Too often, we tend to focus on individual stocks and other investments that will hopefully lead to wealth.

While that is O.K., it isn’t enough.

The issue is investing without a sound “plan” is the same as building a house without a “blueprint.” Yes, you will get something, but it probably won’t be the result you set out to get.

Be A Rooftop Thinker!

By starting with a proper plan you take into account all assets, liabilities and sources of income. From there it becomes much easier to focus on the investments YOU NEED to meet your financial goals.

Work from rooftop to basement for financial success!

Investment Manager, Lance Roberts and Certified Financial Planner, Richard Rosso we’ll help you understand:

How proper Social Security and Medicare strategies can boost retirement income,

Our concept of financial life benchmarking which is there to help you become more self aware of your financial goals, wants and needs,

How using the wrong, or enthusiastic investment returns can place your retirement in jeopardy,

When housing decisions in retirement can affect your quality of life, and;

The art of talking about your gifting and estate intentions with loved ones.

This 30-minute webinar can keep your from making costly investment mistakes and help bring clarity to your future financial plan.

If you would like to access this recorded webinar please click here.

Anatomy of The Bear. Lessons from Russell Napier.

One of my annual re-reads is Russell Napier’s classic tome “Anatomy of the Bear.”

A mandatory study for every financial professional and investor who seeks to understand not only how damaging bear markets can be but also the traits which mark their bottoms. Every bear is shaken from hibernation for different reasons. However, when studying the four great bottoms of bears in 1921, 1932, 1949 and 1982, there are several common traits to these horrendous cycles. I thought it would be interesting to share them with you.

First, keep in mind, bear markets characteristically purge weakness – weak companies, weak advisors, weak investors. I want you to consider them less a bloodletting and more a cleansing of a system. There will be unsuitable investors who will never return to the market and justifiably so. Businesses that were patronized pre-Covid, will either be gone or completely reinvent. Bear markets slash equity valuations. Unfortunately, this doesn’t mean that stocks return to healthy valuations quickly after a bear departure. Some believe the global economy can turn on and off like a light switch without major repercussions. In other words, the belief is once the worst of this horrid virus ceases, business activity invariably will return to normal. I believe it’ll be quite the contrary.

I mentioned on the radio show in December that I expected wage growth to top out in 2019. Keep in mind, through this yet another outlier economic upheaval, there will be employers who will realize they don’t require as many employees and will let them go or cap their wages for years to rebuild profit margins. Without the tailwind of stock buybacks to equity prices, corporate employees will bear the brunt of the pain. In addition, organizations will realize many of their remaining employees are equipped to work from home and perhaps gather in-person perhaps once a month or every couple of weeks. Thus, large commercial space will no longer be required which is going to require massive reinvention by the commercial real estate industry.

The cry of nationalism will rise. Products manufactured overseas especially China, will take a hit which means Americans will face greater inflationary challenges while also dealing with muted or non-existent wage growth. We will experience ‘ more money chasing too-few goods.’ Many, especially younger generations will continue to strip themselves down to basics (I especially envision this in Generation Z; those born in the mid-late 1990s such as my daughter Haley). This sea-change will require most of the U.S. population to finally live below their means, dramatically downsize, reinvent, expand, the definition of wealth to include more holistic, ethereal methods that go way beyond household balance sheets and dollars.

I hope I’m wrong. So very wrong about most of what I envision for the future.

Here are several traits that every major market bottom share – courtesy of Russell Napier:

Bears tend to die on low volume, at least the big bears do.

Low volume represents a complete disinterest in stocks. Keep in mind this clearly contradicts the tenet which states that bears end with one act of massive capitulation – a downward cascade on great volume. Those actions tend to mark the beginning of a bear cycle, not the end. A rise in volume on rebounds, falling volumes on weakness would better mark a bottoming process in a bear market.

2. Bears are tricky.

There will appear to be a recovery; an ‘all-clear’ for stock prices. It’ll suck in investors who believe the market recovery is upon us just to be financially ravaged again. Anecdotally, I know this cycle isn’t over as I still receive calls from people who are anxious to get into the market and perceive the current market a buying opportunity. At the bottom of a bear, I should be hearing great despair and clear disdain for stock investing.

3. Bears can be tenacious.

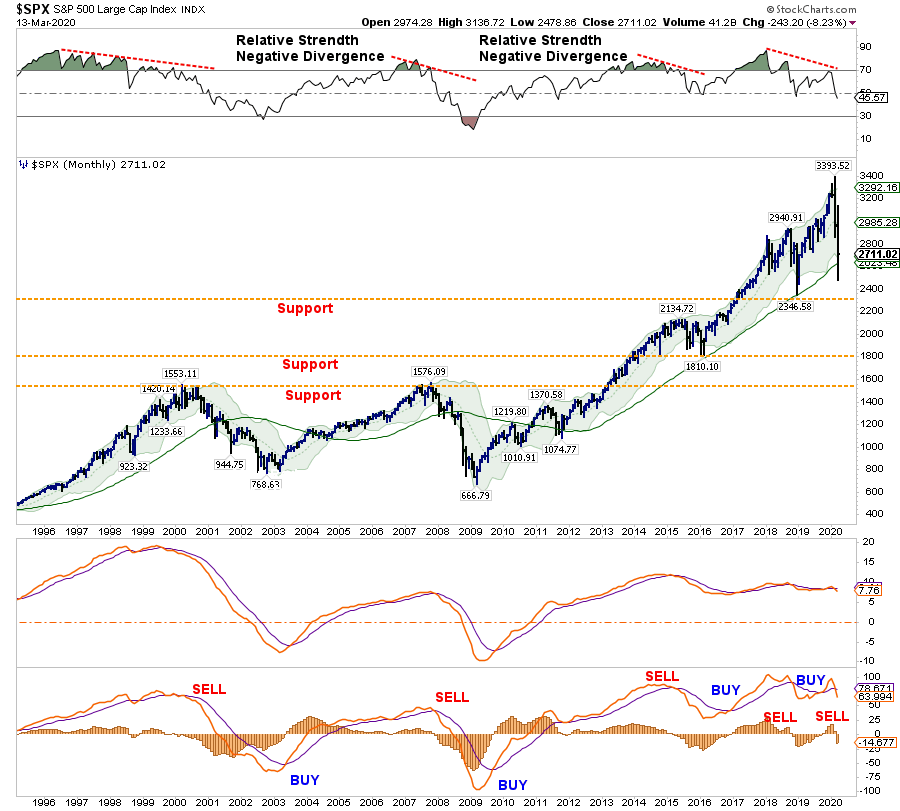

They refuse to die or at the least, quickly return to hibernation. The 1921 move from overvaluation to undervaluation took over ten years. Bear markets, where three-year price declines make overvalued equities cheap, are the exception, not the rule. As of this writing, the Shiller P/E is at 24x – hardly a bargain. At the bottom market cycle of the Great Recession, the Shiller CAPE was at 15x. There is still valuation adjustment ahead.

4. Bears can depart before earnings actually recover.

Investors who wait for a complete recovery in corporate earnings will arrive late to the stock-investment party. Most likely it’s going to take a while (especially with their debt burden), for the majority of U.S. companies to reflect healthy earnings growth. CEOs who employ stock buybacks to boost EPS will be considered pariahs and gain unwanted attention from Congress and even the Executive Branch. My thought is a savvy investor should look to minimize indexing and select individual stocks with strong balance sheets which include low debt and plenty of free cash flow within sectors and industries that are nimble to adjust to the global economy post-crisis.

5. Bear market damage can be inconceivable, especially to a generation of investors who never experienced one.

The bear market of 1929-32 was characterized by an 89% decline. The average is 38% for bears; however, averages are misleading. I have no idea how much damage this bear ultimately unleashes. The closest comparison I have is the 1929-1932 cycle. However, with the massive fiscal and monetary stimulus (and I don’t believe we’ve seen the full extent of it yet), my best guess is a bear market contraction somewhere between the Great Depression and Great Recession. At the least, I believe we re-test lows and this bear is a 40-45% retracement from the highs.

6. Bear markets end on the return of general price stability and strong demand for durables such as autos.

In 1949, as in 1921 and 1932, a return of general price stability coincided with the end of the equity bear market. Demand and price stability of selected commodities augured well for general price stabilization. Watch how industrial metals recover such as copper, now at the lowest levels since the fall of 2017. The Baltic Dry Index is off close to 20% so far this year. Low valuations (not there yet), when combined with a return to normalcy in the general price level, may provide the best opportunity for future above-average equity returns. We are not there.

7. Bear markets that no longer decline on bad news are a positive.

The combination of large short positions in conjunction with a market that fails to decline on bad news was overall a positive indicator of a rebound in 1921, 1932 and 1949. Also, limited stock purchases by retail investors may be considered an important building block for a bottom. Since the worst of economic numbers haven’t been witnessed yet, there remains too much hope of a vicious recovery in stock prices as well as the overall global economies.

8. Not all bear markets lead the economy by six-to-nine months.

Generally, markets lead the economy. However, this tenet failed to hold true for the four great bears. At extreme times, the bottoms for the economy and the equity market were aligned and in several cases, the economy LED stocks higher! It’s unclear whether this bear behaves in a similar fashion only because of massive fiscal and monetary stimulus. We’re not done with stimulus methods either. If anything, they’ve just begun! I know. Tough to fathom.

For me and the RIA Team, every bear provides an important lesson. The beast comes in all sizes; their claws differ in sharpness. However, they are all dangerous to financial wealth.

I believe the market will eventually witness a “V” shaped recovery due to unprecedented stimulus. Unfortunately, I believe the economy will remain sub-par for a long period. Here’s a vision I shared on Facebook recently:

Let me give you one example how an economy cannot turn off, then on, like a light switch.

Joe’s Donuts is closed. Joe lets his 2 employees go, at least temporarily. Joe employs his wife Emily to assist as she’s just been laid off from her job. Joe is a quick thinker. He creates pre-packaged dough-to-go bags and sells them outside the store. His sales are off 75% as most businesses around him are shuttered. Joe was able to negotiate postponement of his rent for one month but will have to pay two months in May.

Joe has a profitable business but he’s already eaten through a quarter of his cash reserves to pay for supplies, maintain expenses to keep going. He can’t afford another month of quarantine.

The quarantine is lifted May 1 (best case scenario). Joe’s establishment is open! He’s hesitant to have employees return because he wants to gauge business for a month. He discovers that business is still off 40% from last year at the same time. Why? Because his patrons have either been let go or in repair of ravaged household balance sheets. In addition, he notices that purchasing boxes of donuts for office meetings is way off.

Joe contacts his former 2 employees. He tells them he still doesn’t require them. He’s handling the traffic sufficiently alone at this time. Joe now owes 2 months of rent. He takes one month from the business’ reserve account; distributes another from his retirement account.

Joe’s wife Ellen has been called back to work by her former employer, a local car dealership. She’s been asked to work the same job, same responsibilities. However, the pay is 10% less. Out of desperation, she takes the job. Meanwhile, Joe tells Ellen that they need to find a way to continue to cut household expenses…. Well, you get the picture.

I think this is reality for at least a year after the ‘all clear.’

There’s never been a better time to catch up on reading. Russell’s book is available through Amazon. For those interested in market history, the pages hold invaluable insights.

For me, markets are always battlefields, but I’ve survived several conflicts.

Consider “Anatomy of The Bear,” part of your financial literary war chest.

Bull Market? No, The Bear Still Rules For Now (Full Report)

The “2020 SOCIALLY DISTANT INVESTMENT SUMMIT” is coming on Thursday, April 2nd.

Click the link below to receive an email with a special “invitation only” link when the summit goes “live.” (Current newsletter subscribers are already registered.)

Catch Up On What You Missed Last Week

NOTE: During these tumultuous times, we are unlocking our full newsletter to help you navigate the markets safely. Make sure you subscribe toRIAPRO.NET (Free 30-Day Trial) if you want to keep receiving the full report after the storm passes.

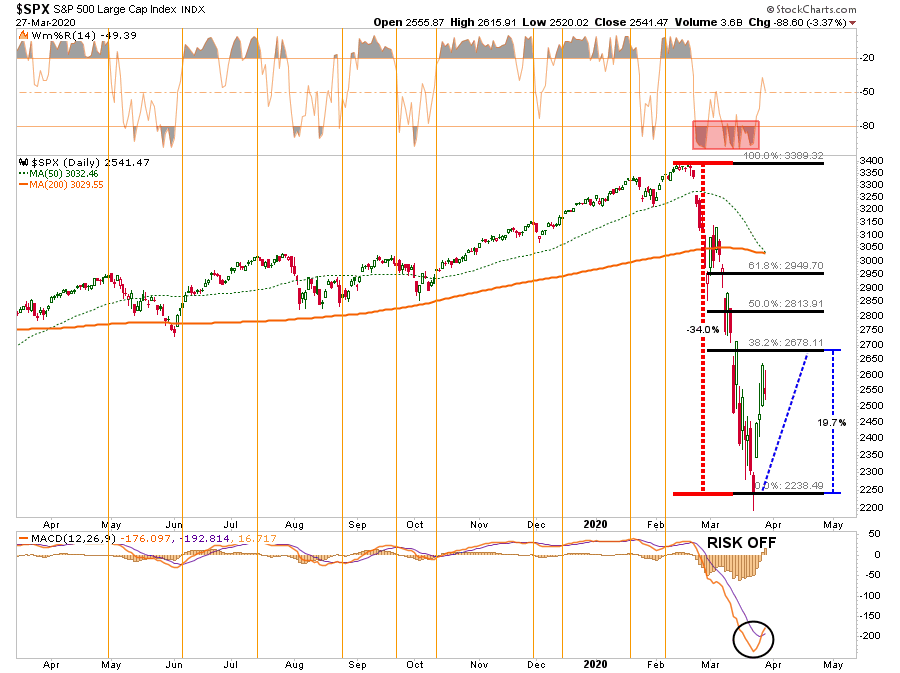

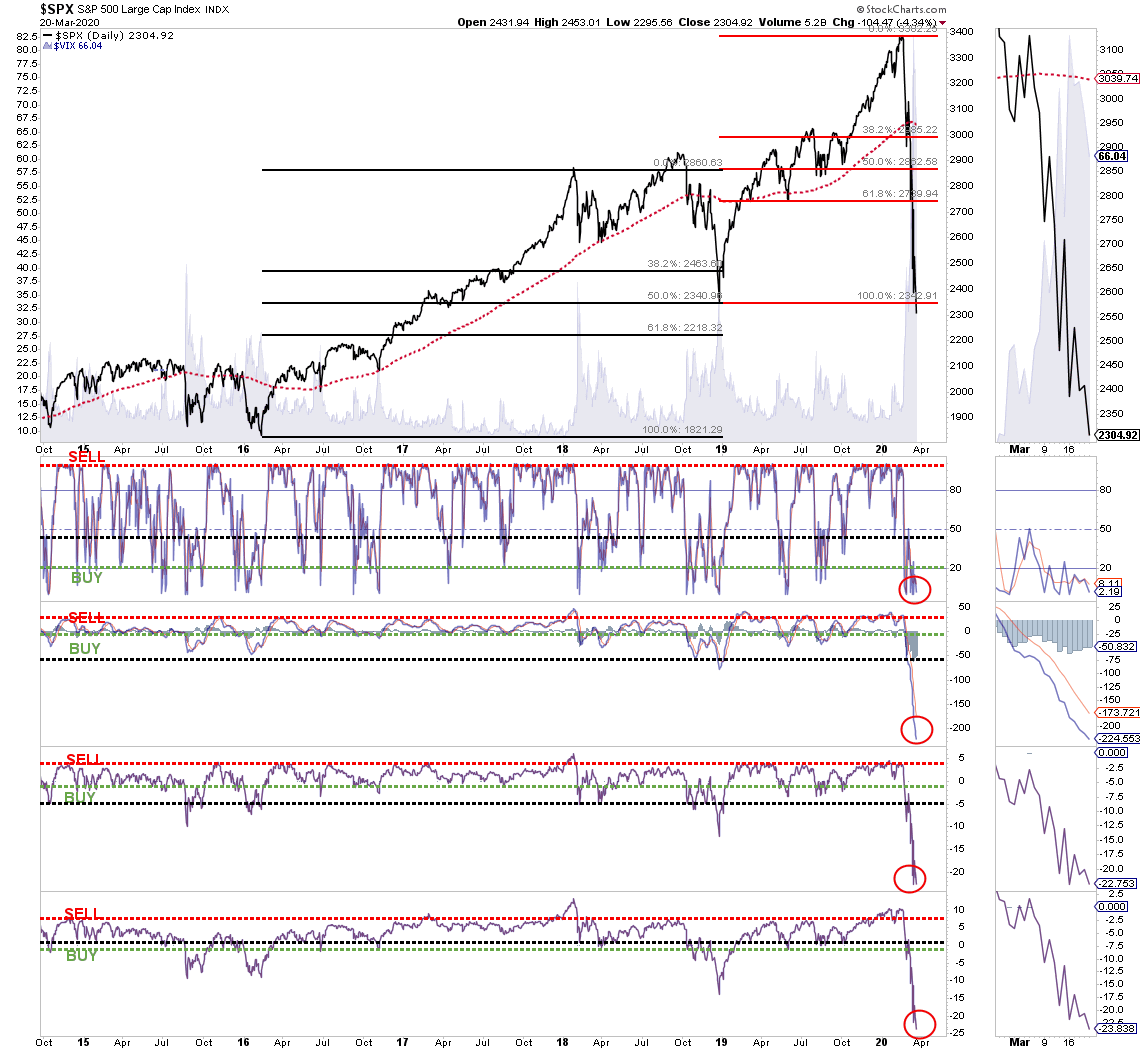

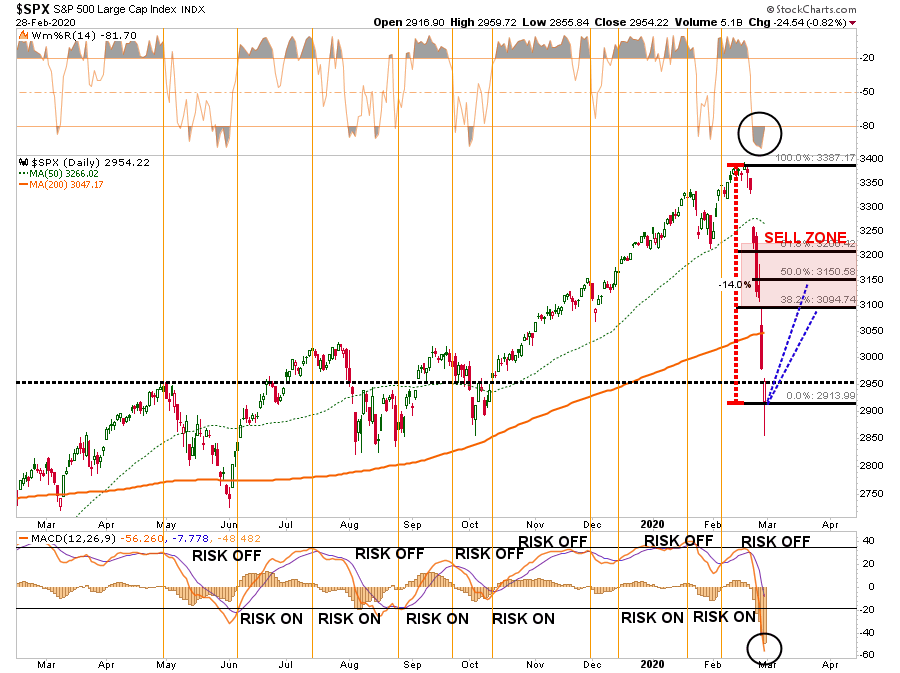

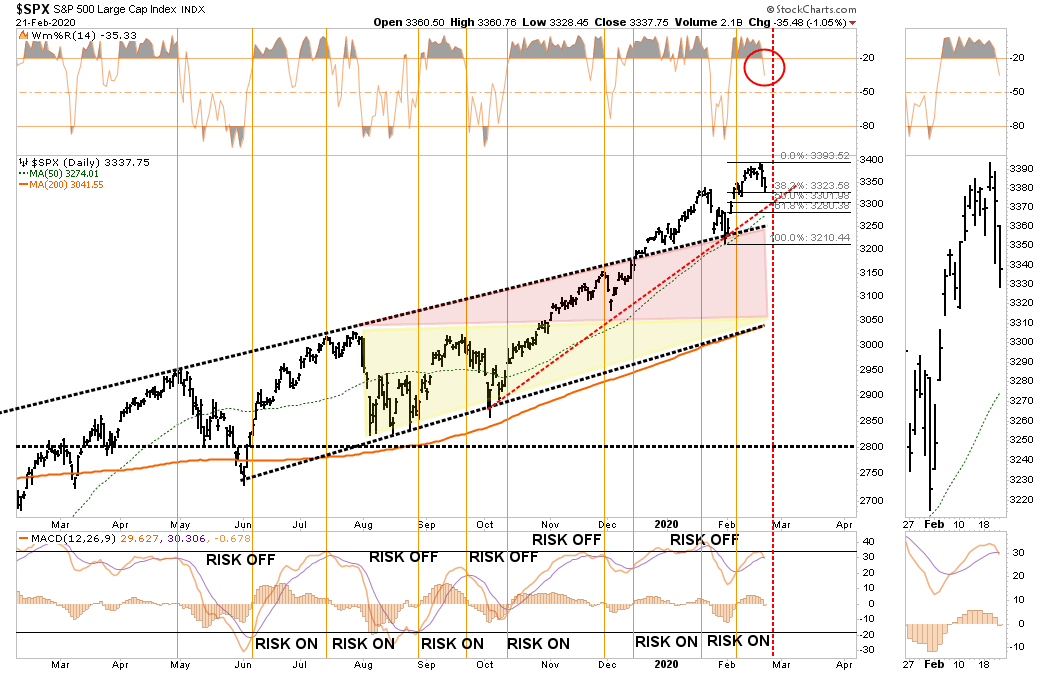

“From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance.

Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Chart Updated Through Friday

Not surprisingly, here were the headlines, almost exactly as we wrote them:

Well, you get the idea.

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. More importantly, “bear markets” only end when “NO ONE wants to buy it.”

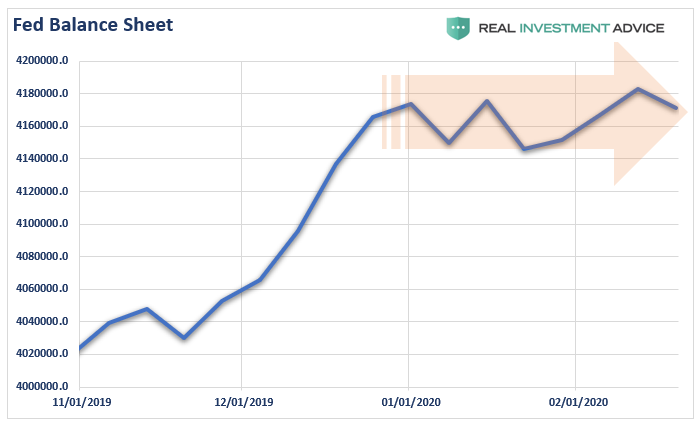

Fed Can’t Fix It

As noted above, the “bear market” will NOT be over until the credit market is fixed. We are a long way from that being done, given the blowout in yields currently occurring.

The Fed has cut rates by 150 basis points to near zero and run through its entire 2008 crisis handbook.

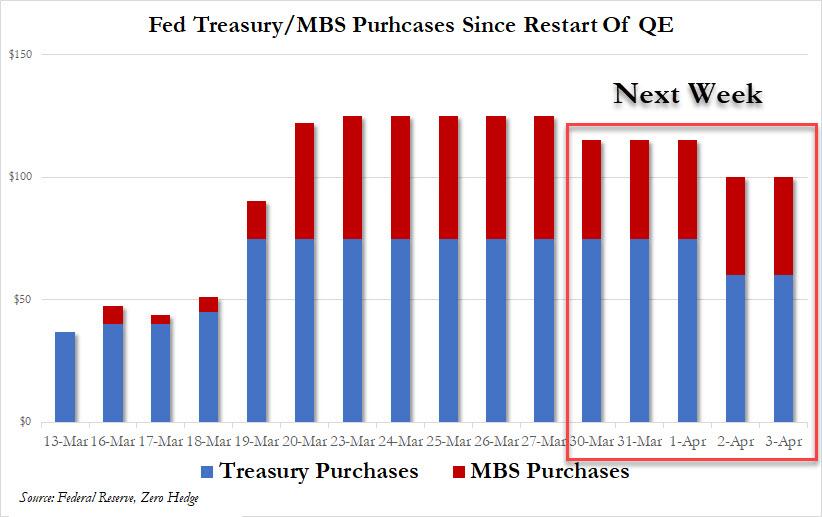

That wasn’t enough to calm markets, though — so the central bank also announced $1 trillion a day in repurchase agreements and unlimited quantitative easing, which includes a hard-to-understand $625 billion of bond-buying a week going forward. At this rate, the Fed will own two-thirds of the Treasury market in a year.

But it’s the alphabet soup of new programs that deserve special consideration, as they could have profound long-term consequences for the functioning of the Fed and the allocation of capital in financial markets. Specifically, these are:

CPFF (Commercial Paper Funding Facility) – buying commercial paper from the issuer.

PMCCF (Primary Market Corporate Credit Facility) – buying corporate bonds from the issuer.

SMCCF (Secondary Market Corporate Credit Facility) – buying corporate bonds and bond ETFs in the secondary market.

MSBLP (Main Street Business Lending Program) – Details are to come, but it will lend to eligible small and medium-sized businesses, complementing efforts by the Small Business Association.

To put it bluntly, the Fed isn’t allowed to do any of this.”

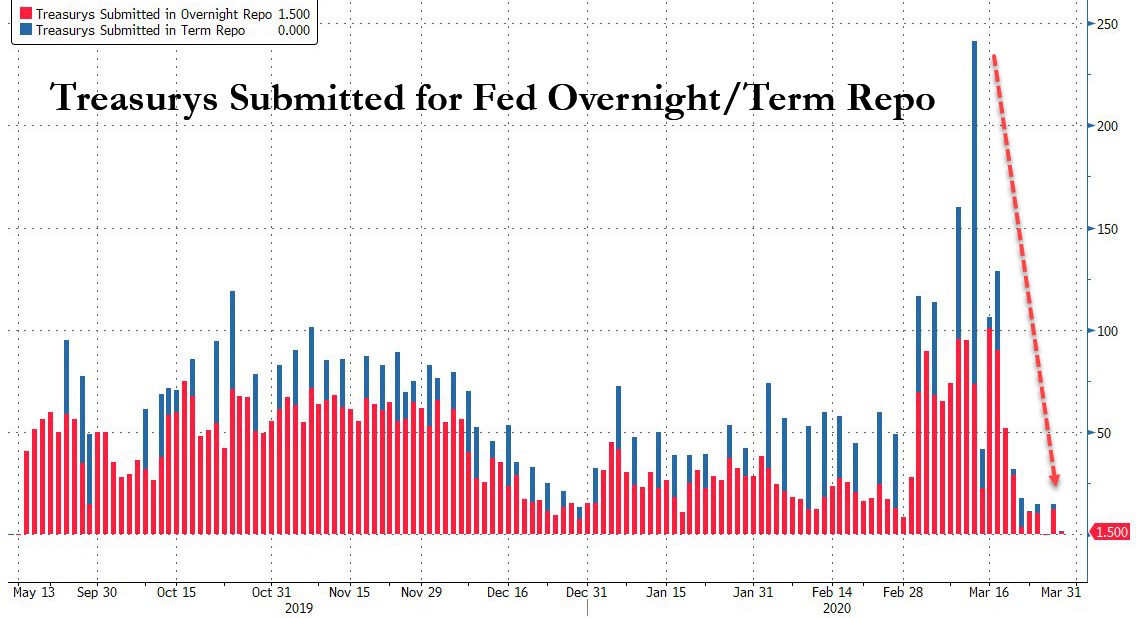

However, on Friday, the Federal Reserve ran into a problem, which could poses a risk for the markets going forward. As Jim noted, the mind-boggling pace of bond purchases quickly hit the limits of what was available to pledge for collateral.

Or rather, the Fed’s “unlimited QE,” may not be so “unlimited” after all.

The consequence is the Fed is already having to start cutting back on its QE program. That news fueled the late-day sell-off Friday afternoon. (Charts courtesy of Zerohedge)

While Congress did pass the “CARES” act on Friday, it will do little to backstop what is about to happen to the economy for two primary reasons:

The package will only support the economy for up to two months. Unfortunately, there is no framework for effective and timely deployment; firms are already struggling to pay rents, there are pockets of funding stress in credit markets as default risks build, and earnings guidance is abandoned.

The unprecedented uncertainty facing financial markets on the duration of social distancing, the depth of the economic shock and when the infection rate curve will flatten, and there are many unknowns which will further undermine confidence.

Both of these points are addressed in this week’s Macroview but here are the two salient points to support my statement:

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance, can be provided. This will lead to higher and longer-duration of, unemployment.”

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any type of disruption to their income going into the recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits leads to higher unemployment and lower asset prices until the cycle is complete.

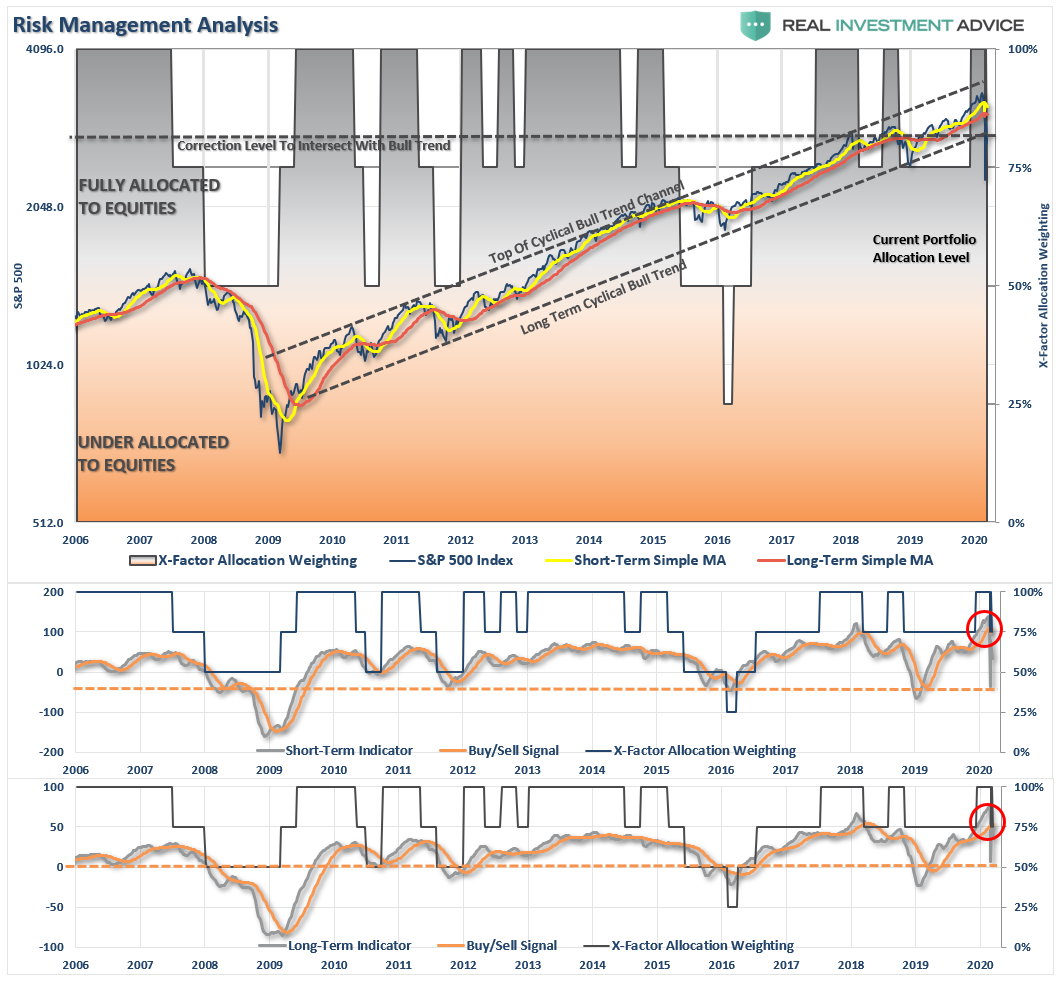

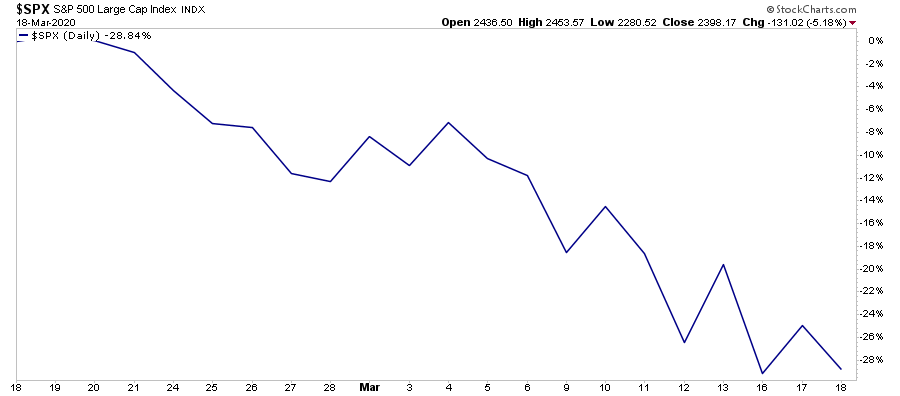

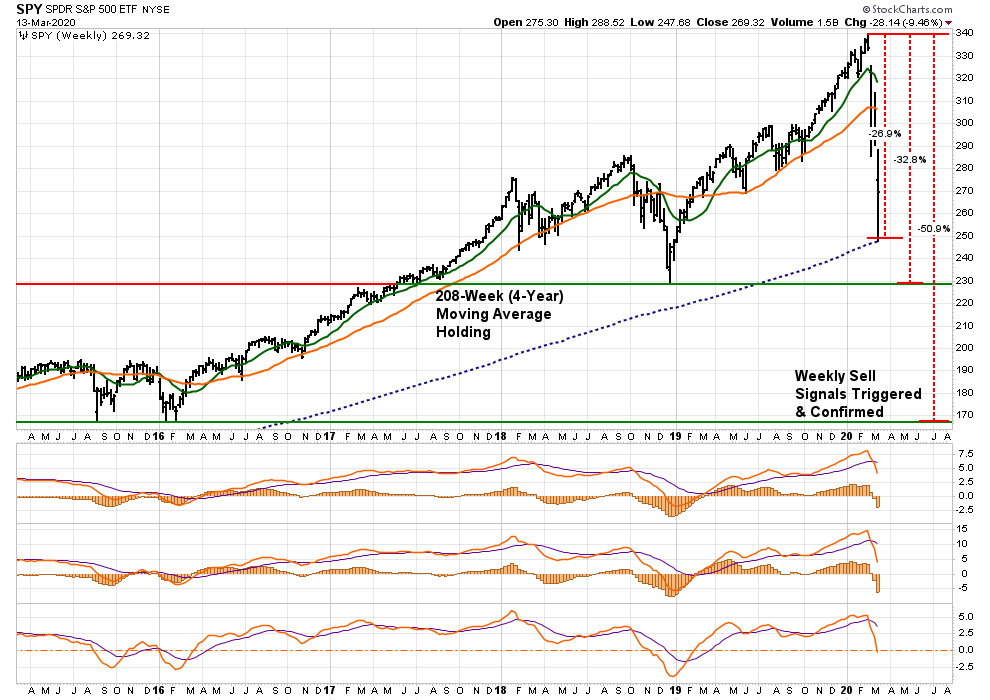

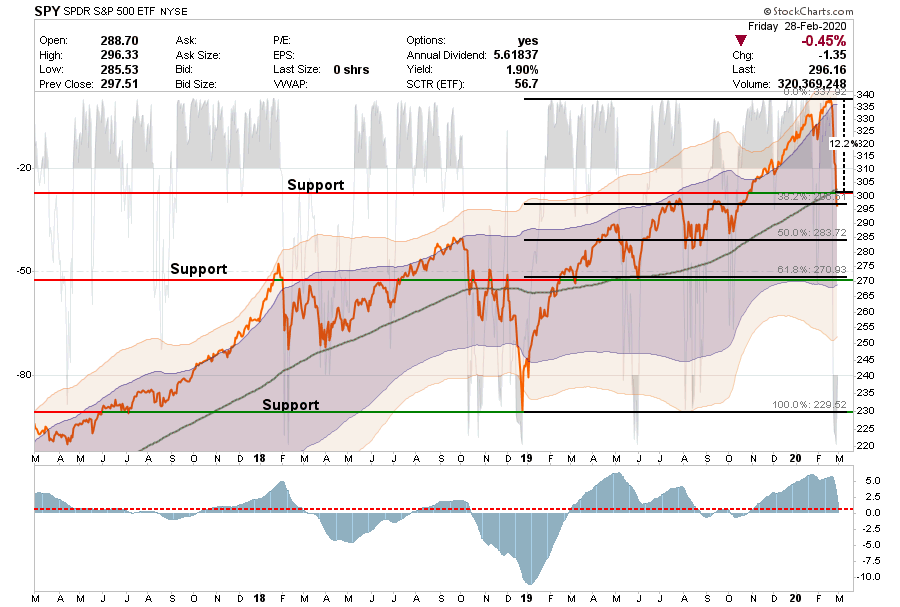

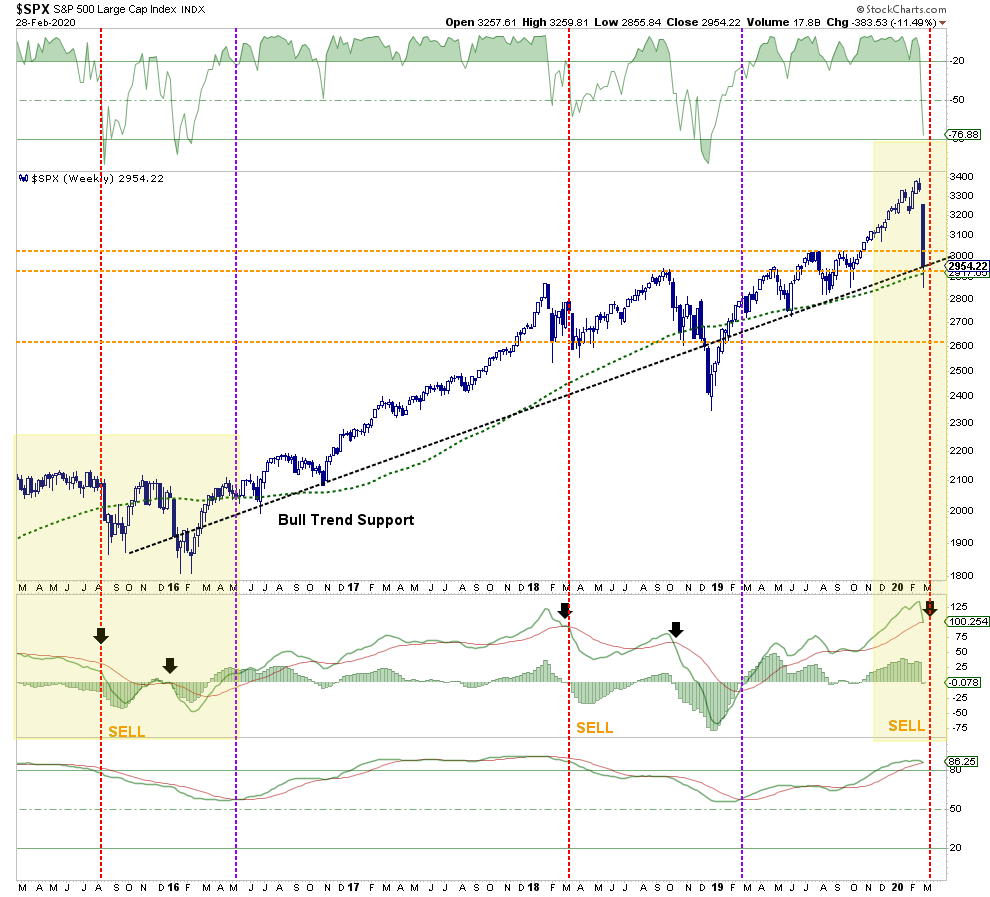

The long term bull pattern that existed since the 3/9/09 is over. That means the pattern of investors confidently buying every decline is over.

The market became historically oversold on 3/23 using many metrics, and that oversold condition coincided with the long term support area of S&P 500 2110-2180.

The short-covering and rebalancing had a lot to do with the size and speed of the 3-day rally. Also, we know the lack of ETF liquidity played a huge role as well as algorithmic trading.

Technically the market can still go up 6.9% higher from here to hit the 50% retracement level (3386 – 2237 = 1149/2 = 574 + 2237 = 2811….2811/2630 = +6.9%.) I would not bet on it.

The market only sustains a rally once there is light at the Coronavirus tunnel.

I do not think the S&P 500 will hit a new high this year. Maybe not in 2021, either.

His analysis agrees with our own, which we discussed with you last week.

