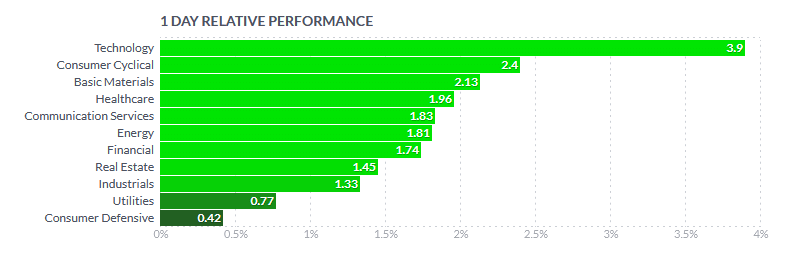

Technology stocks led the markets higher on Tuesday. With little news on the tape, it appears investors are downgrading the risks that the Omicron variant will significantly impede economic activity. The Finviz table below highlights the dominance of technology stocks in yesterday’s trading. Microsoft, Apple, and Nvidia, up 2.7%, 3.8%, and 8.0%, respectively, accounting for nearly 50% of the technology ETF XLK, led the charge. Overall market breadth improved, with all major stock indices and sectors showing decent returns. 80% of NYSE, AMEX, and NASDAQ stocks were higher on the day.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage applications, week ended Dec. 3 (-7.2% during prior week)

- 10:00 a.m. ET: JOLTS Job openings, October (10.5 million expected, 10.438 million in September)

Earnings

- 4:05 p.m. ET: GameStop (GME) to report adjusted losses of 52 cents on revenue of $1.19 billion

- 4:05 p.m. ET: Rent the Runway (RENT) to report adjusted losses of 84 cents on revenue of $53.53 million

- 4:05 p.m. ET: RH (RH) to report adjusted earnings of $6.56 on revenue of $982.14 million

Portfolio Changes

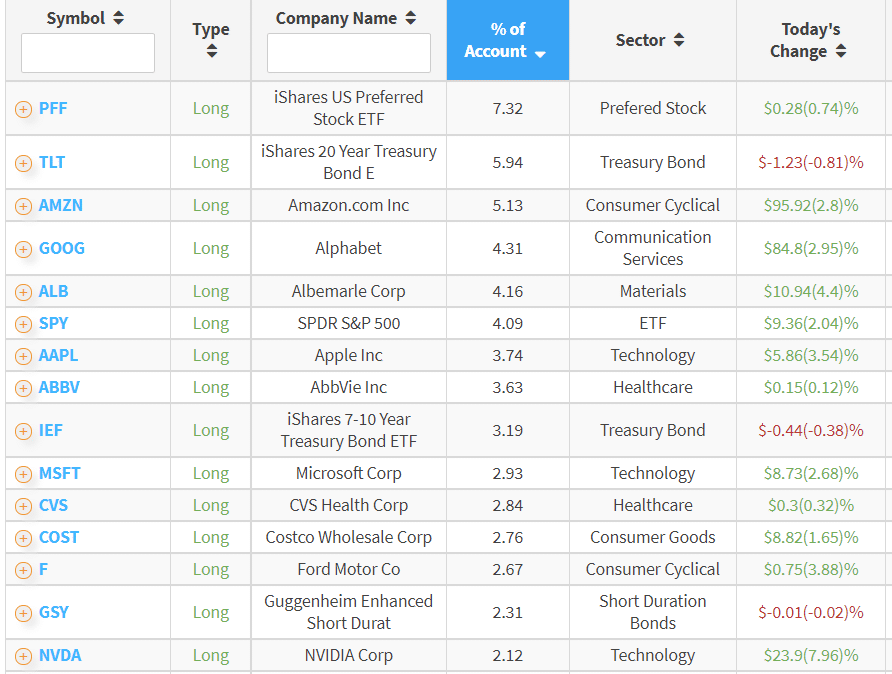

We started discussing last week that we were adding exposure to portfolios in anticipation of an oversold rally. We started by adding an S&P 500 index as a trading position, and then opportunistically added to our existing portfolio positions of MSFT, NVDA, AMD, RTX, and others. Such brought our current equity exposure up to full target weightings currently, and our further increases would lead to an overweight of equity holdings. We will likely further add to our Technology stocks.

