For high-net-worth families, passing wealth to the next generation involves more than just distributing assets. It’s about preserving a legacy, protecting what you’ve built, and preparing heirs to become responsible stewards. Generational wealth transfer is both a technical process and an emotional journey, and getting it right requires clarity, preparation, and expert guidance.

In this article, we’ll explore the legal and tax tools available, the soft factors often overlooked, and how to strike a balance between control and empowerment.

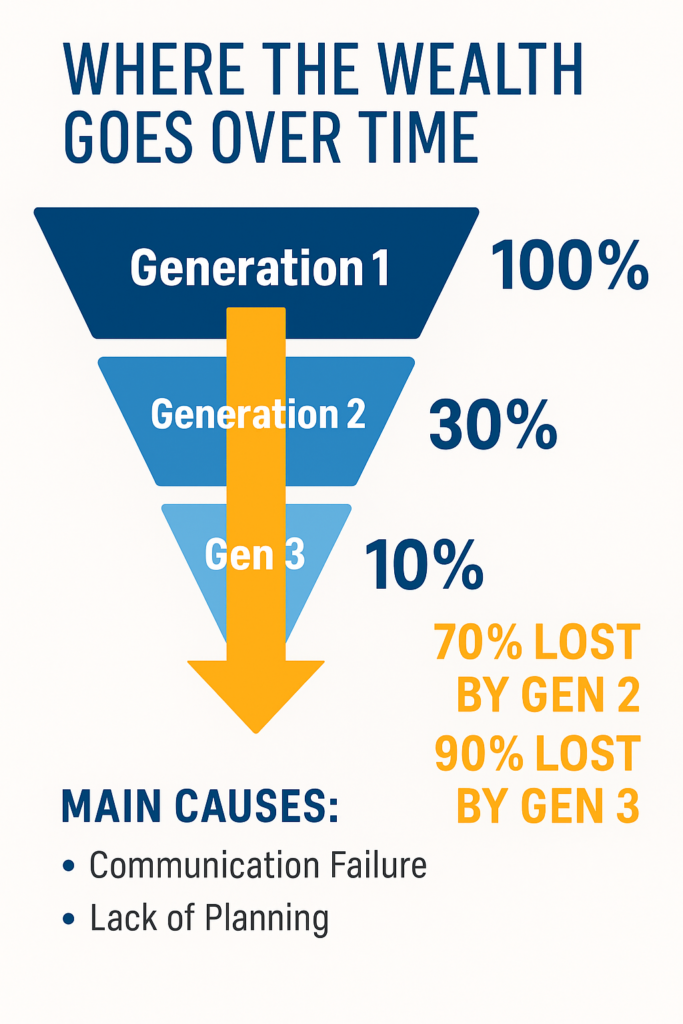

The Stakes Are High: Why Planning Matters

A 20-year study by The Williams Group found that 70% of wealthy families lose their wealth by the second generation, and 90% by the third. These numbers are sobering, especially when considering the intention behind most wealth transfer plans to create lasting security, opportunity, and impact for future generations.

So, what causes this dramatic decline? It’s rarely due to poor investment returns or mismanagement of assets alone. More often, the root causes are soft issues:

- A lack of open, transparent communication across generations

- Failure to prepare heirs for the responsibilities that come with wealth

- Unclear or incomplete estate plans that focus on tax minimization but ignore family dynamics

High net worth families are in a powerful position to reverse this trend, but it requires more than just financial tools. It takes intentional legacy planning, built on values, education, and trust. Even the most sophisticated investment portfolios and estate strategies can fall short without proactive efforts.

At its core, generational wealth transfer is not just about passing down money; it’s about passing down meaning. By creating alignment between family members, articulating a shared vision, and empowering heirs to make wise financial decisions, families can protect not only their assets but also their legacy.

