In this 02-18-22 issue of “Buy Bonds? Yes, And You Should Too.”

- Market Turbulence From “Russia With Love.”

- Why We Are Buying Bonds & You Should Too

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Weekly Market Wrap With Adam Taggart

From Russia With Love

“When is the selling going to stop?”

That was the most common question I received this past week. However, it is an interesting one given that people never ask, “when is the BUYING going to stop?”

The importance of the question drives to the emotional biases that drive our portfolio management decision processes. Last year, investors could do no wrong. Whatever investment you made seemed to work. So far, 2022 remains a “year of nothing working.”

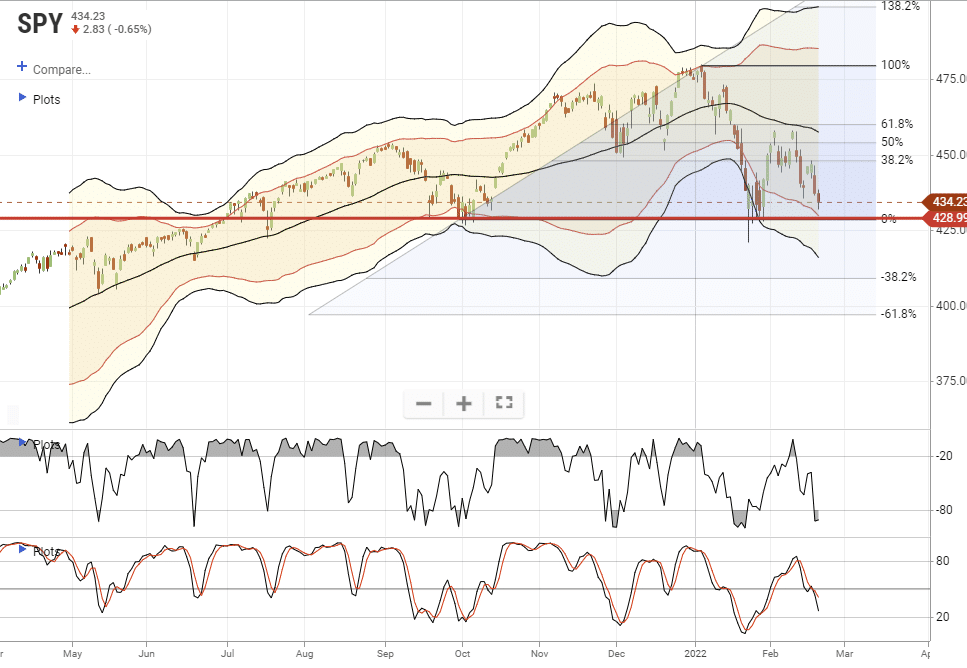

This week was another nauseating week of heightened Russian/Ukrainian headlines that sent stocks tumbling backward. As I discussed Friday morning:

“IF this market is going to maintain its bullish bias, it must hold those January lows otherwise we are looking at a potentially deeper correction. The good news, if you want to call it that, is the market has now reversed its previous overbought condition.”

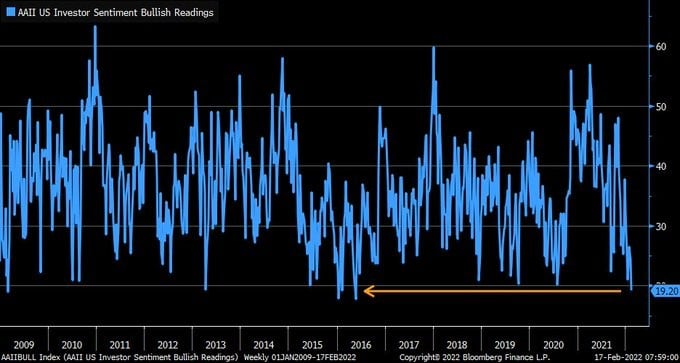

Importantly, investors are extremely bearish. The AAII sentiment index is now at the lowest levels since 2016, following a nearly 20% decline over concerns of Brexit. That was the low point for the year.

While this year is very different, the point is that with the market oversold and sentiment very bearish, we are likely to see a reflexive bounce to rebalance risks into.

As noted previously, the tailwinds pushing markets higher in 2021 and now headwinds into 2022. Liquidity is reversing, economic and earnings growth will slow, and the Fed will tighten monetary policy. Historically, these events have not been kind to market bulls.

However, there is just one question every bullish investor has.

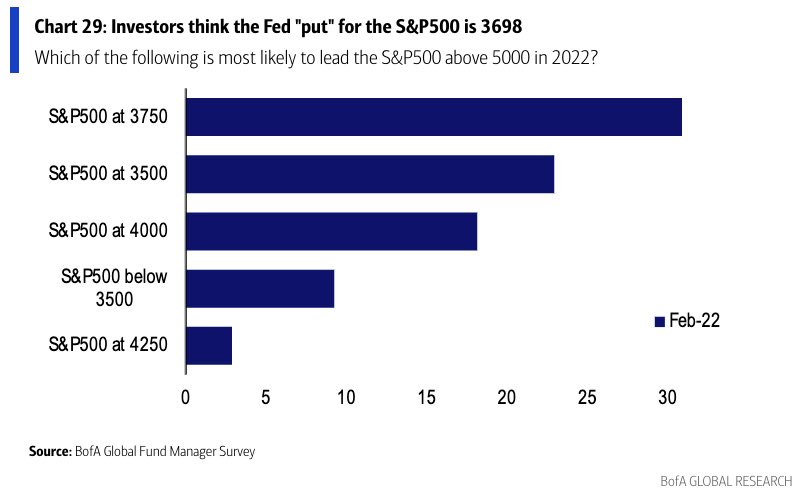

“Where is the Fed put.”

The Fed Put

The “Fed put” is the level where the Federal Reserve will take action to begin supporting asset markets by reversing rate hikes and restarting quantitative easing (QE) programs. Recently, a BofA fund managers survey pegged 3750 as the level they thought the “Fed put” resides.

While the BofA fund managers may be correct, my targets are slightly different as they are a function of Fibonacci retracement levels from the March 2020 closing lows. From the peak close of the market, the targets are:

- 38.2% rally retracement = 3829 = 20% market decline (Fed likely worried)

- 50% rally retracement = 3523 = 27% market decline (Margin calls triggered. Fed likely acts.)

