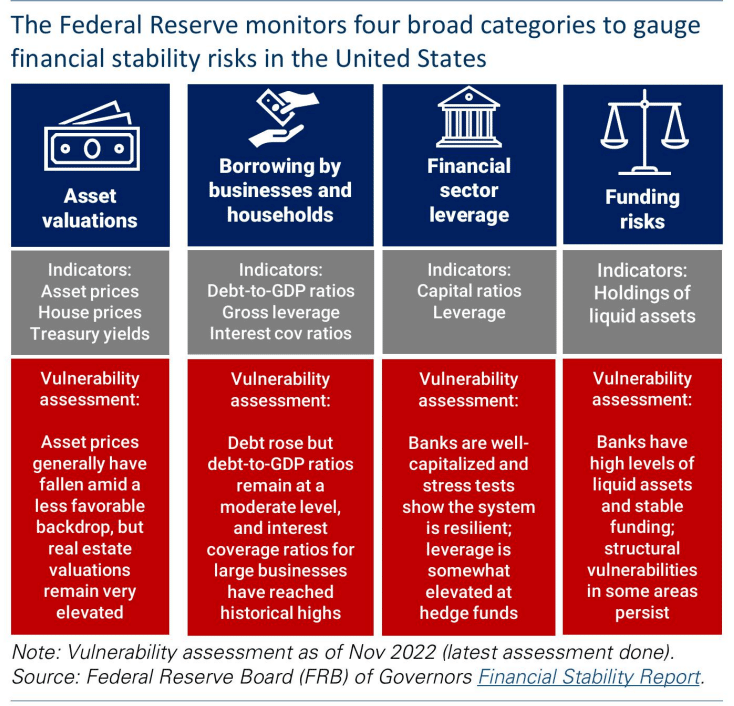

Recently we have noted that the odds are increasing that financial instability, or as we say, “something breaks,” is the likely culprit to force the Fed to reverse course. Given the strong link between Fed policy and asset prices, it’s valuable to appreciate how the Fed monitors financial stability. The illustration below categorizes the four factors the Fed assesses in its Financial Stability Report. The red-shaded areas provide a current update on the four financial stability categories. While conditions can change rapidly, there are few signs of financial instability rearing its ugly head.

Some may argue that stock and bond prices are down 15-20%, which does not portend financial stability. However, as noted, they have been offset to some degree by rising home prices. If stock and bond prices stay down and house prices start falling as many expect, we might see one of the four financial instability measures trigger a warning. However, such would likely not be enough for a pivot unless stock and or bond prices decline further from current levels. As for the three other categories, there is nothing concerning at the moment, but conditions can change quickly.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Nov. 18 (2.7% prior)

- 8:30 a.m. ET: Durable Goods Orders, October preliminary (0.4% expected, 0.4% prior)

- 8:30 a.m. ET: Durables Excluding Transportation, October preliminary (0.0% expected, -0.5% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Nov. 19 (225,000 expected, 222,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Nov. 12 (1.520 million prior)

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, November preliminary (50.0 expected, 50.4 prior)

- 9:45 a.m. ET: S&P Global U.S. Services PMI, November preliminary (48.0 expected, 47.8 prior)

- 10:00 a.m. ET: University of Michigan Consumer Sentiment, November (55.0 expected, 54.7 prior)

- 10:00 a.m. ET: New Home Sales, October (570,000 expected, 603,000 prior)

- 10:00 a.m. ET: New Home Sales, month-over-month, October (-5.5% expected, -10.9% prior)

