In this 04-22-22 issue of “Did We Just Go Through A Major Bear Market?”

- Market Review And Update

- Did We Go Through A Major Bear Market?

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Weekly Market Recap With Adam Taggart

Market Review & Update

The market started the week out okay but finished sour as Jerome Powell ramped up his hawkish rhetoric of a .50% rate hike at the May FOMC meeting. That meeting will also contain details on the timing of the reduction in the Fed’s balance sheet.

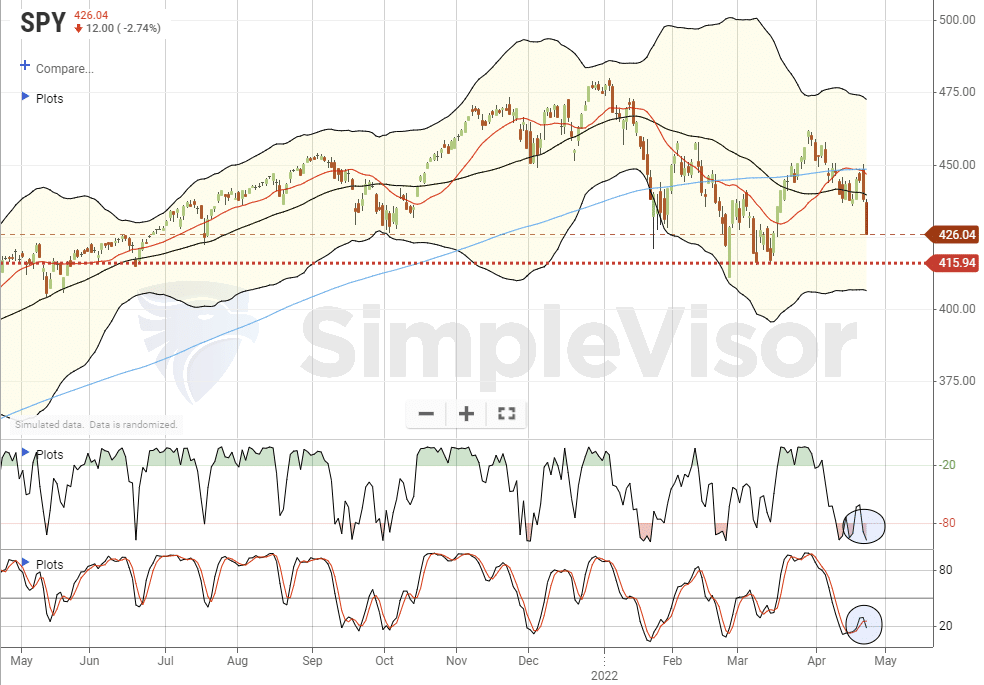

That commentary weighed on the markets even as earnings season rolls in. For the week, the market ended down. While the market is very oversold short-term, the break of the 50-dma suggests we could see a retest of the March lows next week. Such would be around 4150 on the S&P index.

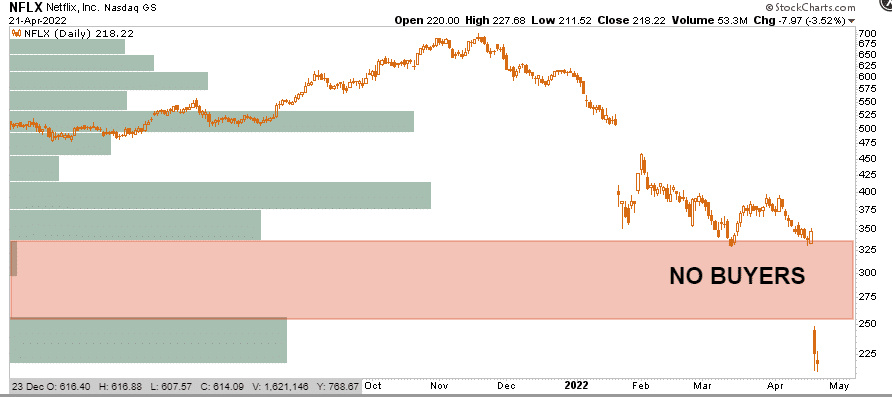

There isn’t much positive news to focus on currently. While we are in the midst of earnings season, we see the impact of higher input costs weighing on profit margins like Newmont Mining (NEM). We saw a shift in consumer sentiment with Netflix (NFLX) and concerns about outlooks as Gap Stores (GPS) consumption slowed. Such doesn’t bode well for earnings and economic growth later this year and, with valuations elevated, makes maintaining current prices more difficult.

It is important to remember that 100% of all the returns in the market since 1871 came ONLY from 5-periods in the market. Those periods started with low valuations and ended with high valuations.

However, in the short term, the technical and psychological setup behind the market does offer the potential for a countertrend rally. Investor sentiment is still very negative, and the markets are oversold on several levels. While such does not mean the next leg of the bull market is about to resume, it is supportive of a rally that could retrace the recent selloff.

Such is what we will be monitoring next week.

Did We Go Through A Major Bear Market

If you haven’t been paying much attention this year, you could be surprised. Despite all of the “bad news, there has not been much consequence.” As shown in the chart below, the markets have made no real progress since September of last year.