- 61.8% rally retracement = 3217 = 33% market decline (Fed put triggered)

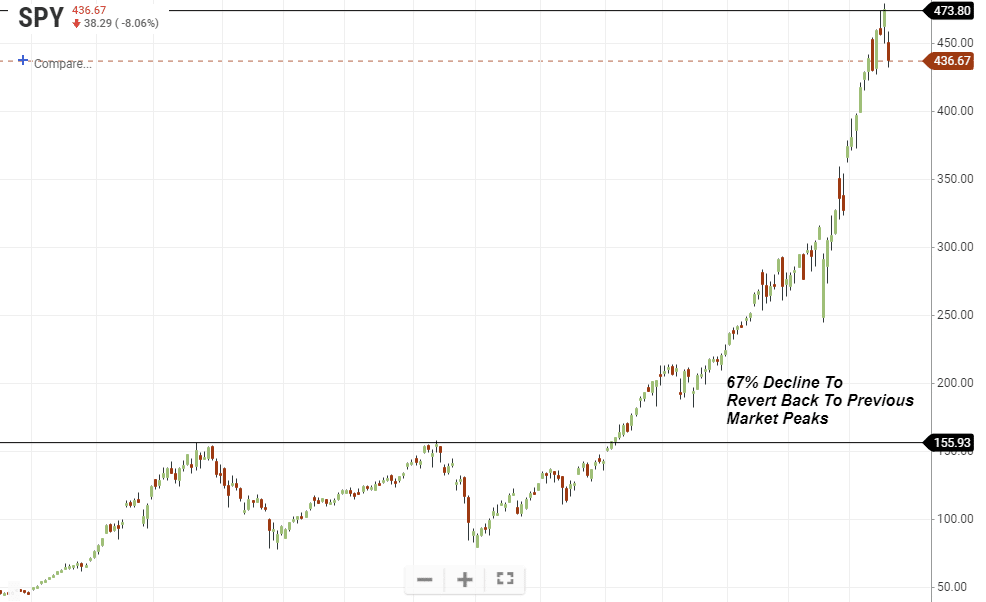

Interestingly, a 33% market decline, while likely causing the Fed to reverse monetary tightening rapidly, only erases the market gains from early 2020. An absolute “reversion to the mean” event would probably take the market back to the previous market peaks of 2000 and 2007. For obvious reasons, the Fed will avoid that at all costs. (This shows just how extensive the Fed-fueled bull run has become.)

Regardless of where you think the Fed put is, one asset class benefits from a “risk-off” move in the markets.

Such is why we are buying bonds.

This Week’s MacroView

Why We Are Buying Bonds & You Should Too

I received many emails and questions on “why” we are adding bonds to our portfolio. It certainly seems “crazy” when inflation is hot, and the Fed talks about increasing rates. I certainly understand the consternation. However, sometimes the obvious may not be so obvious.

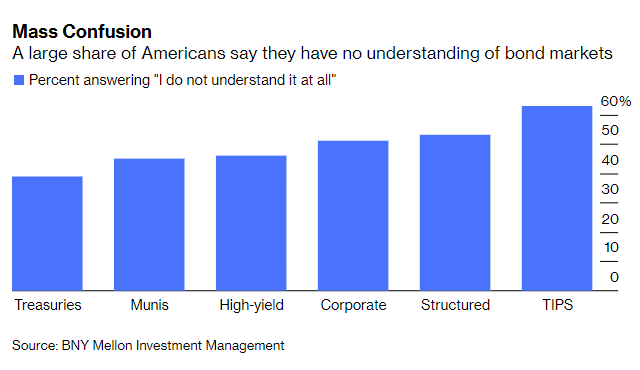

Notably, few people have a fundamental understanding of the bond market, as shown by a previous survey from BNY Mellon.

“A BNY Mellon Investment Management national survey on fixed-income investing was stunning: A measly 8% of Americans were able to accurately define fixed-income investments.“

Such is not surprising since the financial media focuses only on the “sexier” side of the business – equities.

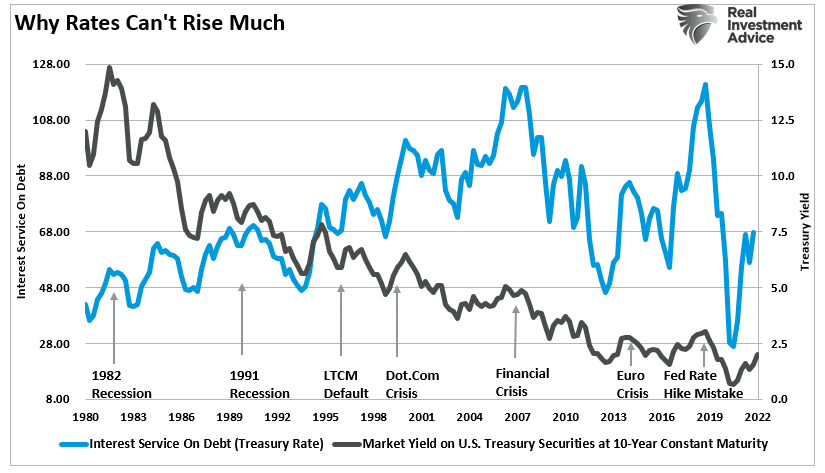

However, bonds are necessary from the investment perspective and the economic view. As we have discussed previously, low-interest rates are a function of an overly indebted economy. If rates rise too much, bad things have historically happened.

“The chart below is the interest service ratio on total consumer debt. (The graph is exceptionally optimistic as it assumes all consumer debt benchmarks to the 10-year treasury rate.) While the media proclaims consumers are in great shape because interest service is low, it only takes small increases in rates to trigger a ‘recession’ or ‘crisis’ event.”

