During my morning routine of caffeine supported information injections, I ran across several articles that just contained generally bad investment advice and poorly formed analysis. Each argument was hinged on the belief that bull markets last indefinitely, bear markets are simply an opportunity to “buy” more, and investing for the long term always works. One such article, in particular, was this gem published at MarketWatch:

“But it’s important to remember that in the grand scheme of things, this sell off is a mere blip.

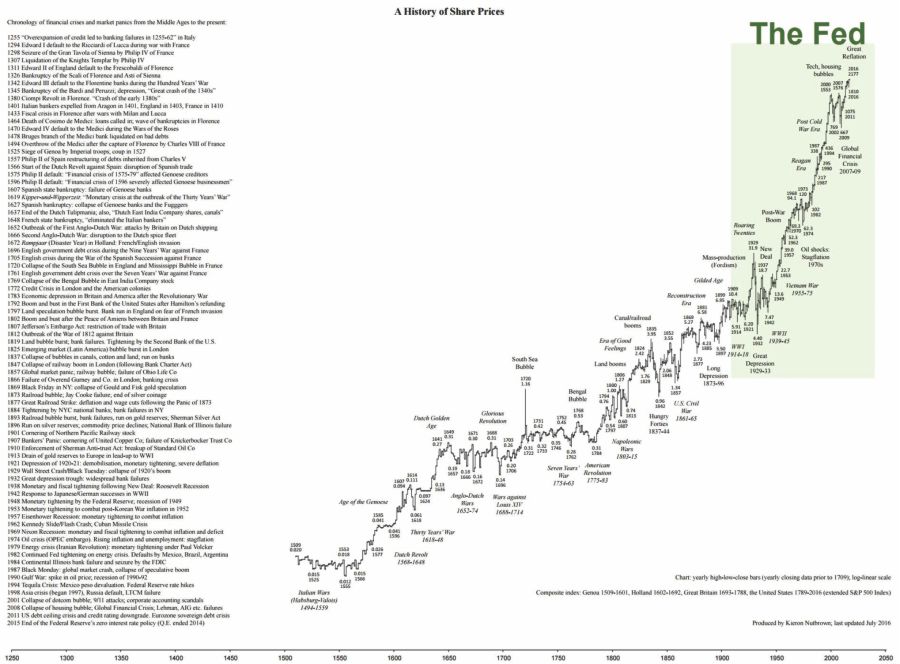

Kieron Nutbrown, former head of global macro fixed income at First State Investments in London, has just the reminder to help investors take a step back and look at things from a long-term perspective.

The chart, which first appeared on his blog, follows the path of global stocks over the past 500 years and demonstrates how prices have fared through wars, revolutions, and depressions.”

See, it is really quite simplistic, just buy the dips.

the 500-year chart of share prices clearly shows that every dip is a buying opportunity pic.twitter.com/1t6oTyHsam

— StockCats (@StockCats) October 19, 2016

Unfortunately, investing doesn’t work that way because this chart ignores both the value and quantity of the one commodity that we can not acquire or create more of – “time.”

While the markets may have recently hit “all-time” highs, for the majority of investors this is not the case. This is because, as I addressed last week, investors tend to do exactly the “opposite” of what they should do when investing. To wit:

“Unfortunately, investors rarely do what is ‘logical,’ but react ’emotionally’ to market swings. When stock prices are rising, instead of questioning when to ‘sell,’ they are instead lured into market peaks. The reverse happens as prices fall. First, comes ‘paralysis,’ then ‘hope’ that losses may be recovered, but eventually ‘capitulation’ sets in as the emotional strain becomes too great and investors ‘dump’ shares at any price to preserve what capital they have left. They then remain out of the market as prices rise only to ‘jump back in’ about mid-way to the next market peak. Wash. Rinse. Repeat.”

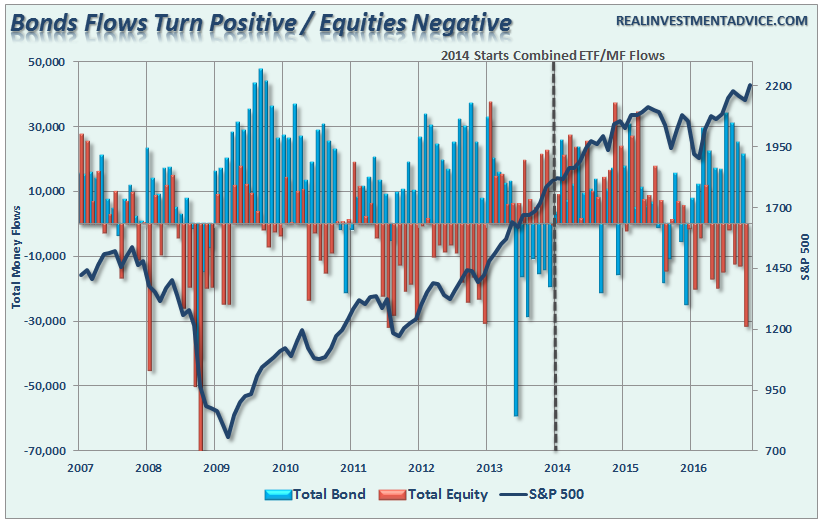

This is shown in the flows of money into bonds/equities by investors according to the research from ICI. (Note: Beginning in 2014, ICI began reporting on ETF fund flows which have been included into the cumulative.)

