Inside This Week’s Bull Bear Report

- P/E Ratios Rising Along With Interest Rates

- How We Are Trading It

- Research Report – Bond Vigilantes And Waiting For Godot

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Update & Review

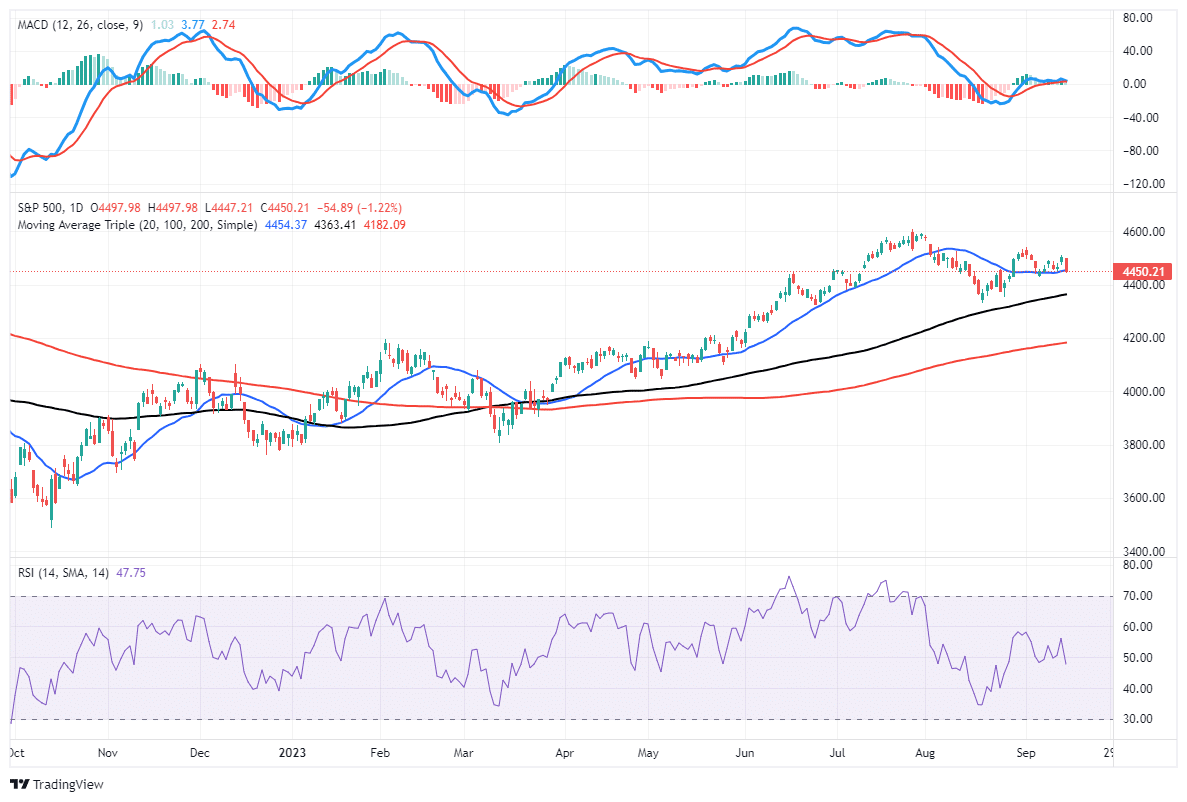

Since the beginning of the year, P/E ratios have risen along with interest rates. Such should be a concern for investors going forward. However, before we delve into that topic, let’s review the market action from this past week.

As we noted last week,

“The more extreme overbought condition is about halfway through a corrective cycle, suggesting we could see further “sloppy” trading next week. With the market holding within a consolidation range, a breakout to the upside should confirm the start of the seasonal strong trading period into year-end.”

Such remained the case this past week. Friday was particularly choppy as one of the most significant options expiration days on record. With nearly $3.2 Trillion in options expiring, stocks traded negatively for the day.

