Heading into today’s BLS employment report, it’s worth summarizing other recent labor market data. Keep in mind, the BLS employment report and the jobs data we review below is of utmost importance to the Fed as they remain hawkish in fear of a price-wage spiral.

ADP shows a marked slow down in job growth. 106k jobs were added in January, down from 253k in December. Leisure and hospitality jobs added 95k jobs accounting for almost 100% of the gain. They do warn some of the weakness is weather related. Per ADP’s Chief Economist- “In January, we saw the impact of weather-related disruptions on employment during our reference week. Hiring was stronger during other weeks of the month, in line with the strength we saw late last year.”

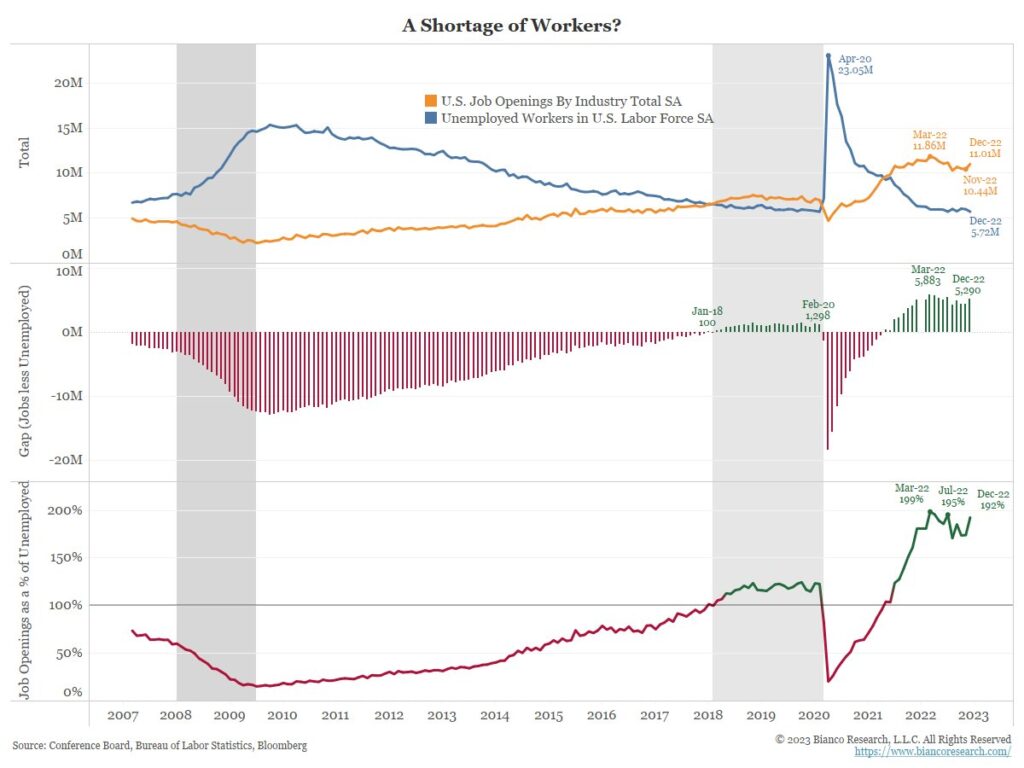

While ADP was weaker, JOLTs data was surprisingly strong. JOLTs is for December, unlike ADP and the BLS employment report, which cover January. The number of job openings rose by 572k to 11 million. Like the ADP report, leisure and hospitality jobs account for a large chunk of the openings. As shown below, the ratio of vacancies to unemployed workers rose to 1.92 from 1.74 in November and 1.81 a year ago. Lastly, the Employment Cost Index (ECI) confirmed a deceleration of wages. The 4% annualized wage growth over the last quarter is still above pre-covid levels, but it’s falling. In summary, there are some signs of weakness, but the data summarized above and recent initial jobless claims data do not lead us to believe the BLS employment report will be troublesome.

What To Watch Today

Economy

- 8:30 a.m. ET: Two-Month Payroll Net Revision, January (-28,000 prior)

- 8:30 a.m. ET: Change in Nonfarm Payrolls, January (190,000 expected, 223,000 prior)

- 8:30 a.m. ET: Change in Private Payrolls, January (190,000 expected, 220,000 prior)

- 8:30 a.m. ET: Change in Manufacturing Payrolls, January (6,000 expected, 8,000 prior)

- 8:30 a.m. ET: Unemployment Rate, January (3.6% expected, 3.5% prior)

- 8:30 a.m. ET: Average Hourly Earnings, month-over-month, January (0.3% expected, 0.3% prior)

- 8:30 a.m. ET: Average Hourly Earnings, year-over-year, January (4.3% expected, 4.6% prior)

- 8:30 a.m. ET: Average Weekly Hours All Employees, January (34.4 expected, 34.3 prior)

- 8:30 a.m. ET: Labor Force Participation Rate, January (62.3% expected, 62.3% prior)

