“Is cash a good hedge?” It’s a focus of a recent article discussing “fast” versus “slow” risk which examined the financial impact on equities and cash over long-term periods. To wit:

“The simplest analogy to differentiate between fast risk and slow risk is heroin vs. cigarettes. Heroin is a fast risk. Cigarettes are a slow risk. Heroin tends to kill people quickly (especially in the event of an overdose), while cigarettes tend to kill people slowly.

Stocks have lots of fast risks, but little slow risks. The S&P 500 could drop 20% tomorrow, but 30 years from now it’s likely to be much higher than it is today. On the other hand, cash has lots of slow risks, but little fast risks. Next year your dollar should be worth about the same as it is worth today. But 30 years from now? Not so much.” – Nick Maggiulli

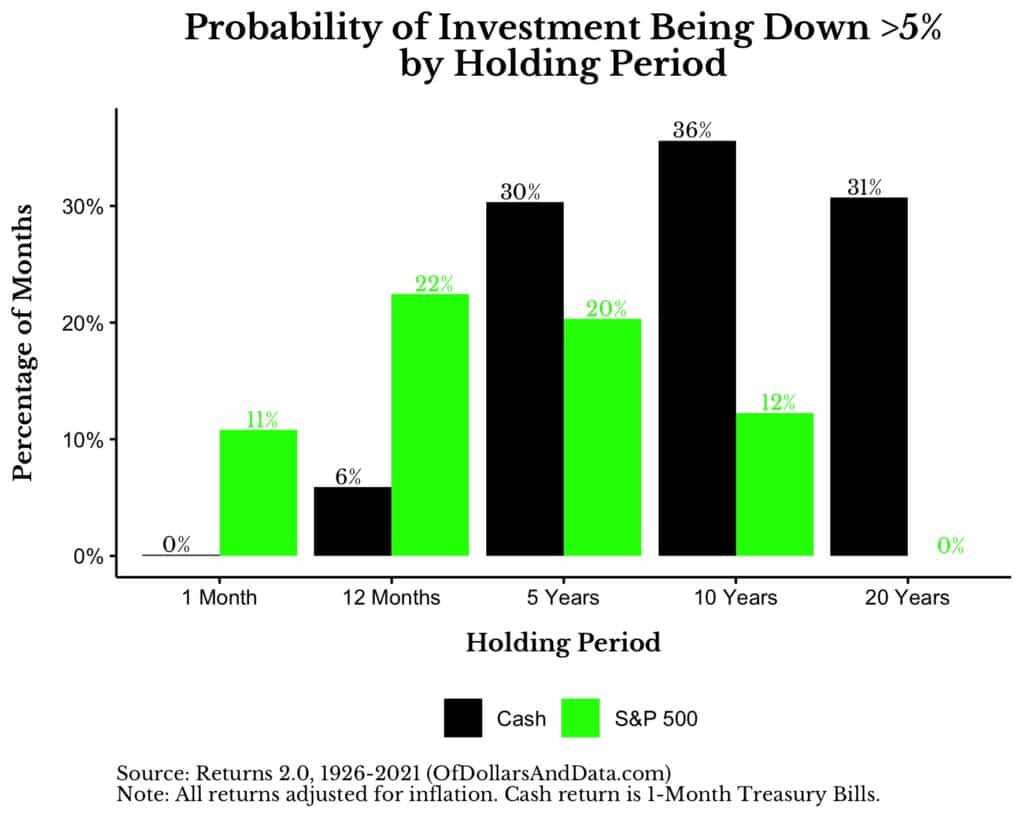

The analysis is correct. The probability of being down 5% during a 20-year period is zero.

Notably, Nick’s point is that cash is NOT a “financially risk-free” asset.

“This is why cash isn’t really a risk-free asset but more of a fast risk-free asset. Cash still has plenty of risk, but it is of the slow variety.

Slow risk doesn’t make headlines. Every time a hedge fund blows up you will probably hear about it. But you never hear about the person who sat in cash for 20 years because they were too afraid to get invested. Both are equally devastating, but one seems less spectacular than the other.”

When thinking about the question of is cash a good hedge or not, remember that holding cash during a bull market can be devastating to financial outcomes. Unfortunately, however, “holding stocks” can also be just as destructive.

Let me explain.

Stocks Have “Fast” And “Slow” Risk

Let’s revisit the graph above. When analyzing returns over long periods, how you interpret the data is crucially important. So, according to the chart, the probability of an index being down 5% over 20-years is zero.

However, this is a vastly different statement than the total return on an investment over a 20-year holding period.

