Inside This Week’s Bull Bear Report

- Market Plunge Took The Bulls By Surprise

- Volatility, Oil Prices & Bond Yields

- How We Are Trading It

- Research Report – Small Business Sales Send A Warning

- Webinar – Market Review With Adam Taggart

- Stock Of The Week

- Daily Commentary Bits

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Plunge Took The Bulls By Surprise

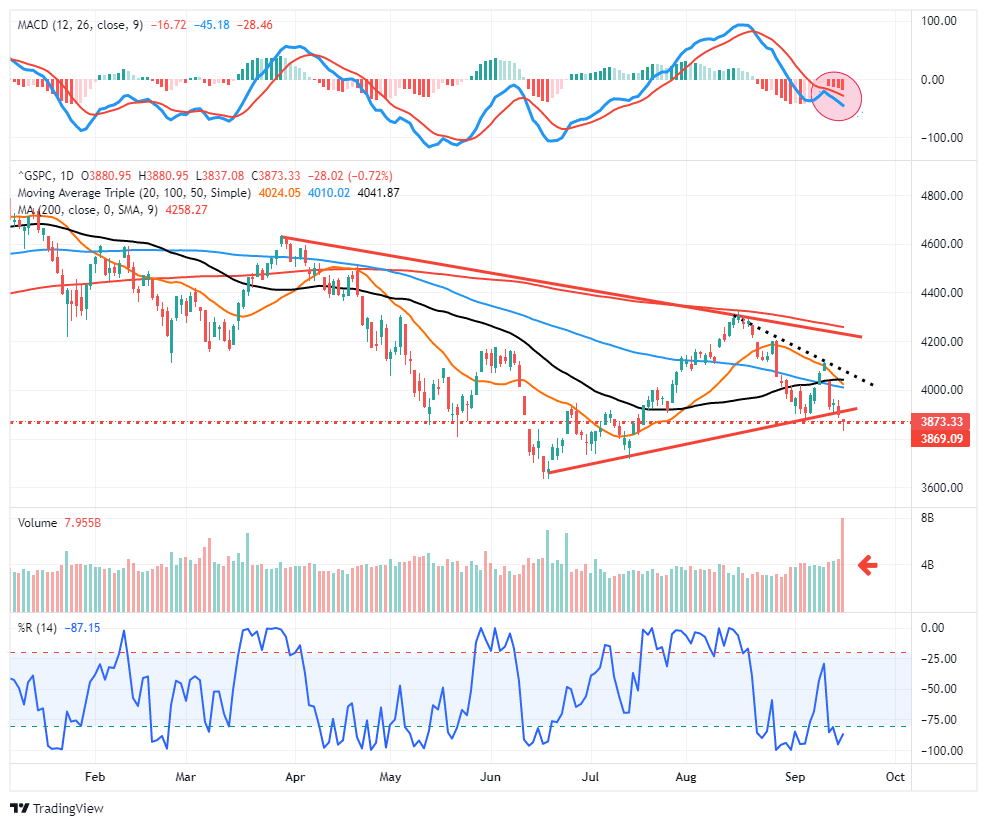

This week did not go quite as planned. In last week’s newsletter, we laid out the case for further gains, given the improvement in some of the technical underpinnings. To wit:

“Notably, the market is setting up a more bullish posture short term, as shown below. First, the market held support at the rising bullish trend line and managed to climb through resistance at the 50- and 100-day moving averages (dma), which now sets up a potential rally to the 20-dma. With markets not overbought, there is fuel for an additional rally into next week, and importantly, the market is very close to flipping the MACD onto a ‘buy signal.‘”

Everything worked fine until the August Consumer Price Index (CPI) numbers hit the headlines. With inflation showing an increase in the inflationary pressures against a general expectation of a decline, the market plunge was severe. Over a single day, stocks erased all of last week’s gains. It was also the most significant single-day decline since June 2020.

Technically, this past week was not good. The market failed at the downtrend resistance line (dotted black), broke below the 50 and 100-dmas, and took out the rising bullish trendline from the June lows. Those levels remain key resistance for the market currently. Furthermore, the MACD signal, close to triggering a “bullish buy signal,” also failed to trigger and continues to work its way lower.

If you want to call it that, the good news is that Friday, which was options expiration, saw a massive surge in volume, suggesting a temporary low. The market also held vital support at the May lows (dotted red line). With the market oversold on a short-term basis, a reflexive rally next week is likely.

As I noted in Friday’s Daily Market Commentary (be sure and subscribe for free pre-market email delivery), the period following options expiration tends to be more positive.

However, investors should sell any rally next week. The technical backdrop remains bearish, and with Fed Ex’s bombshell announcement, the fundamental backdrop likely took a sharper turn for the worse.