- 8:30 a.m. ET: Underemployment Rate, January (6.5% prior)

- 9:45 a.m. ET: S&P Global U.S. Services PMI, January Final (46.6 prior)

- 10:00 a.m. ET: S&P Global U.S. Composite PMI, January Final (46.6 prior)

- 10:00 a.m. ET: ISM Services Index, January (50.5 expected, 49.6 prior, revised to 49.2)

Earnings

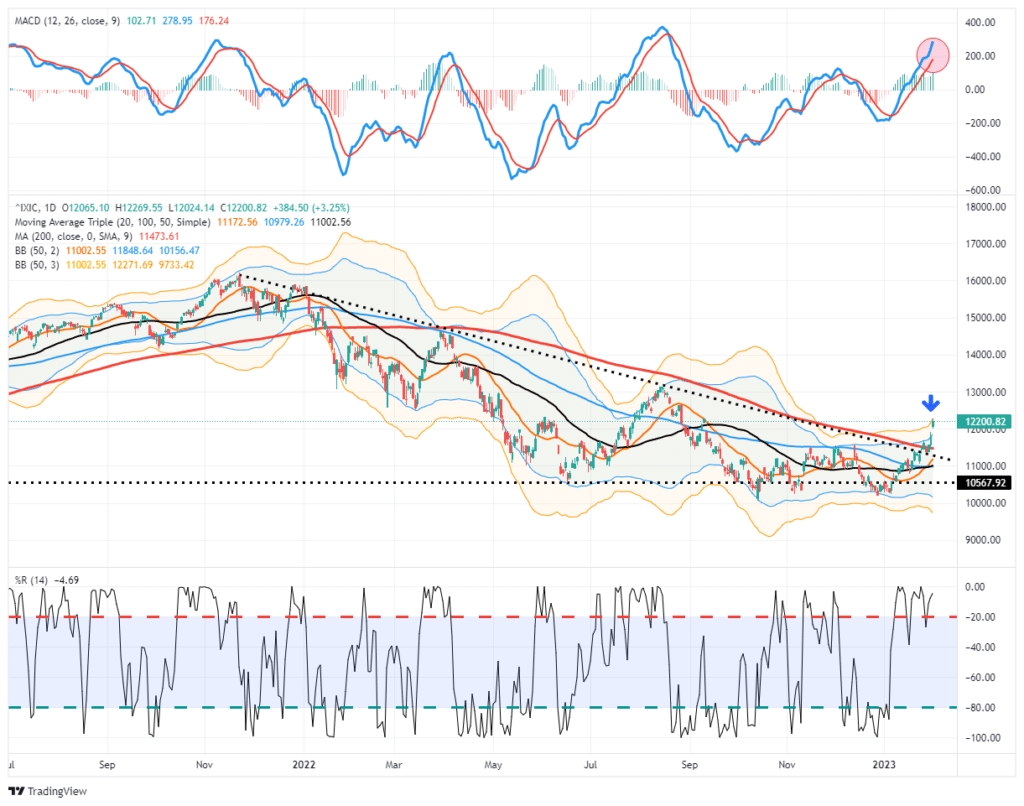

Market Trading Update – The Nasdaq

The Nasdaq has entered the bull market phase as the recent surge has pushed it clear of the 200-DMA and the downtrend from the January highs. While everyone had counted out the FANG stocks, we suggested at the market lows in early November; such was not likely the case. Since then, the Nasdaq has had a spectacular run, with many FANG stocks and beaten-up technology far outpacing the rest of the market.

With the Nasdaq pushing well into 3-standard deviations above the 50-DMA, the MACD “buy signal” at more extreme levels, and the Williams %R Index (%R) near zero, all suggest the market is well due for a pullback. Such a corrective phase should at least see a retest of the downtrend line and the 200-DMA. If the market can work off some overbought conditions but not break technical support levels, such will be a good opportunity to increase technology/growth-related exposures.

The markets are well ahead of fundamentals currently, so be patient chasing markets here.

More Warnings about the January Effect

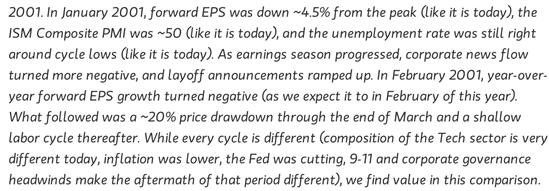

In Thursday’s Commentary, we noted the flaws with the January effect. We also used 2001 as a reason for caution. Per our advice:

In 2001, the Nasdaq started the year with an 8% gain in January. By September, it was down 54% year to date. It rallied to close the year down 35%, resulting in a lot of pain for those following the January effect.