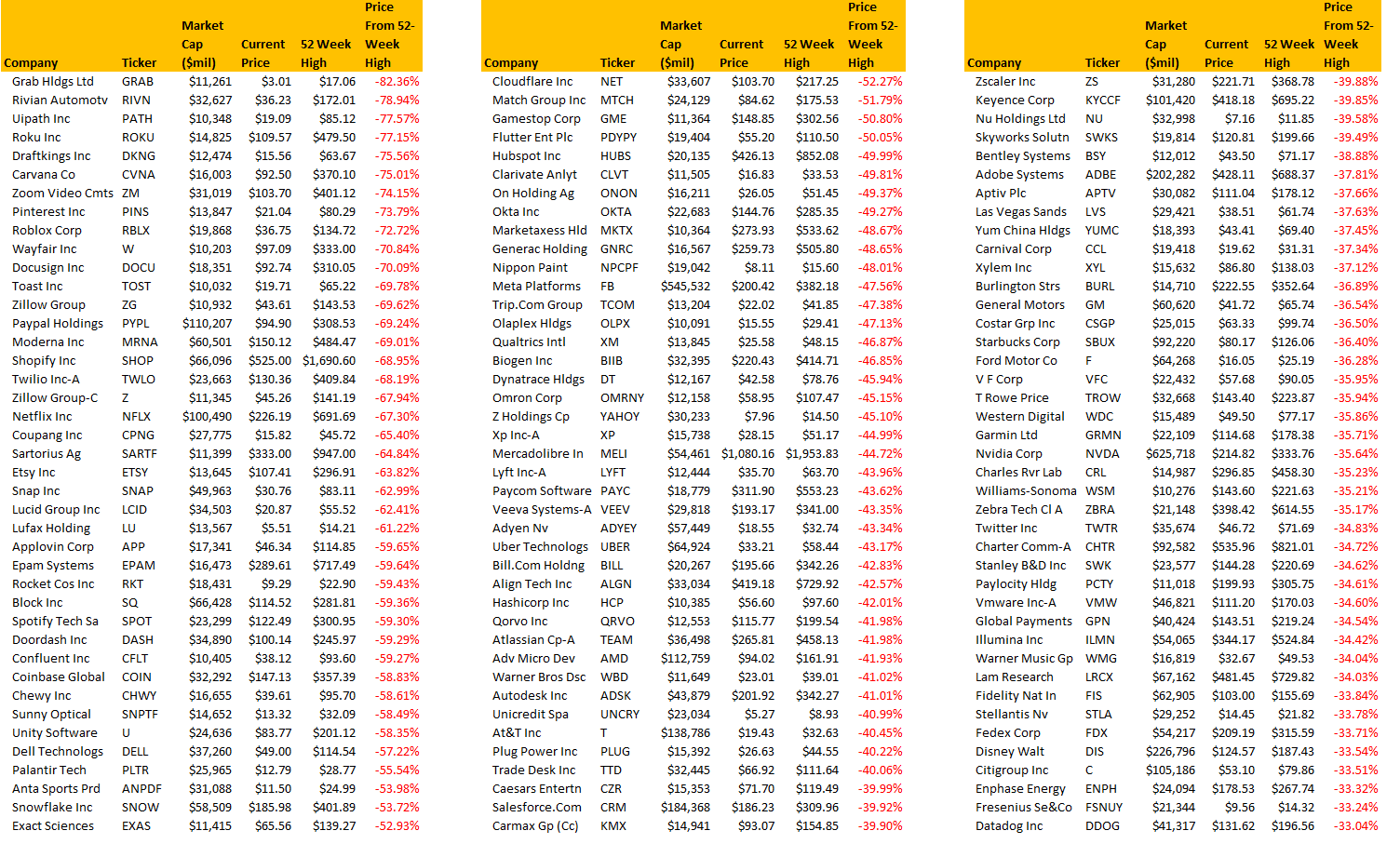

However, despite that lack of progress for the major index below the surface, there was much devastation going on. As the table below shows, of the 700 companies screened with market capitalizations above $7 billion, the 120 companies showed the most price destruction from their 52-week highs. You will notice many of the “meme stock” favorites like Zillow, Zoom, Pinterest, Netflix, etc. These companies are down 33% or more from their 52-week highs. In anyone’s book, that is a “bear market.”

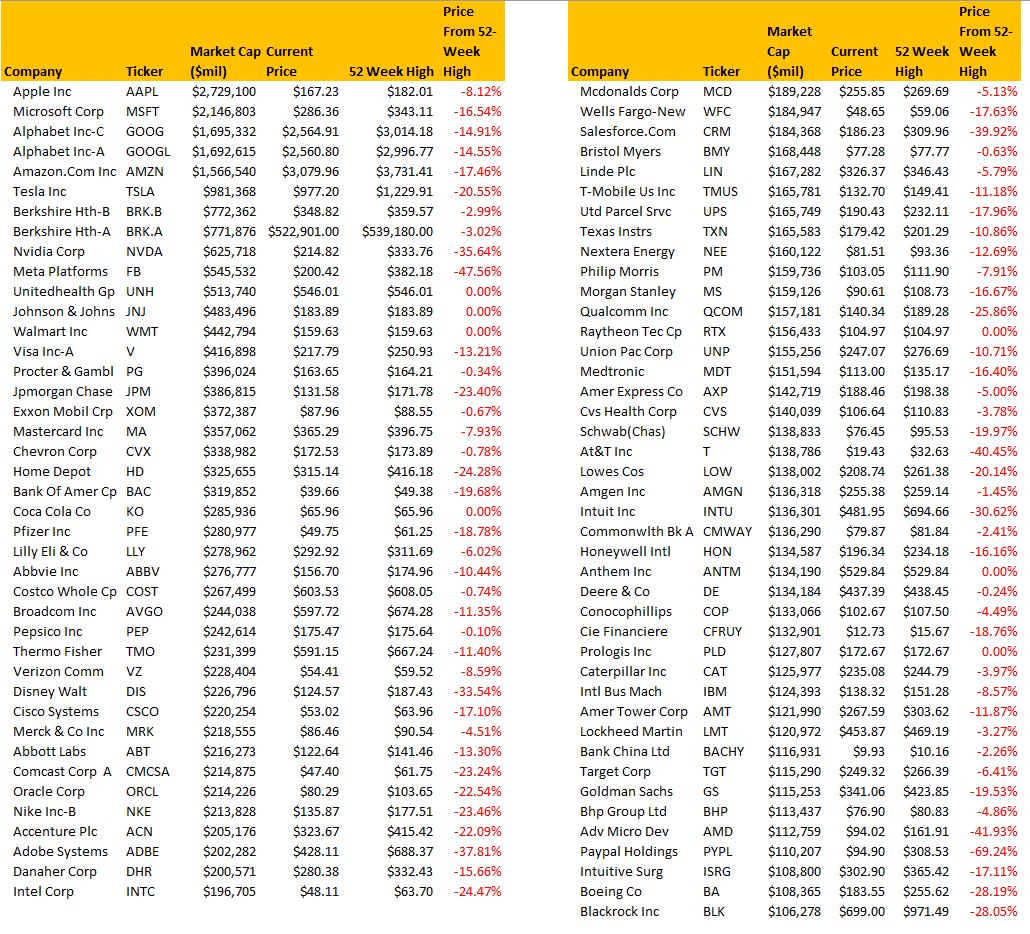

Out of that same scan of 700 companies, the table below shows the 81 companies with the largest market capitalization weight. You will note many companies that are down significantly more than the S&P 500 index for the year. Companies like Nvidia, Facebook (Meta), Salesforce, Paypal, Qualcomm, and even Tesla are down 20% or more from their 52-week highs.