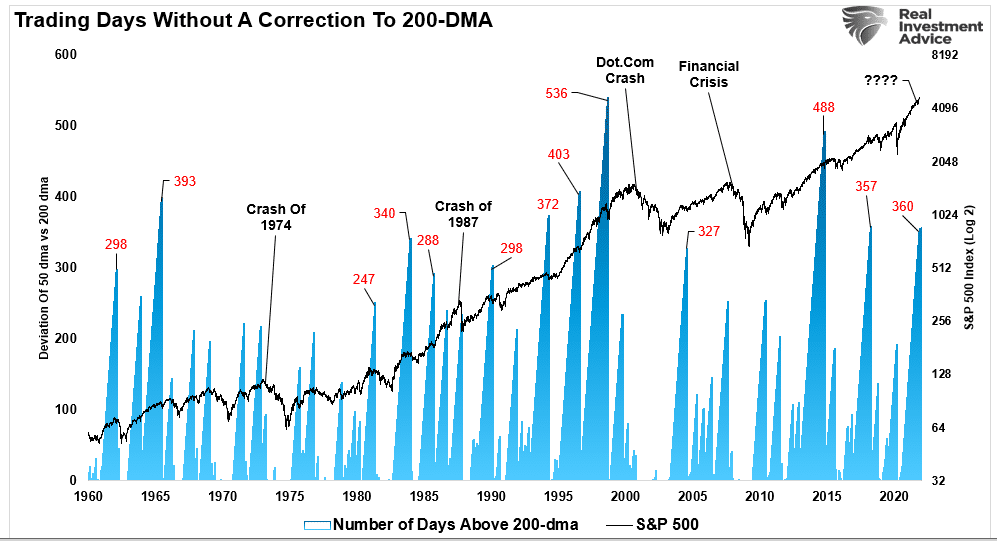

Over a short-term holding period, stocks do indeed have “fast” financial risk. Recently, we reviewed how often stocks mean-revert to their 200-dma.

As noted, corrections to the 200-dma, or more, happen regularly. Sometimes, those drawdowns can be small. At others, they have coincided with crushing bear markets.

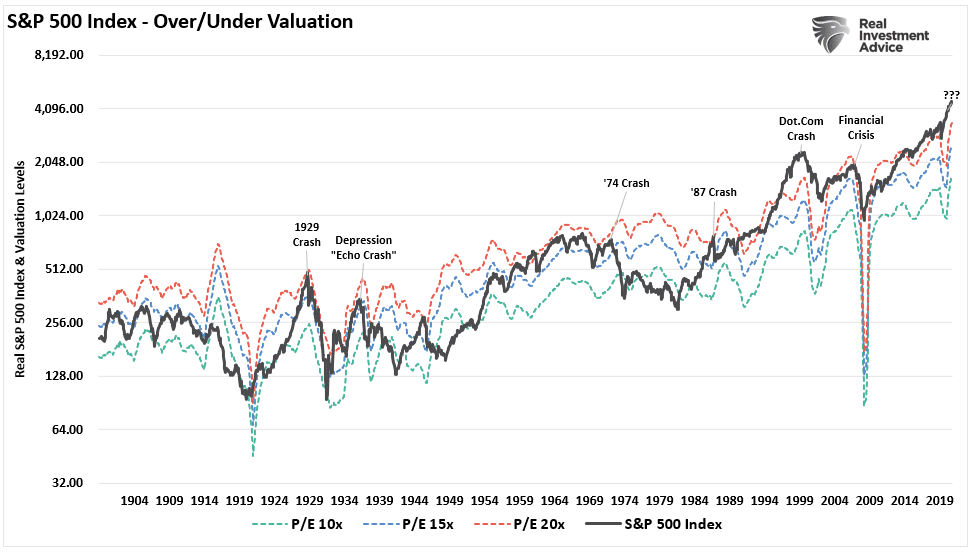

The chart below shows the market from a different perspective. It is the S&P 500 index compared to valuations at 10, 15, and 20x trailing earnings. As shown, the market tends to oscillate between the top of the valuation channel and the bottom over time.

As Nick notes, these “oscillations” represent the financial “fast risks” associated with investing in the equity market. Sometimes, these fast risks can take weeks, months, or a couple of years to play out.

However, investing in the stock market also has “slow risk.”

Starting Valuations Matter To Financial Outcomes

Nick is correct that over 20 years, holding stocks has not had a negative return. However, there is more to the story.

In the short term, a period of one year or less, political, fundamental, and economic data has very little influence over the market. In other words, “price is the only thing that matters.”

Price measures the current “psychology” of the “herd” and is the clearest representation of the behavioral dynamics of the living organism we call “the market.”

