Despite rising interest rates and slowing economic activity, the jobs market remains robust. The BLS monthly jobs market report said the economy added 263k jobs in September, and the unemployment rate fell to 3.5%. The drop in the unemployment rate is welcome news to everyone but the Fed. The Fed is very outspoken about its desire to increase the unemployment rate to help stem high inflation. Given this latest jobs market data, the Fed will likely remain very hawkish.

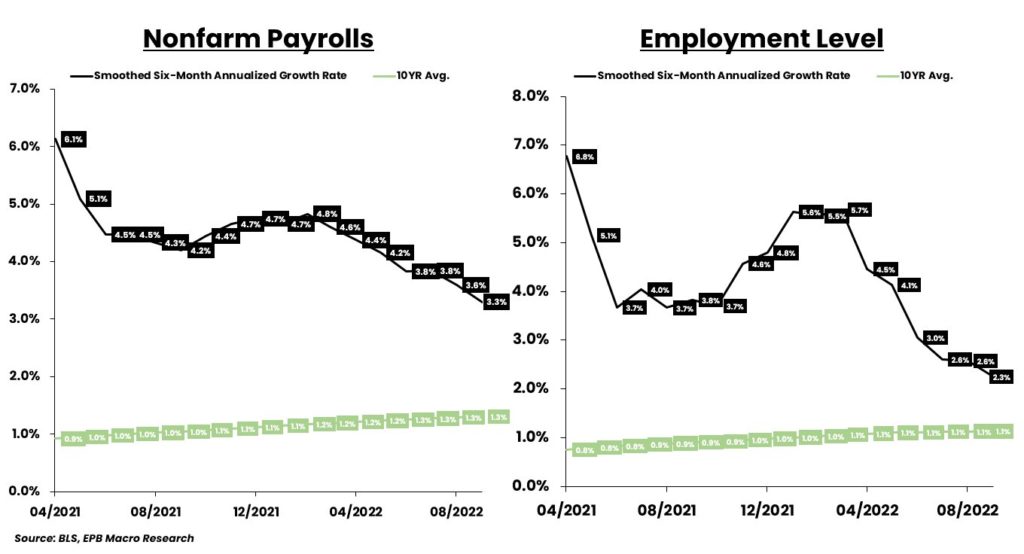

The graphs below from EPB Macro Research compare the two payroll figures the BLS puts out. The well-followed nonfarm payroll data, which surveys businesses, shows 3.3% annualized growth. The less-followed but wider-encompassing household survey shows payroll growth slowing more rapidly. The household survey tends to be more reflective of the jobs market as they survey a broader swath of people and do not double count those with multiple jobs.

What To Watch Today

Economy

- No notable reports are scheduled for release.

