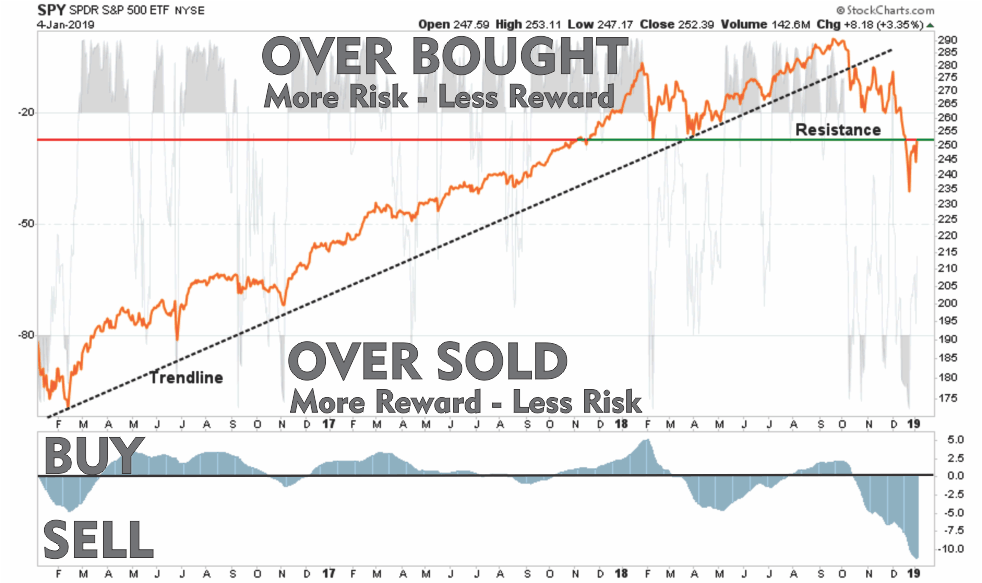

When the gray indicator is at the TOP of the chart, there is typically more risk and less reward available at the current time. In other words, the best time to BUY is when the short-term condition is over-sold. Likewise when the buy/sell indicator is above the ZERO line investments have a tendency of working better than when below the zero line.

With this basic tutorial let’s review the major markets.

NOTE: I have added relative performance information to each graph. Most every graph shows relative performance to the S&P 500 index except for the S&P 500 itself which compares value to growth, and oil to the energy sector.

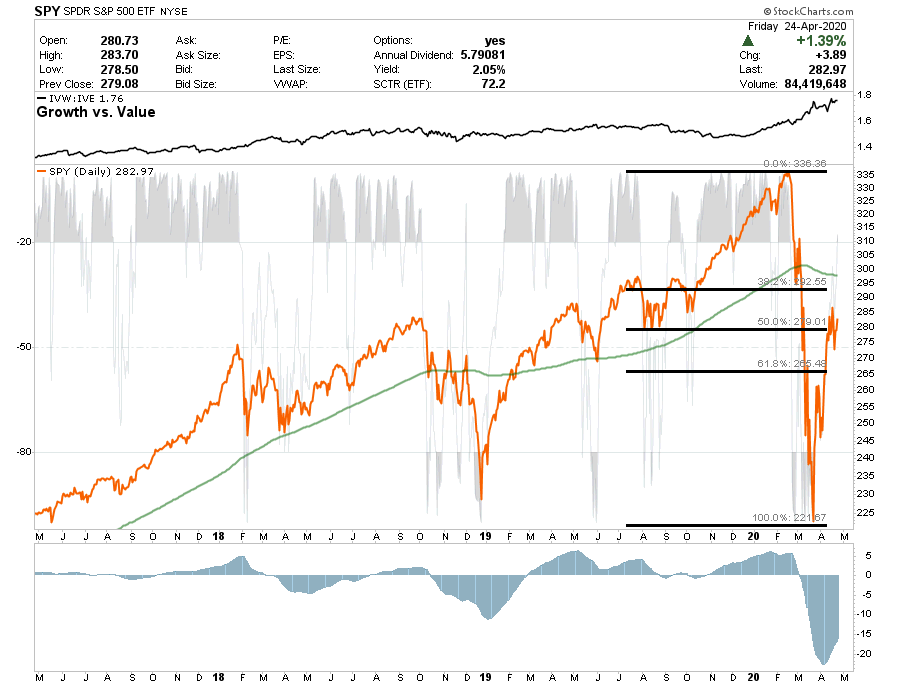

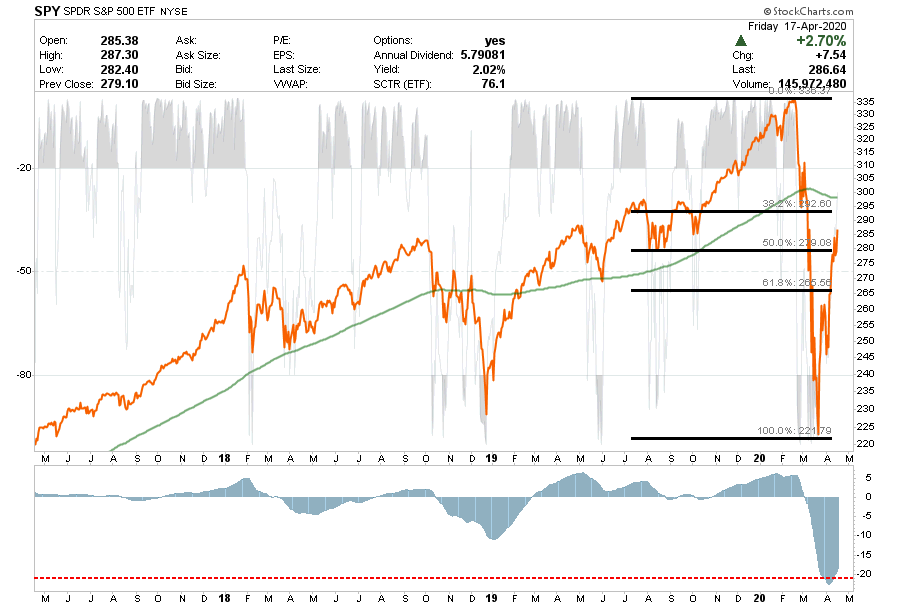

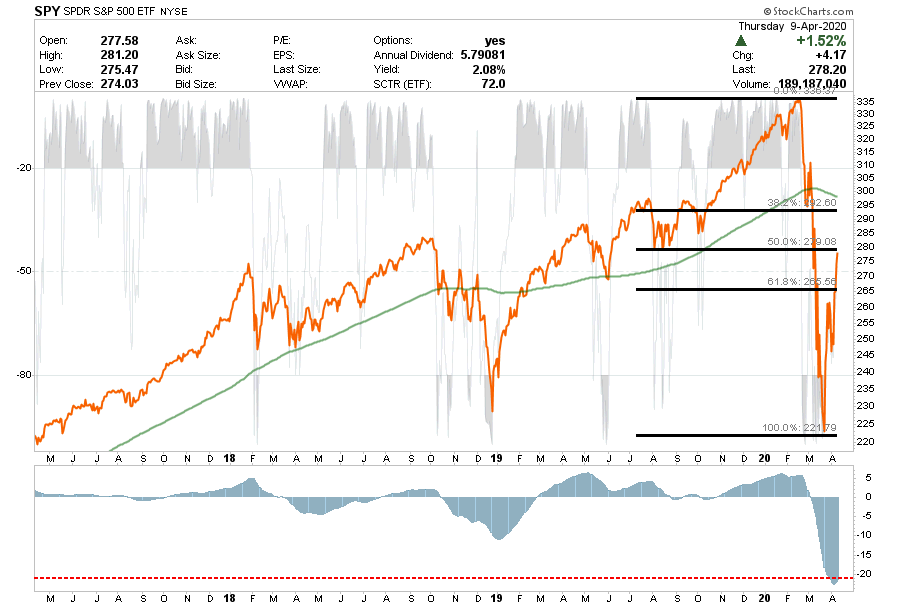

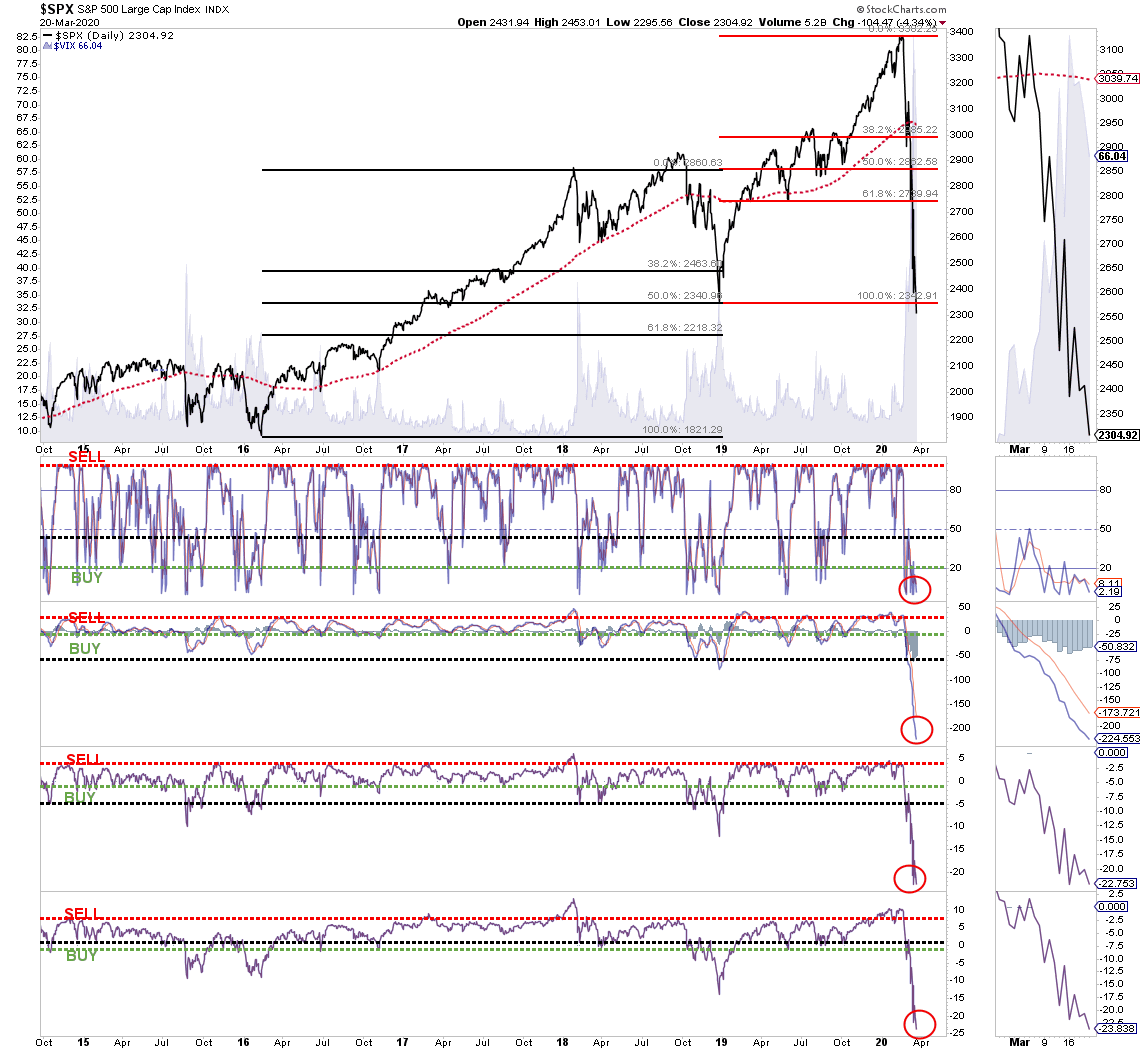

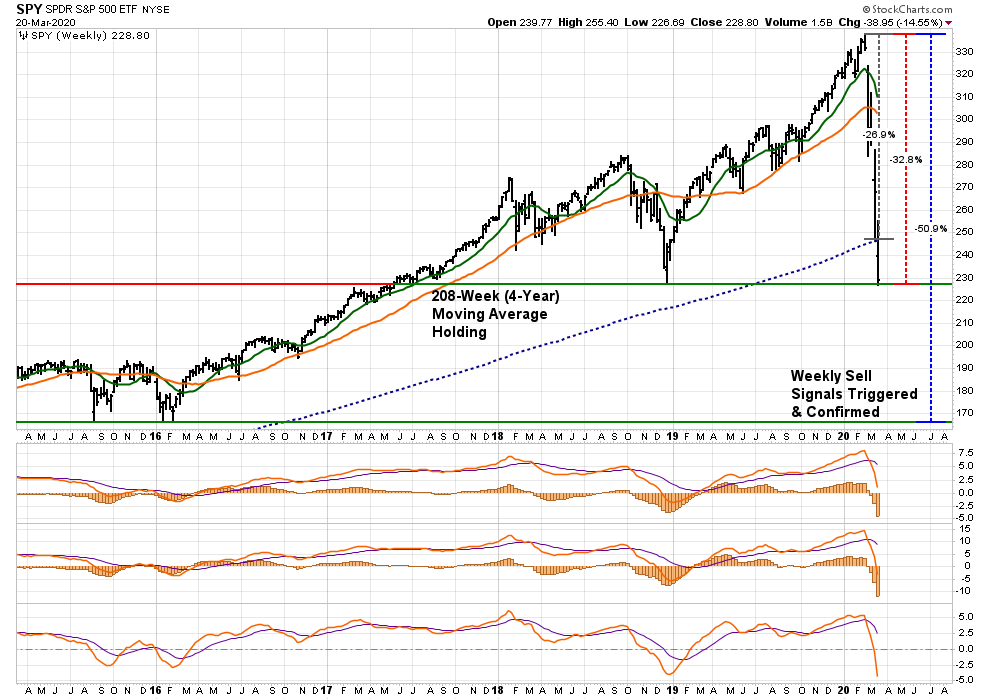

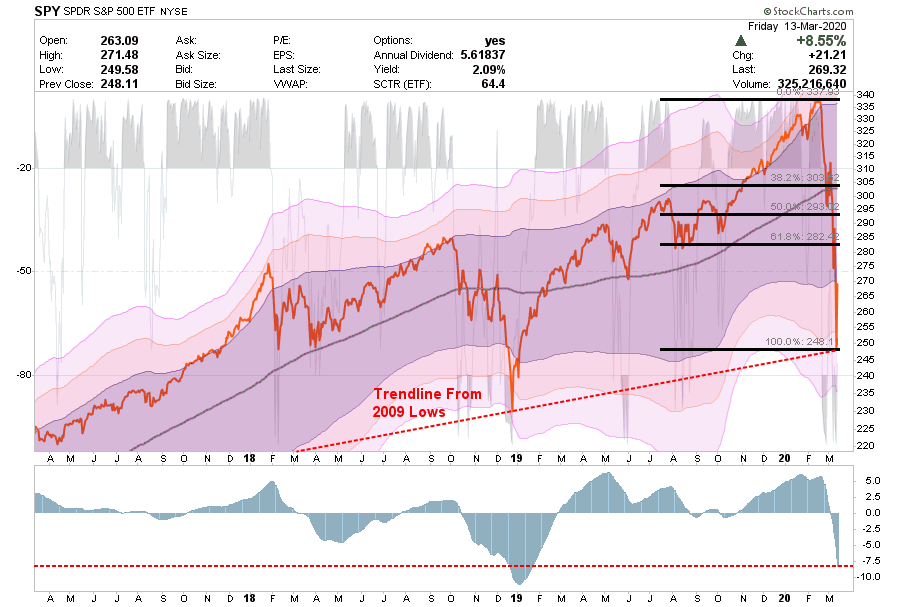

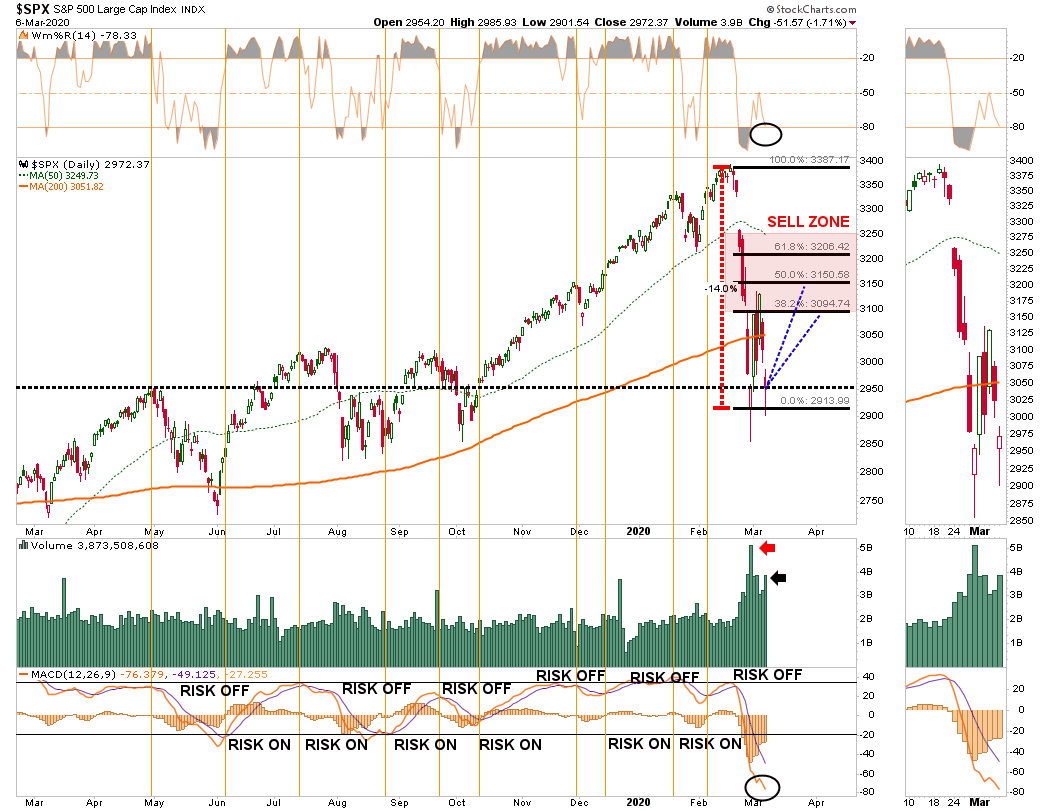

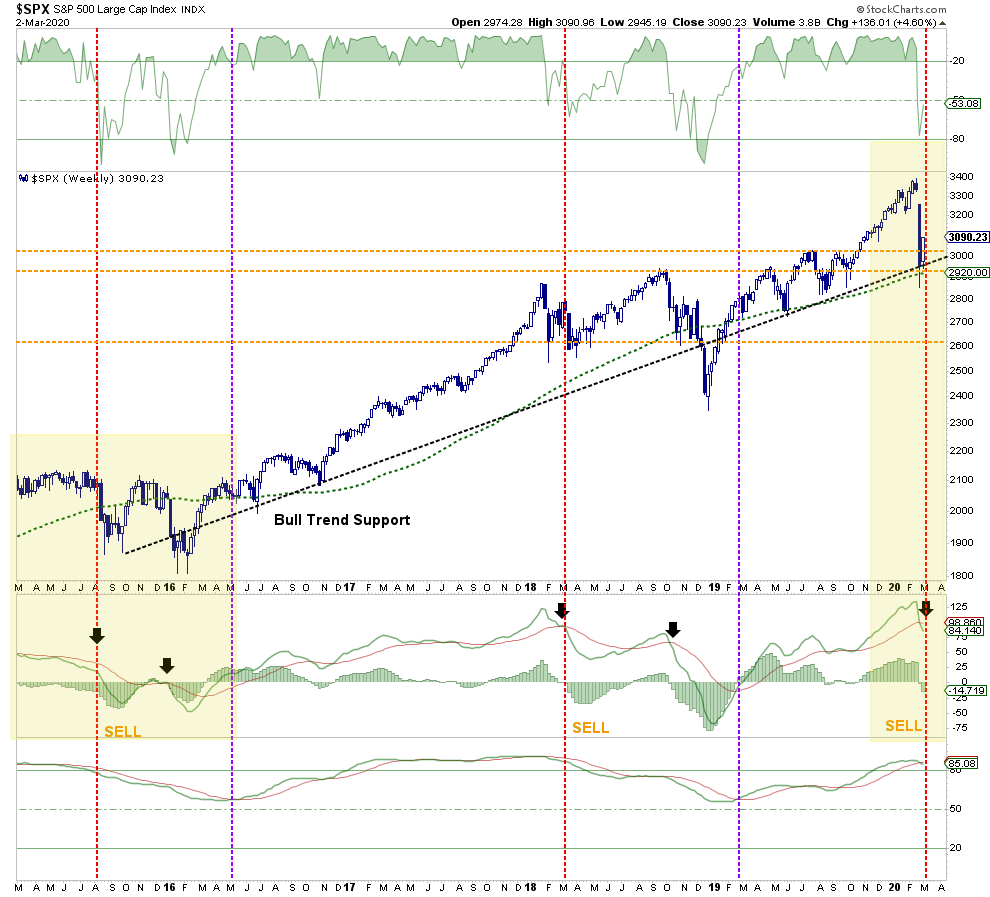

S&P 500 Index

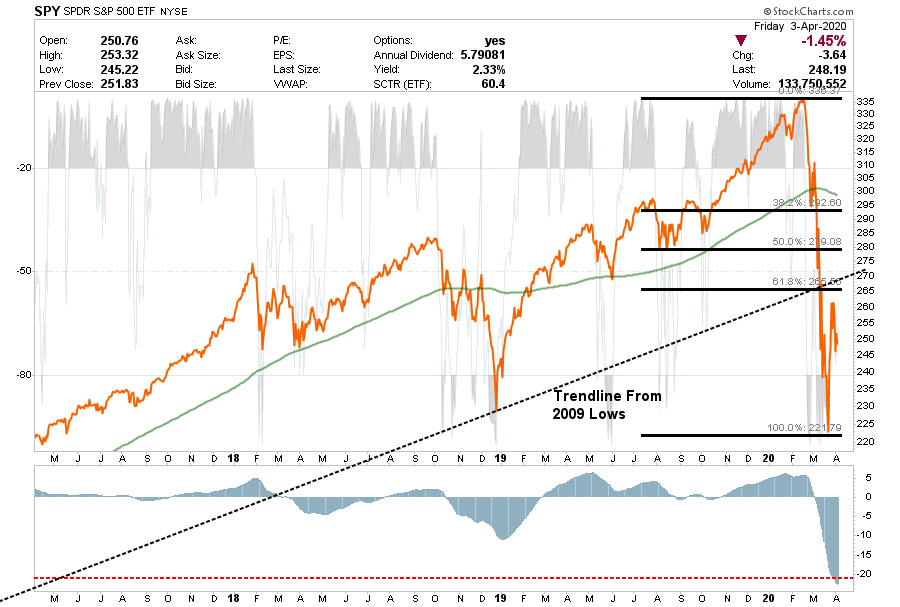

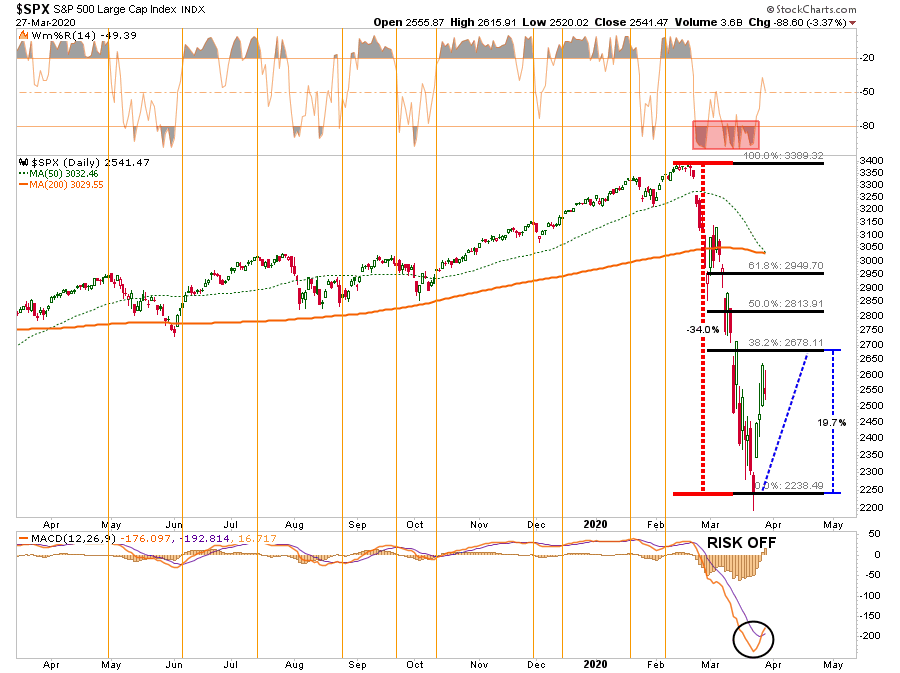

Last week I wrote: “The break of the 50% retracement this past week, is bullish and suggests a run to the 200-dma is likely. However, the risk/reward is not in the favor of longer-term positions, so trading positions only for now.”

This past week, SPY retested, and held above, the 50% retracement keeping a run to the 61.8% retracement still viable. However, the market does appear to be struggling and is overbought short-term.

This analysis still doesn’t negate the risk of more volatility ahead, so be prepared for sharp declines which means keeping trading stops tight.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No core position

This Week: Trading “Rentals” Only

Stop-loss moved up to $265

Long-Term Positioning: Bearish

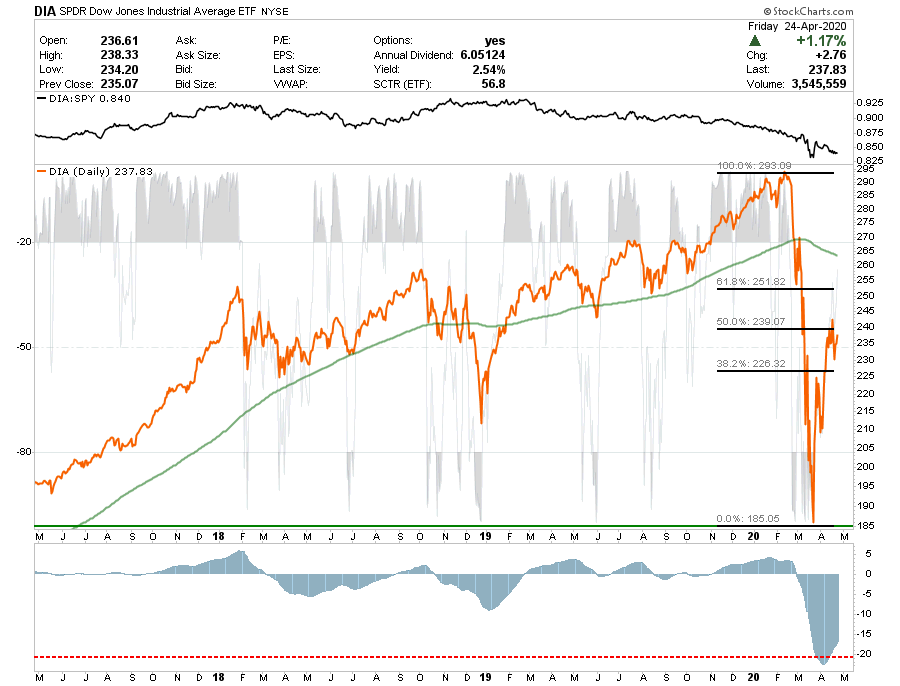

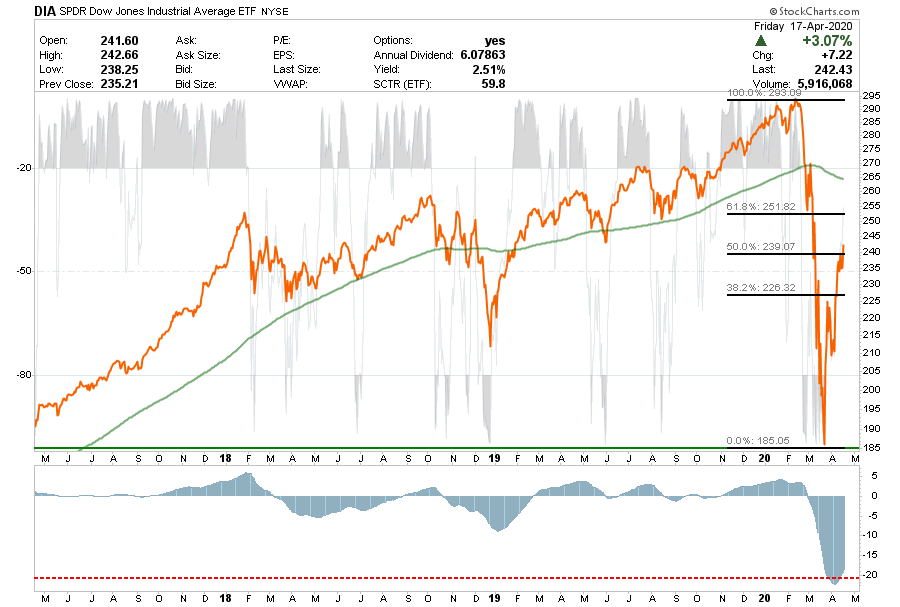

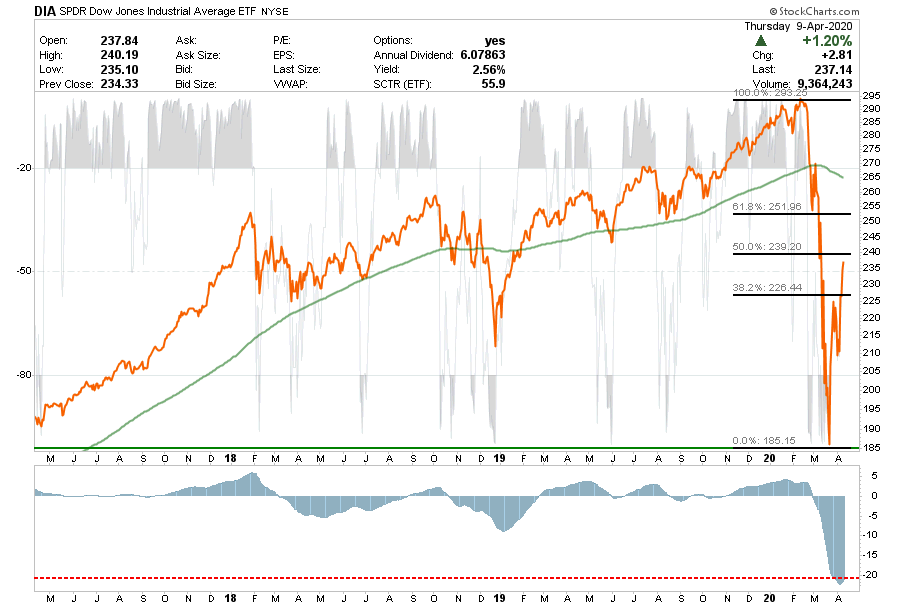

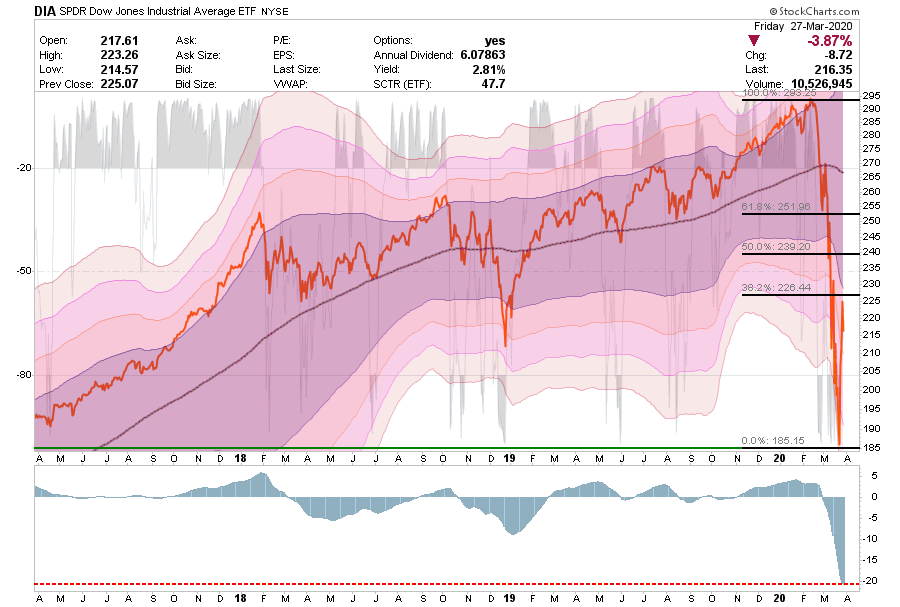

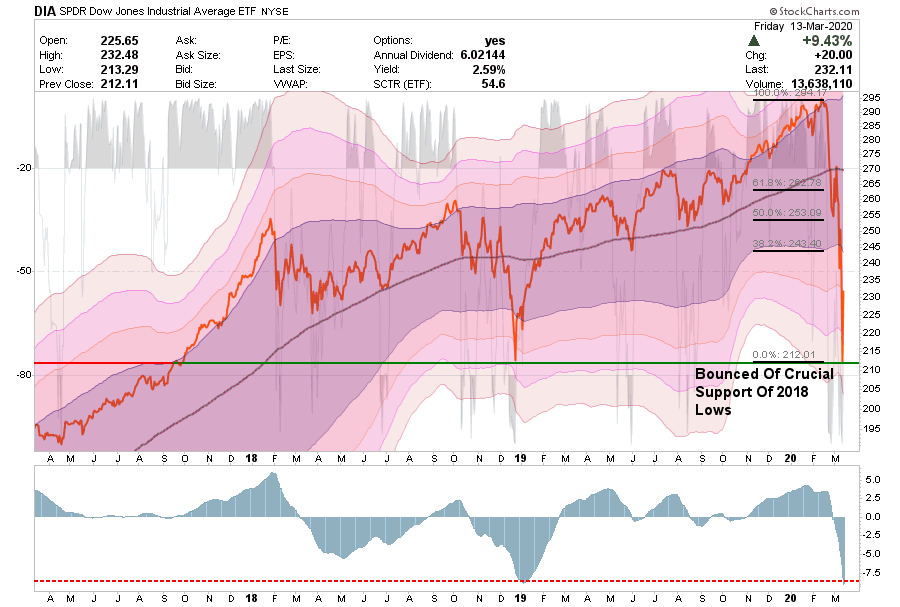

Dow Jones Industrial Average

DIA is a little different story as it failed at the 50% retracement and closed below it.

Also, on a relative basis, SPY continues to smartly outperform DIA.

If DIA fails to gain traction next week, we will likely see a failure of support. Trading “rentals” only for now with a tight stop at $226