Unsurprisingly, given the recent performance of the mega-cap stocks, which has recently attracted most of the liquidity flows, the selling pressure was primarily contained within those names, with value stocks outperforming for the day. However, the market held support at the 50-DMA on Friday, with the overall price conditions remaining neutral. Like a groundhog that sees its shadow, the MACD signal is close to registering a “sell signal.” If the signal triggers, it could signal a couple of additional weeks of sloppy trading action heading into October. Such would be consistent with seasonal weakness before heading into the last trading quarter of the year.

For now, there is no change to the bullish backdrop of the market, and nothing suggests a need to become more cautious in the near term. It is always possible that analysis could change over the next couple of weeks, and if it does, we will suggest reducing equity exposure and becoming more cautious.

With that said, let’s take a look at valuations.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

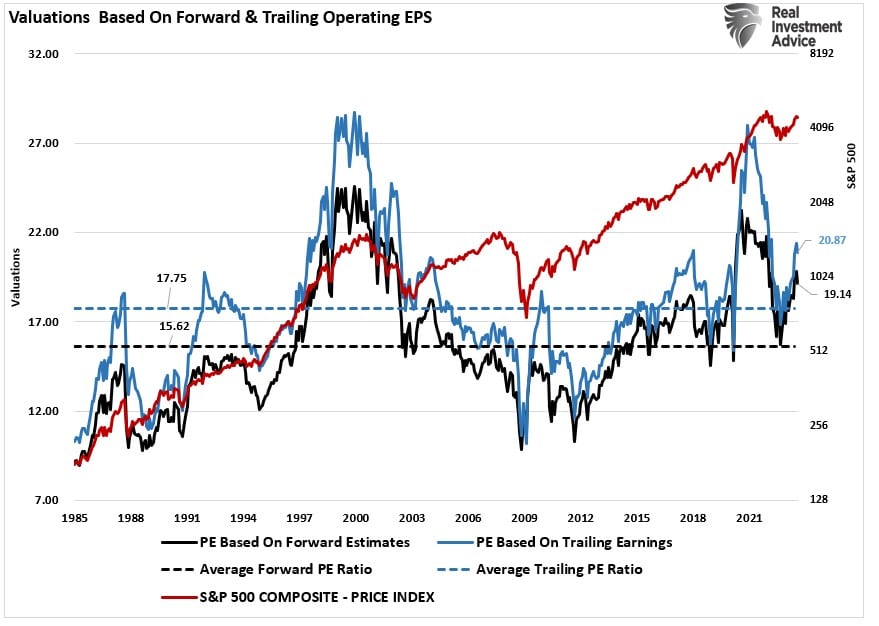

P/E Ratios Are Rising

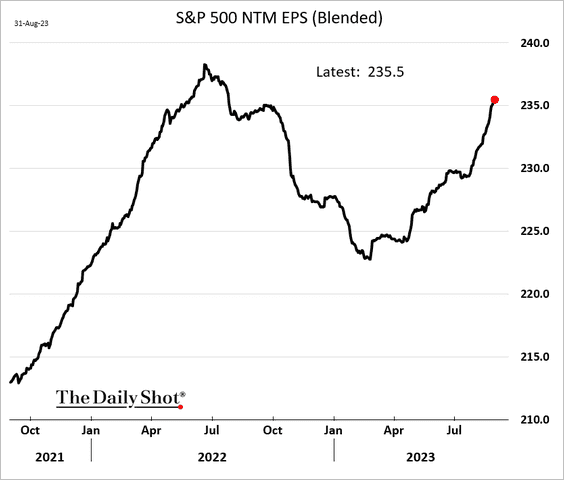

As we noted last week in “Beware Of Market Gurus,” analysts are rapidly raising expectations for both earnings and, by extension, economic growth.

“Despite increasing signs of recessionary risk, analysts are once again becoming increasingly optimistic about earnings growth into 2024. Of course, such would require substantially stronger economic growth to generate those earnings.”

Unsurprisingly, market participants follow those earnings estimate increases by buying companies today, expecting future earnings growth to justify current valuations. As shown, earnings tend to track the ebb and flow of the market over time for that reason.

While earnings are starting to tick up in anticipation of more robust economic growth in 2024, market participants begin bidding up stocks even before earnings have troughed. Since stock prices rose strongly in 2023, such has led to a rather sharp surge in P/E ratios, which are well ahead of estimated earnings.