Earnings

- Columbus Day Holiday – No Earnings Releases Today

Market Trading Update

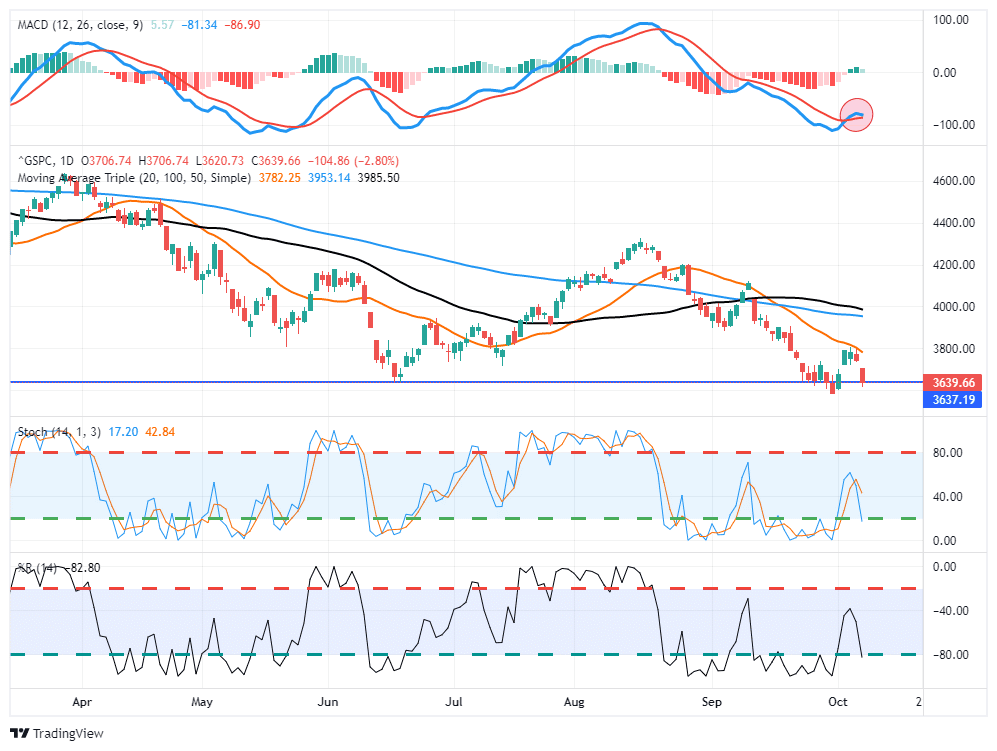

While the market started out the week strong and triggered a MACD “buy signal,” Friday’s selloff was brutal. As shown, the MACD signal remains intact but was weakened considerably, and the market is approaching short-term oversold conditions. I suspect we could see additional selling Monday morning as investors witness their account balances over the weekend and pre-load “sell orders” for the market open.

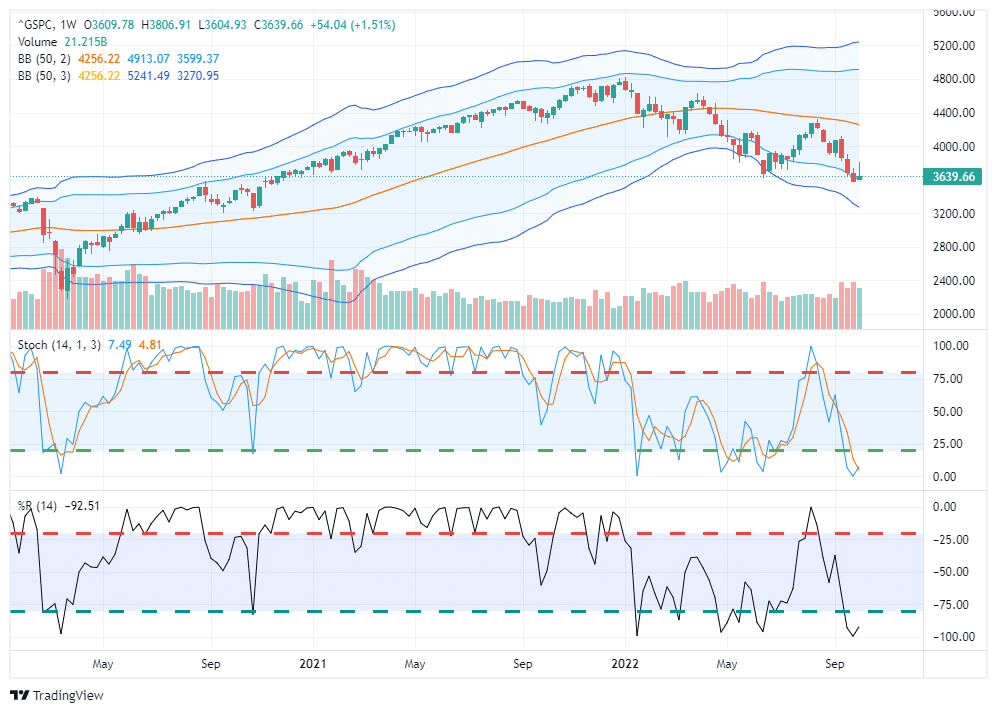

While there was a lot of volatility this week, the market did finish the week in positive territory. As shown in the WEEKLY chart below, the deeply oversold indicators turned up and are close to triggering “buy signals.” The market is also trading 2-standard deviations below the 50-week moving average.