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: Trading “Rentals” Only

Stop-loss moved up to $226

Long-Term Positioning: Bearish

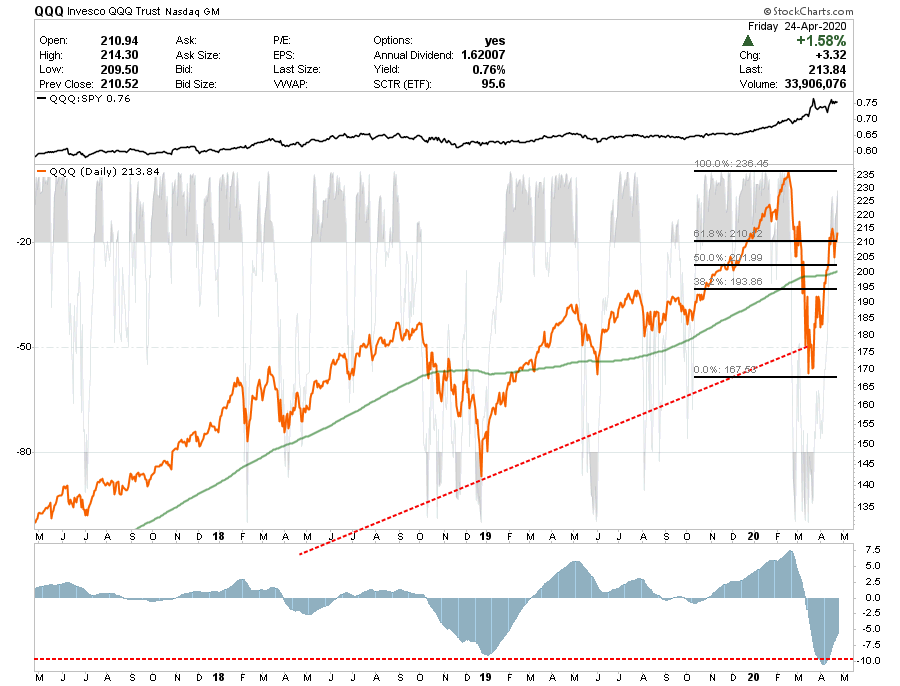

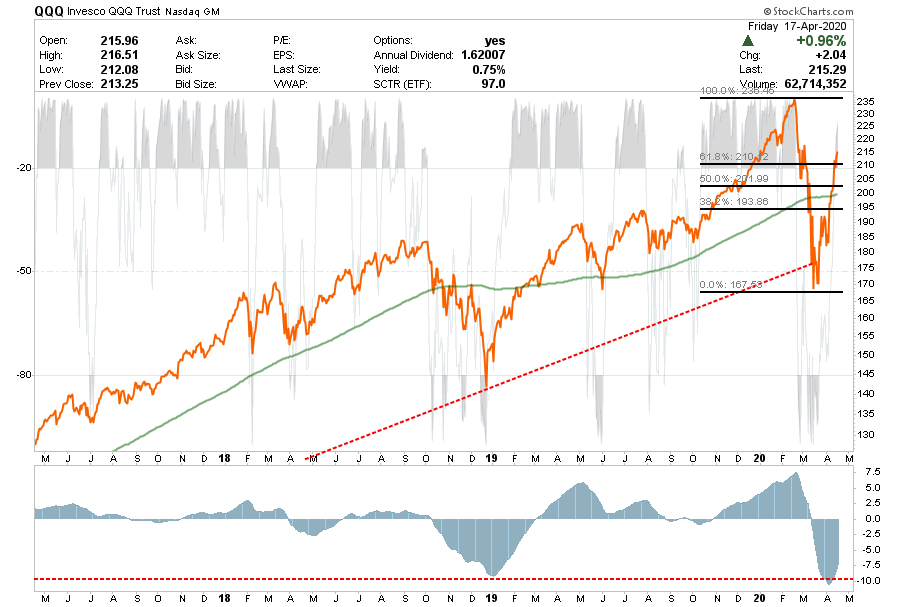

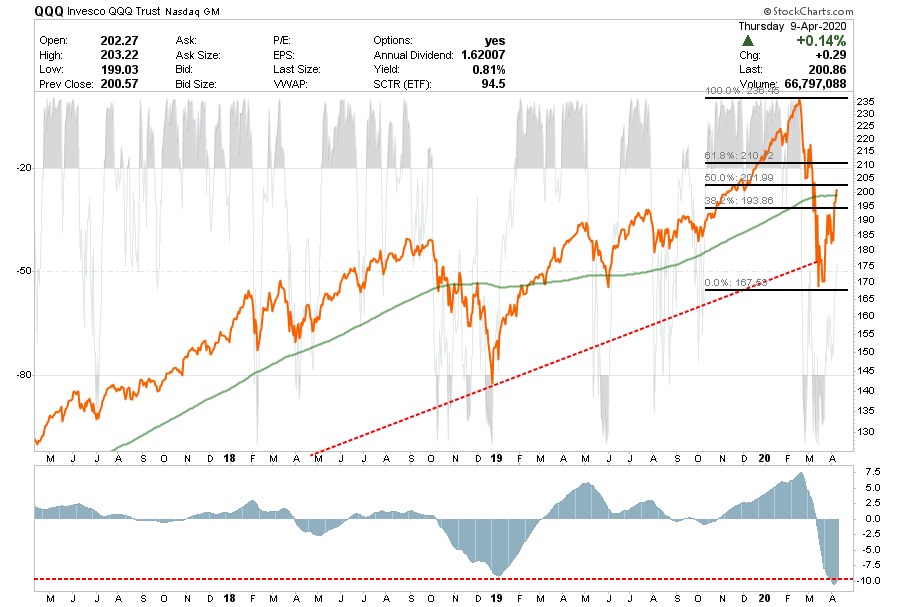

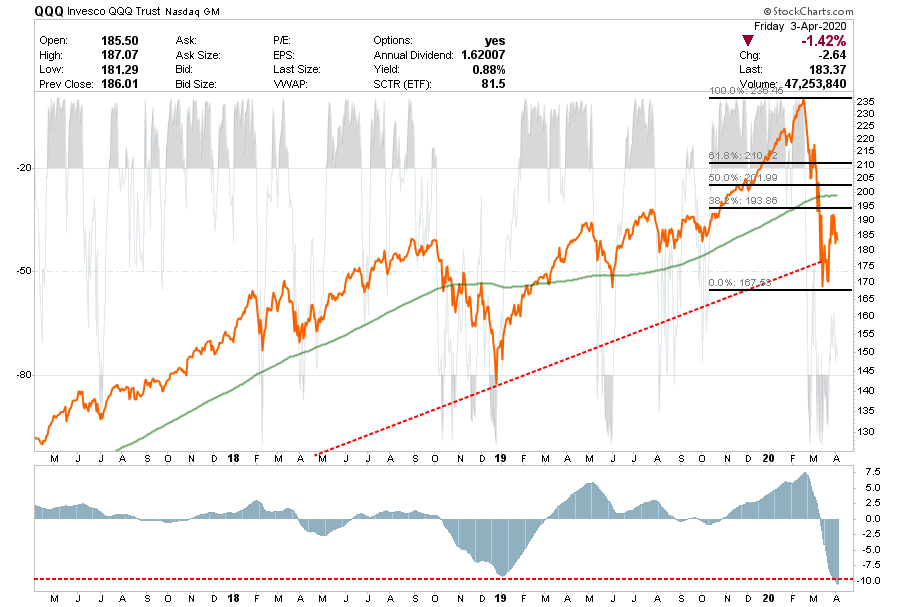

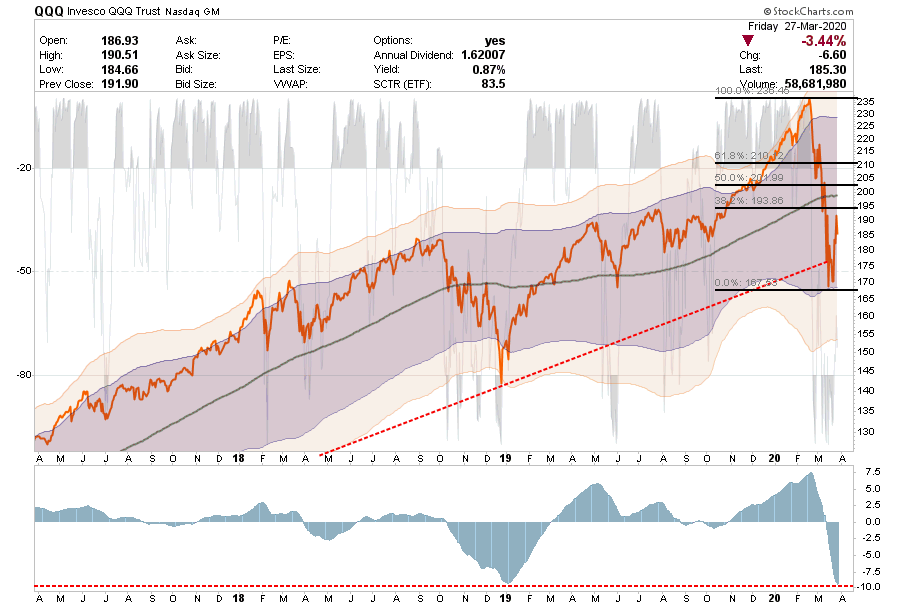

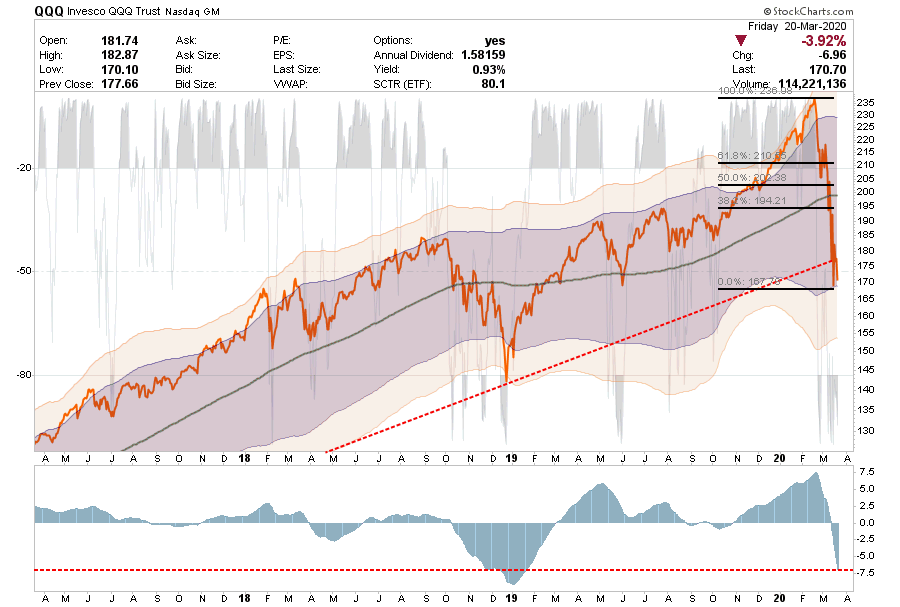

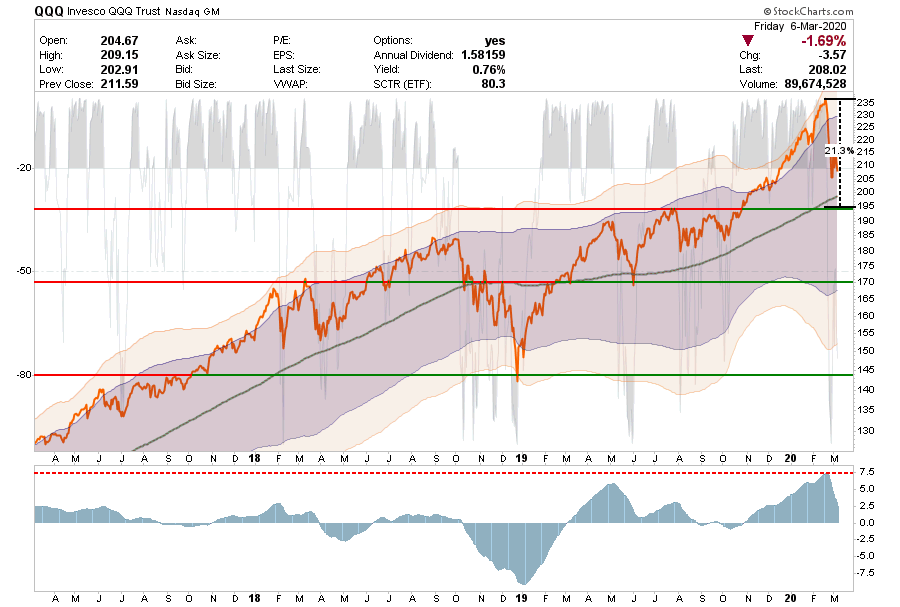

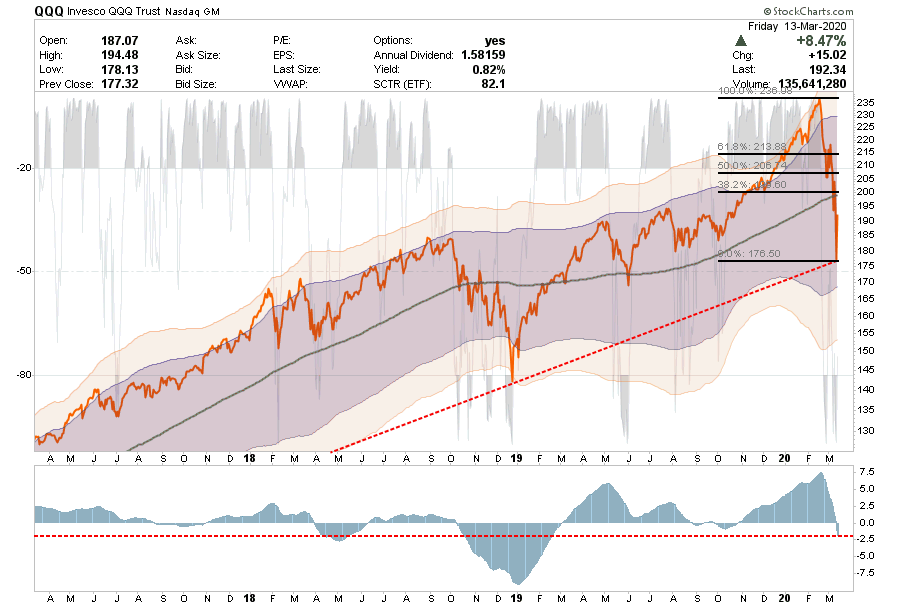

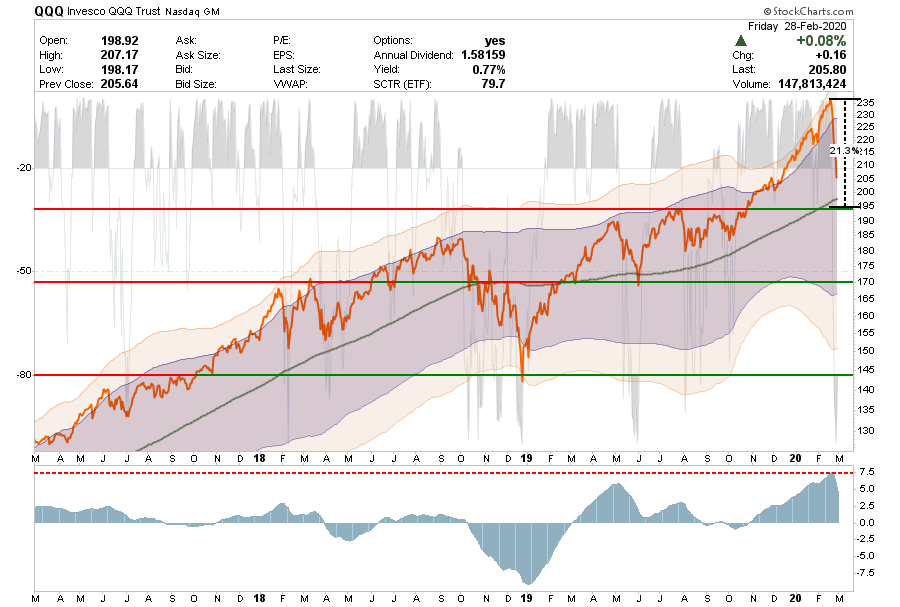

Nasdaq Composite

As we have noted previously, QQQ is by far “the best index” to own currently from a technical basis.

QQQ is outperforming the SPY by a wide margin, but not surprising given the top-5 stocks in the SPY are also the top-5 in the QQQ and are most technology related shares.

Last week’s break above the 200-dma and the 61.8% sets up a test of “all-time” highs. (Pretty incredible when you think about the amount of economic devastation that is coming.)

But, from a trading perspective, “What is…is.”

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: Trading “Rentals” Only

Stop-loss moved up to $200

Long-Term Positioning: Bearish due to valuations

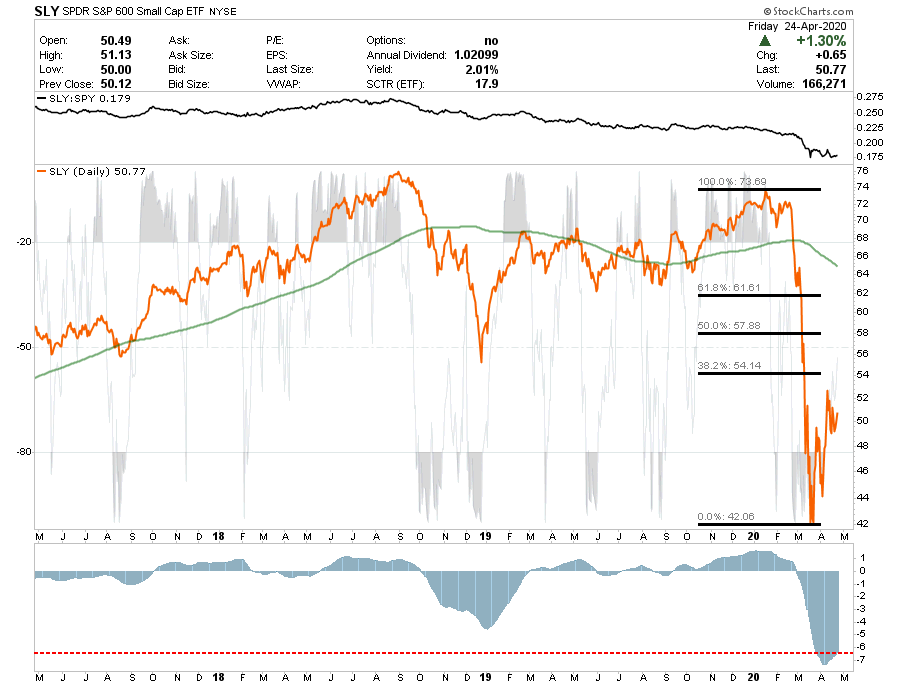

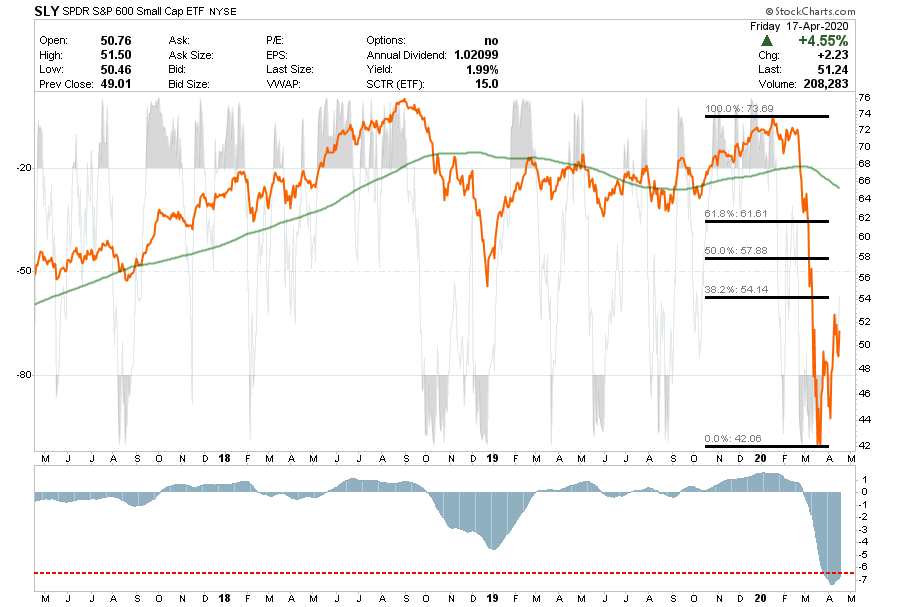

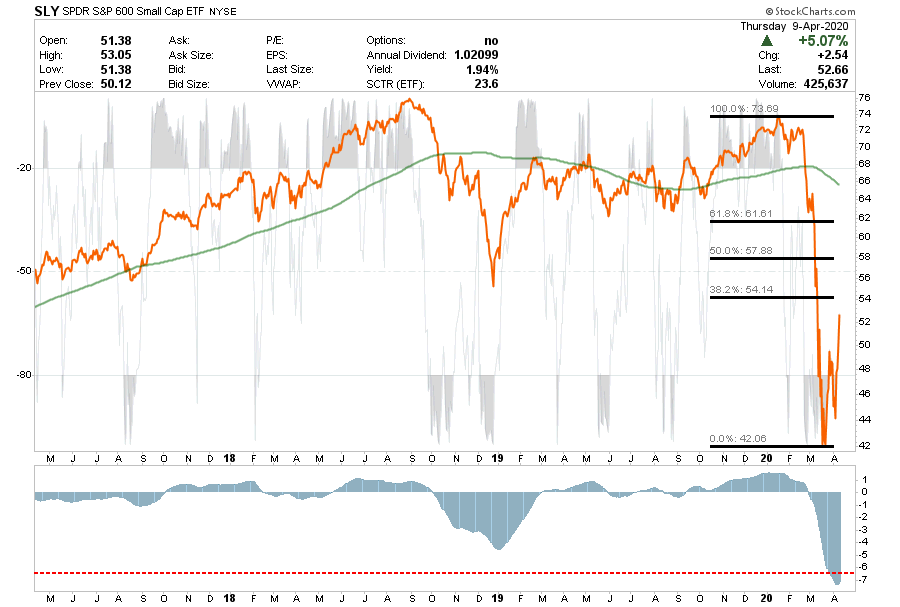

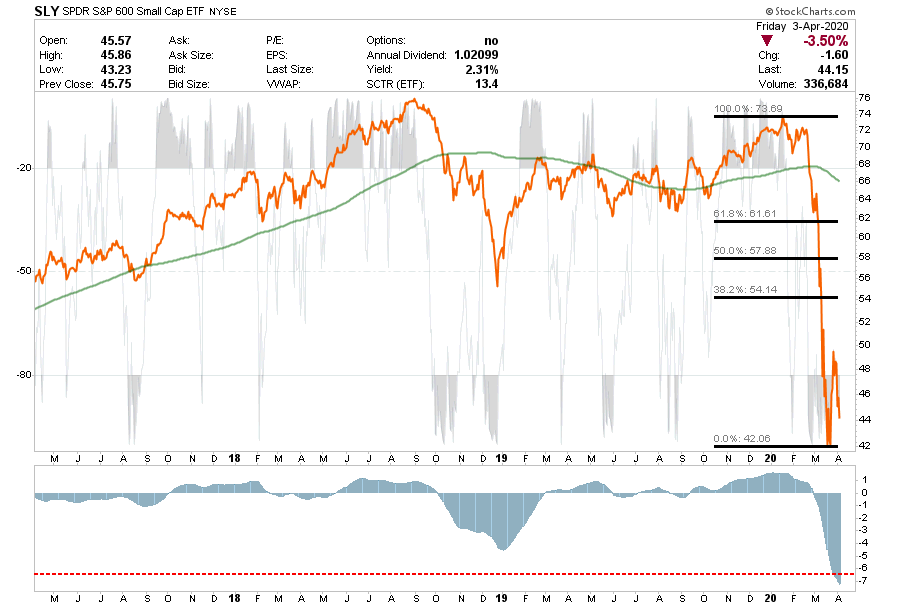

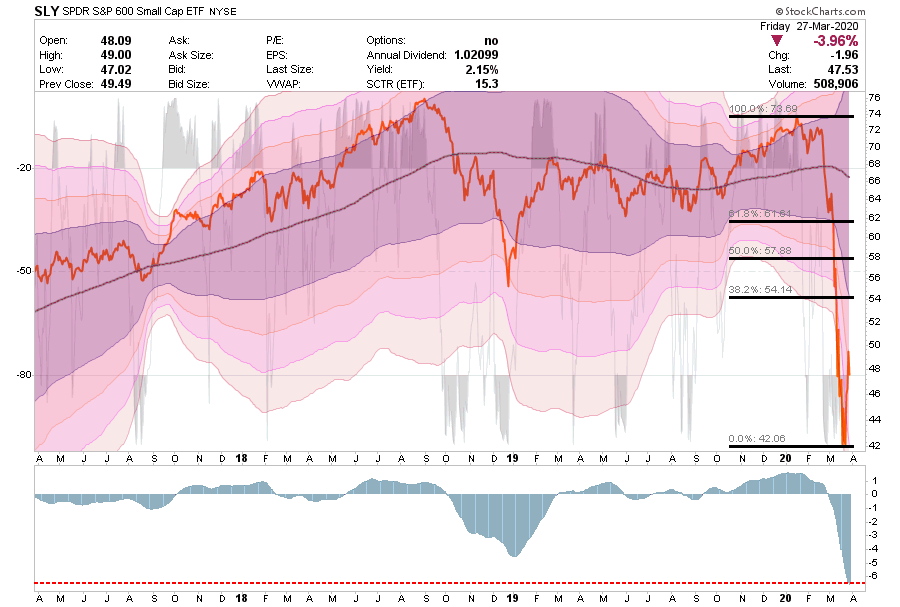

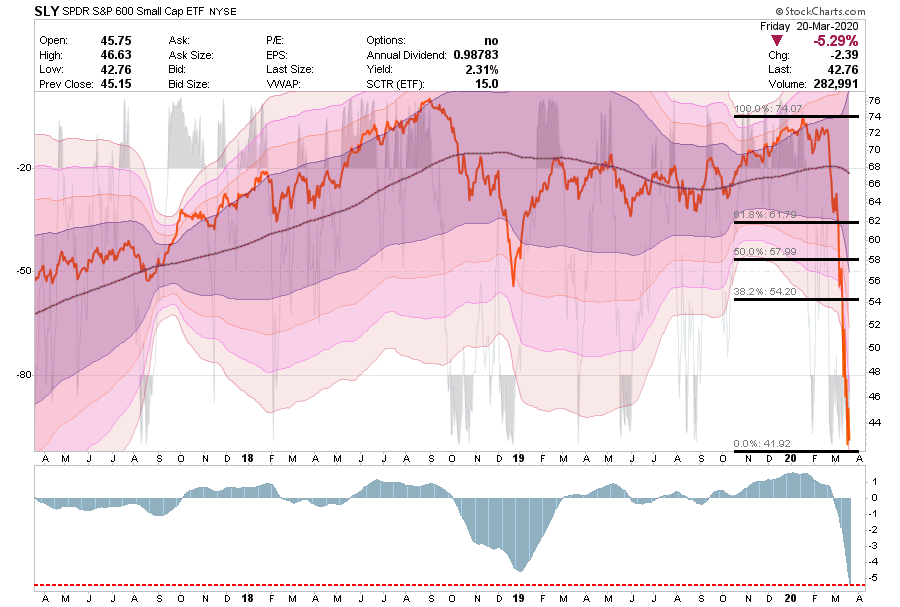

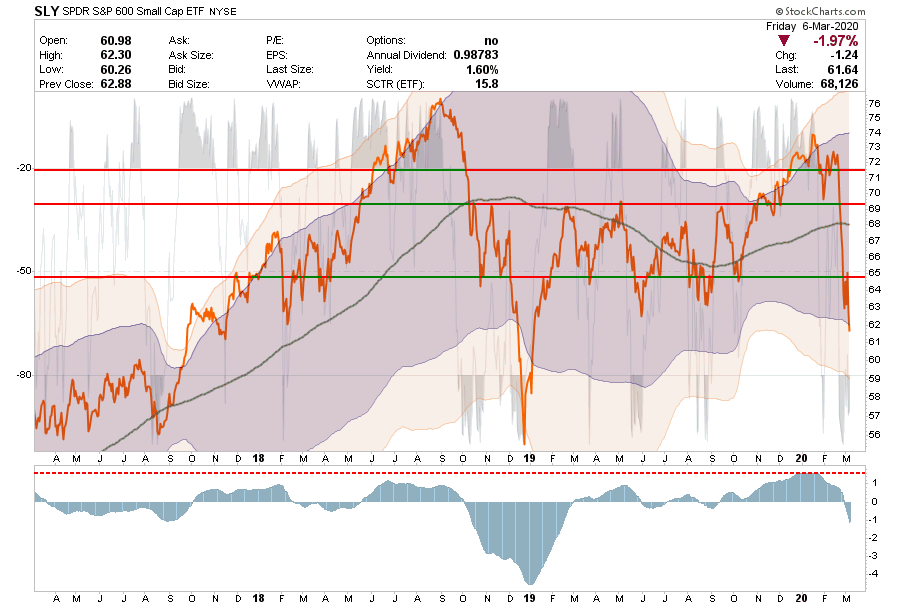

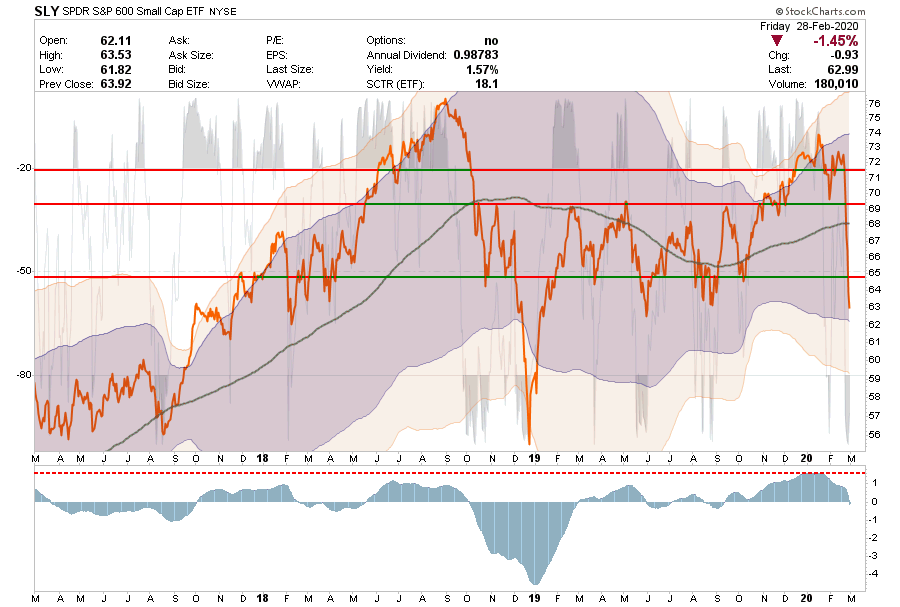

S&P 600 Index (Small-Cap)

Small caps continue to sorely underperform large caps in the current environment which also suggests the broader market remains at risk as well.

No change to our positioning on Small-caps which are still “no place to be as both small and mid-cap companies are going to be hardest hit by the virus.”

Be careful what you own.

Avoid small-caps.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop loss adjusted to $44 on trading positions.

Long-Term Positioning: Bearish

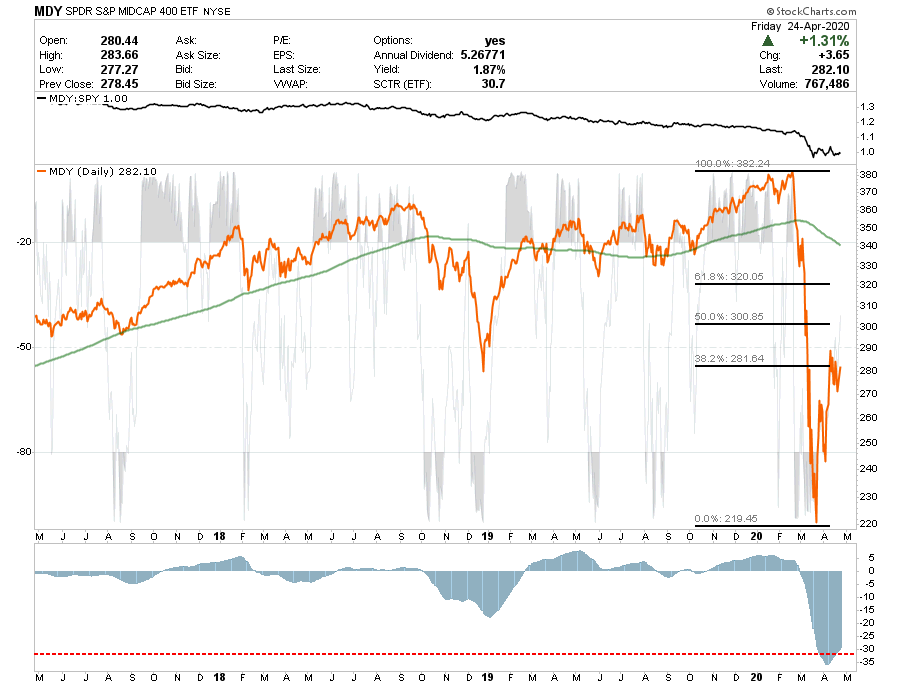

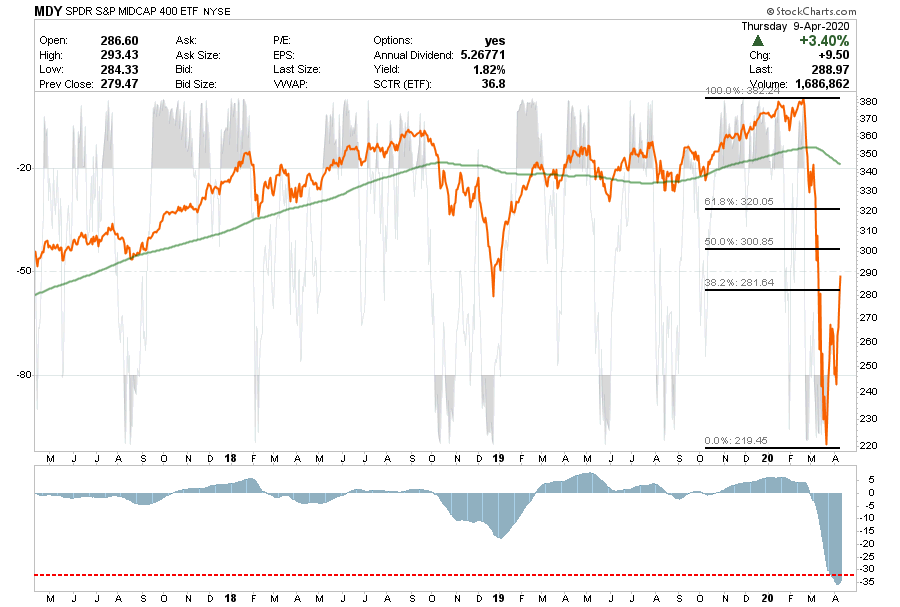

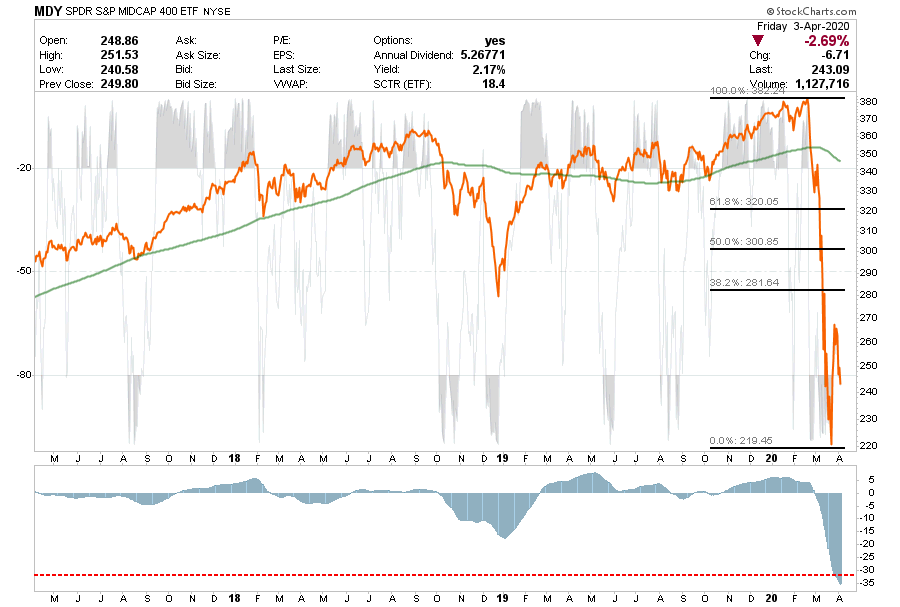

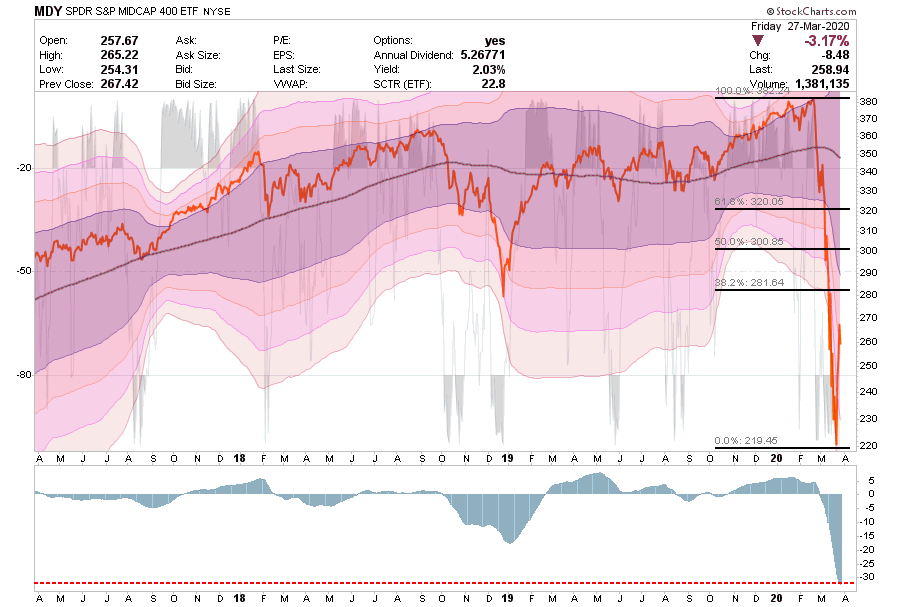

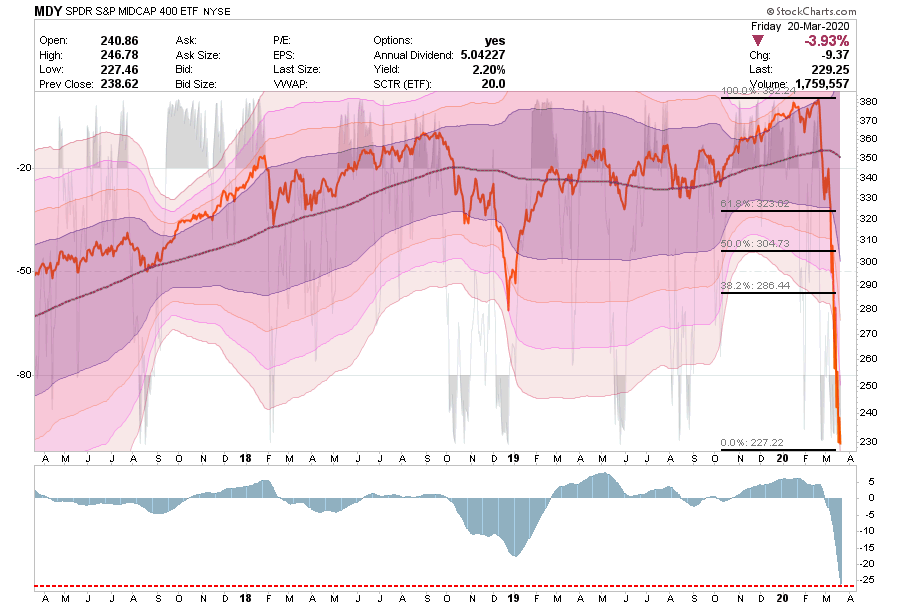

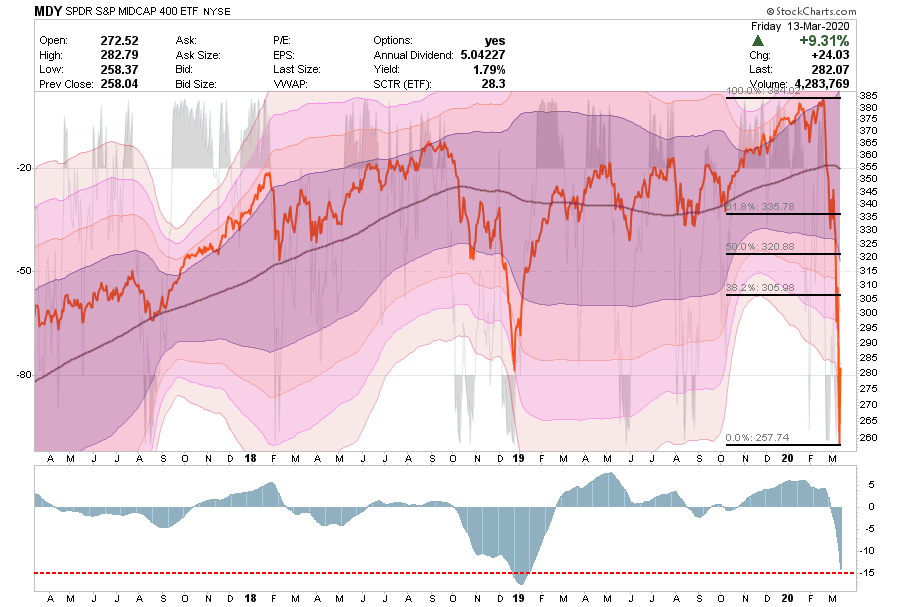

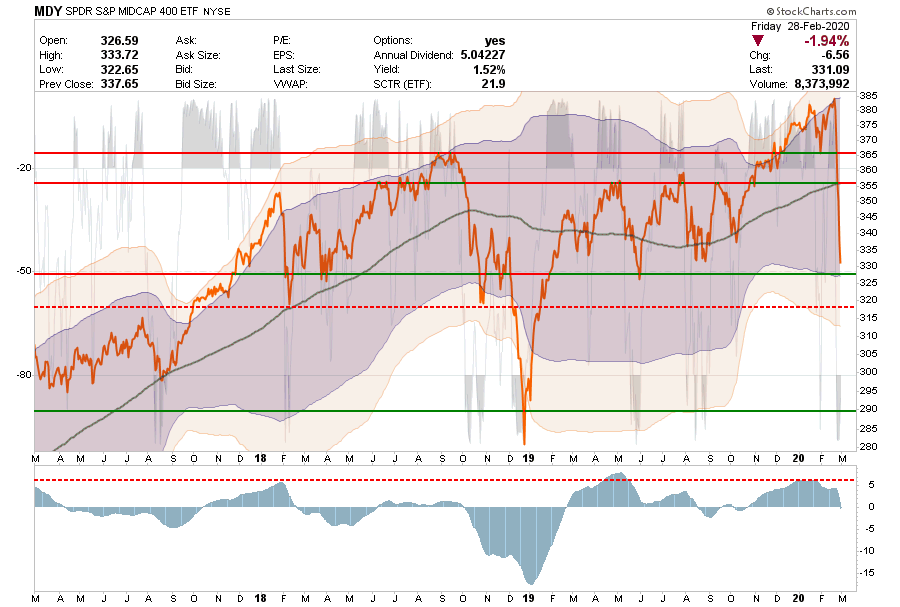

S&P 400 Index (Mid-Cap)

As with Small-caps, we have no holdings.

Relative performance continues to remain exceedingly poor. MDY failed at the 28.2% retracement level and is at risk of a much slower economic environment.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No holding

This Week: No holding

Stop Loss moved up to $245 for trading positions.

