SOTM 2020: State Of The Markets

“I am thrilled to report to you tonight that our economy is the best it has ever been.” – President Trump, SOTU

In the President’s “State of the Union Address” on Tuesday, he used the podium to talk up the achievements in the economy and the markets.

- Low unemployment rates

- Tax cuts

- Job creation

- Economic growth, and, of course,

- Record high stock markets.

While it certainly is a laundry list of items he can claim credit for, it is the claim of record-high stock prices that undermines the rest of the story.

Let me explain.

The stock market should be a reflection of actual economic growth. Since corporate earnings are derived primarily from consumptive spending, corporate investments, and imports and exports, actual economic activity should be reflected in the price investors are willing to pay for the earnings being generated.

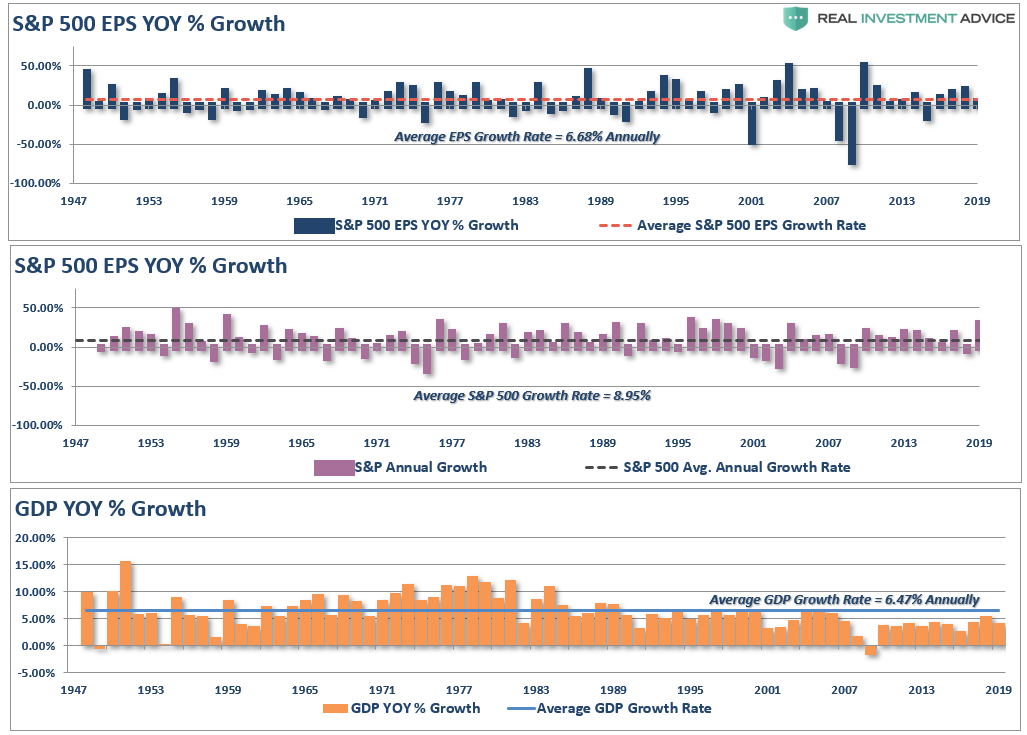

For the majority of the 20th century, this was indeed the case as corporate earnings were reflective of economic activity. The chart below shows the annual change in reported earnings, nominal GDP, and the price of the S&P 500.

Not surprisingly, as the economy grew at 6.47% annually, earnings also grew at 6.68% annually as would be expected. Since investors are willing to a premium for earnings growth, the S&P 500 grew at 9% annually over that same period.

Importantly, note that long-term economic growth has averaged 6% annually. However, as shown in the lower panel, economic growth has been running below the long-term average since 2000, but has been substantially weaker since 2007, growing at just 2% annually.