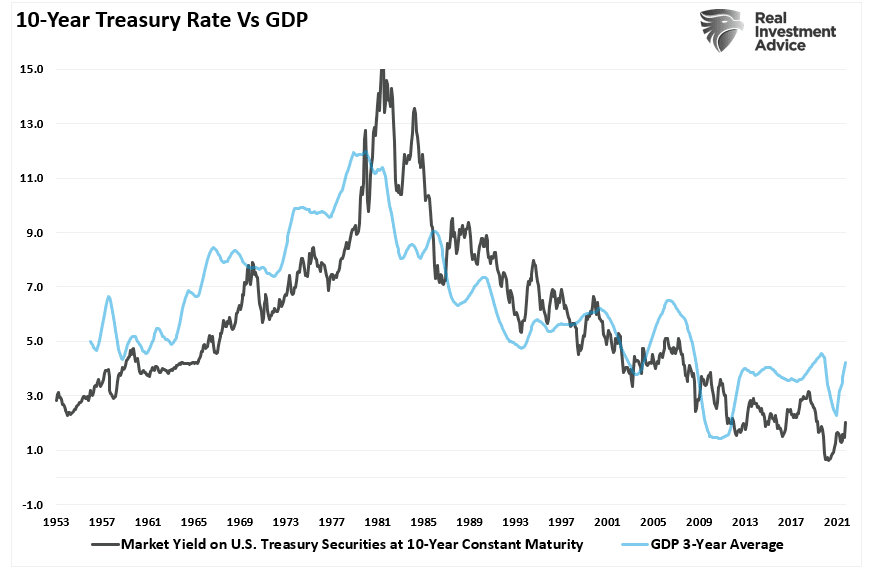

Of course, as noted, interest rates reflect economic growth. As economic growth slows this year and disinflationary pressures present themselves, rates will track economic growth lower.

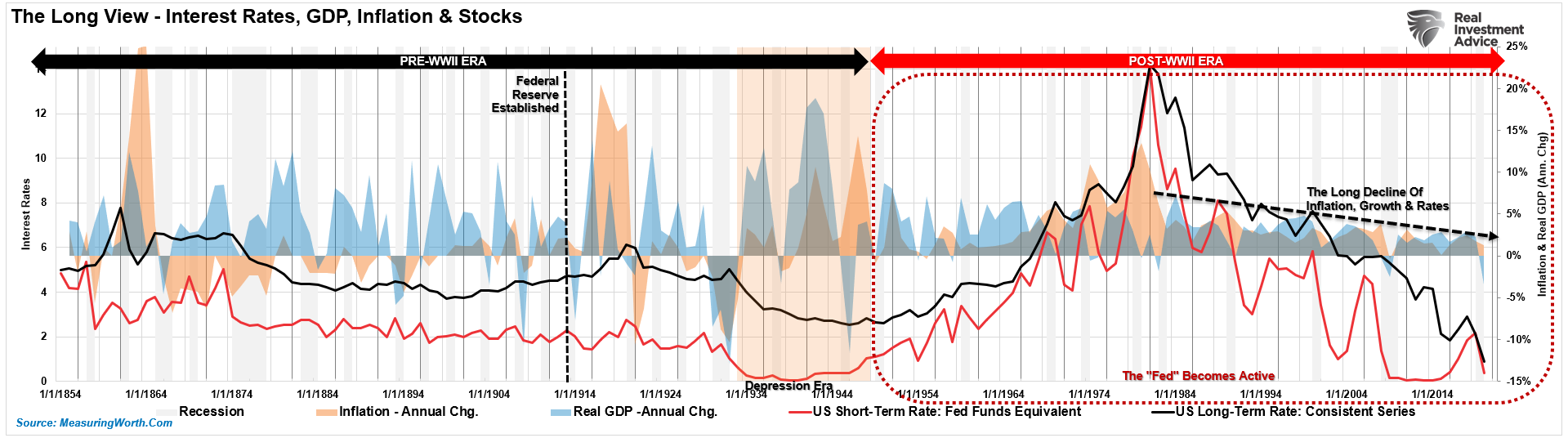

A Long History Of Rates & Economic Growth

The chart below shows a VERY long view of interest rates in the U.S. since 1854.

Interest rates are a function of the general trend of economic growth and inflation. More robust growth and inflation rates allow for higher borrowing costs to be charged within the economy. Such is why bonds can’t be overvalued. To wit:

“Unlike stocks, bonds have a finite value. At maturity, the principal gets returned to the lender along with the final interest payment. Therefore, bond buyers know the price they pay today for the return they will get tomorrow. As opposed to an equity buyer taking on investment risk, a bond buyer is loaning money to another entity for a specific period. Therefore, the interest rate takes into account several risks:”

- Default risk

- Rate risk

- Inflation risk

- Opportunity risk

- Economic growth risk

“Since the future return of any bond, on the date of purchase, is calculable to the 1/100th of a cent, a bond buyer will not pay a price that yields a negative return in the future. (This assumes a holding period until maturity. One might purchase a negative yield on a trading basis if expectations are benchmark rates will decline further.) “

Currently, the inflation surge suggests yields should rise. However, that inflation push was artificial from massive monetary interventions. As monetary inputs fade, disinflation will push yields lower.

Disinflation from the contraction of liquidity will coincide with slower economic growth.

Morgan Stanley and Goldman Sachs suggest a faster economic slowdown than previously expected. Both Wall Street and the Fed will scramble to reassess the central bank’s tightening intentions, especially if the US faces a recession in the second half of 2022. – Zerohedge

Throw on top of that massive geopolitical risk, and the “demand for safety” is evident.

Buy Bonds For Capital Appreciation & Protection

Most people view bonds as an income-only investment. With yields low, why own bonds? However, there is another aspect to bonds; capital appreciation.

In our portfolio management process, we buy bonds for three reasons:

- Capital appreciation – the same reason we buy equities

- Total return – interest income plus capital appreciation

- Risk reduction – lower volatility asset to offset higher volatility assets (equities.)

If you start thinking about bonds as an “equity,” the analysis changes from an income strategy to a capital appreciation opportunity.