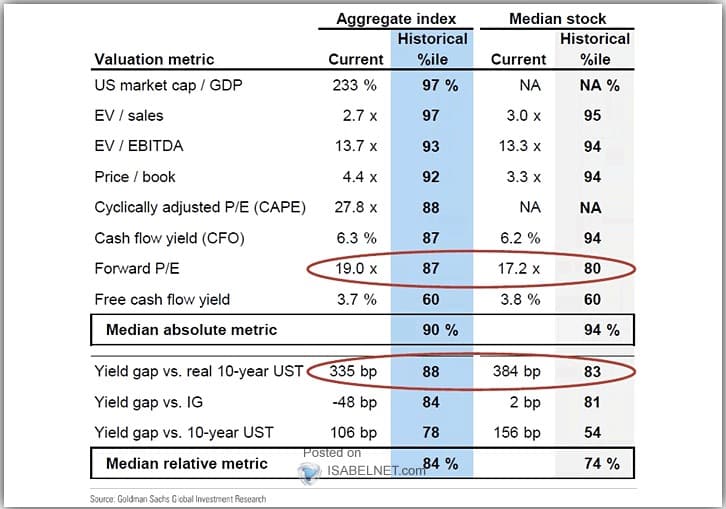

As Goldman Sachs noted recently, valuations across various metrics suggest the market remains overvalued. With the median absolute metric still in the historical 94th percentile, such follows a nearly 20% decline in stocks last year. The most optimistic valuation measure of forward P/E ratios remains in the 80th percentile.

The problem, as discussed many times previously, is that P/E ratios have nothing to do with stock market returns over the next few months or even next year. To wit:

“Valuations are a function of three components:”

- Price of the index

- Earnings of the index

- Psychology

“The price-to-earnings ratio, or the P/E ratio, is the most common visual representation of valuations. However, we tend to forget that ‘psychology’ drives investors to overpay for those future earnings.”

In other words, in the short term, the market reflects investor psychology. However, over the long term, investor returns reflect starting valuations.

Interest Rates Reduce Valuations (Eventually)

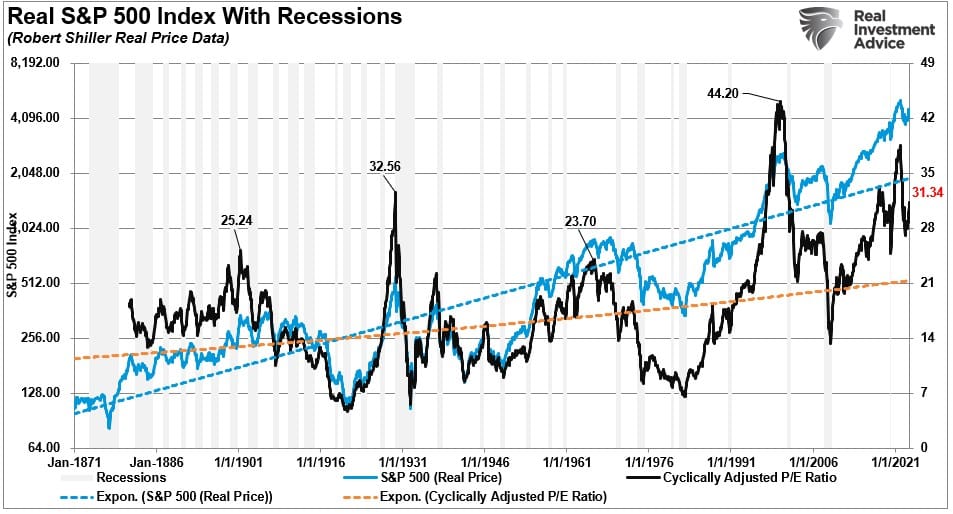

Another problem confronting more bullish investors over the next 12 months is the rise in interest rates. One of the emerging views is that the “bond bull market” of the last 40 years is dead, so equities will be the only place to be. As shown below, the last time the bond-bull market died, in the 60s and 70s, valuations collapsed along with asset prices.