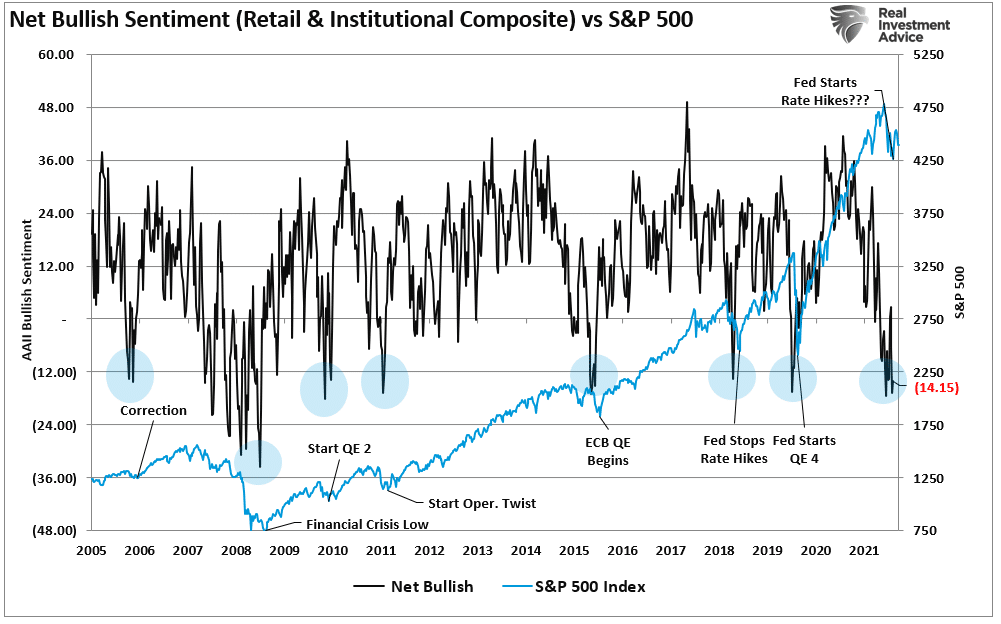

Of course, that destruction of capital weighs on investor sentiment. While the S&P 500 index may only be in correction territory currently, many investors have suffered a “bear market” in their portfolios. That negative sentiment gets shown in many measures, but one of the most common is the American Association of Investors Index. Currently, that sentiment is at levels most often associated with more significant corrections and major bear markets.

The question, of course, is, with many stocks down sharply, how has the market continued to hold up so well?

Market Cap Weighted Illusion

In “Passive ETFs Are Hiding A Bear Market,” I discussed the illusion of performance in the major indices. That illusion gets created by the largest market capitalization-weighted stocks. As a company’s stock price appreciates, it becomes a more significant index constituent. Such means that prices changes in the largest stocks have an outsized influence on the index.

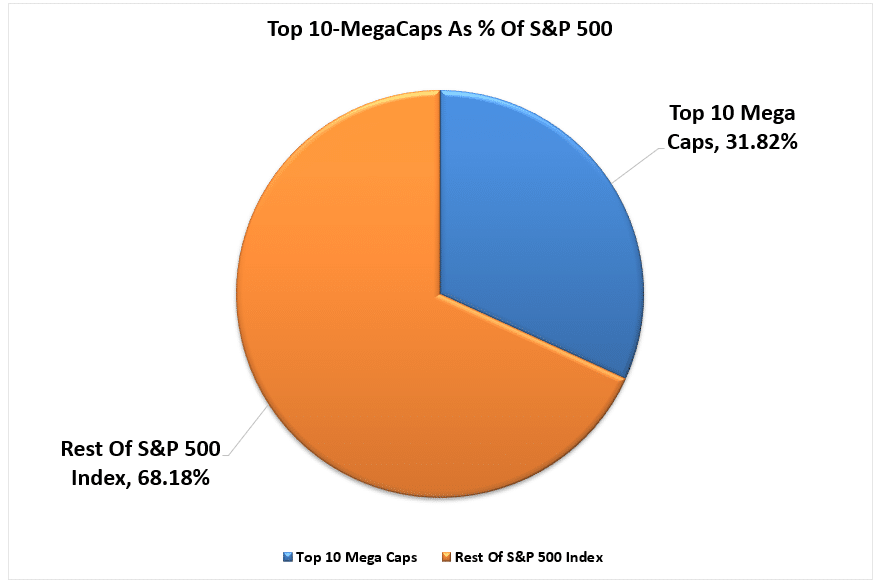

You will recognize the names of the top-10 stocks in the index.