Remain cautious for now.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

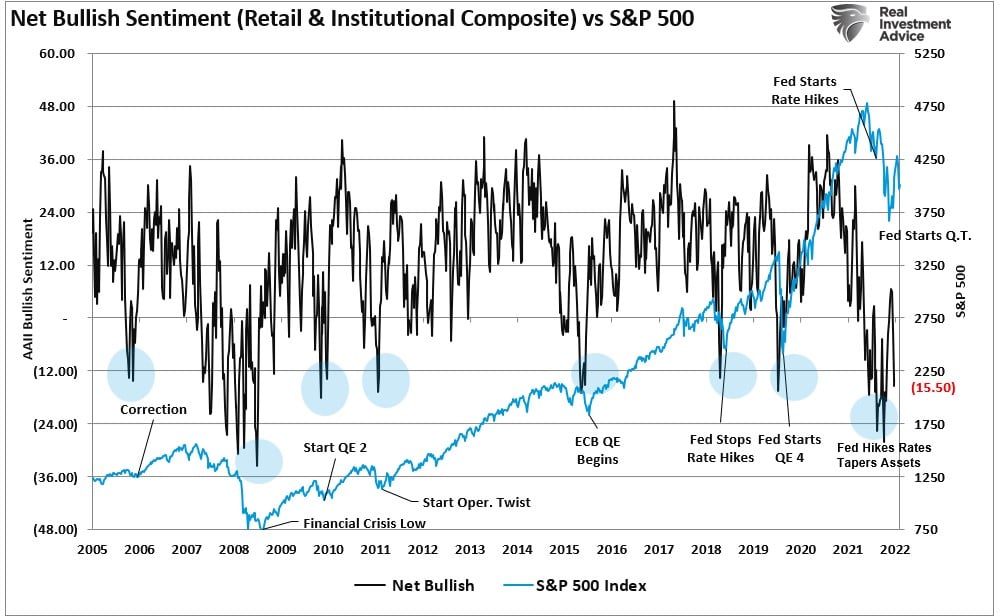

Volatility Remains Very Contained

One of the more interesting aspects of the market this year has been the disconnect between investor sentiment and volatility. As we noted, investor sentiment remains exceptionally bearish, as if the recent market plunge was equivalent to the 2008 “Financial Crisis.”

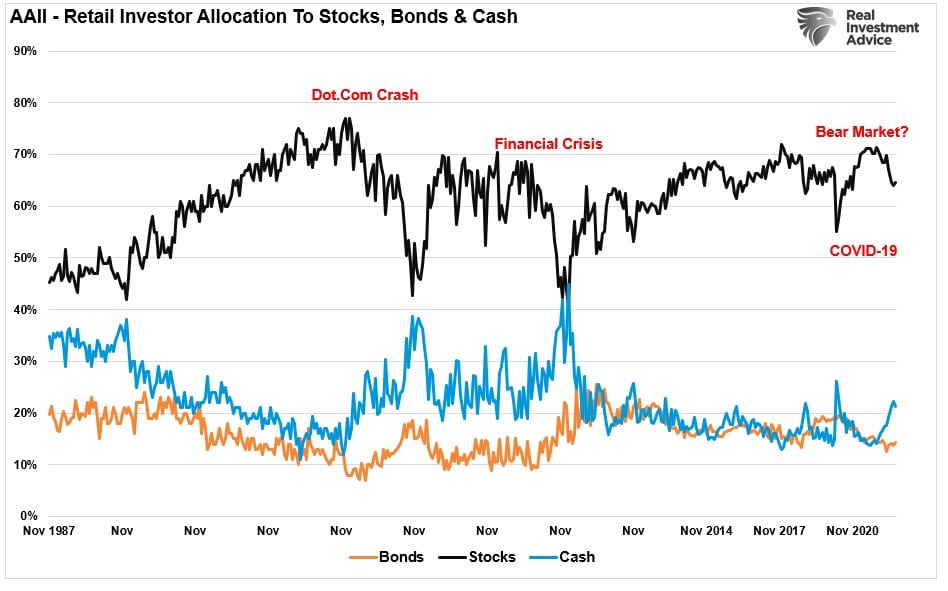

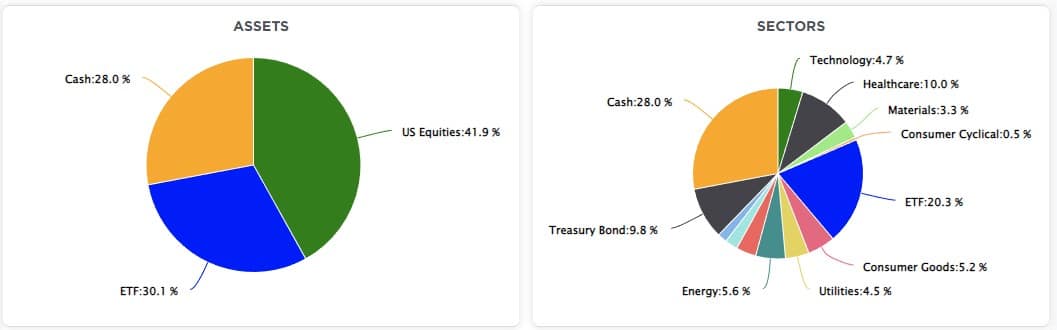

Of course, such is hardly the case, with the market down less the 20% this year. Interestingly, with the Fed aggressively hiking rates and reducing its balance sheet, investors are saying they fear the market. However, they aren’t selling. The chart shows current allocation levels. While equity allocations have declined, they remain well elevated above bear market lows.