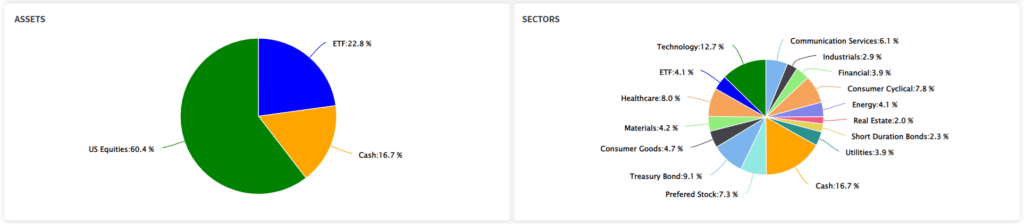

Our Top Holdings (60/40 Allocation)

Profit Margin Pressures Are Coming

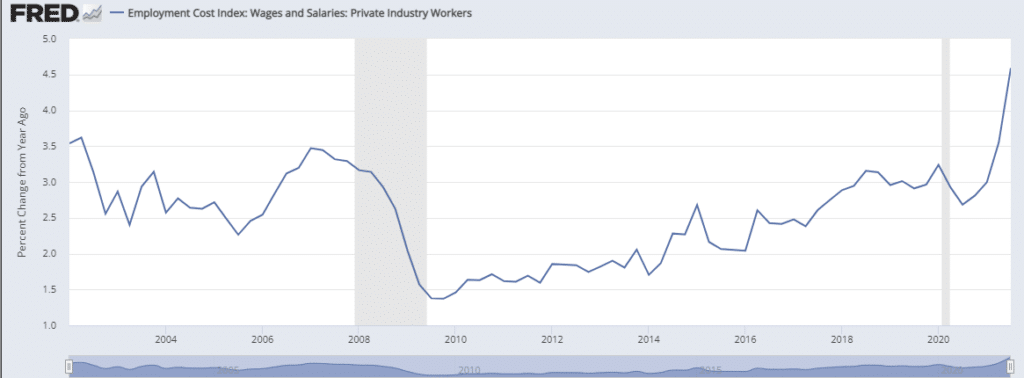

Unit labor costs rose 9.6%, year over year, in part due to productivity, which fell 5.2% over the same period. Hourly compensation rose 3.9%. While wage growth is higher than average, it is well below the inflation rate. The decline in productivity is the largest since 1960. Surging labor costs and falling productivity is a recipe for profit margin compression for many corporations. Given margins are at historically high levels, a decline should not be a surprise.

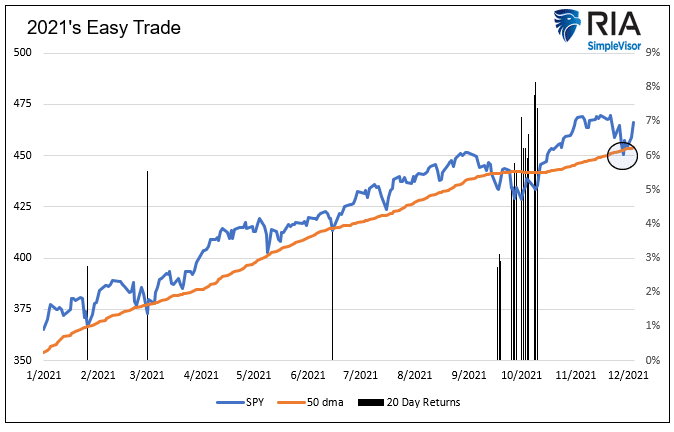

Easy Money- “Buying The 50”

The graph below shows how the S&P 500 (SPY) has repeatedly bounced off its 50dma in 2021. The black bars quantify the 20-day returns from each trading day SPY was below its 50 dma. As we show, buying below the 50 dma and holding for 20 days has been easy money. On December 1st, as circled, SPY fell below its 50 dma. It has since rebounded 3.5% from that day. “Buying the 50” is a great trade and may continue to work well; however, there will come a time SPY breaks below the 50 dma and fails to recover quickly. That could be a signal the market environment is turning.