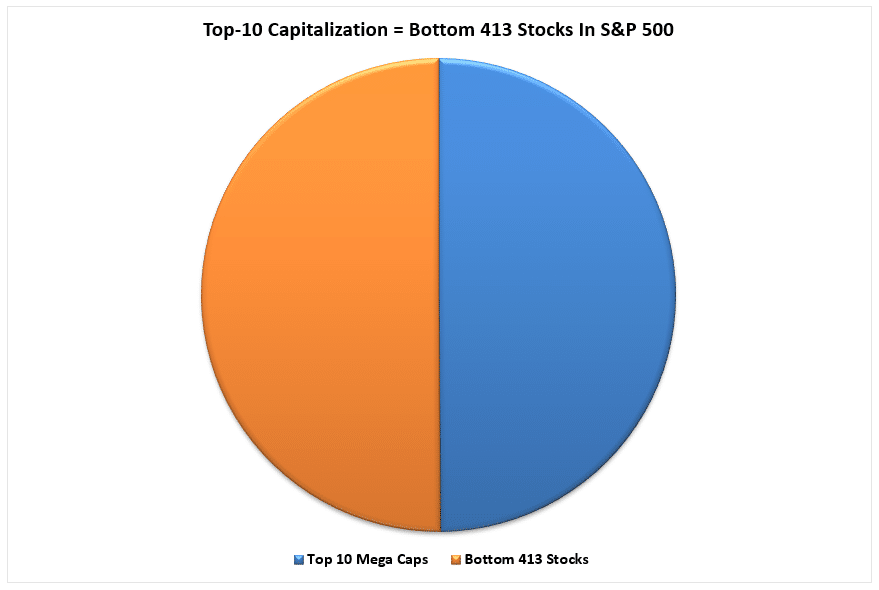

Currently, the top-10 stocks in the S&P 500 index comprise more than 1/3rd of the entire index. In other words, a 1% gain in the top-10 stocks is the same as a 1% gain in the bottom 90%.

Currently, out of 500 stocks, the bottom 413 stocks comprise the same market capitalization as the top-10.

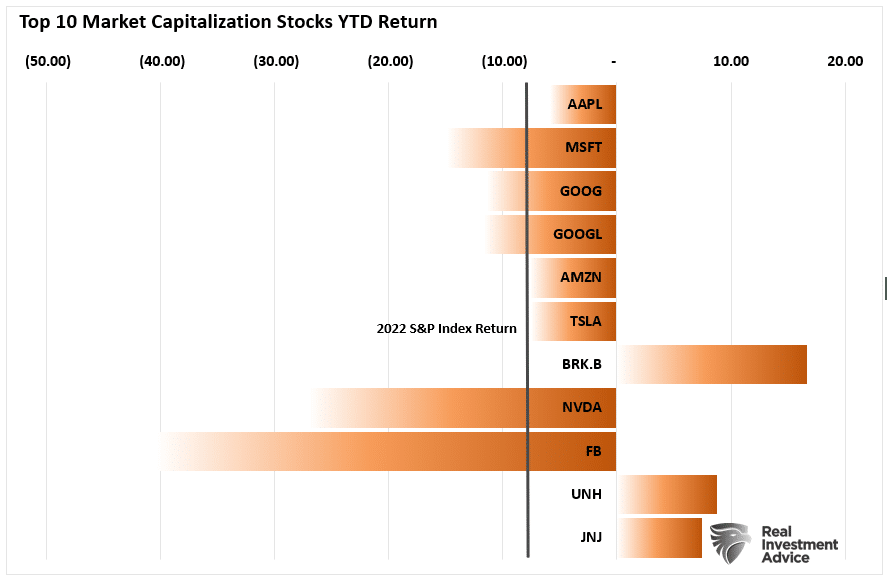

Such is the story of 2022. The year’s return would look different if it were not for the returns in companies like Berkshire Hathaway, United Healthcare, and Johnson & Johnson.

Currently, more than 1750 ETFs are trading in the U.S. Each of those ETFs owns the same underlying companies. For example, according to ETF.com, there are:

- 363 ETFs that own Apple

- 532 own Microsoft

- 322 own Google (GOOG)

- 213 own Google (GOOGL)

- 424 own Amazon

- 330 own Netflix

- 445 own Nvidia

- 339 own Tesla

- 271 own Berkshire Hathaway

- 350 own JPM

In other words, out of roughly 1750 ETFs, the top-10 stocks in the index comprise approximately 25% of all issued ETFs. Such makes sense, given that for an ETF issuer to “sell” you a product, they need good performance.

Therefore, as investors buy shares of a passive ETF, the shares of all the underlying companies must get purchased. Given the massive inflows into ETFs and the subsequent inflows into the top-10 stocks, the mirage of market stability is not surprising.

This Week’s MacroView

A Lack Of Liquidity

The point you should take away from this analysis is the significant risk posed to investors with capital hiding in a handful of stocks. Over the last several weeks, we noted the “lack of liquidity” in the markets and weak breadth. To wit:

The stock market is a function of buyers and sellers agreeing to a transaction at a specific price. Or rather, “for every seller, there must be a buyer.”

Such is why downturns in the market tend to be a “wipe-out” rather than a “pullback.” A good example recently was Netflix (NFLX).

When there are not enough buyers at current prices to absorb an increase in selling pressure, prices gap down. While there are indeed buyers for every seller, they are at significantly lower prices.

However, during these “wipe-outs,” capital continues to flow into the index’s top holdings. Such is because these stocks are highly liquid. For traders, they provide a “safe haven” to move large amounts of capital without creating a gap between buyers and sellers.

However, if capital flows reverse from these top-10 holdings for some reason, the illusion of a strong market will fade quickly. Most likely, those flows will be into bonds for safety as something has likely changed the bullish psychology of the market.

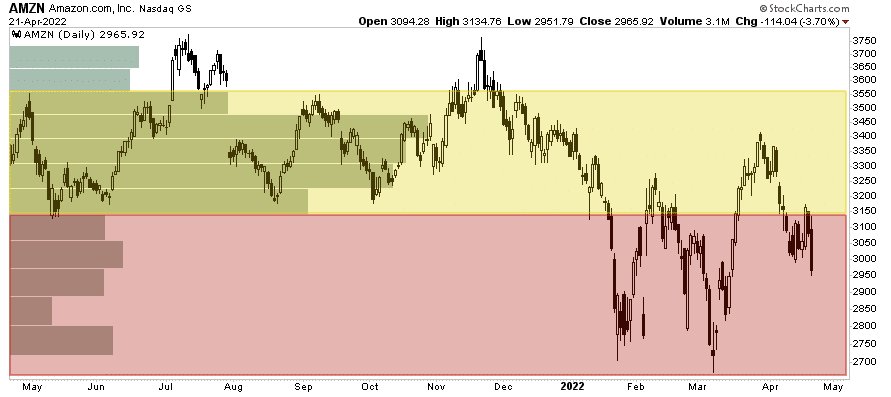

If you are wondering, we recently sold our Amazon (AMZN) as it has now moved to an area with significantly fewer buyers.