Long-Term Positioning: Bearish

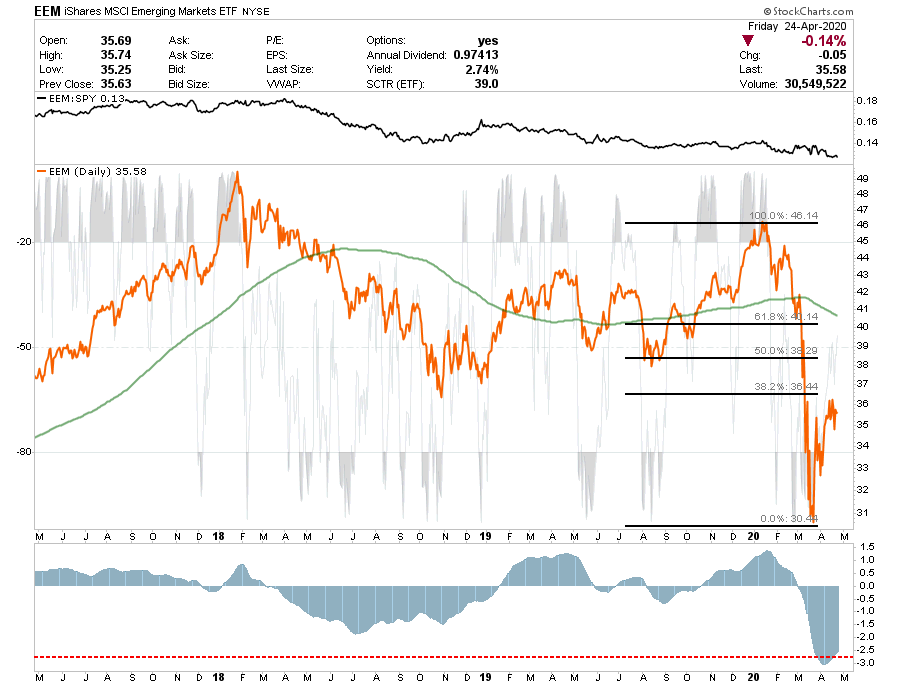

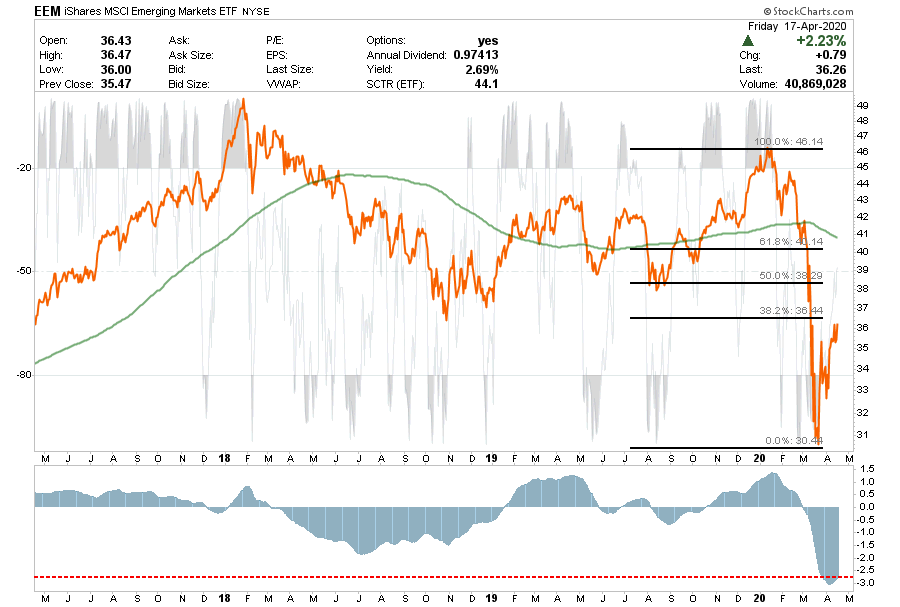

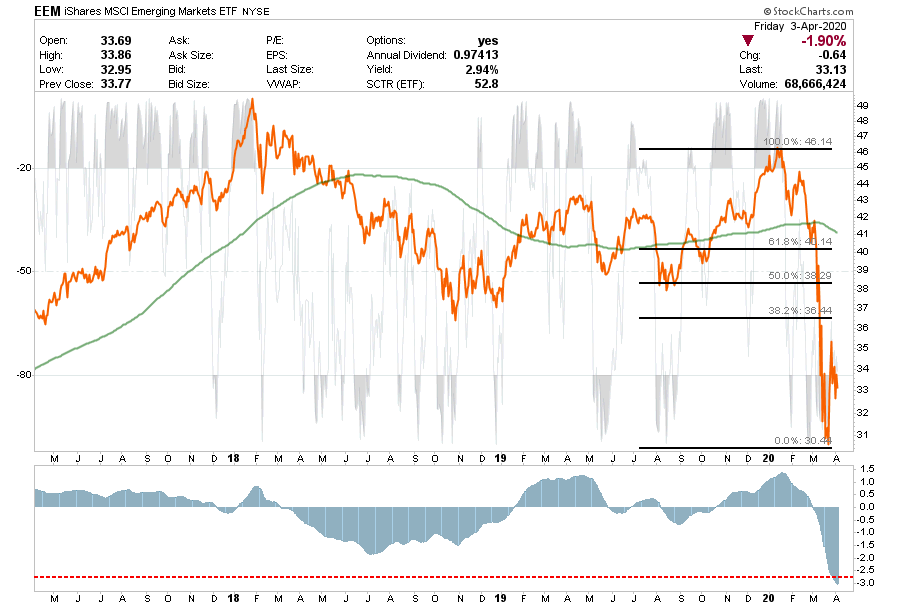

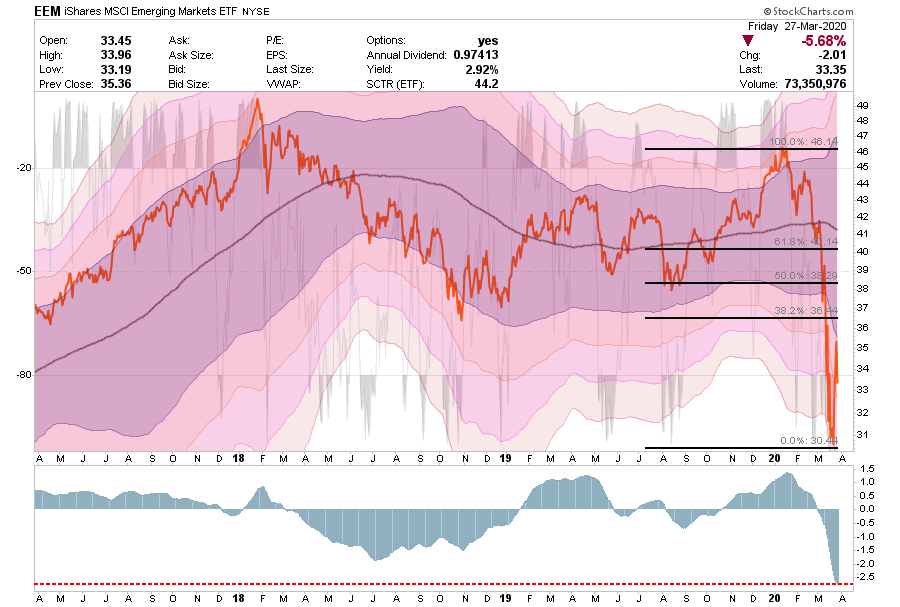

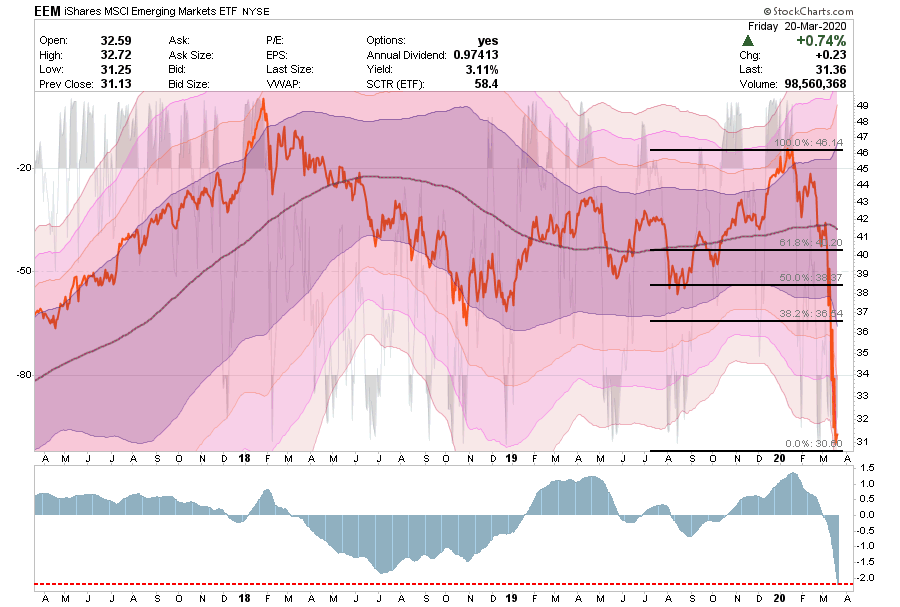

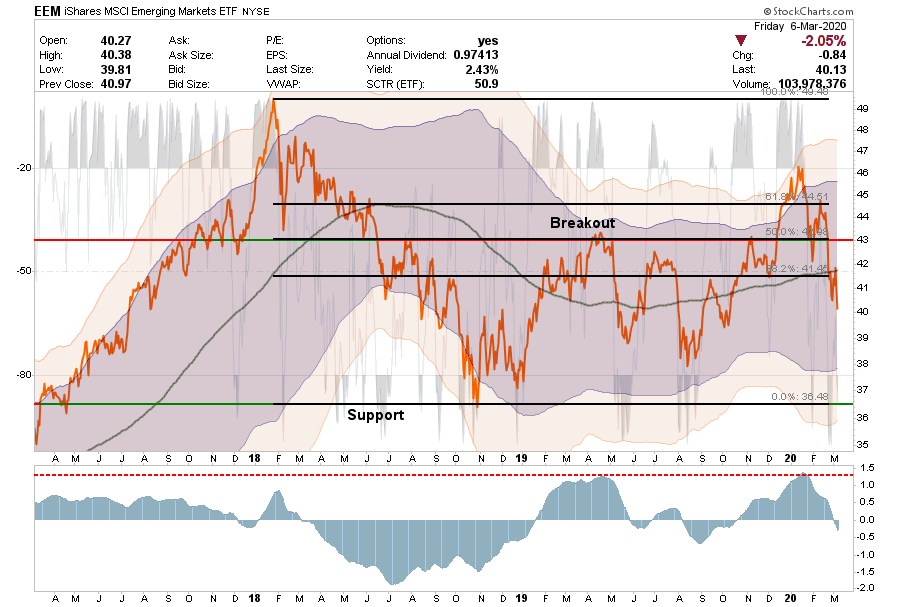

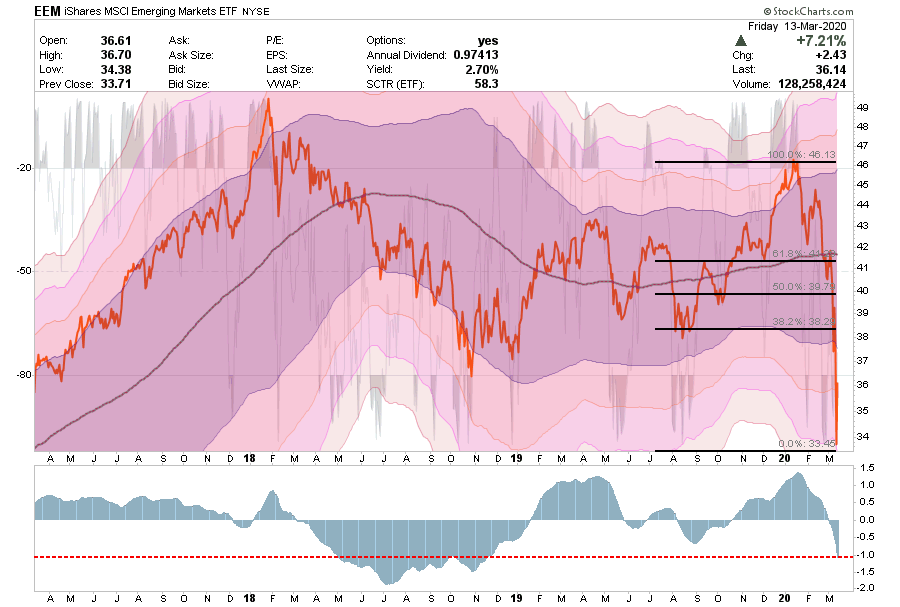

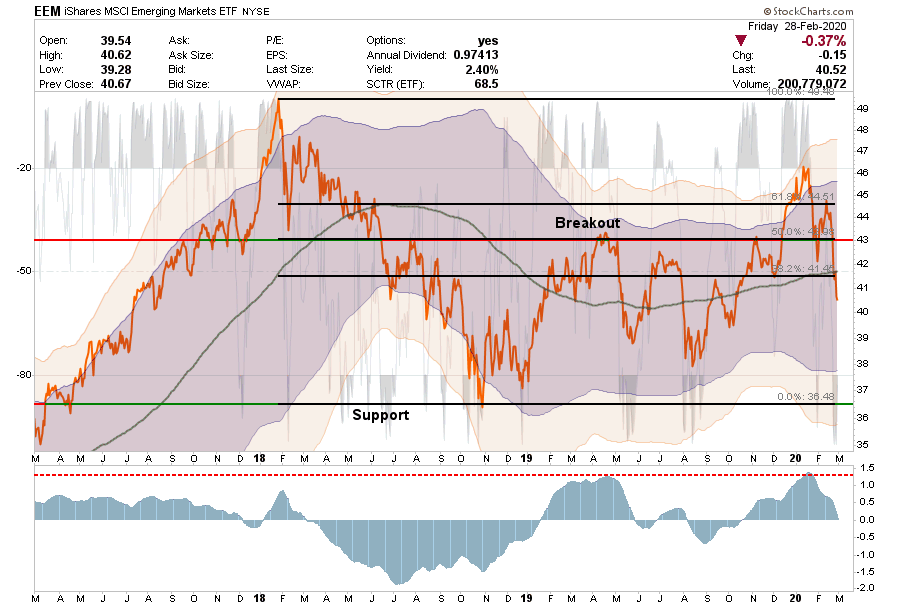

Emerging Markets

As with small and mid-cap stocks, emerging and international markets are being hit hard by the virus. Economically, these countries are being destroyed right now.

We previously stated that investors should use counter-trend rallies to sell into. If you haven’t done so, do so Monday. Relative performance remains exceedingly weak.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position.

Stop-loss moved up to $33 for trading positions.

Long-Term Positioning: Bearish

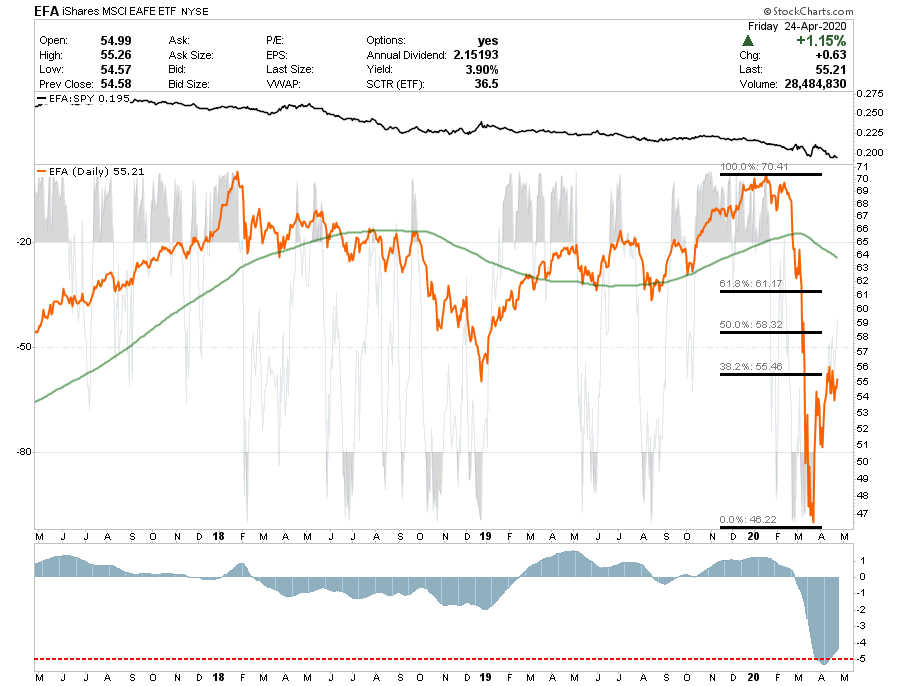

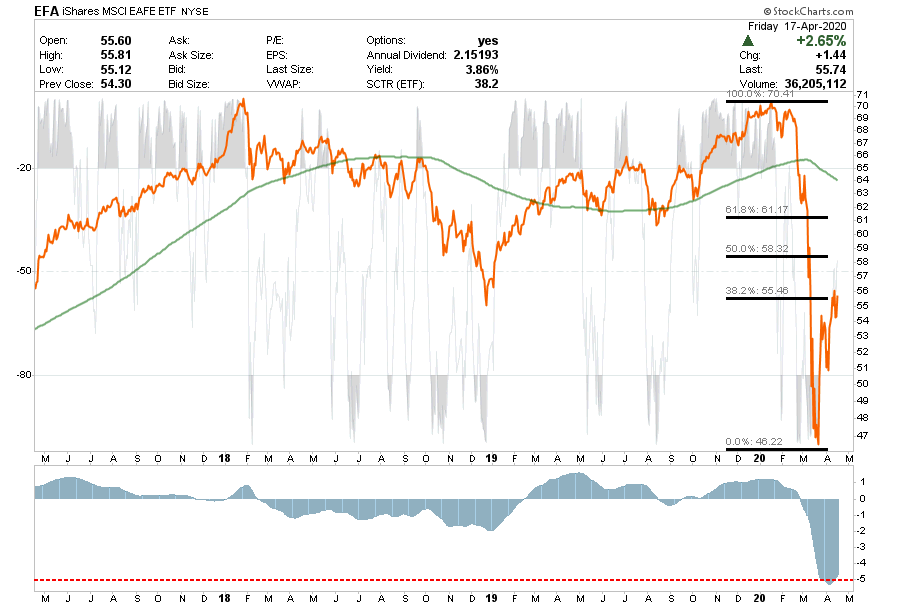

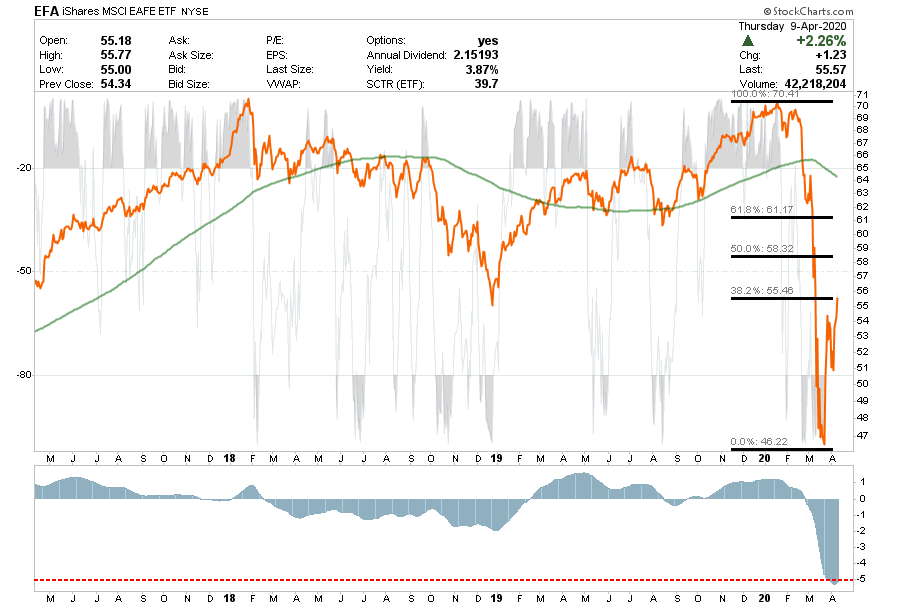

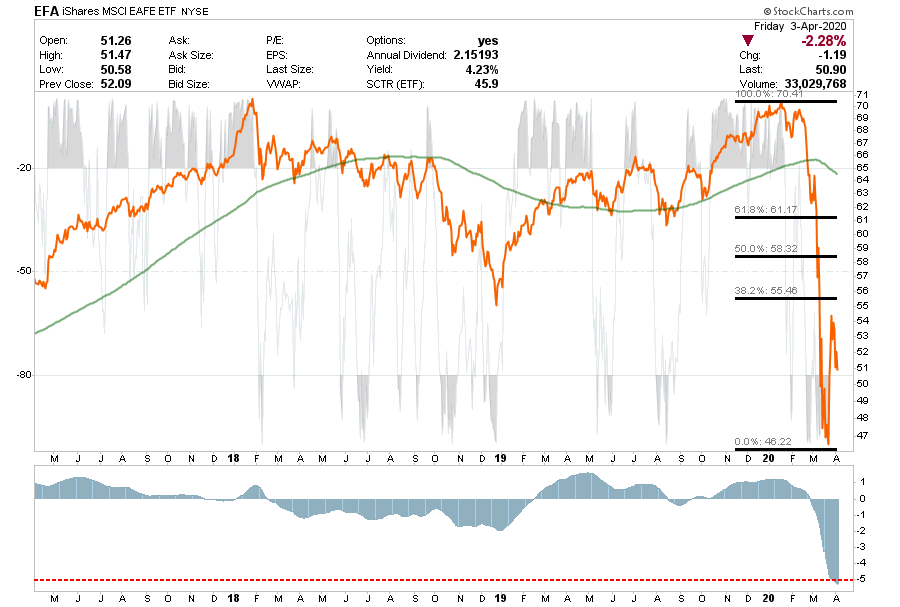

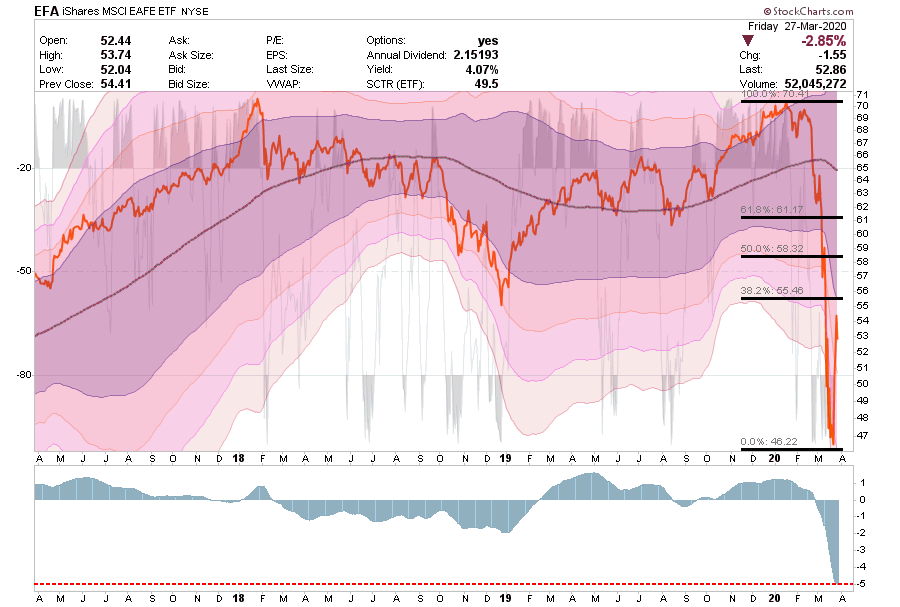

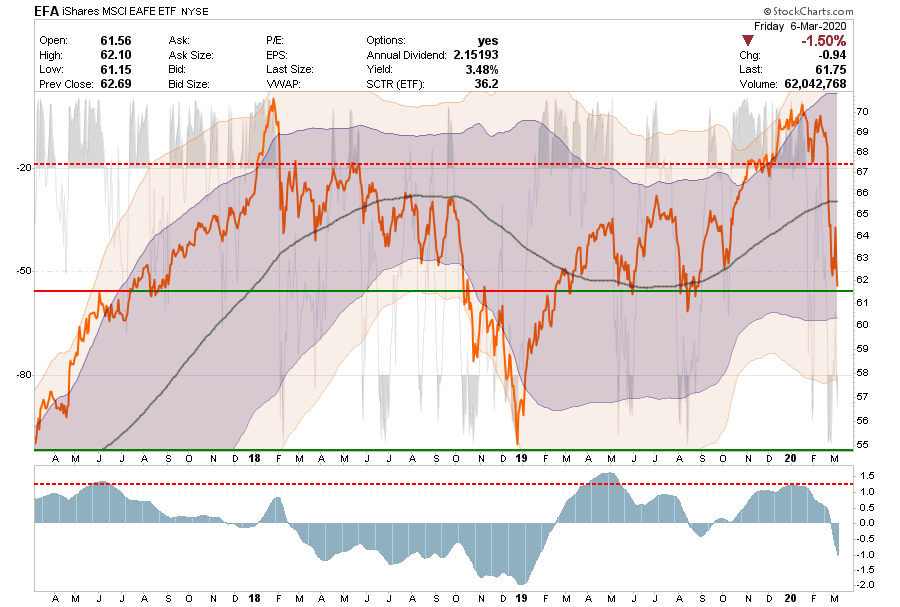

International Markets

Same with EFA as with EEM.

The rally failed at the 28.2% retracement and relative performance remains exceedingly weak.

Remain out of these markets for the time being.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position.

This Week: No position.

Stop-loss moved up to $51 for trading positions.

Long-Term Positioning: Bearish

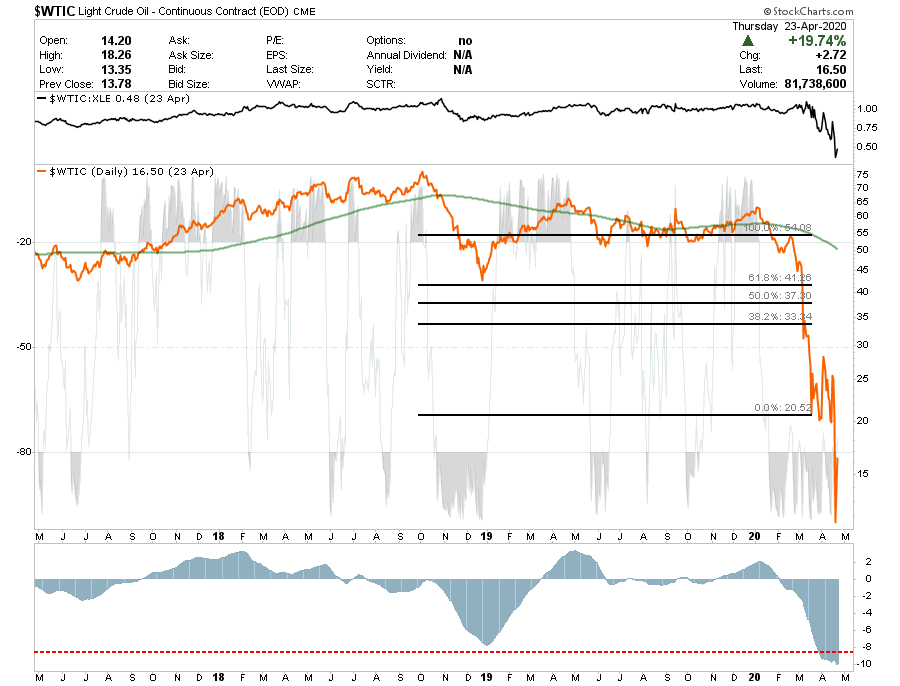

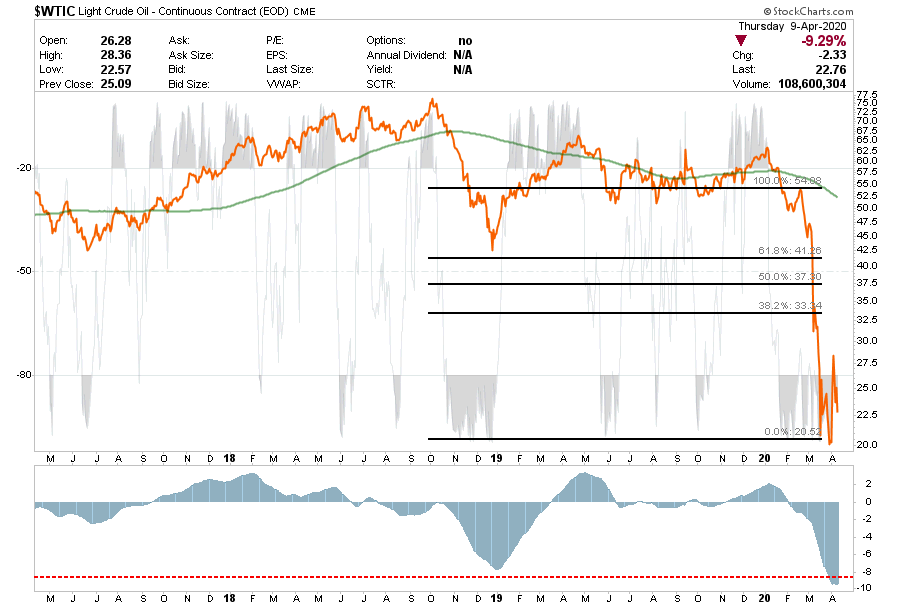

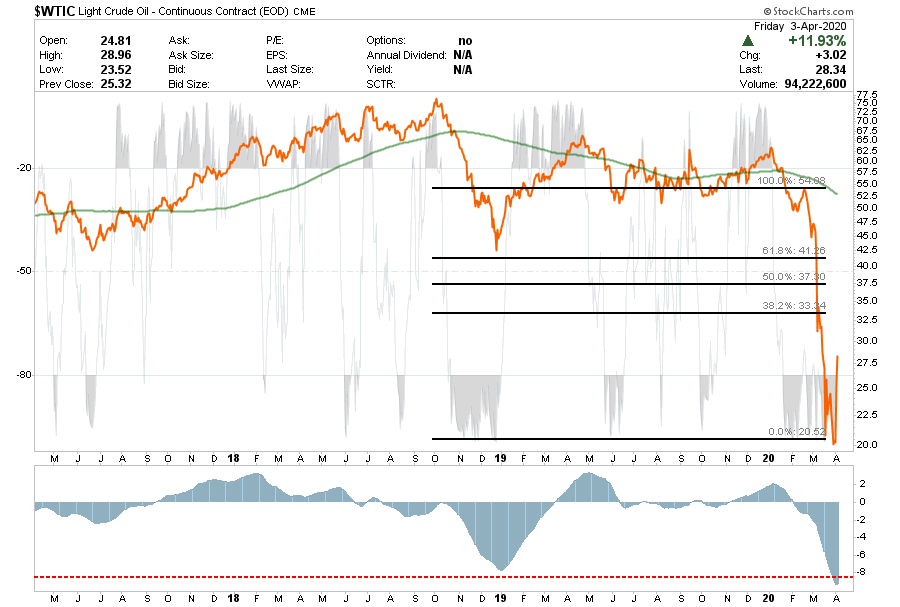

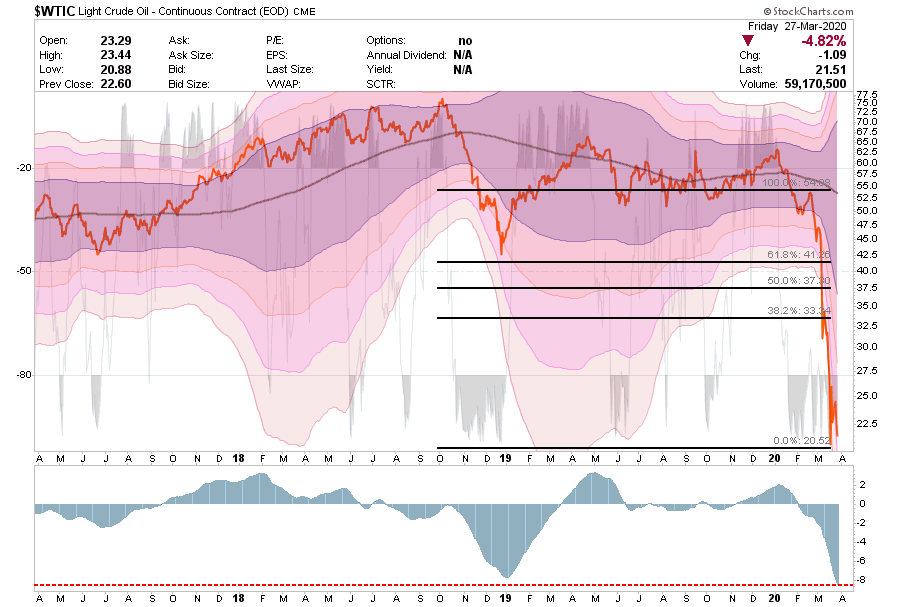

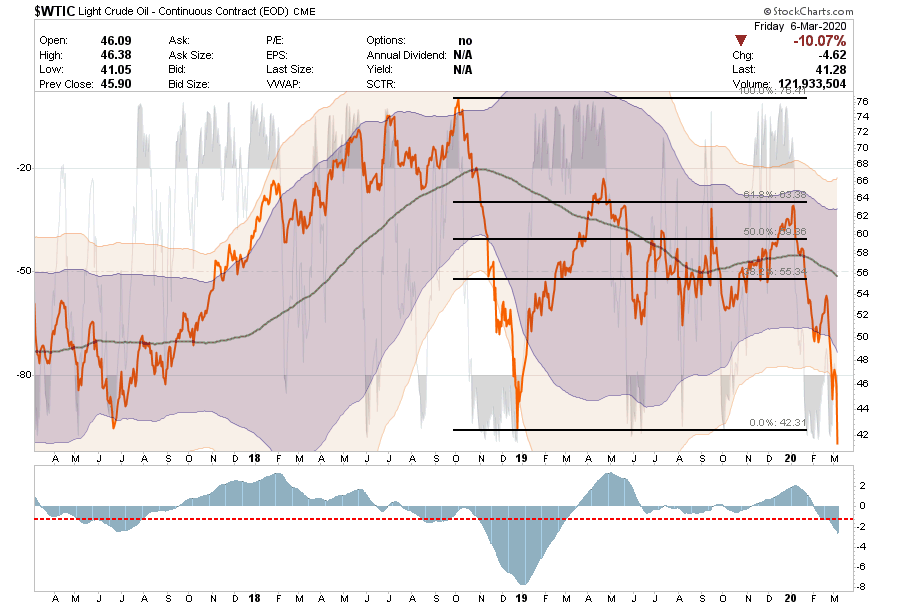

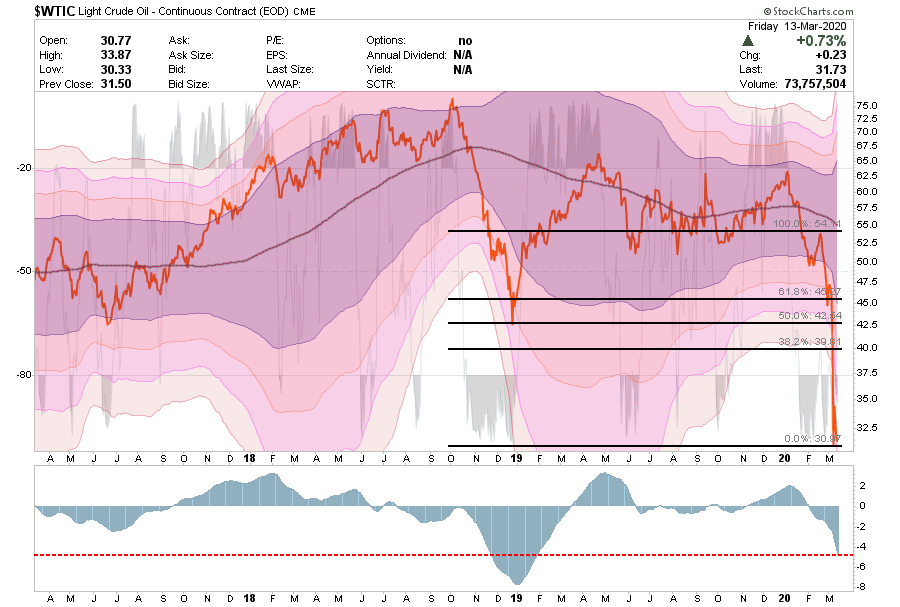

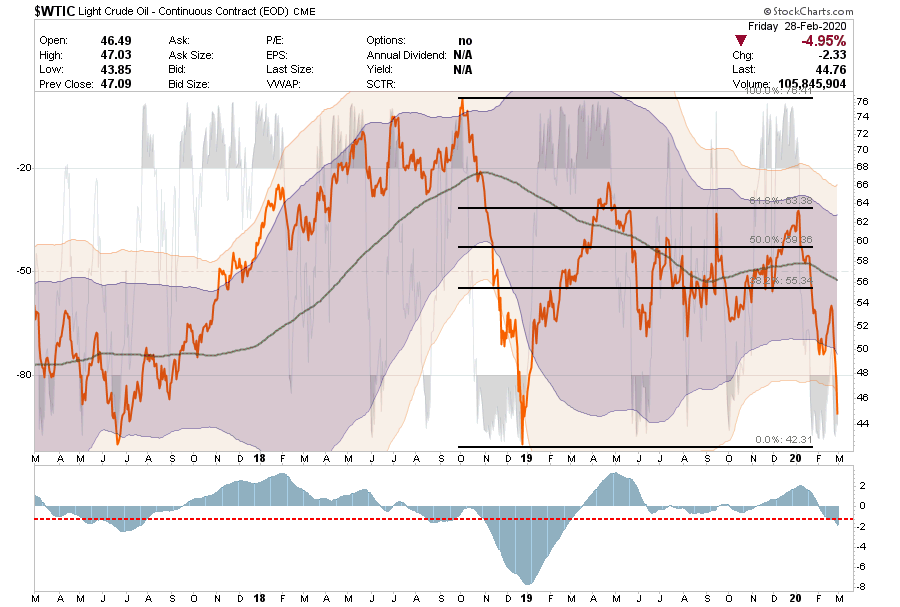

West Texas Intermediate Crude (Oil)

This past week, saw oil prices collapse and then rally back as futures contracts rolled from May to June. That’s the good news, the bad news is that oil prices are going to go lower again as we head into May and storage remains a problem.

We continue to suggest using any rally to clear positions in your portfolio for now.

We have not changed out stance on the sector from a “value” perspective, however, and this past week we nibbled into XOM, CVX, and XLE as oil stocks had exceedingly strong relative performance relative to oil. This suggests most of the risk has been pulled out of the sector. We are still carrying very tight stops though.

Short-Term Positioning: Bearish

Last Week: No positions

This Week: XOM, CVX, and XLE

Stops Triggered for any direct crude oil positions.

Long-Term Positioning: Bearish

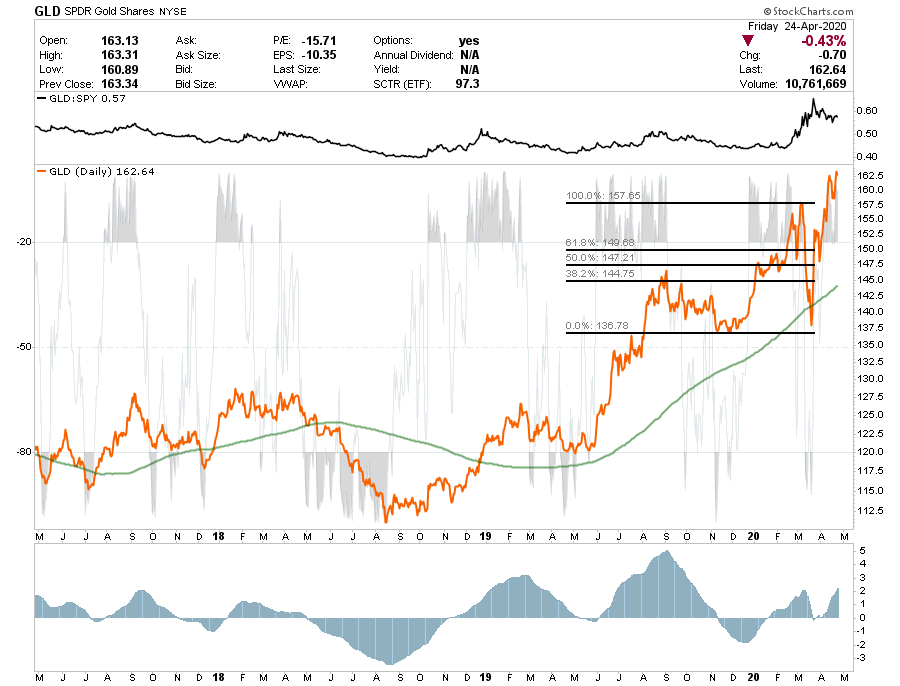

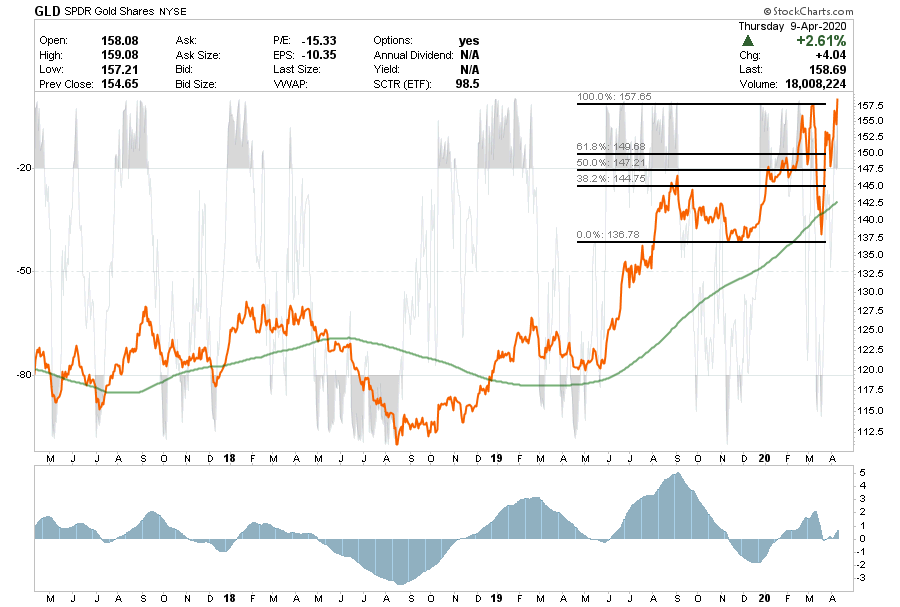

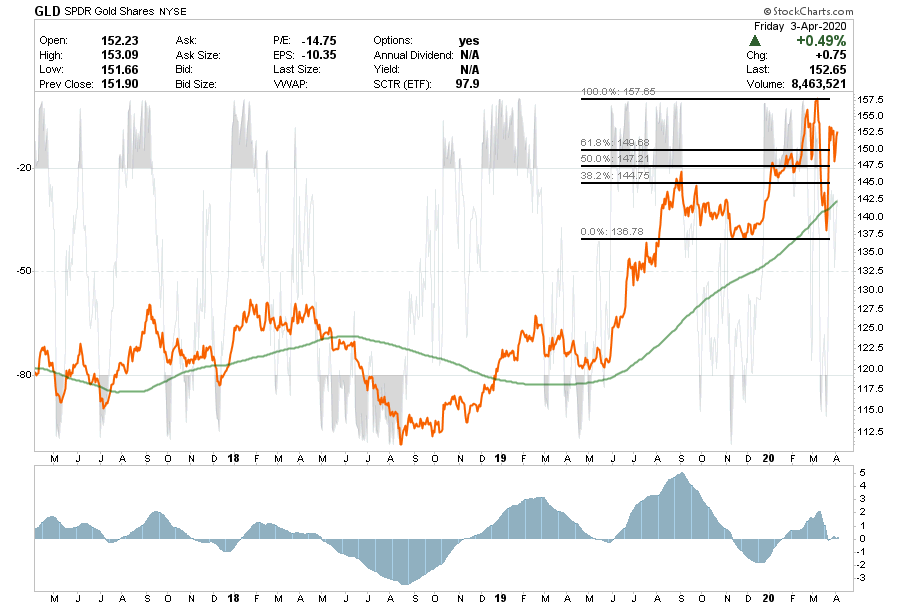

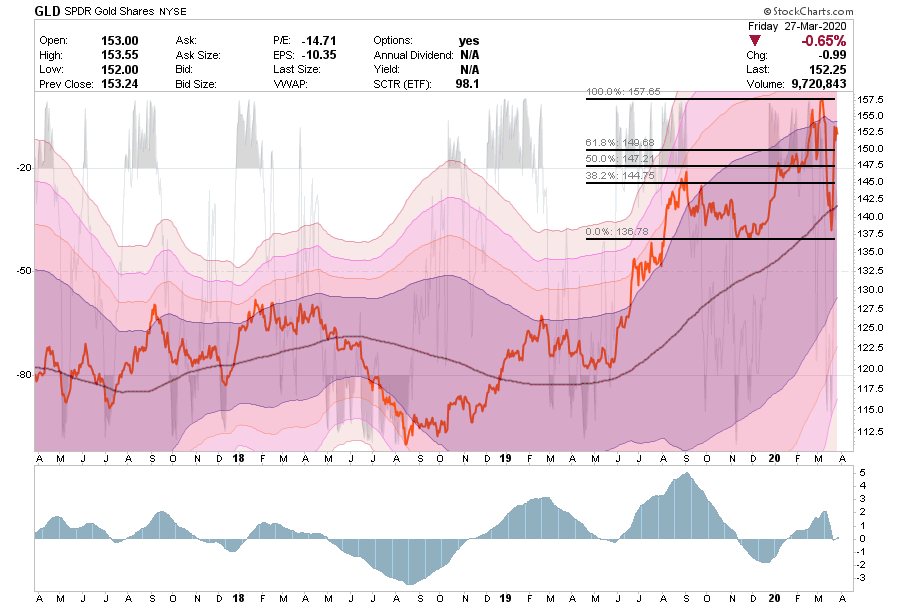

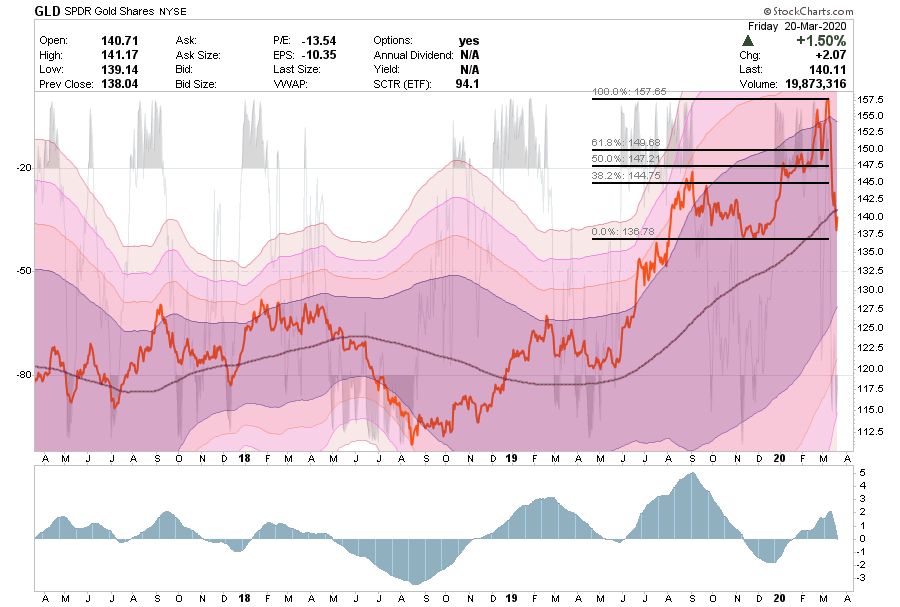

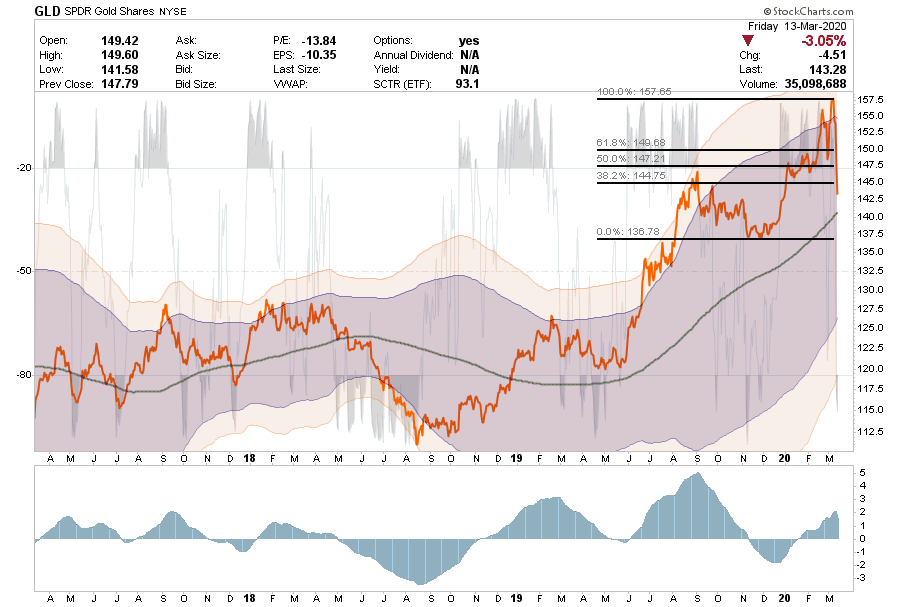

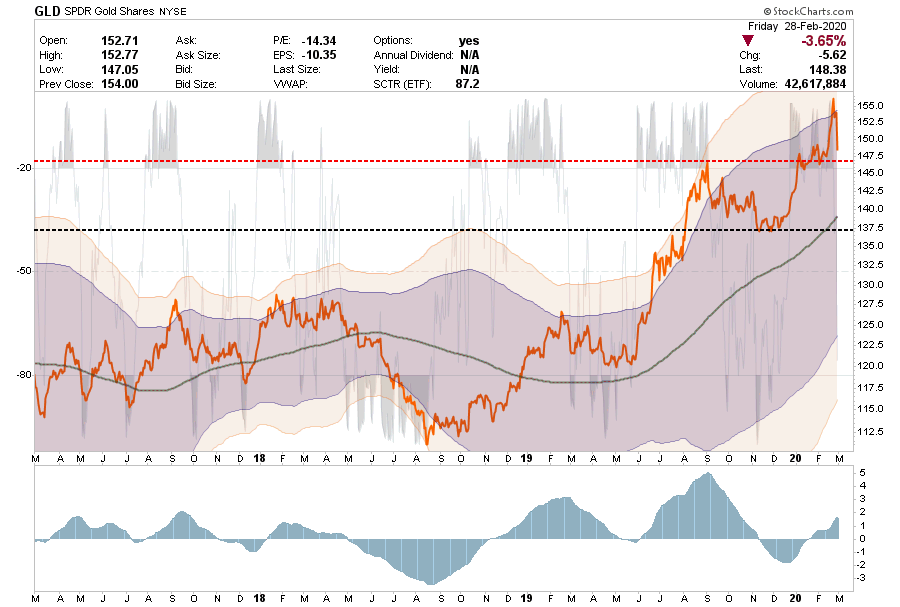

Gold

We previously added to our positions in IAU and GDX.

