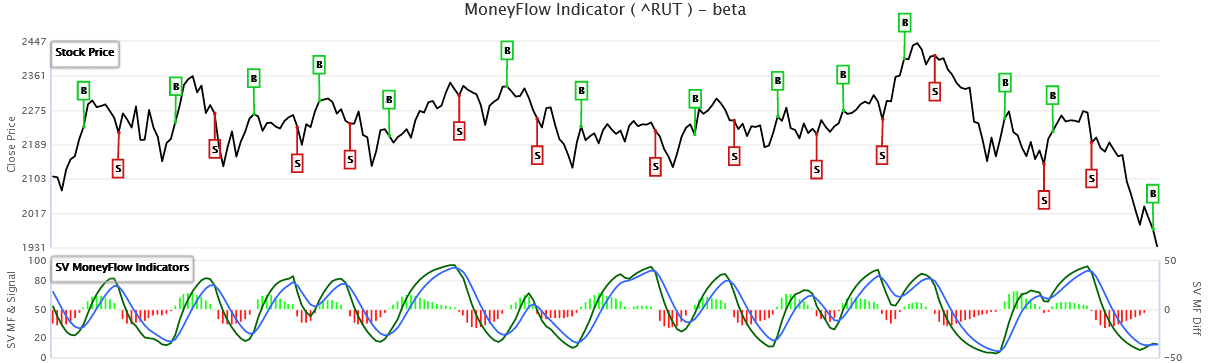

The Russell 2000 Index, a composite of small stocks, closed Thursday down more than 20% below its recent high. A 20% decline typically defines a correction. While the S&P 500, Dow Jones Industrial Average, and NASDAQ, have thus far avoided a correction, many individual stocks in those indices are in a bear market. Per Charles Schwab, 49%, 76%, and 82% of S&P, NASDAQ, and Russell 2000 stocks, respectively, are at least 20% below recent highs. The Russell 2000 tends to be more representative of the broader economy as it is not heavily weighted by large companies. The top graph below from SimpleVisor shows the large decline in the Russell 2000. However, the bottom graph, highlighting our proprietary money flow model, is turning up, signaling the index is oversold and due for a bounce.

What To Watch Today

Economy

- 9:45 a.m. ET: MNI Chicago PMI, January (61.8 expected, 64.3 prior)

- 10:00 a.m. ET: Dallas Fed Manufacturing Activity, January (8.5 expected, 8.1 prior)

Earnings

Pre-market

- Otis WorldWide (OTIS) to report adjusted earnings of $0.69 on revenue of $3.58 billion

Post-market

- NXP Semiconductors (NXPI) to report adjusted earnings of $3.02 on revenue of $3 billion

- Cirrus Logic (CRUS) to report adjusted earnings of $2.13 on revenue of $511 million