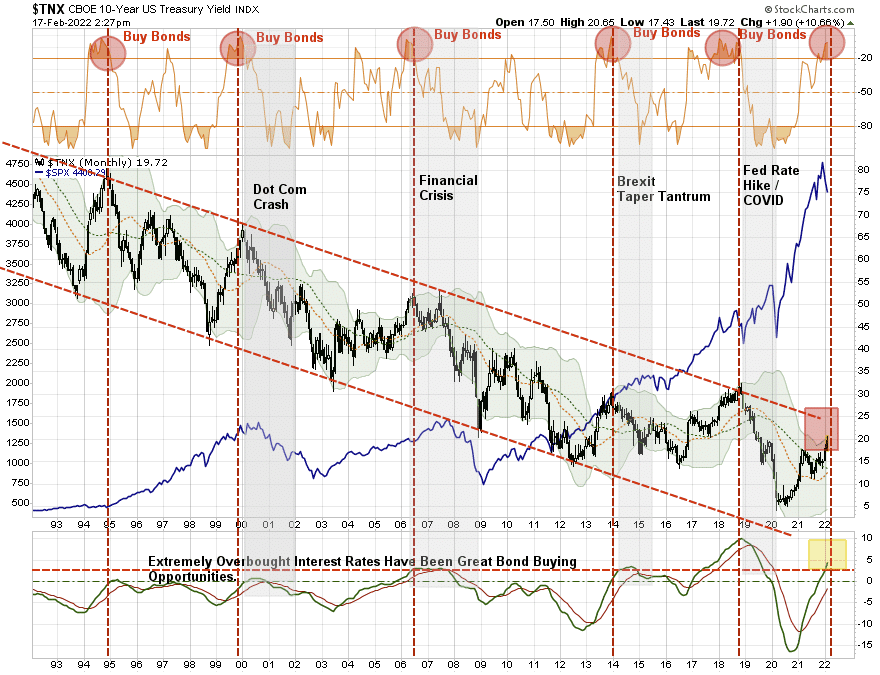

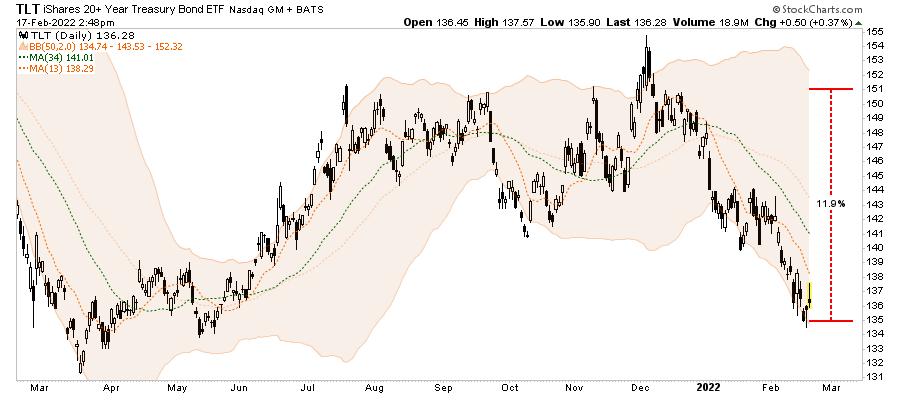

Currently, using a monthly chart, treasury bonds are at a very critical oversold juncture. Historically, when bonds were this oversold such coincided with a financial event or recession. Such is not surprising given, as noted above, the impact of higher rates on a highly leveraged economy.

Since interest rates are the inverse of bond prices, we can look at this long-term chart of rates to determine when bonds are overbought or oversold.

- In 2018, rates slid lower as the realization that Fed rate hikes would negatively impact economic growth and financial stability.

- As 2019 progressed, the yield curve inverted pushing rates lower as investors sought safety.

- In March of 2020, as the pandemic raged, the demand for safety caused rates to plunge to record lows.

Historically, bonds are the beneficiary of a “risk-off” rotation during market downturns. Such not only provides a return but reduces overall portfolio volatility.

With the Fed now set to hike rates and reduce their balance sheet to slow economic growth, not to mention geopolitical risk with Russia, the demand for safety will return. If GS and Morgan Stanley are correct, we suspect yields will fall toward previous lows by the end of 2022, suggesting an 11% return on bonds.

Bonds could outperform stocks this year.

Portfolio Update

There are undoubtedly many issues confronting even the most optimistic of investors currently.

- Geopolitical risk from Russia and the threat to the Ukraine

- Rising interest rates

- Surging inflationary pressures

- Economic growth slowing

- Profit margins under pressure

- Reversal of monetary liqudity

- Tighter monetary policy from the Federal Reserve

- Surging oil prices

The many tailwinds that supported the rapid rise in the markets from 2020 have reversed. As shown, the roughly 120% advance from the March lows was a function of the liquidity surge from the Government.

Now, the tenor of the market is changing.

We reduced equity risk on the previous rally from an investment perspective and added to our portfolio hedges. On the next oversold, counter-trend bounce, we will repeat that process.

The market remains in a very vulnerable position. Again, we can’t say with any confidence whether the next leg of the market is up or down. However, the weight of evidence is starting to suggest the latter.

As such, we have three options currently:

- Do Nothing – if the markets correct, we reduce capital and time waiting for the portfolio to recover.

- Take Profits – This was our choice on the recent reflexive rally. Taking profits, raising cash, and reducing equity exposure mitigates the damage of a decline. However, if wrong, we can repurchase positions, add new ones, or resize portfolio holdings as needed.

- Hedge – We also opted to hedge by adding a position to the portfolio that is the “inverse” of the market.

While we are reducing capital risk opportunistically, we are aware we could give up performance in the short term if the market rallies. For us, that choice we can live with if we bypass the risk of a more significant correction.

