Ten years feels like an eternity, yet close enough to retirement to set the stage for preparation. To make the journey easier, one step at a time, here are ten steps, ten years to retirement.

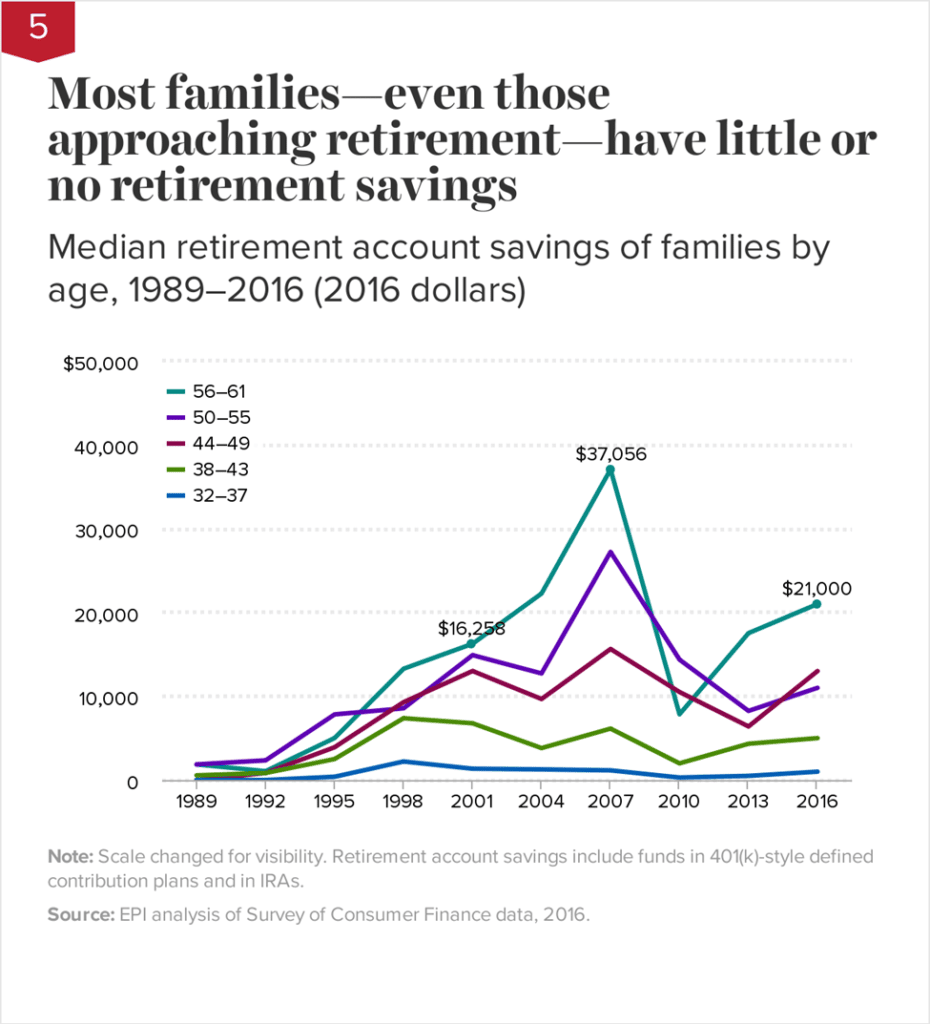

When do people get serious about saving for retirement? The answer probably won’t surprise you. Many families have challenges saving.

Certainly, socking money away for a target a decade or more away is a feat accomplished by those who are genuinely enthusiastic about delayed gratification and place financial security as a top priority – not easy for Americans.

After all, we’re consumers at heart!

The following ten steps, ten years to retirement, are designed to help you make it but not fake it: Every year, one step at a time.

Year One: Meet your older self today.

The ability to visualize what your life will be like and how you’ll age physically is a motivation to get the retirement assessment started. It was tough to connect to your older self until facial aging technology came along to help you meet your future – gray hair and all.

Smartphone apps such as Oldify, AgingBooth, and HourFace will place you electronically in the present with your retired future. Remember, what the mind believes is reality; thus, aging apps and the associated wrinkles will have you planning with a spring in your step.

Year Two: Flip the script.

Time to dig deep and assess your money roots. Adequate time still exists to flip your money script, discard subconscious negative money thoughts and change your fiscal habits. But how does one extract money thoughts from the deepest recesses of the brain? Well, there is a way.

Money Scripts® is a concept created by financial psychologists Brad and Ted Klontz. They are unconscious, trans-generational beliefs about money developed in childhood and drive adult financial behaviors.

Money avoidance, money worship, money status, and money vigilance are the four categories of Money Scripts.