Market Update

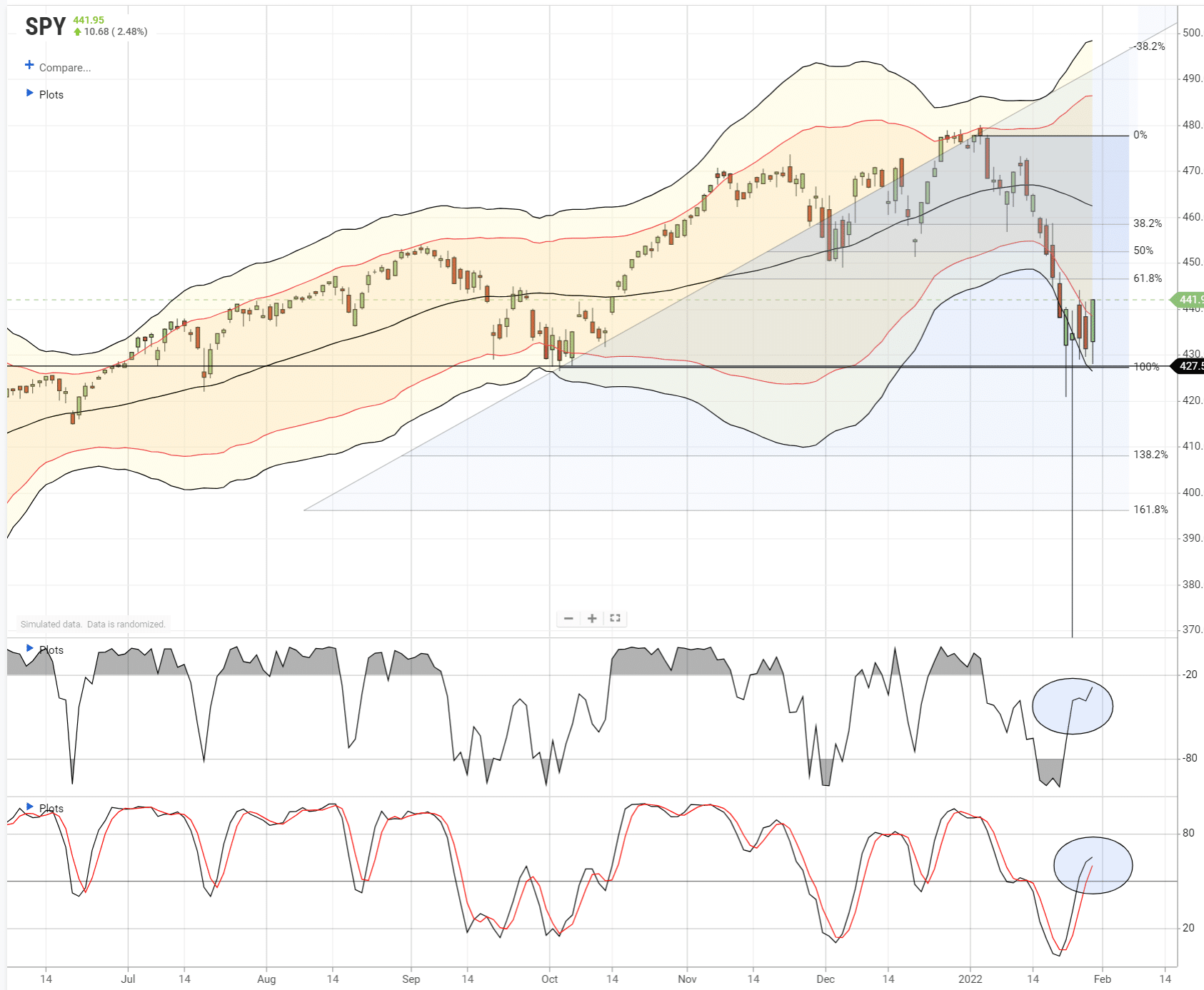

Despite the Fed tightening rhetoric, the market ended the week positively, erasing the week’s losses. The markets do look to be stabilizing, as shown below, and are holding the October lows. That 100% Fibonacci retracement, and multiple rally attempts, triggered a short-term buy signal. All of this is short-term bullish.

While a reflexive rally is very likely, we are starting to use that rally to leg into a short-market hedge and reduce overall equity risk. We are also looking to tilt our portfolio a bit more to the value sector, and away from areas like the Russell 2000. However, we are also maintaining some of our major “growth” stocks which are now profoundly oversold and will benefit from a rise of disinflationary pressures later this year.

The Week Ahead

The labor markets will be of utmost importance in this week’s economic releases. ADP reports on Wednesday, followed by the BLS on Friday. The forecast for both reports is a gain of slightly more than 200k. Given Powell is concerned about the tight labor market and its effect on inflation, the data will be closely followed. On Tuesday, the JOLTS report will update job openings and the quit rate. Both are good measures of labor market tightness.