There is certainly downside risk, as we remain concerned the Fed is making a policy mistake by continuing to hike rates. Furthermore, the risk of a recession is increasing, which will slow earnings growth, as we will discuss momentarily. Such is a bad combination for stock prices as we head into 2023. However, given the deep oversold weekly conditions, we continue to suspect a reflexive rally to liquidate positions is likely.

The Week Ahead

After the robust jobs market data last week, investors will now focus back on inflation, the Fed, and corporate earnings.

CPI will be released on Thursday. Analysts expect the monthly rate to increase by 0.1% and the core by 0.5%. Those figures leave 8.2% and 6.4% year-over-year for the core reading. Both are in line with last month. PPI on Wednesday sheds further light on prices. Retail Sales on Friday will help inform us about the health of consumers. The market is expecting slight 0.2% growth. While positive, it is well below the inflation rate, thus pointing to negative real retail sales growth.

Fed Presidents Brainard and Evans kick off the week with speeches today. We expect the Fed will be full of force throughout the week, as they were last week.

Corporate earnings start in earnest this week. The banks lead the way with Blackrock reporting Tuesday. The other major banks like JPM, Citi, and Wells Fargo will report on Friday. Earnings announcements pick up significantly in the following week.

Does The Fed Have A Liquidity Problem?

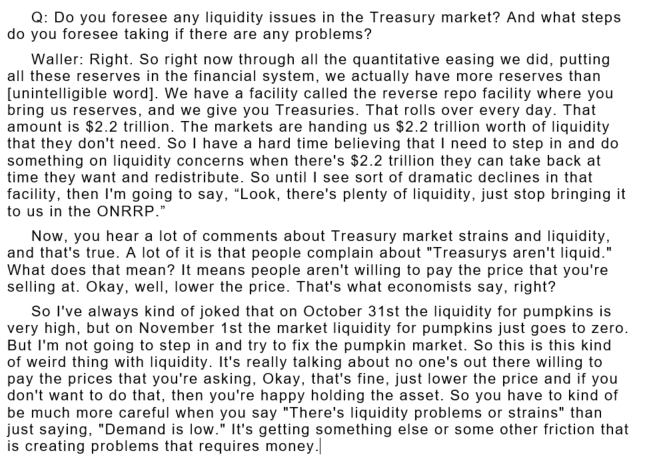

In a recent Daily Commentary, we shared the MOVE volatility index for bonds and associated it with liquidity issues in the bond markets. In a recent question and answer session, Fed Governor Chris Waller has some interesting things to say about liquidity for Treasuries. His thoughts help us consider how serious the Fed views liquidity problems and what they might do to help the bond markets if they think liquidity is problematic.

Waller acknowledges a liquidity problem, but he doesn’t appear to be overly concerned. His comments suggest that he thinks it’s really just a price problem. He equates bond demand with pumpkin prices before and after Halloween. Simply if the price is right, demand will follow. He nonchalantly warns that bond yields may not be high enough to attract sufficient demand. To further his point, he discusses the $2.2 trillion of liquidity parked in the Fed’s overnight repo facilities. Waller views this as pent-up liquidity that will go to the Treasury markets at the right price.

This leads us to conclude that if the Fed deems liquidity problems severe enough, it can tinker with the repo program to make it less advantageous to hold liquidity in its repo programs.

Economic History Says we should be Routing Against the Phillies

The baseball playoffs just started, and with it comes an odd coincident worth considering. While dubious at best, the correlation between Philadelphia baseball teams winning the World Series and economic downturns is frightening. In the early 1900s, the Phillies had a cross-town rival in the Philadelphia Athletics (A’s). The A’s won the World Series in 1910, 1911, and 1913. They won the Series again in 1929 and 1930. We are all aware of the decade-long Great Depression that kicked off with a stock market crash in 1929. However, fewer know of the mini-depression that ran through 1910 and 1911.

In baseball’s modern era, the Phillies won the Series in 1980 and 2008. 1980 began a three-year recession, the most severe since WWII. Inflation at the time was running in the double digits. The most recent world series victory for the Phillies was in 2008. We all remember the Financial Crisis that rocked the economy that year. Whether you are a fan of the Phillies or not, it may be best for your wealth to root against them.

Correlation is not causation, but you have been warned!

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.