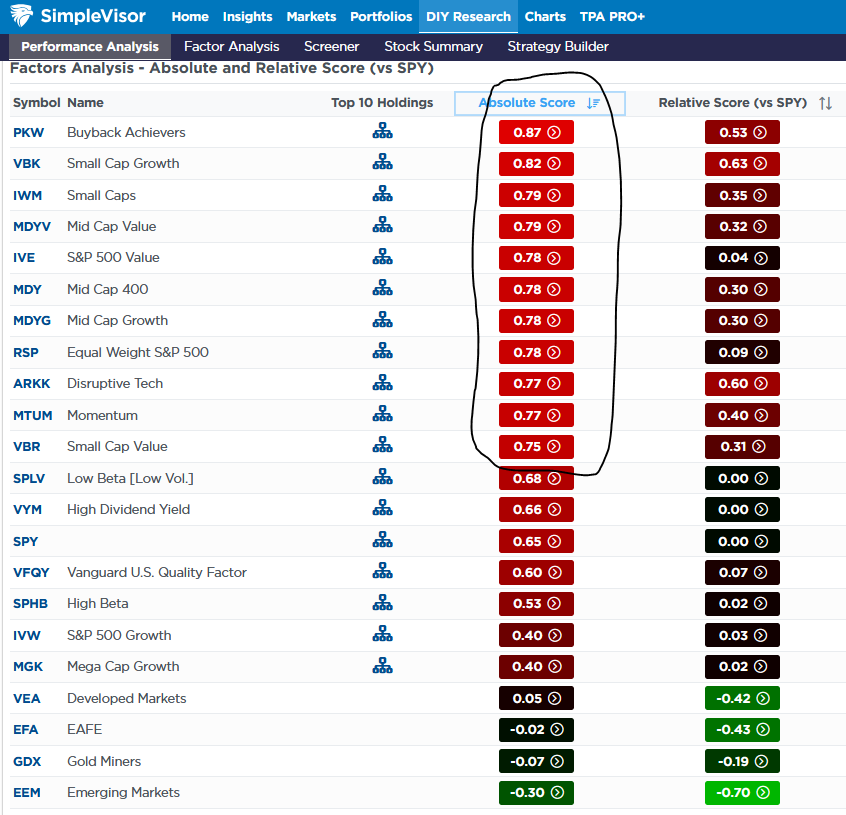

SimpleVisor Points To Frothy Markets

Our SimpleVisor absolute and relative analysis shows that markets are getting frothy. The first graph below highlights that four of the twelve sectors have scores above .75, denoting very overbought conditions. Furthermore, the S&P has an absolute score of .65, which is not as overbought but still a high level. Financial stocks, up nearly 10% over the last month, are the most overbought sector. The second graphic shows that small-cap and buyback achievers are also very overbought. About half of the factors are at .75 or higher.

Unlike most of the year, the technology sector and mega-cap stocks are among the worst performers. Of note, the emerging and developed markets, alongside gold miners, are the weakest relative performers. Largely to blame is the dollar, which has been up about 6% since October.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.