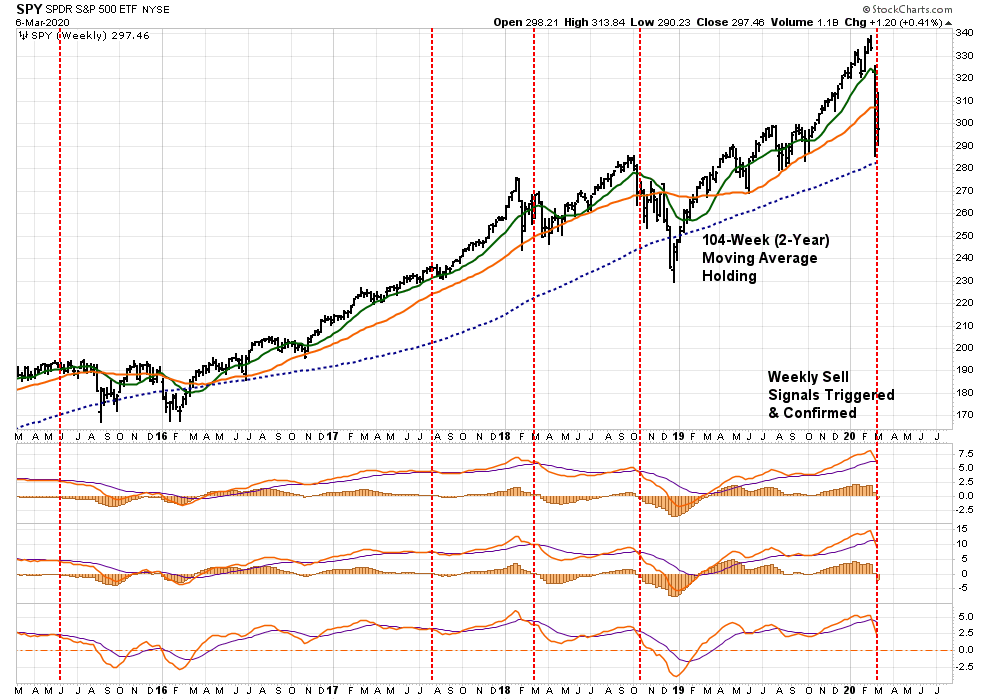

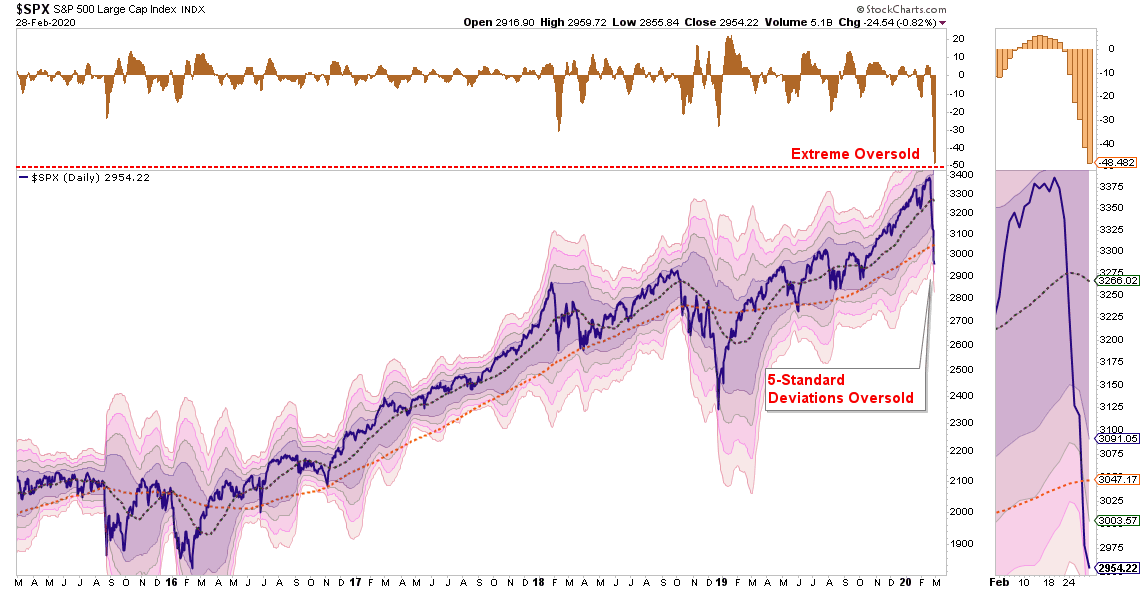

“The good news is the markets are now more extremely oversold on a variety of measures than at just about any other point in history.

Warning: Any reversal will NOT BE the bear market bottom. It will be a ‘bear market’ rally you will want to ‘sell’ into. The reason is there are still many investors trapped in ‘buy and hold’ and ‘passive indexing’ strategies that are actively seeking an exit. Any rallies will be met with redemptions.

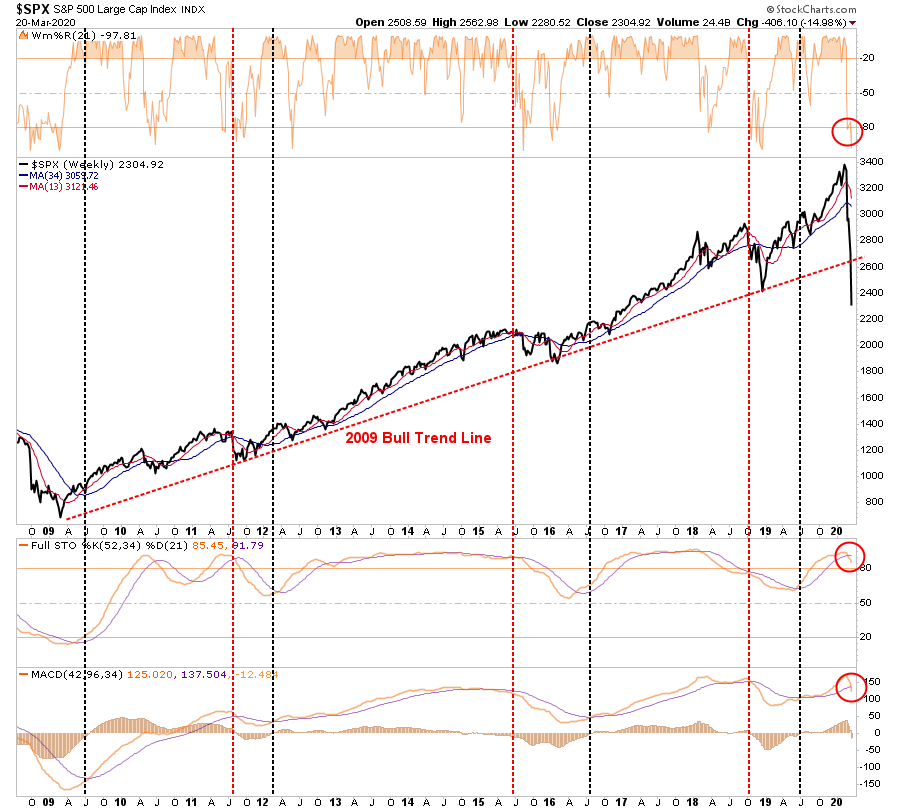

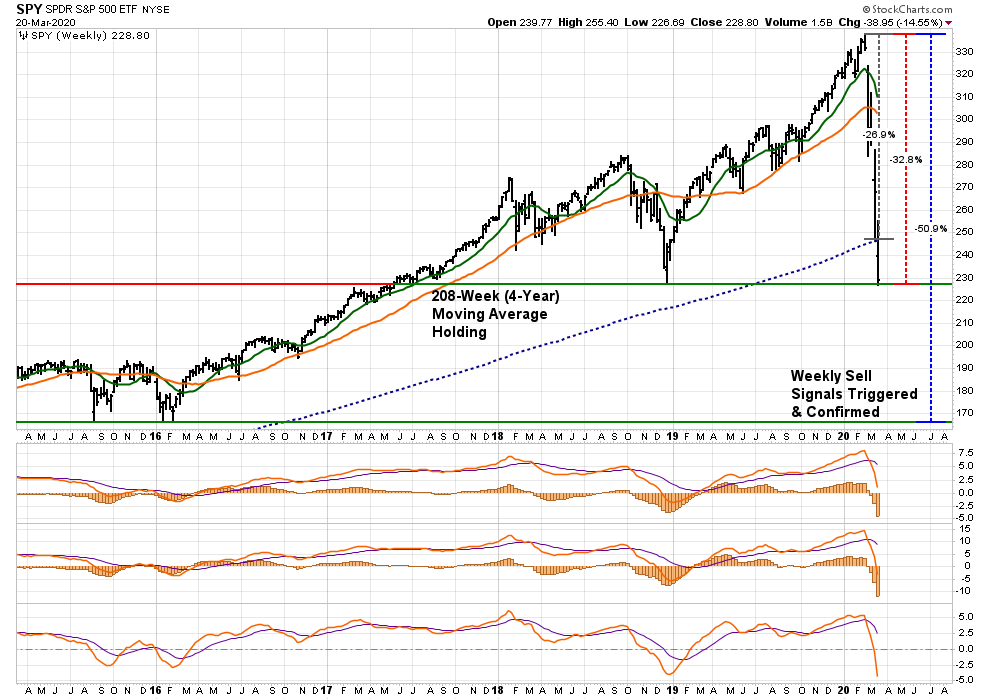

Most importantly, all of our long-term weekly ‘sell signals’ have now been triggered. Such would suggest that a rally back to the ‘bullish trend line’ from 2009 will likely be the best opportunity to ‘sell’ before the ‘bear market’ finds its final low.”

Last week’s chart updated through Friday’s close.

While the recent lows may indeed turn out to be “the bottom,” I highly suspect they won’t. Given the sell signals have been registered at such high levels, the time, and distance, needed to reverse the excesses will require a deeper market draw.

As Jeff Hirsch from Stocktrader’s Alamanc noted:

“While we are all rooting for the market to find support here so much damage has been done. A great deal of uncertainty remains for the economy and health crisis. This looks like a bear market bounce.

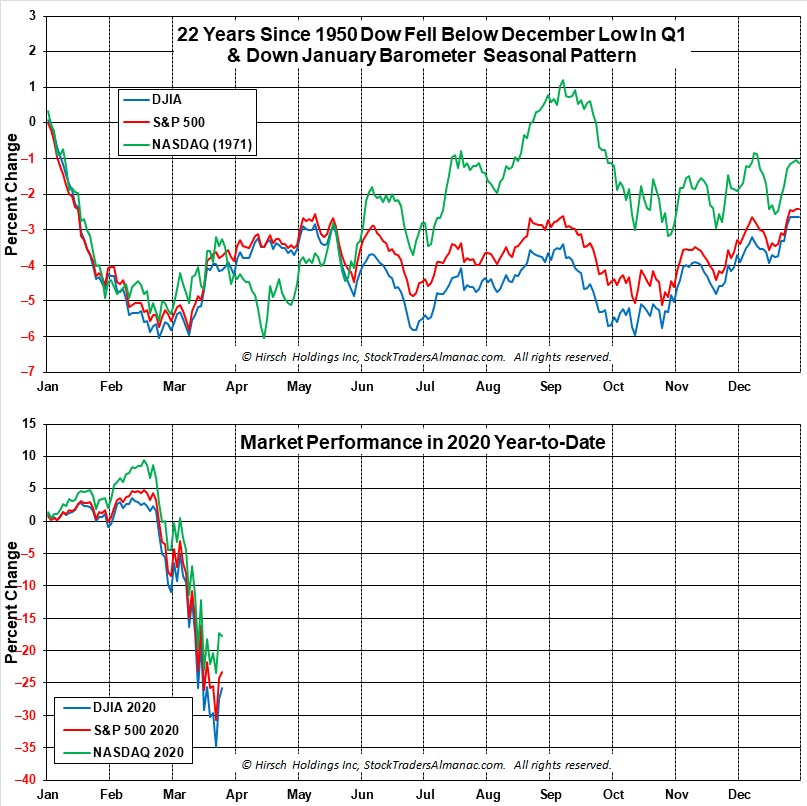

History suggests that we are in for some tough sledding in the market this year with quite a bit of chop. When the January Barometer came in with a negative reading, our outlook for 2020 began to diminish as every down January since 1950 has been followed by a new or continuing bear market, a 10% correction, or a flat year. Then another warning sign flashed when DJIA closed below its December closing low on February 26, 2020 as the impact of this novel coronavirus began to take its toll on Wall Street.

In the March Outlook, we presented this graph of the composite seasonal pattern for the 22 years since 1950 when both the January Barometer as measured by the S&P 500 were down, and the Dow closed below its previous December closing low in the first quarter. Below is a graph of DJIA, S&P 500 and NASDAQ Composite for 2020 year-to-date as of the close on March 25. Comparing 2020 market action to these 22 years, suggests a choppy year ahead with the potential for several tests of the recent low.”

“The depth of this waterfall decline may be too deep for the market to rebound quickly. This bear market also put this year’s Best Six Months (November-April) at risk of being negative. The record of down Best Six Months is not encouraging and it reminds us of a salient quote from the Almanac from an old market sage,

‘If the market does not rally, as it should during bullish seasonal periods, it is a sign that other forces are stronger and that when the seasonal period ends those forces will really have their say.’— Edson Gould (Stock market analyst, Findings & Forecasts, 1902-1987)'”

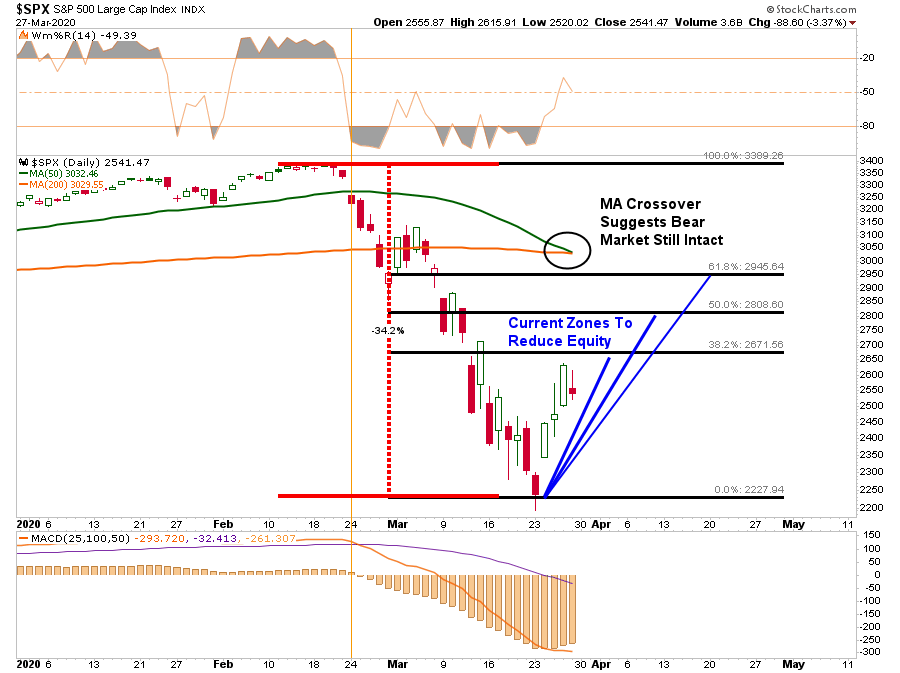

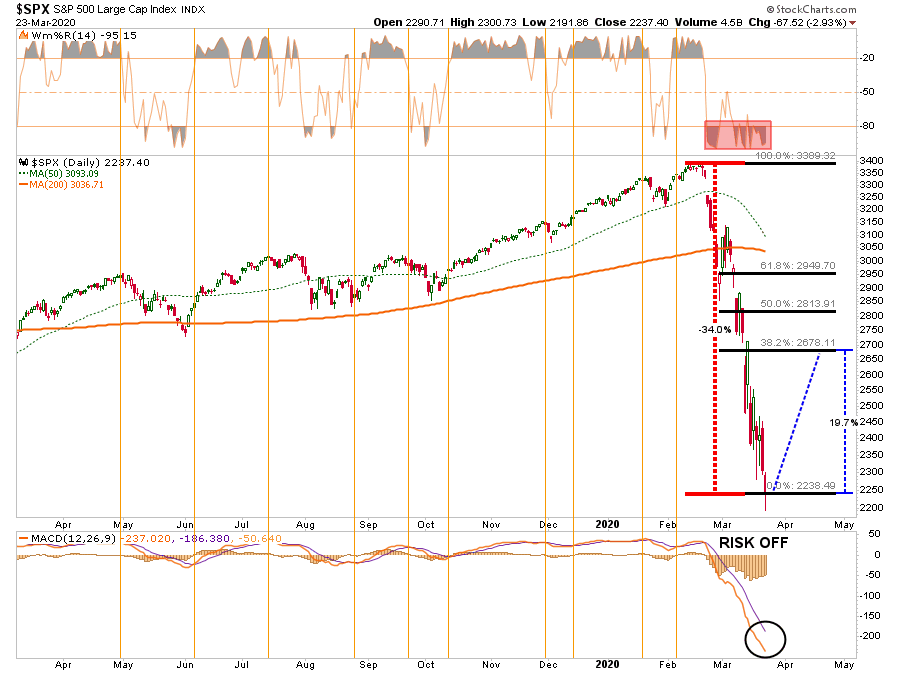

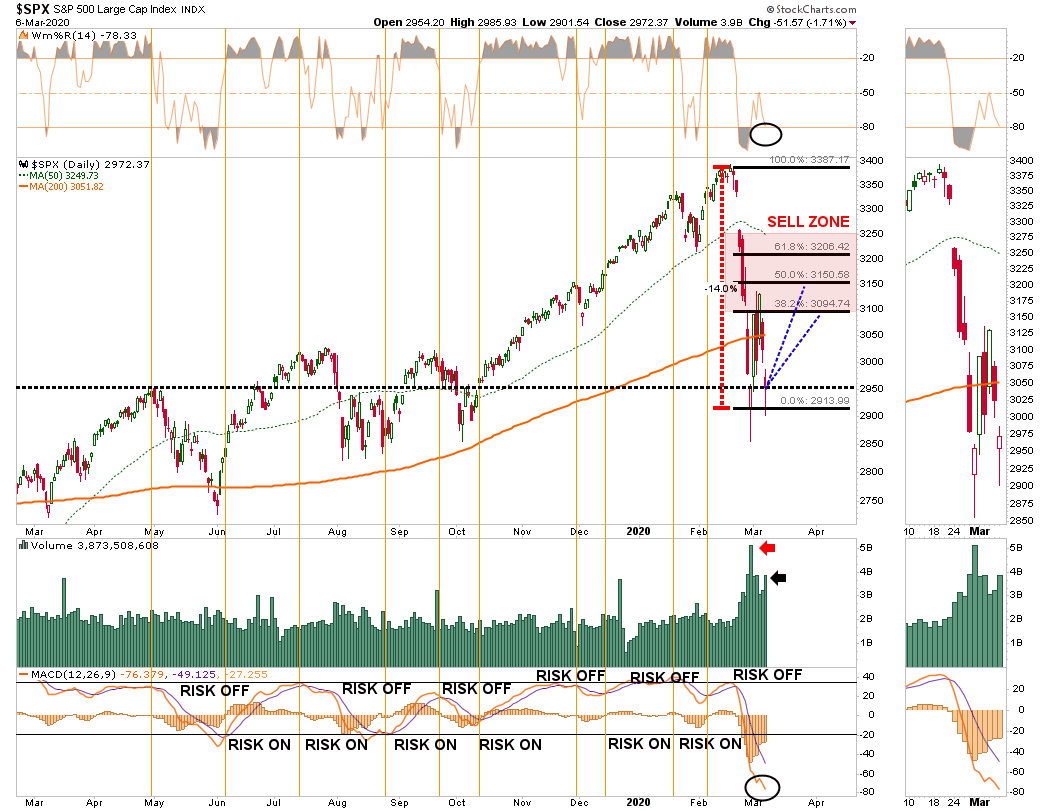

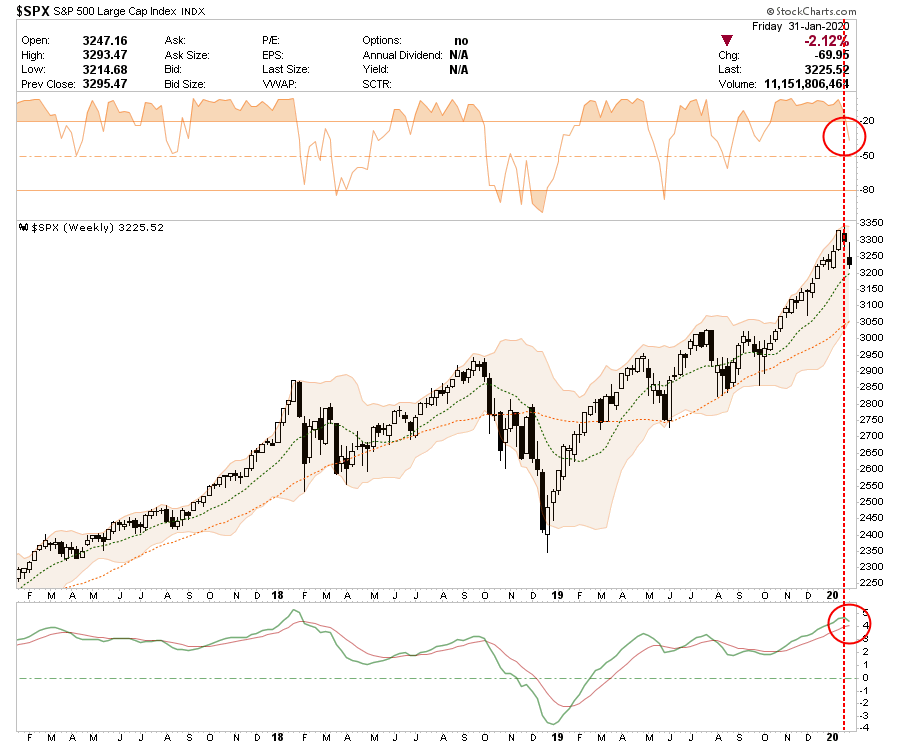

On a short-term basis, the market is also suggesting some risk. The daily chart below shows the market rallied to, and failed at, the first level of the Fibonacci retracement we outlined last week, suggesting profits be taken at this level. While there are two remaining targets for the bear market rally, the probabilities weigh heavily against them. (This doesn’t mean they can’t be achieved, it is “possible,” just not “probable.”)

Furthermore, with the “Death Cross” triggering on Friday (the 50-dma crossing below the 200-dma), this will put further downside pressure on any “bear market” advance from current levels.