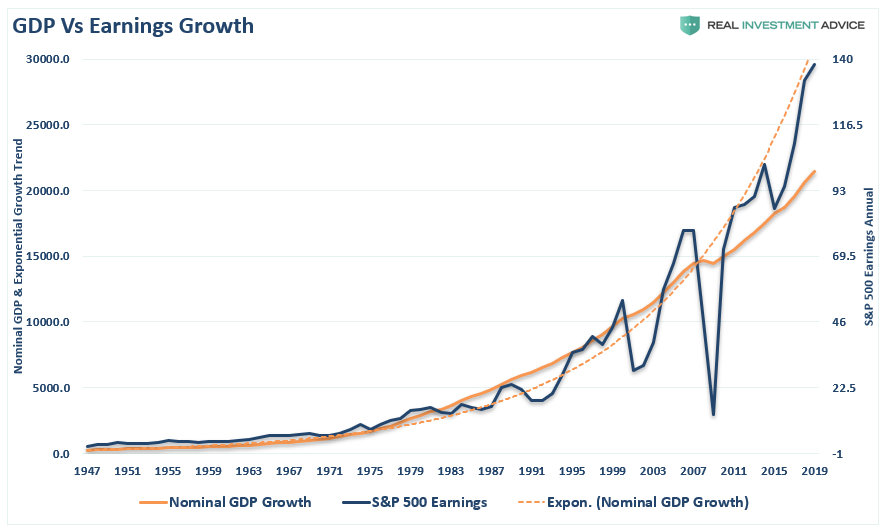

The next chart shows this weaker growth more clearly. Since the financial crisis, economic growth has failed to recover back to its long-term exponential growth trend. However, reported earnings are exceedingly deviated from what actual underlying economic growth can generate. This is due to a decade of accounting gimmickry, share buybacks, wage suppression, low interest rates, and high corporate debt levels.

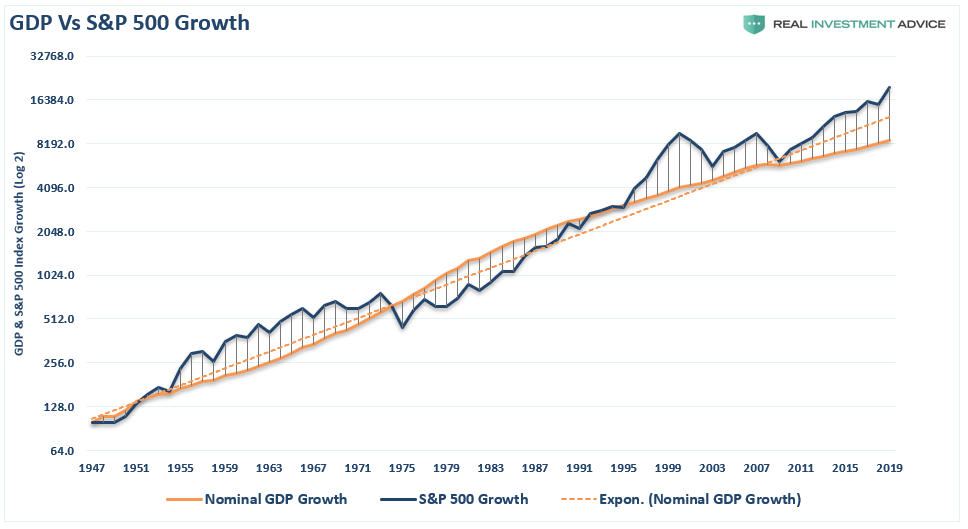

The next chart looks at the deviation by looking at the market itself versus long-term economic growth. The S&P 500 and GDP have been scaled to 100, and displayed on a log-scale for comparative purposes.

The current growth trend of the economy is running well below its long-term exponential trend, but the S&P 500 is currently at the most significant deviation from that growth on record. (It should be noted that while these deviations from economic growth can last for a long-time, the eventual mean reversion always occurs.)