Market Rebound Continues

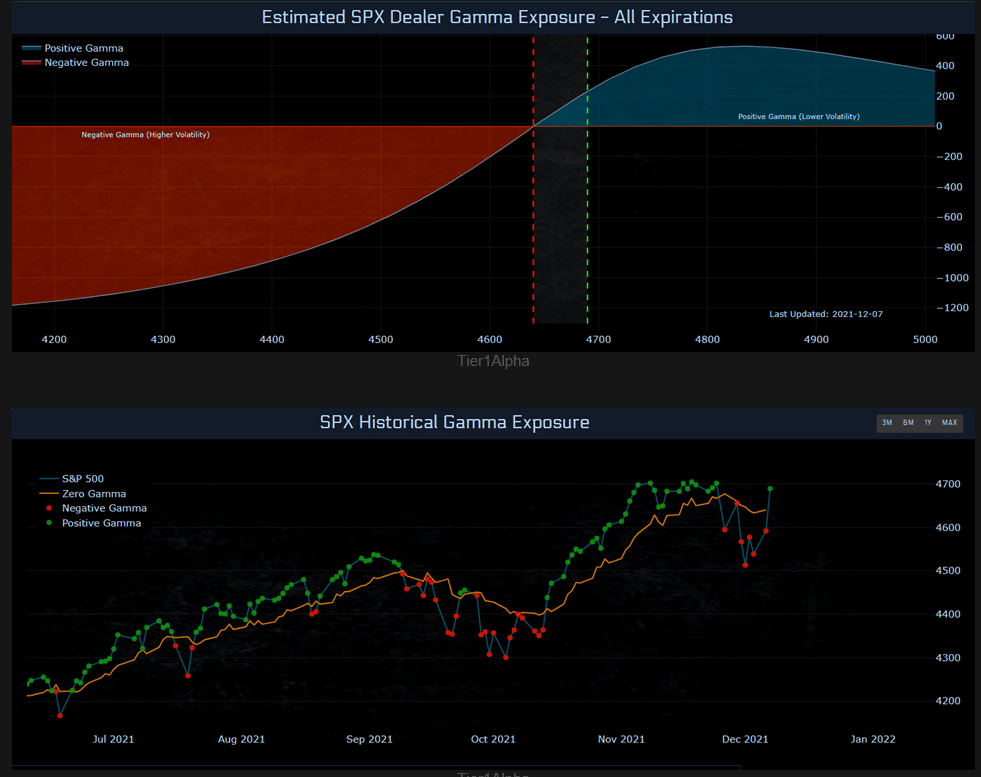

Long-Gamma Leading The Charge

“SPX has flipped into long gamma, but dealers are still in shock and have spent much of the past 24 hours chasing everything higher. Recall, while market was in short gamma, these dealers were busy puking deltas at lows. Despite the market now in long gamma, there has been a lot of delta chasing as all those sold deltas had to be bought back (backlog).

“Moves have picked up. Add to it imploding market depth, as well as the overall dealer gamma picture and you understand why things have been slightly chaotic. Recall, all of these factors work both ways…” This is exactly what is going…The biggest irony and frustration would be to see this market settle down in long gamma land with diminishing moves going forward. That would further suppress volatility as dealers were short gamma during the puke and are now in long gamma territory again.” – @themarketear.

But don’t forget about the risks.

Despite the brutal short squeeze mostly in Technology stocks, there are risks to consider going forward.

- Volatility remains huge, both ways.

- Op-Ex and Fed next week

- CTA deleveraging “sell triggers” will remain “proximate enough” to spot after this imminent covering squeeze tuckers-out

- Skew stays completely “jacked up” and stress-y

- US inflation prints are not expected to peak until 1Q21, it is highly probable that “Fed Put” strike is now much lower

Maybe this market needs to thread water and sober up before any new meaningful direction can take place…