If the top-10 stocks come under more significant selling pressure, such will indicate a change in “investor psychology” has occurred. Such will also be an excellent time to start becoming significantly more defensive.

Failing To Plan

I want to repeat something I wrote recently regarding whether a “bear market is lurking.”

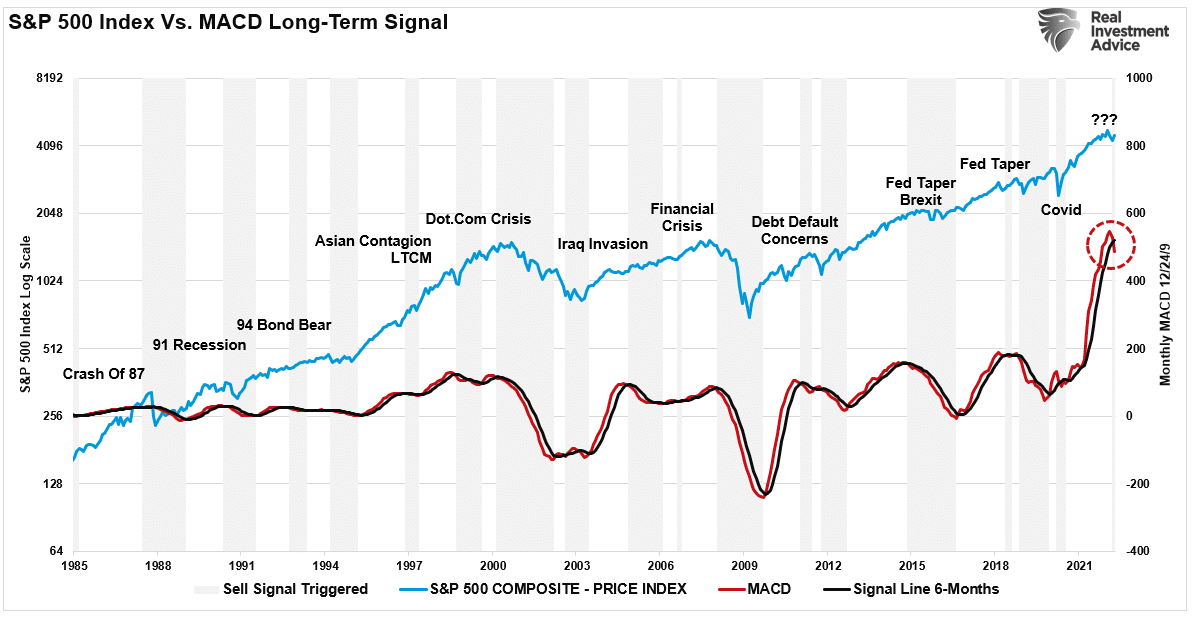

“From a purely technical perspective, the monthly moving average convergence divergence indicator (MACD) also rings a significant warning bell. The chart below measures the difference between the 12 and 24-month moving averages. When that line crosses below the 6-month signal line, such suggests the market is at risk.”

“Such suggests an eventual reversion will be similarly dramatic. The shaded grey bars show when a previous sell signal got triggered. While there are certainly some false signals along the way, it is worth noting that many of the sell signals are closely associated with more critical market-related events, corrections, and major bear markets.”

Is a bear market coming? Maybe. Maybe not. However, we can follow some basic guidelines.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says, “sell everything and go to cash.”

As we concluded:

“Given the weight of evidence currently at hand, it certainly doesn’t hurt to plan and even take some actions to prepare for a storm if, or when, it comes.

If the environment changes, it’s a simple process to reallocate aggressively to equities. By planning, the worst that can happen is underperformance if the bull market suddenly resumes.”

Portfolio Update

We made some minor tweaks to our portfolio allocation this week. We reduced some of our growth names slightly as we head into earnings reporting season. Seeing the sharp selloffs that can occur if a company barely misses expectations, we reduced our exposure to companies we felt had the highest risk.

We kept our reduced equity exposure at current levels by adding an S&P index position to offset single stock equity risk reduction. In hindsight, we would have been better off with the reduced weighting. However, it had a minimal impact on performance.

We continue to expect the next few weeks, and even the next couple of months could remain frustrating. However, as noted above, the markets remain oversold short-term, and earnings could help provide a short-term lift to markets.

Of course, the most significant risk to the market over the next two weeks will be the Fed. As we saw on Thursday and Friday, a more aggressive Fed posture could spook the bond and equity markets. However, I still suspect the Fed will ultimately be more “bark” than “bite.”

One thing is for sure, the “boring market” of 2021 is sorely missed.

The rest of this year will likely remain just as challenging as it started.

See you next week.

