With inflation fears getting stoked by the mainstream media, traders are pushing oil, interest rates, and the dollar higher. Are they right? Or, are they about to get smacked by a slower economy and deflationary headwinds?

Once a quarter, I dig into the Commitment of Traders data to see where speculators are making their bets. Such is an excellent metric to watch from a contrarian view. Generally, when traders are positioned either very long or short in a particular area, it is often a good bet something will reverse.

Positioning Review

The COT (Commitment Of Traders) data, which is exceptionally important, is the sole source of the actual holdings of the three critical commodity-trading groups, namely:

- Commercial Traders: this group consists of traders that use futures contracts for hedging purposes. Their positions exceed the reporting levels of the CFTC. These traders are usually involved with the production and processing of the underlying commodity.

- Non-Commercial Traders: this group consists of traders that don’t use futures contracts for hedging and whose positions exceed the CFTC reporting levels. They are typically large traders such as clearinghouses, futures commission merchants, foreign brokers, etc.

- Small Traders: the positions of these traders do not exceed the CFTC reporting levels, and as the name implies, these are usually small traders.

The data we are interested in is the second group of Non-Commercial Traders (NCTs.)

NCT’s are the group that speculates on where they believe the market will head. While you would expect these individuals to be “smarter” than retail investors, we find they are just as subject to “human fallacy” and “herd mentality” as everyone else.

Therefore, as shown in the charts below, we can look at their current net positioning (long contracts minus short contracts) to gauge excessive bullishness or bearishness.

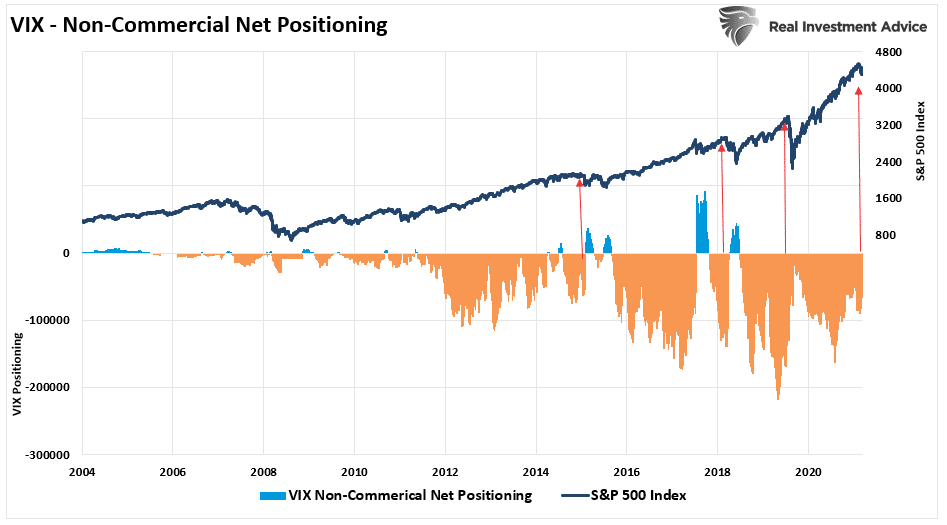

Volatility

Since 2012, the favorite trade of bullish speculators has been to “short the VIX.” Shorting the volatility index (VIX) remains an extraordinarily bullish and profitable trade due to the inherent leverage in options. Leverage is one of those things that works great until it doesn’t.

Currently, net shorts on the VIX are still very elevated but reduced from 2020 levels. However, speculators have once again started to increase their net short-positioning over the last several weeks as the market declined.