Such suggests that while investors “are” terrified of the market, they are unwilling to sell for “fear of missing out.” Much like Pavlov’s dogs, after years of training to “buy the dip,” investors are afraid of missing the Fed “ringing the bell. “

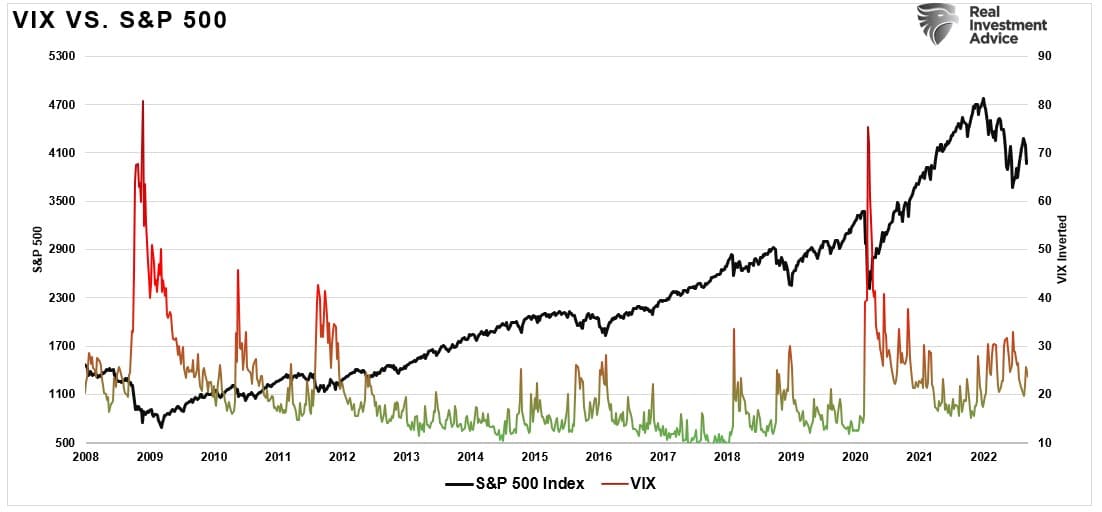

Another interesting measure is the breakdown between investor sentiment and the volatility index. Despite that 4% market plunge on Tuesday, volatility remains significantly suppressed. Historically, market declines should generate higher levels of volatility as investors hedge for a potential crash. Such has not been the case in 2022.

There is currently a large contingent of investors who have never seen an actual “bear market.” As noted above, their entire investing experience consists of continual interventions by the Federal Reserve. Therefore, it is not surprising that despite the recent price decline, they aren’t selling out of the market.

Unfortunately, the risk of disappointment is high as history suggests the Fed will cause a “hard landing” in the economy. If that is the case, a further decline is likely as investors finally give into fear.