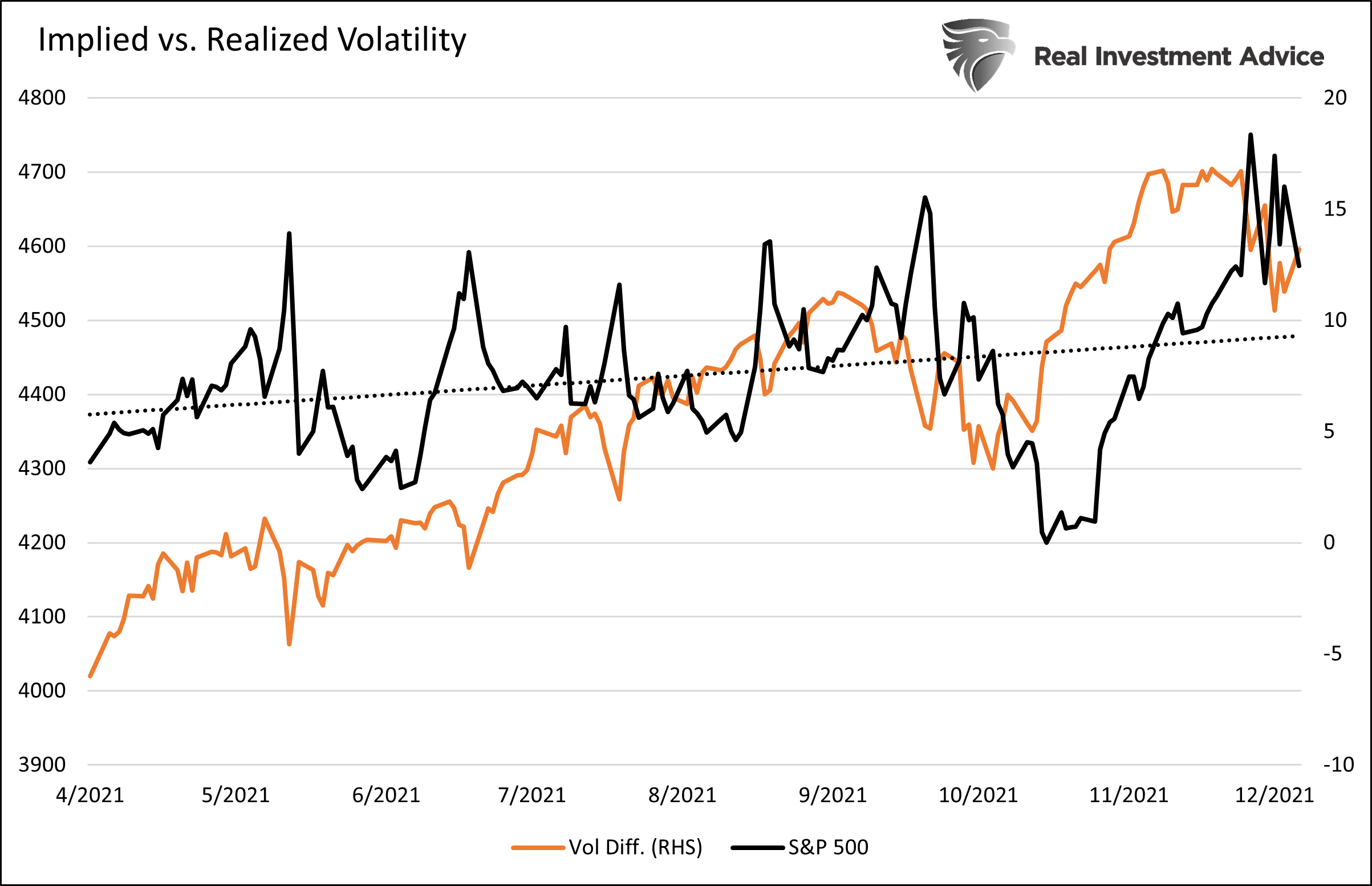

What is Volatility Telling Us?

The black line below charts the difference between implied volatility (VIX) and realized volatility. We use this measure to help us quantify how risk tolerances are changing for the market in aggregate. The difference between implied and realized volatility is frequently above zero, so we prefer to key on the variance around its trend line to assess. When implied volatility spikes above the trend line, it signals that investors are becoming more risk-averse as they bid up options. This is what happened last week as the difference rose to 8-month highs. The large difference has since come down but remains elevated. Also of note, the trend for the differential is gently rising, meaning investor risk-averseness is slowly increasing with the market. Given high valuations and the Fed pivot, the upward trend makes sense.

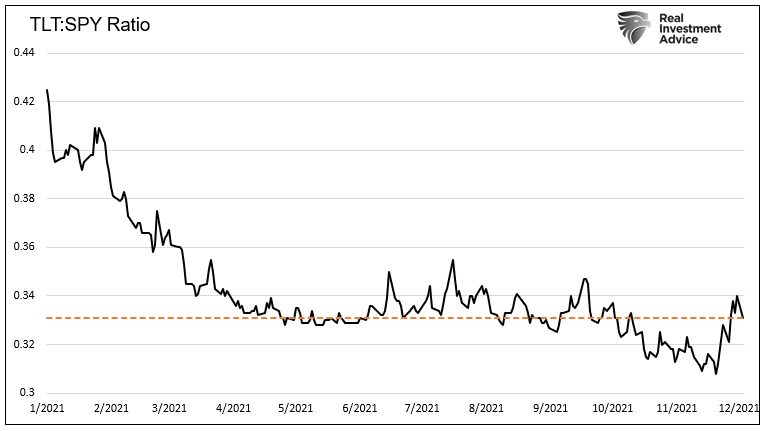

Bonds vs. Stocks

Based on the hoopla surrounding the bullish stock market one would think bonds would have been a bad place to be invested. Contrary to popular opinion, long-duration Treasury bonds (TLT) have kept up with the S&P 500 since April. The graph below shows the price ratio between TLT and SPY. The recent increase in the price of TLT and the decline of SPY have brought the ratio back to April’s levels.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read