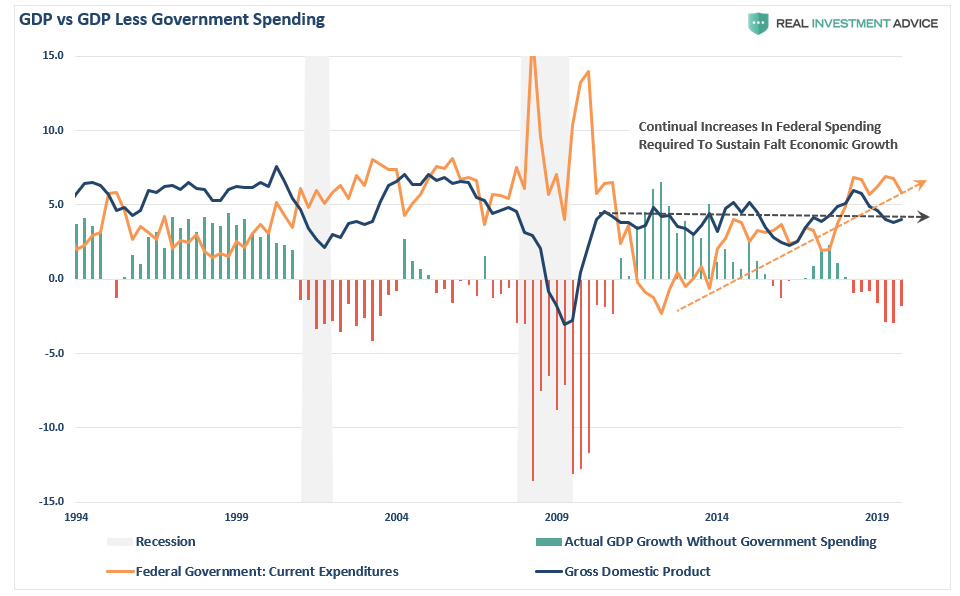

The Spending Mirage

Take a look at the following chart.

While the President’s claims of an exceptionally strong economy rely heavily on historically low unemployment and jobless claims numbers, historically high levels of asset prices, and strong consumer spending trends, there is an underlying deterioration which goes unaddressed.

So, here’s your pop quiz?

If consumer spending is strong, AND unemployment is near the lowest levels on record, AND interest rates are low, AND job creation is high – then why is the economy only growing at 2%?

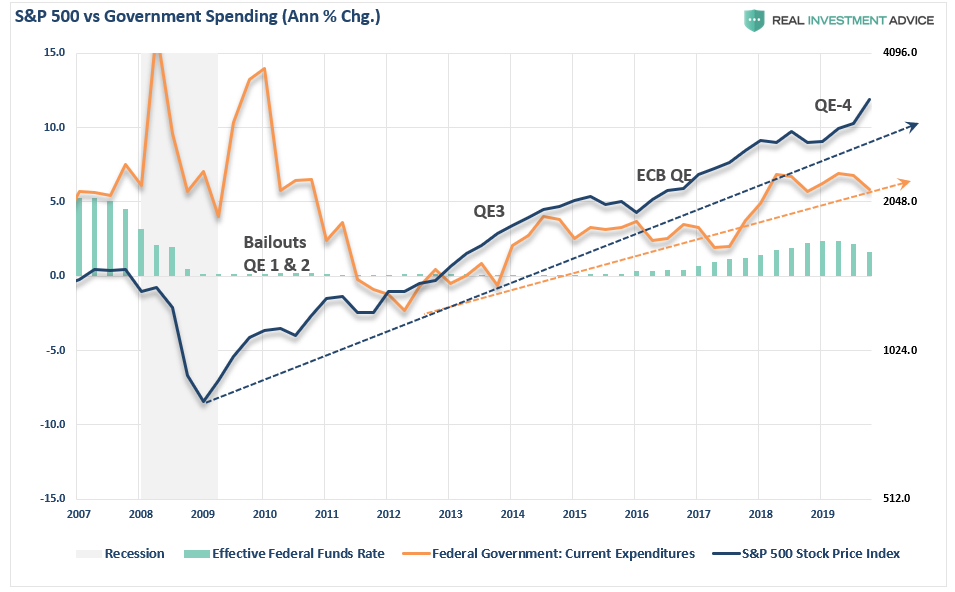

Furthermore, if the economy was doing as well as government statistics suggest, then why does the Federal Reserve need to continue providing the economy with “emergency measures,” cutting rates, and giving “verbal guidance,” to keep the markets from crashing?