Tuesday’s ISM report will be interesting following last week’s weaker than expected PMI report. The current expectation is for a slight decline to 58. A level in the mid to lower 50’s may cause investors anxiety as the Fed is tightening policy into a weakening economy.

The earnings calendar is starting to slow, although Google on Tuesday and Facebook (Meta) on Wednesday will be important.

The Fed’s self-imposed media blackout is over. As Fed members get back to the media outlets and podiums, it will be interesting to see if Powell’s comments were in line with most officials or remain on the dovish side. Markets may struggle if many Fed members continue to push for QT at the March meeting as well as selling bonds in addition to allowing maturities to do the Fed’s job.

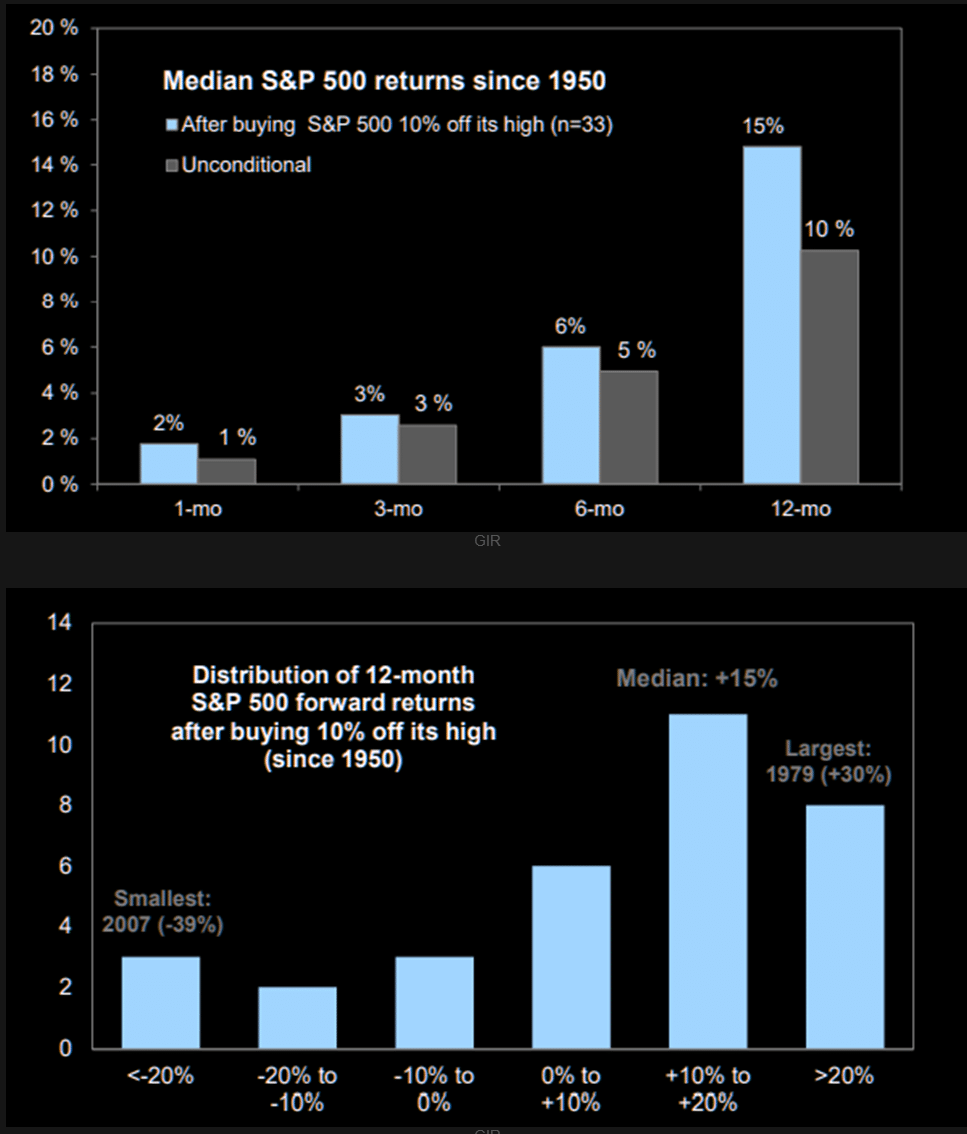

Buy The Dip Has Worked Since 1950, If You Do It Right

Past S&P 500 corrections have typically been buying opportunities. Chart 2 shows the distribution of 12-month S&P 500 returns following 10% declines. – @themarketear

Should I Buy TIPs?