This past week Gold broke out to new highs as inflationary concerns continue to persist.

The sectors are VERY overbought short-term so a pullback is likely that can be used to add to current holdings.

Short-Term Positioning: Bullish

Last week: Hold positions.

This week: Hold positions – Positions can now be added at 157.50

Stop-loss moved up to $150

Long-Term Positioning: Bullish

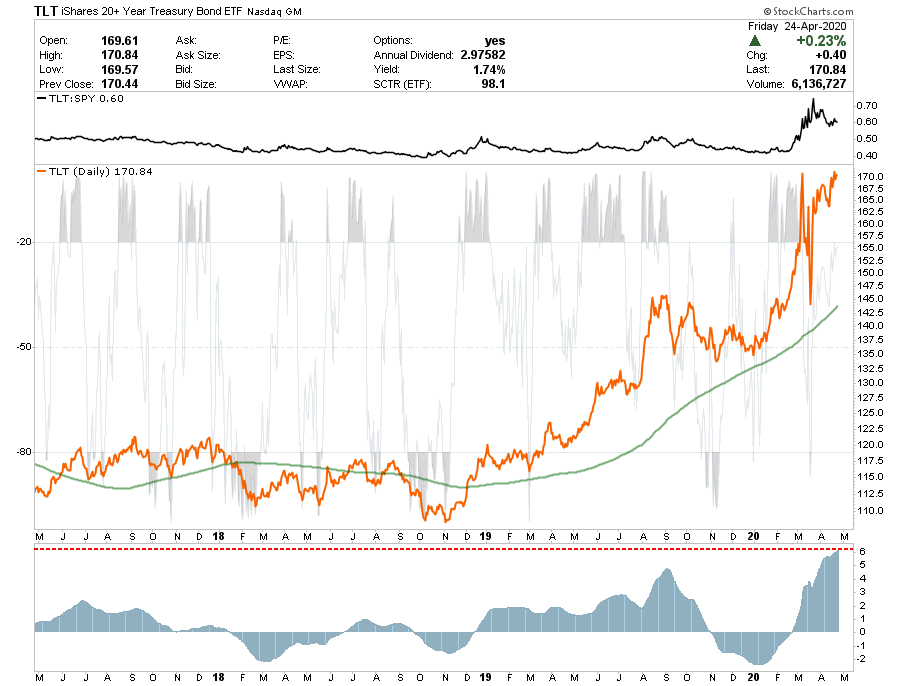

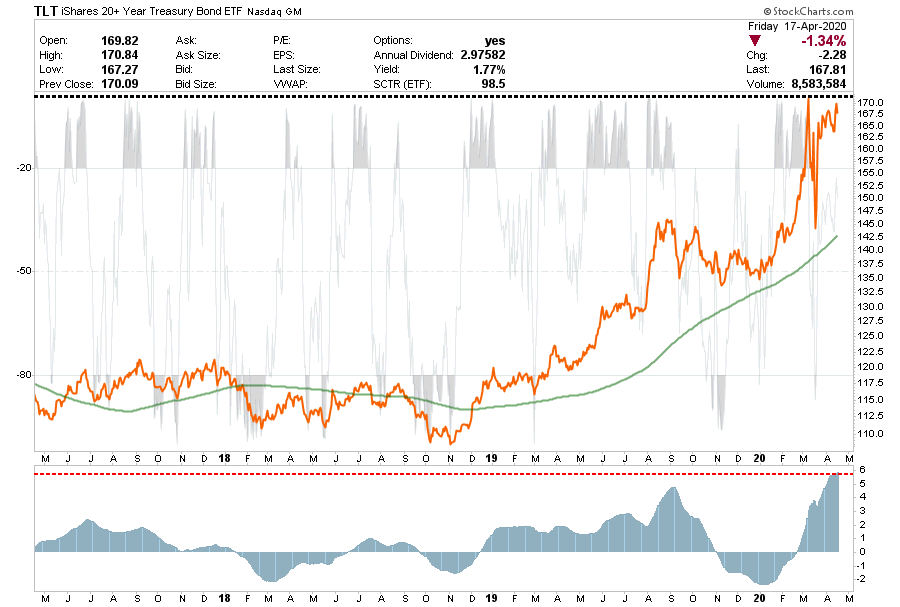

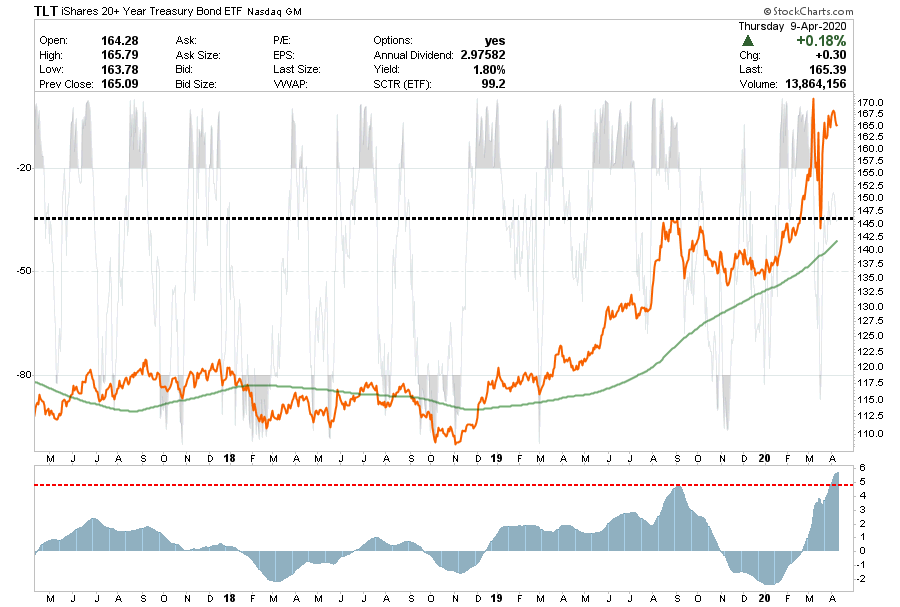

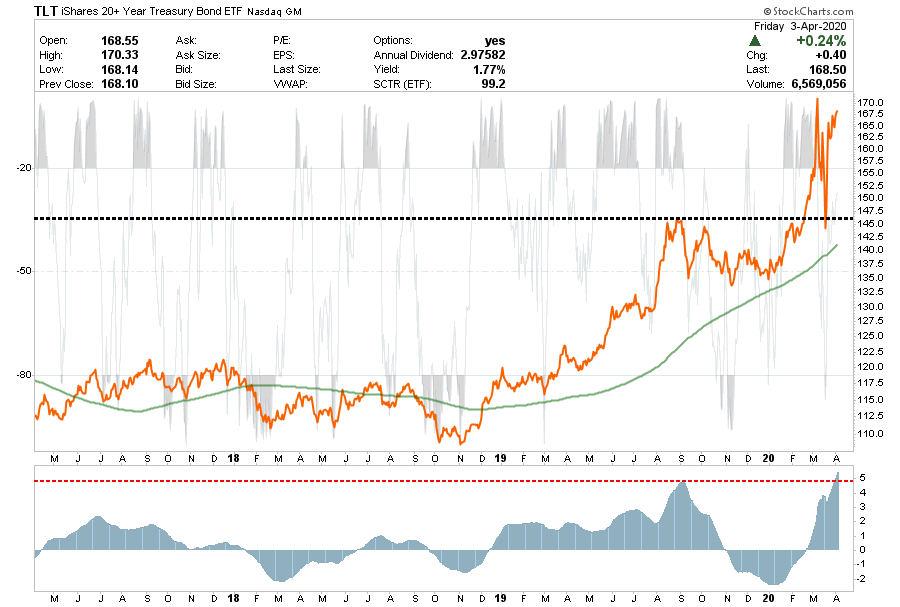

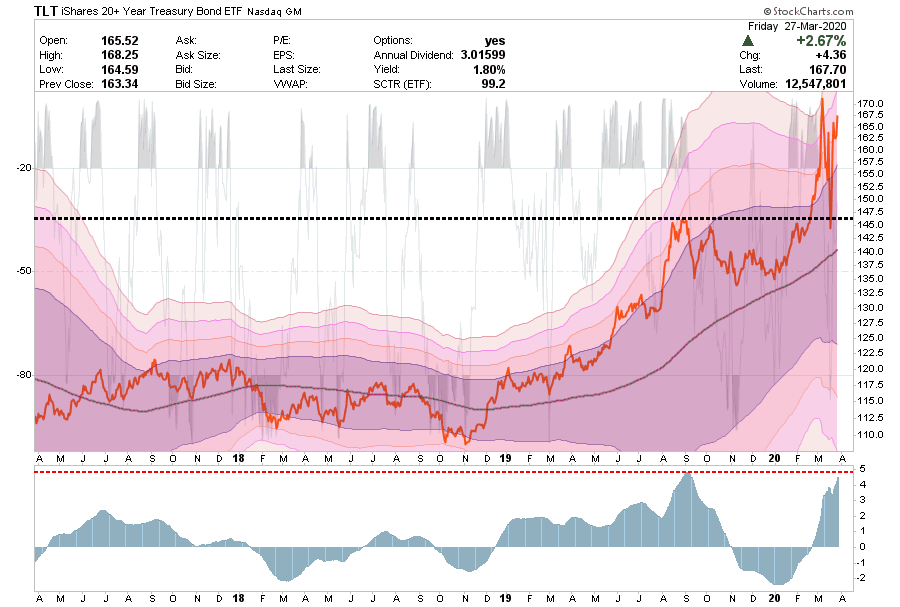

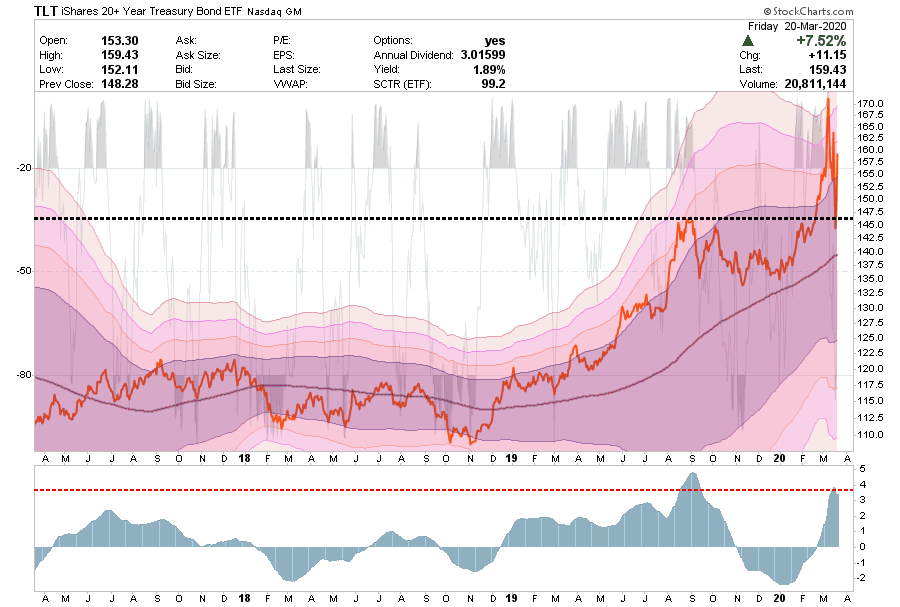

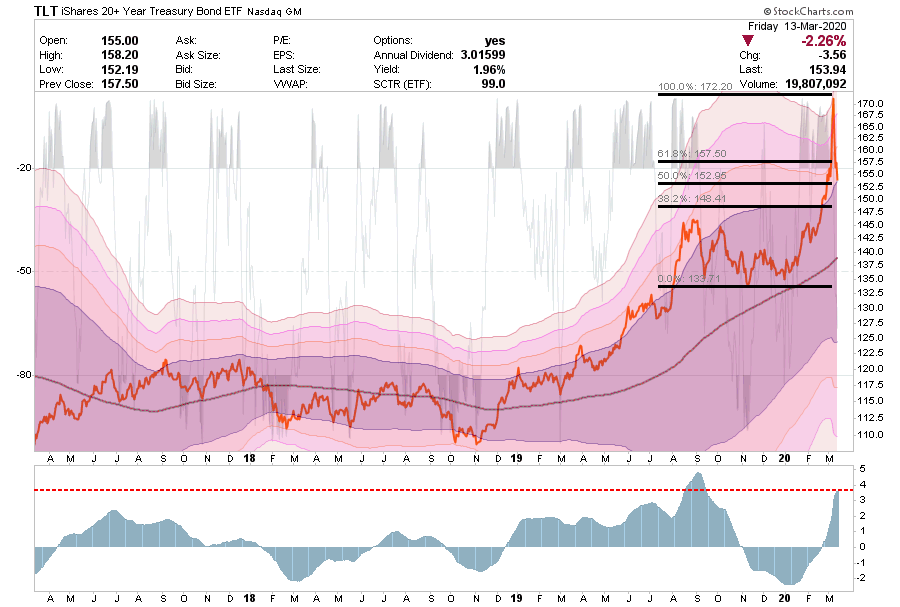

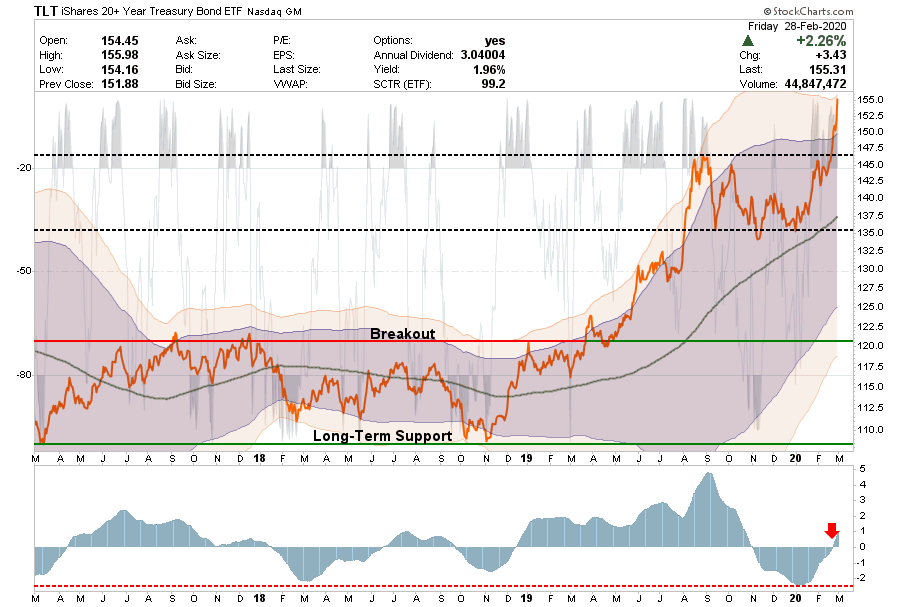

Bonds (Inverse Of Interest Rates)

Bonds are back to “crazy” overbought with the Fed buying everything from the banks who are happy to mark-up prices and sell it to them.

As we have been adding equity exposure to portfolios, we needed to increase our “hedge” against equity risk accordingly. We added a 5% position of TLT on Friday for just this reason.

Short-Term Positioning: Neutral

Last Week: Hold positions

This Week: Added 5% position of TLT

Stop-loss is $152.50

Long-Term Positioning: Bullish

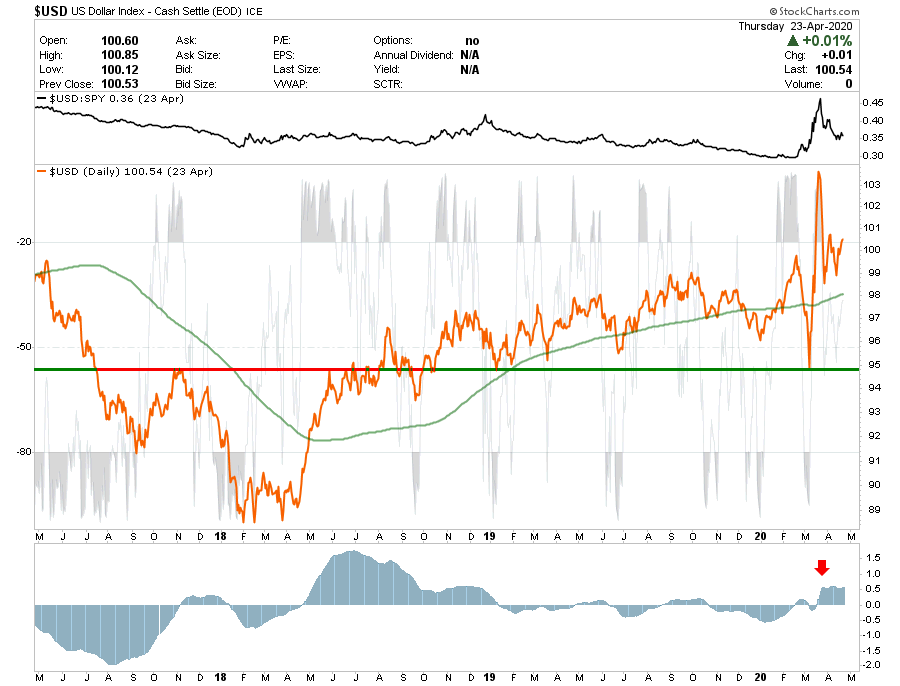

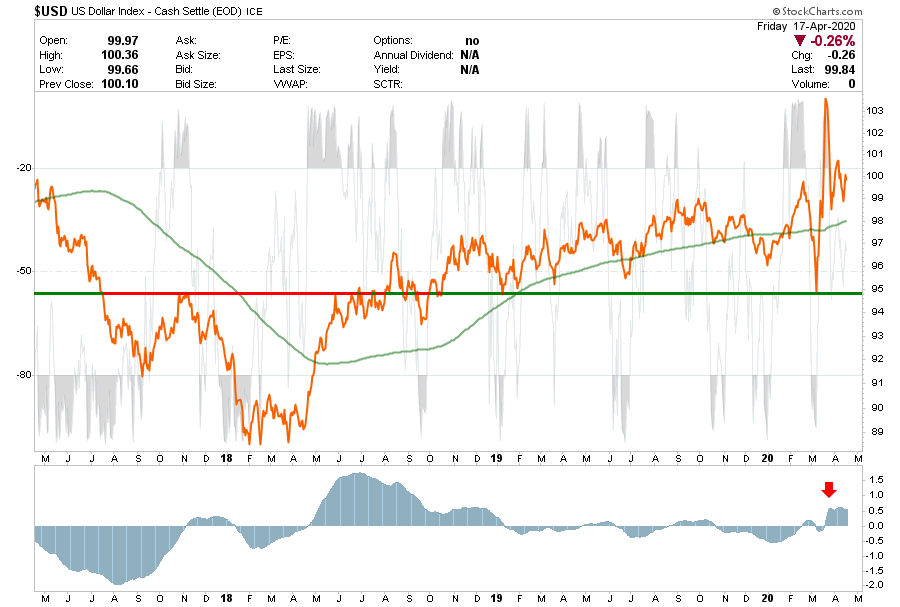

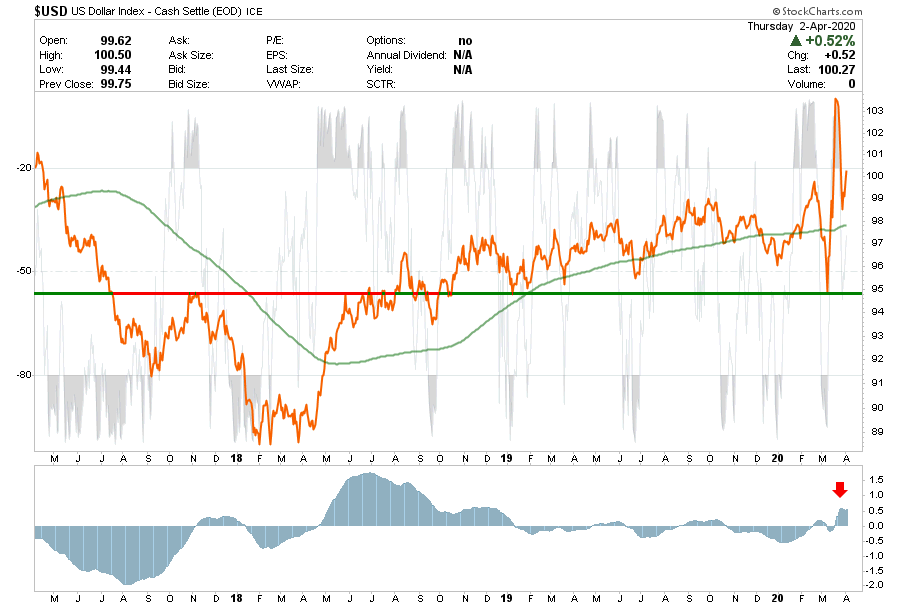

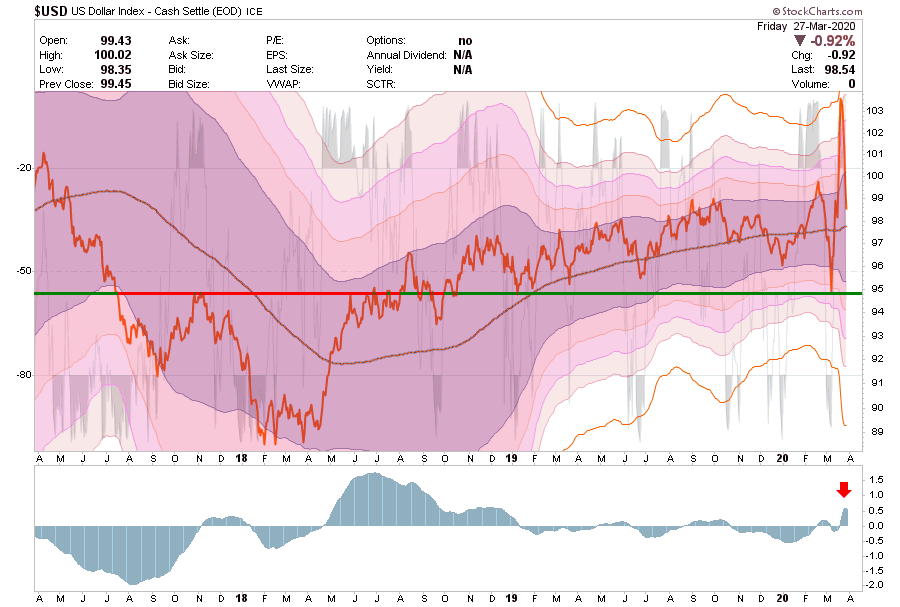

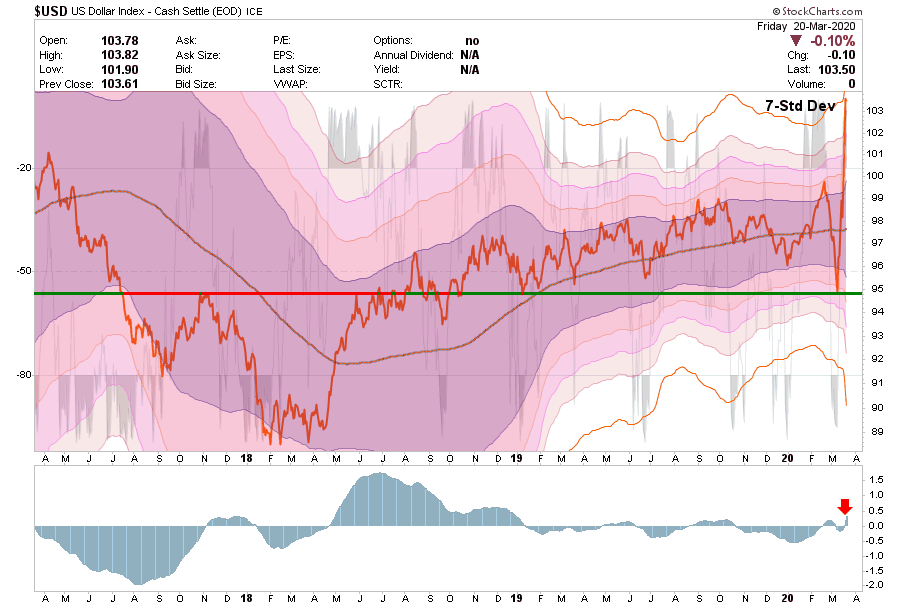

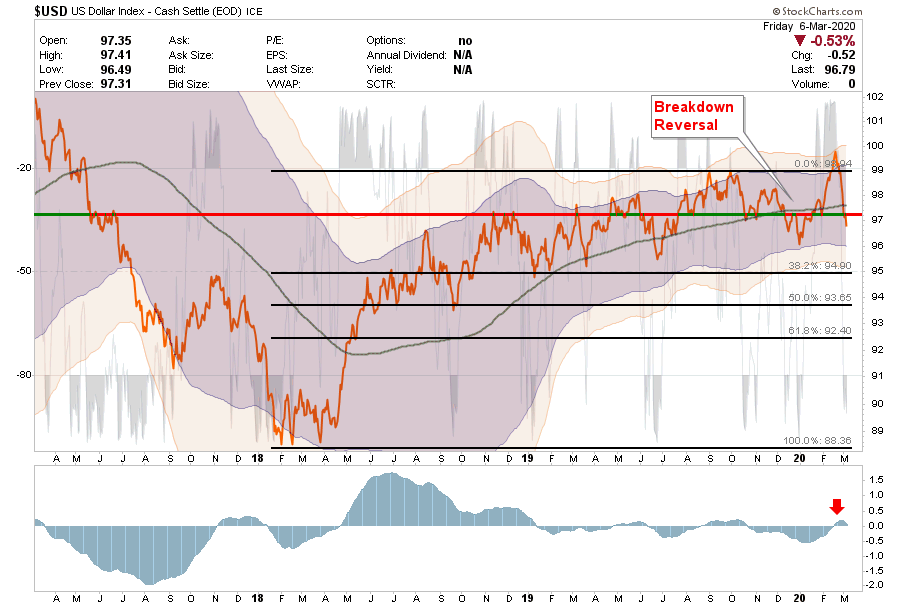

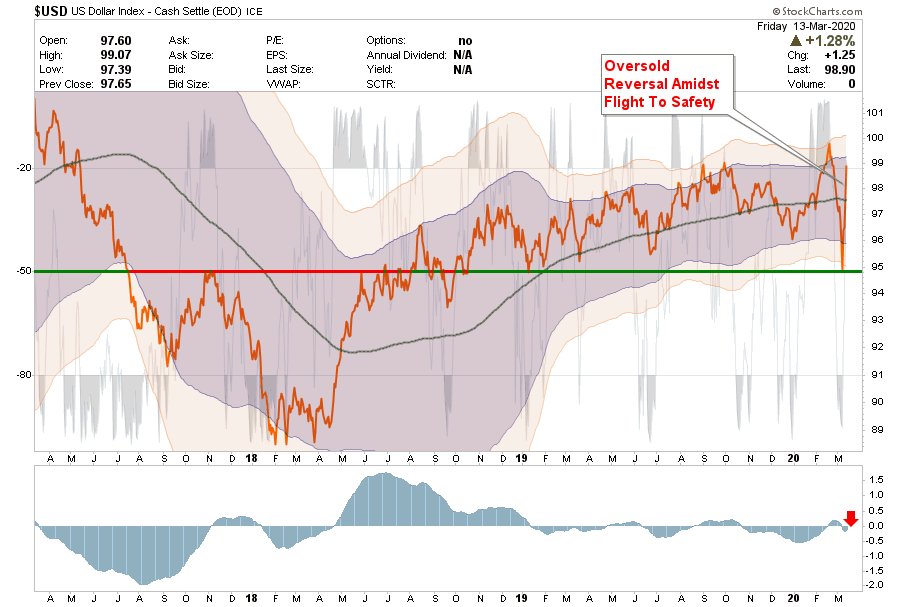

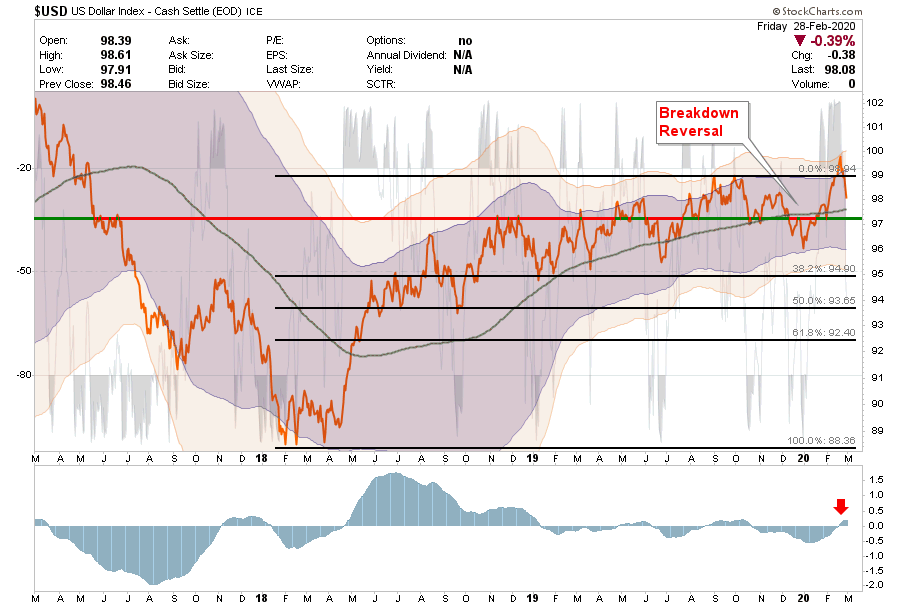

U.S. Dollar

We added a position last week to the Dollar to hedge against the global dollar shortage issue.

When the gray indicator is at the TOP of the chart, there is typically more risk and less reward available at the current time. In other words, the best time to BUY is when the short-term condition is over-sold. Likewise when the buy/sell indicator is above the ZERO line investments have a tendency of working better than when below the zero line.

With this basic tutorial let’s review the major markets.

S&P 500 Index

Last week I wrote: “This past week, the market was able to muster a rally to the 50% retracement level, and on many short-term fronts is extremely overbought. While a retest, and potential break of the March lows is likely, the market does have some lift short-term.”

The break of the 50% retracement this past week, is bullish and suggests a run to the 200-dma is likely. However, the risk/reward is not in the favor of longer-term positions, so trading positions only for now.

This still doesn’t negative the risk of more volatility ahead, so be prepared for quick declines, so keep trading stops tight.

Remain cautious for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No core position

This Week: Trading “Rentals” Only

Stop-loss moved up to $278

Long-Term Positioning: Bearish

Dow Jones Industrial Average

The same situation exists with DIA.

The break of the 50% retracement sets up a run to the 200-dma.

Trading “rentals” only for now with a tight stop at $238

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: Trading “Rentals” Only

Stop-loss moved up to $238

Long-Term Positioning: Bearish

Nasdaq Composite

As we have noted previously, QQQ is by far “the best index in town,” technically speaking.

Last week’s break above the 200-dma and the 61.8% sets up a test of “all-time” highs. (Pretty incredible when you think about the amount of economic devastation that is coming.)

But, from a trading perspective, “What is…is.”

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: Trading “Rentals” Only

Stop-loss moved up to $200

Long-Term Positioning: Bearish due to valuations

S&P 600 Index (Small-Cap)

No change to our positioning on Small-caps which are still “no place to be as both small and mid-cap companies are going to be hardest hit by the virus.”

Be careful what you own.

Avoid small-caps. Use last week’s rally to clear positions for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop loss adjusted to $44 on trading positions.

Long-Term Positioning: Bearish

S&P 400 Index (Mid-Cap)

As with Small-cap, we have no holdings. Use last week’s rally to sell positions.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No holding

This Week: No holding

Stop Loss moved up to $245 for trading positions.

Long-Term Positioning: Bearish

Emerging Markets

As with small and mid-cap stocks, emerging and international markets are being hit hard by the virus. Economically, these countries are being destroyed right now.

We previously stated that investors should use counter-trend rallies to sell into. If you haven’t done so, use last week’s rally to clear positions.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position.

Stop-loss moved up to $33 for trading positions.

Long-Term Positioning: Bearish

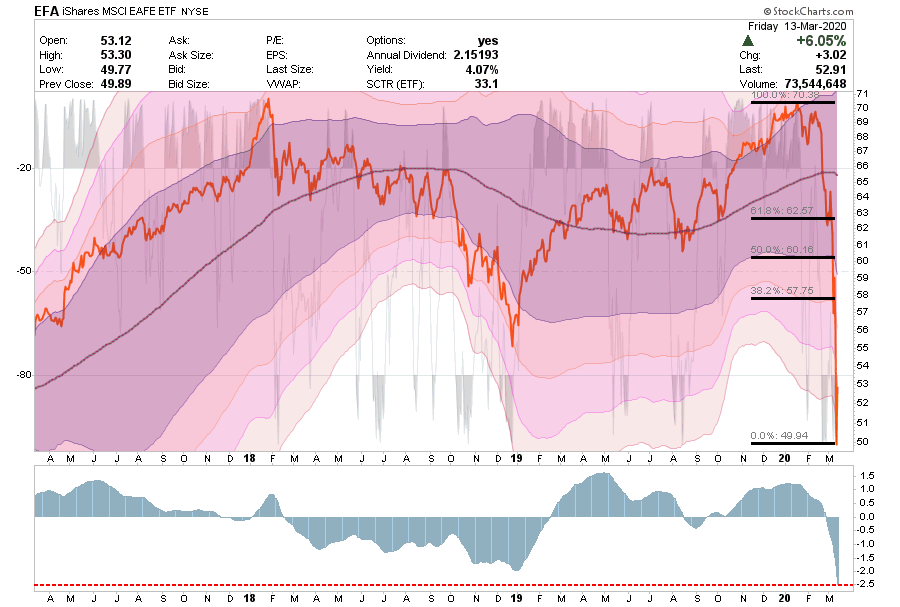

International Markets

As noted previously: “A reflexive rally is likely. Use those levels to sell into.”

Use last week’s rally to sell holdings.

Remain out of these markets for the time being.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position.

This Week: No position.

Stop-loss moved up to $51 for trading positions.

Long-Term Positioning: Bearish

West Texas Intermediate Crude (Oil)

The “spike” in oil prices on Friday was due to the change in oil futures contracts from May to June. Oil actually declined on Friday with the May contract at $17/bbl.

Regardless, $25 is the price for June delivery of oil. Without any help on the horizon, look for the June contract to head back towards $20/bbl.

We continue to suggests using any rally to clear positions in your portfolio for now.

We have not changed out stance on the sector from a “value” perspective, however, the sector still has work to do, so be patient.

Avoid for now.

Short-Term Positioning: Bearish

Last Week: No positions

This Week: No positions.

Stops Triggered for any direct crude oil positions.

Long-Term Positioning: Bearish

Gold

We previously added to our positions in IAU and GDX.

The sectors are VERY overbought short-term so a pullback is likely that can be used to add to current holdings.

Short-Term Positioning: Bullish

Last week: Hold positions.

This week: Hold positions – Look at add if support holds at $150

Stop-loss moved up to $147.50

Long-Term Positioning: Bullish

Bonds (Inverse Of Interest Rates)

Bonds are back to “crazy” overbought with the Fed buying everything from the banks who are happy to mark-up prices and sell it to them.

Bond prices will correct and provide a better entry point to add exposure. So, be patient for now. Short-Term Positioning: Neutral

Last Week: Hold positions

This Week: Take Profits and rebalance holdings as needed.