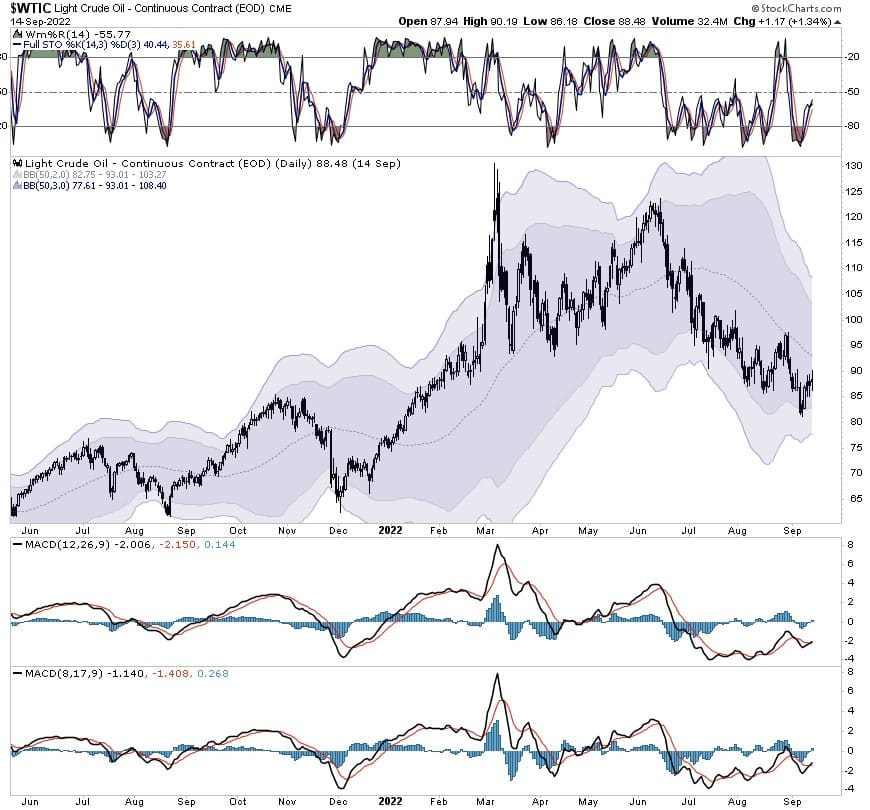

Oil Prices Look Set To Increase

While the market plunge of late got investors’ attention, the decline in oil prices has also become more extreme. Earlier this year, as oil prices surged toward $120/bbl, investors were overly exuberant about the direction of oil prices and related energy stocks. We wrote then that an oil price correction was very likely. To wit:

“Sell energy stocks? Such certainly seems counter-intuitive advice given high oil prices, geopolitical stress, and surging inflation. However, some issues suggest this could be the time to ‘sell high.'”

The most crucial point of that article was this:

“Of course, slowing economic growth and deflationary pressures will contribute to the decline in oil prices. One of the things that could generate that environment sooner than later is the Federal Reserve tightening its monetary policy.

Historically, when the Fed has hiked rates or tapered its balance sheet, oil prices fall due to slower economic growth. Such should not be surprising since oil prices are a function of supply and demand.”

While energy stock prices have not declined sharply yet, oil prices have fallen as demand gave way. The best cure for “high prices” remains “high prices.”

Oil prices have given up a chunk of their recent gains and are now back to more oversold levels, as shown below. With OPEC starting to cut production and the Biden Administration discussing refilling the Strategic Petroleum Reserves (SPR,) there is a demand story getting built to support higher prices. With oil prices very oversold, a rally in oil prices to between $95 and $100/bbl would not be surprising. Such a rally should also give a lift to related energy stocks as well.

However, do not dismiss the impact of the Fed hiking rates and slowing economic demand. As shown in the chart above, while we may see a short-term reversal in oil prices from a technical perspective, the economics will weigh on prices longer-term. As noted, historically, as the Fed hikes rates to the point it causes a recession, oil prices will contract as demand falters.

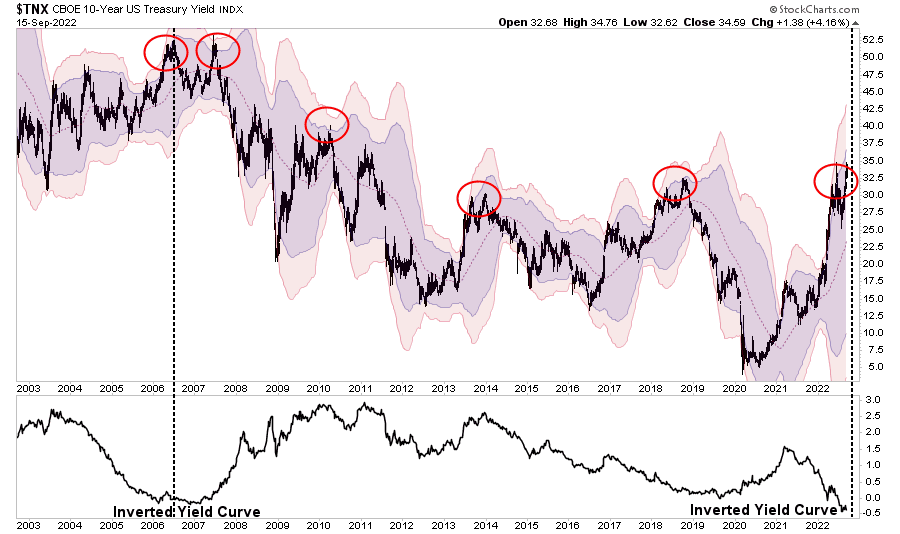

Yields Are Back To A Peak

Recently, we added to our long-bond positions once again. Such seems contrary to the mainstream notion that rates can only go higher as the Fed hikes rates. However, in reality, the Fed only controls the short end of the yield curve. The long end gets influenced by economic growth and inflation. Currently, rates are rising because inflation is rising. However, as is becoming more apparent, inflation has peaked, and the economy is slowing down.

As shown below, the surge in 2-year bond yields is unprecedented. Historically, such sharp increases coincide with recessions or market events.

What is essential about the 2-year treasury yield is that it maintains a very high correlation to the Fed funds rates. As shown below, the current surge in the 2-year rate is leading the Fed funds rate suggesting the Central Bank is still behind the curve on rate hikes.

The longer end of the yield curve, the 10-year Treasury rate, is also pushing extreme deviations. Furthermore, when that yield peak occurs in conjunction with an inverted yield curve, such remains an excellent time to extend the duration of bonds in portfolios.

