The First Trillion is Always the Hardest- Analyzing Apple Mania

“Fundamentals might be good for the first third or first 50 or 60 percent of a move, but the last third of a great bull market is typically a blow-off, where the mania runs wild and prices go parabolic.” – Paul Tudor Jones

From 1976 when Apple (AAPL) began in Steve Jobs’s garage to 2019, its worth rose to $1 trillion. Subsequently, from March 20, 2020, the trough of the COVID market crash, to today, the value increased by another $1 trillion. Over 44 years to hit the first trillion, and less than half a year for the second. Apple is up 240% from the March lows.

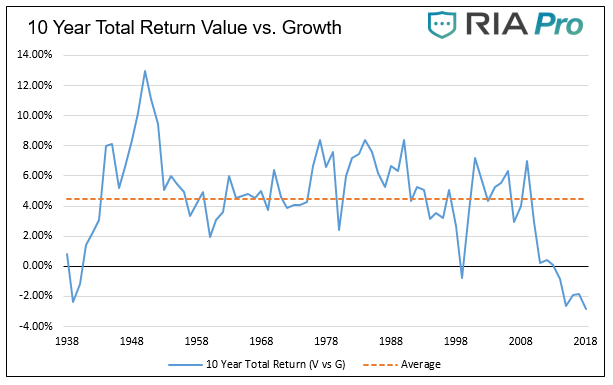

We consider ourselves value investors. That means we prefer to invest in companies that are “underpriced.” Over time, this strategy typically translates into better than market returns and a margin of safety. In our view, it offers a better risk/return profile. The graph below shows the value of this strategy over the last 80 years.

We own Apple, yet fully admit it is anything but a value investment. This article provides the opportunity to discuss Apple’s valuation and current market conditions that lead value investors, like ourselves, to own a very expensive company like Apple.

We own Apple, yet fully admit it is anything but a value investment. This article provides the opportunity to discuss Apple’s valuation and current market conditions that lead value investors, like ourselves, to own a very expensive company like Apple.

