There is a gap between the logic of the stock and bond markets. Most stock market analyst expectations are bullish, while Fed Funds futures warn of a recession. The following Business Insider interview with Jeremy Seigel highlights the dichotomy of opinions. Per the article:

“The S&P 500 could surge by 10% to a record high of 5,200 points this year — and plunging interest rates could spell trouble for stocks.”

The gist of his statement is that if the economy remains relatively strong, the Fed will not likely cut rates by much. However, the Fed would likely decrease interest rates by more than a couple of token rate cuts in the event of a recession. Hence, a recession would likely lead to weaker earnings and lower stock prices.

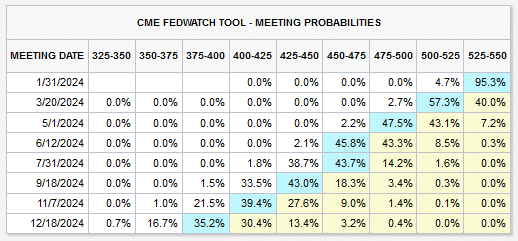

As illustrated in the table below, the expectations based on Fed Funds futures favor 1.75% in rate cuts or seven 25 bps rate cuts in 2024. Siegel concludes: “One has to realize big rate cuts might mean a real slowdown and recession,” he said. “Well, the stock market doesn’t want that.” In the Fed’s latest meeting, they reported their consensus Fed Funds expectations are for three rate cuts. That forecast aligns with a slowing but good economy and continued declines in inflation. Such a Goldilocks scenario would be a best-case outlook for stock and bond investors. Unfortunately, as the markets allude, strong stocks and much lower interest rates represent the dichotomy of having your cake and eating it, too!

What To Watch Today

Earnings

Economy

Investing Summit: Early Bird Registration Available Now

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Joining Greg will be Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

Market trading has remained troubled since the beginning of the year. Despite the surge in stocks, mostly the beaten down Technology sector, on Monday, stocks were mostly mixed yesterday in continued directionless trade. Volume remains light, and conviction remains missing. However, we are working through a consolidation process, which is beginning to work off some of the previously overbought conditions.

The good news is that the market continues to hold above the 20-DMA, which is bullish. Continue to hold long positions as needed and watch for oversold opportunities to pick entry points for new or existing positions to increase overall equity exposure.

Is The BLS Employment Report Rigged?

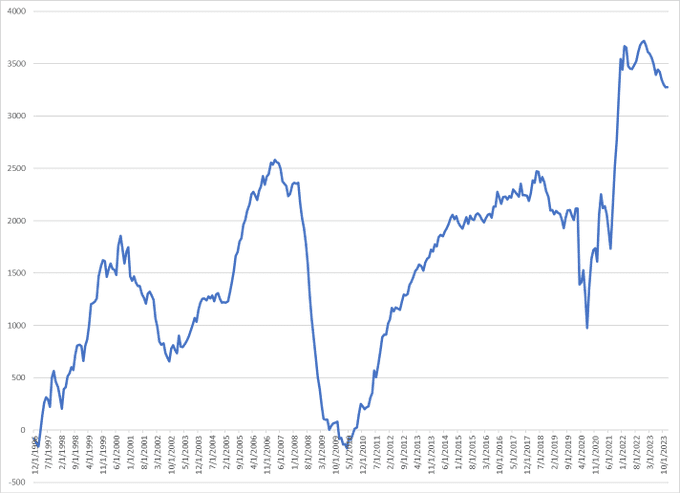

A reader messaged us the Tweet below, showing that the initial payroll count was revised lower in all but one month in 2023. Furthermore, they asked if we thought the BLS employment data was “politically motivated.”

To help answer the question, we share a graph and commentary from Brent Donelly. His graph shows the cumulative net revisions over the last 25 years.

For all those saying NFP is rigged because it’s always strong then revised lower. That’s the opposite of what is true. Chart shows net revisions back to 1997. Massive upward revisions in this cycle. The downward revisions are a recent thing. There have been 172 upward revisions and 149 downward revisions and the average upward revision is much larger than the downward ones. Net revisions in 2021 alone were plus 1.9 million jobs. Revisions go up. Revisions go down. It’s noise, not a complex government conspiracy. NFP is kind of useless anyway. Initial Claims tells you everything you need to know in a more accurate and timely manner. The US labor market is still strong (for now). Data from Bloomberg back to 1997. Final NFP data minus initial release (cumulative) 1997 to now

His data clearly shows a bias toward upward revisions. However, during recessionary periods, downward revisions to employment data are the norm. Therefore, might the recent decline be a recession omen? Consequently, as Brent advises, let’s keep a close eye on initial jobless claims for evidence that the labor market is weakening.

To answer our reader’s question, it seems there is nothing out of the ordinary with the recent revisions, especially if a recession is in the near future. Note that the downward revisions preceded the 2008 recession by over a year.

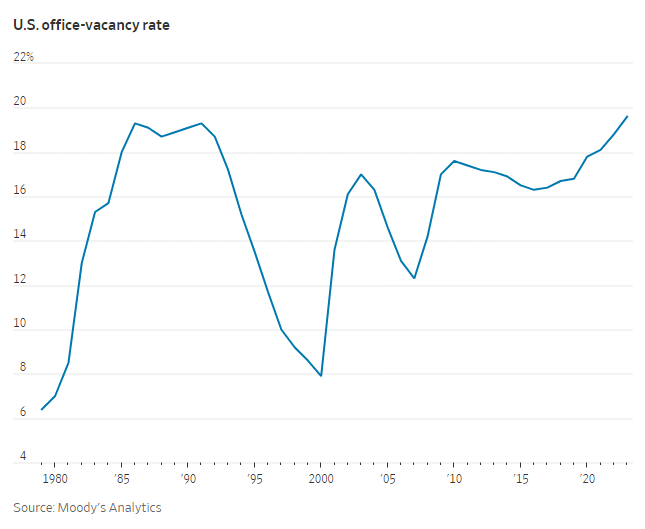

Office Vacancies Set Record

As an example of the woes in commercial office properties, we share the story of a recent sale of an office building in Bethesda, Maryland. The building, pictured below, just sold for $30 million. Not only is the building in a robust economic zone, but it sits on top of a Metro train station.

The 339k square foot building in the close suburbs of Washington D.C. was bought in 2019 for $134 million. The buyer then spent $21 million on renovations and improvements. Consequently, the owner lost about 80% of their investment in four years!

We share the example because office space vacancies are wreaking havoc on the market for office properties nationwide.

To elaborate on the problems, we share a passage from the Wall Street Journal:

A staggering 19.6% of office space in major U.S. cities wasn’t leased as of the fourth quarter, according to Moody’s Analytics, up from 18.8% a year earlier. That is slightly above the previous records of 19.3% set in 1986 and 1991 and the highest number since at least 1979, which is as far back as Moody’s data go.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.