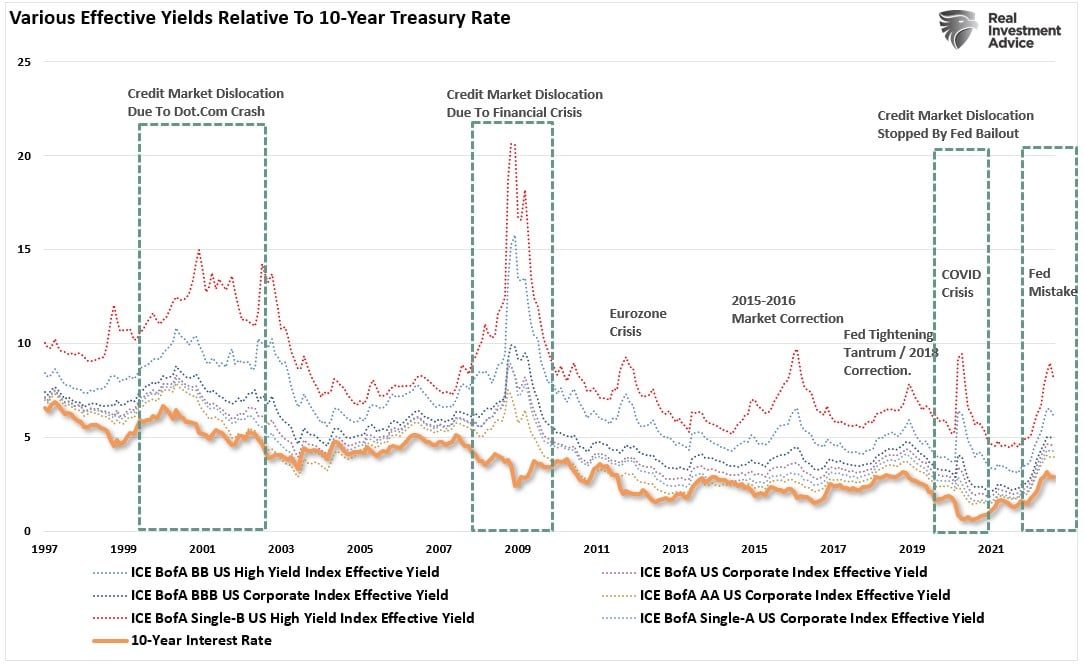

Such is because money flows from risk assets into Treasury bonds for safety when a recession occurs. We see this clearly in the chart below of corporate bond and Treasuries yields. While it hasn’t happened yet, corporate yields rise during a bear market or economic event as money rotates into Treasuries’ safety, causing long-dated yields to fall.

As Jeff Gundlach, the CEO of Doubleline, recently noted:

“The action of the credit market is consistent with economic weakness and stock market trouble. I think you have to start becoming more bearish on stocks. Buy long-term Treasuries. Although the narrative today is exactly the opposite, the deflation risk is much higher today than it’s been for the past two years. I’m not talking about next month. I’m talking about sometime later next year, certainly in 2023.”

While most investors are too short-sighted and try and trade the market from one day or week to the next, the setup for owning long-dated Treasuries into 2023 is continuing to shape up. Such is why we added to our exposures recently.

Not Getting The Bull Bear Report Each Week In Your Mailbox? Subscribe Here For Free.

How We Are Trading It

What a difference a week can make. Last week, we discussed that the market rally was not surprising and, given the reversal of the overbought conditions, provided a setup for an additional rally. Unfortunately, the latest inflation print spooked investors, creating a market plunge of 4% in a single session.

The setup is more bearish than bullish, so we maintain our risk-averse positioning. With higher levels of cash, underweight equity, and bonds, we continue to err towards caution for now. As noted, there is a developing opportunity to own long-dated Treasury bonds, but you will need to give that thesis time to play out into 2023.

The recent sell-off has once again pushed markets back into an oversold condition, so we will look to use rallies to raise some cash and rebalance portfolios. The risk and reward in the market are becoming less favorable, and it appears we may remain trapped in a relatively large trading range for the remainder of this year.

This past week we only made no changes to our portfolio.

In our view, the most significant risk to the market short term is the Fed. While the markets may ignore its more aggressive monetary policy program, the draining of liquidity will eventually impact earnings and asset prices. As Michael Lebowitz noted this past week:

“Tried and trustworthy relationships are failing bond investors. While powerful and concerning, we think the abnormal relationships are temporary. When the supply and demand for bonds normalize, bond investors will likely realize that economic, inflation and other factors warrant much lower yields.“

Got bonds?

See you next week.