Market & Sector Analysis

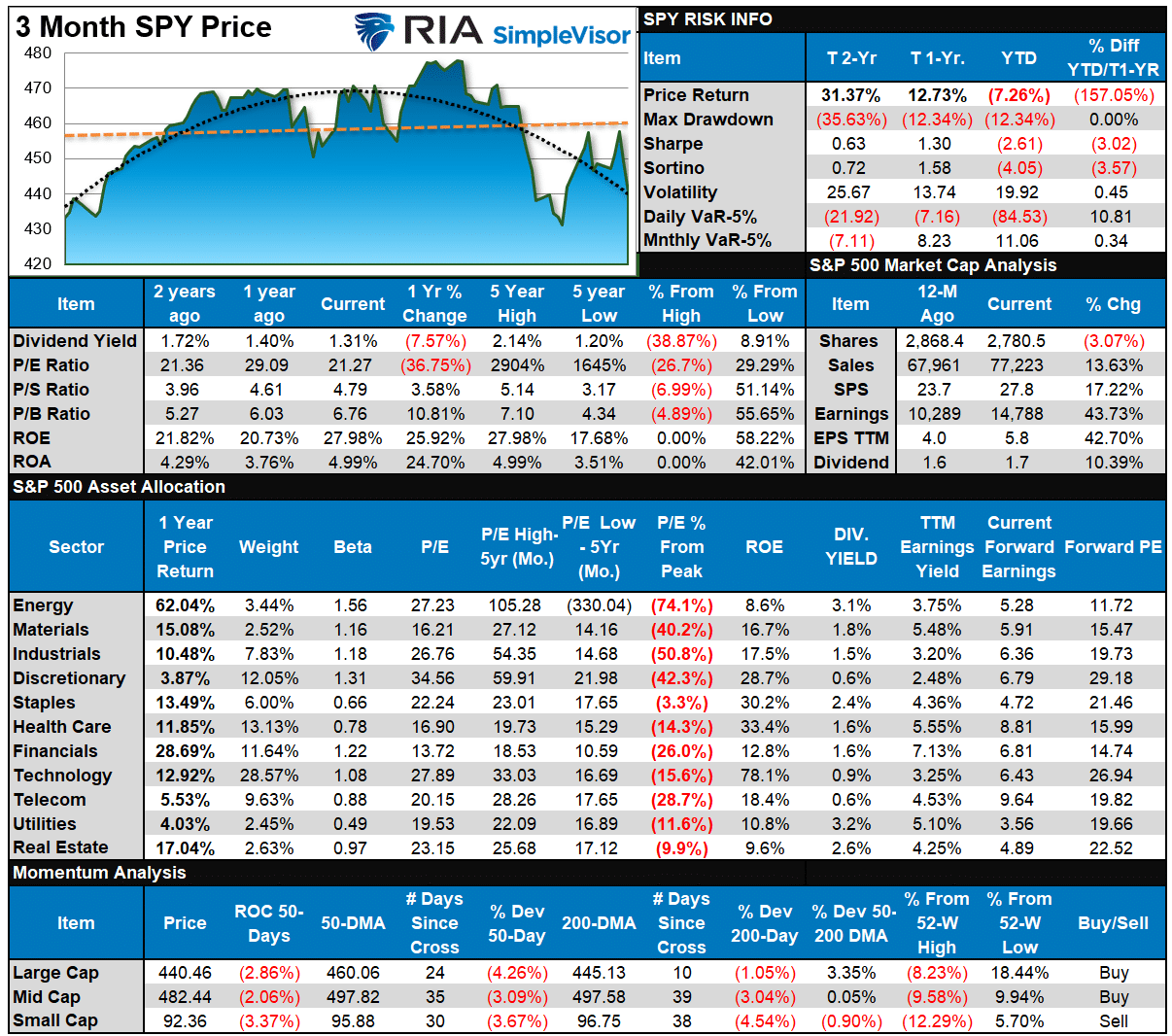

S&P 500 Tear Sheet

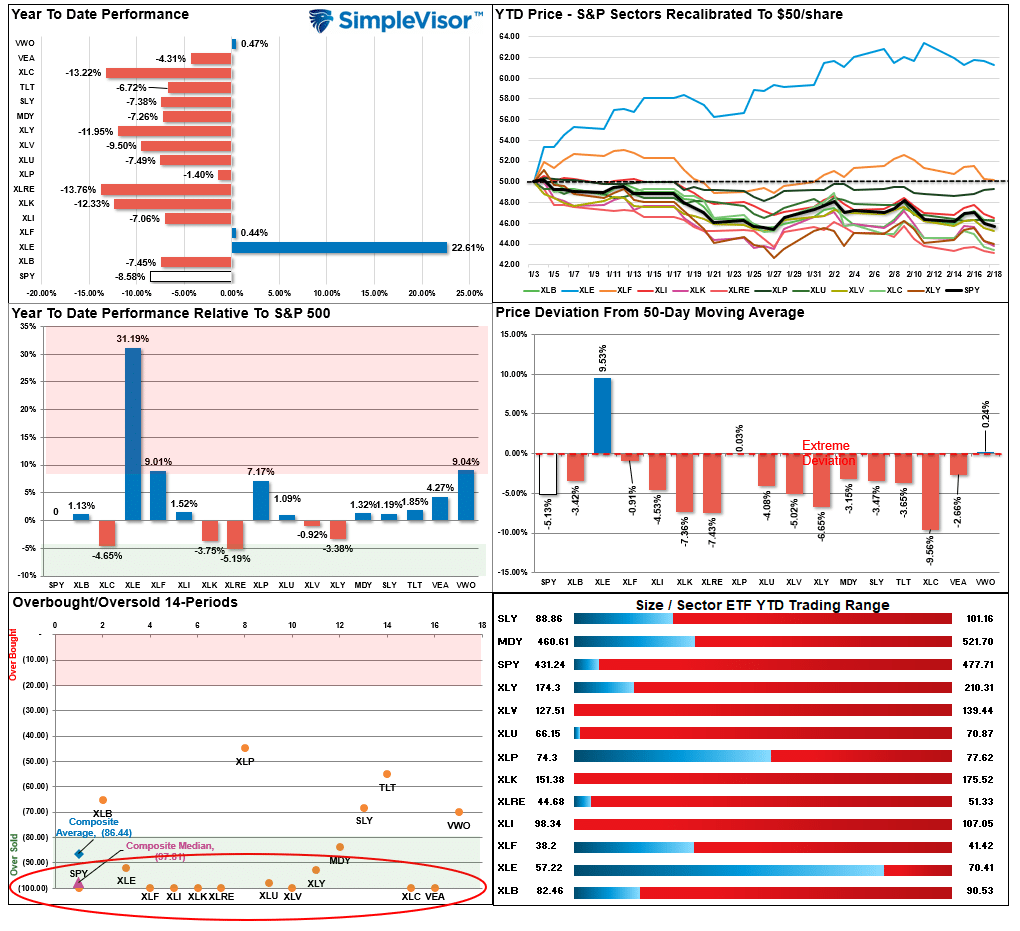

Relative Performance Analysis

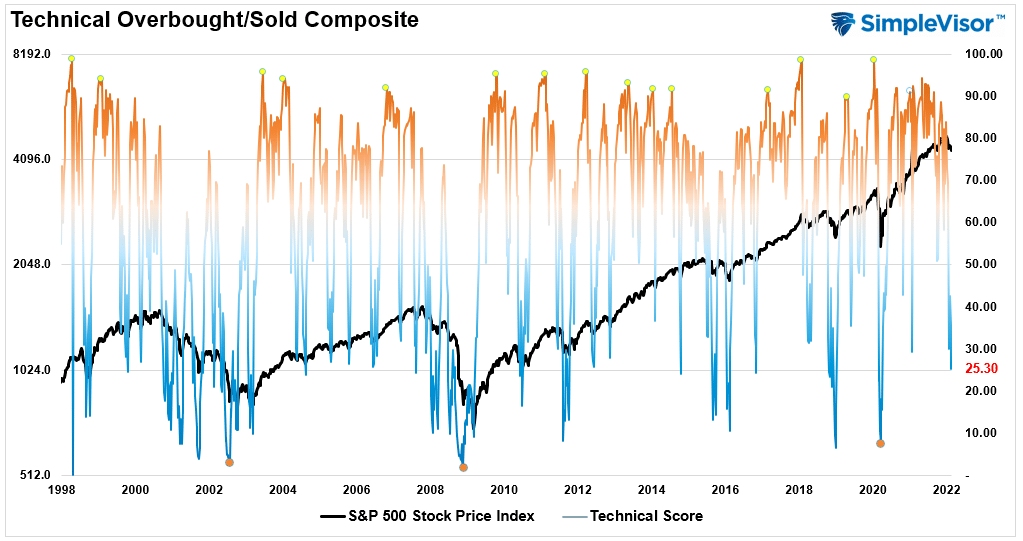

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 25.30 out of a possible 100.

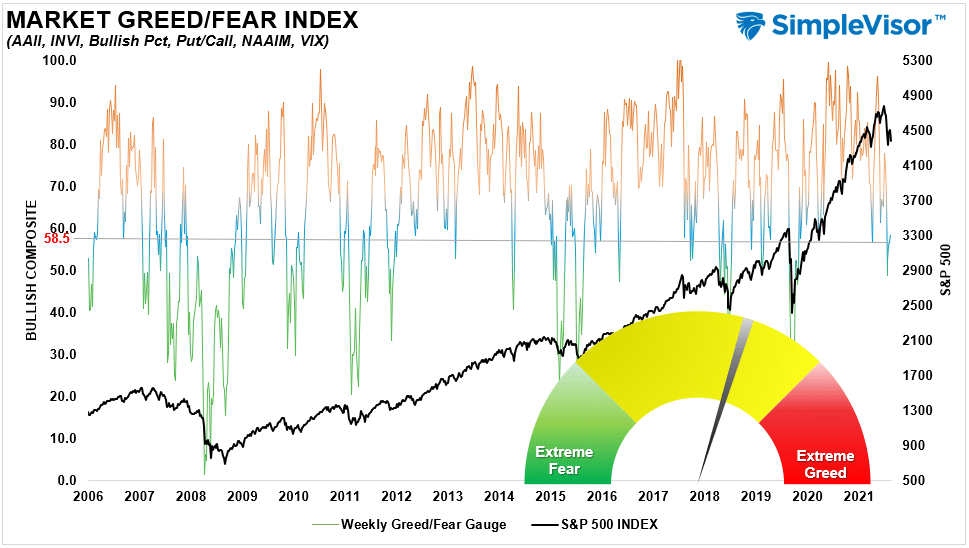

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 58.5 out of a possible 100.