Furthermore, since 1990, increases in interest rates have regularly aligned with reversals in P/E ratios, bear markets, recessions, or financial events.

Therefore, the logic should be pretty evident. If interest rates rise, so are the borrowing costs for corporations and consumers. Subsequently, higher interest costs reduce consumption and investment, which reduces earnings growth rates. Therefore, if the current rise in interest rates continues, valuations must revert to accommodate a slower economic and earnings growth pace. Given the extremely high debt and leverage ratios in the current economy, it should not take long before P/E ratios begin to reflect the impact of higher borrowing costs.

Such is particularly the case concerning monetary policy from the Federal Reserve. Throughout history, each time the Federal Reserve has engaged in a rate hiking campaign, valuations ultimately reverted. The reason for the reversion in valuations was that higher rates eventually created either a recession, a financial event, or both, leading to a bear market in stock prices.

It is currently believed that “this time is different” because the economic reversion has not occurred as of yet. However, as discussed recently, the “lag effect” of monetary policy is delayed due to the massive stimulus and support programs fostered during the pandemic-driven economic shutdown. However, as those programs expire and the support programs work through the economic system, the lag will eventually catch up, exposing economic realities.

Unfortunately, valuation extremes are always reversed by a repricing of financial assets lower to realign with the impact of higher rates on economic growth.

The Inverse Of The P/E Ratio Is A Warning

While valuations have remained elevated over the last several years due to the massive injections of liquidity from the Government and the Federal Reserve, combined with near-zero interest rates, the more bullish media turned to the “earnings yield” to justify overpaying for stocks. However, there are some important considerations with that justification.

The “earnings yield” is the inverse of the P/E ratio. While the P/E ratio is calculated by taking the price of the investment and dividing it by its earnings per share, the earnings yield is just the earnings divided by the price.

This argument’s basic premise is rooted in the “Fed Model,” as promoted by Alan Greenspan during his tenure as Federal Reserve Chairman. The Fed Model states that when the earnings yield on stocks is higher than the Treasury yield, you invest in stocks and vice-versa. In other words, disregard valuations and buy yield.

This is a very faulty analysis for the following reasons. When you own a U.S. Treasury, you receive the interest payment stream and the return of the principal investment at maturity. Conversely, with equity, you DO NOT receive an “earnings yield,” and there is no promise of repayment in the future.

For example, if I own a Treasury bond with a 1% coupon and a stock with a 2% earnings yield, if the price of both assets doesn’t move for one year – my net return on the bond is 1% while the net return on the stock is 0%.

Stocks are all risk, and U.S. Treasuries are considered a “risk-free” investment.

There is only a slight spread between equities and the risk-free rate. Such suggests there is little reason to take on significant “equity risk” levels relative to a risk-free investment.

However, a more appropriate comparison is between the yield on investment-grade bonds, which is currently higher than the earnings yield on stocks. Historically, rising bond rates, as noted with valuations above, suggest problems for investors soon. Previous periods where there was such a sharp spike in bond yields above the earnings yield were in 2000 and 2008.

Is “this time different,” maybe?

However, the continuing decline in the earnings yield is just another of the many warning signs discussed lately, suggesting there is still a viable risk to investors heading into next year.

The problem, as always, with all valuation-related analysis is that it can take much longer to impact the equity cycle than many think. Therefore, it is often dismissed under the guise of “it’s different this time.”

Unfortunately, it never is.

How We Are Trading It

We obviously remain concerned about the direction of the markets over the next 12-18 months due to the numerous risks posed on economic growth. Tighter financial conditions, higher borrowing costs, slowing wage growth, etc., certainly cloud the picture of where earnings will be.

However, as noted in last week’s blog on market predictions, it is a futile effort to try and predict that far into the future. Understanding that we must deal with the market we have, which is driven entirely by psychology, we continue to remain almost fully allocated to equity risk in the portfolios.

