In this edition of the Value Seeker Report, we analyze an investment opportunity in WESCO International (NYSE: WCC) using fundamental and technical analysis.

Overview

- WESCO International (WCC) is a distributor of electrical and communications construction products in the US and abroad. WCC also offers value-added services ranging from supply chain management, to inventory management, to system installation and partial assembly of products.

- The firm’s customers include independent contractors, industrial manufacturers, utility firms, public institutions, and various government agencies. WCC belongs to the Industrials sector and currently has a market cap of $2.4B.

- WCC completed a large merger with Anixter in June 2020, making the combined firm a leader in the markets it serves. Still, the industrial distribution market remains fragmented, leaving plenty of room for organic growth.

- WCC’s stock is currently trading at $48.95 per share. Using our forecasts, we arrive at an intrinsic value of $61.42 per share. This implies an upside of roughly 25% on the investment.

Pros

- WCC is doing an exceptional job of integrating the two firms, especially considering the challenges presented by closing a merger mid-pandemic. Leadership has given some of the credit to the strong cultural alignment between the firms heading into the merger. Other contributing factors include the detailed pre-merger planning and sound execution of those plans at all levels of the business.

- Overall, leadership has been proactive in providing investors with a clear view of its vision and the steps WCC will take to get there. This is particularly apparent in WCC’s second quarter earnings call and presentation.

- WCC expects to exploit substantial cost synergies through its merger with Anixter. Further, the once-separate entities offer complementary products and services. This opens the opportunity for cross-selling to existing customers.

- Management is very intent on reducing leverage its target range by 2024. Although WCC substantially increased its debt to finance the deal, the firm has a proven ability to de-lever following acquisitions. As shown below, our forecasts confirm that WCC is capable of generating the free cash flow required to meet this goal.

Cons

- In the industrial and construction end-markets that WCC serves, demand has been materially impacted by the pandemic. For example, most of WCC’s contractor customers work in non-residential construction. An area which has suffered more than its residential counterpart and could remain weak for some time.

Key Assumptions

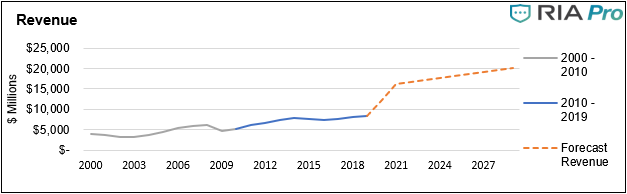

- Revenue growth forecasts for 2020 and 2021 are primarily because of the Anixter deal’s expected impact on revenue. However, we do not expect the combined firm’s revenue to fully recover until 2023. The chart below illustrates our forecasts in relation to historical revenue.

- As part of the integration, WCC will begin Anixter’s “gross margin improvement program”. Under this program, Anixter managed to deliver seven consecutive quarters of gross margin improvement. Taking this and other cost synergies into count, we forecast WCC operating margins to improve slightly each year until 2024 and settle thereafter. The chart below shows how our forecasts of operating profit evolve over time.

- Based on guidance, we forecast the release of roughly $75M in working capital over the next three years as WCC realizes synergies from the merger.

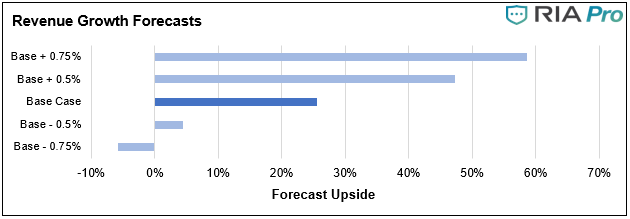

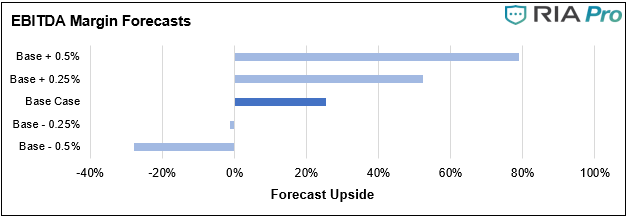

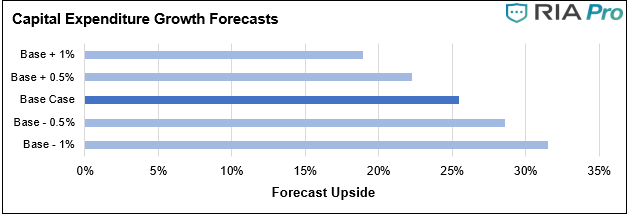

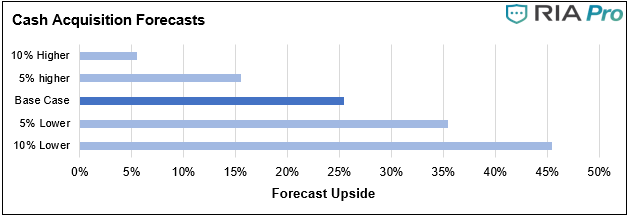

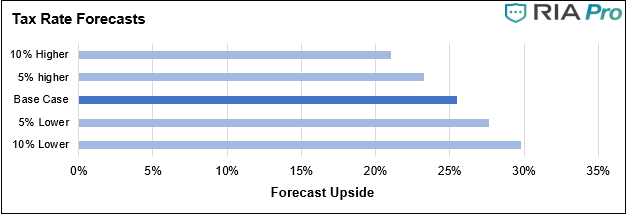

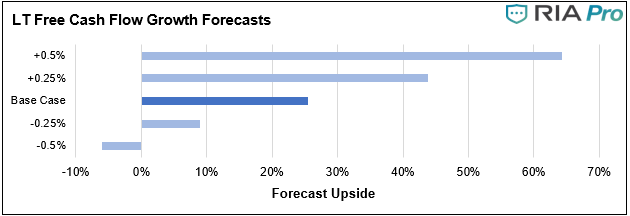

Sensitivity Analysis

- A brief note on why we present sensitivity analysis can be found here.

- Incremental movements in margins are crucial to WCC’s intrinsic value because of the low margin nature of its business. The realization of cost synergies and margin improvements by the firm are an important part of our investment thesis, and thus will require special attention when the firm reports earnings.

Technical Snapshot

- WCC is currently testing resistance near $48.35 per share. The stock recently closed above said level, but whether it can hold above remains to be seen. On the downside, the stock should receive support near its 50-day moving average.

- The stock is sitting in overbought territory. Accordingly, it may be wise for investors to wait for a slight pull-back before initiating a position.

Value Seeker Report Conclusion On WCC

- Following the deal with Anixter, WCC is better equipped to leverage the size and scale of its operations to create value for shareholders. Clearly, Management has a plan in place to achieve its targets and intends to execute it well.

- We suspect that the stock remains undervalued because of the timing of the deal. It was announced just before the pandemic ensued and closed in June. For a small/mid-cap firm in the industrials sector, it is not implausible that this deal was simply overshadowed by the pandemic and is not yet fully priced in.

- WCC reports third quarter earnings on November 5th, 2020. It will be WCC’s first report with a full quarter’s contribution from Anixter, and an early improvement in margins could spark the stock’s move to intrinsic value.

- Based on our forecasts, WCC has 25.5% of upside remaining before reaching its intrinsic value.

For the Value Seeker Report, we utilize RIA Advisors’ Discounted Cash Flow (DCF) valuation model to evaluate the investment merits of selected stocks. Our model is based on our forecasts of free cash flow over the next ten years.