The Technical Value Scorecard Report uses 6-technical readings to score and gauge which sectors, factors, indexes, and bond classes are overbought or oversold. We present the data on a relative basis (versus the assets benchmark) and on an absolute stand-alone basis. You can find more detail on the model and the specific tickers below the charts.

Commentary 1-15-21

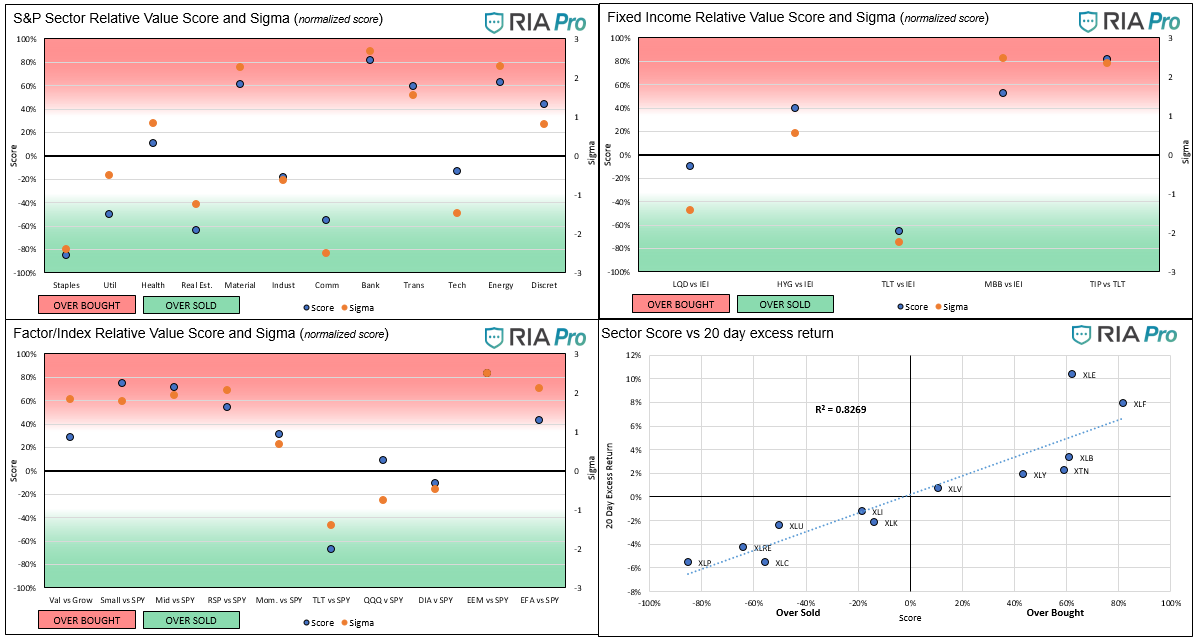

- The banking sector (XLF) remains the most overbought sector on a relative basis, closely followed by energy and materials. Again, more inflation and a resulting steeper yield curve will boost earnings for most companies in those sectors. The risk is that the deflationary trend of the last decade rears its head. On the flip side of the reflation trade are staples, real estate, and utilities.

- The communications sector traded about 3% weaker than the S&P 500 last week. Google and Facebook represent 40% of the sector. Recent censorship actions they have taken and the potential repercussions weighed on those stocks and given their huge weighting, the entire sector.

- This analysis provides what appears to be a clear road map for the weeks and months ahead. Tracking TIP breakevens, Treasury yields, the U.S. dollar, and the inflation/deflation mindset over the coming months should help dictate if current trends continue or not.

- Small-cap and mid-cap, along with emerging markets are the most overbought indexes. Emerging markets benefit from a weaker dollar and inflation as many emerging economies are commodity producers. RSP, the equal-weighted S&P 500, is now well overbought versus the S&P 500. This is in large part due to the outperformance of smaller companies and the relatively weak performance of the FANG stocks.

- The correlation graph in the lower right of the sector graph remains very high. As such, if you think the inflation trade stays in vogue, those sectors and indexes with high scores and sigmas should continue to do well on a relative basis, and vice versa.