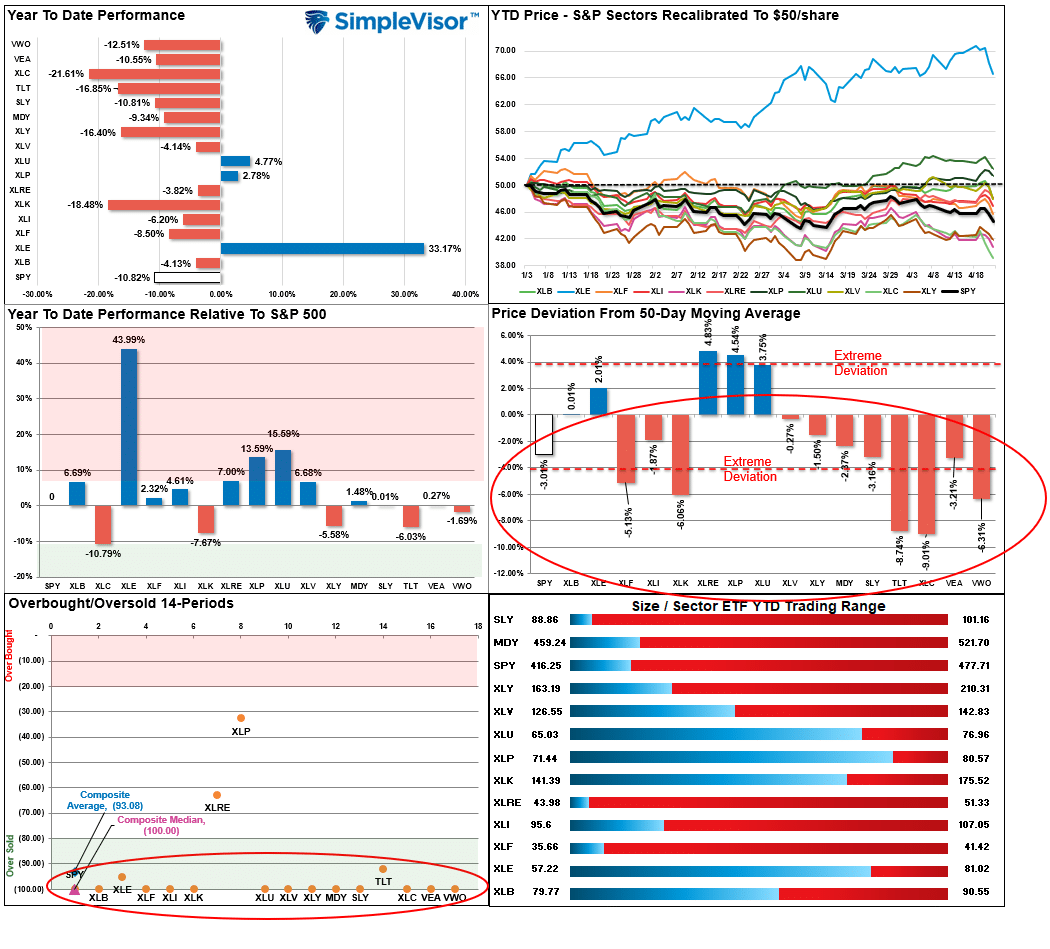

Market & Sector Analysis

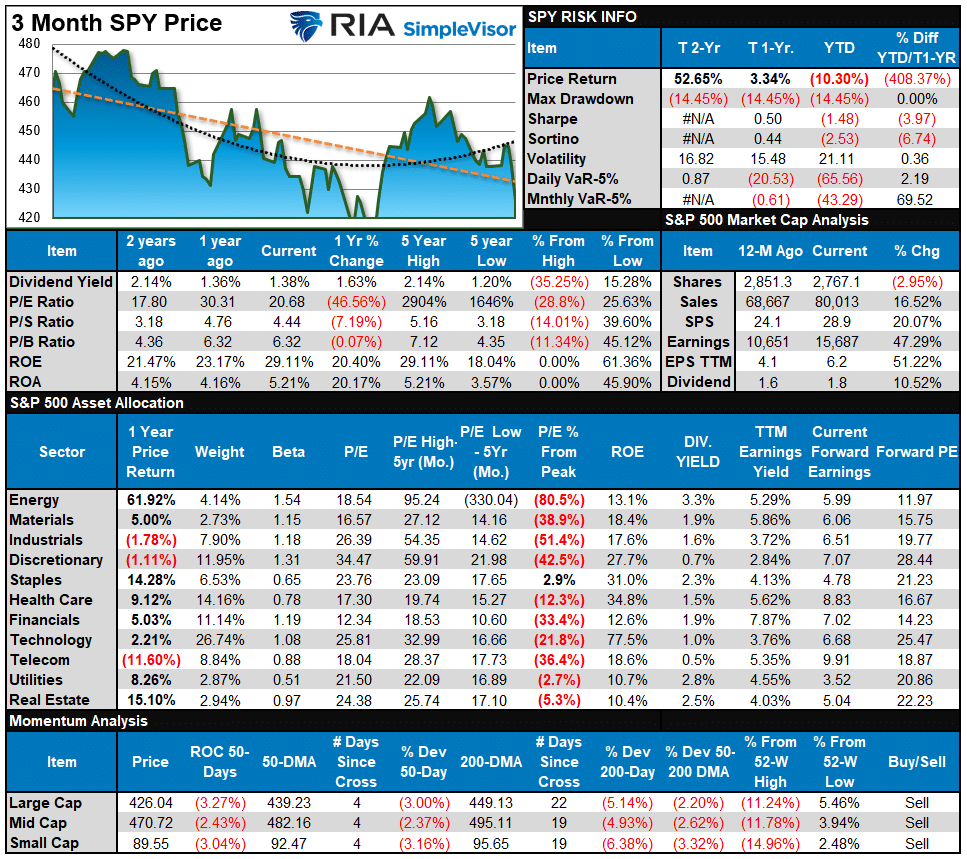

S&P 500 Tear Sheet

Relative Performance Analysis

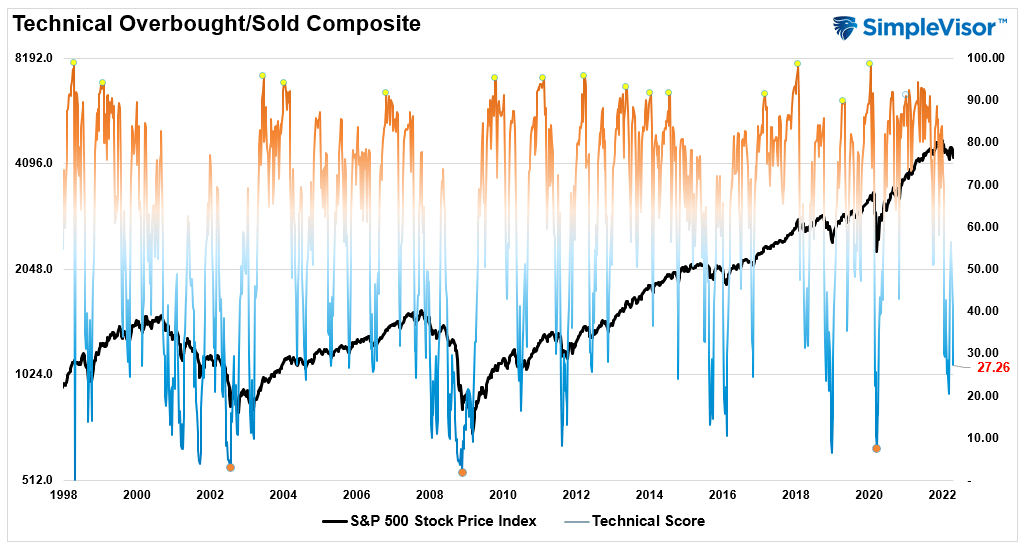

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 27.26 out of a possible 100.