When the gray indicator is at the TOP of the chart, there is typically more risk and less reward available at the current time. In other words, the best time to BUY is when the short-term condition is over-sold. Likewise when the buy/sell indicator is above the ZERO line investments have a tendency of working better than when below the zero line.

With this basic tutorial let’s review the major markets.

S&P 500 Index

Previously we wrote: “Well, that bounce finally came and it was as vicious as we expected. While this remains a “bear market” rally, the media was quick to jump on the “Bear market is over” bandwagon. It isn’t, and investors will likely pay a dear price in April.”

This past week, the market was able to muster a rally to the 50% retracement level, and on many short-term fronts is extremely overbought. While a retest, and potential break of the March lows is likely, the market does have some lift short-term.

Despite the Fed flooding money into the system, we could be set up for some very volatile moves as the economic data is about to become horrific, and earnings estimates will be revised sharply lower.

Remain cautious for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No core position

This Week: No core position

Stop-loss moved up to $245

Long-Term Positioning: Bearish

Dow Jones Industrial Average

The same situation exists with DIA.

The bounce we discussed previously retraced to the 50% retracement level. We could see some positive action on Monday, but we remain firmly entrenched in a bear market for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop-loss moved up to $210

Long-Term Positioning: Bearish

Nasdaq Composite

We had previously put on a small QQQ trade for a reflexive rally, but we closed that out.

As with SPY and DIA, the QQQ has established a downtrend, but technically is in MUCH better shape than the other markets with the bull-trend still intact.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions

Stop-loss moved up to $180

Long-Term Positioning: Bearish due to valuations

S&P 600 Index (Small-Cap)

Small-caps are no place to be as both small and mid-cap companies are going to be hardest hit by the virus.

Be careful what you own, there are going to be quite a few companies that don’t make it.

Avoid small-caps. Use last week’s rally to clear positions for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop loss adjusted to $44 on trading positions.

Long-Term Positioning: Bearish

S&P 400 Index (Mid-Cap)

As with Small-cap, we have no holdings. Use last week’s rally to sell positions.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No holding

This Week: No holding

Stop Loss moved up to $245 for trading positions.

Long-Term Positioning: Bearish

Emerging Markets

As with small and mid-cap stocks, emerging and international markets are being hit hard by the virus. Economically, these countries are being destroyed right now.

We previously stated that investors should use counter-trend rallies to sell into. If you haven’t done so, use last week’s rally to clear positions.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position.

Stop-loss moved up to $33 for trading positions.

Long-Term Positioning: Bearish

International Markets

As noted previously: “‘A reflexive rally is likely. Use those levels to sell into.”

Use last week’s rally to sell holdings.

Remain out of these markets for the time being.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position.

This Week: No position.

Stop-loss moved up to $51 for trading positions.

Long-Term Positioning: Bearish

West Texas Intermediate Crude (Oil)

As stated last week, “Saudi and Russia are NOT likely going to cut production meaningfully as they now have shale drillers in a stranglehold. They are going to talk a lot, but they aren’t going to do anything until they extinguish shale to some degree. For the last couple of years, I have warned this outcome would eventually occur.”

Shockingly they did come to an agreement, but it may be too little ,too late and whose to say that member OPEC countries adhere to their commitments.

We also stated to use the rally last week to clear positions in your portfolio for now stating:

“We will very likely retest or set new lows in the coming months as drillers are forced to “shut in” production. At that point we can start picking through the ruble for portfolio positioning.”

We still like the sector from a “value” perspective and expect that we will wind up making a lot of money here. We clearly aren’t at lows yet, so be patient.

Avoid for now.

Short-Term Positioning: Bearish

Last Week: No positions

This Week: No positions.

Stops Triggered for any direct crude oil positions.

Long-Term Positioning: Bearish

Gold

We added to our positions in IAU and GDX last week as the Fed’s action are starting to raise the specter of rather serious inflation problems.

Last week, Gold broke out to highs and brought the “buy signal” back online.

Gold is a little overbought short-term so use pullbacks to support to add further holdings.

Short-Term Positioning: Bullish

Last week: Hold positions.

This week: Hold positions.

Stop-loss moved up to $142.50

Long-Term Positioning: Bullish

Bonds (Inverse Of Interest Rates)

We have reduced our overall bond exposure, because we are running a very reduced equity exposure currently. This aligns our “hedge” of fixed income relative to our equity book.

However, bonds are now MORE overbought that at just about any other point in history which suggests we could see a tick up in rates and a fall in bond prices. (Such will provide a good opportunity to add bond exposure to portfolios.)

Normally, such a reversion would coincide with a “risk on” trade into equities. However, given the economic devastation coming, we need to look back at 2008. In November of 2008, the Fed hit the markets with QE which caused bonds and stocks to rise in unison. However, shortly thereafter, both declined sharply in price as economic realities came to the fore.

Short-Term Positioning: Neutral

Last Week: Hold positions

This Week: Take Profits and rebalance holdings as needed.

Stop-loss is $147.50

Long-Term Positioning: Bullish

U.S. Dollar

The dollar fell sharply as we had a reflexive “bear market” rally. However, with concerns over the deteriorating global economy and the demand for dollars from abroad, money is flowing back into the dollar for safety.

The recent volatility of the dollar makes it hard to trade for now, so be patient for the moment and let things calm down. We may look to add a long-dollar trade on a pull back to the $98-99 areas.

The dollar is on a strong “buy signal” and is NOT “overbought,” which suggests dollar strength may be with us for a while longer.

Major Market Buy/Sell Review: 04-06-20

HOW TO READ THE CHARTS

There are three primary components to each chart:

The price chart is in orange

The Over Bought/Over Sold indicator is in gray

The Buy / Sell indicator is in blue.

When the gray indicator is at the TOP of the chart, there is typically more risk and less reward available at the current time. In other words, the best time to BUY is when the short-term condition is over-sold. Likewise when the buy/sell indicator is above the ZERO line investments have a tendency of working better than when below the zero line.

With this basic tutorial let’s review the major markets.

S&P 500 Index

Last week: “Well, that bounce finally came and it was as vicious as we expected. While this remains a “bear market” rally, the media was quick to jump on the “Bear market is over” bandwagon. It isn’t, and investors will likely pay a dear price in April.”

After running into the bullish trend line and the initial 38.2% retracement, the market failed and has established a downtrend. A retest, and potential break of the March lows is likely, but we will monitor this carefully. With the Fed flooding money into the system, we could be set up for some very volatile moves, but the economic data is about to become horrific and earnings estimates will be revised sharply lower.

Remain cautious for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position

Stop-loss set at $220

Long-Term Positioning: Bearish

Dow Jones Industrial Average

The same situation exists with DIA.

The bounce we discussed previously retraced to the 38.2% retracement level and failed. We could see some positive action on Monday, but we remain firmly entrenched in a bear market for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop-loss set at $185

Long-Term Positioning: Bearish

Nasdaq Composite

We had previously put on a small QQQ trade for a reflexive rally, but we closed that out.

As with SPY and DIA, the QQQ has established a downtrend, but technically is in MUCH better shape than the other markets with the bull-trend still intact.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions

Stop-loss set at $170

Long-Term Positioning: Bearish due to valuations

S&P 600 Index (Small-Cap)

Small-caps have a lot more downside to go as both small and mid-cap companies are going to be hardest hit by the virus.

Be careful what you own, there are going to be quite a few companies that don’t make it.

Avoid small-caps. Use any reflexive rally to step-aside for the time being.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop loss adjusted to $42 on trading positions.

Long-Term Positioning: Bearish

S&P 400 Index (Mid-Cap)

As with Small-cap, we have no holdings.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No holding

This Week: No holding

Long-Term Positioning: Bearish

Emerging Markets

As with small and mid-cap stocks, emerging and international markets are being hit hard by the virus. Economically, these countries are being destroyed right now.

We previously stated that investors should use counter-trend rallies to sell into. If you haven’t done so, use any rally to clear positions.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position.

Stop-loss set at $30 for trading positions.

Long-Term Positioning: Bearish

International Markets

As noted last week: “‘A reflexive rally is likely. Use those levels to sell into. Do so this week.”

Remain out of these markets for the time being.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position.

This Week: No position.

Stop-loss set at $46 for trading positions.

Long-Term Positioning: Bearish

West Texas Intermediate Crude (Oil)

Last week, the President said he talked to Saudi Arabia and they were in talks with Russia to cut $10 million barrels of production. That tweet sparked a vicious rally in oil keeping prices above the critical level of $20.

Saudi and Russia are NOT likely going to cut production meaningfully as they now have shale drillers in a stranglehold. They are going to talk a lot, but they aren’t going to do anything until they extinguish shale to some degree. For the last couple of years, I have warned this outcome would eventually occur.

Use this rally in oil to clear positions in your portfolio for now. We will very likely retest or set new lows in the coming months as drillers are forced to “shut in” production. At that point we can start picking through the ruble for portfolio positioning.

We still like the sector from a “value” perspective and expect that we will wind up making a lot of money here. We clearly aren’t at lows yet, so be patient.

Avoid for now.

Short-Term Positioning: Bearish

Last Week: No positions

This Week: No positions.

Stops Triggered for any direct crude oil positions.

Long-Term Positioning: Bearish

Gold

We previously added to our position in IAU and continue to have a small holding in GDX, as the previous liquidation left a lot of value in the sector. However, performance remains lazy at this point, so we are looking for pullbacks to support to add to our holdings.

Short-Term Positioning: Bullish

Last week: Hold positions.

This week: Hold positions.

Stop-loss set at $137.50.

Long-Term Positioning: Bullish

Bonds (Inverse Of Interest Rates)

We have reduced our overall bond exposure, because we are running a very reduced equity exposure currently. This aligns our “hedge” of fixed income relative to our equity book.

We remain very cautious on our bond exposure currently, and will look to add to that exposure once the credit markets calm down a bit.

Short-Term Positioning: Neutral

Last Week: Hold positions

This Week: Hold positions

Stop-loss is moved up to $147.50

Long-Term Positioning: Bullish

U.S. Dollar

The dollar fell sharply as we had a reflexive “bear market” rally. However, with concerns over global economic strength rising, money is flowing back into the dollar for safety.

The recent volatility of the dollar makes it hard to trade for now, so be patient for the moment and let things calm down. We can look to add a long-dollar trade on a pull back to the $98-99 areas.

The dollar has reversed its sell signal, which suggests dollar strength may be with us for a while longer.

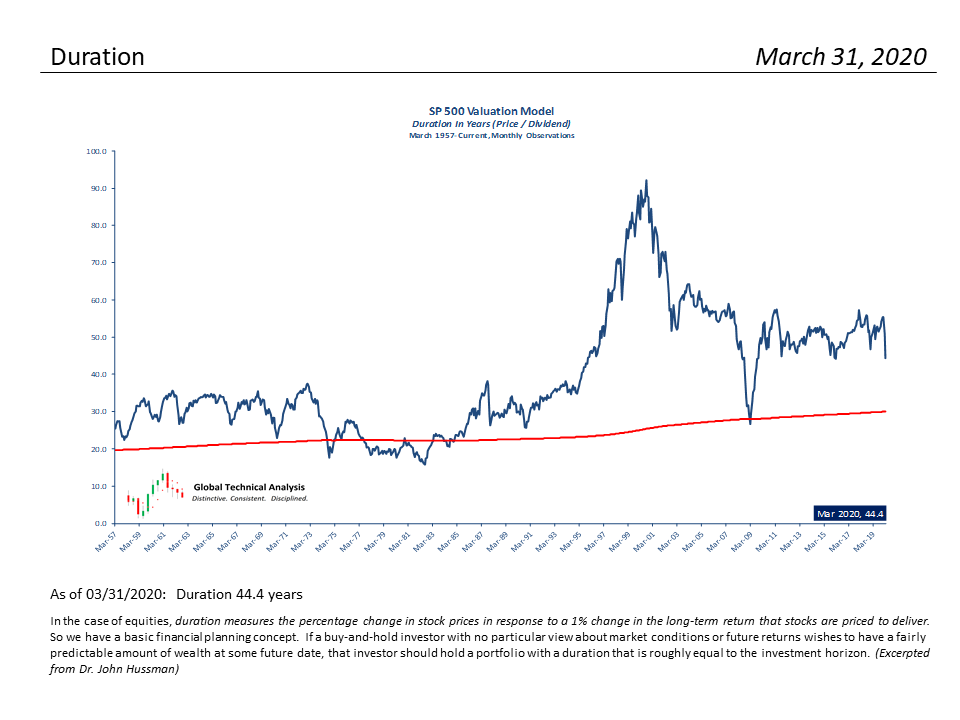

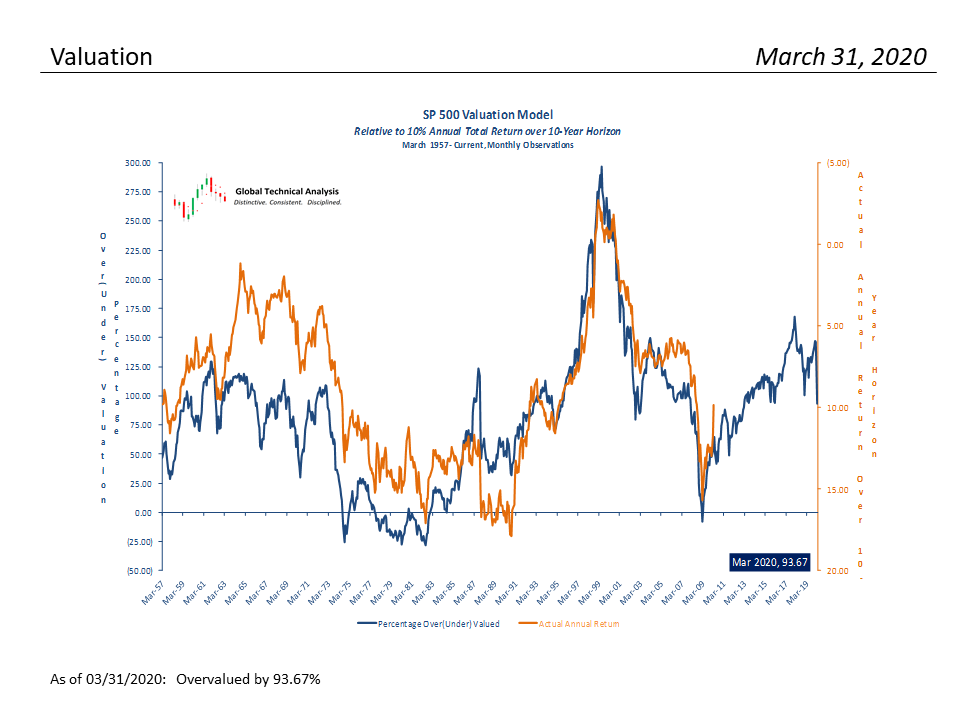

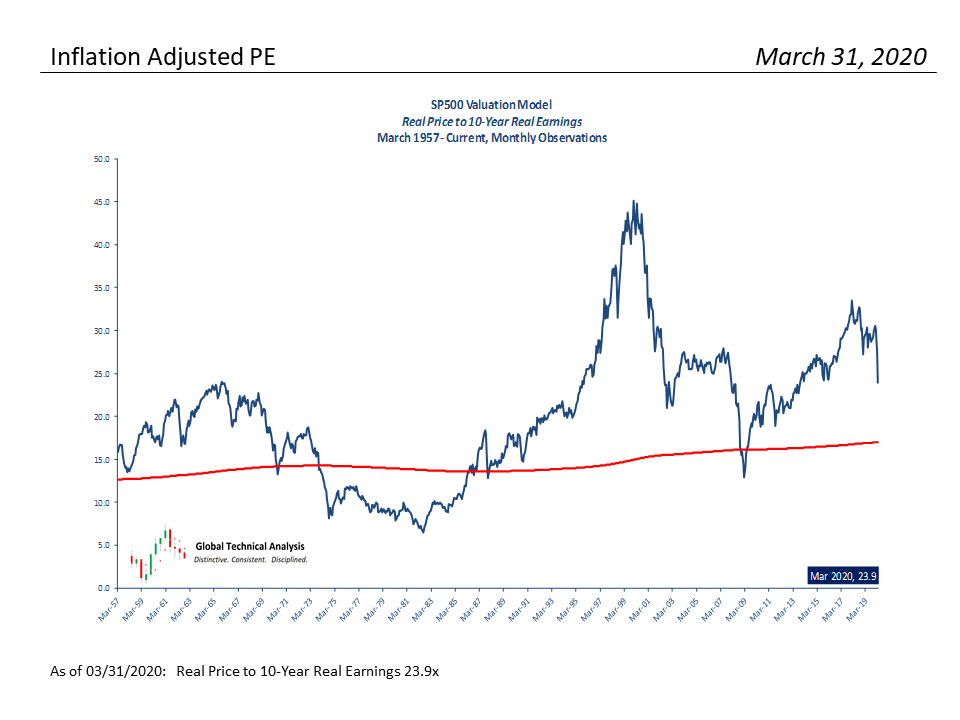

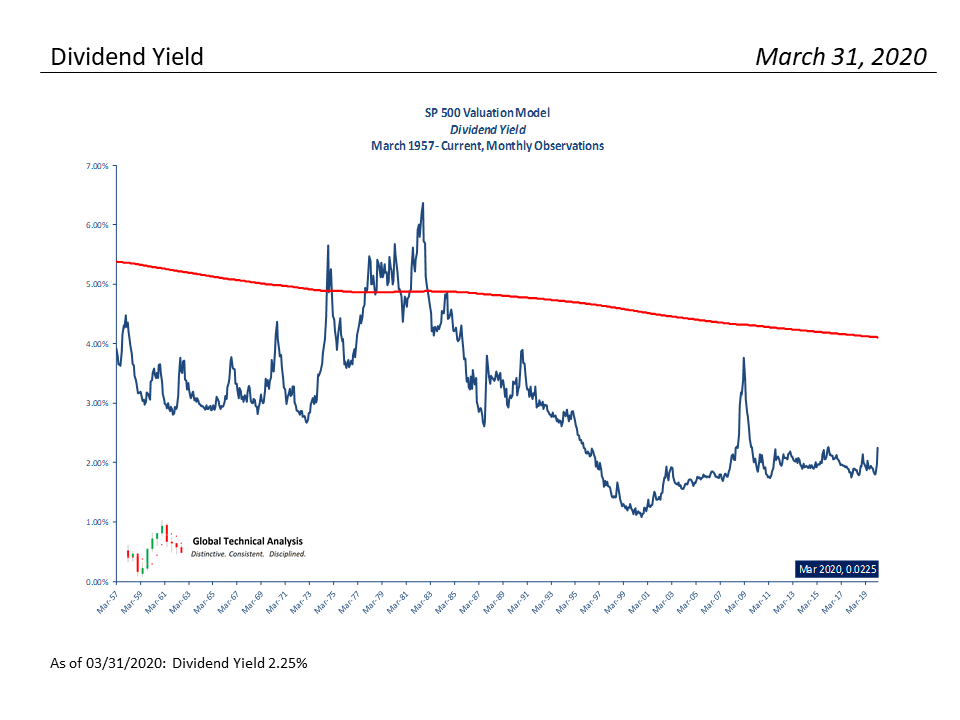

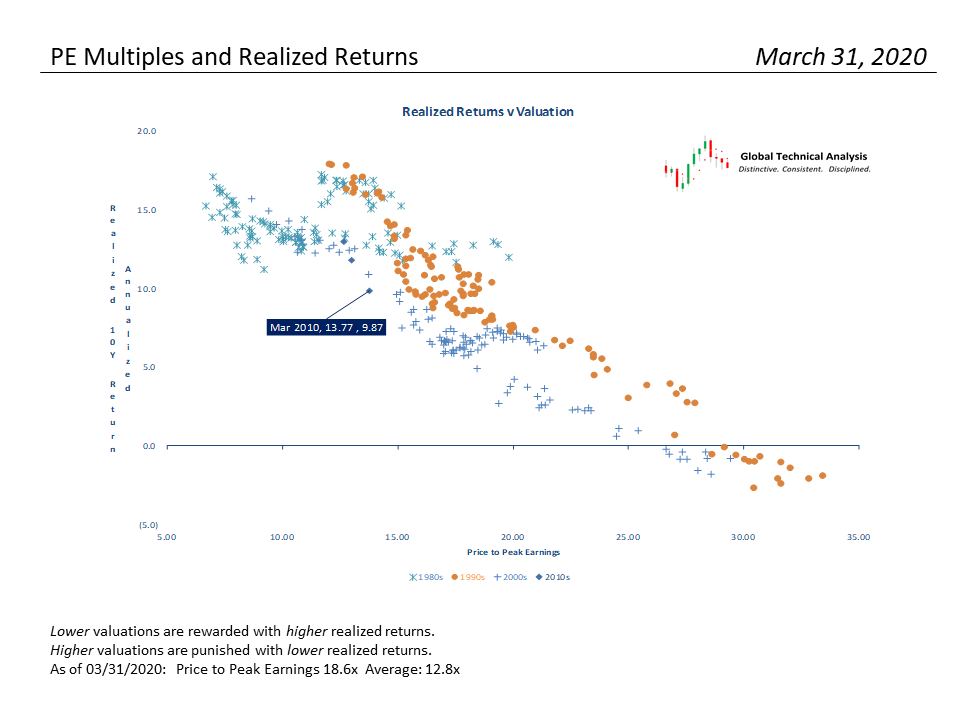

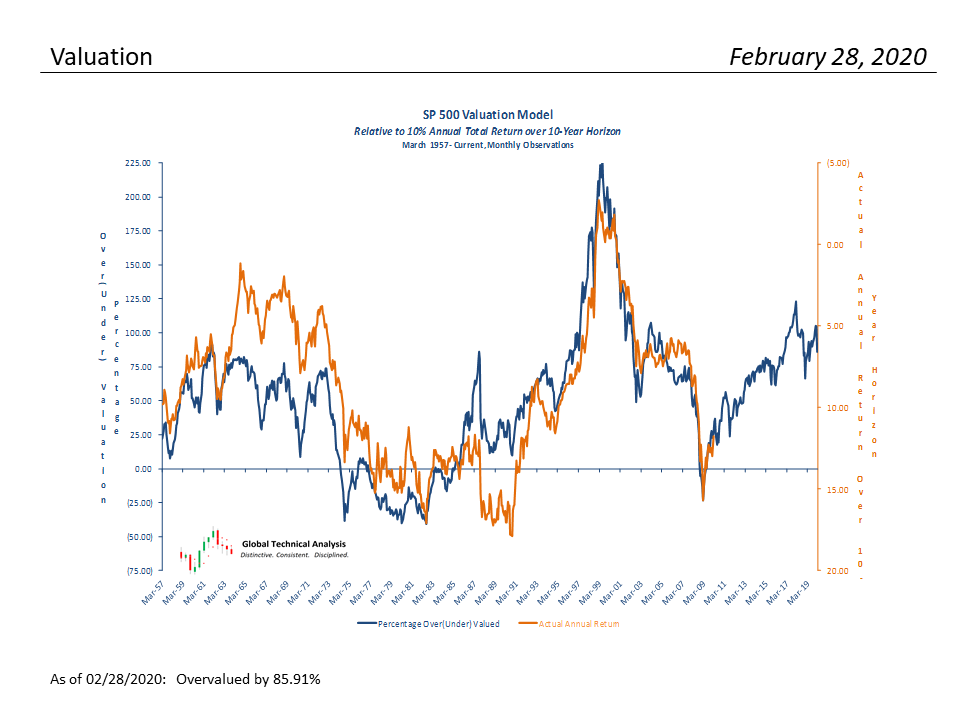

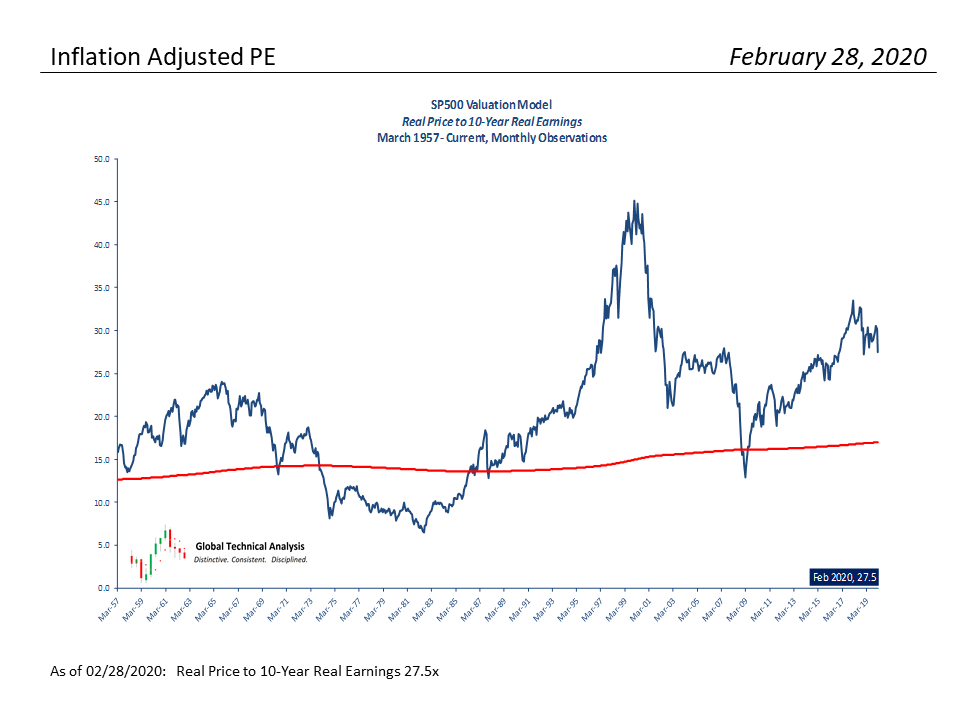

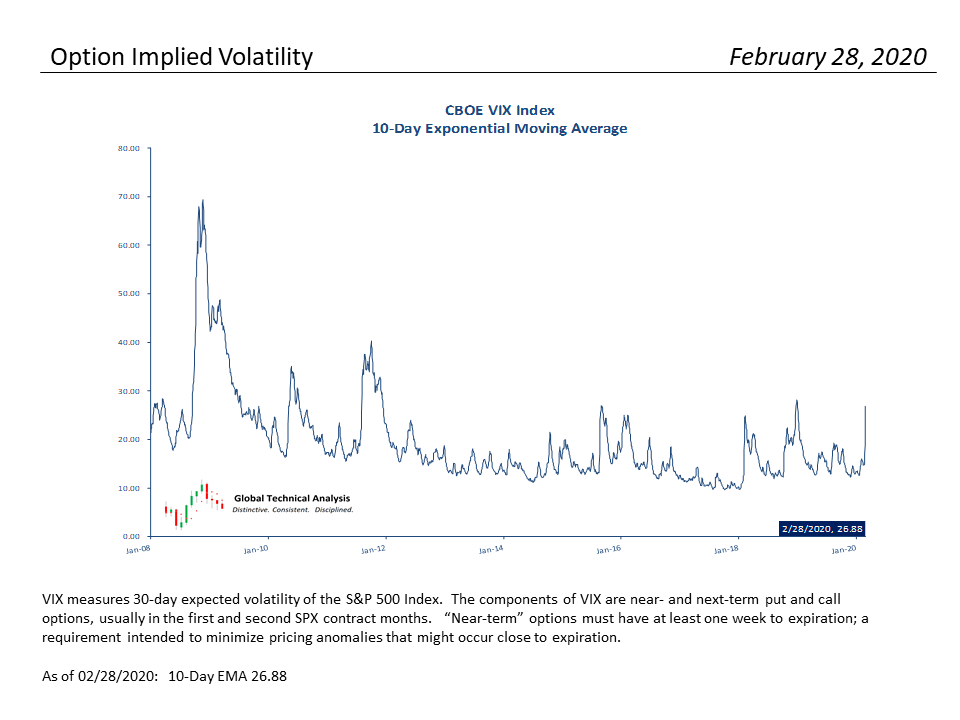

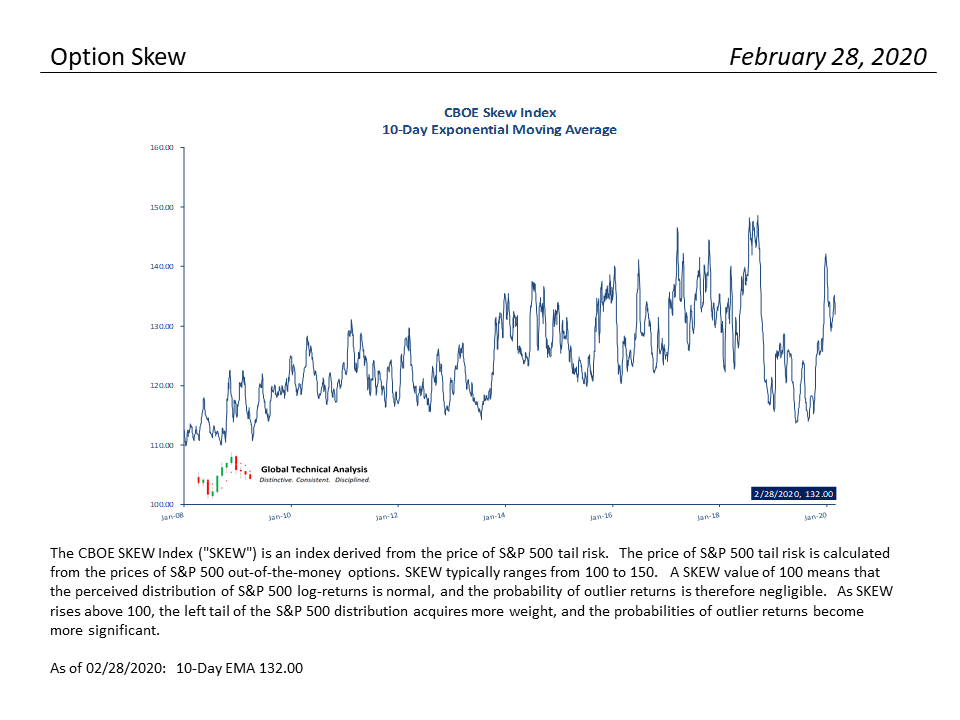

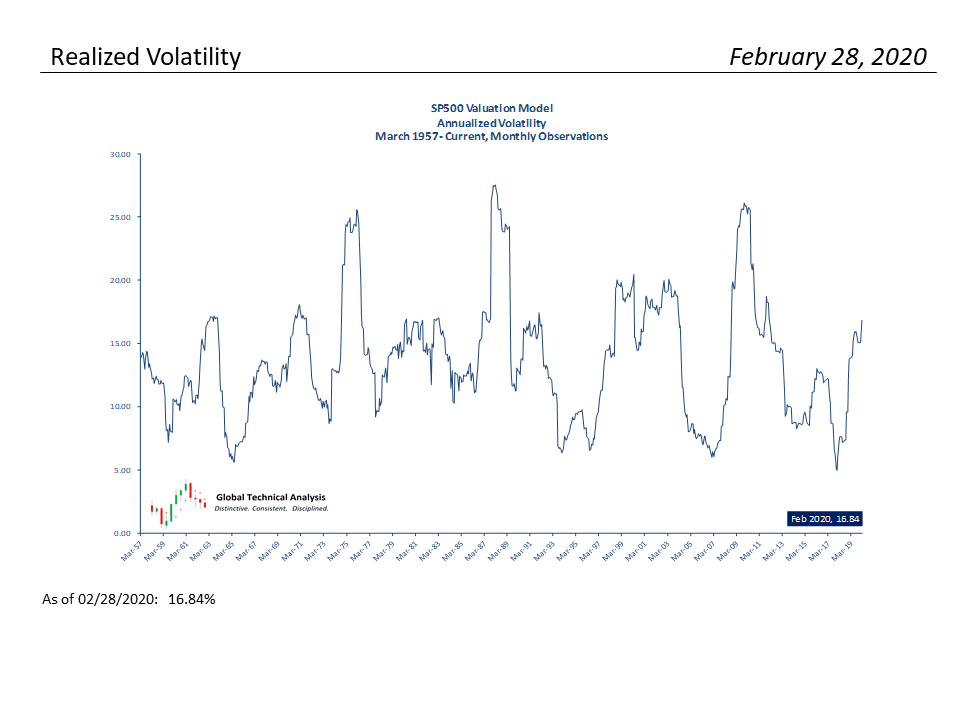

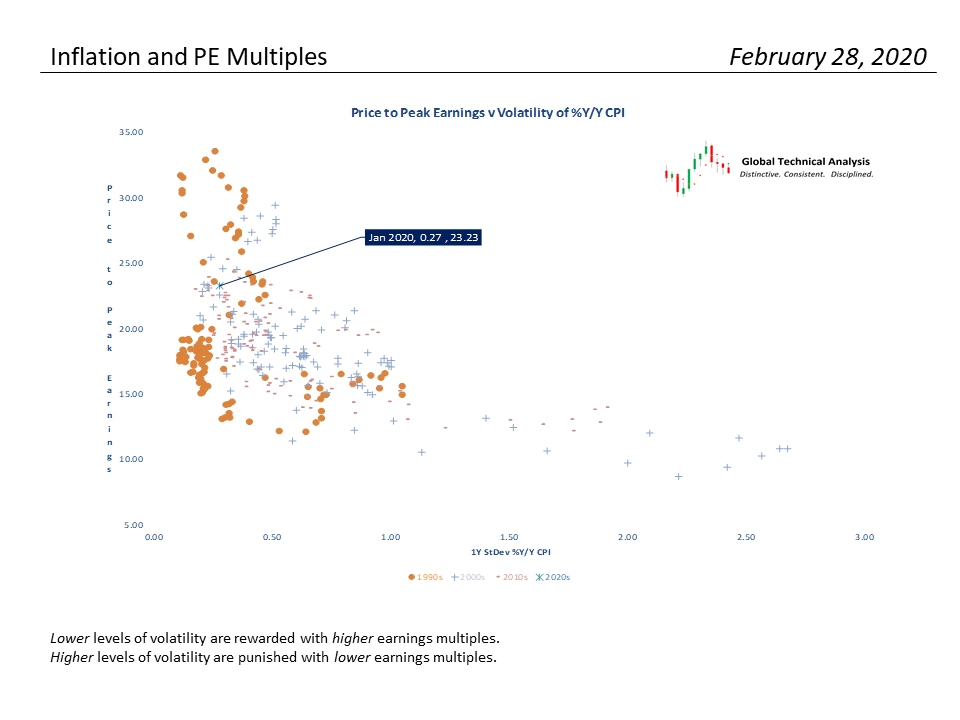

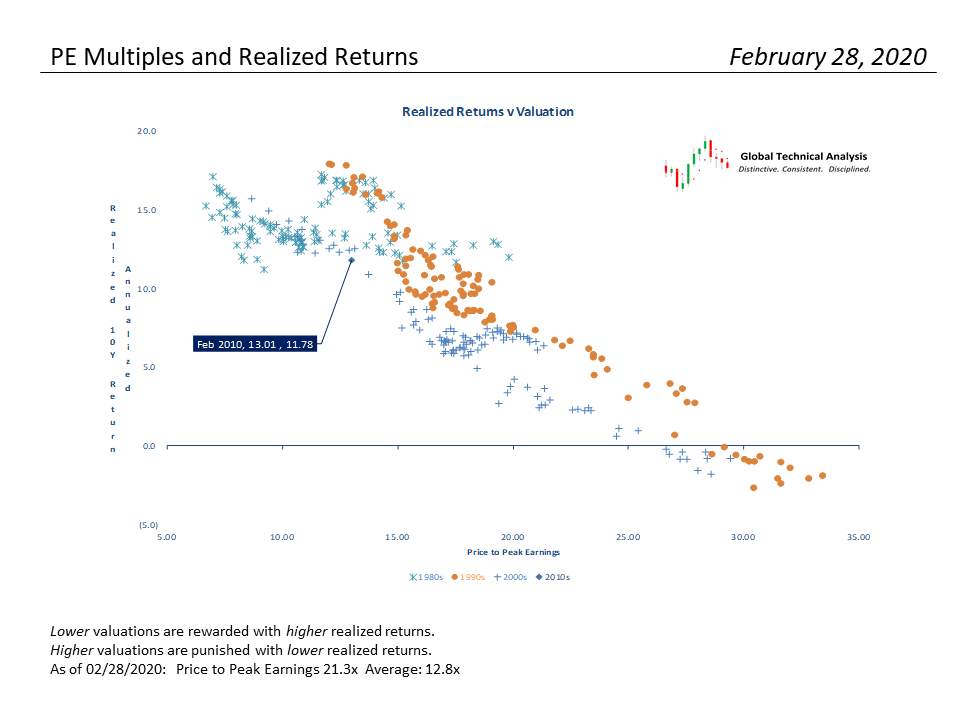

J. Brett Freeze, CFA, founder of Global Technical Analysis. Each month Brett will provide you their valuable S&P 500 Valuation Chart Book. This unique analysis provides an invaluable long term perspective of equity valuations. If you are interested in learning more about their services, please connect with them.

Michael Markowski: Embrace The Bear – Next Leg Down Is Coming

Michael Markowski has been involved in the Capital Markets since 1977. He spent the first 15 years of his career in the Financial Services Industry as a Stockbroker, Portfolio Manager, Venture Capitalist, Investment Banker and Analyst. Since 1996 Markowski has been involved in the Financial Information Industry and has produced research, information and products that have been used by investors to increase their performance and reduce their risk. Read more at BullsNBears.com

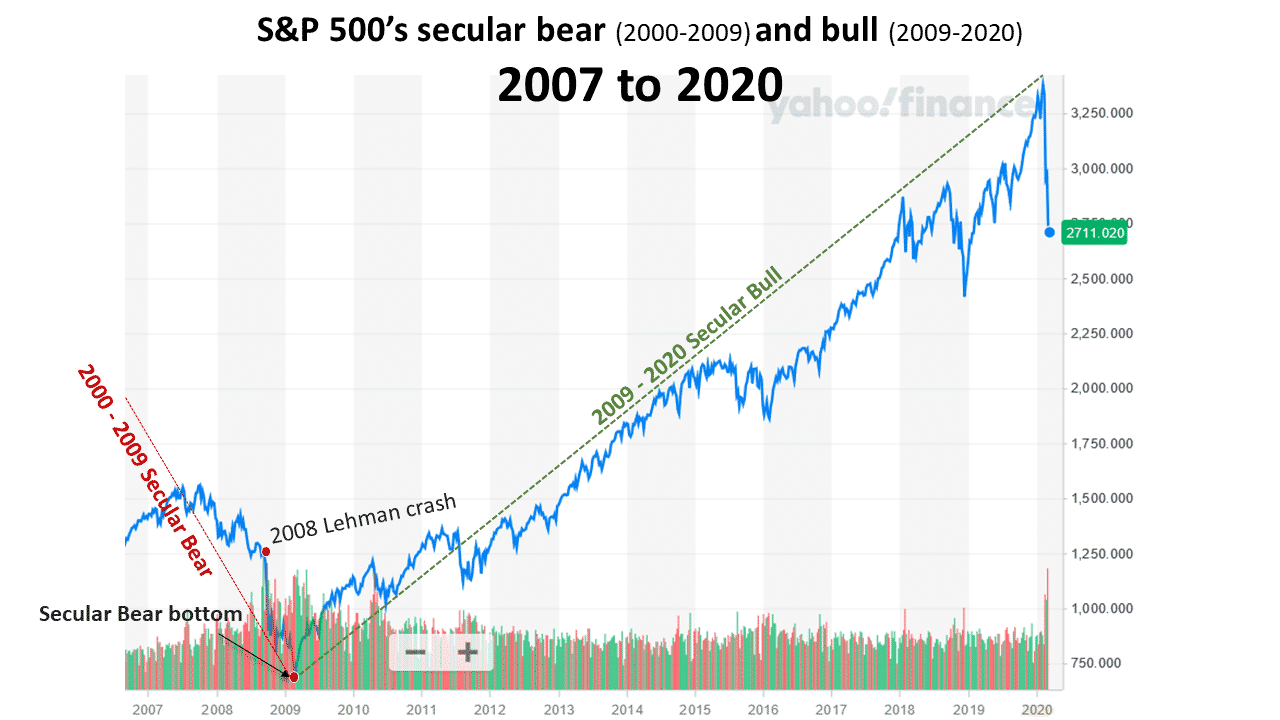

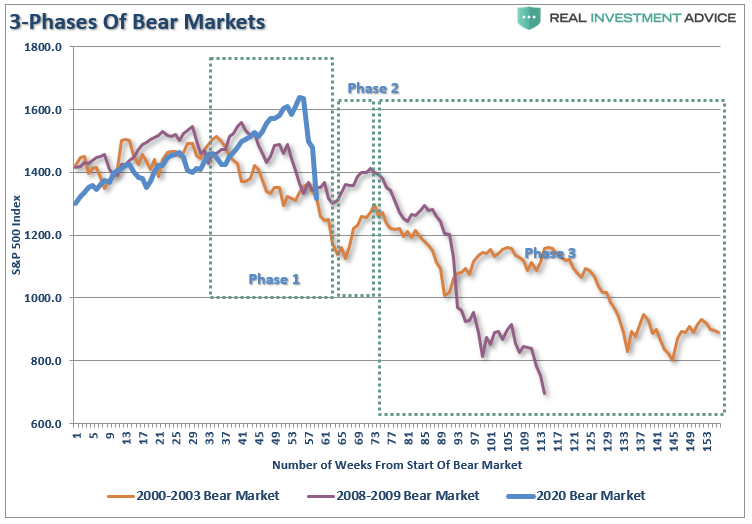

Investors must embrace the bear. A savvy investor or advisor can generate significantly more profits from a secular bear, than a secular bull. It’s also much easier to predict the behavior of a wild and vicious bear than a domesticated bull.