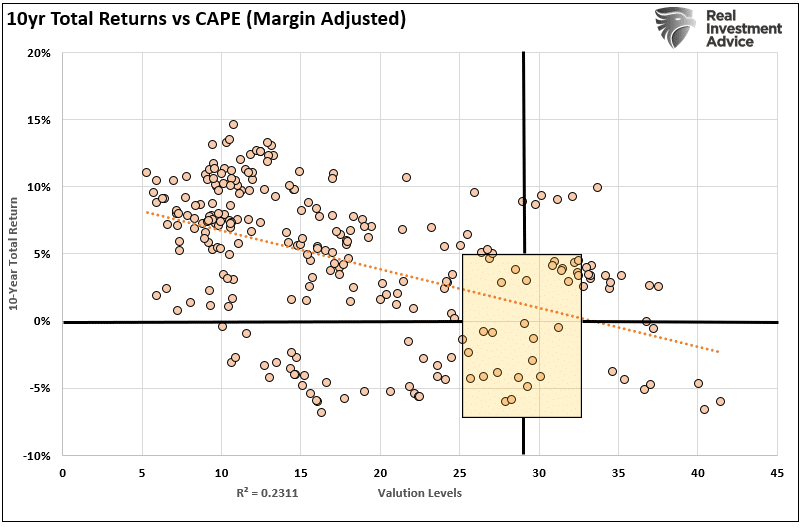

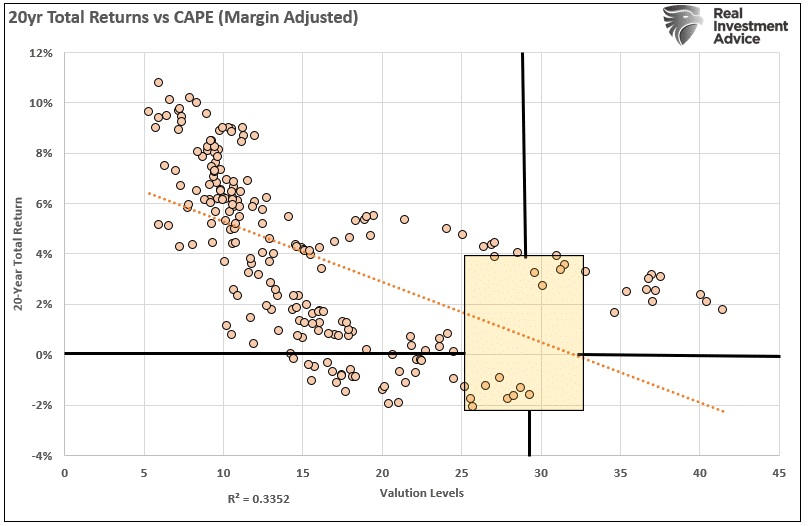

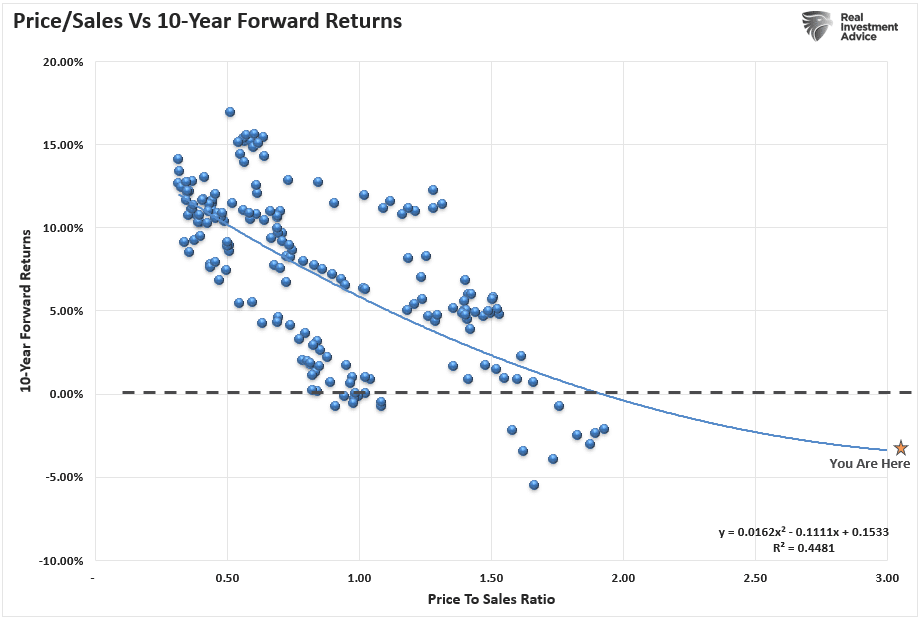

But in the long-term, valuation matters. Both charts compare 10- and 20-year forward total real returns to the margin-adjusted CAPE ratio.