The reality is that if it wasn’t for the Government running a massive trillion-dollar fiscal deficit, economic growth would actually be recessionary.

In GDP accounting, consumption is the largest component. Of course, since it is impossible to “consume oneself to prosperity,” the ability to consume more is the result of growing debt. Furthermore, economic growth is also impacted by Government spending, as government transfer payments, including Medicaid, Medicare, disability payments, and SNAP (previously called food stamps), all contribute to the calculation.

As shown below, between the Federal Reserve’s monetary infusions and the ballooning government deficit, the S&P 500 has continued to find support.

However, nothing is “produced” by those transfer payments. They are not even funded. As a result, national debt rises every year, and that debt adds to GDP.

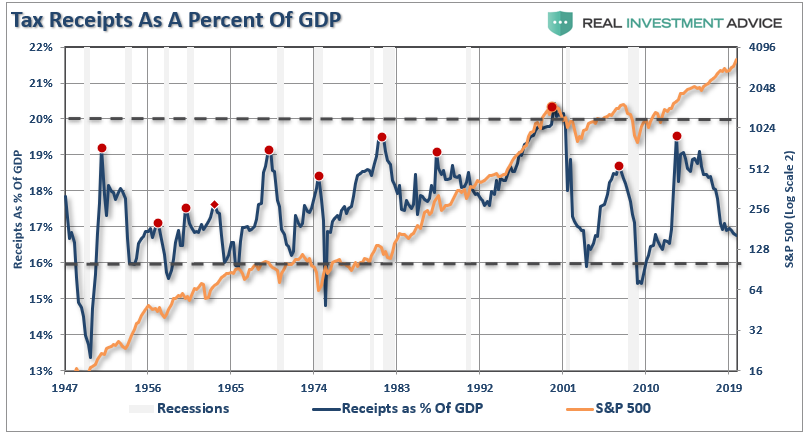

Another way to look at this is through tax receipts as a percentage of GDP. If the economy was indeed “the strongest ever,” then we should see an increase in wage growth commensurate with increased economic activity. As a result of higher wages, there should be an increase in the taxes collected by the Government from wages, consumption, imports, and exports.

See the problem here?

Clearly, this is not the case as tax receipts as a percentage of GDP peaked in 2012, and have now declined to levels which historically are more coincident with economic recessions, rather than expansions. Yet, currently, because of the artificial interventions, the stock market remains well detached from what economic data is actually saying.

Corporate Profits Tell The Real Story

When it comes to the state of the market, corporate profits are the best indicator of economic strength.

The detachment of the stock market from underlying profitability guarantees poor future outcomes for investors. But, as has always been the case, the markets can certainly seem to “remain irrational longer than logic would predict,” but it never lasts indefinitely.