The new 2020 secular bear is the first for which an investor can utilize an inverse ETF (Exchange Traded Fund) to invest in a bear market from start to finish. The share price of an inverse ETF increases when a market goes down. The first inverse ETFs were invented in 2007. The new ETFs enabled investors to make significant profits at the end of the 2000 to 2009 secular bear market. The chart below depicts the gains for the Dow’s inverse ETF before and after Lehman went bankrupt in 2008.

The increased volatility caused by the secular bear can be leveraged by algorithms which had not been utilized in prior bear markets. Two of my algorithms have the potential to produce substantial gains:

Bull & Bear Tracker (BBT)

From April 9, 2018, and through February 29, 2020, the Bull & Bear Tracker (BBT) trend trading algorithm which trades both long and inverse ETFs produced a gain of 77.3% vs. the S&P 500’s 14.9%. March of 2020 will be the BBT’s 9th consecutive profitable month.

The Bull & Bear Tracker thrives on market volatility. The algorithm’s best performance days since the inception of the signals have been when the markets are most volatile.

SCPA (Statistical Crash Probability Analysis)

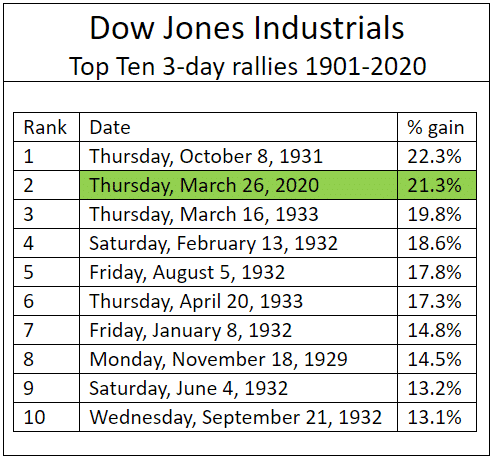

The SCPA is a crash event forecasting algorithm. The algorithm has been very accurate at forecasting the crash of 2020’s events. The SCPA’s forecast that the market had reached a bottom on March 23rd was precisely accurate. From 03/23/20 to 0/3/26/20, the Dow had its biggest one-day gain (11.4%) and three-day percentage gain (21.3%) since 1929 and 1931, respectively. Those investors who purchased the Dow’s long ETF (symbol: DIA) by close of the market on March 23, 2020, after reading “Probability is 87% that market is at interim bottom” which was published during market hours, had a one day gain of 11% at the close of the market on March 24, 2020.

The SCPA’s future event forecasts throughout the life of the crash of 2020 are being utilized to trade long and inverse ETFs until the US markets reach their final bottoms in the fourth quarter of 2022. Had the SCPA and inverse ETFs been available to trade the SCPA’s forecasts in 1929, savvy investors would have made more than 572% from December of 1929 through July of 1932. There were 14 Bear market rallies with average gains of 17%. The rallies were followed by 14 declines which averaged 23%. could have produced average gains of 23% for inverse ETF investors.

Both the Bull & Bear Tracker (BBT) and SCPA complement each other. The BBT predicts market volatility before it increases. The SCPA forecasts the percentage increases for the bear market rallies and the percentage declines from the bear rally highs. My prediction is that the utilization of both of the algorithms will reduce the failed signals ratio for the Bull & Bear Tracker.

Based on the findings from my recently completed empirical research of the Dow’s best rallies from 1901 to 2020, the markets will remain extremely volatile for the foreseeable future.

The Truth About The Biggest One Day Jump Since 1933

The Wall Street Journal’s “Dow Soars More Than 11% in Biggest One-Day Jump Since 1933” was inaccurate. It should have read since “1929”. The article should have been about the Dow Jones industrials composite index having its best one day and three-day percentage gains since 1929 and 1931 respectively.

The gain of 21.3% for the Dow’s three-day rally that ended on March 26th was the index’s second best since 1901. The one-day gain of 11.4% on March 24th ranks as the Dow’s fourth best day since 1901. To understand the significance of the error read on.

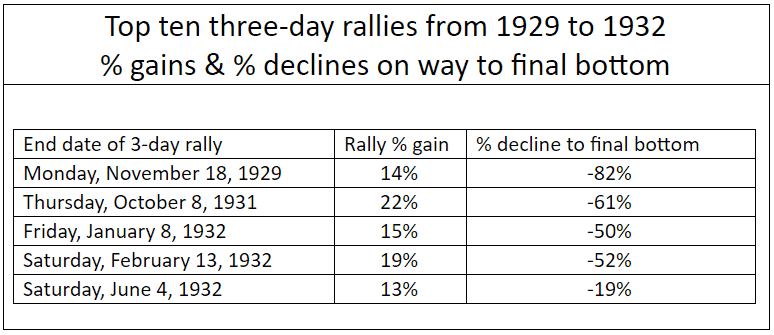

Nine of the top ten three-day percentage gainers occurred during the first four years of the 1929 to 1949 secular bear market. The Five rallies which occurred before the 1929 crash reached its final bottom on July 8, 1932 all failed. Their post rally declines ranged from 19% to 82%.

Six of the 10 biggest daily percentage increases in the table below for the Dow over the last 120 years occurred from 1929 to 1933. There were two 2008 secular bear market rallies, October 13 and 28, 2008 among the top ten one day wonders. The losses for both of the one-day 2008 rallies at the March 2009 were 31.1% and 28.7% respectively.

Of the 100 best percentage gain days for the Dow since 1901, 29 of them occurred between the post 1929 crash and the final July 1932 bottom. From the 1932 bottom to the end of 1933 accounted for an additional 23 of the 100 best days. All of those rallies were profitable. From the low to the end of 1933, the Dow increased by more than 100%. The only other period or year which had concentrated representation in the top 100 was 2008 which had seven.

The Wall Street Journal’s error is significant since 100% of the top 100 best one day rallies from:

October 1929 to July 1932 resulted in significant losses

July 1932 bottom to end of 1933 resulted in significant gains

The error has created a false sense of security for investors and especially for investment professionals, who are aware that after the 1929 crash, the Dow bottomed in 1932. Had the performance for the Dow’s performance cited in the headline been compared to 1929, the context of the article would have been very bearish instead of somewhat bullish.

From my preliminary empirical research findings there were only seven bull market rallies within the top 100 one day percentage gainers. Three of seven in the table below were represented by 1987 and two by 2009.

The three post 1987 “Black Monday’ crash rallies enabled the secular bull which began in 2002 to resume. To understand why it’s not possible for the secular bull which began in 2009 to resume read my two March 2020 articles below. The 1987 crash does not share the genealogy of the Dow 1929, NASDAQ 2000 and the 2020 crashes for the markets of the US, Japan, Germany, Canada, France and South Korea which are now underway.

Based on the findings from my empirical research the probability is 94.4% (17/18) that the Dow 2020’s one day and three-day top ten percentage gainers last week were bear market rallies.

Many are hopeful that the crash which has been underway since February 20, 2020, is just a correction for the continuation of the secular bull market which began in 2009. Based on my just concluded empirical research of the Dow’s best daily and three-day gains and my previous findings from my prior statistical crash probability analysis, the rationale is in place for the markets to continue to crash. My deep fear is that the world is on the verge of a 1930’s style economic depression.

Everyone should take advantage of the Bear market rally that is currently underway to exit the market as soon as possible.

According to the Statistical Crash Probability Analysis (SCPA) forecast the probability is 100% that the relief rally high has either already occurred or will occur by April 8, 2020.

The probability is the same for the markets of the six countries to make new lows by April 30, 2020.

For more about the SCPA click here for access to all of my 2020 crash related articles. To view the SCPA’s very accurate track record for March 2020 click here.

All mutual funds and stocks over $5.00 per share should be liquidated by April 8th. My suggestion is to utilize a methodical approach by liquidating 20% of all holdings per day from April 1st to April 8th.

The SCPA is also forecasting the probability is 100% for the coming attractions from the crash of 2020:

Interim bottom by or before May 4, 2020

At interim bottom market will be 41% to 44% below 2020 highs

Post-crash high before the journey begins to final Q 4 2022 bottom will occur from June 24, 2020 to September 18, 2020.

Post-crash highs to get market to within 17% of 2020 highs.

My only argument against the SCPA’s statistical probability analyses is can the markets get back to above, or even to their March/April 2020 post-crash relief rally highs? The simultaneous crashes in multiple markets for more than one country, let alone six countries, is historically unprecedented.

My hunch is that the damage to the markets and economies of the world’s leading developed countries will be much more severe than the damage caused by the 1929 crash. The relief rally highs could prove to be the post-crash highs.

If that proves to be the case, according to the SCPA the probability is 100% that it will take the markets a minimum of 15 years to get back above the highs already made by the relief rally and longer to get back to their post-crash highs. Additionally, the findings from my extensive research on all of the secular bear markets since 1929 further support the SCPA’s forecast.

There are only three reasons why anyone who is reading my articles would not to sell:

Waiting to get back to break even. It’s against human nature to take losses.

Not wanting to pay capital gains. Securities with gains can be “sold short against the box” to delay a taxable capital gain,

Financial advisor advising otherwise. Beware of the following:

a) An advisor’s largest percentage fee that can be charged is for the amount that an investor has in stocks. If the investor is in cash the advisor can-not charge the fee.

b) The majority of financial advisors are affiliated with big brand name firms including Merrill Lynch, Morgan Stanley, Goldman Sachs and UBS, etc. These advisors have to follow the party line. They do not have the independence to get their clients out of the market even if they wanted to.

c) The financial advisor industry utilizes propaganda to get clients to remain invested during volatile periods. Read “No One Saw It Coming’ – Should You Worry About The 10-Best Days” by Lance Roberts. He is among a few of the independent advisors who I know which had his clients’ 90% out of the market.

TPA Analytics: Death Cross On Russell 3000 Signals More Pain To Come

Jeffrey Marcus is the President of Turning Point Analytics. Turning Point Analytics utilizes a time-tested, real world strategy that optimizes client’s entry and exit points and adds alpha. TPA defines each stock as Trend or Range to identify actionable inflection points. For more information on TPA check out: http://www.TurningPointAnalyticsllc.com

Major Market Buy/Sell Review: 03-30-20

HOW TO READ THE CHARTS

There are three primary components to each chart:

The price chart is in orange

The Over Bought/Over Sold indicator is in gray

The Buy / Sell indicator is in blue.

When the gray indicator is at the TOP of the chart, there is typically more risk and less reward available at the current time. In other words, the best time to BUY is when the short-term condition is over-sold. Likewise when the buy/sell indicator is above the ZERO line investments have a tendency of working better than when below the zero line.

With this basic tutorial let’s review the major markets.

S&P 500 Index

We previosly wrote: “With the market now 3-standard deviations oversold, a bounce is likely next week as it is expected the Fed will cut rates and restart a substantial QE program. A retracement to the 31.8%, 50%, 62.8% levels are possible and each level should be used to reduce equity risk and hedge.”

Well, that bounce finally came and it was a vicious as we expected. While this remains a “bear market” rally, the media was quick to jump on the “Bear market is over” bandwagon. It isn’t, and investors will likely pay a dear price in April.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position

Stop-loss set at $220

Long-Term Positioning: Bearish

Dow Jones Industrial Average

The same situation exists with DIA.

The bounce we discussed previously retraced to the 38.2% retracement level and failed. While Monday and Tuesday could see a push higher for quarter end rebalancing, this is still a bear market to be sold into.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop-loss set at $185

Long-Term Positioning: Bearish

Nasdaq Composite

Last Monday, in anticipation of a rally, we put on a small QQQ trade. The rally did occur and ran into resistance at the 38.2% retracement level. We closed out the trade Friday afternoon, as we were unwilling to hold over the weekend.

We may put on another trade soon, depending on getting the right setup. April promises to be sloppy.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions

Stop-loss set at $170

Long-Term Positioning: Bearish due to valuations

S&P 600 Index (Small-Cap)

As noted last week, small-caps are extremely oversold, and on a very deep “sell signal.” They did bounce this past week, but underperformed the major indexes substantially.

Avoid small-caps. This particular group of stocks are the most susceptible to an economic slowdown from the virus. Use any reflexive rally to step-aside for the time being.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No positions

This Week: No positions.

Stop loss adjusted to $42 on trading positions.

Long-Term Positioning: Bearish

S&P 400 Index (Mid-Cap)

As with Small-cap, we have no holdings.

MDY is oversold, and is on a very deep a “sell signal.” The rally this past week also underperformed the broad market.

As noted last week, “MDY is oversold enough for a counter-trend bounce to sell into. Trading positions only.” That rally is likely done for now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No holding

This Week: No holding

Long-Term Positioning: Bearish

Emerging Markets

As noted last week, EEM was extremely oversold and on a deep sell-signal. A bounce was likely which occurred.

We previously stated that investors should use counter-trend rallies to sell into. Do that now.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position

This Week: No position.

Stop-loss set at $30 for trading positions.

Long-Term Positioning: Bearish

International Markets

Like EEM, EFA was also sold previously. as we return our focus back to large cap value.

As noted last week: “EFA is very sold and on a deep sell signal. A reflexive rally is likely. Use those levels to sell into.” Do so this week.

Short-Term Positioning: Bearish – Market Risk Is High

Last Week: No position.

This Week: No position.

Stop-loss set at $46 for trading positions.

Long-Term Positioning: Bearish

West Texas Intermediate Crude (Oil)

We still like the sector from a “value” perspective and expect that we will wind up making a lot of money here. We clearly aren’t at lows yet, so be patient.

Oil continues to weaken and supplies are building as economic shutdowns are not good for the crude market. Bankruptcies are rising as well.

Avoid for now.

Short-Term Positioning: Bearish

Last Week: No positions

This Week: No positions.

Stops Triggered for any direct crude oil positions.

Long-Term Positioning: Bearish

Gold

Last week we noted: “It seems that liquidation event may be passing. If Gold can climb back above the 200-dma we will look to add back our holdings.

It did.

We added to our position in IAU and continue to have a small holding in GDX, as the previous liquidation left a lot of value in the sector.

Short-Term Positioning: Bullish

Last week: Hold positions.

This week: Added to position

Stop-loss set at $137.50.

Long-Term Positioning: Bullish

Bonds (Inverse Of Interest Rates)

We have reduced our overall bond exposure, because we are running a very reduced equity exposure currently. This aligns our “hedge” of fixed income relative to our equity book.

We remain very cautious on our bond exposure currently, and will look to add to that exposure once the credit markets calm down a bit.

Short-Term Positioning: Neutral

Last Week: Hold positions

This Week: Hold positions

Stop-loss is moved up to $147.50

Long-Term Positioning: Bullish

U.S. Dollar

Previously we stated: “This past week, the dollar surged through that resistance and is now extremely overbought short-term. Looking for a reflexive rally in stocks next week that pulls the dollar back towards the breakout level of last week.”

That occurred this past week, and the dollar is now approaching its moving average support.

The credit crisis, and rush to cash, sent the dollar surging to 7-deviations above the mean. As we noted previously, with the credit markets calming down we are starting to see previous relationships between asset classes return to normal.

The dollar has reversed its sell signal, which suggests dollar strength may be with us for a while longer.

Bull Market? No, The Bear Still Rules For Now (Full Report)

The “2020 SOCIALLY DISTANT INVESTMENT SUMMIT” is coming on Thursday, April 2nd.

Click the link below to receive an email with a special “invitation only” link when the summit goes “live.” (Current newsletter subscribers are already registered.)

Catch Up On What You Missed Last Week

NOTE: During these tumultuous times, we are unlocking our full newsletter to help you navigate the markets safely. Make sure you subscribe toRIAPRO.NET (Free 30-Day Trial) if you want to keep receiving the full report after the storm passes.

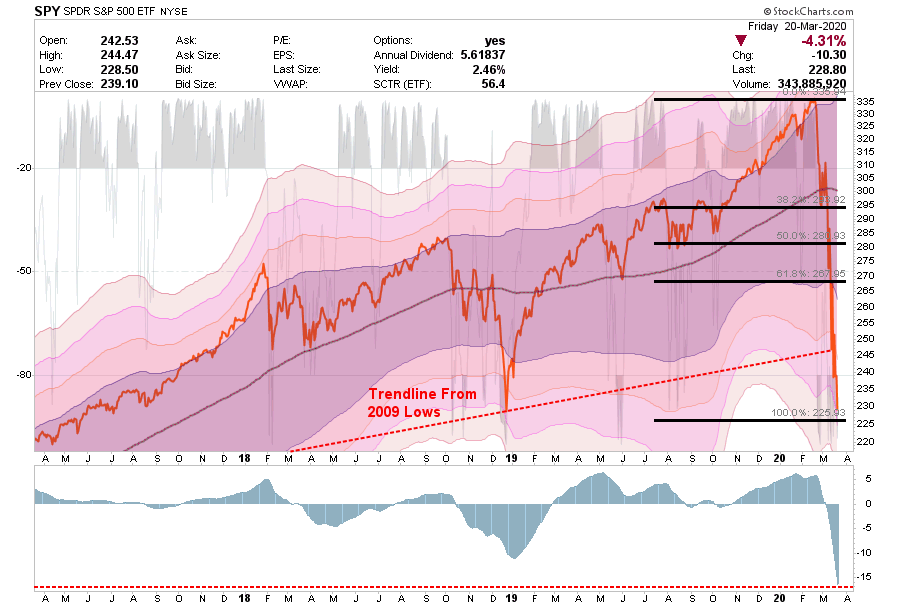

“From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance.

Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Chart Updated Through Friday

Not surprisingly, here were the headlines, almost exactly as we wrote them:

Well, you get the idea.

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. More importantly, “bear markets” only end when “NO ONE wants to buy it.”

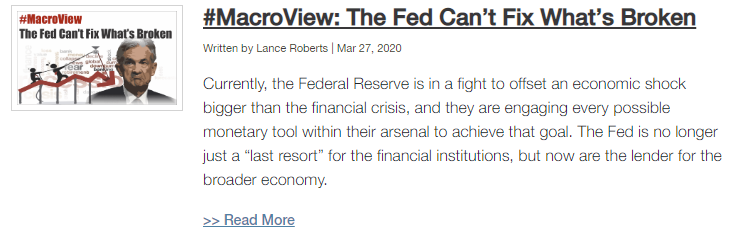

Fed Can’t Fix It

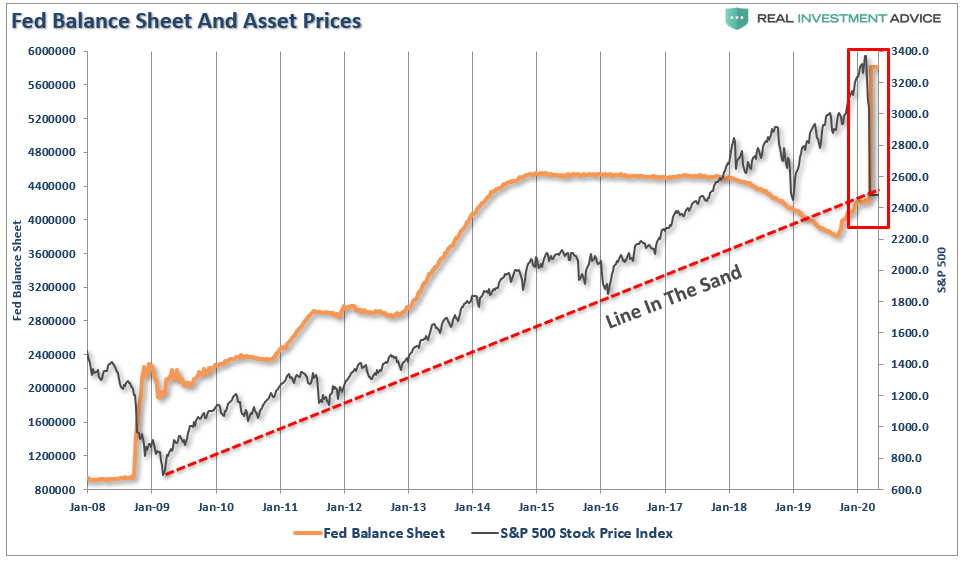

As noted above, the “bear market” will NOT be over until the credit market is fixed. We are a long way from that being done, given the blowout in yields currently occurring.

The Fed has cut rates by 150 basis points to near zero and run through its entire 2008 crisis handbook.

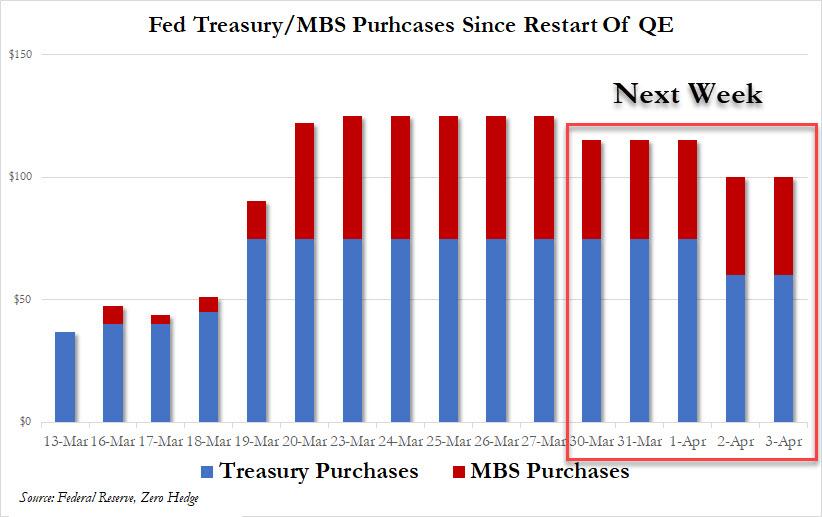

That wasn’t enough to calm markets, though — so the central bank also announced $1 trillion a day in repurchase agreements and unlimited quantitative easing, which includes a hard-to-understand $625 billion of bond-buying a week going forward. At this rate, the Fed will own two-thirds of the Treasury market in a year.

But it’s the alphabet soup of new programs that deserve special consideration, as they could have profound long-term consequences for the functioning of the Fed and the allocation of capital in financial markets. Specifically, these are:

CPFF (Commercial Paper Funding Facility) – buying commercial paper from the issuer.

PMCCF (Primary Market Corporate Credit Facility) – buying corporate bonds from the issuer.

SMCCF (Secondary Market Corporate Credit Facility) – buying corporate bonds and bond ETFs in the secondary market.

MSBLP (Main Street Business Lending Program) – Details are to come, but it will lend to eligible small and medium-sized businesses, complementing efforts by the Small Business Association.

To put it bluntly, the Fed isn’t allowed to do any of this.”

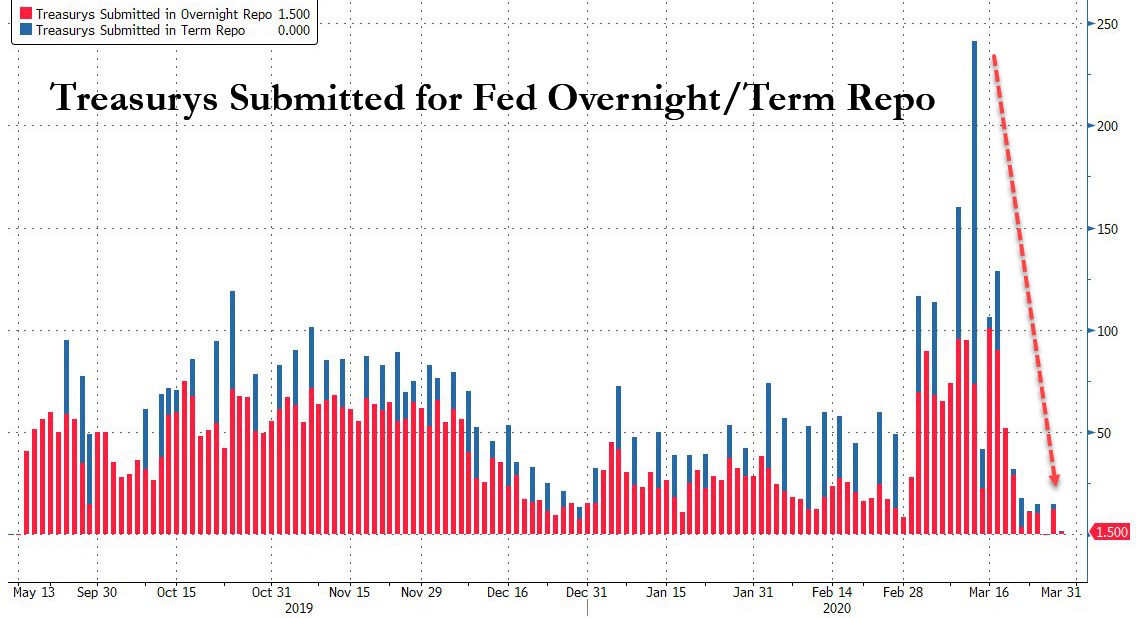

However, on Friday, the Federal Reserve ran into a problem, which could poses a risk for the markets going forward. As Jim noted, the mind-boggling pace of bond purchases quickly hit the limits of what was available to pledge for collateral.

Or rather, the Fed’s “unlimited QE,” may not be so “unlimited” after all.

The consequence is the Fed is already having to start cutting back on its QE program. That news fueled the late-day sell-off Friday afternoon. (Charts courtesy of Zerohedge)

While Congress did pass the “CARES” act on Friday, it will do little to backstop what is about to happen to the economy for two primary reasons:

The package will only support the economy for up to two months. Unfortunately, there is no framework for effective and timely deployment; firms are already struggling to pay rents, there are pockets of funding stress in credit markets as default risks build, and earnings guidance is abandoned.

The unprecedented uncertainty facing financial markets on the duration of social distancing, the depth of the economic shock and when the infection rate curve will flatten, and there are many unknowns which will further undermine confidence.

Both of these points are addressed in this week’s Macroview but here are the two salient points to support my statement:

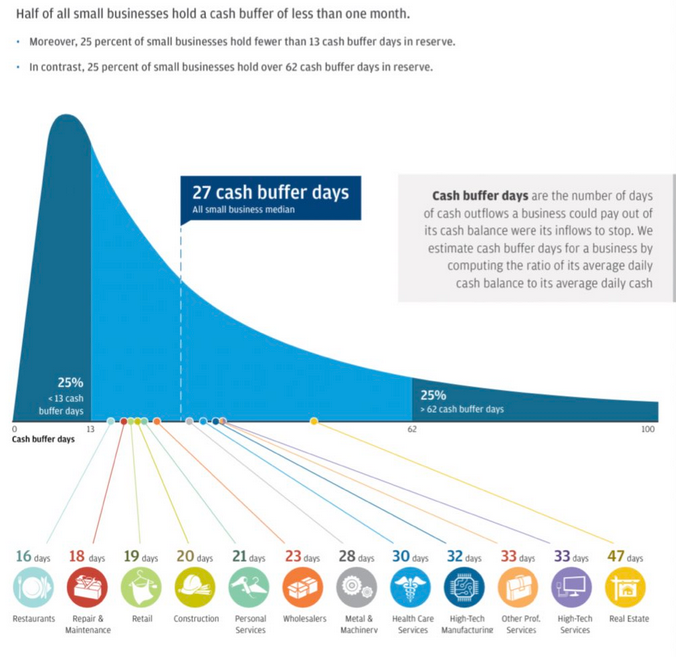

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance, can be provided. This will lead to higher and longer-duration of, unemployment.”

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any type of disruption to their income going into the recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits leads to higher unemployment and lower asset prices until the cycle is complete.

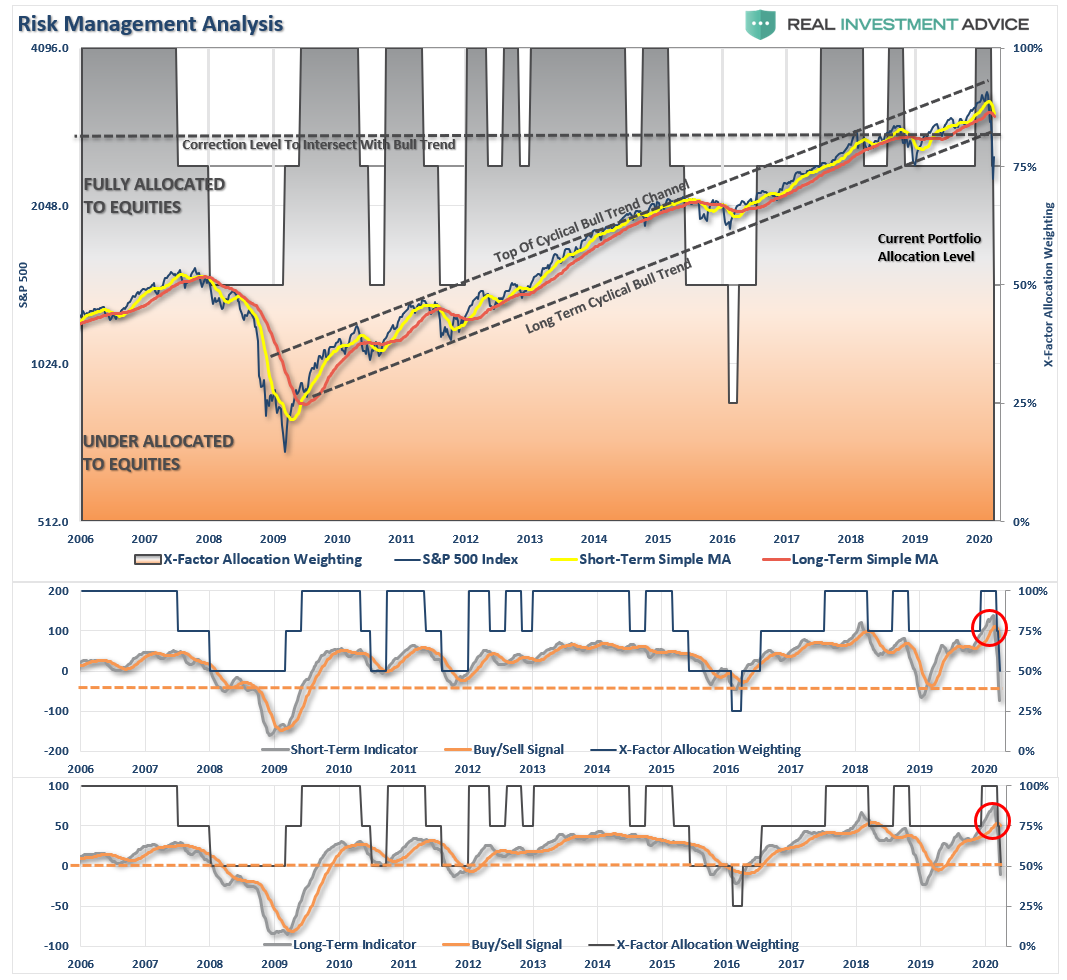

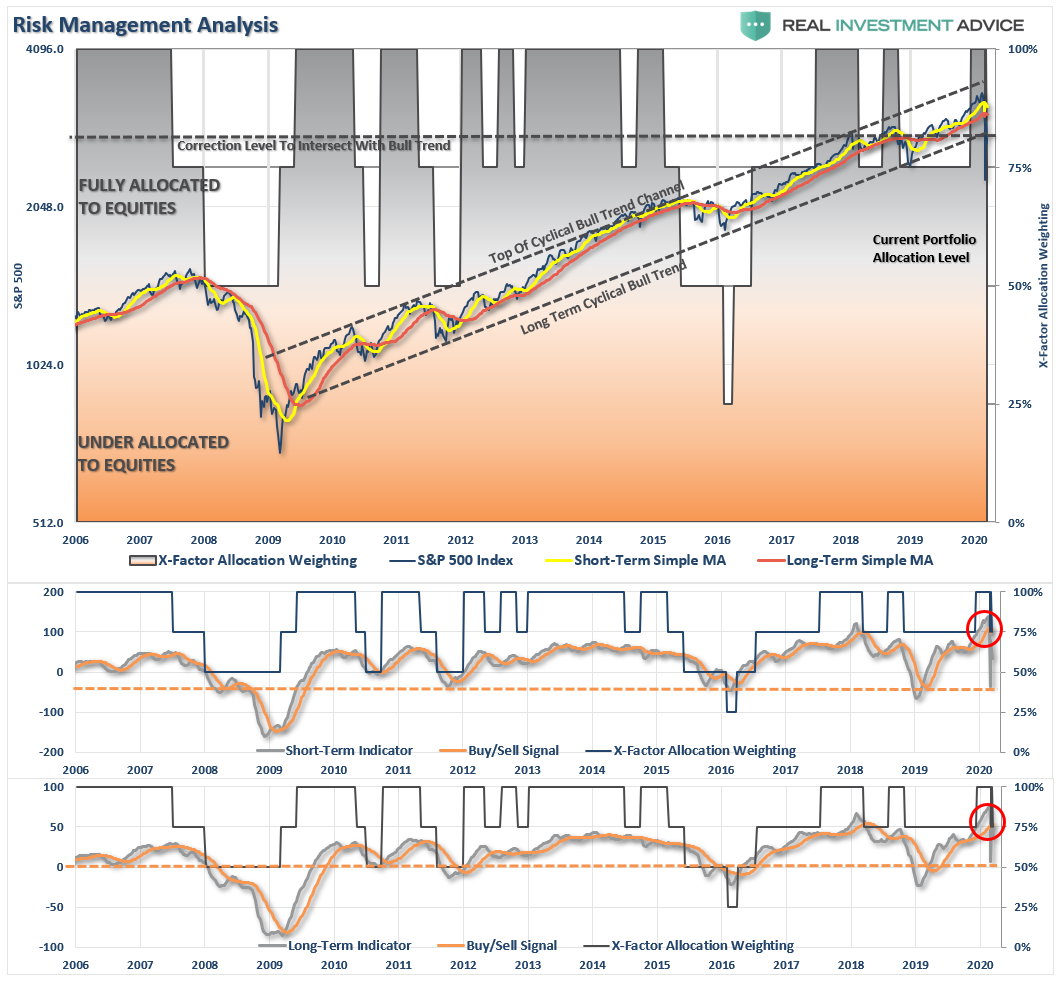

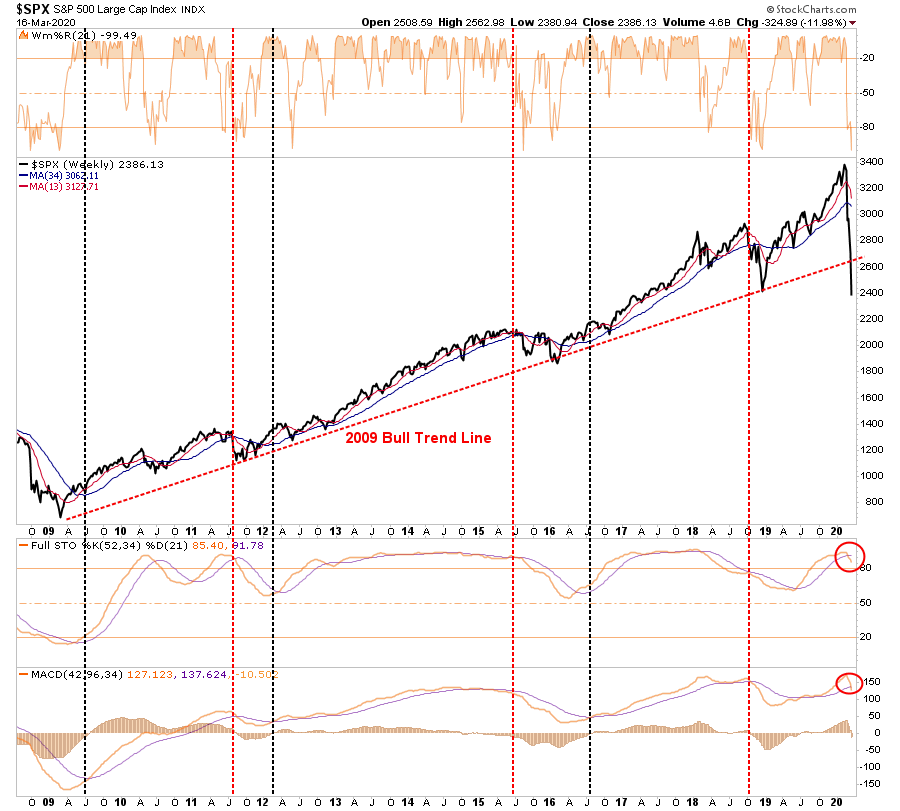

The long term bull pattern that existed since the 3/9/09 is over. That means the pattern of investors confidently buying every decline is over.

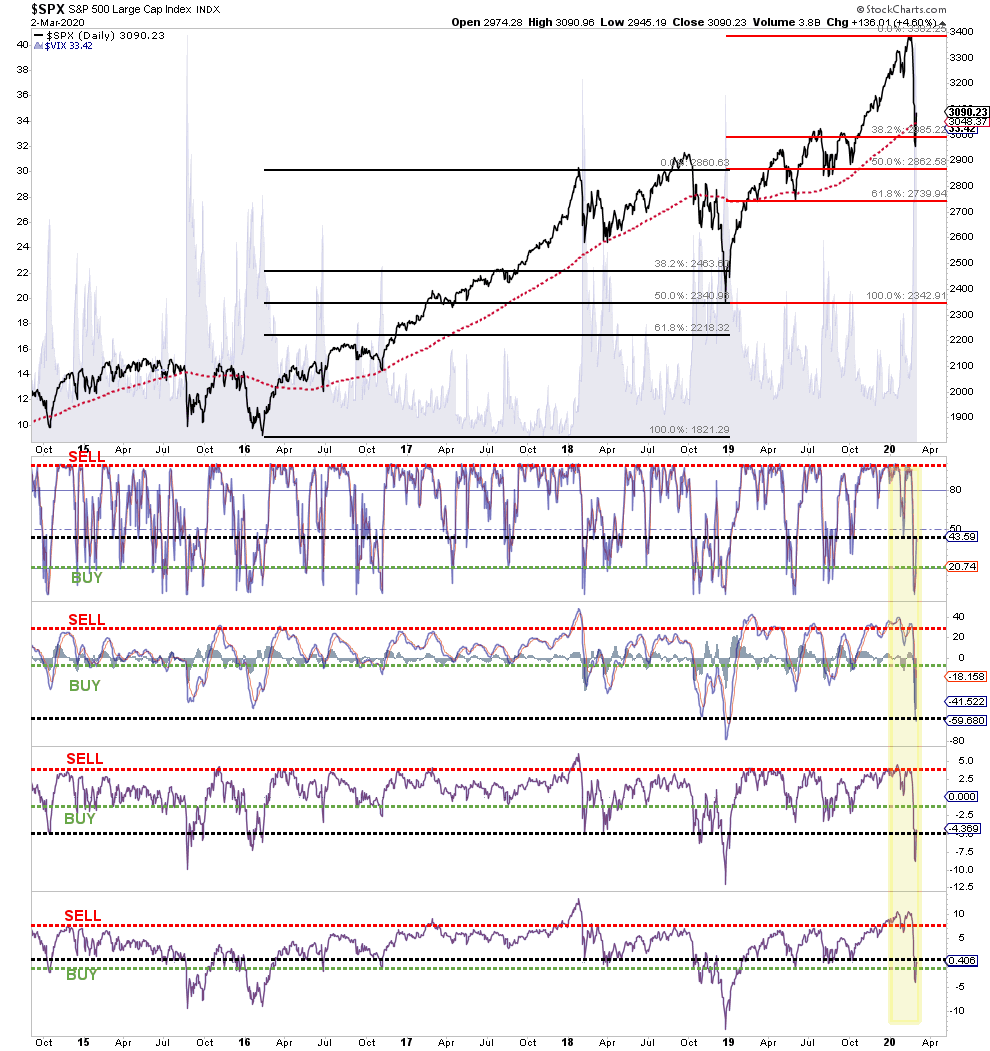

The market became historically oversold on 3/23 using many metrics, and that oversold condition coincided with the long term support area of S&P 500 2110-2180.

The short-covering and rebalancing had a lot to do with the size and speed of the 3-day rally. Also, we know the lack of ETF liquidity played a huge role as well as algorithmic trading.

Technically the market can still go up 6.9% higher from here to hit the 50% retracement level (3386 – 2237 = 1149/2 = 574 + 2237 = 2811….2811/2630 = +6.9%.) I would not bet on it.

The market only sustains a rally once there is light at the Coronavirus tunnel.

I do not think the S&P 500 will hit a new high this year. Maybe not in 2021, either.

His analysis agrees with our own, which we discussed with you last week.

“The good news is the markets are now more extremely oversold on a variety of measures than at just about any other point in history.

Warning: Any reversal will NOT BE the bear market bottom. It will be a ‘bear market’ rally you will want to ‘sell’ into. The reason is there are still many investors trapped in ‘buy and hold’ and ‘passive indexing’ strategies that are actively seeking an exit. Any rallies will be met with redemptions.

Most importantly, all of our long-term weekly ‘sell signals’ have now been triggered. Such would suggest that a rally back to the ‘bullish trend line’ from 2009 will likely be the best opportunity to ‘sell’ before the ‘bear market’ finds its final low.”

Last week’s chart updated through Friday’s close.

While the recent lows may indeed turn out to be “the bottom,” I highly suspect they won’t. Given the sell signals have been registered at such high levels, the time, and distance, needed to reverse the excesses will require a deeper market draw.