Is it a good time to buy Treasury Inflation-Protected bonds (TIPs)? The answer: it depends on your inflation forecast versus the markets.

TIPs are a bet on the breakeven inflation rate. If actual inflation over the life of a TIP bond is less than the implied breakeven inflation rate when you bought the bond, you will earn a lower total return than you would have made on a nominal Treasury bond with the same maturity. Conversely, the TIP is the better bond if inflation turns out to be more than the breakeven rate.

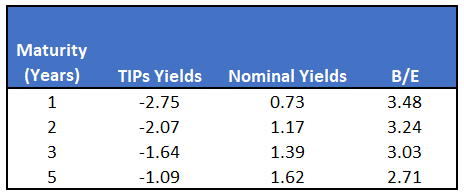

The table below compares current TIP yields and nominal yields over the next five years. The break-even rate is simply the nominal yield less the TIP yield. If you think inflation will run hotter than the breakeven rates below, TIPs are the preferred instrument. Even if your base forecast calls for inflation below the breakeven rate, using TIPs as a hedge against higher than expected inflation can make sense. There are a lot of unusual factors driving high inflation. As such, predicting inflation for the next few years will remain difficult. As part of a diversified portfolio, TIPs can provide a needed inflation hedge even if high inflation is not your forecast.

Stocks on Blockchain

The SEC approved a block-chain powered securities national exchange. The new exchange run by a joint venture called BTSX will allow for more efficient securities settlement, including same-day stock settlement. Currently, it takes two days for a typical stock to settle. The exchange will be open for retail and institutional use. The use of blockchain will make market data more widely available. T-zero, a subsidiary of Overstock (OSTK), is teaming up with BOX Digital Markets in this venture.

A year ago, we wrote Bye Bye Brokers, Hello Blockchain Technology. The article discusses the benefits of a blockchain approach to making securities markets more efficient. To wit:

Tokenizing assets is the act of digitally representing securities, commodities, collateral, future deliveries, and almost everything else on to the blockchain database. Transaction details on these assets reside in a public database for all to see.

Tokenized assets do not require intermediaries to trade or settle securities. Banks and brokers can still play a central role in introducing buyers and sellers and making markets when needed. But the system is not beholden to them.

In a tokenized world, the Lehman default might have been avoided with real-time collateral management and pricing. Scams like Madoff are impossible to perpetrate as regulators can more easily see if there are actual “assets.”

We highly recommend listening to blockchain expert and market veteran Charlie McGarraugh on Smarter Markets for more on tokenizing assets.

Valuations Are Not For the Feint of Heart

David Robertson recently posted the following warning about equity valuations and future returns.

Now is an appropriate time to refresh those warnings, however. Part of the reason is valuations are still shockingly high. Grant’s Interest Rate Observer (December 21, 2021 edition) points out, “At presstime, 83 constituents of the S&P 500 trade at a ratio of enterprise value to revenue of more than ten times.”

As a result, the returns to stocks in general are likely to be terrible. The valuation measure conceived of by John Hussman that most closely correlates with future returns suggests returns of about -6% per year for the next ten years. This is the risk.

We would add one point about Hussman’s measure. Equity valuations typically correct in short periods. As such, the eventual correction will not likely be a series of gradual 6% annual declines for a decade, but a much sharper and shorter decline, ala 2000 or 2008.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read