- 2:00 p.m. ET: FOMC Meeting Minutes, November 1-2

Earnings

Market Trading Update

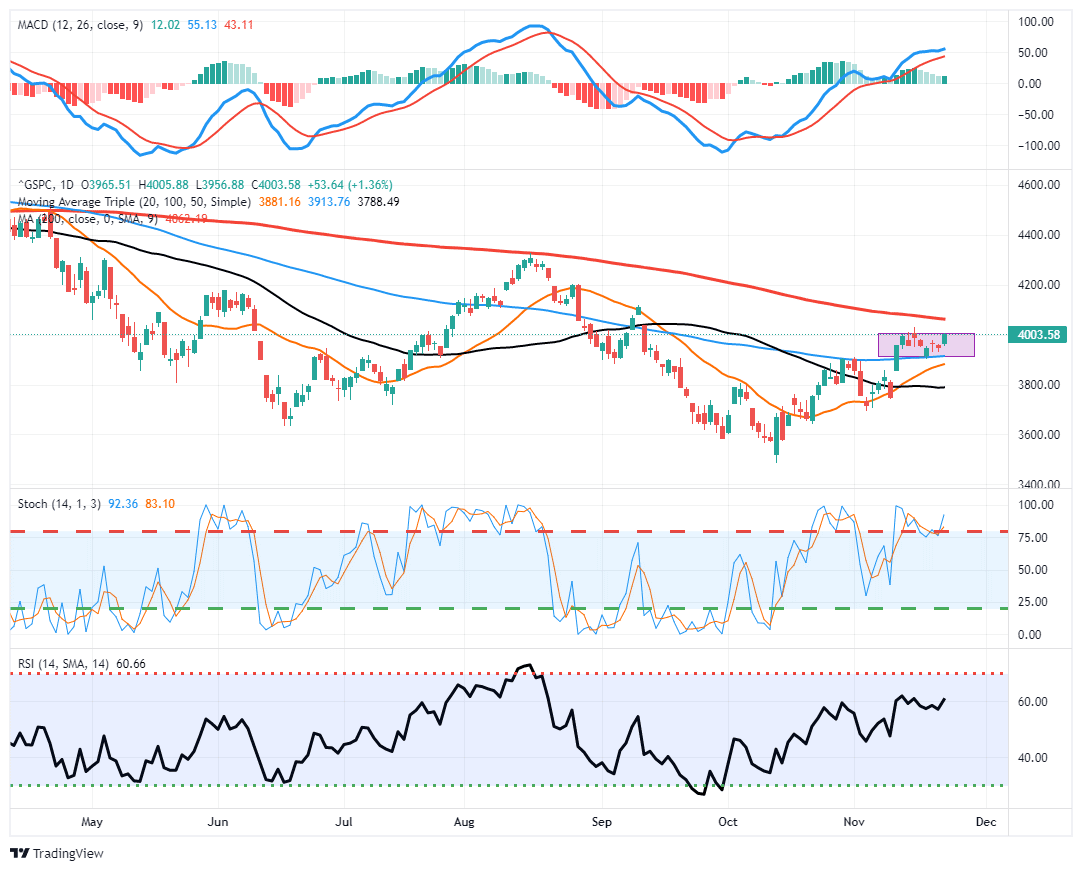

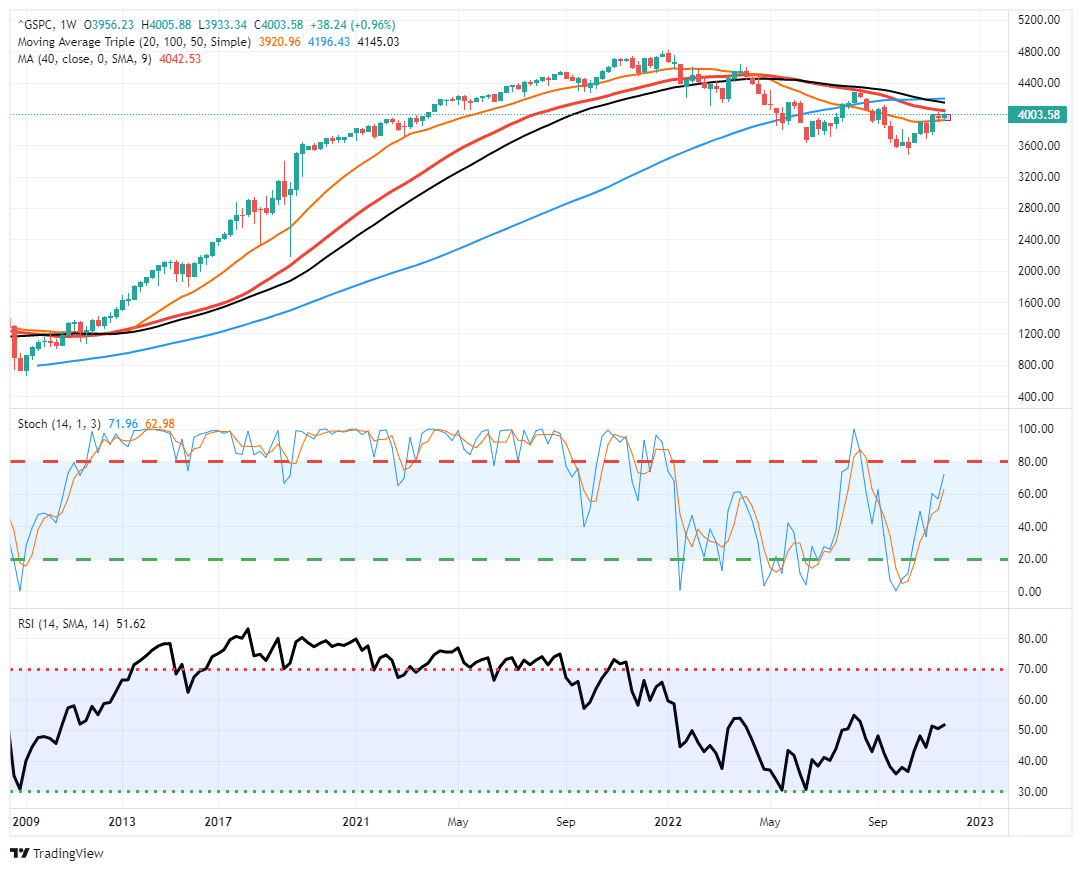

Yesterday, the market traded all day positively, building on the gains from the morning open. As noted previously, there is little volume this week due to the holiday-shortened trading week, so don’t read too much into yesterday’s action. The market has been trading in a consolidation pattern for the last two weeks, and a rally tomorrow will set up a test of the 200-dma, which has acted as important resistance to the market all year. A confirmed break above the 200-dma would suggest a continued rally higher, but there are still many headwinds currently facing asset prices.

While the bulls are getting excited short-term by the action, the longer-term picture remains challenging, with numerous weekly moving averages sitting just above the market. We still suspect a rally into year-end, but the beginning of next year will likely be more challenging. Continue to use rallies to raise cash and rebalance positions heading into year-end.