As Jeff Hirsch from Stocktrader’s Alamanc noted:

“While we are all rooting for the market to find support here so much damage has been done. A great deal of uncertainty remains for the economy and health crisis. This looks like a bear market bounce.

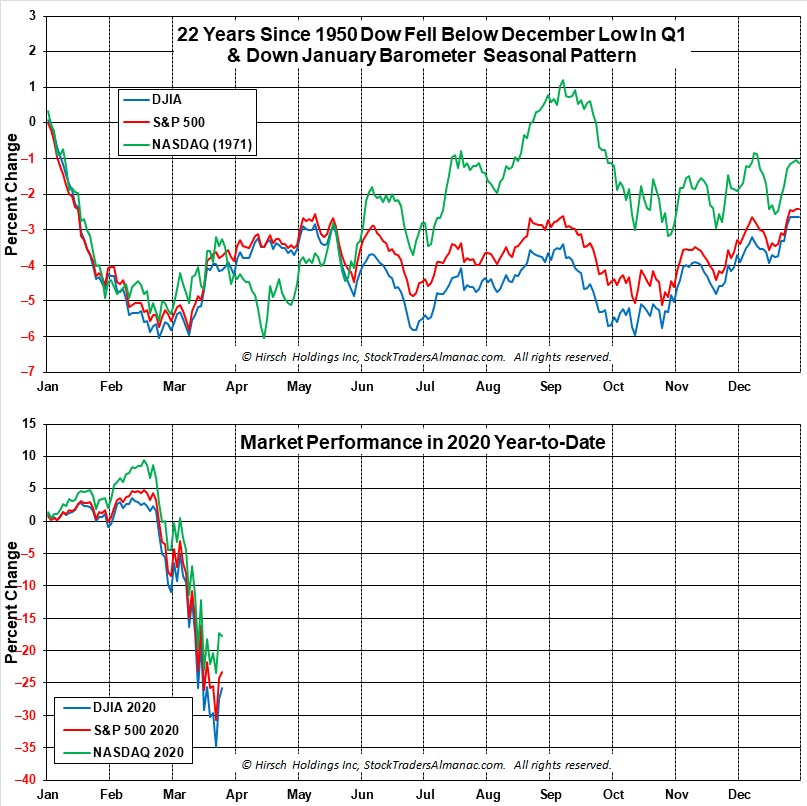

History suggests that we are in for some tough sledding in the market this year with quite a bit of chop. When the January Barometer came in with a negative reading, our outlook for 2020 began to diminish as every down January since 1950 has been followed by a new or continuing bear market, a 10% correction, or a flat year. Then another warning sign flashed when DJIA closed below its December closing low on February 26, 2020 as the impact of this novel coronavirus began to take its toll on Wall Street.

In the March Outlook, we presented this graph of the composite seasonal pattern for the 22 years since 1950 when both the January Barometer as measured by the S&P 500 were down, and the Dow closed below its previous December closing low in the first quarter. Below is a graph of DJIA, S&P 500 and NASDAQ Composite for 2020 year-to-date as of the close on March 25. Comparing 2020 market action to these 22 years, suggests a choppy year ahead with the potential for several tests of the recent low.”

“The depth of this waterfall decline may be too deep for the market to rebound quickly. This bear market also put this year’s Best Six Months (November-April) at risk of being negative. The record of down Best Six Months is not encouraging and it reminds us of a salient quote from the Almanac from an old market sage,

‘If the market does not rally, as it should during bullish seasonal periods, it is a sign that other forces are stronger and that when the seasonal period ends those forces will really have their say.’— Edson Gould (Stock market analyst, Findings & Forecasts, 1902-1987)'”

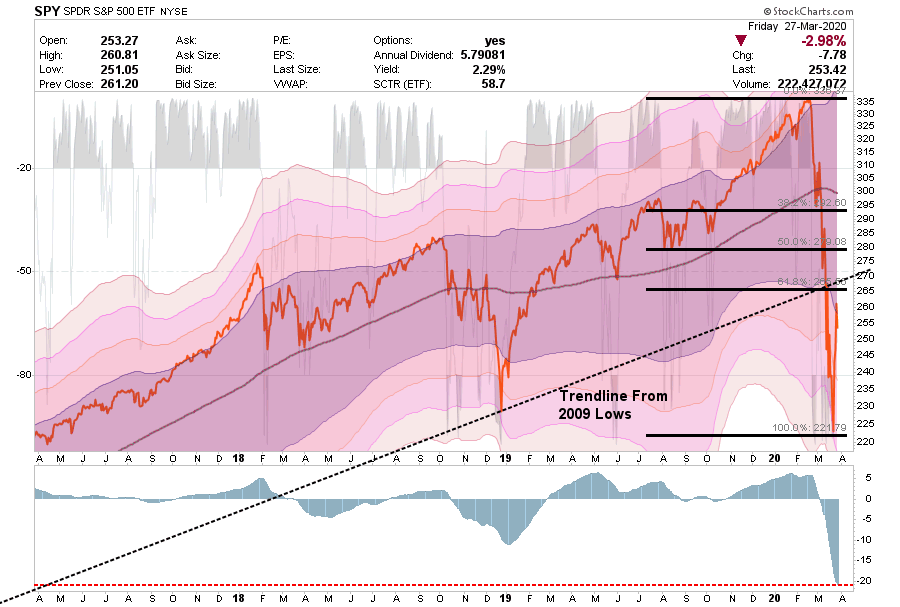

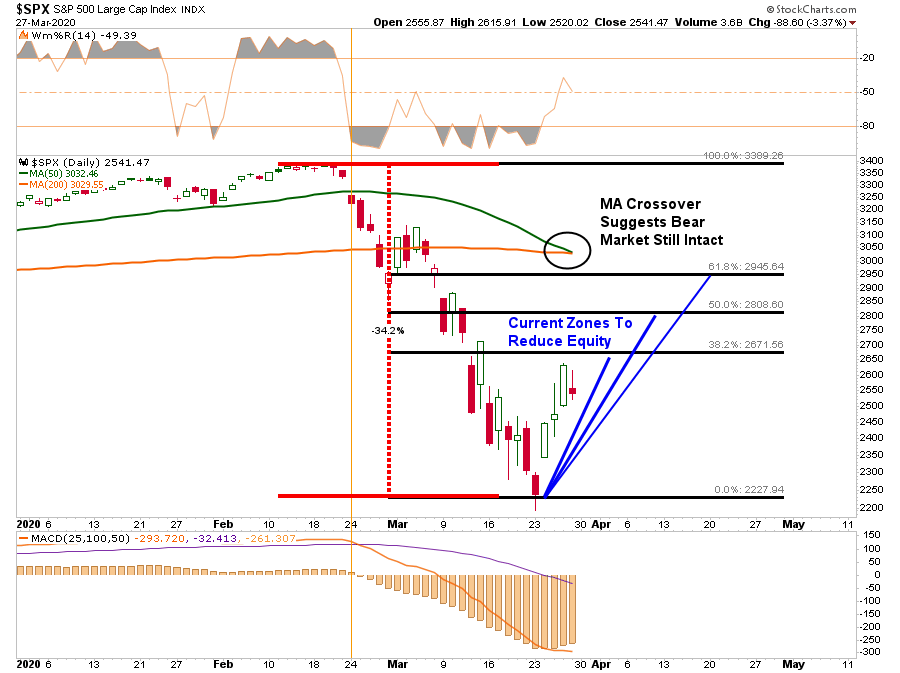

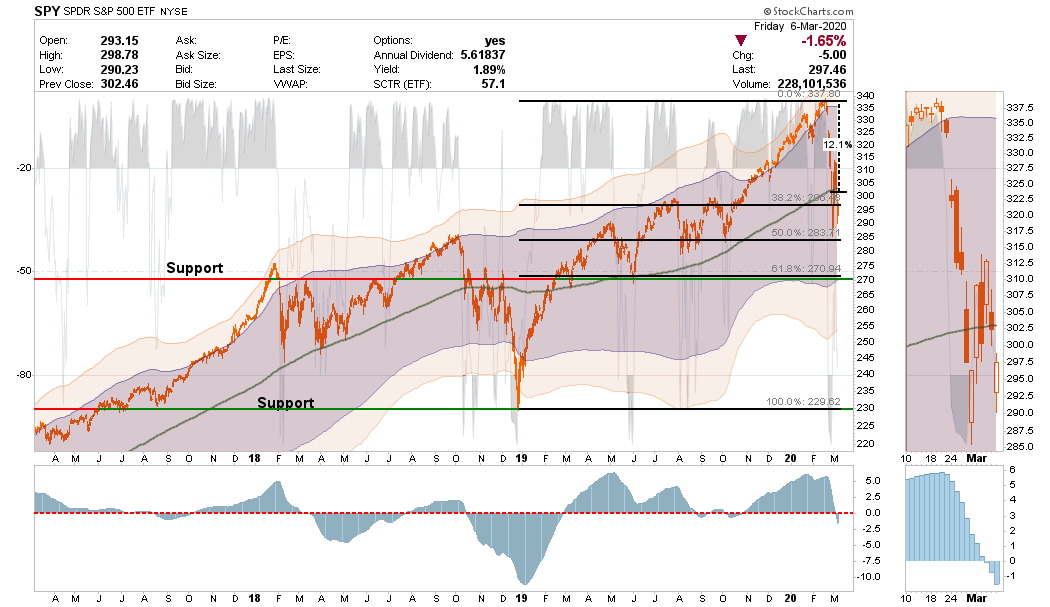

On a short-term basis, the market is also suggesting some risk. The daily chart below shows the market rallied to, and failed at, the first level of the Fibonacci retracement we outlined last week, suggesting profits be taken at this level. While there are two remaining targets for the bear market rally, the probabilities weigh heavily against them. (This doesn’t mean they can’t be achieved, it is “possible,” just not “probable.”)

Furthermore, with the “Death Cross” triggering on Friday (the 50-dma crossing below the 200-dma), this will put further downside pressure on any “bear market” advance from current levels.

Given the magnitude, and multiple confirmations, of these signals, it is far too soon to assume the “bear market” is over. This is particularly the case, given the sell-off is less than one-month-old.

Bear markets, and recessions, tend to last 18-months on average.

The current bear market and recession are not the results of just the “coronavirus” shock. It is the result of many simultaneous shocks from:

Economic disruption

Surging unemployment

Oil price shock

Collapsing consumer confidence, and

Most importantly, a “credit event.”

We likely have more to go before we can safely assume we have turned the corner.

In the meantime, use rallies to raise cash. Don’t worry about trying to “buy the bottom.”There will be plenty of time to see “THE” bottom is in, and having cash will allow you to “buy stocks” from the last of the “weak hands.”

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

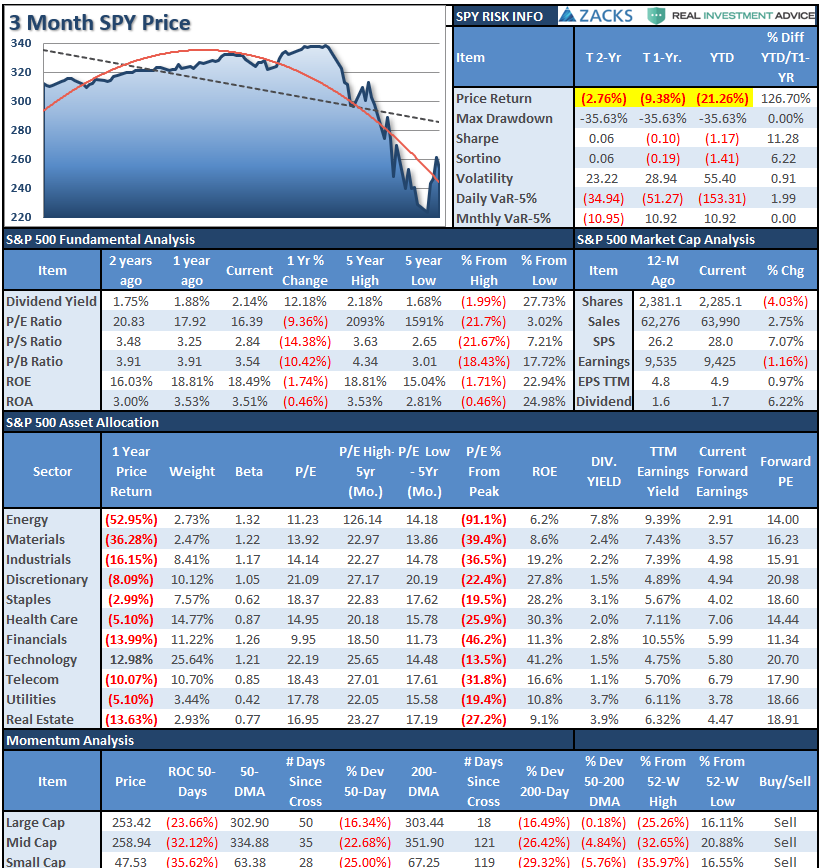

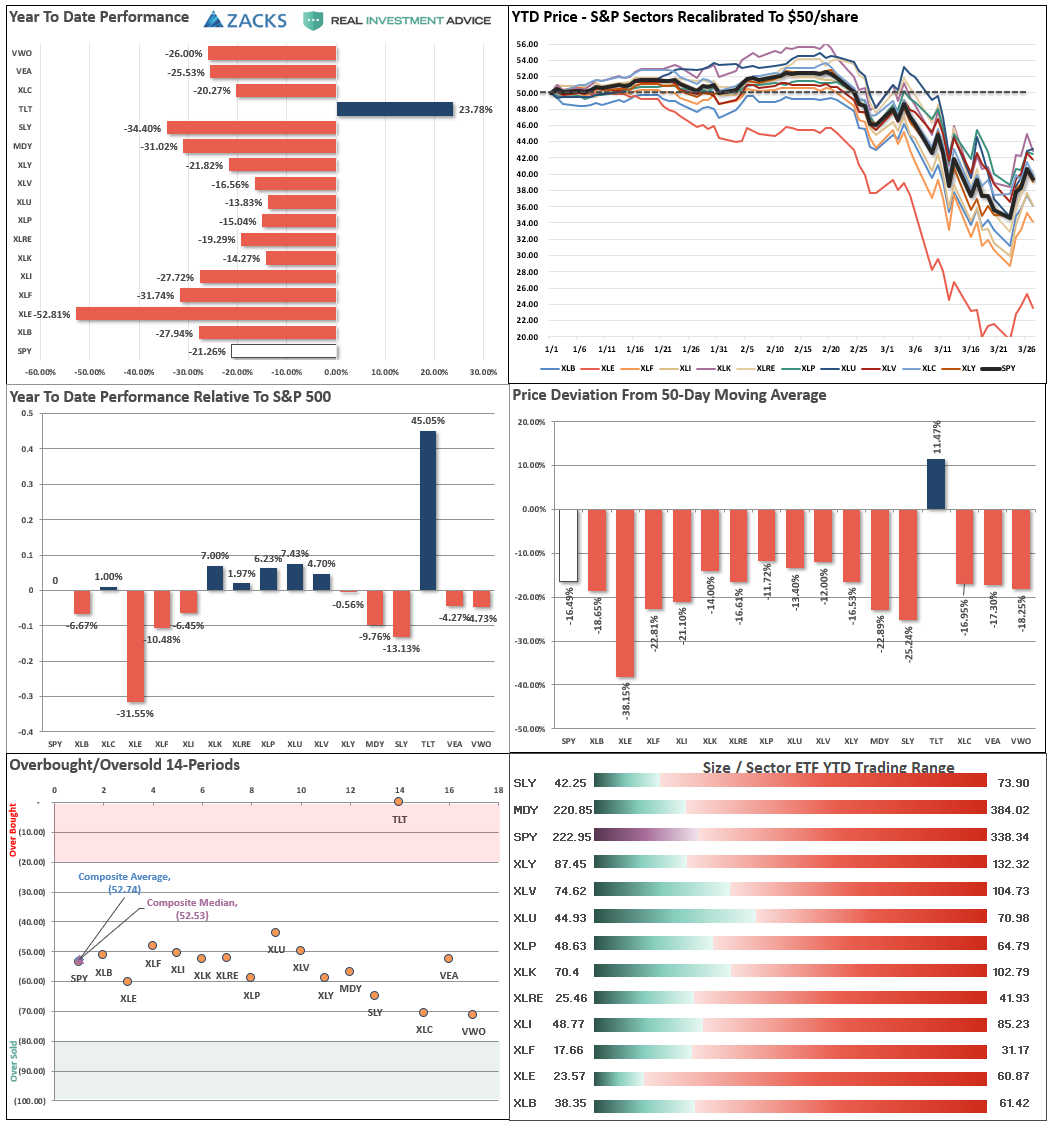

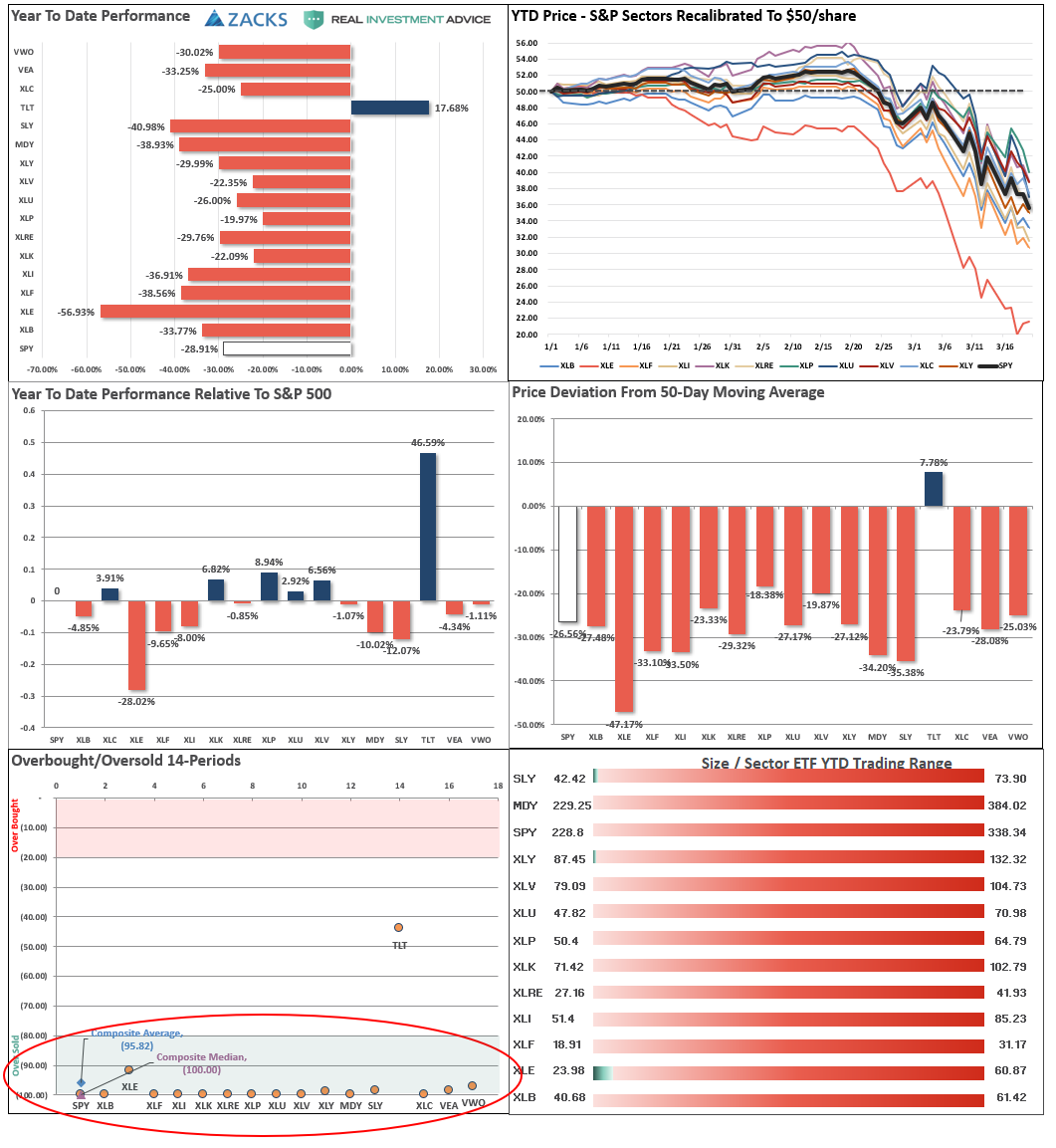

S&P 500 Tear Sheet

Performance Analysis

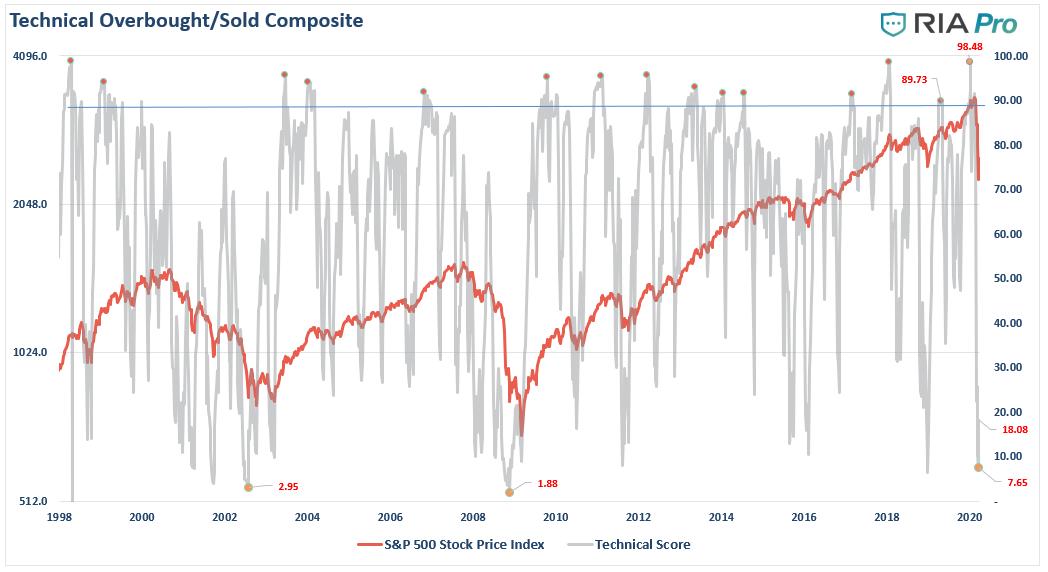

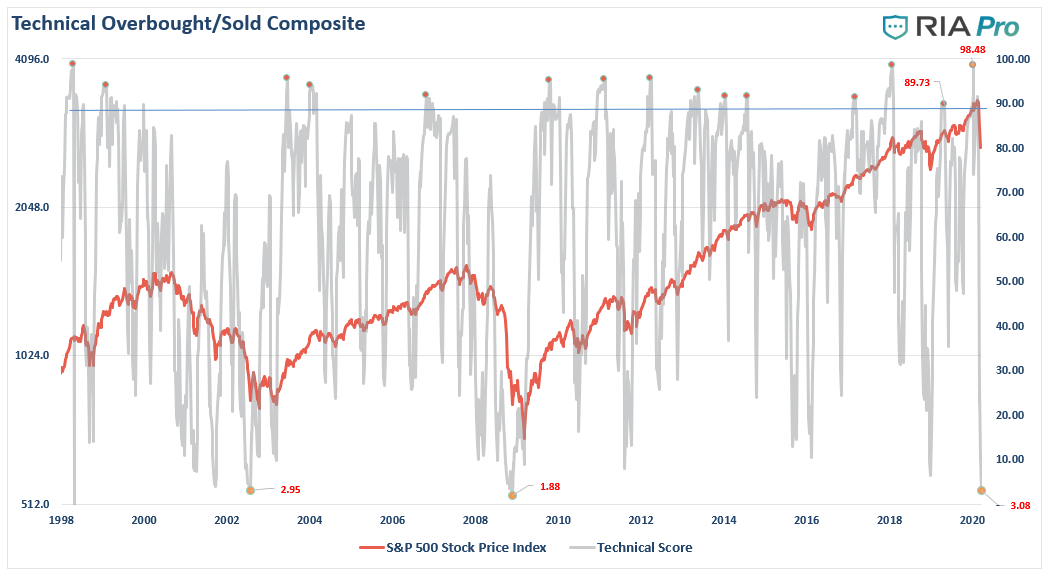

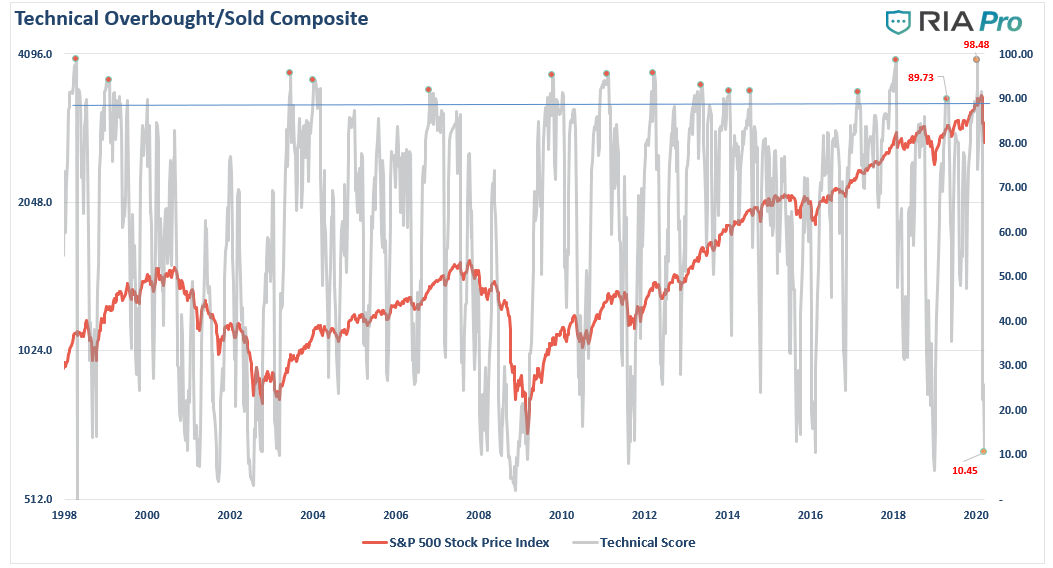

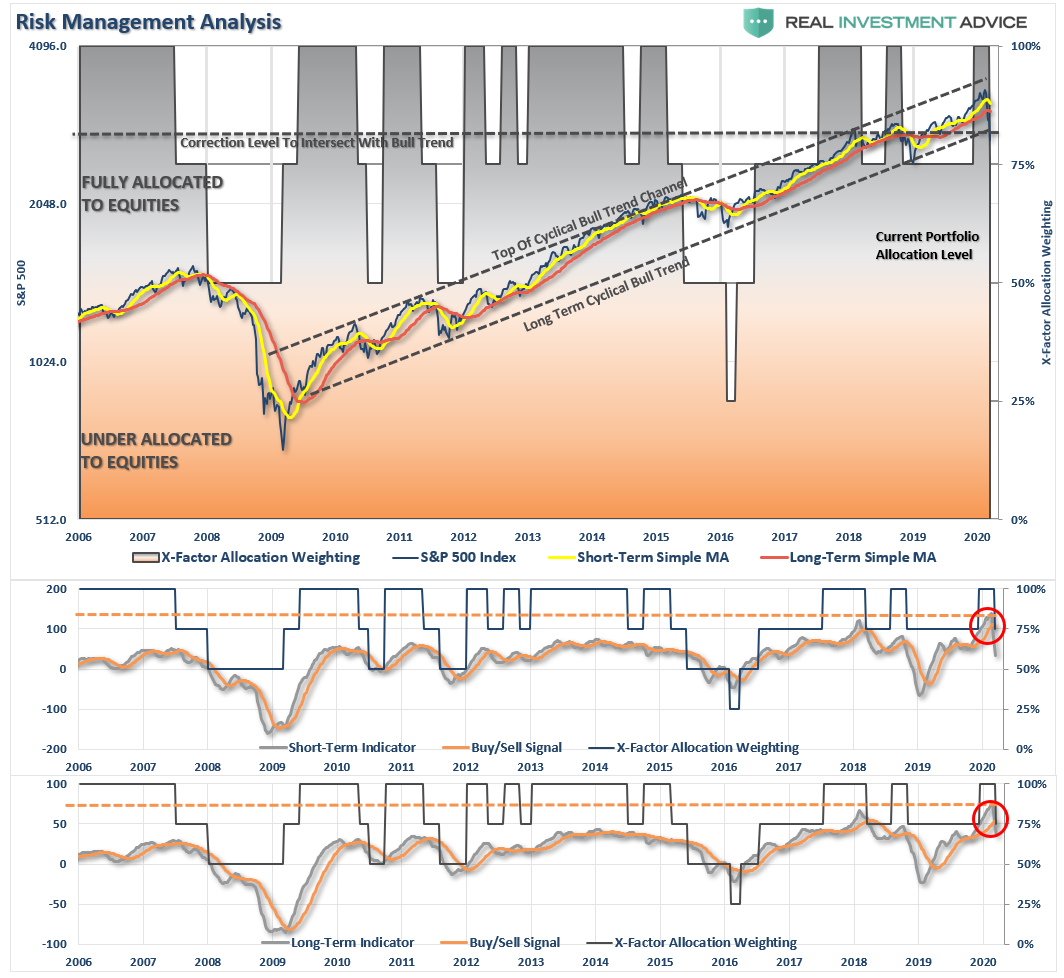

Technical Composite

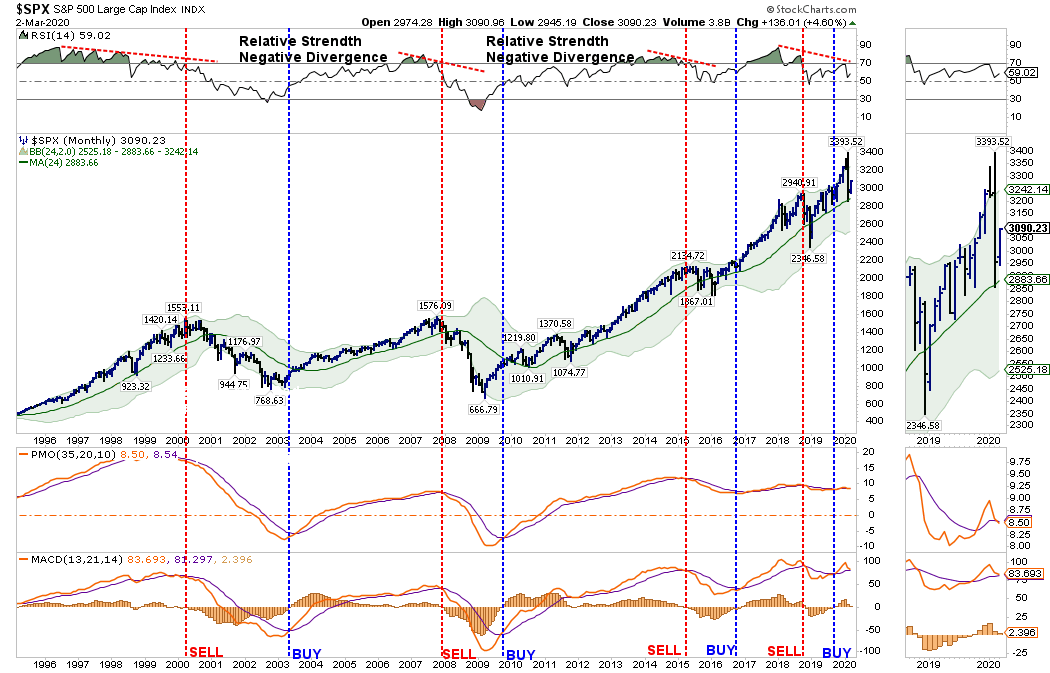

Note: The technical gauge bounced from the lowest level since both the “Dot.com” and “Financial Crisis.” However, note the gauge bottoms BEFORE the market bottoms. In 2002, lows were retested. In 2008, there was an additional 22% decline in early 2009.