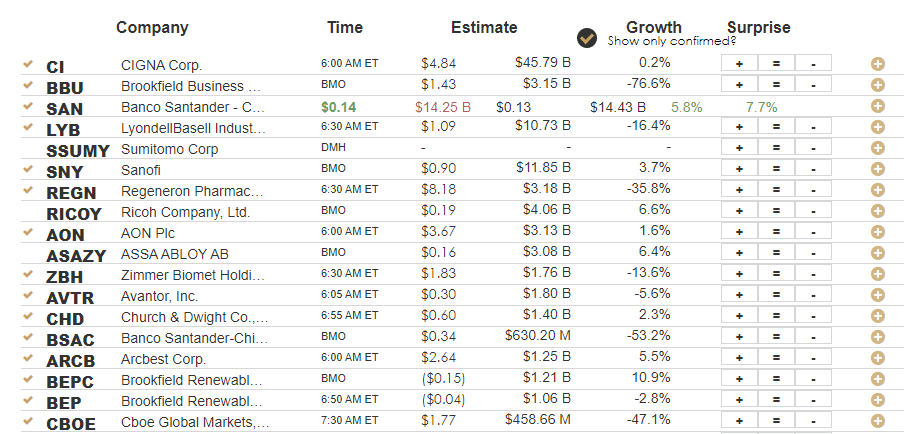

In the table below, Morgan Stanley compares January 2001 to last January. In particular, they show how the 2000 laggards were the top performers in January 2001. Similarly, last years laggards led the way this January. As the title says, Morgan Stanley thinks January’s rally will not end well. Below the table, Morgan Stanley explains that it’s not just the performance of laggards that explains their bearishness. There are other similarities worth noting.

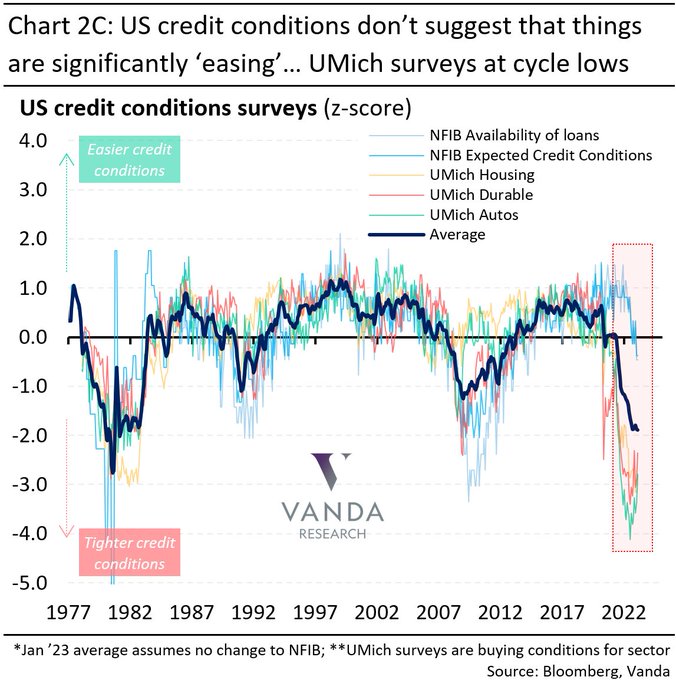

Financial Conditions – Another Opinion

Financial conditions, as defined by Powell, are generally easing. His definition of financial conditions heavily emphasizes stock prices, bond yields, and the dollar. As the graph below shows, Vanda Reserach thinks financial conditions are not easing. Their gauge thinks they are tightest since the late 1970s. The factors used for their gauge are things that truly matter to the real economy. If they are correct, the lagged effect of extremely tight financial conditions will result in a recession, and the Fed quickly pivoting to a much more accommodative stance.

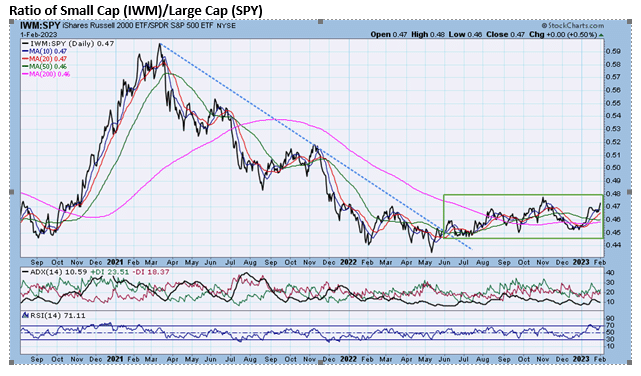

Small Caps Vs. Large Caps Favor Goldilocks

Jeffrey Marcus from Turning Point Analytics (TPA) thinks the recent outperformance of small cap versus large cap stocks is another indicator that the market is betting on a soft landing, aka the Goldilocks scenario. If Jeff is right, small caps have a lot of ground they can potentially pick up versus large-cap stocks. Per Jeff:

The ratio of Small Caps versus Large Caps broke out of a steep 17-month downtrend in August and appears to have established a series of higher lows. Small Caps are the most vulnerable to an economic downturn and their outperformance is a reason for optimism.

TPA is an add-on service available within SimpleVisor. Click HERE and check out the great research Jeff and TPA provide SimpleVisor subscribers.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.