Per the research, money avoiders believe money is evil and rich people are greedy. Worshipers believe more money will solve all their problems. Status seekers equate self-worth to net worth and place a premium on buying the newest and best things. The vigilant is alert, watchful, and concerned about their financial health.

My Money Script.

Recently, I went through the short Klontz Money Script Inventory-R (KMSI-R) to identify my Money Scripts®. The key is to be dominant or have higher levels of conviction in the healthiest category. Scores less than or equal to 3 suggest an individual doesn’t exhibit the money script. Scores above 4 indicate one shows many of the characteristics of the money script.

My scores:

- Money Avoidance: Low 1.50

2. Money Focus: Medium 3.57

3. Money Status: Low 1.57

4. Money Vigilance: High 4.25

I’m not surprised at my high Money Vigilance score. However, a medium Money Focus forces me to dig deeper and figure out why. Again, the Money Focused believe the solution to their problems is to have more money.

At the same time, they believe that one can never have enough money and find that the pursuit of money never quite satisfies them. Although money does signify security to me, I am far from a status chaser. I live in a modest home and am not interested in catching up with others or buying expensive goods and services.

My father would have been dominant on the Money Focus score as he was prone to buying things to achieve happiness and status. I am a big gift-giver. Perhaps that’s the problem. I’m still delving into my money behavior and grateful to have a tool that generates awareness.

Do you dare to understand your Money Scripts®? You can receive a complimentary KMSI-R here. The assessment is part of your self-discovery.

Also, beginning in 2023, RIA will offer a series of free money quizzes at www.riaadvisors.com. These behavioral assessments can help identify deep seeded good money habits and explore the subconscious, self-defeating motivations that require attention.

Year Three: Begin financial planning on your ten-step, ten years to retirement adventure.

Begin with the basics and build on that foundation. Perhaps you’re not ready for comprehensive planning. That’s ok. Start small. Initially, consider a modular exercise such as maintaining or finetuning a family budget, tracking household cash flow, and beginning the exercise of clearly identifying retirement needs, wants, and wishes.

Year Four: Get anchored.

Around six years before retirement, the most successful pre-retirees have reviewed their housing options, especially for the active early years of retirement. With one of their most significant decisions out of the way, pre-retirees can anchor down in smaller, more affordable digs or begin thinking about the home improvements required to age in place.

Steps taken include – downsizing to one-story homes, aging-friendly renovations to bathrooms, doorways, and acceleration of mortgage pay downs.

Also, it is time to lay the groundwork for the first iteration of a comprehensive financial plan and start attaching numbers and inflation rates to future retirement aspirations. When people think of planning, they think of investments.

A plan is much more.

Unfortunately, the financial services industry treats financial plans as loss leaders and create them for free to forge a so-called ‘legit’ path to commissioned product. To believe a financial plan is only about investments is like enjoying one layer of a delicious seven-layer cake.

What should a financial plan do?

A financial plan, adequately designed, along with your behavioral assessment and financial coach, can create a lifelong blueprint for every financial step you take in and through retirement.

A holistic plan should be a function of the financial life benchmarks one seeks to achieve.

- Begin with needs. They are the priorities. How much do you require for rent, mortgage, and insurance, for example?

- Then, wants: The fun stuff and other expenses are secondary benchmarks. Day trips? A second home?

- Last are your wishes: GO for the gusto! List the most incredible bucket list items. Can your plan handle them?

- You and your planner are responsible for developing a practical plan that works. It’s a give-and-take. It would help if you remained flexible to be successful.

Candidly, the financial plan becomes the glue that seals the ten steps, ten years to retirement path.

Year Five: Take on a Roth mindset.

Regular blog readers know that at RIA, we recommend investors maintain pre-tax, after-tax, and Roth accounts to allow for a tax-efficient, flexible retirement income strategy.

With U.S. national debt at the $31 trillion mark, the highest in history, it’s easier to understand why we believe marginal tax rates are headed higher. Retirees will discover how easy it will be for their incomes to surpass the lower tax brackets with the taxation of Social Security benefits included.

Ultimately, mainstream finance and tax professionals encourage investors to maximize contributions to pre-tax accounts. It’s all about saving taxes today. While this could be an ineffective strategy for accumulators as careers advance and incomes grow, people closer to retirement should have a plan to diversify their accounts.

At the year five benchmark, pre-retirees should re-direct their current plan contributions from traditional to Roth options. Your employer plan likely has a Roth selection. Use it. I understand this tactic sounds painful (it’s tough to break the SAVE MONEY NOW habit).

However, in retirement, you’ll thank me because instead of one account with every distribution taxed as ordinary income, you will have multiple accounts taxed at different rates or not at all.

Year Six: Consider your ten steps, ten years to retirement plan a health journey too.