Given the magnitude, and multiple confirmations, of these signals, it is far too soon to assume the “bear market” is over. This is particularly the case, given the sell-off is less than one-month-old.

Bear markets, and recessions, tend to last 18-months on average.

The current bear market and recession are not the results of just the “coronavirus” shock. It is the result of many simultaneous shocks from:

Economic disruption

Surging unemployment

Oil price shock

Collapsing consumer confidence, and

Most importantly, a “credit event.”

We likely have more to go before we can safely assume we have turned the corner.

In the meantime, use rallies to raise cash. Don’t worry about trying to “buy the bottom.”There will be plenty of time to see “THE” bottom is in, and having cash will allow you to “buy stocks” from the last of the “weak hands.”

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

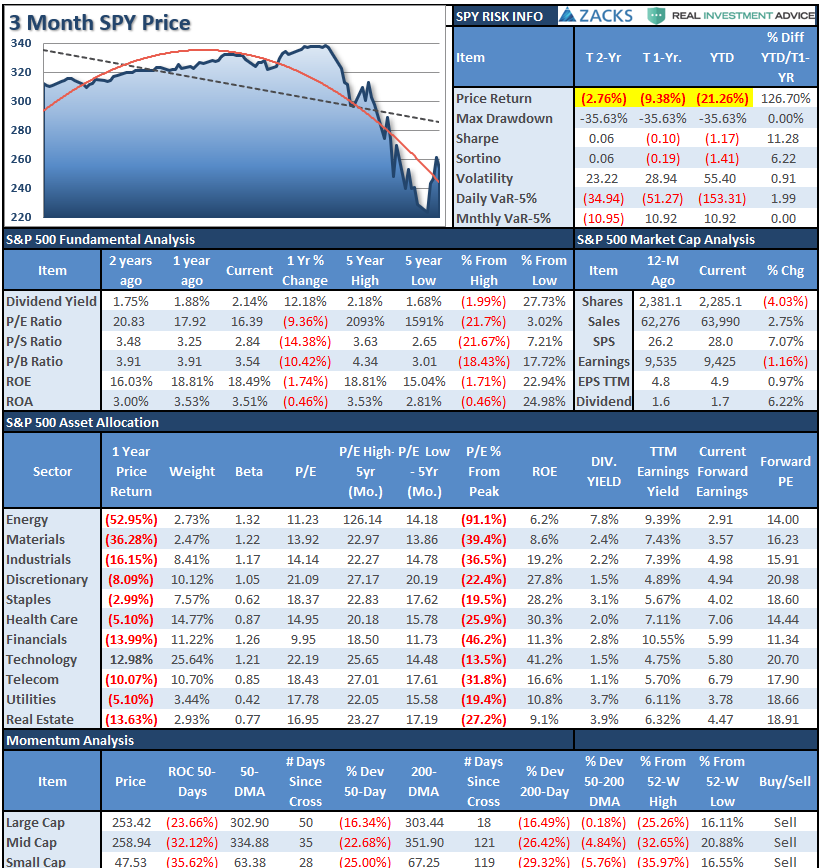