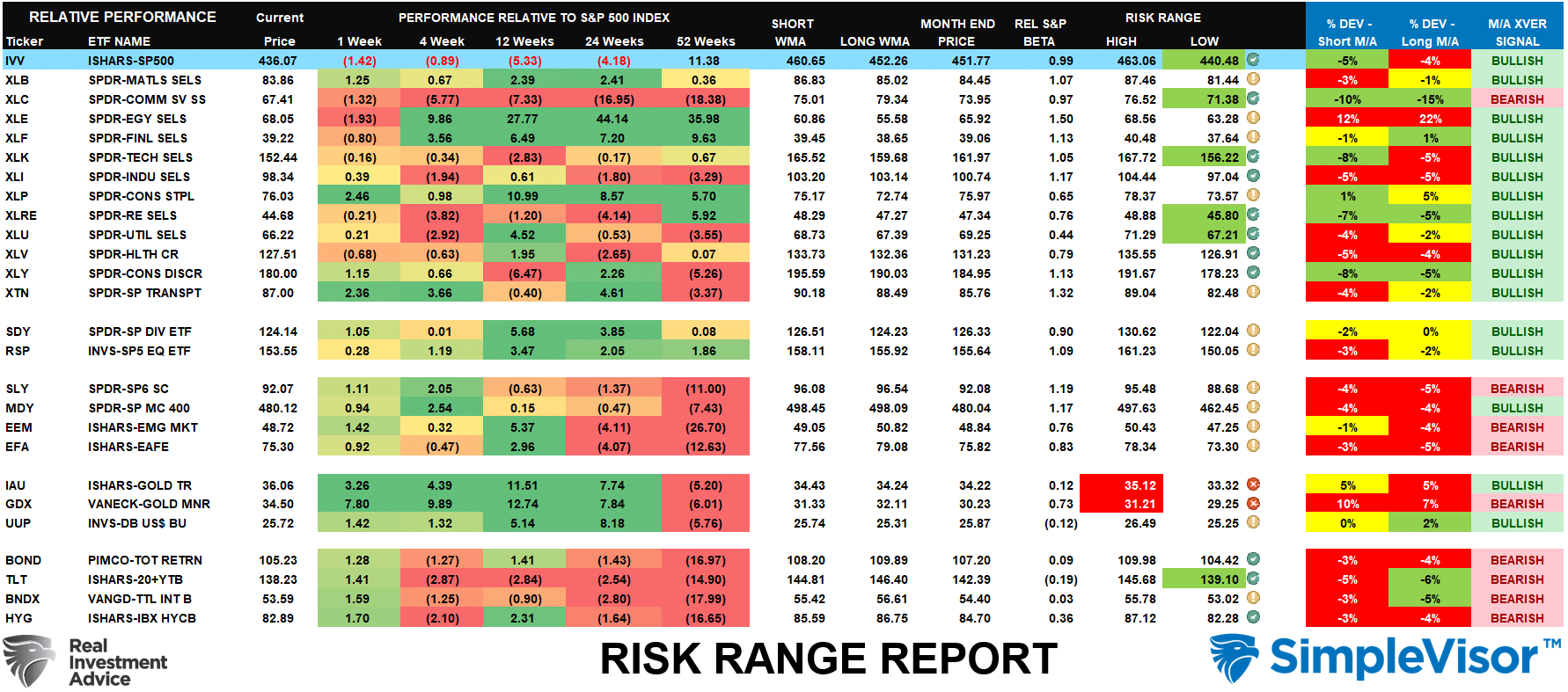

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is on under the Dashboard/Sentiment tab at SimpleVisor