Research Report

Market Week In Review With Adam Taggart

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Stock Of The Week In Review

Buying Cash At A Discount

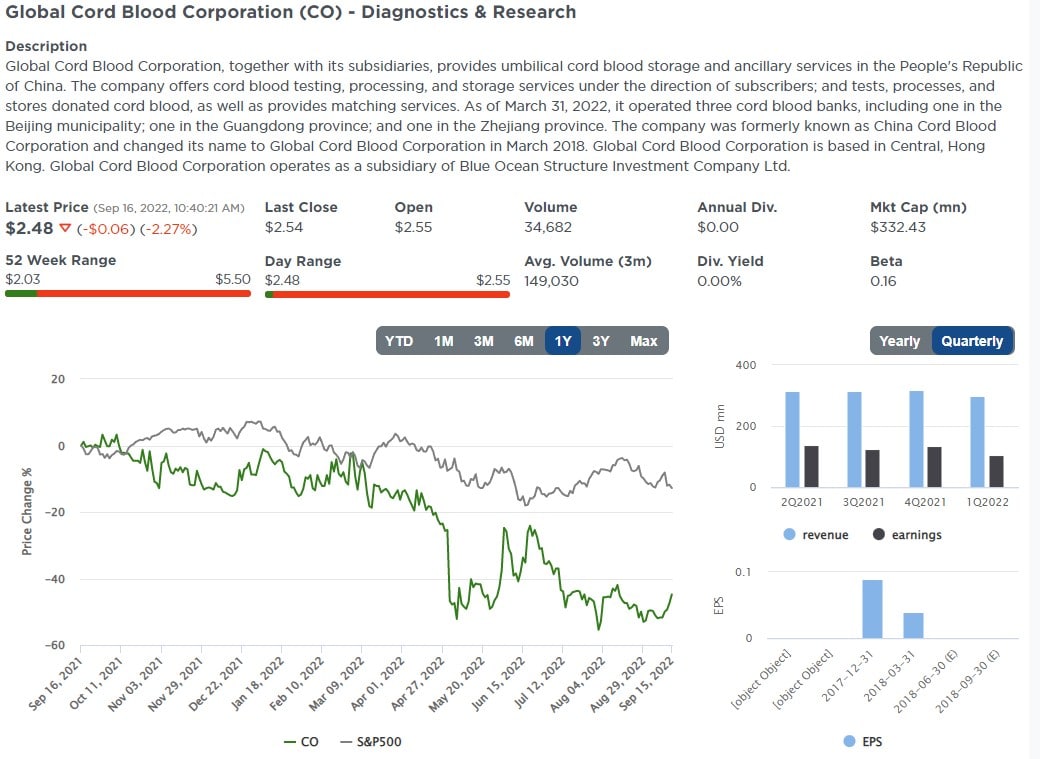

This week’s scan searches for stocks with market caps that are less than the amount of cash on their books. As if buying dollars for pennies isn’t enticing enough, we added a few other factors to our scan to increase the odds the companies can maintain or even increase their cash balances.

The companies below have almost no debt and a good past and forecast earnings growth. All four companies have had double-digit earnings growth rates for the past five years and are expected to grow by at least 10% over the next five years. As small-cap companies, their high cash balance with low debt offers flexibility to jump on high growth opportunities at the right time.

Screening Criteria

- Price to Cash < 1.0

- Market Cap >$100 million

- EPS Growth Last 5yrs >10%

- EPS Growth Next 5yrs >10%

- Debt to Equity <.1

Global Cord Blood Corporation (CO)

Login to Simplevisor.com to read the full 5-For-Friday report.

Daily Commentary Bits

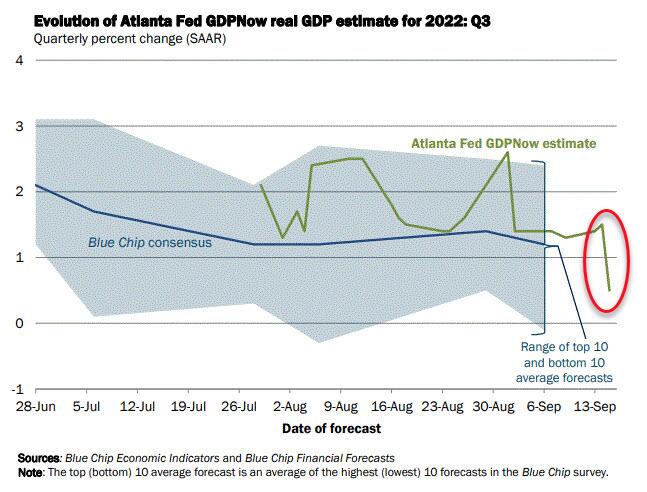

The Economy Is Sick

“Echoing Jim Cramer’s infamous 2007 “they know nothing” rant, a far more calm and eloquent Barry Sternlicht, Chairman and CEO of Starwood Capital, warned the co-anchors on CNBC this morning that if the Fed doesn’t pump the brakes on its rate hikes, the US economy is facing a serious downturn.” – Zerohedge

“The economy is braking hard,” Sternlicht told the outlet.

“If the Fed keeps this up, they are going to have a serious recession and people will lose their jobs.”