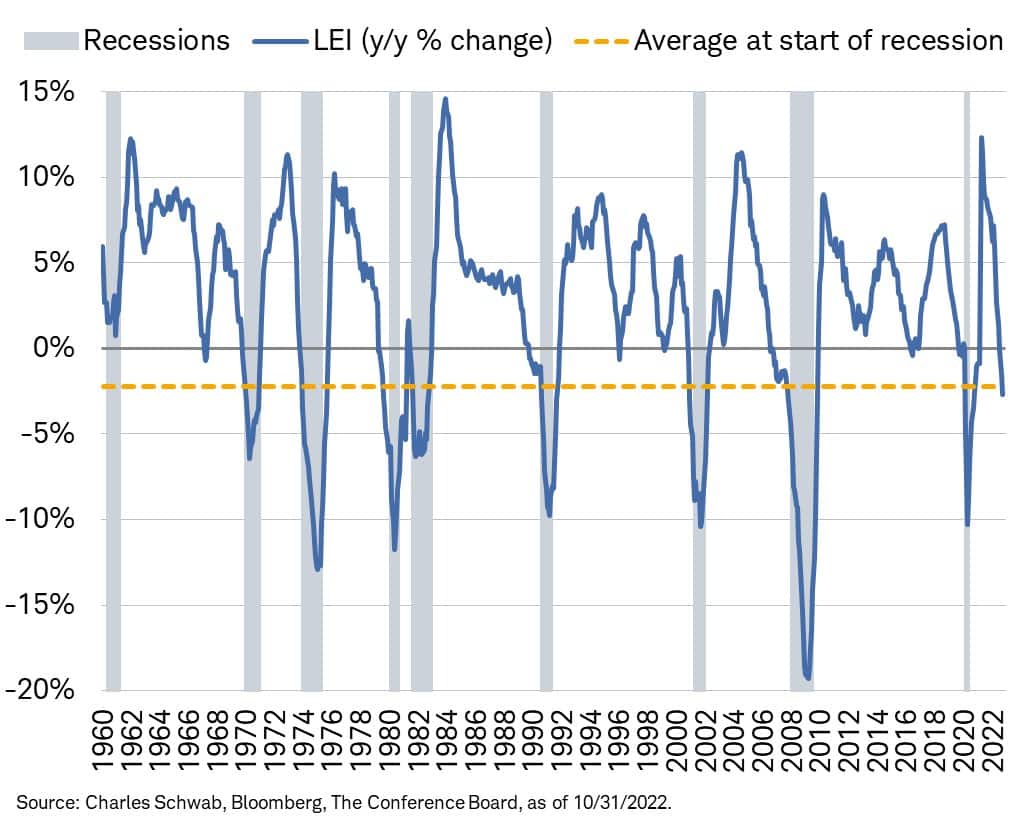

Another Day, Another Recession Warning

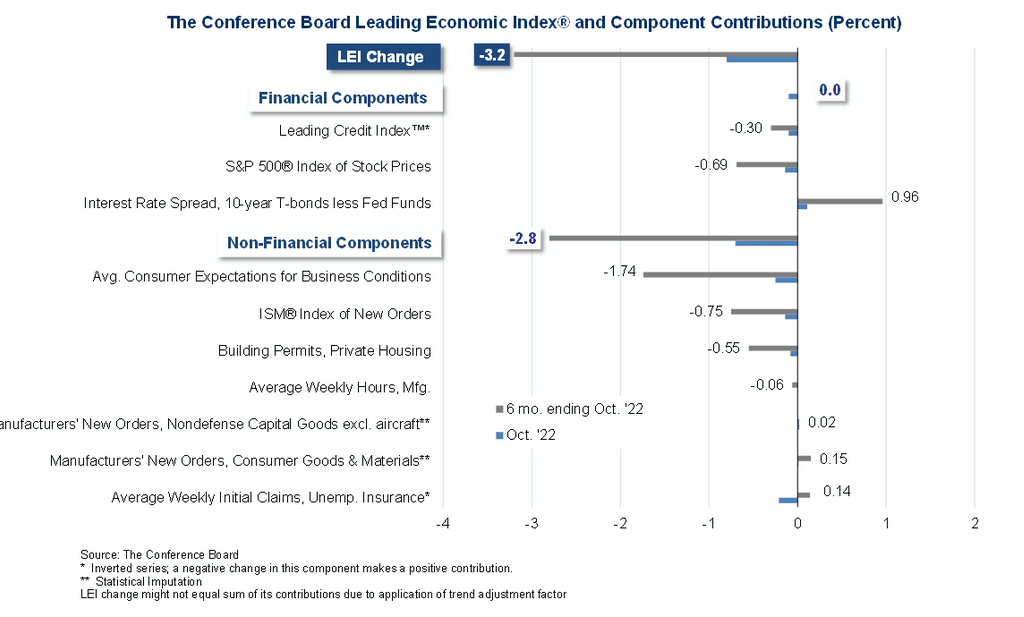

The graph from Charles Schwab shows that the Conference Board’s Leading Economic Indicators (LEI) is -2.7%, below -2.2%, the average start of recessions since 1960. The second chart shows the factors that make up the LEI. It shows that market indicators for a recession portend flat growth. Non-financial indicators are flashing red. Of note, the biggest drag to the LEI index is Consumer Expectations. Consumer consumption accounts for almost two-thirds of GDP, so it is not surprising consumers’ dour outlook raises the odds of a recession.

Inflation Set To Plummet

The graph below shows the robust correlation between the NFIB (small business owners survey) and CPI. Assuming the correlation holds up as it has for the last 20 years, we should expect inflation to normalize quickly. It is worth caveating that the reasons for inflation today are unlike any prior experiences of the last 20 years. While we think inflation will decline, we are not sold it will be as much or as fast as the graph portends.

Crypto vs. Sub-Prime, Perspective Matters

Joe Weisenthal of Bloomberg, in his daily commentary, reminds us there is a vast difference between the popping of the cryptocurrency bubble and the subprime/mortgage meltdown of 2007-8. People need housing. Nobody needs cryptocurrency. Accordingly, there is a natural bottom to home prices and, therefore, a limit to losses for mortgage debt investors. In contrast with crypto, “There’s no obvious circuit breaker or curb to stem the decline.”

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.