This report will now be released on Mondays so we can capture the full trading week (Monday through Friday).

Relative Value Graphs

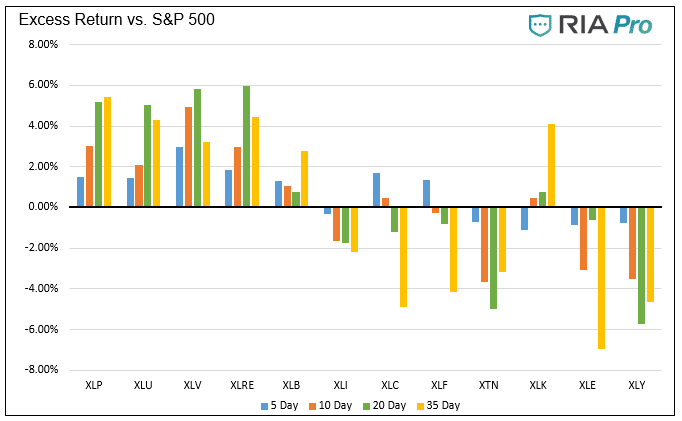

- Accompanying the quick sector rotations in the markets over the past few weeks, are significant weekly changes in our relative sector scores. To this point, technology’s score fell sharply due to the weakness of its generals – Apple, Microsoft, and NVDA. Conversely, the lower beta, higher dividend sectors saw sharp improvements in their scores. These include real estate, utilities, staples, and healthcare. Those same four sectors account for four of the top five performing sectors over the last 35 trading days, as shown in the third graph.

- The inflation-deflation rotation has been the main story this year. Since mid-October, deflationary sectors have beat inflationary sectors by over 10%. More recently, it appears value and dividend stocks are among the best performers. 2022 may shape up to be rotations between value/dividend and growth. Given year-end window dressing, tax related trading, and mutual fund rebalancing, we will wait to hold judgment on which rotations may play a prominent role in 2022.

- The scatter plot in the lower right of the first graph shows a robust statistical correlation (R2=.86) between our scores and relative performance. This means that our scores have recently been good predictors of relative performance.

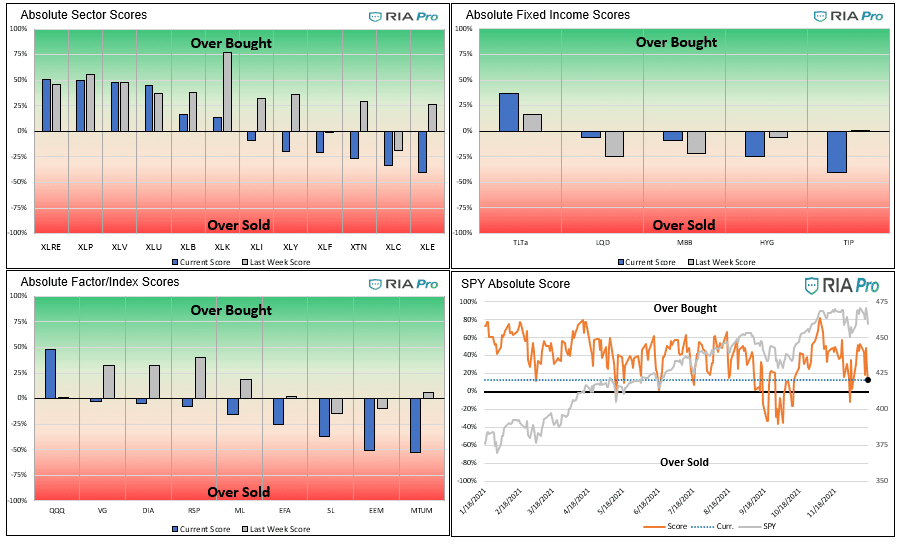

- Momentum is now grossly oversold, which is not surprising given its holdings. Microsoft, NVIDIA, and Tesla currently make up its top three holdings. As shown in the absolute section, MTUM has the lowest score. We may see broad improvement in the ETF next week. However, the ETF changes holdings frequently, so those stocks accounting for its weakness may have less weighting and not contribute as much if they recover.

- Foreign markets, both developed and emerging, continue to register poor relative scores. The U.S. economy is generally stronger than most foreign economies, and inflation is higher in the U.S., leading to a more hawkish Fed and ultimately an appreciating dollar.

Absolute Value Graphs

- The absolute and relative graphs tell similar stories, with safety, lower beta, and high dividends leading the way.

- Except for the NASDAQ, QQQ, all factors and indexes are oversold. The S&P 500, bottom right graph, is at relatively low levels, but it is still above zero and therefore in overbought territory.

- Staples are trading at 2.5 standard deviations above its 200 dma. It may continue to run higher through the remainder of the year, but we suspect it will consolidate or give back some gains once we enter 2022. Emerging markets are over two standard deviations oversold versus its 50 and 200-dmas. Due to dollar appreciation and global macroeconomic conditions, we remain wary of the sector.

- Long government bonds (TLT) remain the most overbought fixed income sector on a relative basis and absolute basis. With the Fed actively fighting inflation by tapering QE and expected rate hikes, we might see the sector continue to be the best performing bond sector.

Users Guide

The technical value scorecard report is one of many tools we use to manage our portfolios. This report may send a strong buy or sell signal, but we may not take action if other research and models do not affirm it.

The score is a percentage of the maximum score based on a series of weighted technical indicators for the last 200 trading days. Assets with scores over or under +/-70% are likely to either consolidate or change the trend. When the scatter plot in the sector graphs has an R-squared greater than .60, the signals are more reliable.

The first set of four graphs below are relative value-based, meaning the technical analysis is based on the ratio of the asset to its benchmark. The second set of graphs is computed solely on the price of the asset. At times we present “Sector spaghetti graphs,” which compare momentum and our score over time to provide further current and historical indications of strength or weakness. The square at the end of each squiggle is the current reading. The top right corner is the most bullish, while the bottom left corner is the most bearish.

The ETFs used in the model are as follows:

- Staples XLP

- Utilities XLU

- Health Care XLV

- Real Estate XLRE

- Materials XLB

- Industrials XLI

- Communications XLC

- Banking XLF

- Transportation XTN

- Energy XLE

- Discretionary XLY

- S&P 500 SPY

- Value IVE

- Growth IVW

- Small Cap SLY

- Mid Cap MDY

- Momentum MTUM

- Equal Weighted S&P 500 RSP

- NASDAQ QQQ

- Dow Jones DIA

- Emerg. Markets EEM

- Foreign Markets EFA

- IG Corp Bonds LQD

- High Yield Bonds HYG

- Long Tsy Bonds TLT

- Med Term Tsy IEI

- Mortgages MBB

- Inflation TIP

- Inflation Index- XLB, XLE, XLF, and Value (IVE)

- Deflation Index- XLP, XLU, XLK, and Growth (IWE)

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read