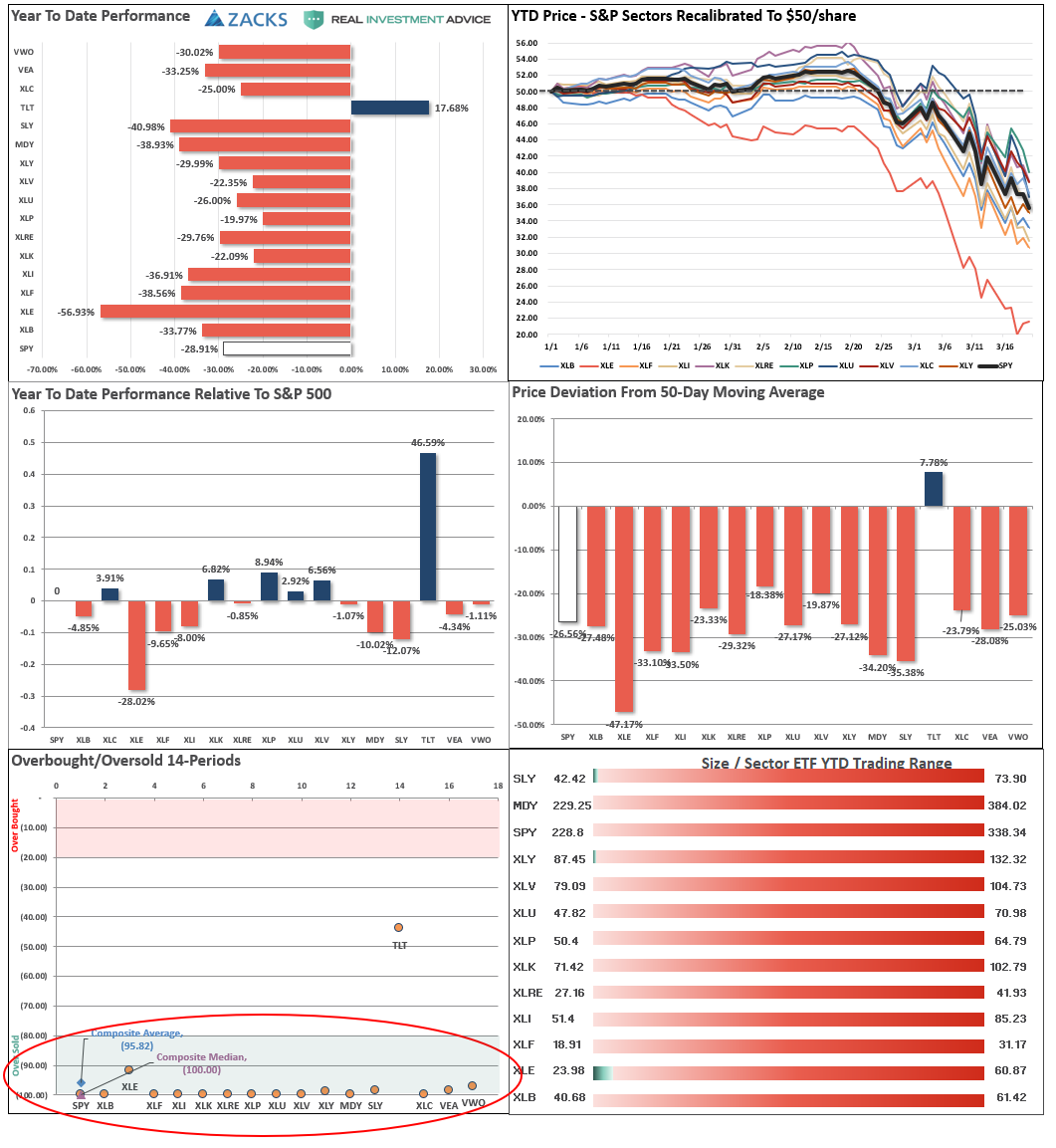

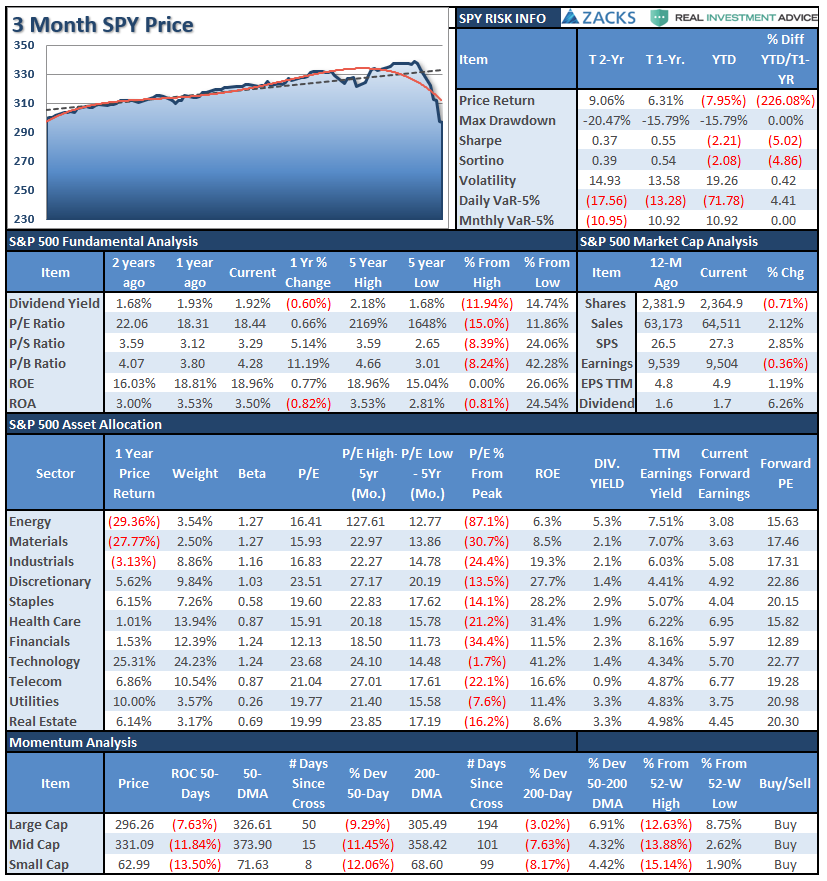

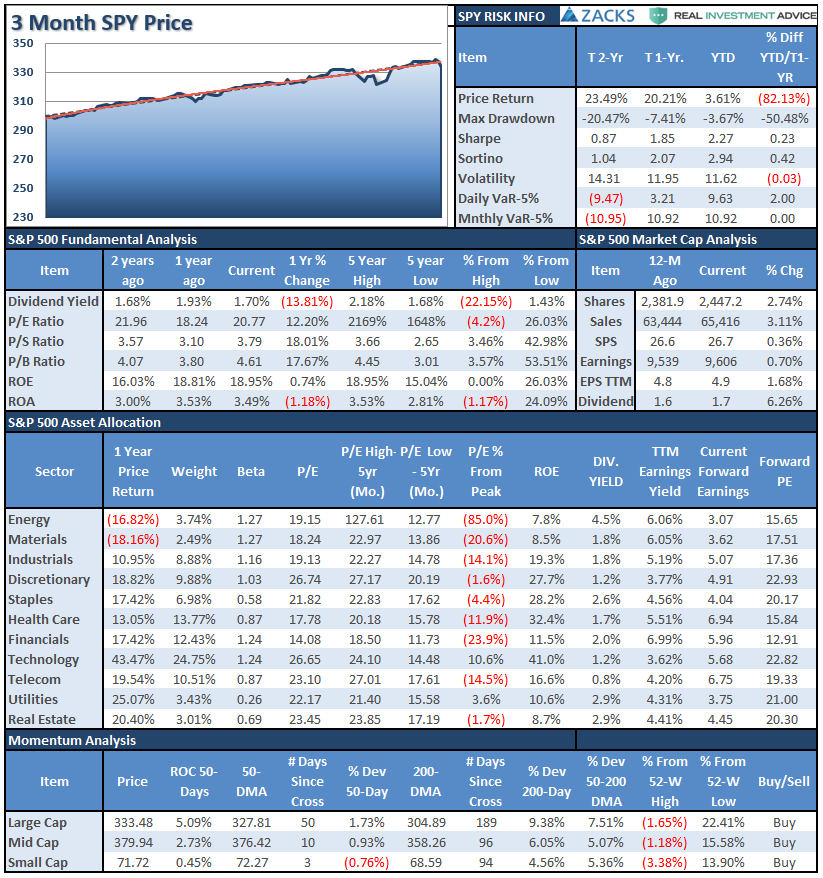

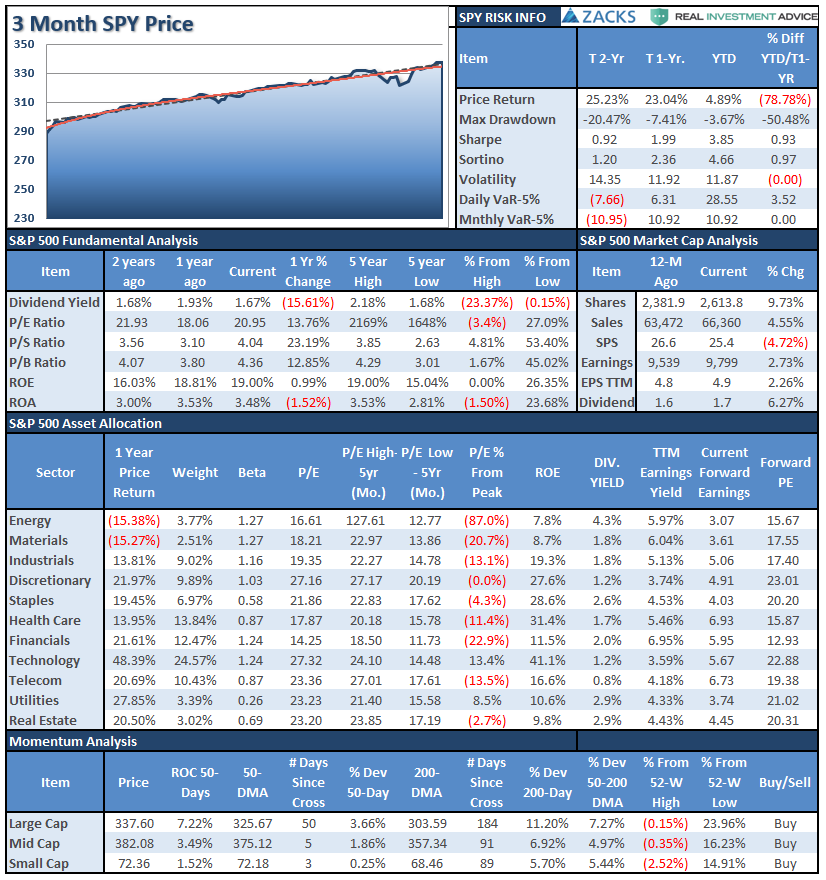

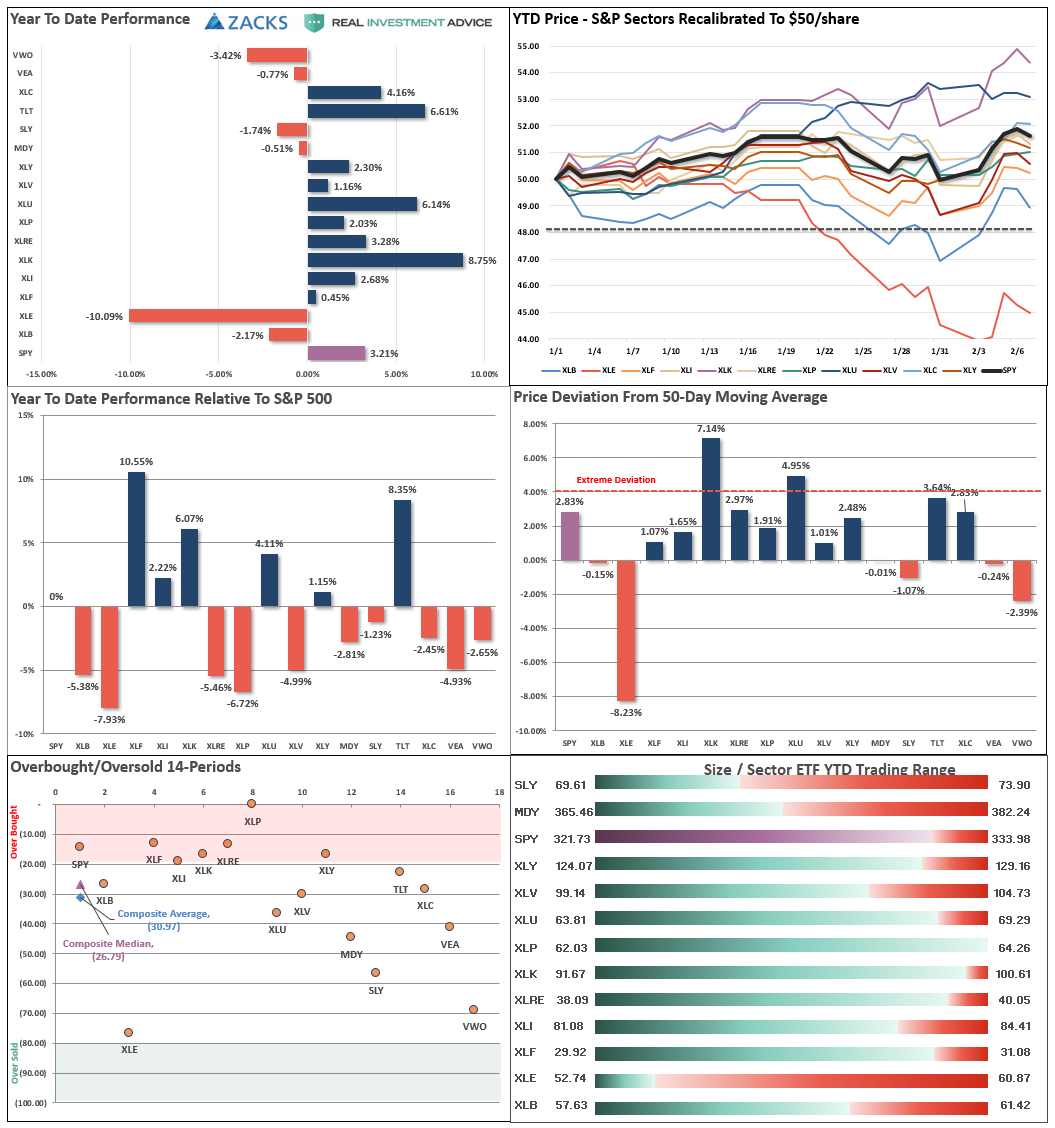

S&P 500 Tear Sheet

Performance Analysis

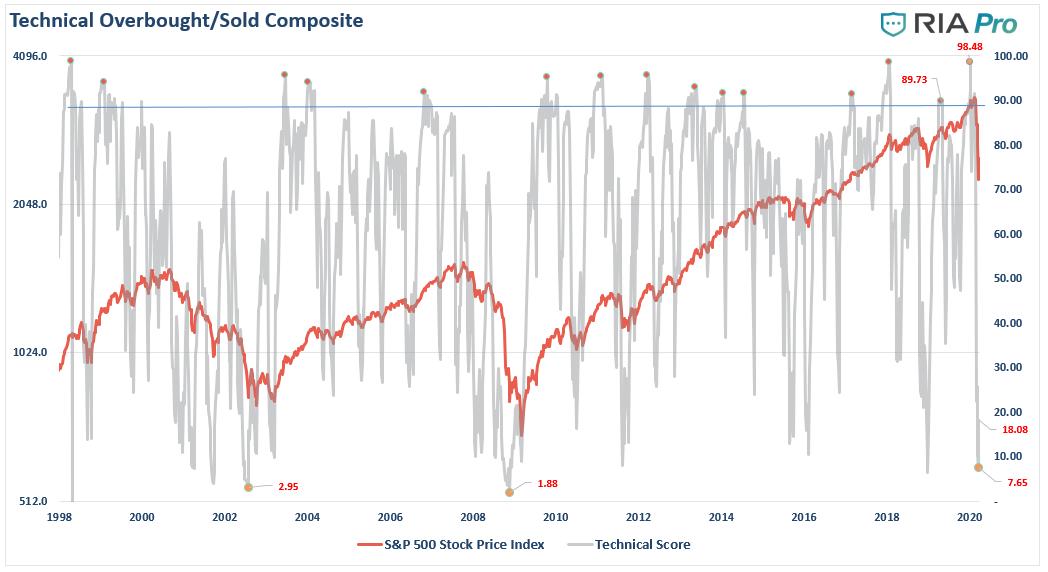

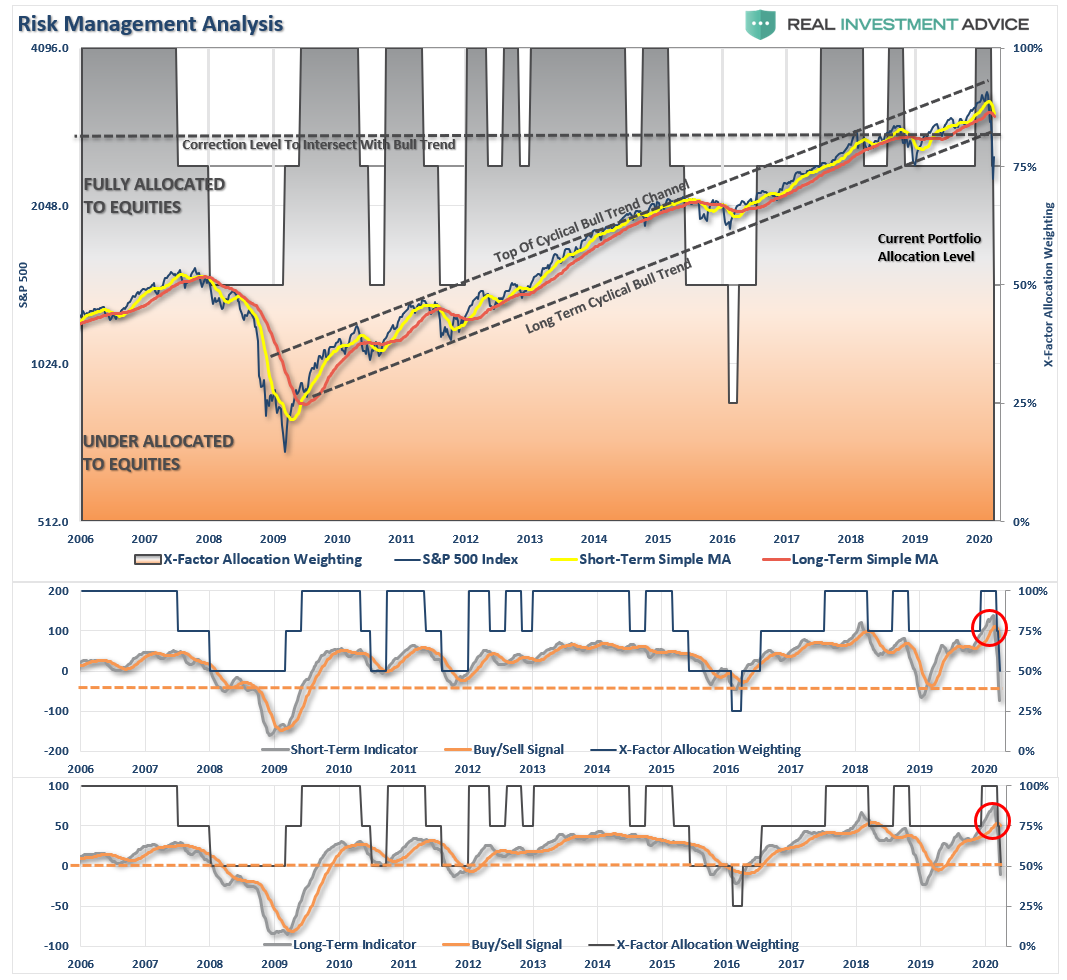

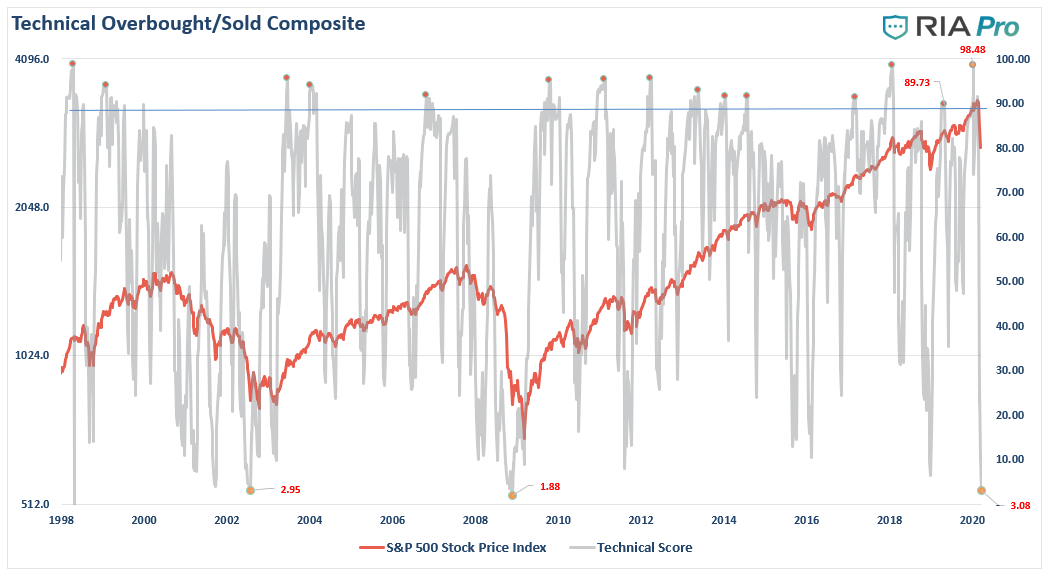

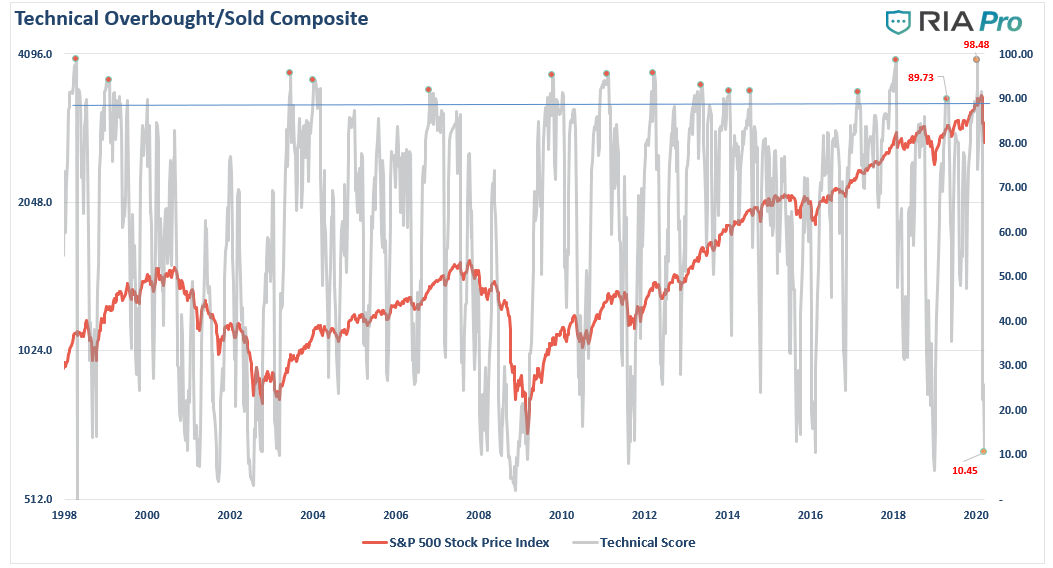

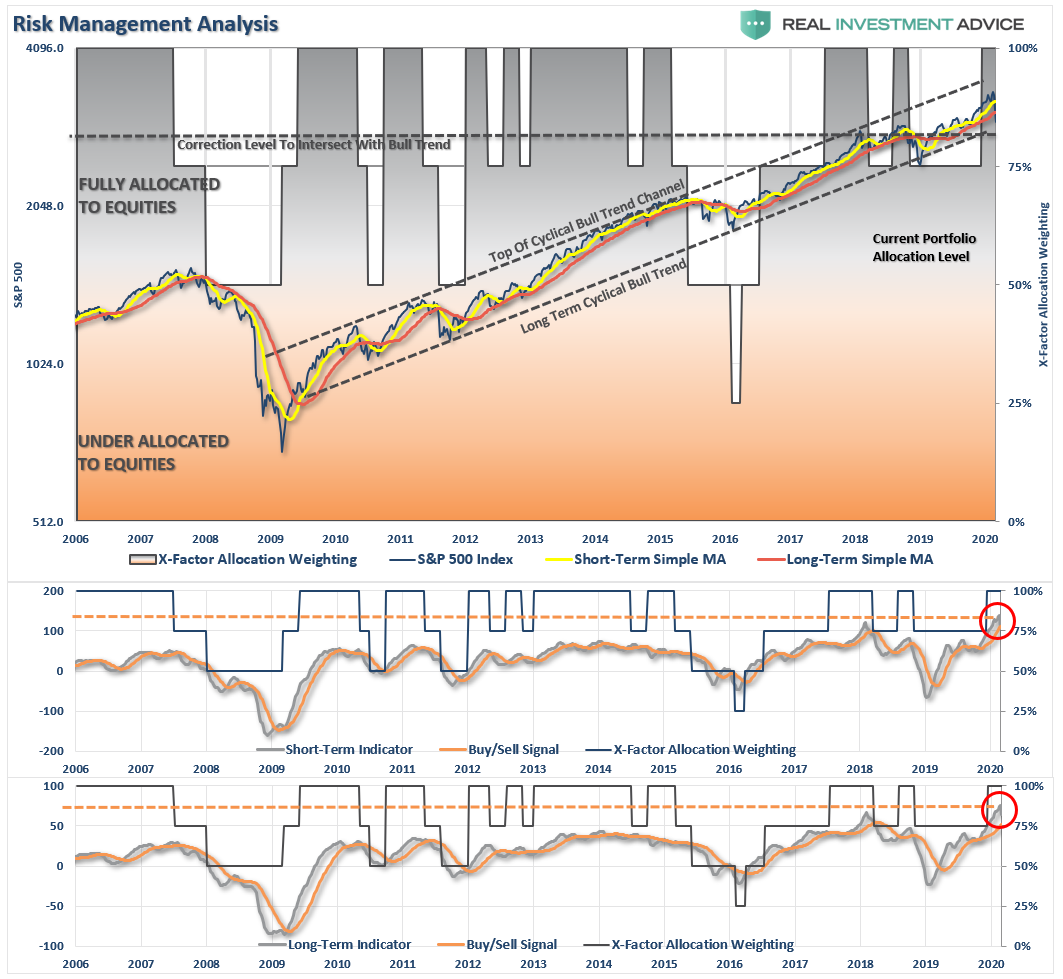

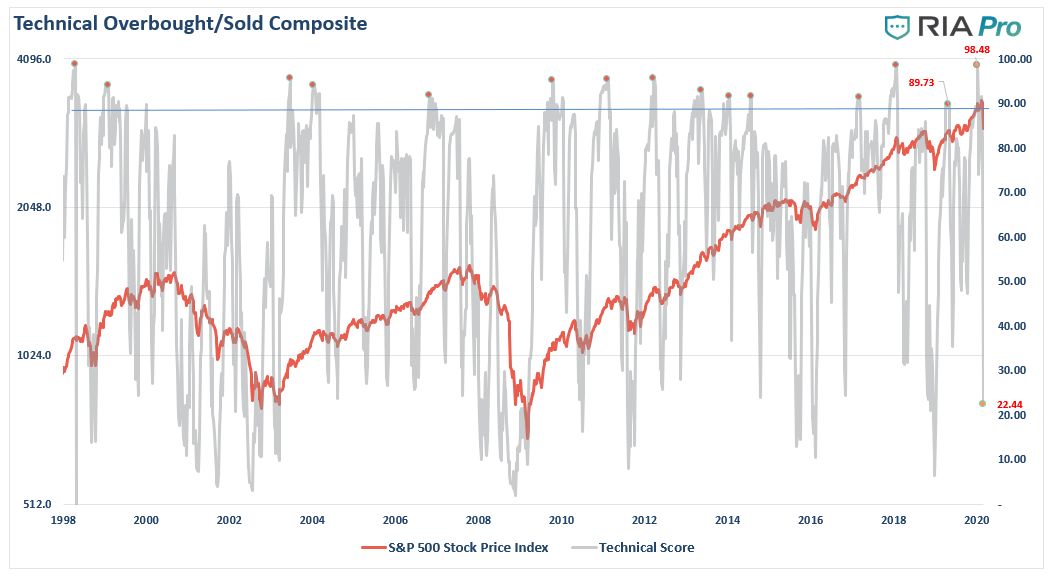

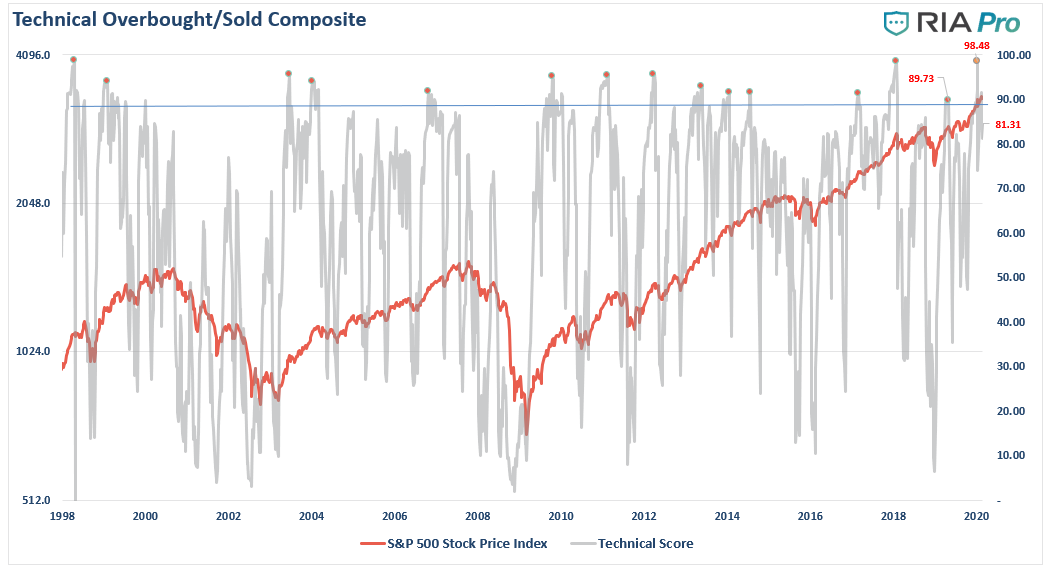

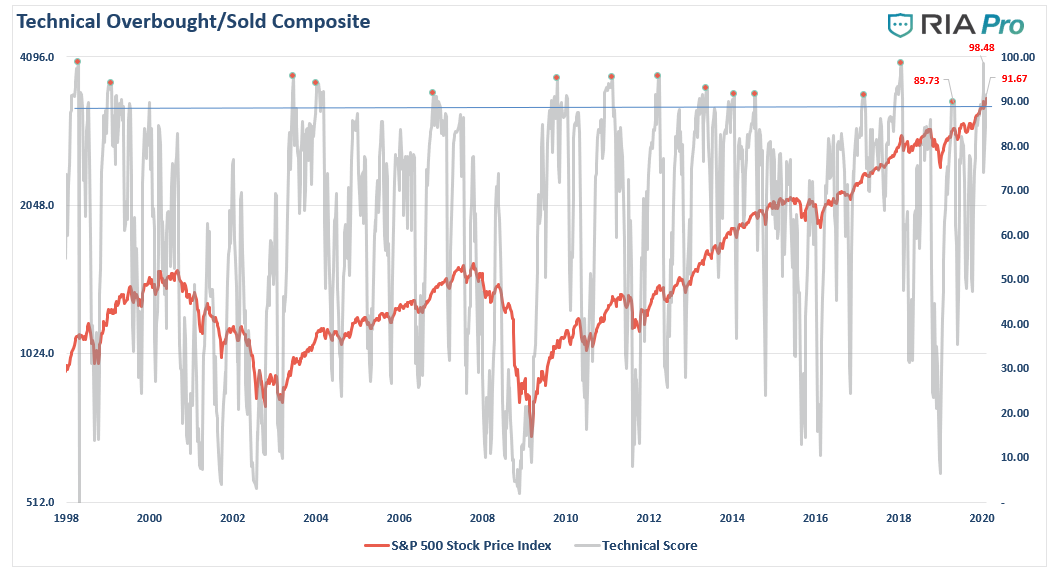

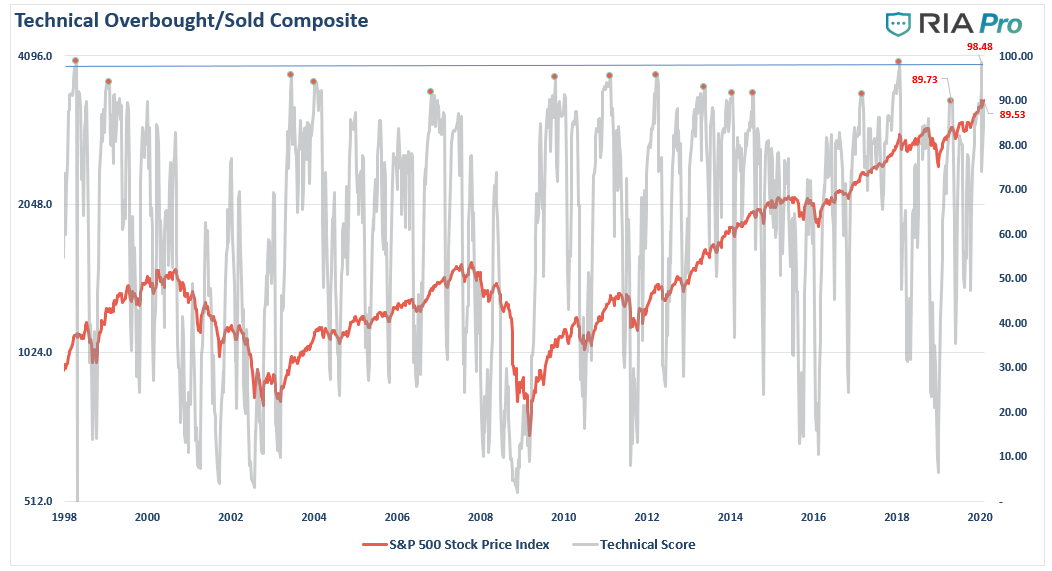

Technical Composite

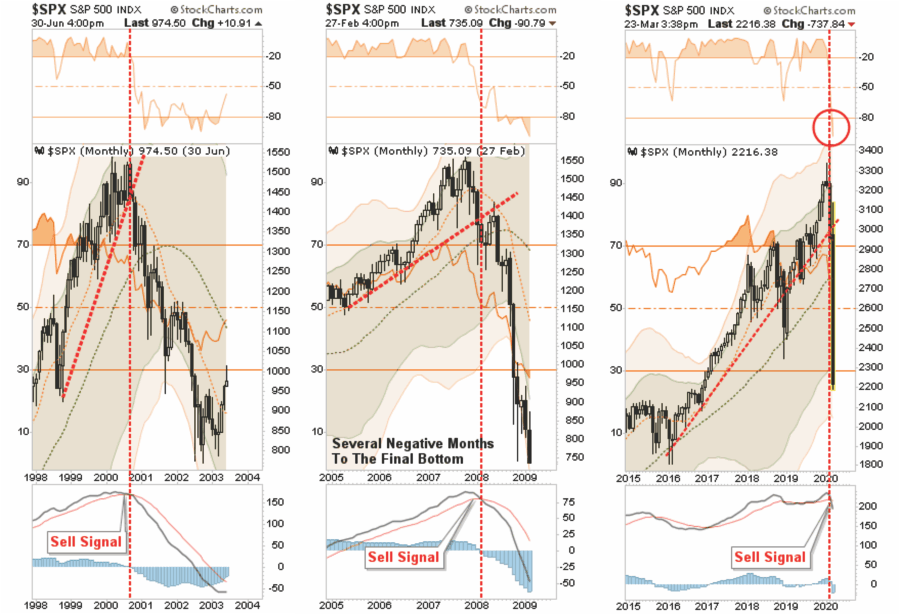

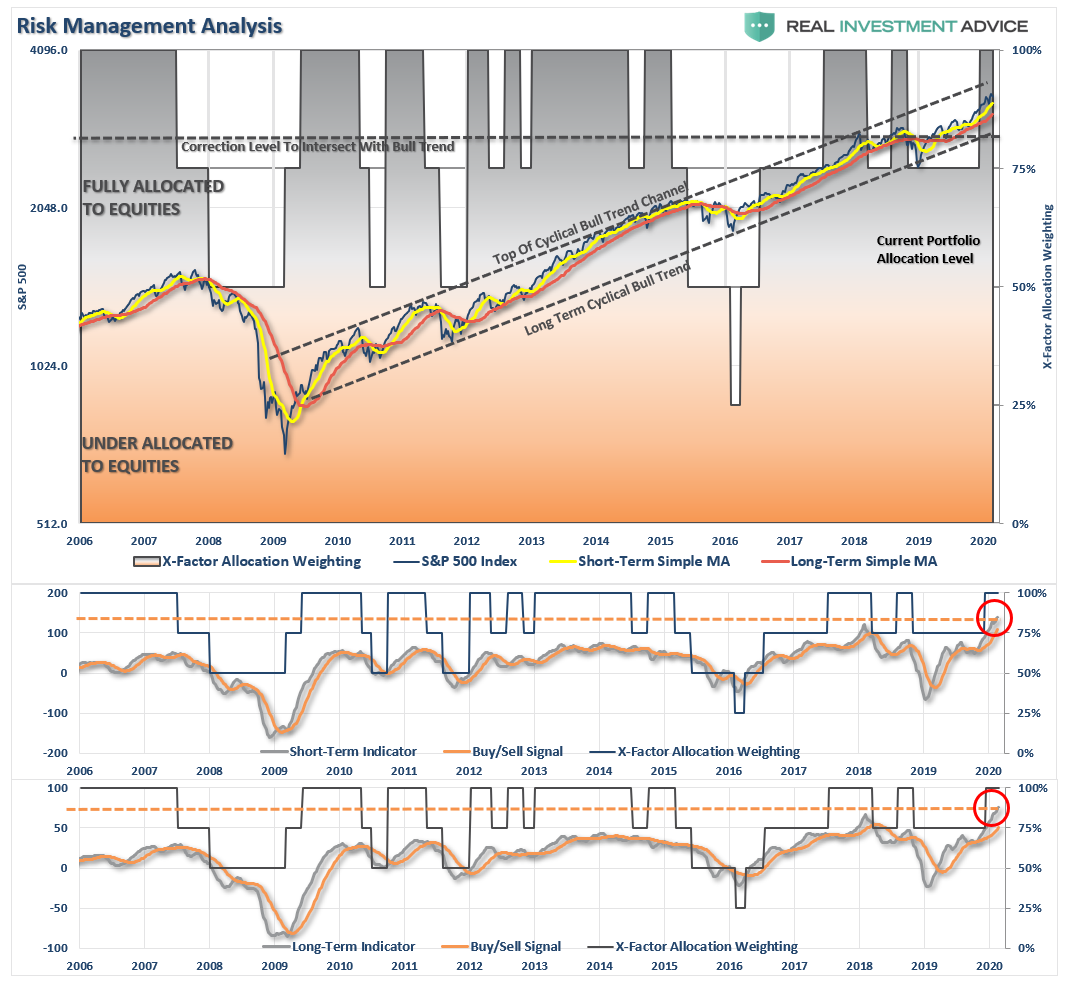

Note: The technical gauge bounced from the lowest level since both the “Dot.com” and “Financial Crisis.” However, note the gauge bottoms BEFORE the market bottoms. In 2002, lows were retested. In 2008, there was an additional 22% decline in early 2009.