In case you missed last week’s newsletter, we did execute the “bond swap” we have discussed lately. This video clip with Michael Lebowitz and me explains the “why” behind the swap. As noted in that video, the reasons for swapping the majority of our portfolio allocations in Treasury Bond ETFs into a similar duration Treasury Bond were three-fold: 1) Provides a guaranteed, and slightly better, yield to the maturity, 2) maintains portfolio liquidity, and, 3) reduced the portfolio’s expenses overall.

We continue to look for opportunities in the portfolio to take advantage of market weakness near-term. Our ongoing premise remains a more substantial rally into year-end. Such should be supported by the portfolio manager’s performance chasing into reporting, roughly $5 billion a day in corporate share buybacks, and the realization by the market that the Fed is done hiking rates.

However, next year could be an entirely different story.

See you next week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

The bifurcation of the market remains clear. However, we have seen a bit of rotation, with Utilities performing well last week despite the higher interest rates. Bonds, Technology, Mid-Cap, and the broad market are oversold short-term. Therefore, expect a post-options expiration rally this week.

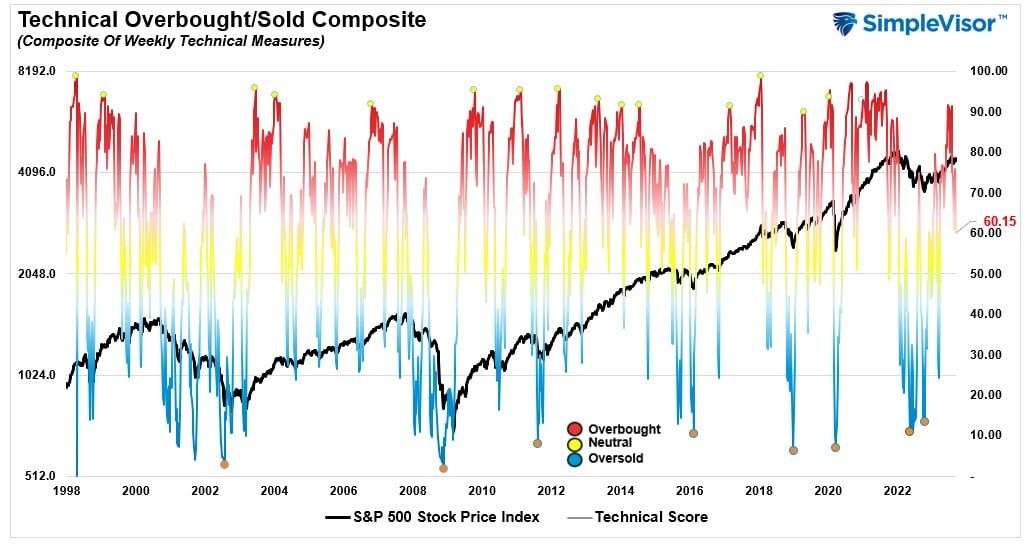

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 60.15 out of a possible 100.

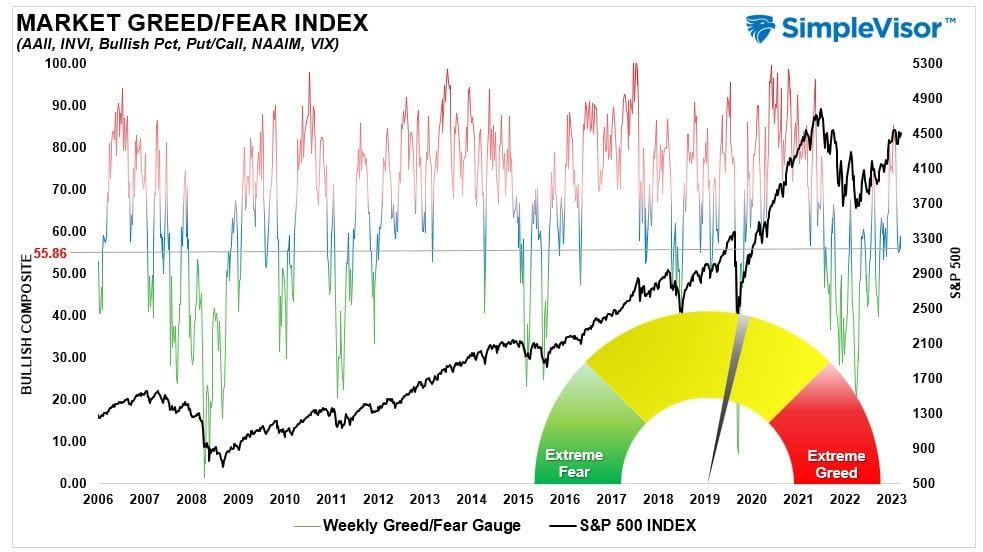

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 55.86 out of a possible 100.