Key Legal and Financial Tools for Passing Wealth to Heirs

1. Trusts

Trusts are essential in estate planning for high net worth individuals. They allow for controlled distribution of assets, protection from estate taxes, and privacy. Common options include:

- Revocable Living Trusts: Useful for avoiding probate and managing assets during your lifetime.

- Irrevocable Trusts: Offer greater tax advantages and asset protection.

- Dynasty Trusts: Allow wealth to be passed down for multiple generations with minimal tax impact.

2. GRATs (Grantor Retained Annuity Trusts)

GRATs are a popular strategy for transferring appreciating assets to heirs with little to no gift tax. The grantor receives annuity payments for a set period, after which remaining assets pass to beneficiaries, often with significant tax savings.

3. Family Limited Partnerships (FLPs)

FLPs provide control, tax efficiency, and asset protection. Parents can retain control while transferring interests to children at discounted values, helping reduce estate and gift taxes.

4. Annual Gifting Strategies

The IRS allows individuals to gift a certain amount per year ($18,000 per recipient in 2024) without triggering gift taxes. Over time, these gifts can add up to a significant wealth transfer.

5. Charitable Giving Vehicles

Donor-advised funds (DAFs), charitable remainder trusts (CRTs), and private foundations are all effective tools for aligning tax planning with philanthropic goals.

The Human Side of Wealth Transfer: Communication & Culture

While legal strategies are important, they’re only one part of the equation. Generational wealth transfer is most successful when families also address the soft skills, education, expectations, and values.

Educating Heirs Early

Providing financial literacy and education to heirs is vital. Many inheritors are unprepared to manage wealth and make decisions aligned with the family’s legacy. Consider including heirs in discussions about investments, philanthropy, or business operations.

Creating a Family Mission Statement

A written mission statement clarifies your values and goals, providing a foundation for how wealth should be used and passed on. It helps younger generations connect emotionally with the legacy and make decisions accordingly.

Managing Expectations

Unspoken assumptions about wealth often lead to conflict. Open conversations around inheritance timing, responsibilities, and structure can minimize surprises and resentment.

Balancing Control with Empowerment

Trusts and other legal structures are designed to provide oversight, but too much control can create dependency or resentment. Work with advisors to find the right level of flexibility, enough to protect wealth while still empowering beneficiaries.

The Advisor’s Role in Guiding Generational Wealth Transfer

This process isn’t one you should go through alone. A fiduciary financial advisor brings objectivity and clarity to an emotionally charged topic. At RIA Advisors, we work with high net worth families to:

- Design multi-generational estate plans

- Facilitate family meetings and legacy discussions

- Align investment, tax, and legal strategies under one roof

- Build frameworks that foster education, protection, and intention

We understand that legacy isn’t just about money, but more about meaning.

Don’t Wait Until It’s Too Late

Whether your estate plan is already in place or still on your to-do list, now is the time to consider the future. The earlier you involve trusted advisors and start the conversation with your family, the more successful your legacy will be.

Ready to create a generational wealth transfer plan that reflects your values and protects your family? Contact RIA Advisors today to schedule a consultation.

FAQs

What is generational wealth transfer?

Generational wealth transfer is the process of passing assets, investments, or businesses from one generation to the next. It includes legal, financial, and interpersonal considerations.

Why is estate planning for high net worth individuals more complex?

Higher asset levels mean more exposure to estate taxes, legal complications, and family dynamics. Strategic tools like trusts, GRATs, and FLPs help manage these challenges.

How can I prepare my children to inherit wealth responsibly?

Start early with financial education, involve them in family financial decisions, and communicate your values and expectations clearly.

What is the difference between a trust and a will?

A will outlines asset distribution after death, while a trust allows for more control, tax benefits, and privacy, especially important for high net worth estates.

Can a financial advisor help with both the technical and emotional sides of legacy planning?

Yes. A fiduciary advisor like RIA Advisors not only helps with strategy and structure but also facilitates conversations that align the family’s vision and goals.