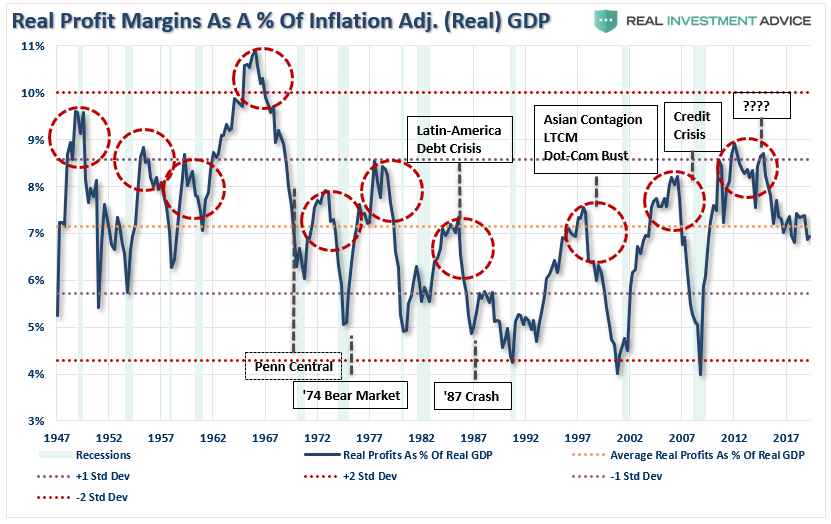

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.” – Jeremy Grantham

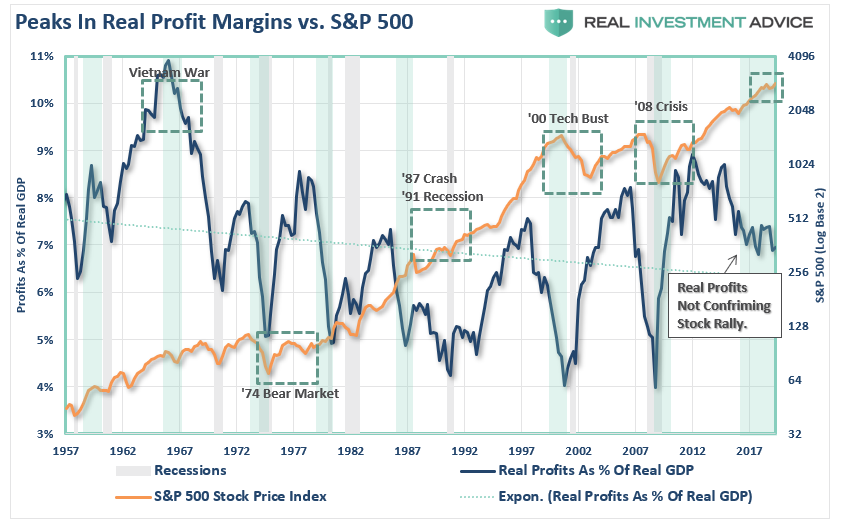

As shown, when we look at inflation-adjusted profit margins as a percentage of inflation-adjusted GDP, we see a clear process of mean-reverting activity over time. Of course, those mean reverting events are always coupled with recessions, crises, or bear markets.

More importantly, corporate profit margins have physical constraints. Out of each dollar of revenue created, there are costs such as infrastructure, R&D, wages, etc. Currently, the biggest contributors to expanding profit margins has been the suppression of employment, wage growth, and artificially suppressed interest rates, which have significantly lowered borrowing costs. Should either of the issues change in the future, the impact to profit margins will likely be significant.

The chart below shows the ratio overlaid against the S&P 500 index.

I have highlighted peaks in the profits-to-GDP ratio with the green vertical bars. As you can see, peaks, and subsequent reversions, in the ratio have been a leading indicator of more severe corrections in the stock market over time. This should not be surprising as asset prices should eventually reflect the underlying reality of corporate profitability.

It is often suggested that, as mentioned above, low interest rates, accounting rule changes, and debt-funded buybacks have changed the game. While that statement is true, it is worth noting that each of those supports are artificial and finite.

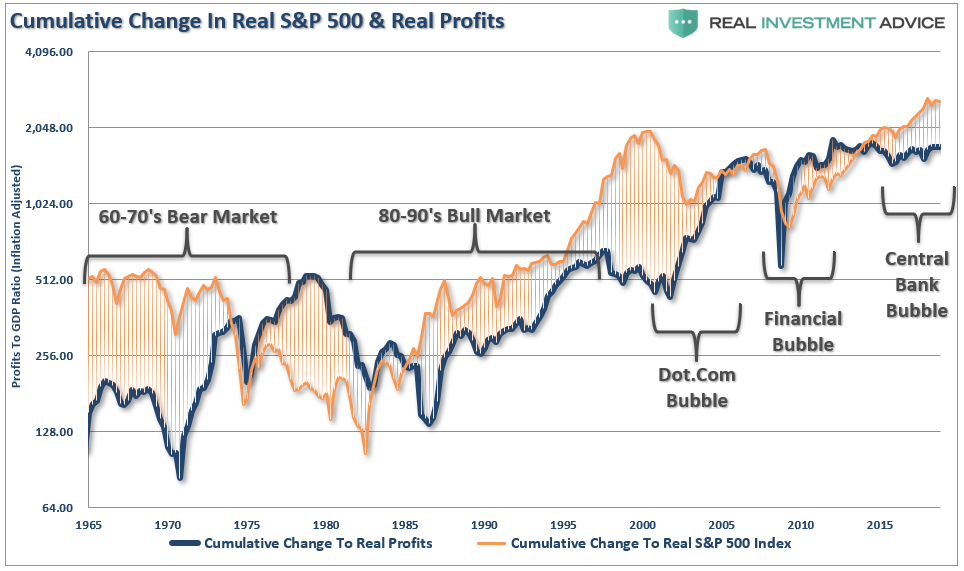

Another way to look at the issue of profits as it relates to the market is shown below. When we measure the cumulative change in the S&P 500 index as compared to the level of profits, we find again that when investors pay more than $1 for a $1 worth of profits, there is an eventual mean reversion.