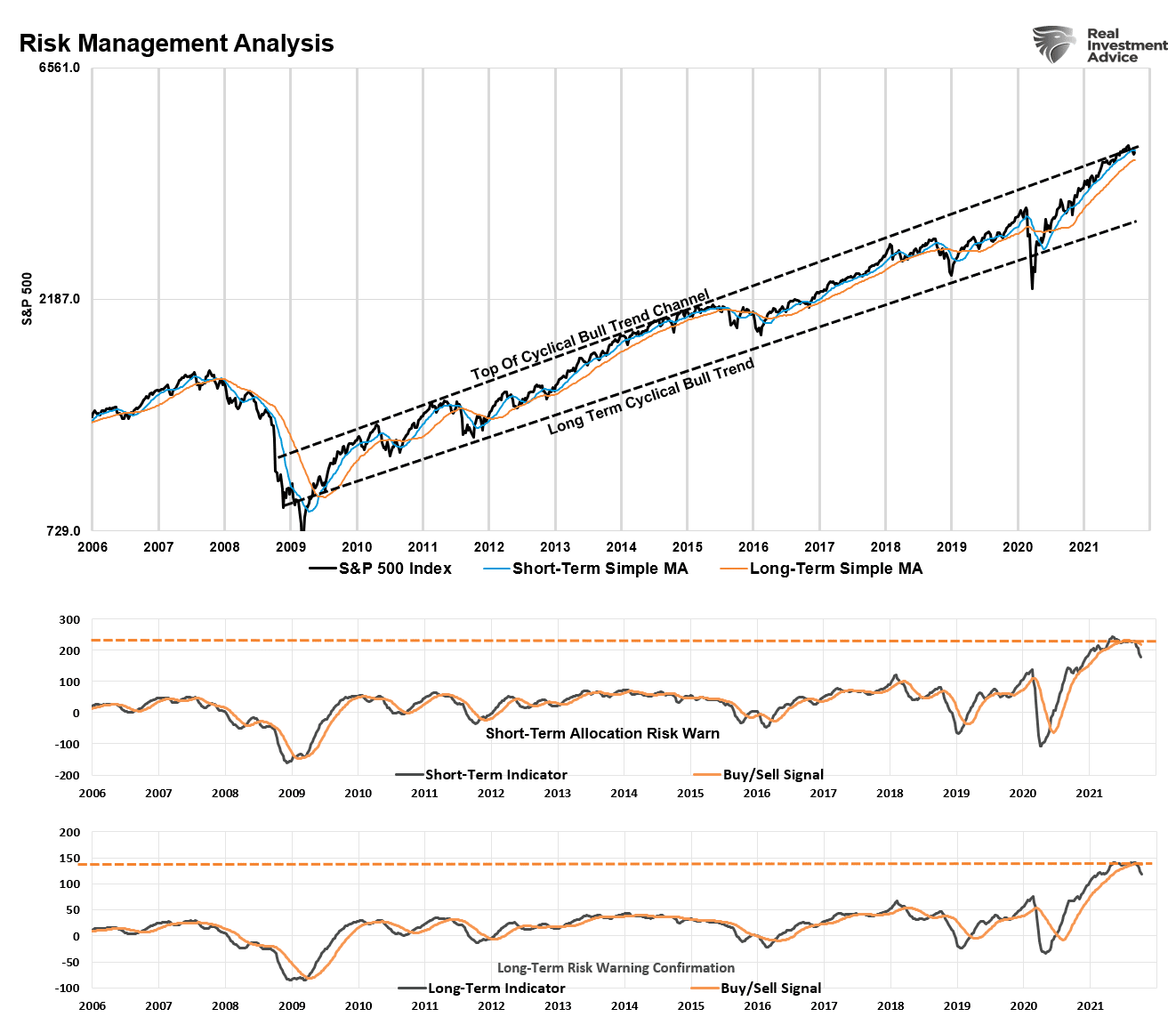

The current positioning is large enough to fuel a more substantial correction if markets fail current support levels. Moreover, as noted on Tuesday, weekly signals suggest that downside risk is present. To wit:

“The recent decline triggered both weekly signals for the first time since the March 2020 correction. (The chart below is the same model we use to manage 401k allocations. You can see the related models and analysis here)“

Given that volatility has remained compressed during the entirety of the September correction, a break below recent support will trigger short-covering of VIX options. Such would also be coincident with a more significant decline in the index.