Despite the rally to all-time highs, flows into equities continue to remain negative. While November’s data has not been fully released yet, it will be interesting to see if the spike in interest rates has done much to change the net cumulative flows into bonds vs. equities.

However, the problem for far too many Americans today is that time will run out for them as they are faced with tough retirement choices and being forced to work far longer than any of them ever planned.

Amazingly, after two major bear market reversions, individuals still place too much faith on predictions of future outcomes when it comes to their savings, and more importantly, their retirement.

While looking at a 500-year history of the markets is certainly interesting, it is the reality that most investors have far less life-span than that.

In order to be truly successful over the long term, and this is especially important if you are close to your retirement date, a focus on 1) capital preservation and 2) returns at a rate to offset inflationary pressures are the most critical.

The second part of that statement is the most important. Just as the problem with pension funds continues to prove, trying to use financial markets to offset a lack of savings has consistently turned out badly. People that try to build wealth by investing, rather than saving, tend to lose more often than not as they inherently take on excessive risk trying to “beat the market.”

What has been lost in recent years is the financial markets are a tool to make sure that your “savings” maintain their future purchasing power parity. In other words, your savings are adjusted for inflation over time.

If you truly have 30 years to be invested before you retire, then you can ignore this article, buy a stock market index fund, stick money in it every month and most likely you will be fine.

However, if you are like me, and the millions of other Americans who are within 10-15 years to retirement, we don’t have the luxury of time on our side. Therefore, sudden market losses can be devastating to long term financial sustainability in retirement.

Hopes Vs Reality

While we all “hope” that markets will provide a positive net impact on our long-term goals, there are several issues that individuals must understand. The first, is while markets have risen over time, the markets spend roughly 95% of their time making up for previous losses. The chart below shows this fairly clearly.

Secondly, exactly how much time do individuals really have? While it certainly sounds charming that “youngsters” are throwing their money into the Wall Street casino, the reality is this is hardly the case. Youngsters rarely have sufficient levels of investible savings to actually invest. Between starting a career, raising a family and maintaining their specific standard of living there is rarely little remaining to be “saved.” (Read this)

For most, it is not until the late 30’s or early 40’s that individuals are earning enough money to begin to save aggressively for retirement. More importantly, it takes even longer before they “save” enough investible capital to actually make investing work for them after fees, expenses and taxes.

Therefore, by the time most achieve a level of income and stability to begin actually saving and investing for retirement – they have, on average, about 40 years of investable time horizon before they expire. Unfortunately, that is only about 460 years short of the first chart in achieving those rates of return.

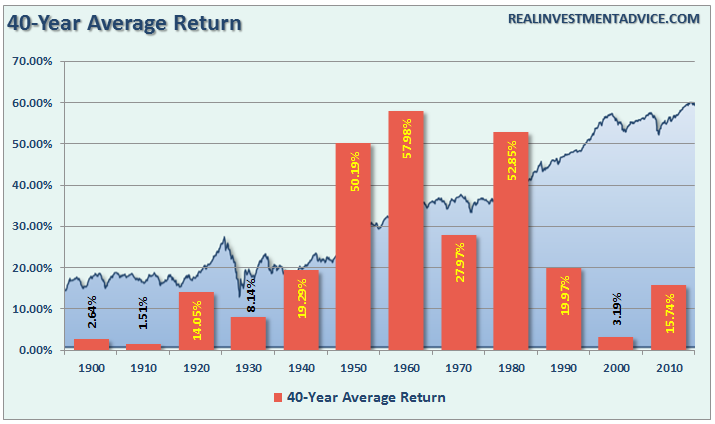

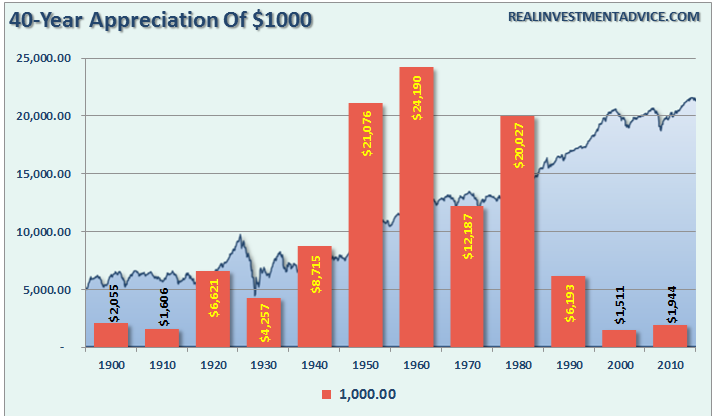

I have prepared two different charts to show you the impact of investing over a 40-year time span. I used an initial investment of $1000 at the beginning of each decade and analyzed the capital appreciation for the ensuing 40 year period. In this regard, we can garner a clearer picture about the impact of both secular bull and bear market cycles on the total investment returns. [Note: The data below uses Shiller’s price data on a nominal basis and is based on monthly capital appreciation only.]