Since many regularly discount the importance of trailing P/E valuations, I will also provide you with the current price to sales ratio.

All three charts suggest that forward returns over the next 10- to 20-years will fall somewhere between -2% and +3%. Such is the “slow risk” of investing in the stock market when valuations get elevated at the beginning of the investment cycle.

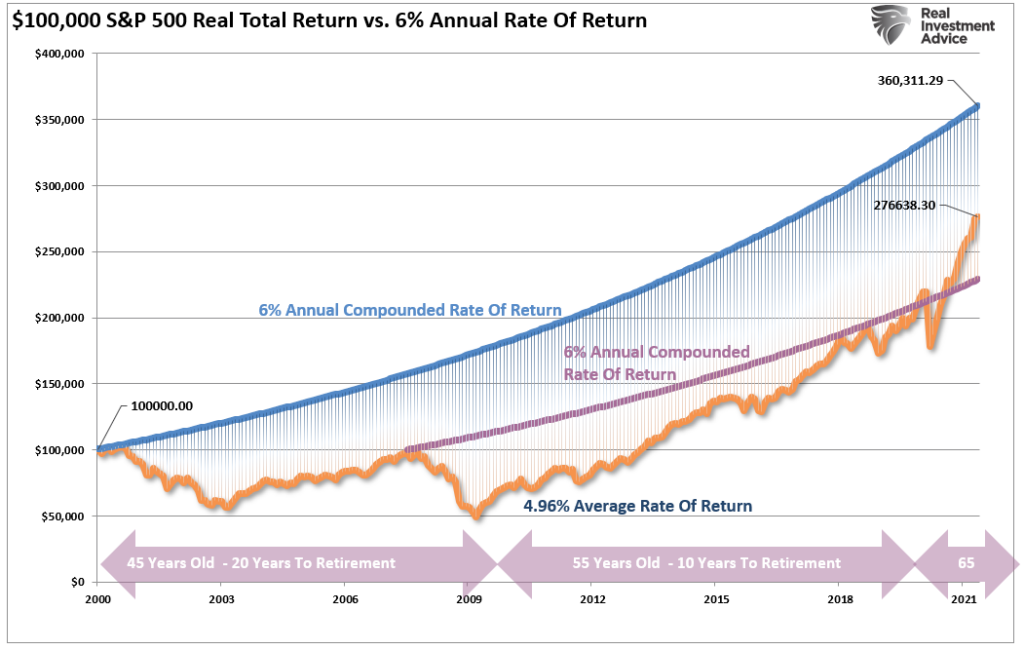

To visualize the importance of “slow risk,” the chart below shows $100,000, adjusted for inflation, invested in 2000 versus a 6% annual compound rate of return. The shaded area presents the difference between the portfolio value and the 6% rate of return.

As noted, due to the impact of two bear markets, the investor that started in 2000 is still well short of the rate of return promised. The investor that began in 2007 only just recently achieved their goal. However, a bear market in the future will set them back markedly.

The problem of “time” is crucially important. For example, if you were 45 in 2000, you didn’t make your retirement goal.

With markets now back to some of the highest valuations on record, the “risk” of “slow risk” has risen markedly.

Is Cash A Good Hedge?

The problem for investors is obvious. Both cash and equities have risks. However, as noted, cash has no “fast risk” but does have “slow risk.” Equities, unfortunately, has both “fast and slow risk.”

That is an important statement. If cash has no “fast risk,” then cash acts as a natural hedge against that risk.

Nick misses in his analysis that investors should never weigh one asset over another over an extended period. Thus, investors never face a choice of solely one investment over another. Instead, the goal is to invest in the correct asset at the correct time. When one is unsure, cash is a natural hedge against uncertainty. As many great investors throughout history state in one form or another:

“The goal of investing is not only the ‘return ON my principal’ but also ensuring the ‘return OF my principal.'”

If I ignore the relevant risk, the outcome is that I will fall short of my financial goals.

Importantly, I am not talking about being 100% in cash. Instead, I am suggesting that during periods of uncertainty, cash provides both stability and opportunity.

Yes, cash will lose purchasing power over the holding period, but equities can lose a lot more when “fast risk” happens.

With the fundamental and economic backdrop becoming much more hostile toward investors in the intermediate term, understanding the value of cash as a “hedge” against loss becomes more important.

Given the length of the current market advance, deteriorating internals, high valuations, and weak economic backdrop, reviewing cash as an asset class in your allocation may make some sense.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is another reason they are so adamant that you remain invested all the time.