It seems the entirety of the financial media and many on Wall Street believe a “V” shaped economic recovery is in our future. While we hope they are right, we would be foolish to take such analysis and, quite frankly, unwarranted optimism, at face value.

If history teaches us one thing, it is that significant, life-altering events are rarely if ever followed by a quick return to normality. In this article, we raise a few considerations that may make you reconsider popular economic narratives. Today, the importance for investors to think outside of the box cannot be overstated. Or to put it another way, the parameters of “the box” have likely changed and, if so, we should be cognizant of those changes in our decision making.

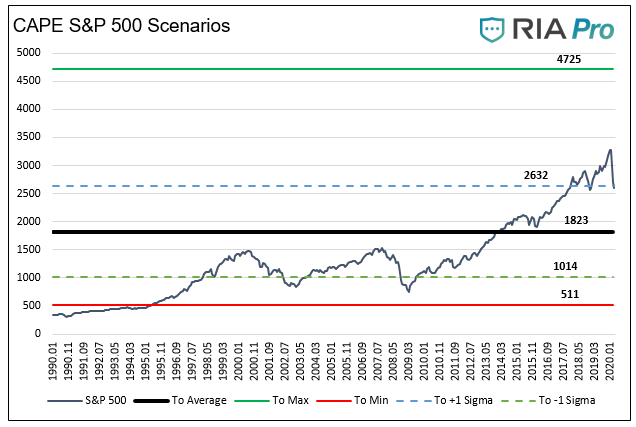

If the future economic recovery does not resemble the “V” shape that the financial markets are depending on, the stock market may be even more over-valued than we think. To that end, consider the following graph showing where the S&P 500 could trade based on a range of historical valuations.

Data Courtesy Shiller

Short Term Prognosis

The COVID-19 Crisis may be short-lived or not. Although it seems as though progress is being made, there is nary a sign that a full-fledged cure or vaccine is at hand. Social distancing and mass closures of commercial enterprise appear to slow the exponential spreading of the virus considerably. While very effective in saving lives, these measures come with immense economic costs. The productive output of the global economy has ground to a near-total halt.

As the virus appears to have peaked in Asia and is starting to show signs of peaking in Europe, we are hopeful the U.S. will also peak shortly. Then what? From a health standpoint, the answer depends on whether a cure or vaccine is discovered.

If a cure or vaccine is found and can be produced, distributed, and administered quickly, then mandatory and self-regulated social distancing will end, and people will hopefully resume normal activities. This may be the rationale backing a “V” shaped recovery, but as we discuss later in the article, normal may not be the same normal we knew before February 2020.

If the spreading of the virus is significantly curtailed, but there is no cure or vaccine developed, the outcome may be very different. Just ask yourself, are you ready to stand in a crowded elevator, hop on a packed train, or stand shoulder to shoulder with other fans at a sporting event or concert? It is quite likely that in the bleaker scenario with no cure or vaccine, there will be some recovery, but most people will dramatically alter their everyday life. Such a change will radically reshape the outlook for human behavior on a vast scale.

As you consider those scenarios, also consider their respective economic impacts. The first scenario, a return to normal with a cure or vaccine, offers a higher probability of bringing about a “V” shaped recovery. We, however, would argue for a “U” shaped recovery as the damage already done is not easy to overcome so quickly. A “U” shaped recovery entails a prolonged period of slow to negligible growth versus a “V’s” sharp reversal higher of growth

We fear that the second, no cure/vaccine scenario will look much more like an “L” shaped stagnation.

Those two scenarios may help guide you in the short run, but left out of the discussion thus far is the long term change to our psyches and the effect it will have on our economic behaviors and decision making.

Long Term

In our daily discussions with neighbors, family, and friends, we are inundated with concern over economic well being. Jobs are at stake, and for the more fortunate, pay cuts are likely. As if those concerns were not enough, most people have seen a sharp decline in the value of their investment portfolios and retirement savings accounts. Almost overnight, many people saw their financial stability weaken dramatically.

The economic and financial concerns brought on by the current day stresses we are harboring will play a big role in the future.

If you have ever known someone that lived through the Great Depression, you probably noticed that their economic and financial behaviors are not what you might consider normal. Regardless of their financial standing, they tend to have considerable savings, of which a good portion resides in non-risky assets or cash. They also seek out the best deals and are never shy to pick up a penny or use a coupon. Some of these people are millionaires, but in many cases, onlookers would not have any clue by looking at their lifestyles.

These survivors learned that money for a rainy day is much more than a cute saying. A common motto during the Depression and one that survived long afterward was “use it up, wear it out, make do or do without.”

The current economic crisis has some similarities to the Great Depression. Still, so far, it pales in comparison as the duration of current hardships is only measured in weeks, not years. The Depression raged on for an entire decade.

The longer this crisis continues, the more likely our economic and financial preferences will change.

This experience will remind us why rainy day funds are so necessary, the value of frugality, and in general, it could put our economic behavior back on par with more historical norms. These norms are not at all primitive as we are re-learning, they are wise, they are prudent, and they are critical.

This experience may not rival the Great Depression in impact, but understand the crisis is reviving valuable lessons that were long forgotten. Many people will rethink their consumption habits and many companies and governments will assess the risks of globalization when this crisis ends. The repercussions will be large.

Summary

The possible changes in our behaviors described above will not only affect the economy but will also change investor behaviors. The longer the crisis rages and the deeper the market declines, the harsher and longer-lasting the lessons that will be imposed by the market. It seems reasonable that buying shares at extreme valuations from companies that perpetually lose money will cease to be a badge of honor. Cash, Treasury Bonds, active investment strategies, and value may all come back into fashion.

Like everyone else, we have no idea what the future holds. The virus may be cured, and life may go on as if nothing happened. If so, great, but that is not the lesson that history teaches.

We would be remiss not to consider at least that the COVID-19 crisis transforms our economic logic. This shift would be healthy but demands a new logic for investing in such an environment.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read