He was proved right quickly as The Atlanta Fed cut its GDP forecast for Q3 to just +0.5%.

Click Here To Read The Latest Daily Market Commentary (Subscribe For Pre-Market Email)

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

SimpleVisor Asset Class Trend Analysis

Relative Performance Analysis

Last week, we stated:

“The markets are not yet back to extreme overbought, so further gains next week will not be surprising. However, for now, we continue to suggest selling rallies as markets remain highly vulnerable to reversals,.“

As noted above, that was not what happened, as the CPI report led to a sharp market plunge this week. That decline took the vast majority of sectors back to more extreme oversold levels, likely supporting a reflexive rally next week. We are back into “selling rallies and reducing risk” mode until the technical backdrop improves.

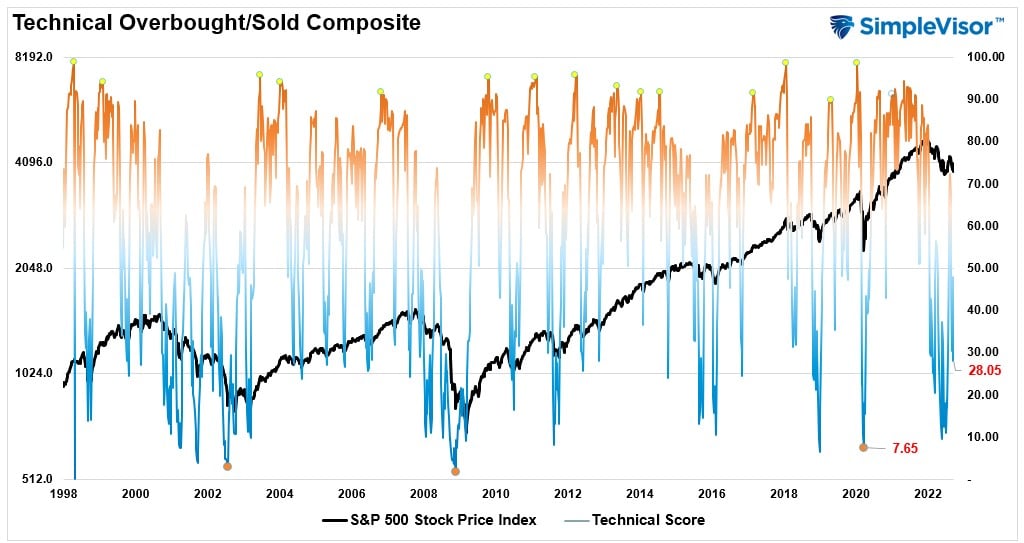

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. Markets tend to peak when readings are at 80 or above, which suggests profit taking and risk management are prudent. The best buying opportunities exist when readings are 20 or below.

The current reading is 28.05 out of a possible 100 and rising. Remain long equities for now.

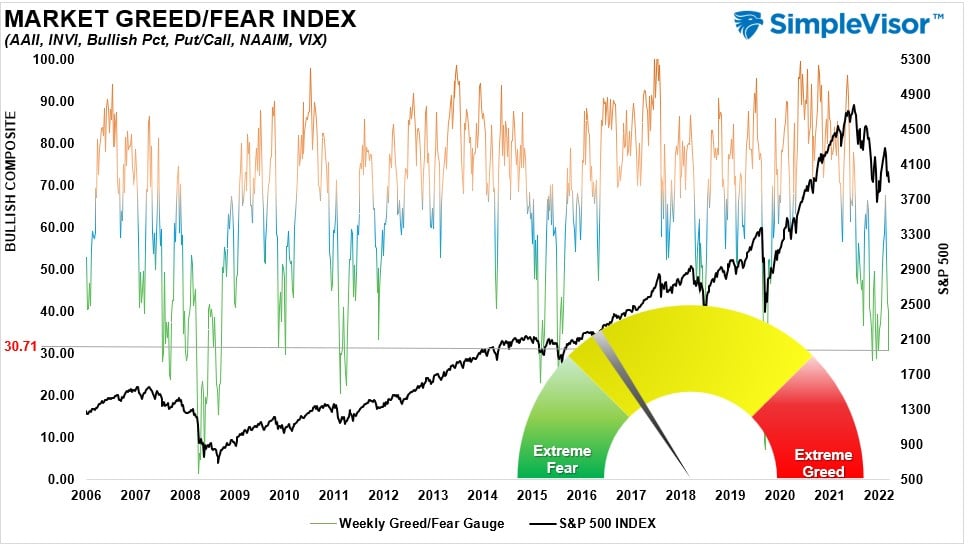

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 30.71 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M/A XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

The market plunge on Wednesday took several sectors and markets into short-term “buy ranges” for a reflexive rally. Communications, Technology, Industrials, Real Estate, and Transportation are below monthly ranges. Bonds are also in a buy zone as well for a trading opportunity. While the market does have room to rally a bit more next week, some profit-taking would be warranted. The risk of a market reversal remains present for now.