Crude Oil Extreme

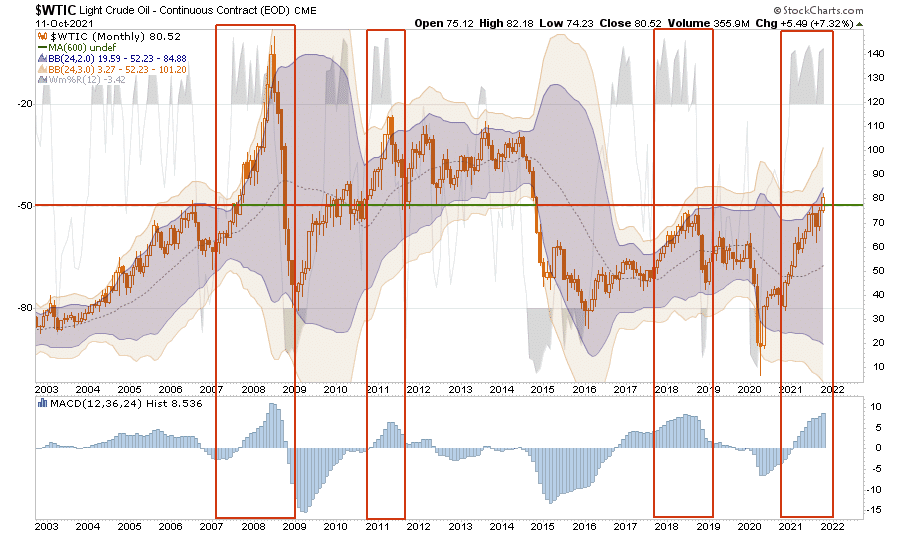

Crude oil has gotten a lot more interesting as of late. After a brutal 2020, the price of oil futures going negative at one point, oil is now pushing above $80/bbl. Given current views of “inflation” from the massive liquidity infusions and supply chain disruptions, the focus on speculative positioning is not surprising.

As shown in the monthly chart below, the price advance in crude oil is now back to historical extremes that have previously denoted tops in oil prices. As a result, the current extreme overbought, extended, and deviated positioning in crude will likely lead to a rather sharp correction. (The boxes denote previous periods of exceptional deviations from long-term trends.)

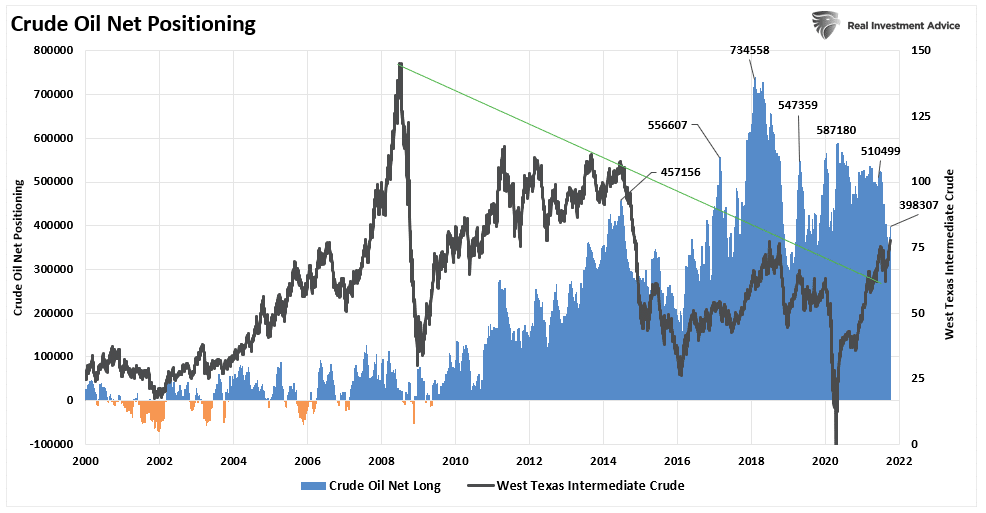

The speculative long-positioning is driving the dichotomy in crude oil by NCTs. While levels fell from previous 2018 highs during a series of oil price crashes, they remain elevated at 398,307 net-long contracts and rising quickly.

The good news is that oil did finally break above the long-term downtrend. However, it is too soon to know if these prices will “stick.”

Furthermore, the deflationary push and the dollar rally will likely derail oil prices if it continues.

U.S. Dollar Rally Is Here

As I stated earlier this year:

“There are two significant risks to the entire ‘bull market’ thesis: interest rates and the dollar. For the bulls, the underlying rationalization for high valuations has been low inflation and rates. In February, we stated:

Given an economy that is pushing $87 trillion in debt, higher rates and inflation will have immediate and adverse effects:“

- The Federal Reserve gets forced to begin talking tapering QE, and reducing accommodation; and,

- The consumer will begin to contract consumption as higher costs pass through from producers.

“Given that personal consumption expenditures comprise roughly 70% of economic growth, higher inflation and rates will quickly curtail the ‘reflation’ story.‘

A few months later, the Fed started to talk about tapering their balance sheet purchases.