The first chart shows the average annual return for each starting decade.

The next chart shows the capital appreciation of a $1000 initial investment.

Importantly, the major difference on the ending result depends greatly on “WHEN” you start investing. If you started investing during the 50’s and 60’s then you were lucky enough to capture the raging “bull market” of the 80’s and 90’s which offset the secular bear market of the 70’s. However, if it started in 1990, so far, results haven’t been all that great as the secular bear market of the 21st century has slowly chipped away at the gains of the 90’s.

One very important thing to be noted here, which I discussed in “Yes, You Should Worry About Corrections,” is valuations have been a key driver of these 40-year cycles. The best 40-year returns came from when the starting point in valuations was below 10x trailing reported earnings. Today, at over 20x trailing reported earnings (the only valuation measure that is historically consistent), it suggests that returns in the years ahead will likely be substandard.

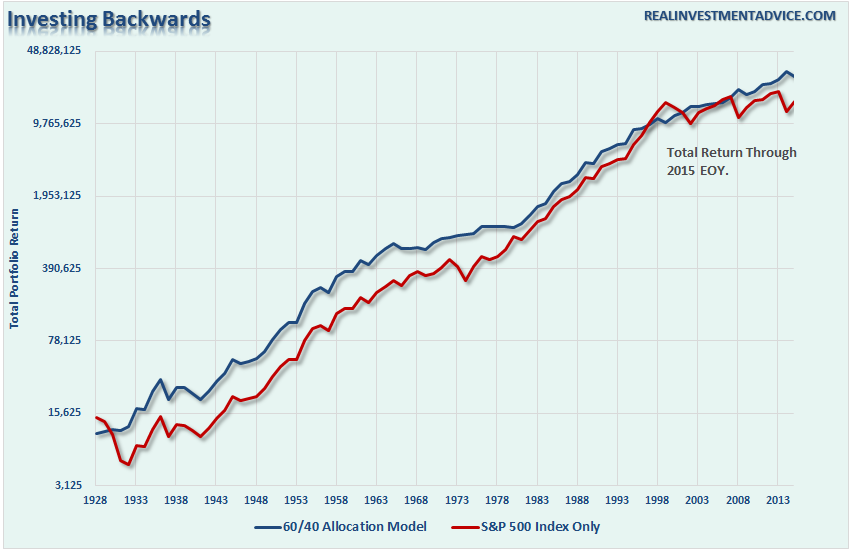

So, what if we “invest backward?”

What would portfolio returns look like if stocks were bought when trailing valuations were at 7x earnings, or less, and then the portfolio was fully rotated into bonds whenever trailing valuations exceed 25x or more. While this is what we should do as investors, it is completely backward to what is espoused in the mainstream media.

The chart below is a $10,000 investment invested into a switching strategy versus the total return S&P 500 index.

As you can see, the returns over the VERY long term investment horizon closely correlate with the total return of the S&P 500 without the downside volatility risk during major market reversions. (Again, however, you likely died at least twice along the way)

While this is an extreme example, and not something I would recommend, the point to be made is the incessantly bullish commentary is not necessarily in your best interest due to the following:

1) You don’t have 86 years to invest

2) The accumulation phase of portfolios is generally much shorter than the distribution phase, particularly now as average life expectancy creeps ever closer to 100.

3) The returns actually received by investors are far lower due to inflation, taxes, and expenses.

4) Returns are diminished further due to investor behaviors such as “chasing returns” and “panic selling.”

With forward returns likely to be lower and more volatile than what was witnessed in the 80-90’s, the need for a more conservative allocation model is rising. Controlling risk, reducing emotional investment mistakes and limiting the destruction of investment capital will likely be the real formula for investment success in the decade ahead.

This brings up some very important investment guidelines that I have learned over the last 30 years.

- Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel” you should be doing.

- The ONLY investments that you can “buy and hold”are those that provide an income stream with a return of principal function.

- Market valuations (except at extremes) are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short term trading. Knowing what type of investor you are determines the basis of your strategy.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

As an investment manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long term capital appreciation will take of itself.

But one thing I absolutely know for sure – you aren’t going to live for 500-years.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read