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 51.0 out of a possible 100.

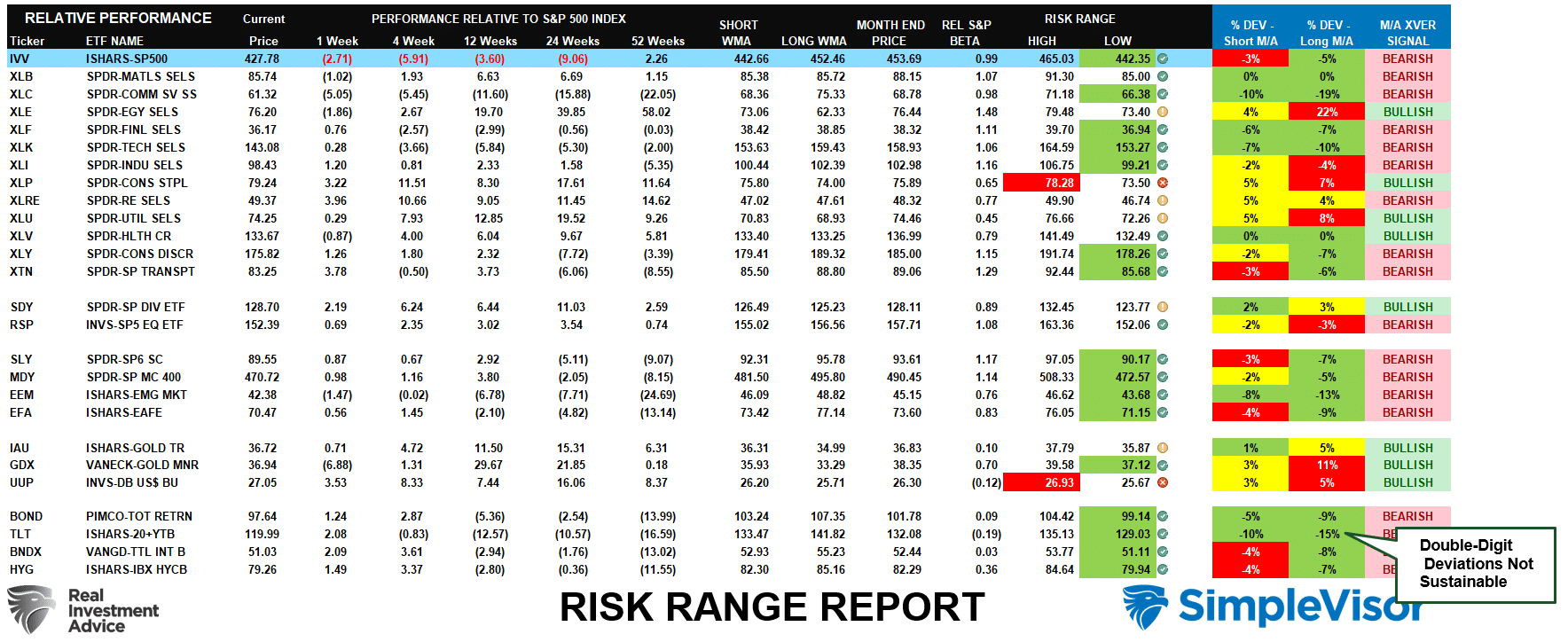

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M/A XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is under the Dashboard/Sentiment tab at SimpleVisor.