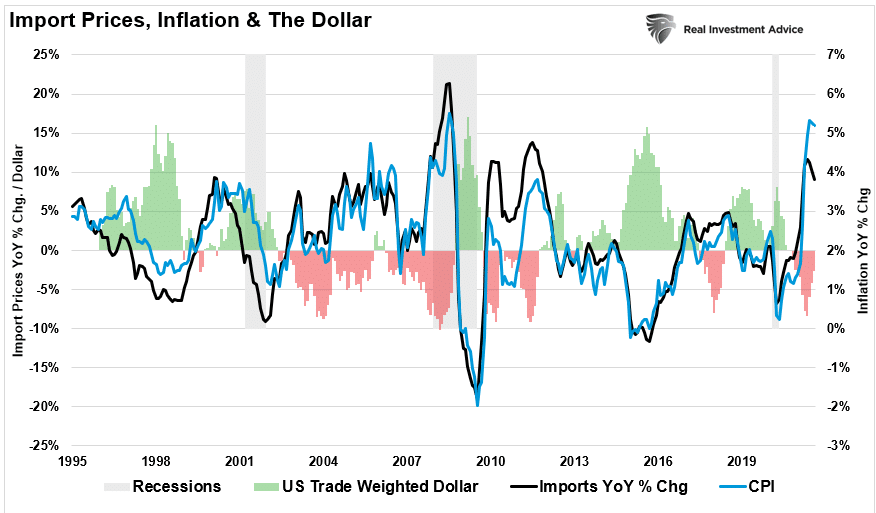

With the market currently priced for perfection, the disappointment of economic growth caused by the rising dollar, interest rates, and a contraction in consumer spending is a significant risk to the market. As shown, the rally in the dollar is already starting to weaken the inflationary impact of higher import prices and suggests a peak in CPI.

The one thing that always trips the market is what no one is paying attention to. For me, that risk lies with the US Dollar. As noted previously, everyone expects the dollar to continue to decline, and the falling dollar has been the tailwind for the emerging market, commodity, and equity risk-on trade.

As noted previously,

“Whatever causes the dollar to reverse will likely bring the equity market down with it.”

The dollar has been rising very quietly, and traders are becoming more aggressively long the dollar trade.