The correlation is clearer when looking at the market versus the ratio of corporate profits to GDP. (Again, since corporate profits are ultimately a function of economic growth, the correlation is not unexpected.)

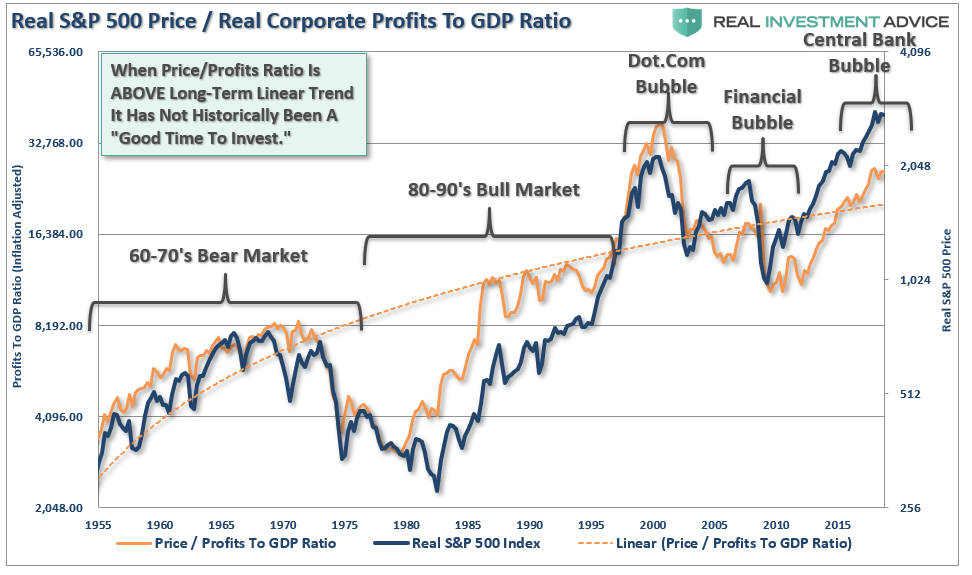

It seems to be a simple formula for investors that as long as the Fed remains active in supporting asset prices, the deviation between fundamentals and fantasy doesn’t matter.

However, investors are paying more today than at any point in history for each $1 of profit, which history suggests will not end well.

While the media is quick to attribute the current economic strength, or weakness, to the person who occupies the White House, the reality is quite different.

The political risk for President Trump is taking too much credit for an economic cycle which was already well into recovery before he took office. Rather than touting the economic numbers and taking credit for liquidity-driven financial markets, he should be using that strength to begin the process of returning the country to a path of fiscal discipline rather than a “drunken binge” of government spending.

With the economy, and the financial markets, sporting the longest-duration in history, simple logic should suggest time is running out.

This isn’t doom and gloom, it is just a fact.

Politicians, over the last decade, failed to use $33 trillion in liquidity injections, near-zero interest rates, and surging asset prices to refinance the welfare system, balance the budget, and build surpluses for the next downturn.

Instead, they only made the deficits worse, and the U.S. economy will enter the next recession pushing a $2 Trillion deficit, $24 Trillion in debt, and a $6 Trillion pension gap, which will devastate many in their retirement years.

While Donald Trump talked about “Yellen’s big fat ugly bubble” before he took office, he has now pegged the success of his entire Presidency on the stock market.

It will likely be something he eventually regrets.

“Then said Jesus unto him, Put up again thy sword into his place: for all they that take the sword shall perish with the sword.” – Matthew 26, 26:52