Apple Mania Running Wild

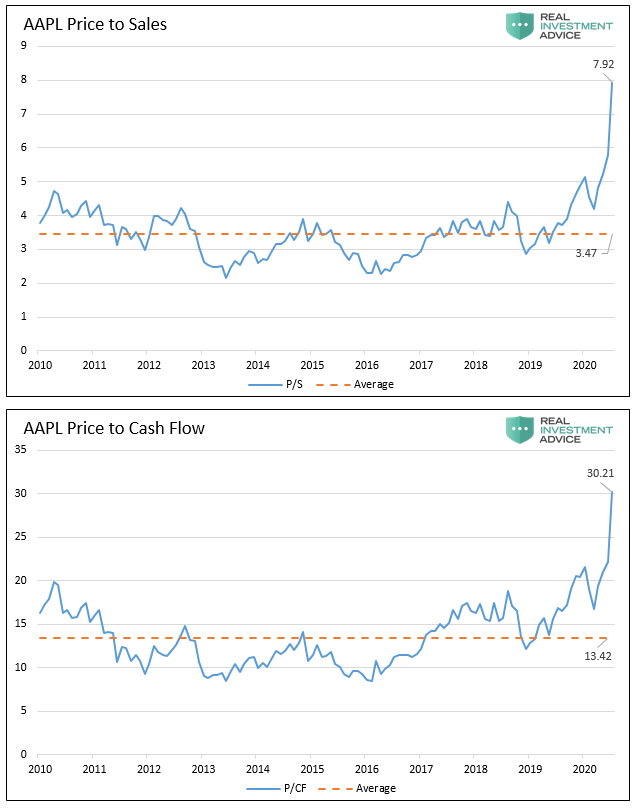

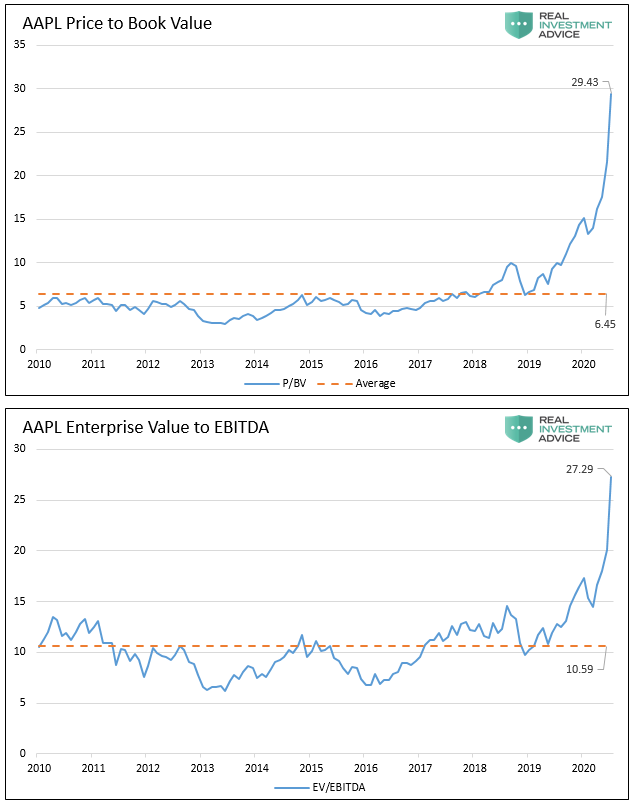

Is Apple worth $1 trillion, let alone the recently added second trillion? To answer this question, we share some well-followed valuation ratios and financial trends. The orange dotted line in each graph is its respective ten-year average.

As shown, valuation ratios are more than double their ten-year averages. Without any doubt, Apple is expensive using these historically reliable techniques.

As shown, valuation ratios are more than double their ten-year averages. Without any doubt, Apple is expensive using these historically reliable techniques.

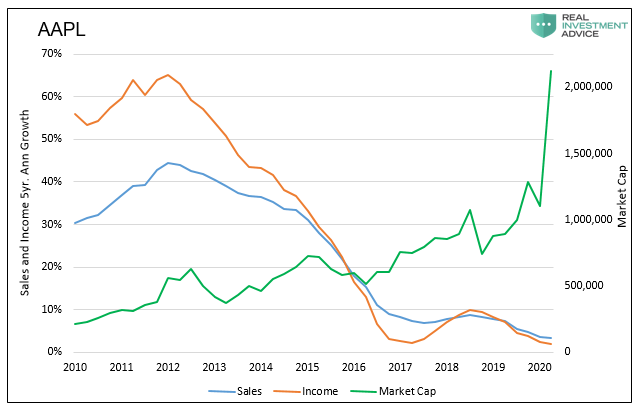

The disconnect between fundamentals and market cap, shown below, explains why valuation ratios are soaring.

Over the last ten years, sales and income growth have slowed considerably. Sales over the previous five years have grown by 3.22% per year, while income by 1.82%. Despite the troubling trends, the stock has nearly quintupled since 2015.

Over the last ten years, sales and income growth have slowed considerably. Sales over the previous five years have grown by 3.22% per year, while income by 1.82%. Despite the troubling trends, the stock has nearly quintupled since 2015.

What’s Apple Worth?

We employ two internally built cash flow models to help us assess Apple’s value.

Model #1 – Our first model uses the present value of 30 years of projected earnings for comparison to the current market cap. We assume a forward 5% income growth rate, which is faster than the 3% rate of the last five years.

Model #1, using a generous income assumption, values Apple’s current stock price at a 58% premium to its future cash flows. This model tends to agree with the ratios shown above.

Model #2 – Our second model uses forecasted cash flows instead of net earnings and similar assumptions as our first model. Model #2 is more friendly but still puts the current stock price at a nearly 15% premium to its valuation.

Why A Value Investor Owns Apple

So, why do we own such an expensive company?

Weak growth trends, expensive valuations, and our models are all meaningless if one thinks Apple can grow earnings at much faster rates. For instance, in our first model, Apple is fairly valued if it can grow net income at 9%.