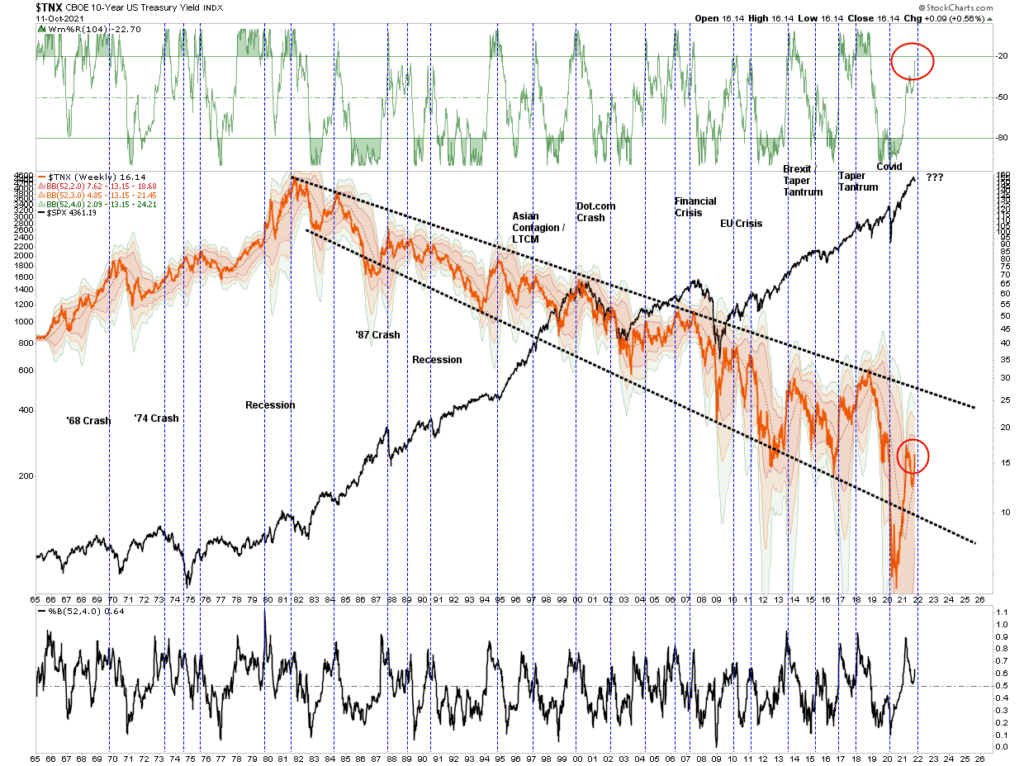

Interest Rate Conundrum

Over the latest several years, I have repeatedly addressed why financial market “experts” remain confounded by rates failing to rise. In March 2019, I wrote: “The Bond Bull Market,” which followed our earlier calls for a sharp drop in rates as the economy slowed.

At that time, the call was a function of the extreme “net-short positioning” in bonds, which suggested a counter-trend rally was likely. Then, in March 2020, unsurprisingly, rates fell to the lowest levels in history as economic growth collapsed. Notably, while the Federal Reserve turned back on the “liquidity pumps,” juicing markets to all-time highs, bonds continue to attract money for “safety” over “risk.”

Recently, “bond bears” have again returned, suggesting rates must rise because of inflationary concerns. However, again, such is unlikely as economic growth is quickly stalling as liquidity runs dry.

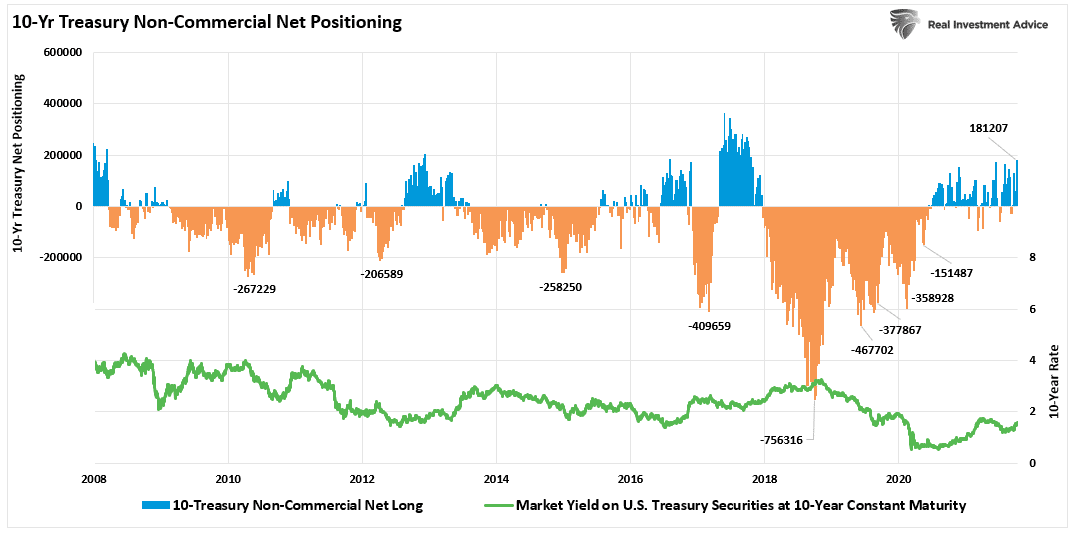

Currently, traders are more aggressively long contracts suggesting rates could still rise a bit further. However, while there is upside to rates, it is likely limited to less than 2% before economic growth gets impacted.

Conclusion

The markets are oversold enough on a short-term basis to rally. However, numerous headwinds are mounting from higher rates, inflation, oil prices, and the dollar. So while traders are piling into inflationary trade, they are likely going to be disappointed.

While the markets can undoubtedly discount these headwinds short-term, they won’t be able to do it indefinitely. Such is why we remain concerned over the weekly and monthly “sell signals,” which are suggestive of increasing risk.

The biggest problem is that technical indicators do not distinguish between a consolidation, a correction, or an outright bear market. As such, if you ignore the signals as they occur, by the time you realize it’s a deep correction, it is too late to do much about it.

I suggest that with our “sell signals” triggered, taking some action could be beneficial.

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

There is minimal risk in “risk management.” In the long term, the results of avoiding periods of severe capital loss will outweigh missed short-term gains.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read