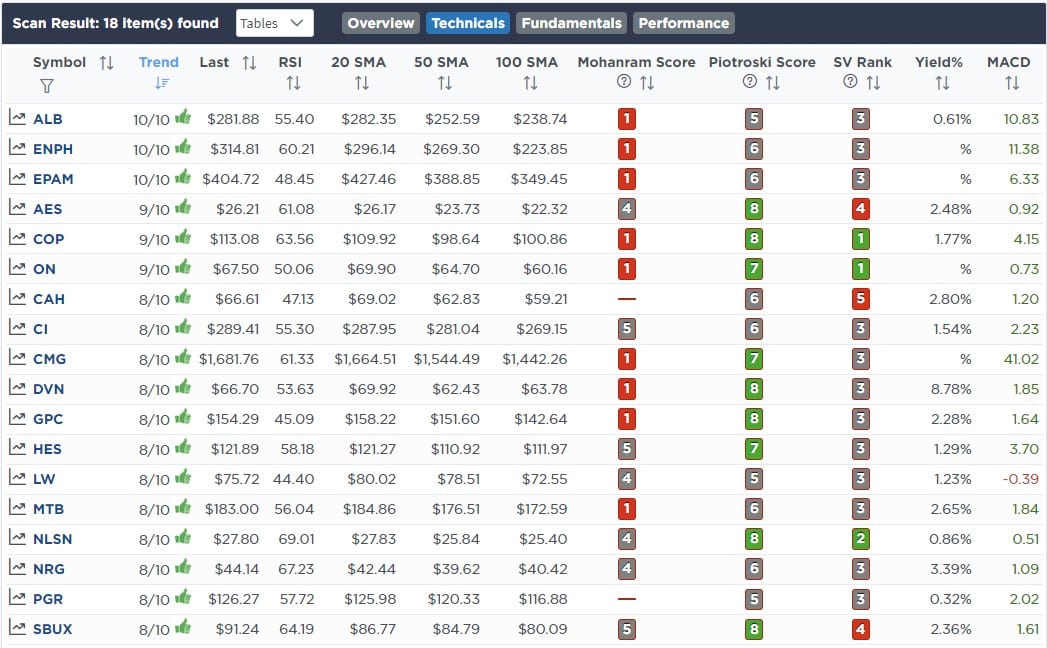

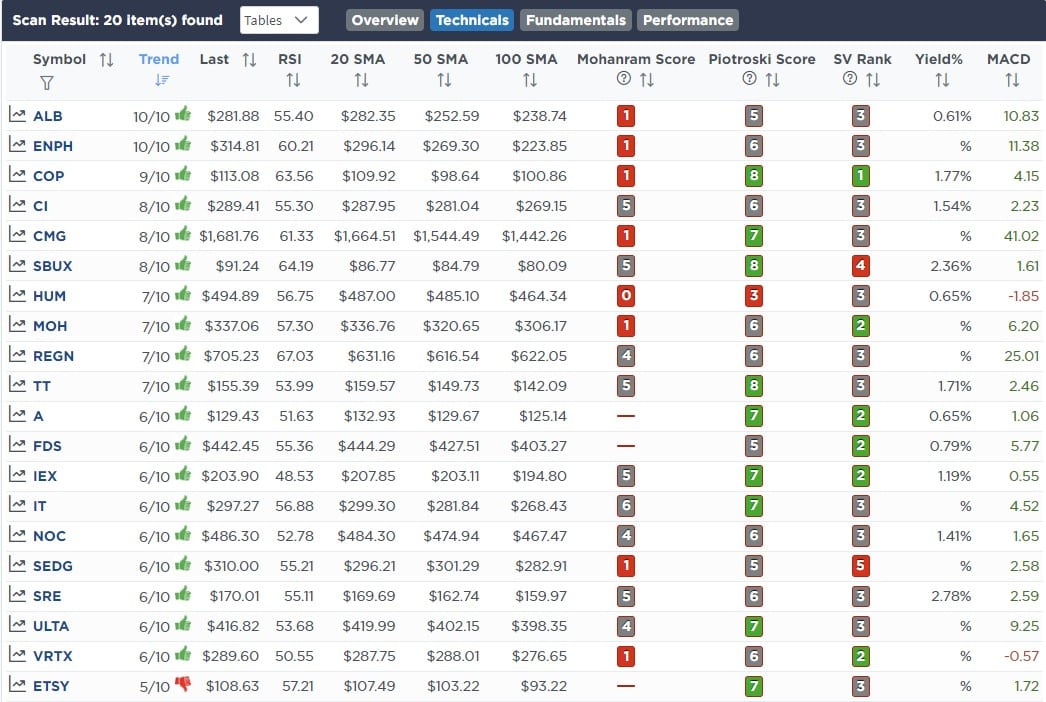

Weekly SimpleVisor Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Changes This Week

Lance Roberts, CIO

Have a great week!