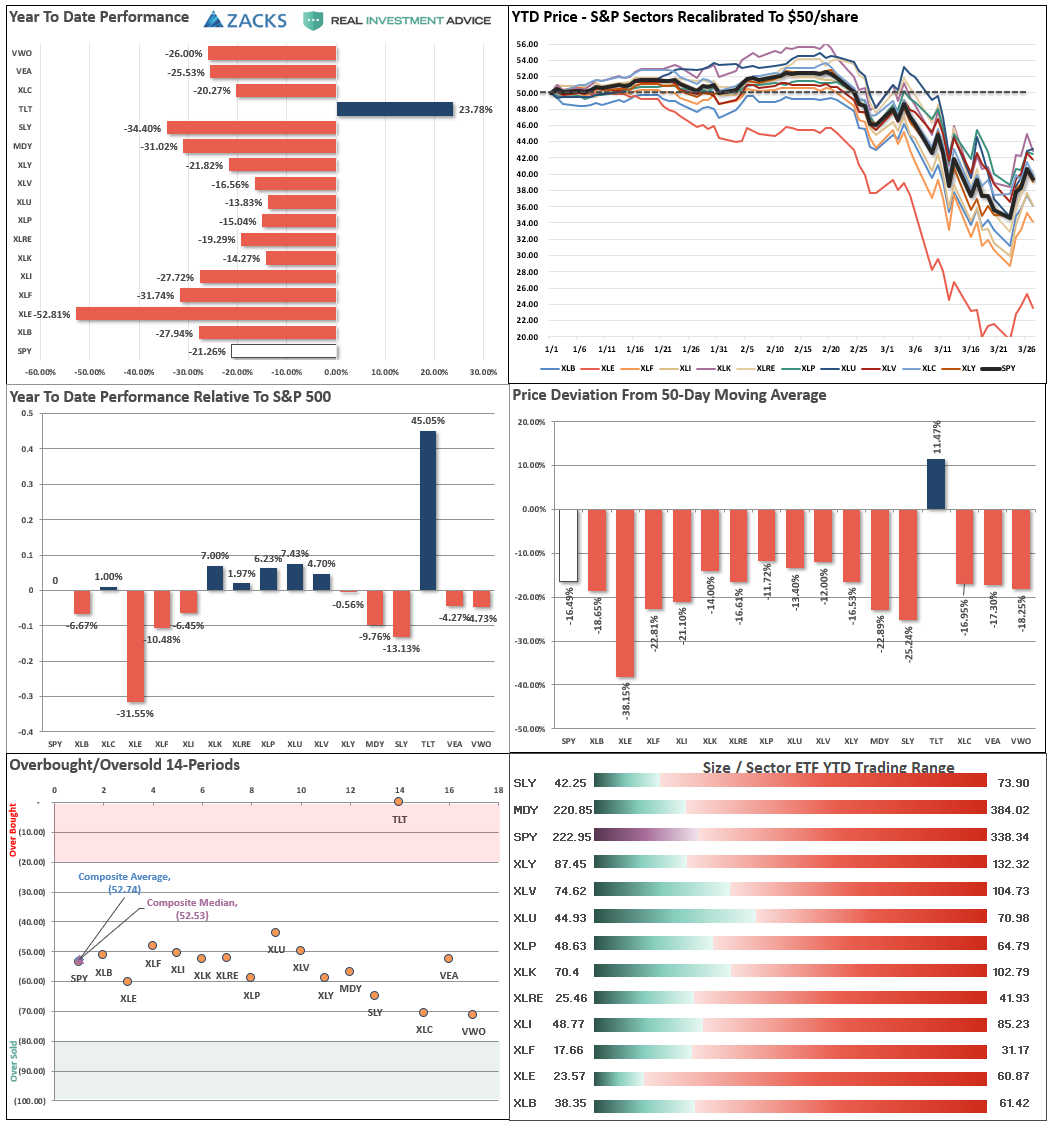

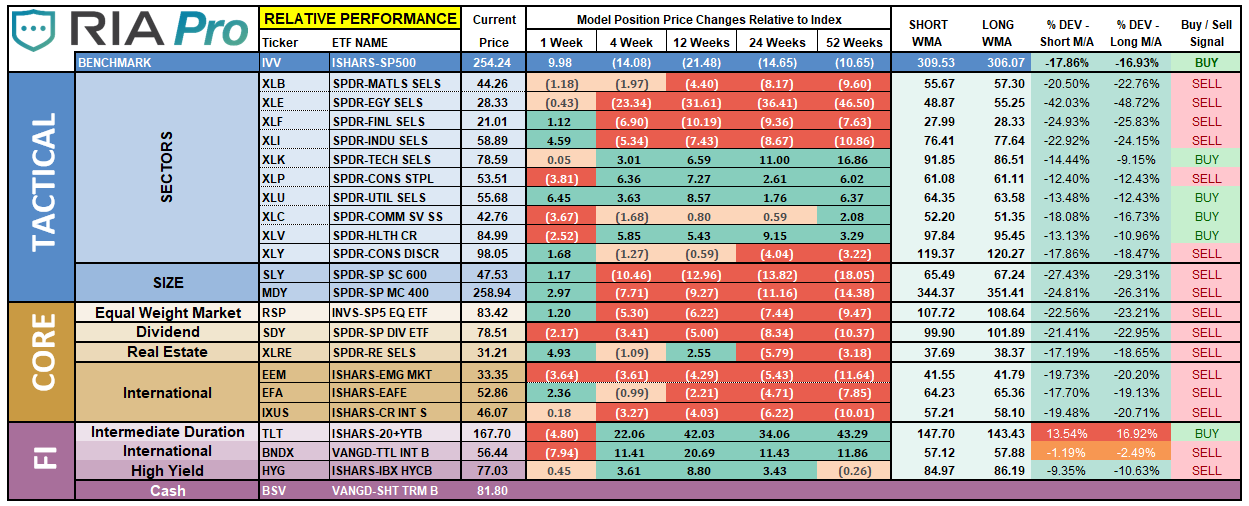

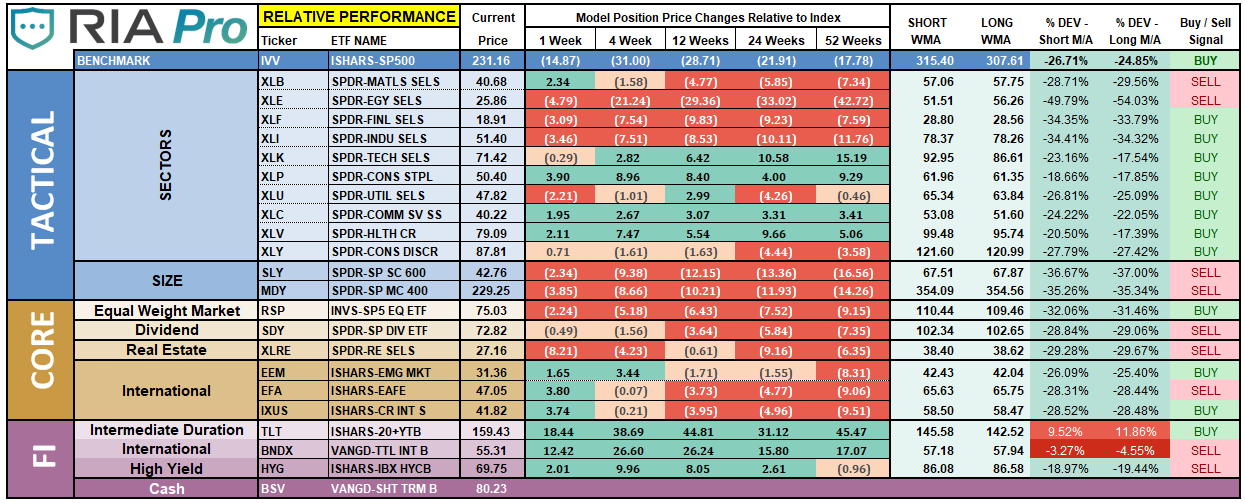

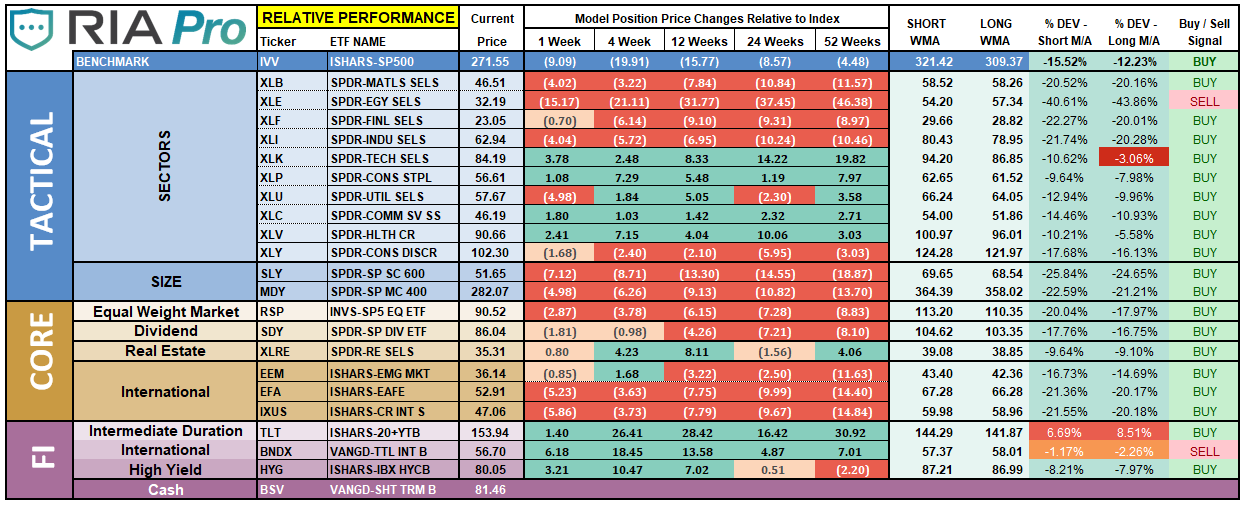

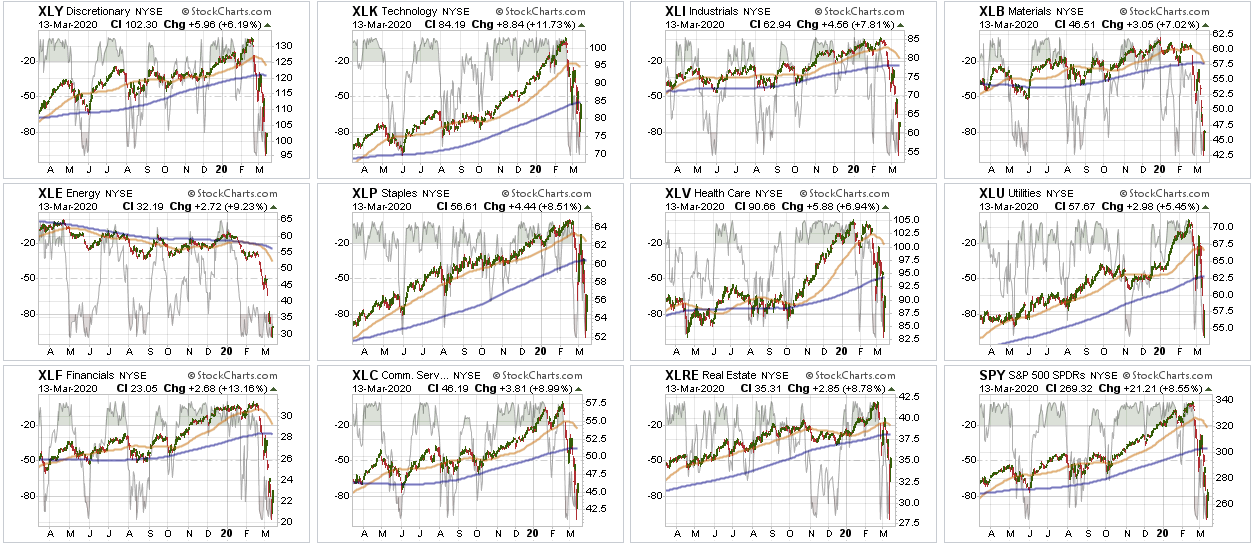

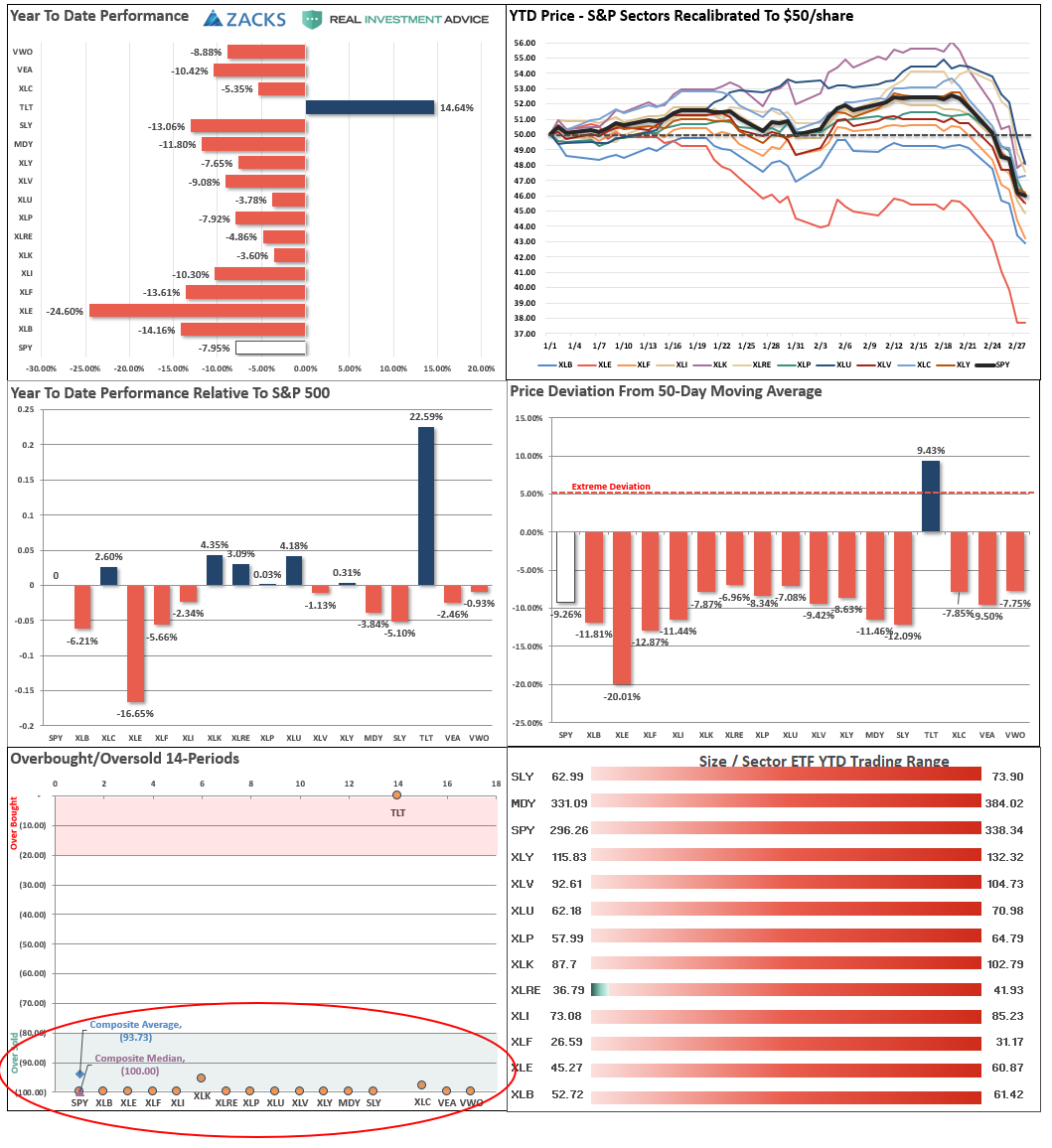

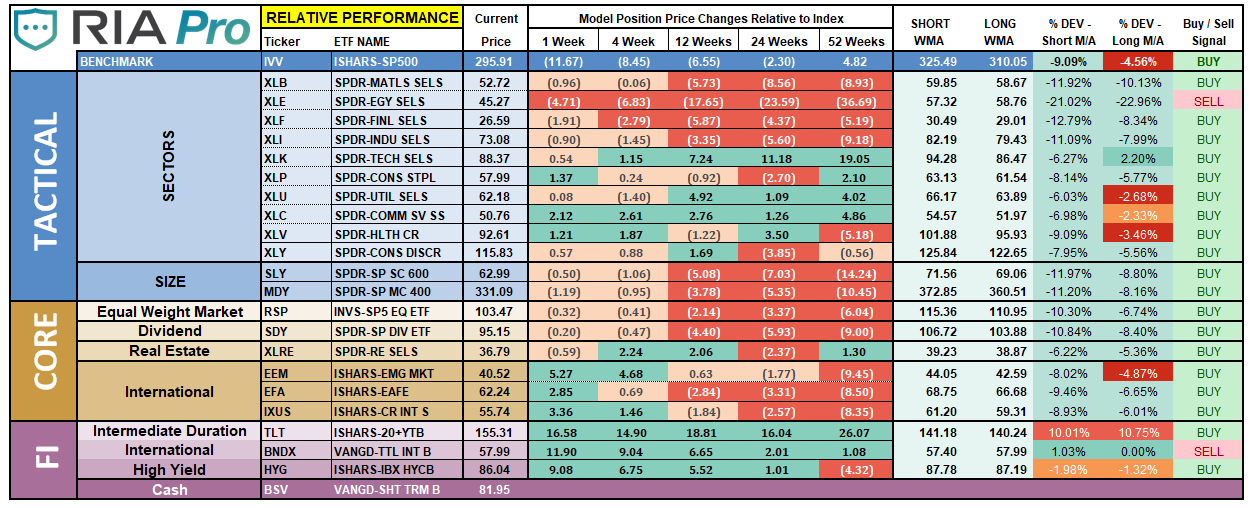

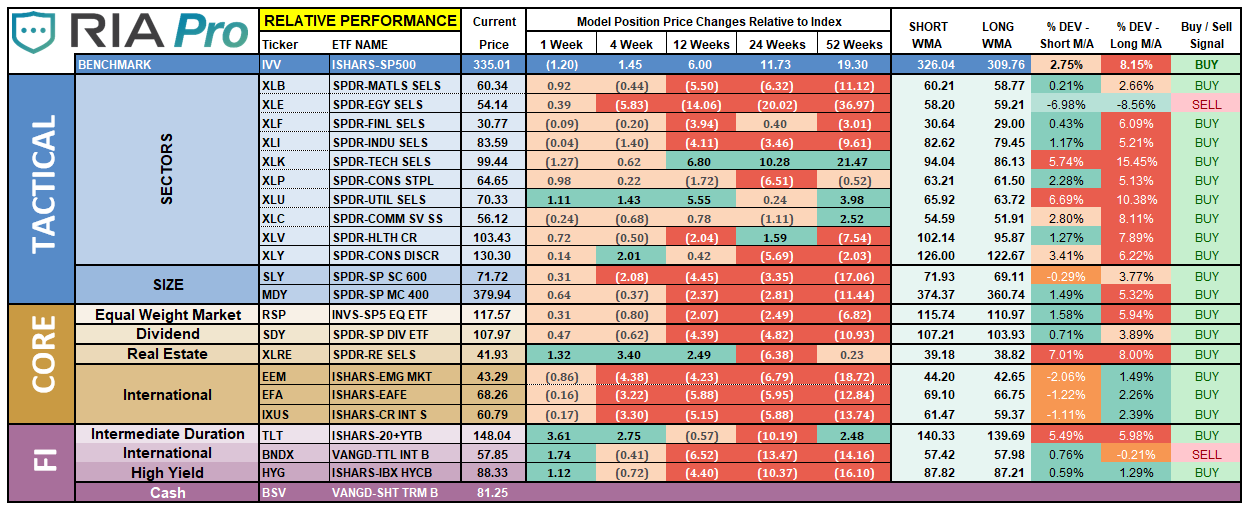

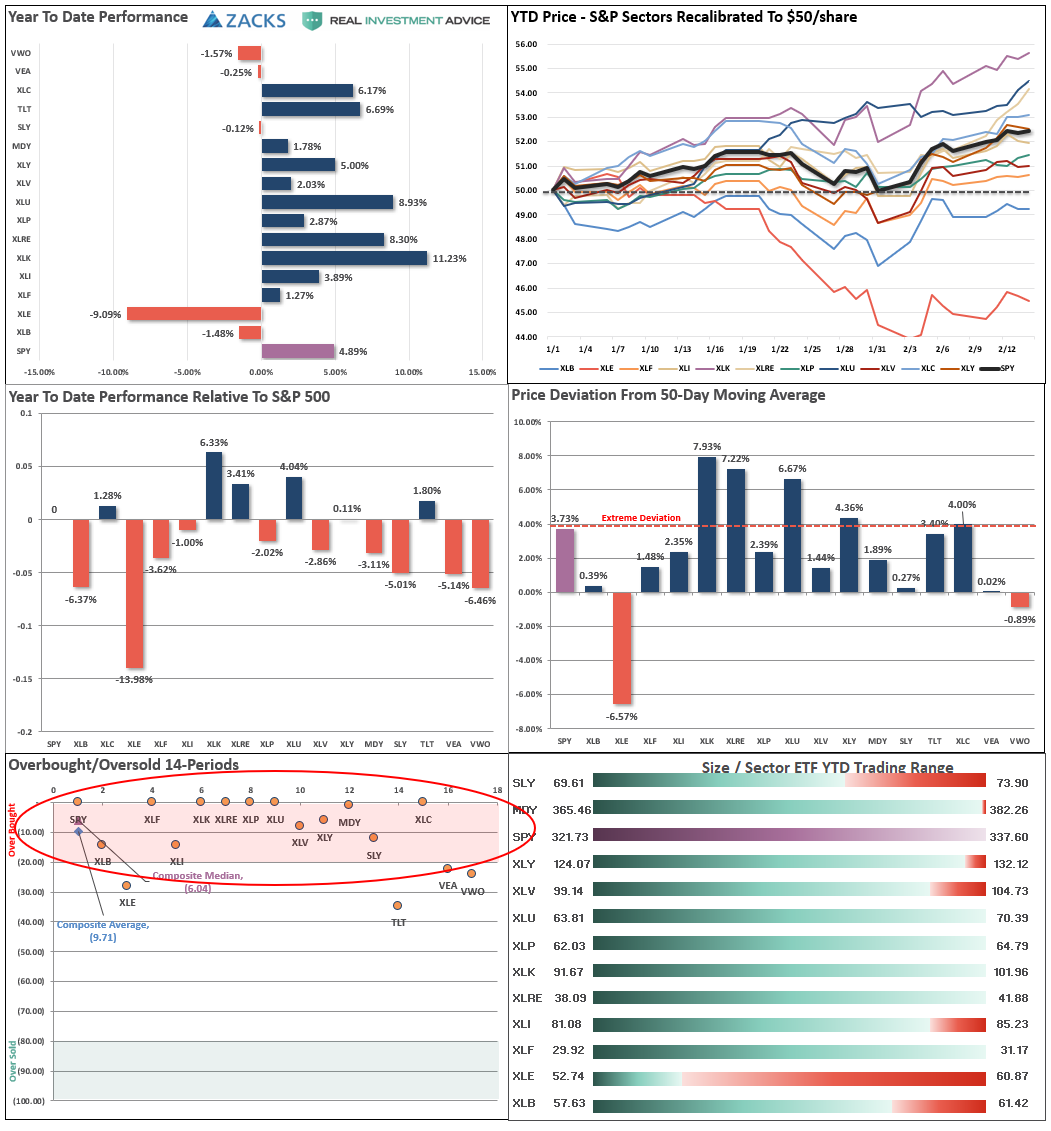

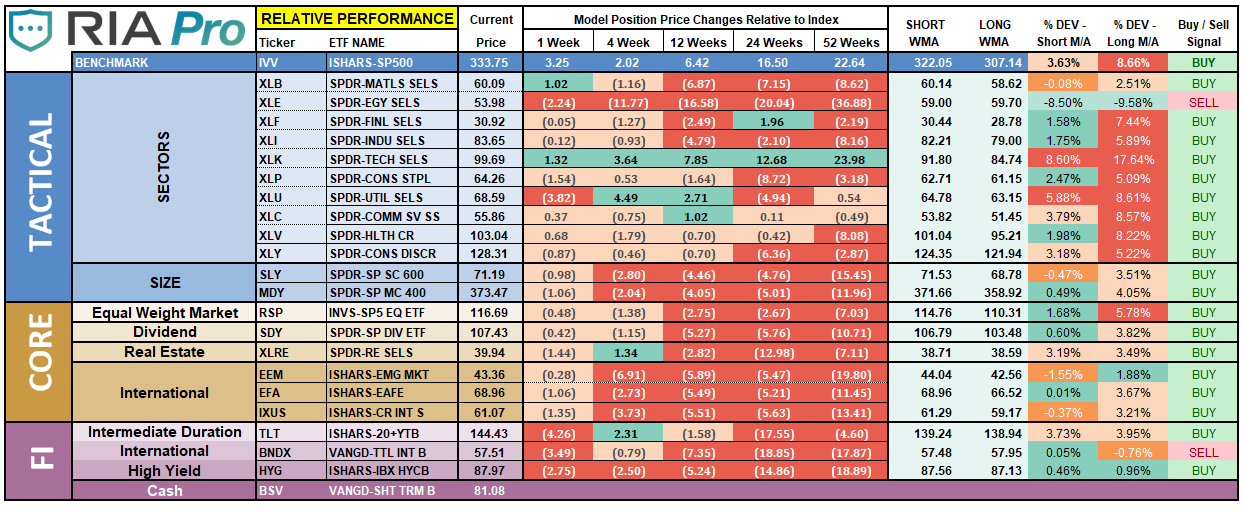

ETF Model Relative Performance Analysis

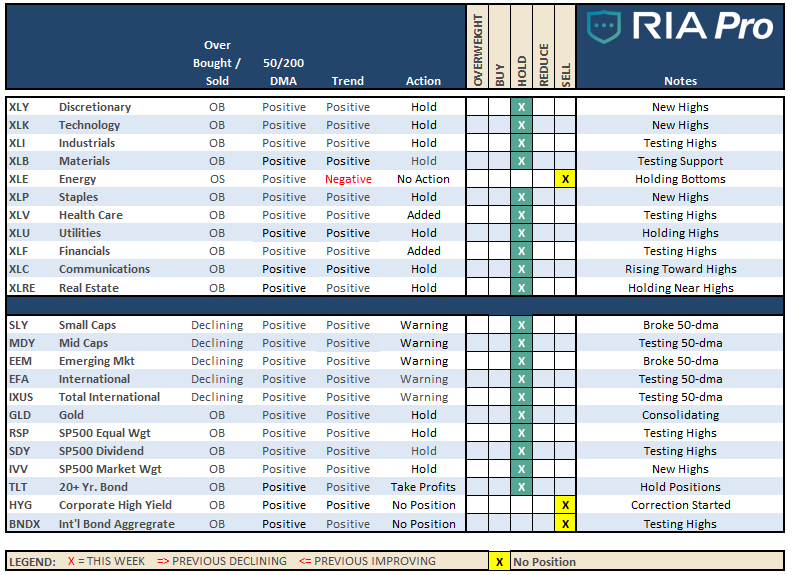

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

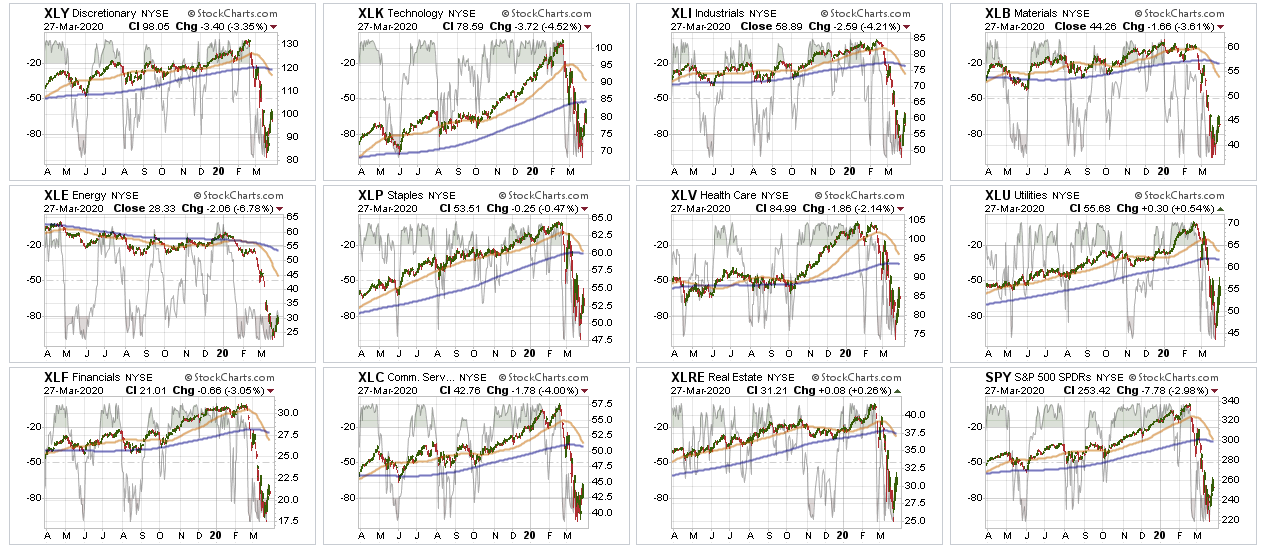

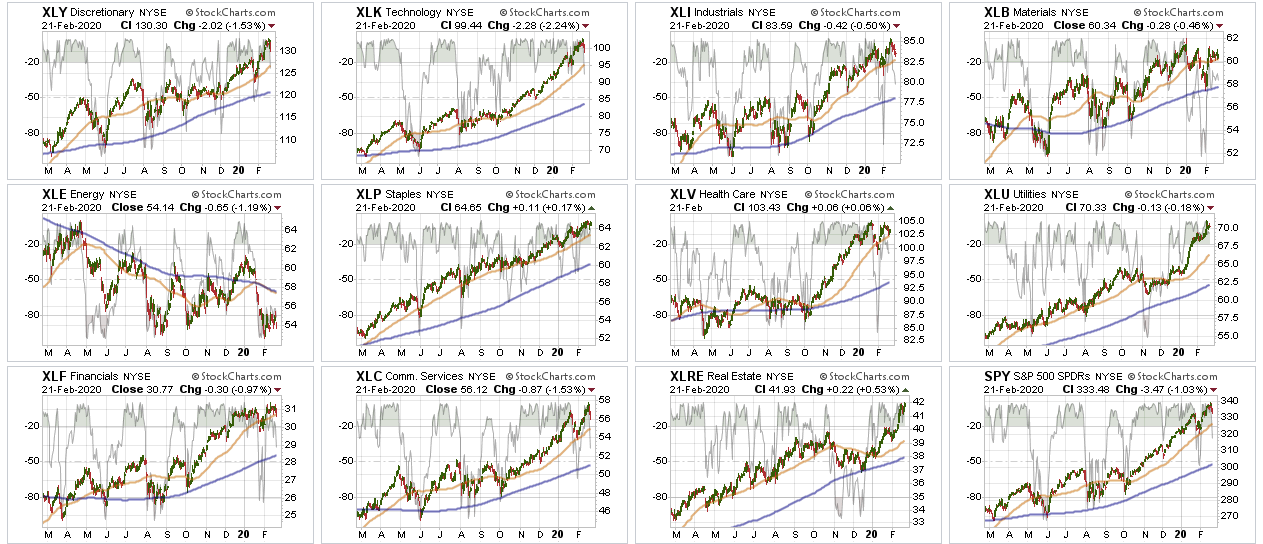

Finally, the markets bounced this past week.

However, don’t get too excited; there has been a tremendous amount of technical damage done which keeps us on the sidelines for now.

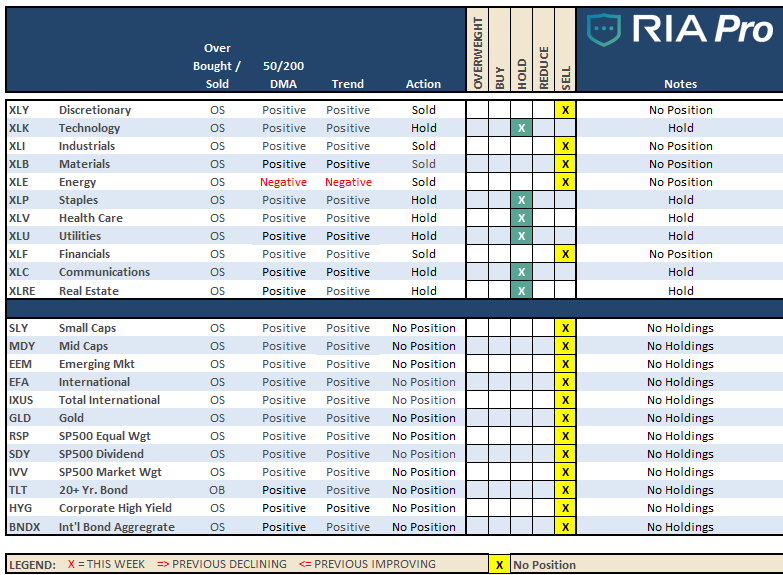

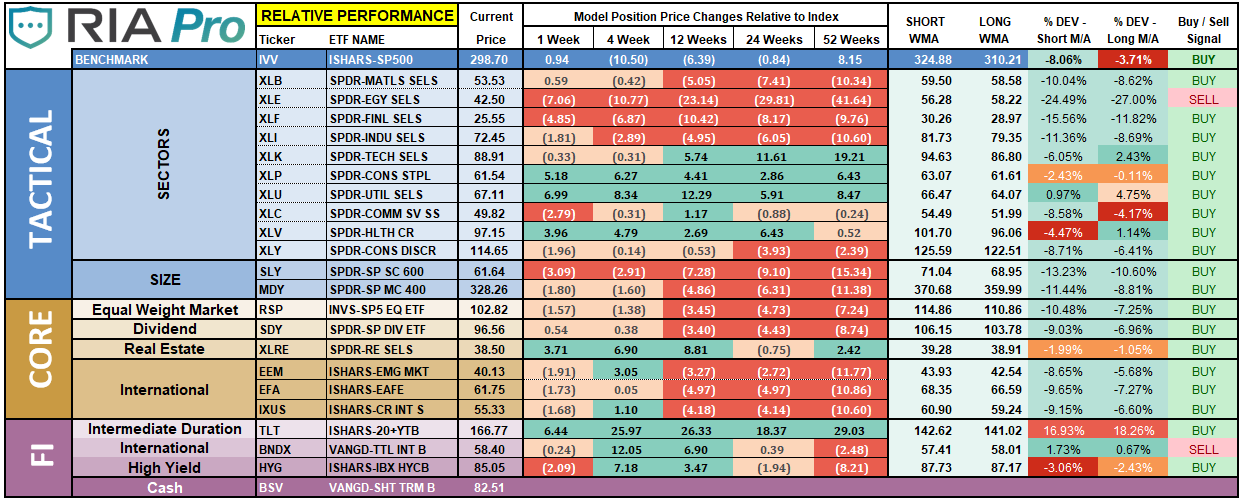

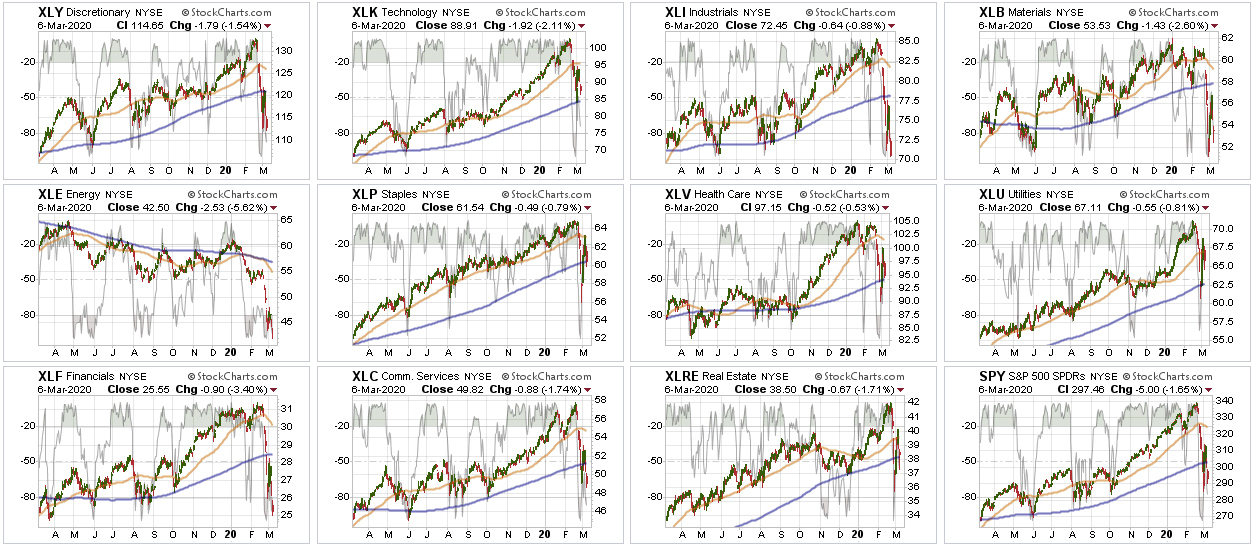

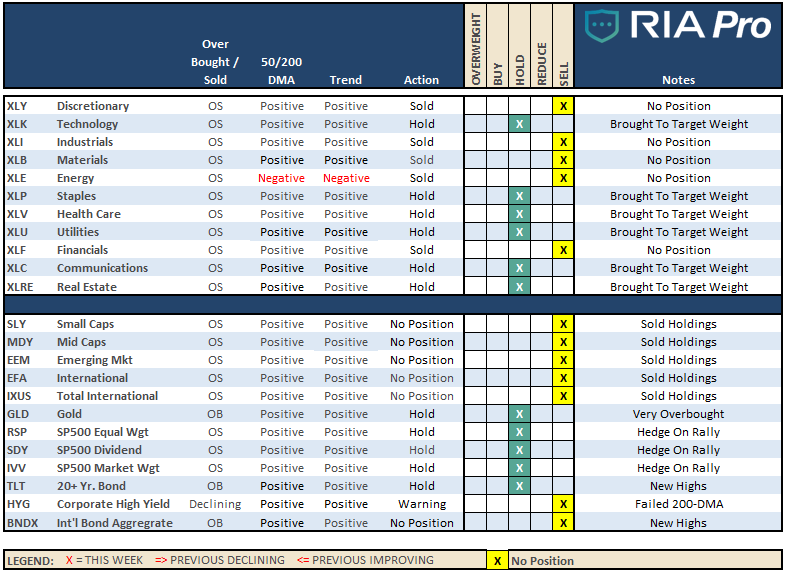

Improving – Discretionary (XLY), and Real Estate (XLRE)

We previously reduced our weightings to Real Estate and liquidated Discretionary entirely over concerns of the virus and impact on the economy. No change this week. We are getting more interested in REITs again, but are going to select individual holdings versus the ETF due to leverage concerns in the REITs.

Discretionary is going to remain under pressure due to people being able to go out and shop. This sector will eventually get a bid, so we are watching it, but we need to see an eventual end to the isolation of consumers.

Early last week, we shifted exposures in portfolios and added to our Technology and Communications sectors, bringing them up to weight. We also added QQQ, which was closed out on Friday.

Current Positions: XLK, XLC, 1/2 weight XLP, XLV

Weakening – None

No sectors in this quadrant.

Current Position: None

Lagging – Industrials (XLI), Financials (XLF), Materials (XLB), and Energy (XLE)

No change from last week, with the exception that performance continued to be worse than the overall market.

These sectors are THE most sensitive to Fed actions (XLF) and the shutdown of the economy. We eliminated all holdings in late February and early March.