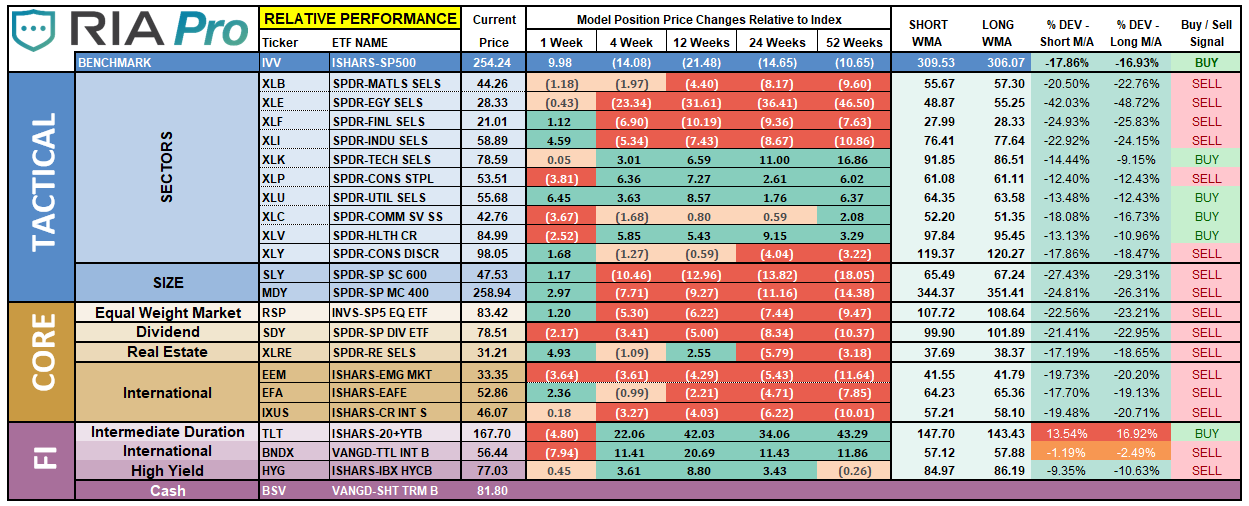

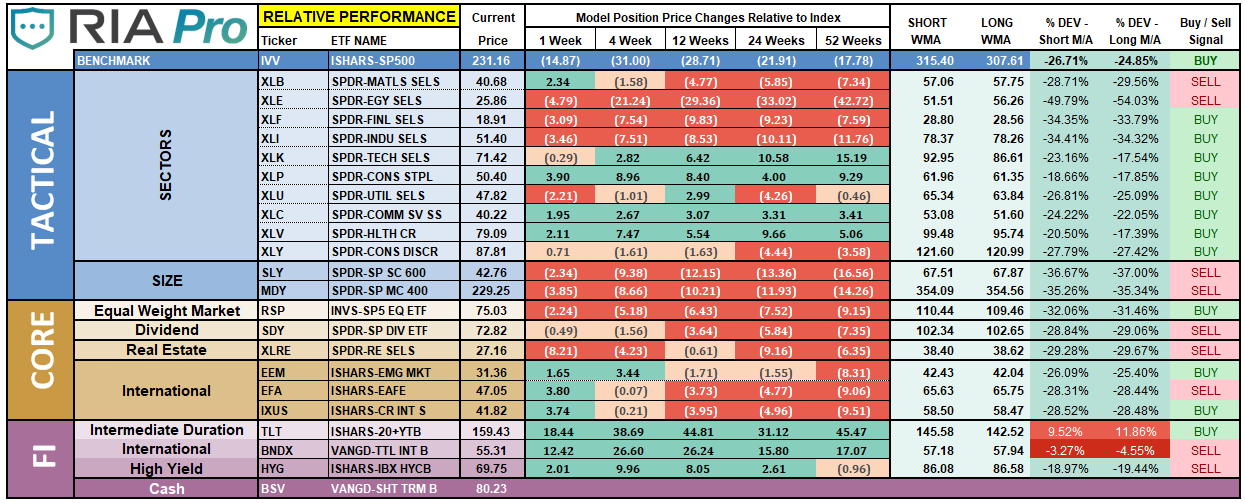

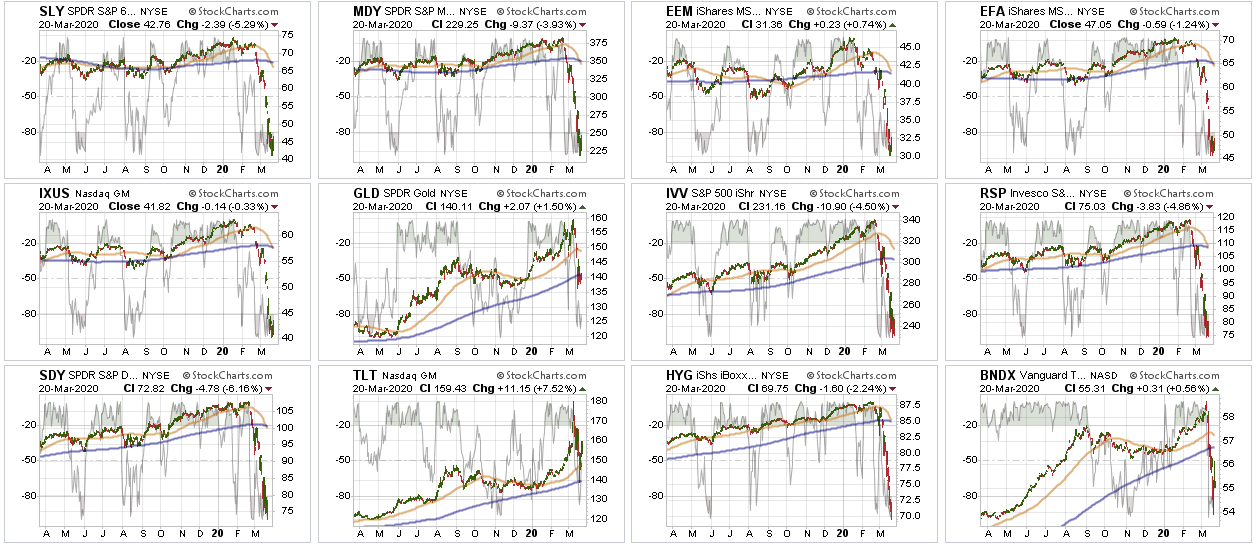

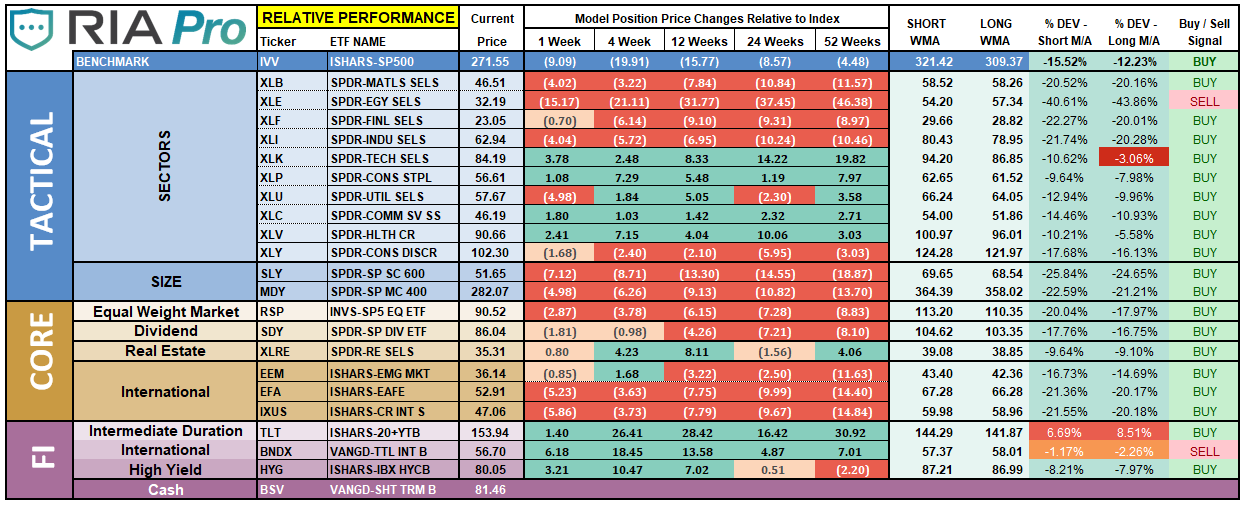

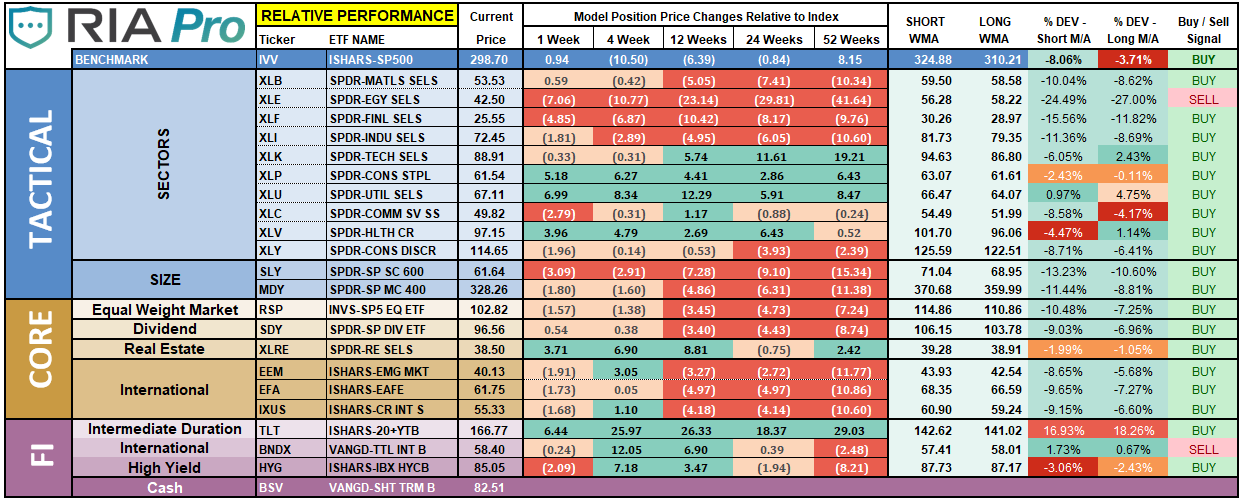

ETF Model Relative Performance Analysis

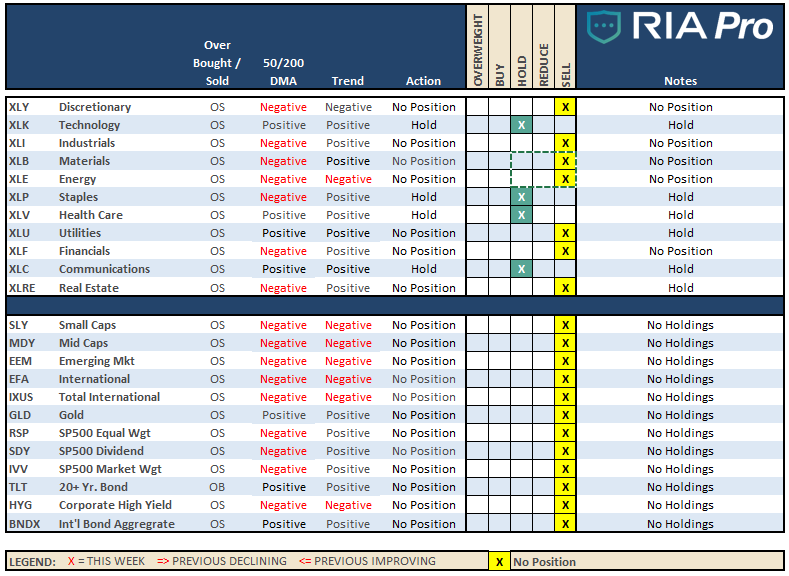

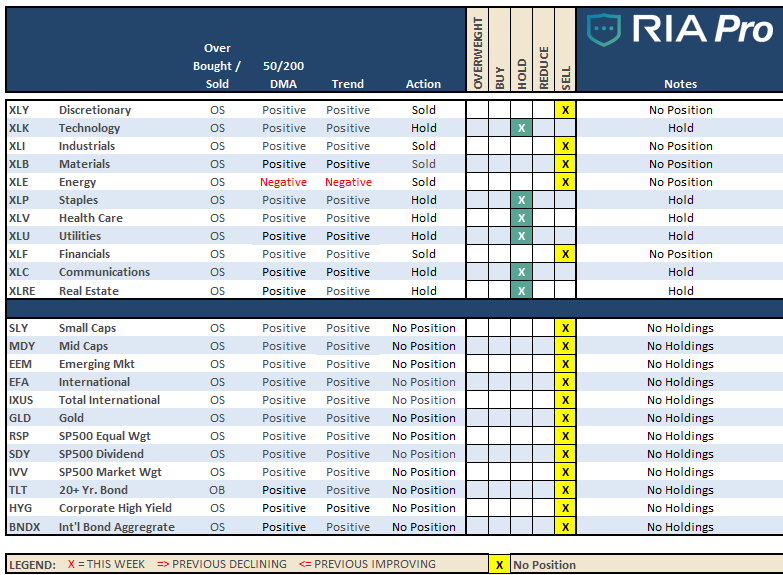

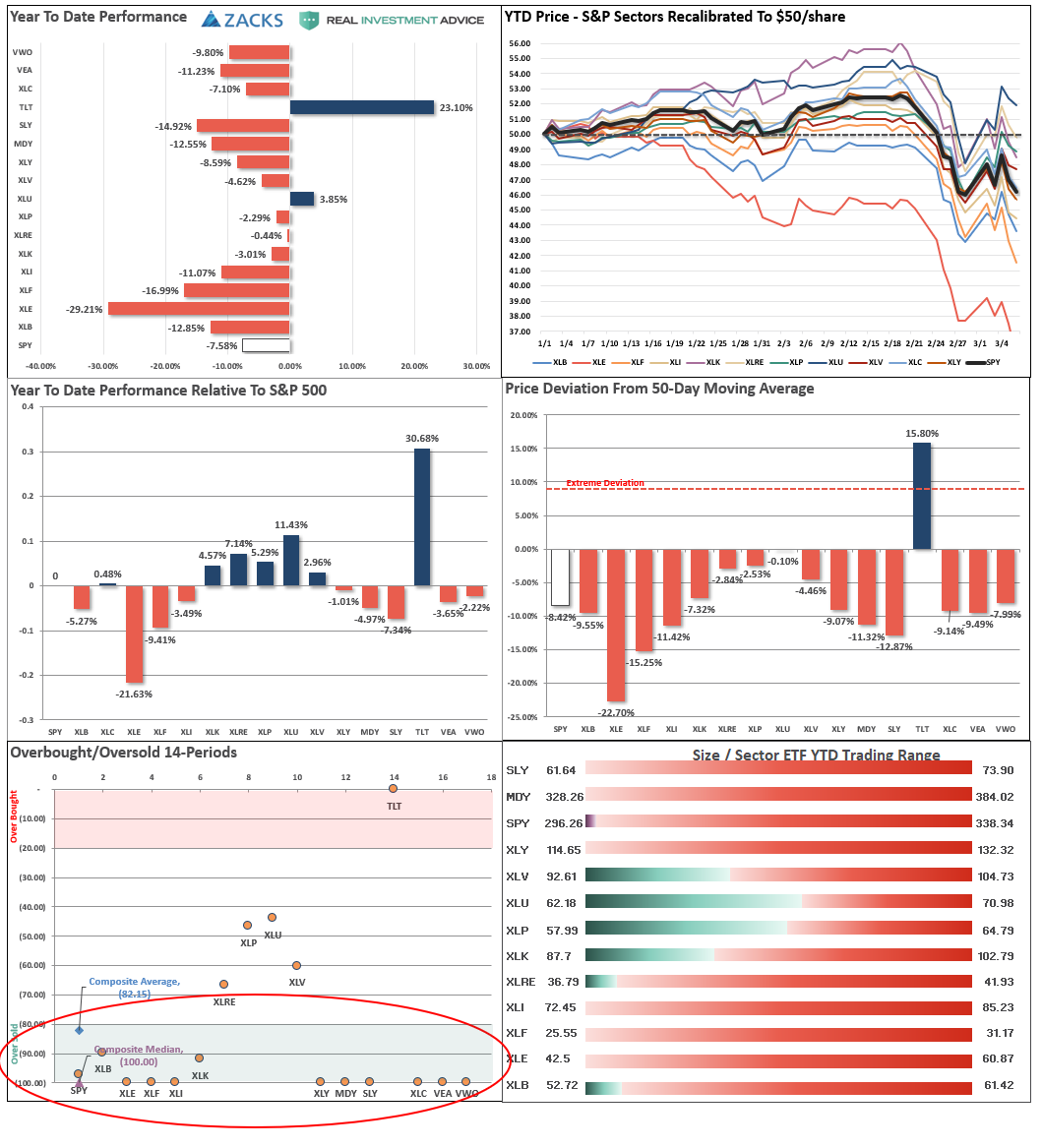

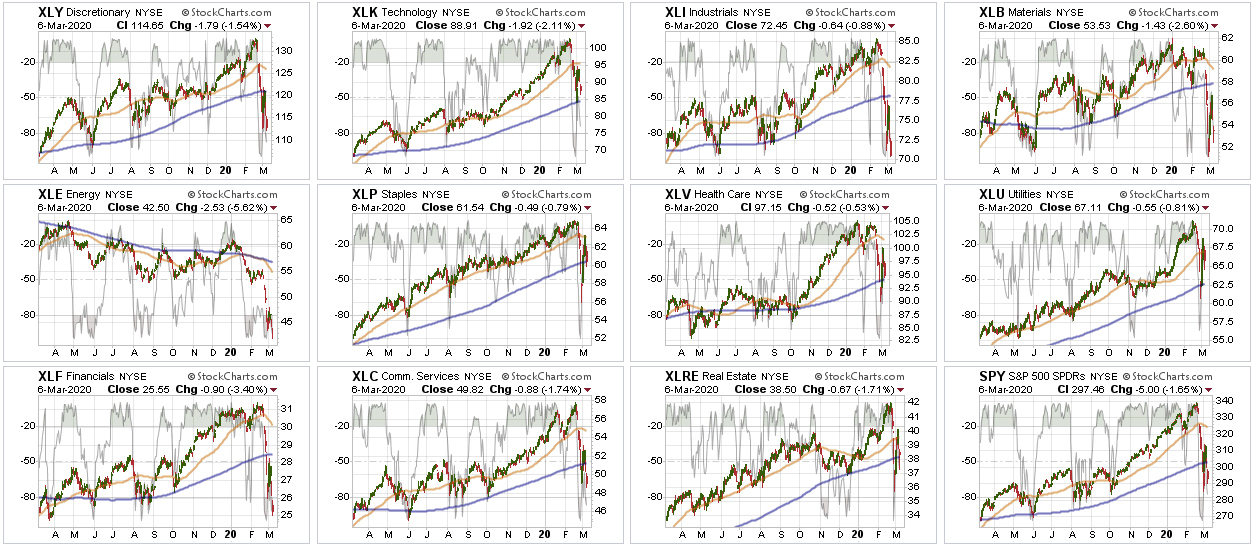

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

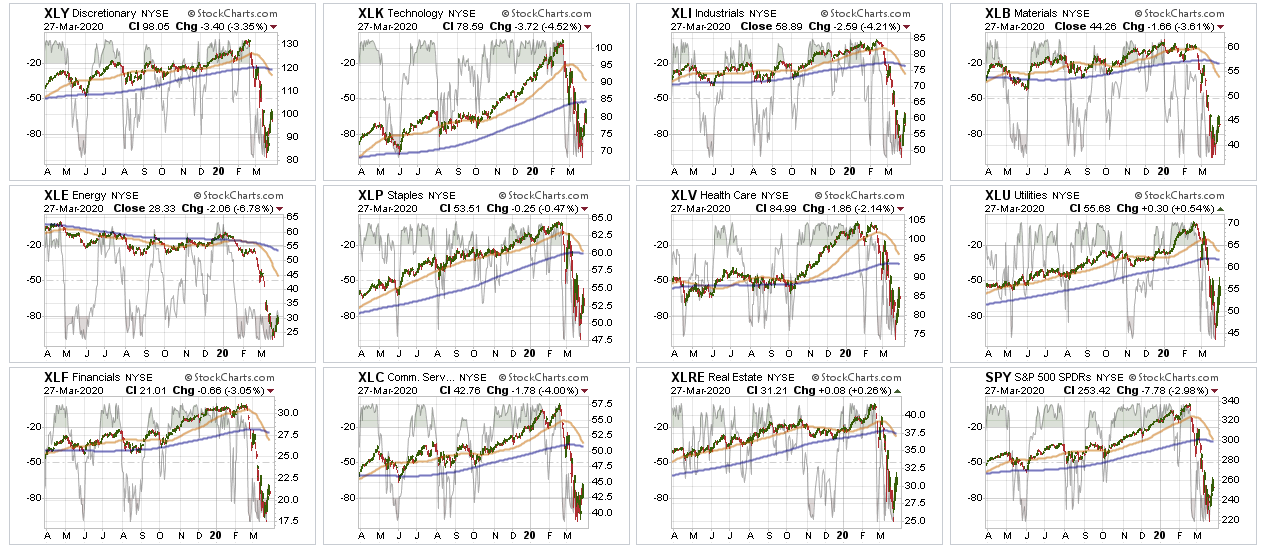

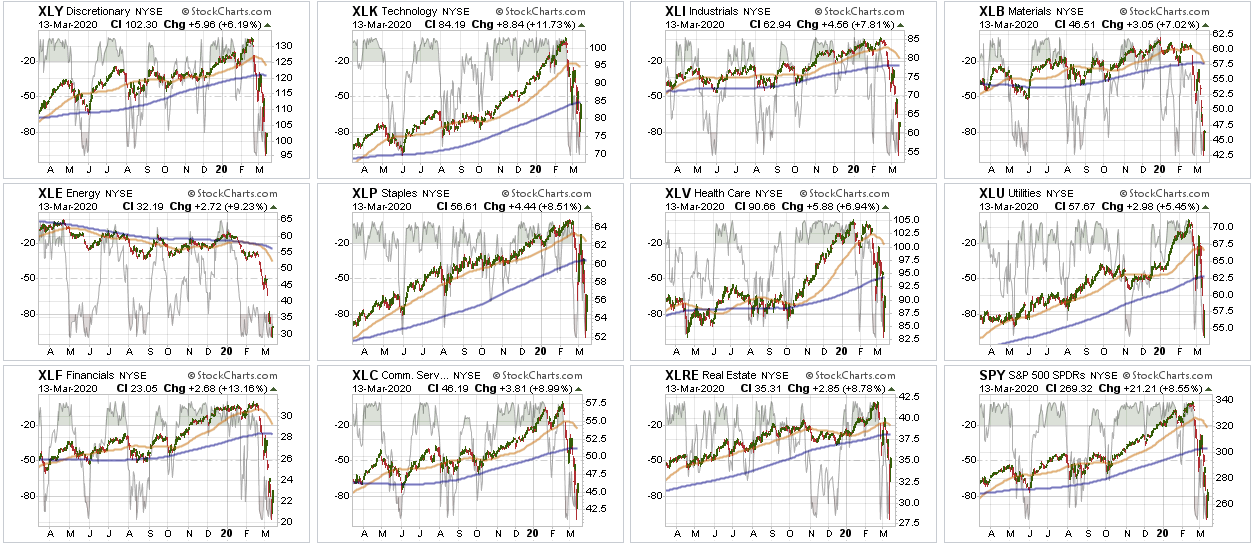

Finally, the markets bounced this past week.

However, don’t get too excited; there has been a tremendous amount of technical damage done which keeps us on the sidelines for now.

Improving – Discretionary (XLY), and Real Estate (XLRE)

We previously reduced our weightings to Real Estate and liquidated Discretionary entirely over concerns of the virus and impact on the economy. No change this week. We are getting more interested in REITs again, but are going to select individual holdings versus the ETF due to leverage concerns in the REITs.

Discretionary is going to remain under pressure due to people being able to go out and shop. This sector will eventually get a bid, so we are watching it, but we need to see an eventual end to the isolation of consumers.

Early last week, we shifted exposures in portfolios and added to our Technology and Communications sectors, bringing them up to weight. We also added QQQ, which was closed out on Friday.

Current Positions: XLK, XLC, 1/2 weight XLP, XLV

Weakening – None

No sectors in this quadrant.

Current Position: None

Lagging – Industrials (XLI), Financials (XLF), Materials (XLB), and Energy (XLE)

No change from last week, with the exception that performance continued to be worse than the overall market.

These sectors are THE most sensitive to Fed actions (XLF) and the shutdown of the economy. We eliminated all holdings in late February and early March.

Current Position: None

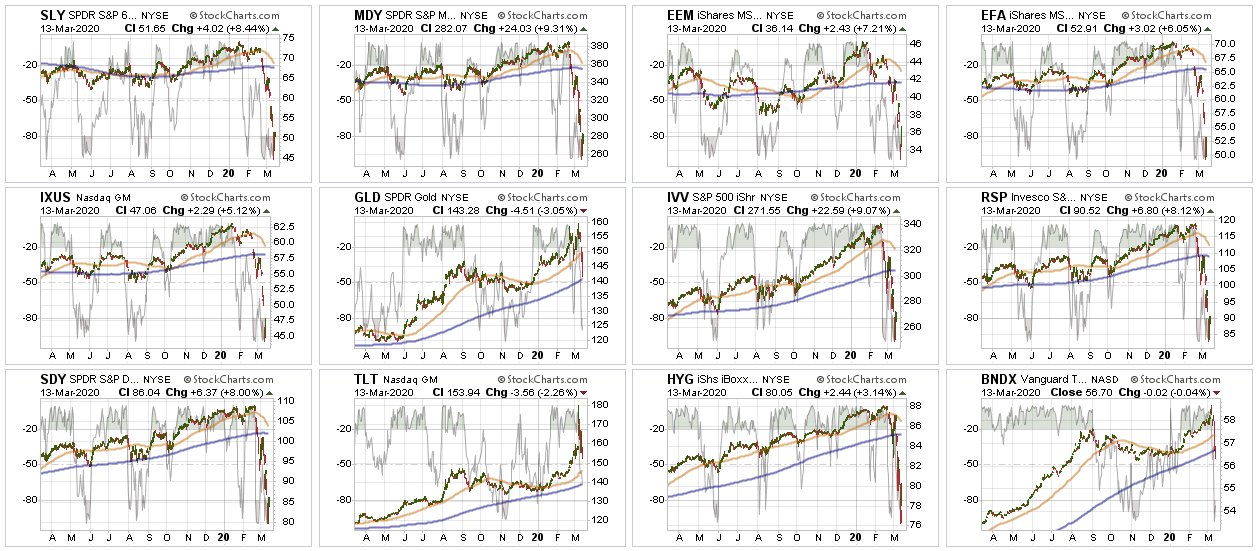

Market By Market

Small-Cap (SLY) and Mid Cap (MDY) – Four weeks ago, we sold all small-cap and mid-cap exposure over concerns of the impact of the coronavirus. We remain out of these sectors for now.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Same as small-cap and mid-cap. Given the spread of the virus and the impact on the global supply chain. Trading opportunities only.

Current Position: None

S&P 500 Index (Core Holding) – Given the rapid deterioration of the broad market, we sold our entire core position holdings for the safety of cash. We did add a small trading position in QQQ on Monday afternoon, and sold it on Friday.

Current Position: None

Gold (GLD) – We added a small position in GDX recently, and increased our position in IAU early this week. With the Fed going crazy with liquidity, this will be good for gold long-term, so we continue to add to our holdings on corrections.

Bonds regained their footing this week, as the Fed became the “buyer” of both “first” and “last” resort. Simply, “bonds will not be allowed to default,” as the Fed will guarantee payments to creditors. We have now reduced our total bond exposure to 20% of the portfolio from 40% since we are only carrying 10% equity currently. (Rebalanced our hedge.)

Current Positions: SHY, IEF, BIL

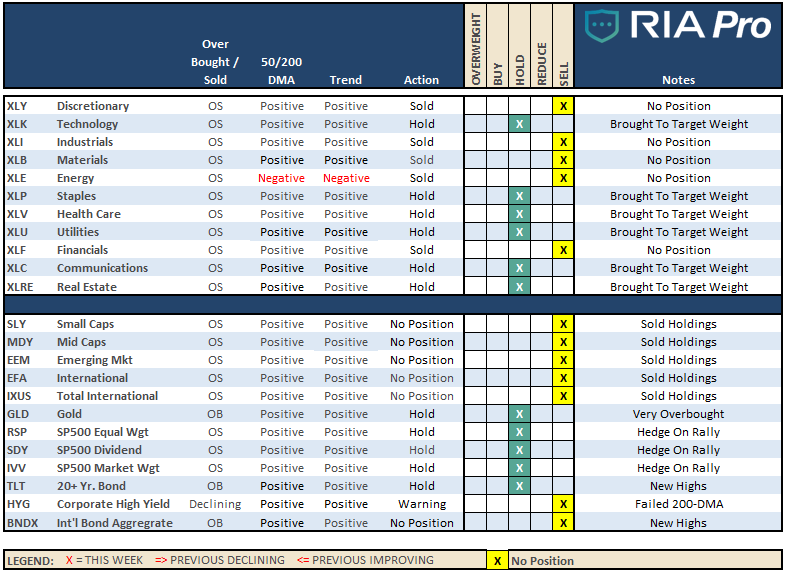

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

Despite the headlines of the “biggest rally in history” this past week, it’s easy to get sucked into the “Media headline” hype. However, let’s put this into some perspective:

Over the last “X” days the S&P 500 is:

5-days: +10.2%

6-days: +5.4%

10-days: -6.25%

It is much less exciting when compared to the fastest 30% plunge in history.

Keeping some perspective on where we are currently is very important. It’s easy to get swayed by the media headlines, which can lead us into making emotional investment mistakes. More often than not, emotional decisions turn out poorly.

We are starting our process of adding equities to the ETF models. As we head out of this bear market, ETF’s will have less value relative to our selective strategies.

This doesn’t mean we won’t use ETF’s at all, but we will selectively use them to fill in gaps to our individual equity selection, or for short-term trading opportunities.

Such was the case on Monday when we took on a position in QQQ for a bounce, and was subsequently closed out on Friday.

We also added small holdings of CLX and MRK to our long-term equity portfolio, as well as increased our exposure to IAU.

We continue to remain very defensive, and are in an excellent position with plenty of cash, reduced bond holdings, and minimal equity exposure in companies we want to own for the next 10-years.

We are just patiently waiting for the right opportunity to buy large chunks of these holdings with both stable, and higher yields.

Let me repeat from last week:

The ONLY people who care more about your money than you, is all of us at RIA Advisors.

We will NOT “buy the bottom” of the market. We will buy when we SEE the bottom of the market is in and risk/reward ratios are clearly in our favor.

This has been THE fastest bear market in history. We are doing our best to preserve your capital so that you meet your financial goals. Bear markets are never fun, but they are necessary for future gains.

We’ve got this.

Please don’t hesitate to contact us if you have any questions, or concerns.

Lance Roberts

CIO

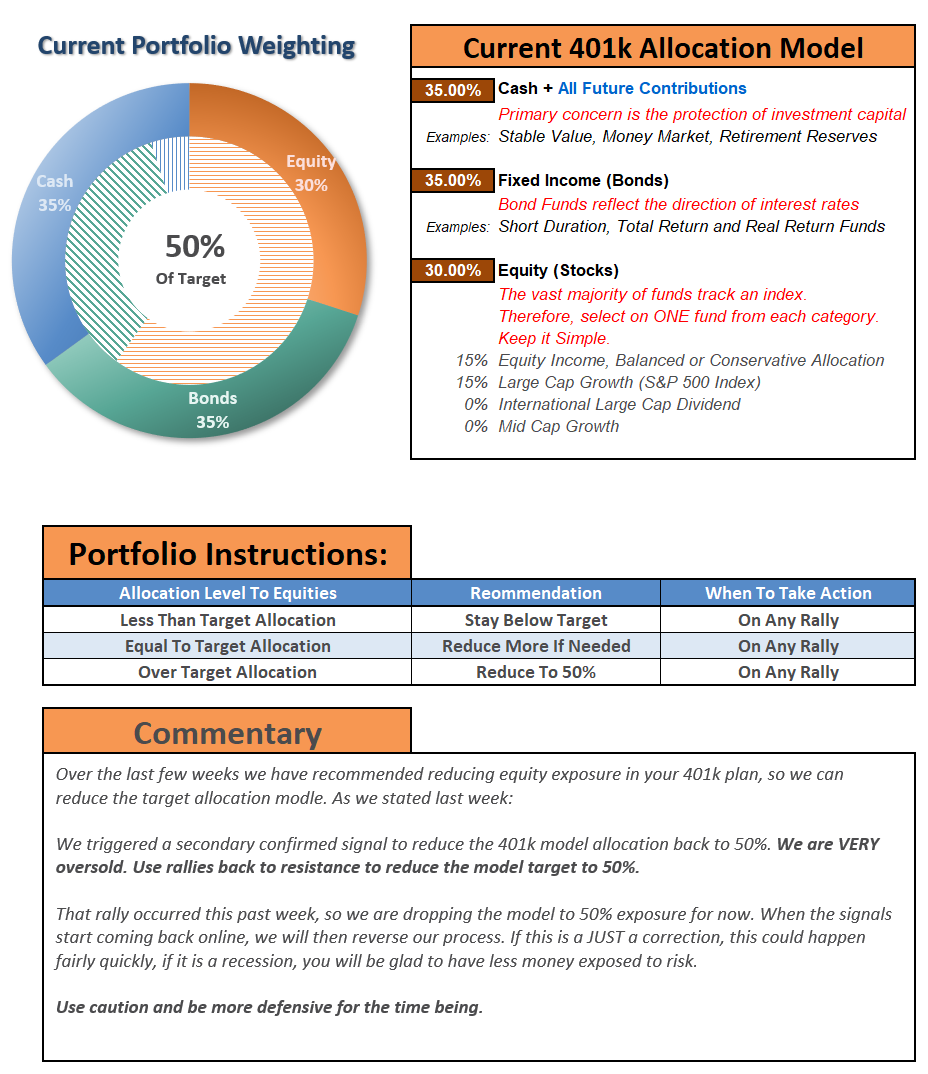

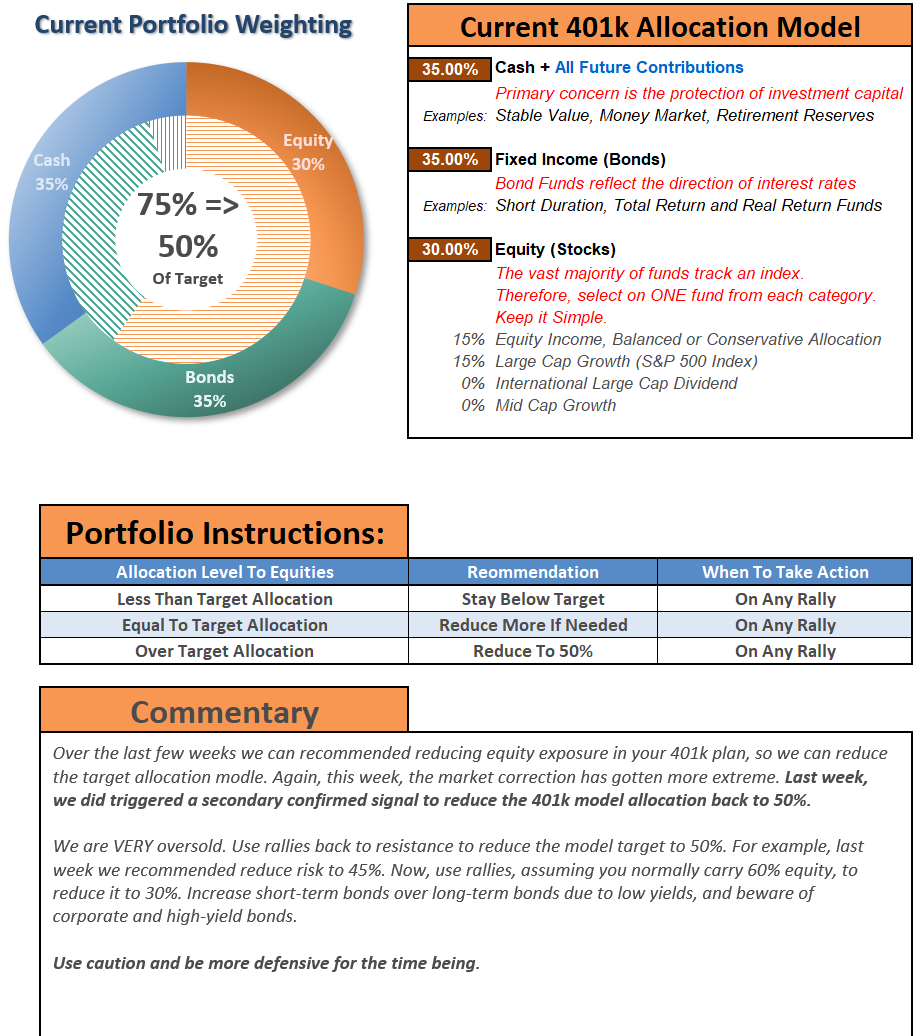

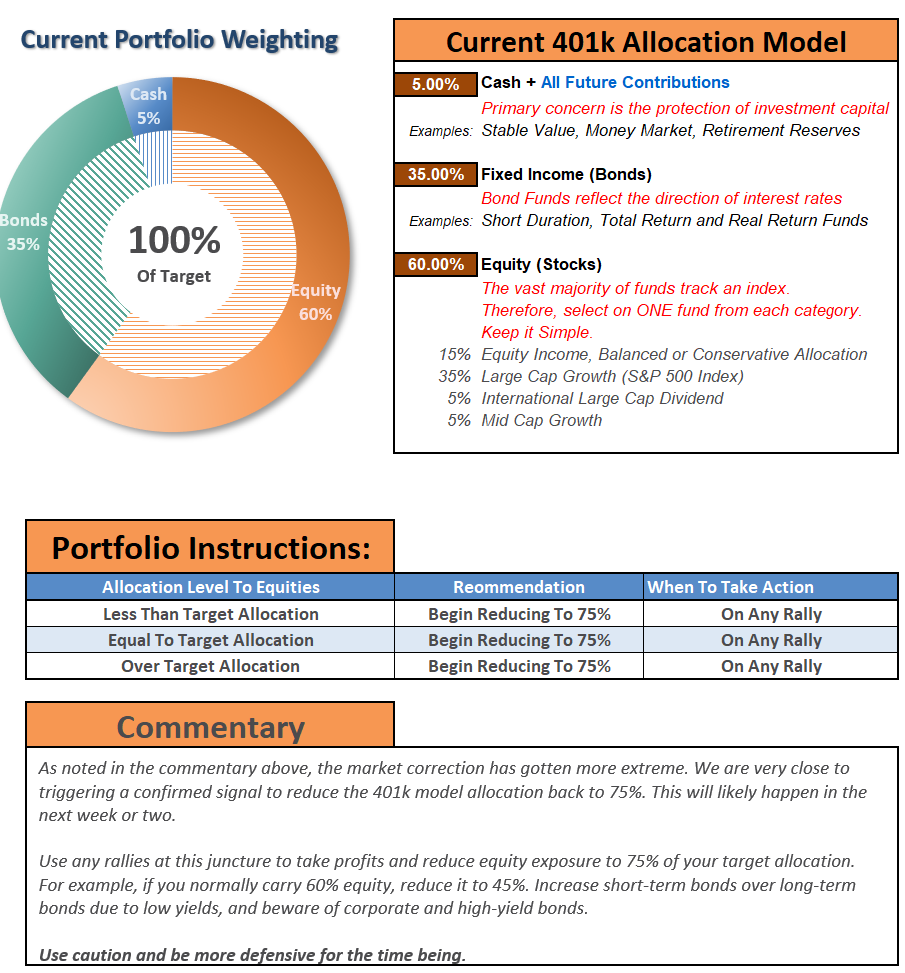

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber(You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

Name of the company

Plan Sponsor

A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

The “2020 SOCIALLY DISTANT INVESTMENT SUMMIT” is coming on Thursday, April 2nd.

Click the link below to receive an email with a special “invitation only” link when the summit goes “live.” (Current newsletter subscribers are already registered.)

“From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance.

Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Chart Updated Through Friday

Not surprisingly, here were the headlines, almost exactly as we wrote them:

Well, you get the idea.

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. More importantly, “bear markets” only end when “NO ONE wants to buy it.”

Fed Can’t Fix It

As noted above, the “bear market” will NOT be over until the credit market is fixed. We are a long way from that being done, given the blowout in yields currently occurring.

The Fed has cut rates by 150 basis points to near zero and run through its entire 2008 crisis handbook.

That wasn’t enough to calm markets, though — so the central bank also announced $1 trillion a day in repurchase agreements and unlimited quantitative easing, which includes a hard-to-understand $625 billion of bond-buying a week going forward. At this rate, the Fed will own two-thirds of the Treasury market in a year.

But it’s the alphabet soup of new programs that deserve special consideration, as they could have profound long-term consequences for the functioning of the Fed and the allocation of capital in financial markets. Specifically, these are:

CPFF (Commercial Paper Funding Facility) – buying commercial paper from the issuer.

PMCCF (Primary Market Corporate Credit Facility) – buying corporate bonds from the issuer.

SMCCF (Secondary Market Corporate Credit Facility) – buying corporate bonds and bond ETFs in the secondary market.

MSBLP (Main Street Business Lending Program) – Details are to come, but it will lend to eligible small and medium-sized businesses, complementing efforts by the Small Business Association.

To put it bluntly, the Fed isn’t allowed to do any of this.”

However, on Friday, the Federal Reserve ran into a problem, which could poses a risk for the markets going forward. As Jim noted, the mind-boggling pace of bond purchases quickly hit the limits of what was available to pledge for collateral.

Or rather, the Fed’s “unlimited QE,” may not be so “unlimited” after all.

The consequence is the Fed is already having to start cutting back on its QE program. That news fueled the late-day sell-off Friday afternoon. (Charts courtesy of Zerohedge)

While Congress did pass the “CARES” act on Friday, it will do little to backstop what is about to happen to the economy for two primary reasons:

The package will only support the economy for up to two months. Unfortunately, there is no framework for effective and timely deployment; firms are already struggling to pay rents, there are pockets of funding stress in credit markets as default risks build, and earnings guidance is abandoned.

The unprecedented uncertainty facing financial markets on the duration of social distancing, the depth of the economic shock and when the infection rate curve will flatten, and there are many unknowns which will further undermine confidence.

Both of these points are addressed in this week’s Macroview but here are the two salient points to support my statement:

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance, can be provided. This will lead to higher and longer-duration of, unemployment.”

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any type of disruption to their income going into the recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits leads to higher unemployment and lower asset prices until the cycle is complete.

The long term bull pattern that existed since the 3/9/09 is over. That means the pattern of investors confidently buying every decline is over.

The market became historically oversold on 3/23 using many metrics, and that oversold condition coincided with the long term support area of S&P 500 2110-2180.

The short-covering and rebalancing had a lot to do with the size and speed of the 3-day rally. Also, we know the lack of ETF liquidity played a huge role as well as algorithmic trading.

Technically the market can still go up 6.9% higher from here to hit the 50% retracement level (3386 – 2237 = 1149/2 = 574 + 2237 = 2811….2811/2630 = +6.9%.) I would not bet on it.

The market only sustains a rally once there is light at the Coronavirus tunnel.

I do not think the S&P 500 will hit a new high this year. Maybe not in 2021, either.

His analysis agrees with our own, which we discussed with you last week.

“The good news is the markets are now more extremely oversold on a variety of measures than at just about any other point in history.

Warning: Any reversal will NOT BE the bear market bottom. It will be a ‘bear market’ rally you will want to ‘sell’ into. The reason is there are still many investors trapped in ‘buy and hold’ and ‘passive indexing’ strategies that are actively seeking an exit. Any rallies will be met with redemptions.

Most importantly, all of our long-term weekly ‘sell signals’ have now been triggered. Such would suggest that a rally back to the ‘bullish trend line’ from 2009 will likely be the best opportunity to ‘sell’ before the ‘bear market’ finds its final low.”

Last week’s chart updated through Friday’s close.

While the recent lows may indeed turn out to be “the bottom,” I highly suspect they won’t. Given the sell signals have been registered at such high levels, the time, and distance, needed to reverse the excesses will require a deeper market draw.

As Jeff Hirsch from Stocktrader’s Alamanc noted:

“While we are all rooting for the market to find support here so much damage has been done. A great deal of uncertainty remains for the economy and health crisis. This looks like a bear market bounce.

History suggests that we are in for some tough sledding in the market this year with quite a bit of chop. When the January Barometer came in with a negative reading, our outlook for 2020 began to diminish as every down January since 1950 has been followed by a new or continuing bear market, a 10% correction, or a flat year. Then another warning sign flashed when DJIA closed below its December closing low on February 26, 2020 as the impact of this novel coronavirus began to take its toll on Wall Street.

In the March Outlook, we presented this graph of the composite seasonal pattern for the 22 years since 1950 when both the January Barometer as measured by the S&P 500 were down, and the Dow closed below its previous December closing low in the first quarter. Below is a graph of DJIA, S&P 500 and NASDAQ Composite for 2020 year-to-date as of the close on March 25. Comparing 2020 market action to these 22 years, suggests a choppy year ahead with the potential for several tests of the recent low.”

“The depth of this waterfall decline may be too deep for the market to rebound quickly. This bear market also put this year’s Best Six Months (November-April) at risk of being negative. The record of down Best Six Months is not encouraging and it reminds us of a salient quote from the Almanac from an old market sage,

‘If the market does not rally, as it should during bullish seasonal periods, it is a sign that other forces are stronger and that when the seasonal period ends those forces will really have their say.’— Edson Gould (Stock market analyst, Findings & Forecasts, 1902-1987)'”

On a short-term basis, the market is also suggesting some risk. The daily chart below shows the market rallied to, and failed at, the first level of the Fibonacci retracement we outlined last week, suggesting profits be taken at this level. While there are two remaining targets for the bear market rally, the probabilities weigh heavily against them. (This doesn’t mean they can’t be achieved, it is “possible,” just not “probable.”)

Furthermore, with the “Death Cross” triggering on Friday (the 50-dma crossing below the 200-dma), this will put further downside pressure on any “bear market” advance from current levels.

Given the magnitude, and multiple confirmations, of these signals, it is far too soon to assume the “bear market” is over. This is particularly the case, given the sell-off is less than one-month-old.

Bear markets, and recessions, tend to last 18-months on average.

The current bear market and recession are not the results of just the “coronavirus” shock. It is the result of many simultaneous shocks from:

Economic disruption

Surging unemployment

Oil price shock

Collapsing consumer confidence, and

Most importantly, a “credit event.”

We likely have more to go before we can safely assume we have turned the corner.

In the meantime, use rallies to raise cash. Don’t worry about trying to “buy the bottom.”There will be plenty of time to see “THE” bottom is in, and having cash will allow you to “buy stocks” from the last of the “weak hands.”

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

S&P 500 Tear Sheet

Performance Analysis

Technical Composite

Note: The technical gauge bounced from the lowest level since both the “Dot.com” and “Financial Crisis.” However, note the gauge bottoms BEFORE the market bottoms. In 2002, lows were retested. In 2008, there was an additional 22% decline in early 2009.

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

Finally, the markets bounced this past week.

However, don’t get too excited; there has been a tremendous amount of technical damage done which keeps us on the sidelines for now.

Improving – Discretionary (XLY), and Real Estate (XLRE)

We previously reduced our weightings to Real Estate and liquidated Discretionary entirely over concerns of the virus and impact on the economy. No change this week. We are getting more interested in REITs again, but are going to select individual holdings versus the ETF due to leverage concerns in the REITs.

Discretionary is going to remain under pressure due to people being able to go out and shop. This sector will eventually get a bid, so we are watching it, but we need to see an eventual end to the isolation of consumers.

Early last week, we shifted exposures in portfolios and added to our Technology and Communications sectors, bringing them up to weight. We also added QQQ, which was closed out on Friday.

Current Positions: XLK, XLC, 1/2 weight XLP, XLV

Weakening – None

No sectors in this quadrant.

Current Position: None

Lagging – Industrials (XLI), Financials (XLF), Materials (XLB), and Energy (XLE)

No change from last week, with the exception that performance continued to be worse than the overall market.

These sectors are THE most sensitive to Fed actions (XLF) and the shutdown of the economy. We eliminated all holdings in late February and early March.

Current Position: None

Market By Market

Small-Cap (SLY) and Mid Cap (MDY) – Four weeks ago, we sold all small-cap and mid-cap exposure over concerns of the impact of the coronavirus. We remain out of these sectors for now.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Same as small-cap and mid-cap. Given the spread of the virus and the impact on the global supply chain. Trading opportunities only.

Current Position: None

S&P 500 Index (Core Holding) – Given the rapid deterioration of the broad market, we sold our entire core position holdings for the safety of cash. We did add a small trading position in QQQ on Monday afternoon, and sold it on Friday.

Current Position: None

Gold (GLD) – We added a small position in GDX recently, and increased our position in IAU early this week. With the Fed going crazy with liquidity, this will be good for gold long-term, so we continue to add to our holdings on corrections.

Bonds regained their footing this week, as the Fed became the “buyer” of both “first” and “last” resort. Simply, “bonds will not be allowed to default,” as the Fed will guarantee payments to creditors. We have now reduced our total bond exposure to 20% of the portfolio from 40% since we are only carrying 10% equity currently. (Rebalanced our hedge.)

Current Positions: SHY, IEF, BIL

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

Despite the headlines of the “biggest rally in history” this past week, it’s easy to get sucked into the “Media headline” hype. However, let’s put this into some perspective:

Over the last “X” days the S&P 500 is:

5-days: +10.2%

6-days: +5.4%

10-days: -6.25%

It is much less exciting when compared to the fastest 30% plunge in history.

Keeping some perspective on where we are currently is very important. It’s easy to get swayed by the media headlines, which can lead us into making emotional investment mistakes. More often than not, emotional decisions turn out poorly.

We are continuing our process of blending the Equity and ETF models. As we head out of this bear market, ETF’s will have much less value relative to our selective strategies.

This doesn’t mean we won’t use ETF’s at all, but we will selectively use them to fill in gaps to our individual equity selection, or for short-term trading opportunities.

Such was the case on Monday when we took on a position in QQQ for a bounce, and was subsequently closed out on Friday.

We also added small holdings of CLX and MRK to our long-term portfolio, as well as increased our exposure to IAU.

We continue to remain very defensive, and are in an excellent position with plenty of cash, reduced bond holdings, and minimal equity exposure in companies we want to own for the next 10-years.

We are just patiently waiting for the right opportunity to buy large chunks of these holdings with both stable, and higher yields.

Let me repeat from last week:

The ONLY people who care more about your money than you, is all of us at RIA Advisors.

We will NOT “buy the bottom” of the market. We will buy when we SEE the bottom of the market is in and risk/reward ratios are clearly in our favor.