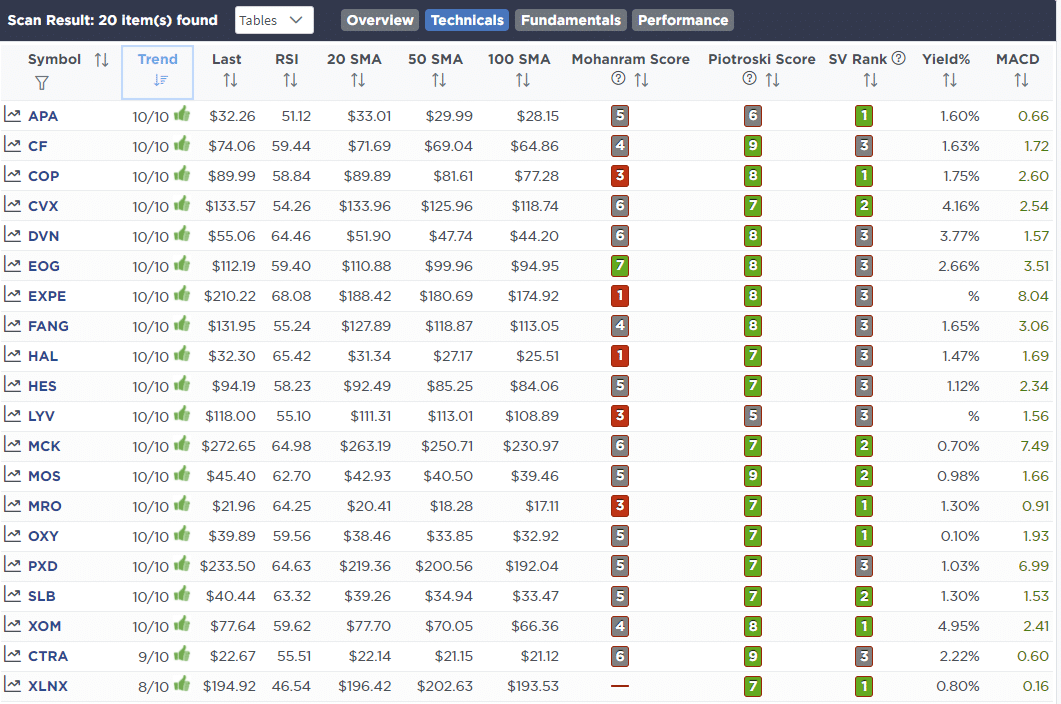

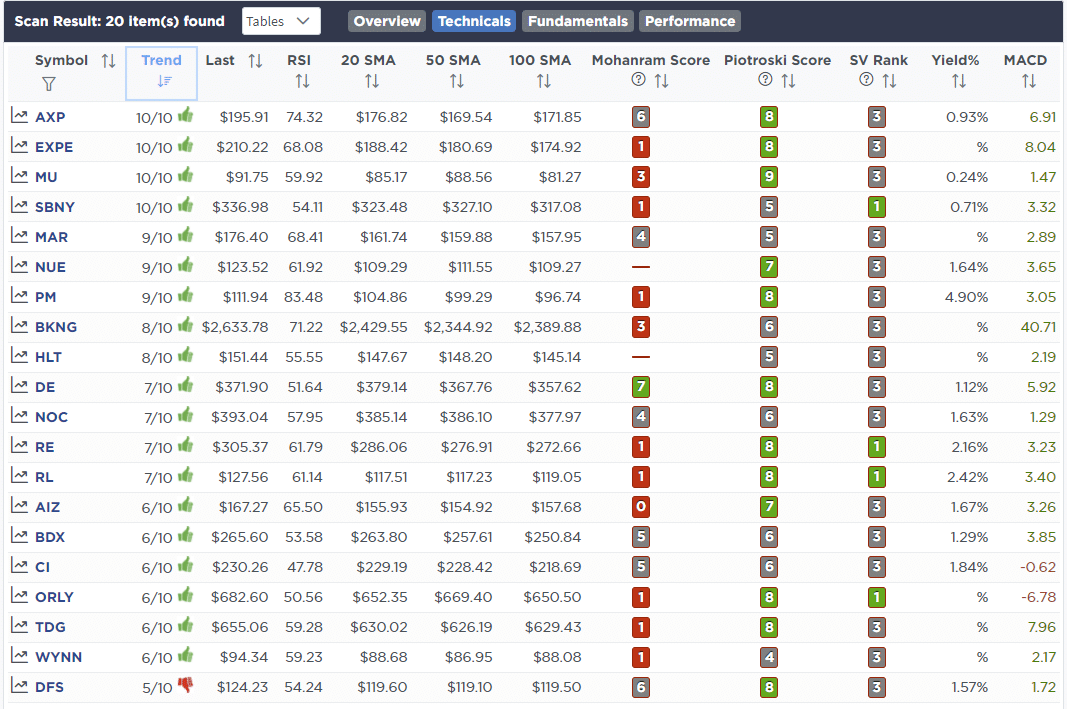

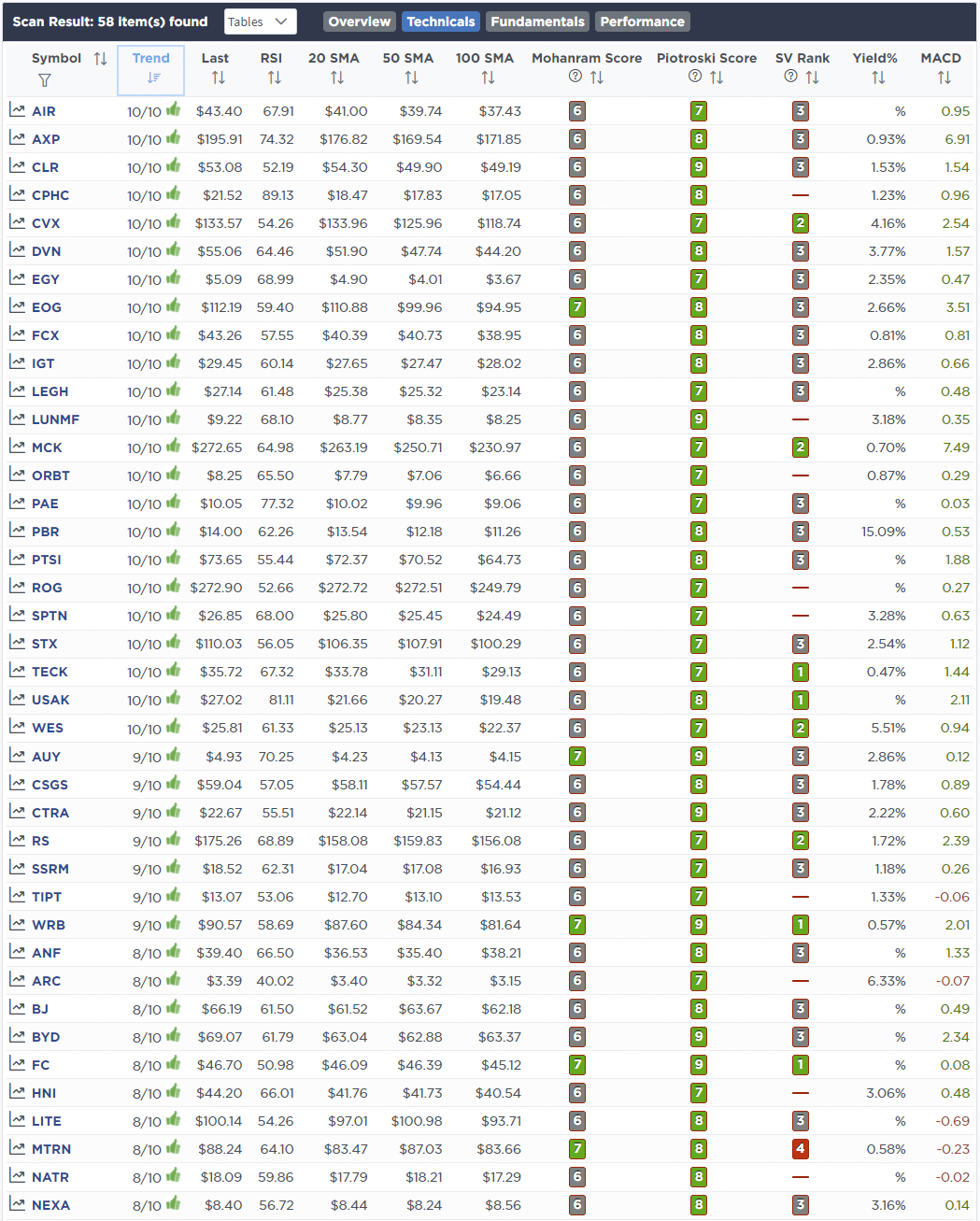

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

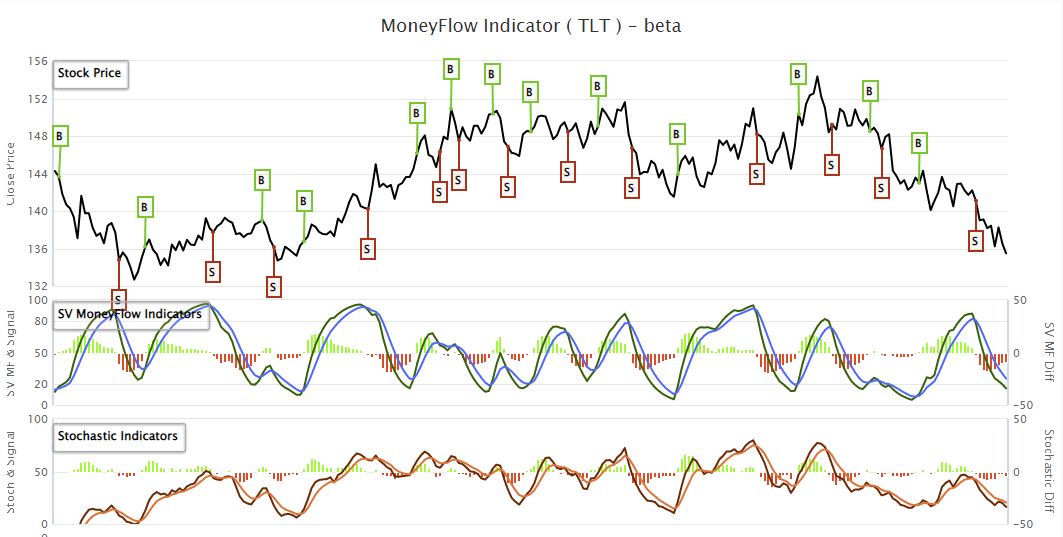

February 15th

We added 1% TLT to both models on the bond sell-off this morning. TLT has been bouncing around with the ebbs and flows of the possible Russian invasion. Behind the scenes, the important driver that we think will push yields lower is weakening economic activity and a likely stabilization in inflation in the coming months. TLT should flip to a buy signal in the coming days from a deeply oversold level.

- Add 1% of portfolio value to TLT. Total portfolio weight is now 10%.

Lance Roberts, CIO

Have a great week!