Relative Sector Analysis

Most Oversold Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

Since last week’s report, despite Friday’s sell-off, the market remained bullish. However, Bonds and Technology are now very oversold to start the month, and Utilities are the most overbought. The move in Utilities is not surprising given the previous analysis on the relative sector analysis being very oversold.

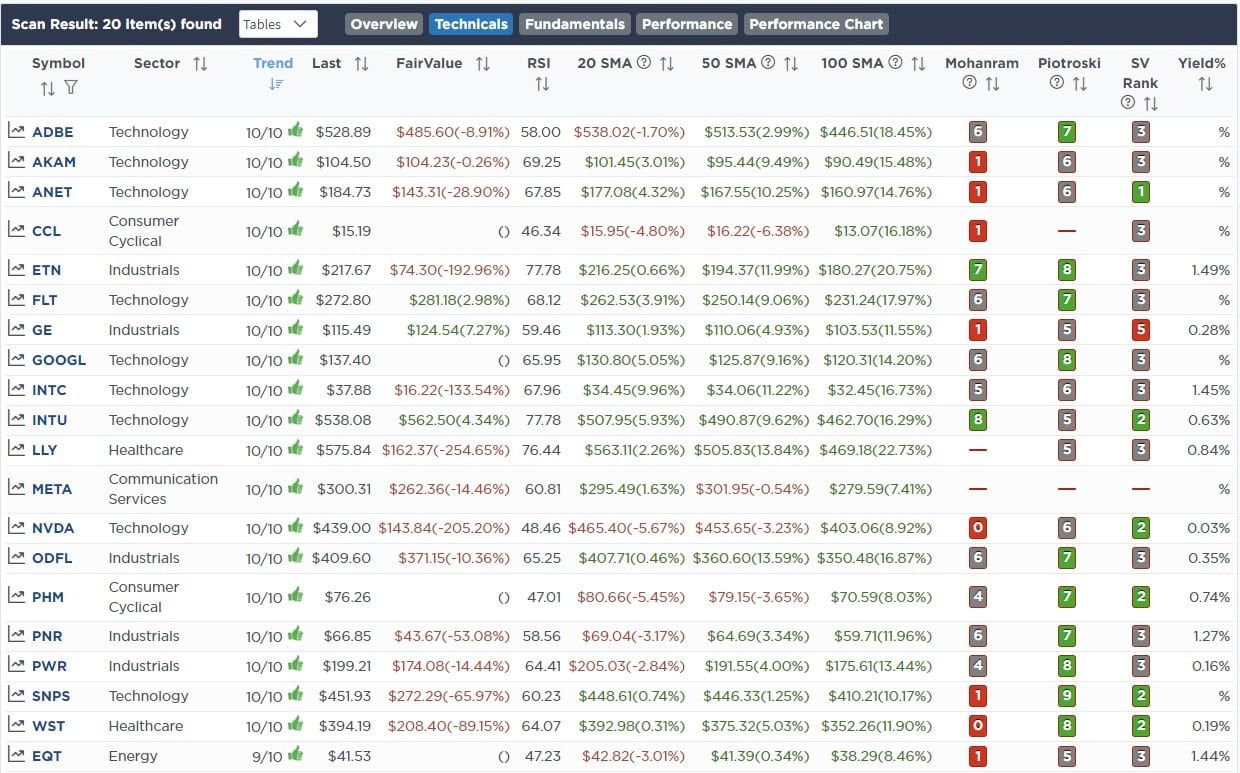

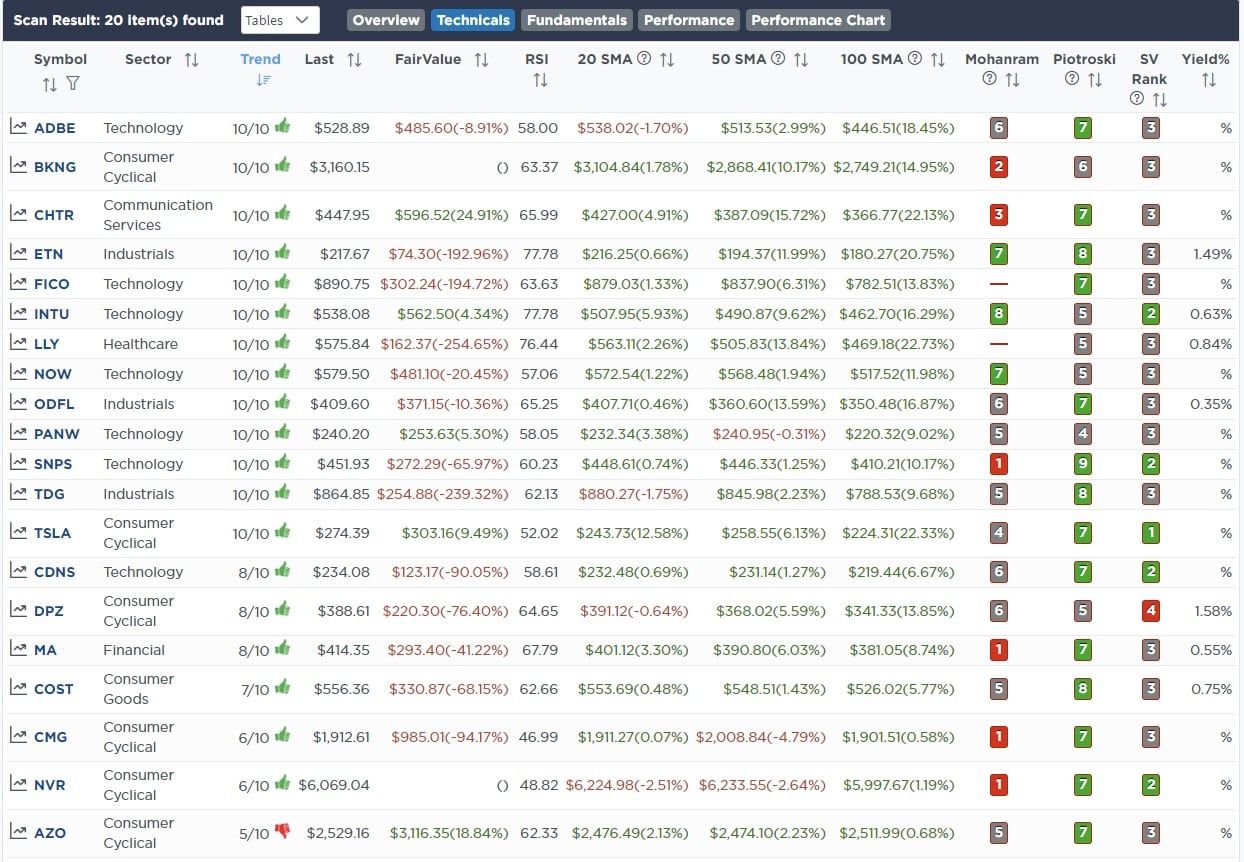

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental & Technical Strength

(Click Images To Enlarge)

R.S.I. Screen

Momentum Screen

Fundamental & Technical Strength

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

September 11th

This morning, we are taking some actions to accomplish two goals. 1) The first is the continued rebalancing of the portfolio to more closely align the weighting to our benchmark index, and 2) to reduce the number of holdings to 20 in total. After today’s rebalancing, we are holding 25 stocks, which we will continue to work on further reducing and consolidating the portfolio.

Equity Model

- Sell 100% of Coca-Cola Company (KO)

- Add 1% of the portfolio to both Proctor & Gamble (PG) and Apple (AAPL)

Lance Roberts, C.I.O.

Have a great week!