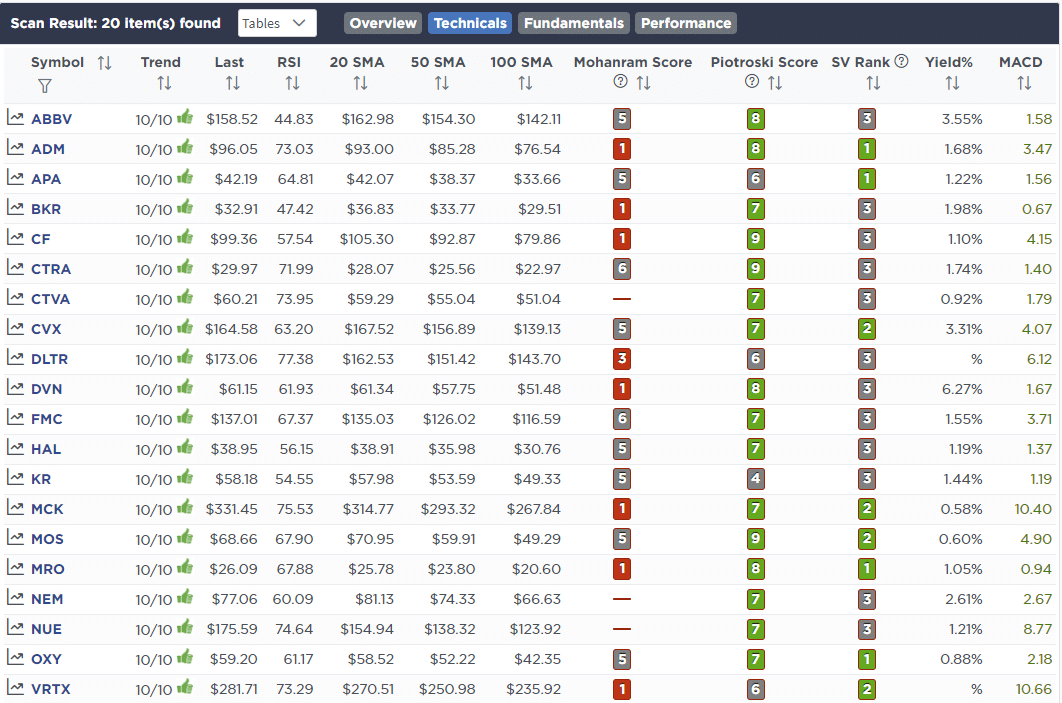

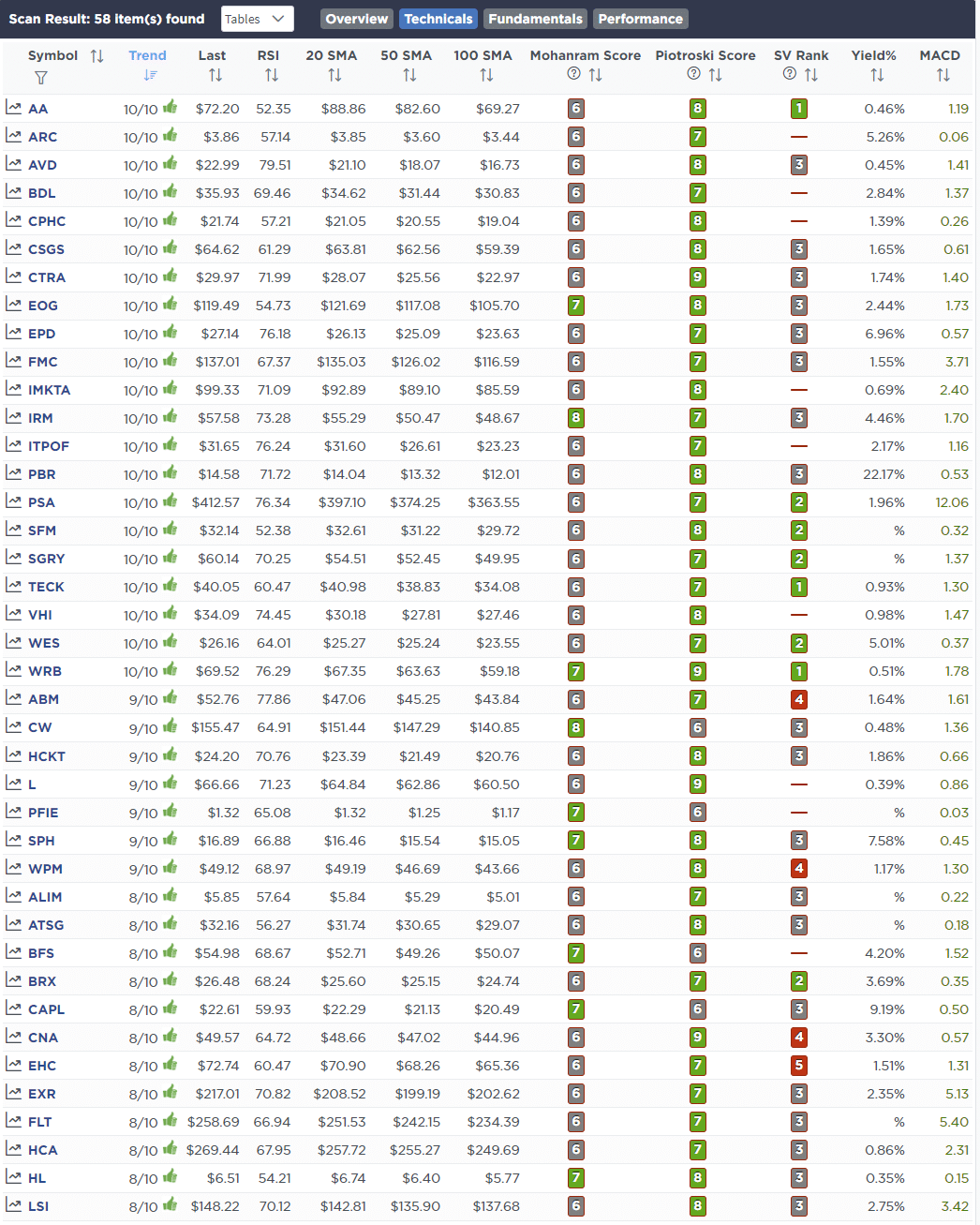

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

April 21st

“As we head into earnings season, we are rebalancing equity risk in the portfolio models. While we like the growth-oriented side of our portfolio allocation heading into a slower economic environment, we realize there may be an earnings-related risk to those companies short term. Importantly, the markets have not been kind to short-falls as witnessed by the recent clubbing of NFLX.

As such we are reducing our specific earnings risk exposure in AAPL, AMD, and NVDA and replacing that reduction with a holding in the S&P 500 ETF (SPY). This keeps our equity weighting roughly the same but reduces some of the potential risks of a specific earnings miss. If that event does NOT occur, we will simply add back to those holdings.

We are also just reducing our holding in PSA (Public Storage) back to the target weight and taking profits.

In the ETF model we are reducing Technology (XLK) and Real Estate (XLRE) for the same related risks. We are also rebalancing Staples (XLP) and Utilities (XLU) back to model weights to take profits.”

Equity Model

- Sell 1% of NVDA and AMD

- Reduce AAPL by 1%

- Reduce PSA to 2% of the portfolio

- Initiate a 3% position of SPY

ETF Model

- Reduce XLRE by 1/2% of the portfolio.

- Sell 1% of the portfolio weight in XLK

- Reduce XLP to 5% of the portfolio weight.

- Reduce XLU to 4% of the portfolio weight.

Lance Roberts, CIO

Have a great week!