First, I implore you to buy the newest book by Tony Robbins called Life Force. The cutting-edge health information within is a game changer. The breakthroughs in preventative health technology are nothing short of amazing, and if even half the technology goes mainstream, I feel great about your health equals wealth connection in retirement.

For now, consider 23andMe®. Their subscription service provides ongoing insights indispensable to health improvement. Most important, DNA testing helps detect genetic variants.

Are you predisposed to macular degeneration? Prostate cancer? Type 2 Diabetes? It’s most important to discover whether you’re inclined to late-onset Alzheimer’s disease to manage your health better and bolster preparation for long-term care needs.

I am relieved that I don’t have a variant detected for Alzheimer’s. However, I have a typical likelihood of various heart ailments, which motivates me to exercise more, follow a stricter diet and get plenty of sleep.

Last, this technology isn’t perfect. Yet, the information can motivate subscribers to make smarter, healthier choices.

After all, we all want to live long enough to see our ten steps, ten years to retirement plan pay off, don’t we?

Year Seven: Set financial boundaries.

You’re coasting now in the right lane. The time for retirement has almost arrived but beware of the traps. Seven is the year of creating and enforcing financial boundaries. It’s a harsh lesson for some, but once learned, never forgotten. Nothing is inappropriate about maintaining boundaries and saying “no” to obligations that may jeopardize your financial security.

For example, we witness parents who extend themselves to co-sign for children. We all know people who lend to friends and family members and are disappointed when loan obligations are not met. It’s acceptable to establish charitable intentions and gifts as part of your plan; it’s honorable to help people you love who are in need.

However, it’s best to understand upfront the financial impact on your situation.

Know your boundaries and stick with them. If you say ‘no’ enough, others will respect them, too.

Year Eight: Get all the significant home improvements completed.

New roofs, air conditioners, windows, and even backyard improvements. Preferably, it’s best to take care of significant expenses before the last work day. Call it a head start, but costs out of the way before retirement provide a sense of financial well-being and an emotional breather knowing you’re still working.

Need ideas for housing modifications to consider? Read here.

Year Nine: Document a transition plan.

Maintain a bucket list, travel aspirations, or a journal. Year nine is the time to prepare your mind for transitioning from a career to the next exciting phase of life. Consider an activity log. Be mindful of how you’re going to remain social and relevant. Don’t have a hobby? Find one, learn it, and sharpen it when the work clock stops.

Year Ten: One last run before takeoff.

I am concerned there’s a retirement headwind, and the storm has been brewing. The RIA financial planning team reduced forward-looking returns for all asset classes in 2018. Therefore, even with all the market turmoil today, client plans are still on target.

Current retirees take note. A new study, The Safe Withdrawal Rate: Evidence from a Broad Sample of Developed Markets, paints an ominous picture. According to the research, the 4% portfolio withdrawal rule is outdated. Frankly, we’ve been writing about this topic for years.

The authors conclude:

We find that there is no withdrawal rate that allows most retirees to maintain a reasonable standard of living while being virtually assured they will not outlive their wealth. Even if a couple is willing to bear a 5% ruin probability, the withdrawal rate is just 2.26%. This modest withdrawal rate implies that households must accumulate substantial savings to avoid severe spending cuts during retirement.

In addition, we think retirees can increase their income by considering smart Social Security planning and guaranteed income options. Recently, I penned The Money-Savvy Guide to Retirement Income, available for free download here.

The guide can help you consider where you fall regarding retirement income sustainability using the three types of investors classified by RIA. Comprehensive financial planning is the best way to outline an action plan to generate a retirement ‘paycheck.’

However, a simple calculation can motivate you to complete a retirement income analysis with a financial professional who has your best interest at heart. Inspired by the work of entrepreneur and author David Macchia who focuses on the processes of retirement income planning, there are three categories investors who require retirement income fall into. Read the guide, do the quick calculations, and see where you fall!

Sadly, investors are told by financial media and their brokers how they’re able to withdraw a FIXED 4% annually from a VARIABLE portfolio comprised of stocks, bonds, and cash. It’s like somebody telling you – sure, oil and water DO MIX (occasionally).

Let me be clear. Repeat after me:

AN INVESTOR CANNOT WITHDRAW AN INDEFINITE, SAME FIXED PERCENTAGE from a portfolio throughout retirement. Therefore, I cannot tell advise with complete confidence that a VARIABLE PORTFOLIO CAN PROVIDE THE SAME FIXED WITHDRAWAL RATE over a lifetime. If I did, I’d be lying. Or, at the least, I’d depend blindly on a stale academic study older than most of our adult children.

Early 2023 is a good time to review your income plans in the face of market headwinds.

Ten steps, ten years to retirement, is a decade-long preparation strategy to build out your dream of security, wealth, and health, created by those who took the steps before you.