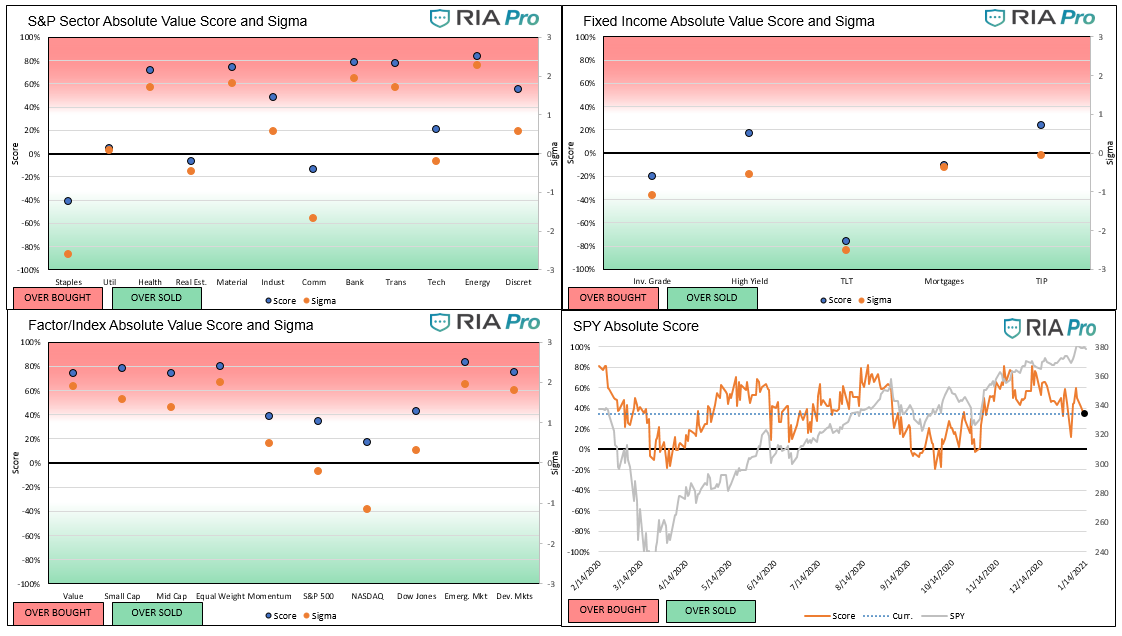

- The broad themes are very similar in the absolute graphs. Energy, transports, banks, materials, health care, small/mid caps, and emerging/ developed foreign markets are extremely overbought. The NASDAQ remains the weakest index for a second week. If we think the reflation trade reverses and the markets fall, it is not implausible to think of the tech sector as a safety trade, similar to the way utilities and staples traditional act in down markets.

- The S&P, like the NASDAQ, is near fair value on an absolute basis.

- Energy, small cap, and emerging markets are above two standard deviations over their 50 dma and 200 dma respectively. Communications and staples are close to two standard deviations below their 20 dma.

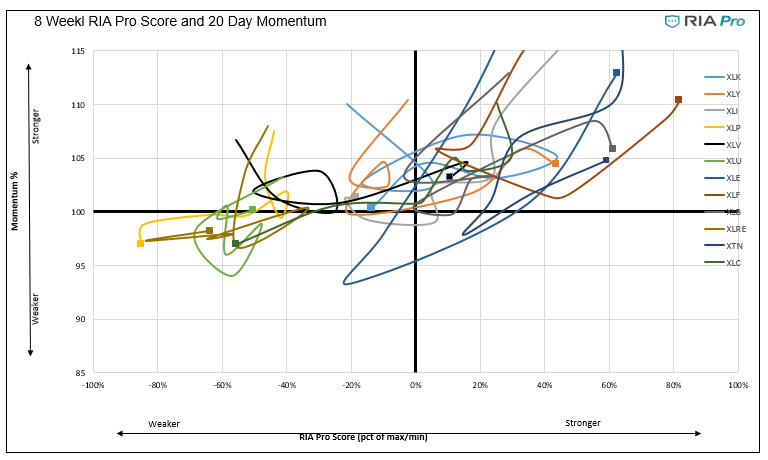

- The “spaghetti” chart shows how XLF (brown) and XLE (blue) are pushing into the extreme upper right of the graph. They can keep going up, but we frequently see a rotation at such levels to fairer valued sectors.

Graphs (Click on the graphs to expand)

Users Guide

The score is a percentage of the maximum/minimum score, as well as on a normalized basis (sigma) for the last 200 trading days. Assets with scores over or under +/-60% and sigmas over or under +/-2 are likely to either consolidate or change trend. When both the score and sigma are above or below those key levels simultaneously, the signal is stronger.

The first set of four graphs below are relative value-based, meaning the technical analysis score and sigma is based on the ratio of the asset to its benchmark. The second set of graphs is computed solely on the price of the asset. Lastly, we present “Sector spaghetti graphs” which compare momentum and our score over time to provide further current and historical indications of strength or weakness. The square at the end of each squiggle is the current reading. The top right corner is the most bullish, while the bottom left corner the most bearish.

The technical value scorecard report is just one of many tools that we use to assess our holdings and decide on potential trades. This report may send a strong buy or sell signal, but we may not take any action if other research and models do not affirm it.

The ETFs used in the model are as follows:

- Staples XLP

- Utilities XLU

- Health Care XLV

- Real Estate XLRE

- Materials XLB

- Industrials XLI

- Communications XLC

- Banking XLF

- Transportation XTN

- Energy XLE

- Discretionary XLY

- S&P 500 SPY

- Value IVE

- Growth IVW

- Small Cap SLY

- Mid Cap MDY

- Momentum MTUM

- Equal Weighted S&P 500 RSP

- NASDAQ QQQ

- Dow Jones DIA

- Emerg. Markets EEM

- Foreign Markets EFA

- IG Corp Bonds LQD

- High Yield Bonds HYG

- Long Tsy Bonds TLT

- Med Term Tsy IEI

- Mortgages MBB

- Inflation TIP

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read