That is not the reason we own Apple.

Here is a hint: “The equity market has traded soft under the surface of the headline indices, which are now being driven by just one stock—Apple.” Morgan Stanley

The passive nature of the market compels us to own it. To better understand the effect that passive investing is having on all types of investors, we suggest reading our article, Passive Fingerprints Are All Over This Crazy Market.

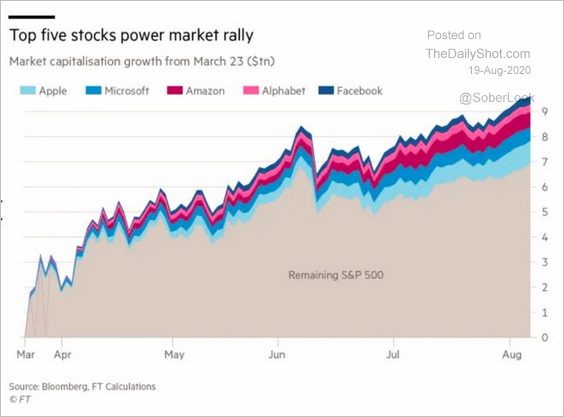

The market is putting a proverbial gun to our head and other investors. It whispers in our ears; if you want to keep up with your benchmark, you must own the “Big 5.” (Apple, Microsoft, Amazon, Google, and Facebook) Failing to hold some or all of them guarantees you will underperform. Those five companies account for 26% of the S&P 500.

As we wrote in Bulls Chant Into A Megaphone:

“What investors are missing is that the top-5 stocks are distorting the movements in the overall index.

For each $1 put into each of those top-5 stocks, the impact on the index is the same as putting $1 into each of the bottom 394 stocks. Such is clearly not a true representation of either the market or the economy.”

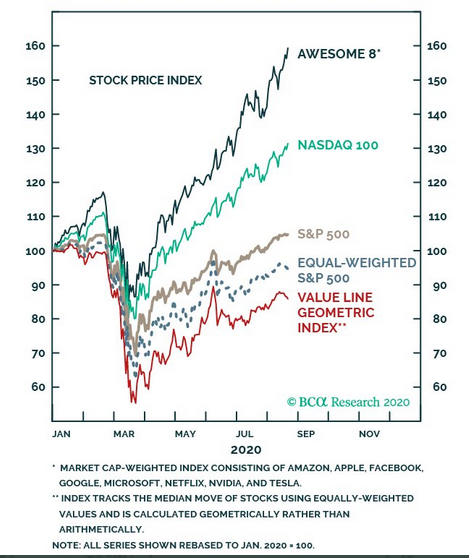

The graph below tells another version of the same story, the “Awesome 8.” This slightly expanded list of companies has also grossly outpaced the “market.”

We own Apple and some of the others listed above. We have done very well in them allowing us to keep pace with the market. However, we fully understand the gains are not commensurate with underlying fundamentals.

Managing Risk

We do not take Apple’s high price and precarious valuations for granted. There is little doubt that over time they regress to the norm, barring substantial growth. At some point, Apple investors will get burnt.

To properly manage risk and sleep well at night, we establish tight stop limits. Further, we frequently take profits and reduce exposure when Apple becomes technically overextended.

For example, we are currently holding only half our original position as the price is extended by three standard deviations. Typically such an aberration results in a pullback or at least a consolidation.

Summary

There is little doubt that we are in the mania stage of the bull market. In this phase, value is grossly underperforming growth. To keep up, we are accepting of the risks embedded in expensive stocks such as Apple. We do this, however, with full knowledge of the risks and employ tactical risk management strategies.

We look forward to a day when we can own a portfolio of value stocks. When we can buy and sell securities based on economic and fundamental reasoning. When the irrationality of mania does not impinge upon our strategies.

We believe there will be a day when we can scoop up Apple shares for fractions of the current cost and possibly when it is once again a value. Admittedly though, the price of Apple as a value play is well below where it is today.

We leave you with an age-old question- is this time different?

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read