Current Position: None

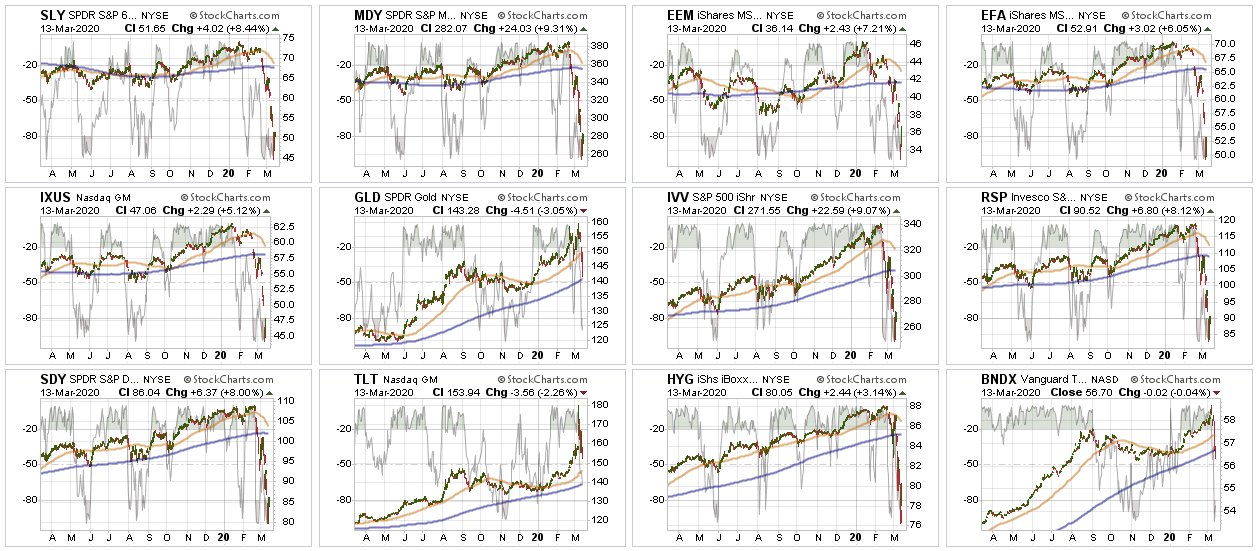

Market By Market

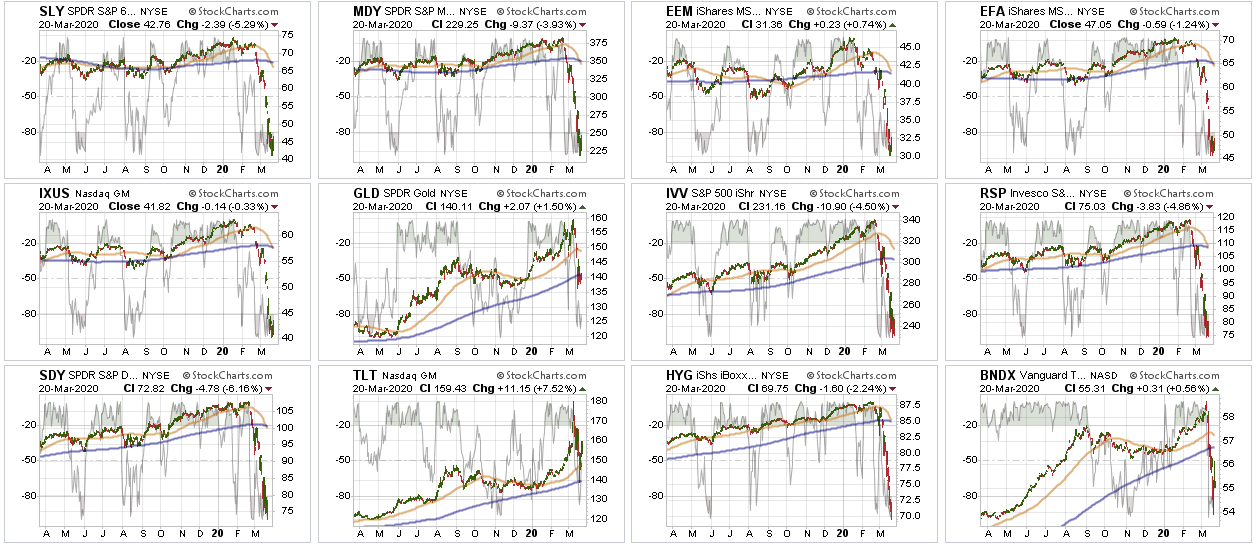

Small-Cap (SLY) and Mid Cap (MDY) – Four weeks ago, we sold all small-cap and mid-cap exposure over concerns of the impact of the coronavirus. We remain out of these sectors for now.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Same as small-cap and mid-cap. Given the spread of the virus and the impact on the global supply chain. Trading opportunities only.

Current Position: None

S&P 500 Index (Core Holding) – Given the rapid deterioration of the broad market, we sold our entire core position holdings for the safety of cash. We did add a small trading position in QQQ on Monday afternoon, and sold it on Friday.

Current Position: None

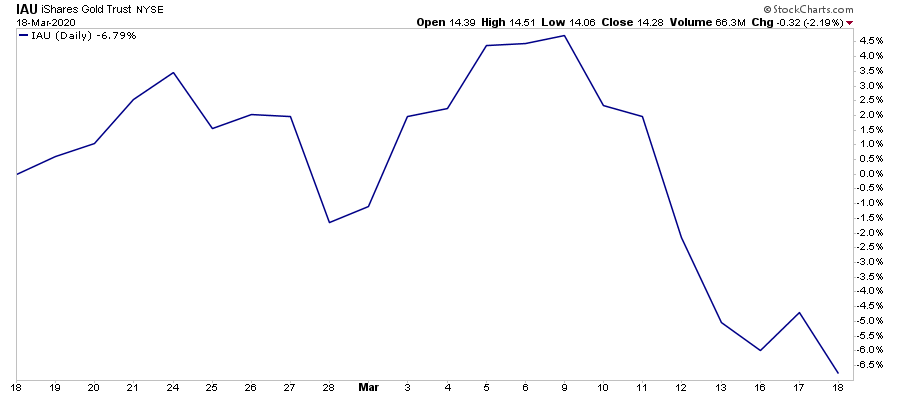

Gold (GLD) – We added a small position in GDX recently, and increased our position in IAU early this week. With the Fed going crazy with liquidity, this will be good for gold long-term, so we continue to add to our holdings on corrections.

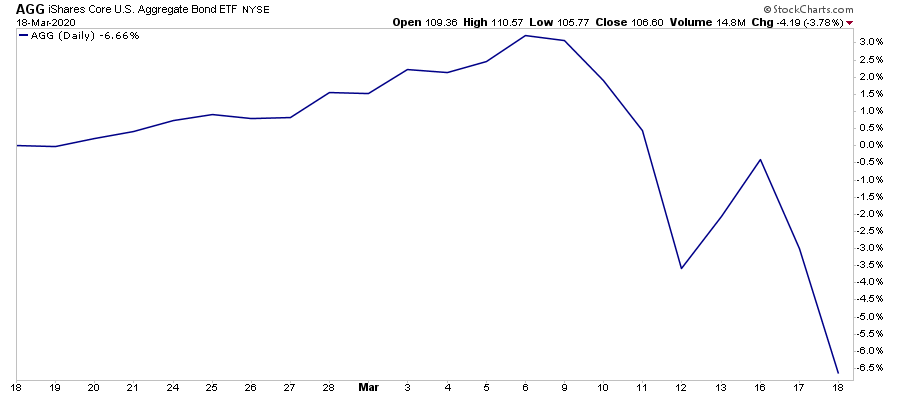

Bonds regained their footing this week, as the Fed became the “buyer” of both “first” and “last” resort. Simply, “bonds will not be allowed to default,” as the Fed will guarantee payments to creditors. We have now reduced our total bond exposure to 20% of the portfolio from 40% since we are only carrying 10% equity currently. (Rebalanced our hedge.)

Current Positions: SHY, IEF, BIL

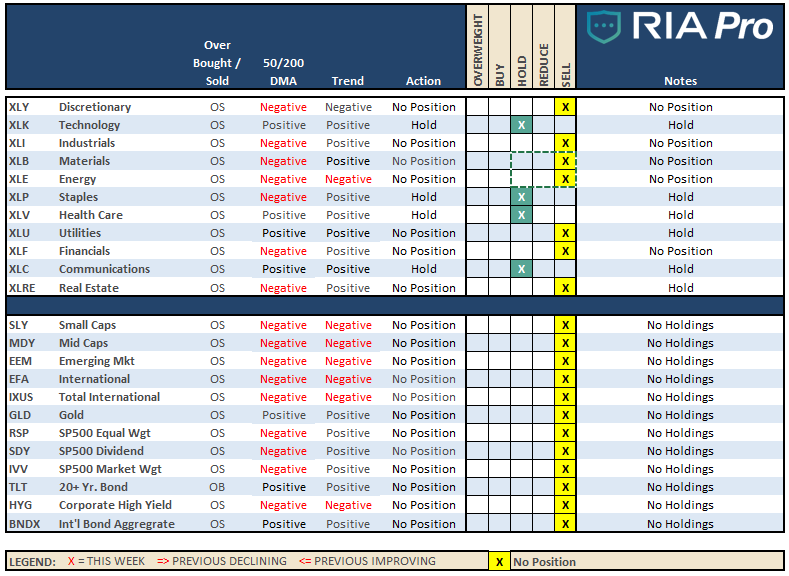

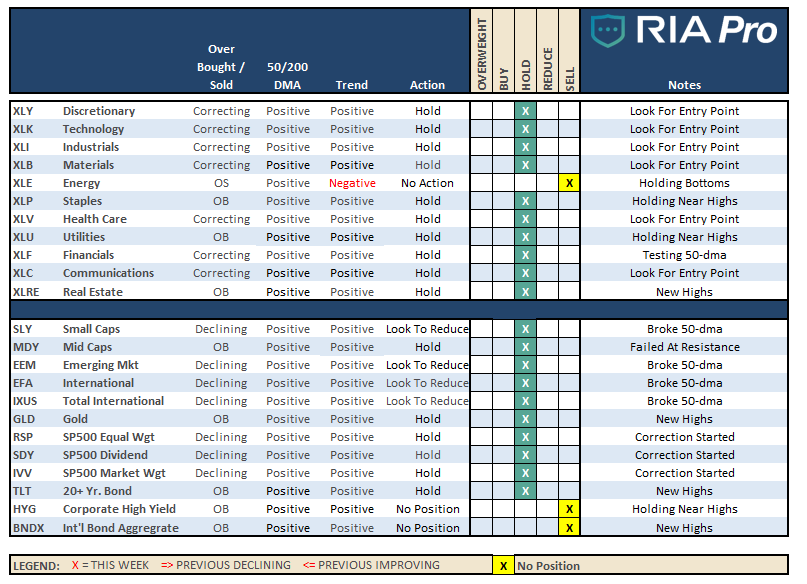

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

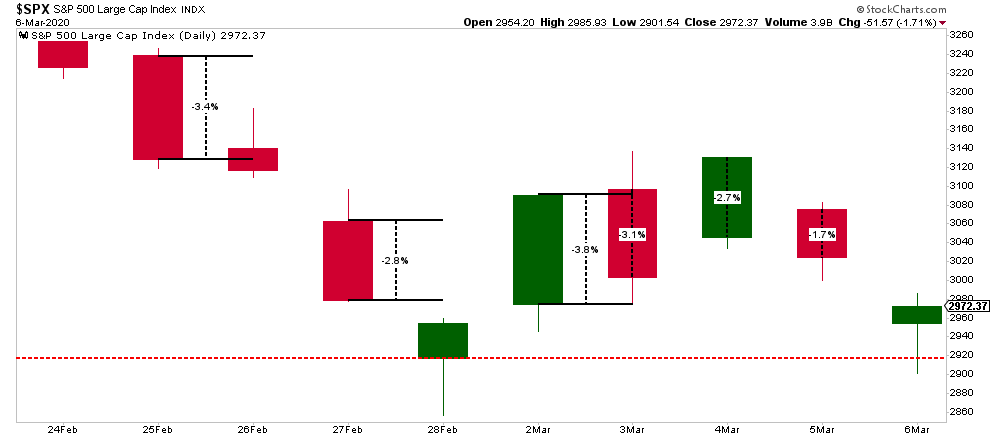

Despite the headlines of the “biggest rally in history” this past week, it’s easy to get sucked into the “Media headline” hype. However, let’s put this into some perspective:

Over the last “X” days the S&P 500 is:

5-days: +10.2%

6-days: +5.4%

10-days: -6.25%

It is much less exciting when compared to the fastest 30% plunge in history.

Keeping some perspective on where we are currently is very important. It’s easy to get swayed by the media headlines, which can lead us into making emotional investment mistakes. More often than not, emotional decisions turn out poorly.

We are starting our process of adding equities to the ETF models. As we head out of this bear market, ETF’s will have less value relative to our selective strategies.

This doesn’t mean we won’t use ETF’s at all, but we will selectively use them to fill in gaps to our individual equity selection, or for short-term trading opportunities.

Such was the case on Monday when we took on a position in QQQ for a bounce, and was subsequently closed out on Friday.

We also added small holdings of CLX and MRK to our long-term equity portfolio, as well as increased our exposure to IAU.

We continue to remain very defensive, and are in an excellent position with plenty of cash, reduced bond holdings, and minimal equity exposure in companies we want to own for the next 10-years.

We are just patiently waiting for the right opportunity to buy large chunks of these holdings with both stable, and higher yields.

Let me repeat from last week:

The ONLY people who care more about your money than you, is all of us at RIA Advisors.

We will NOT “buy the bottom” of the market. We will buy when we SEE the bottom of the market is in and risk/reward ratios are clearly in our favor.

This has been THE fastest bear market in history. We are doing our best to preserve your capital so that you meet your financial goals. Bear markets are never fun, but they are necessary for future gains.

We’ve got this.

Please don’t hesitate to contact us if you have any questions, or concerns.

Lance Roberts

CIO

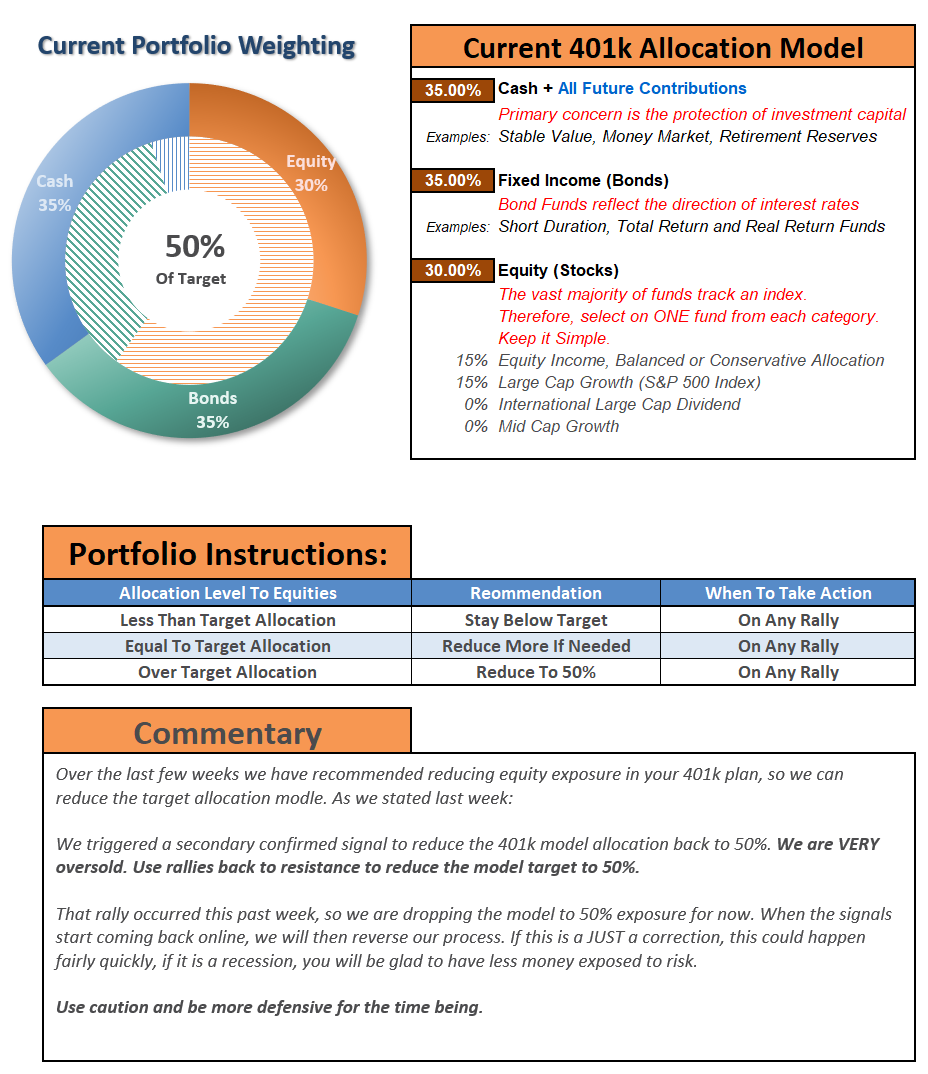

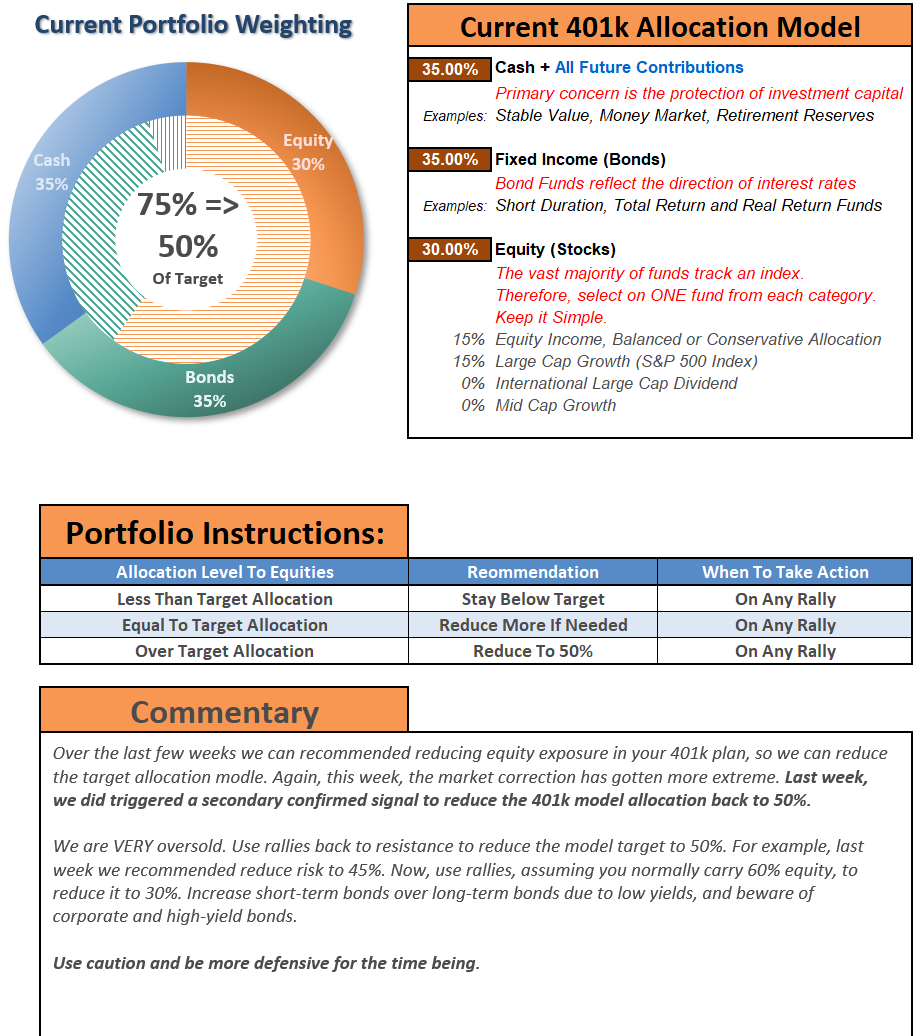

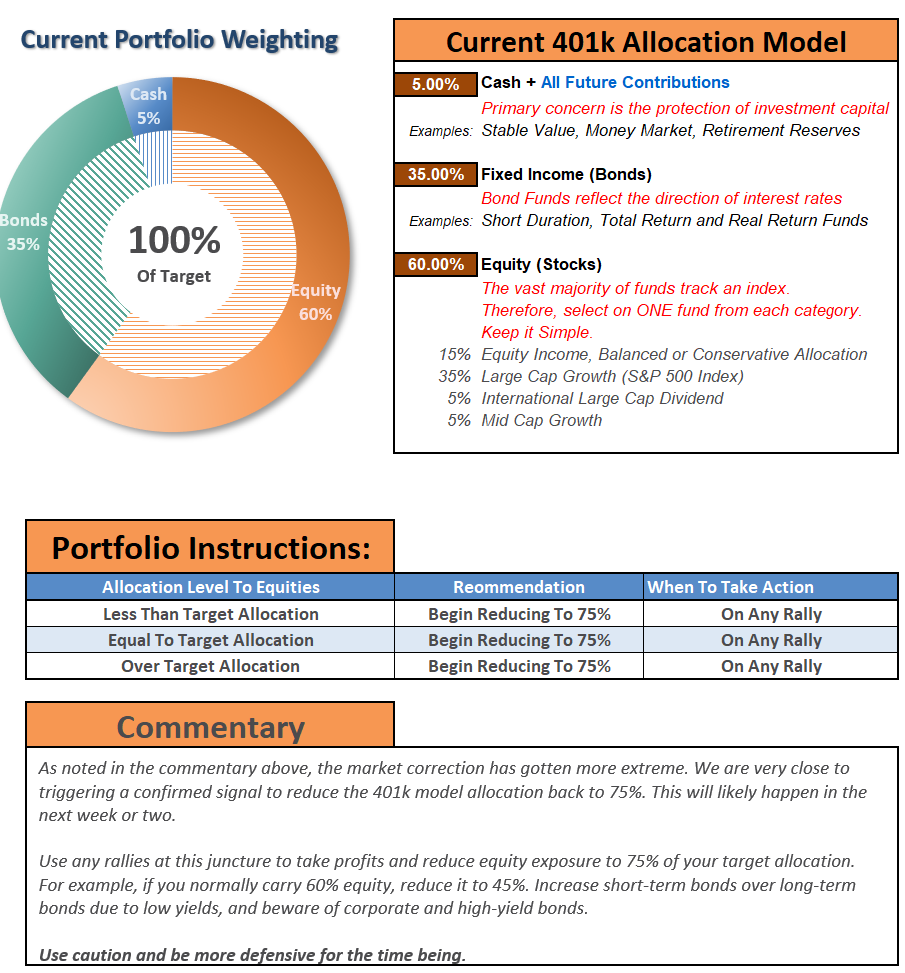

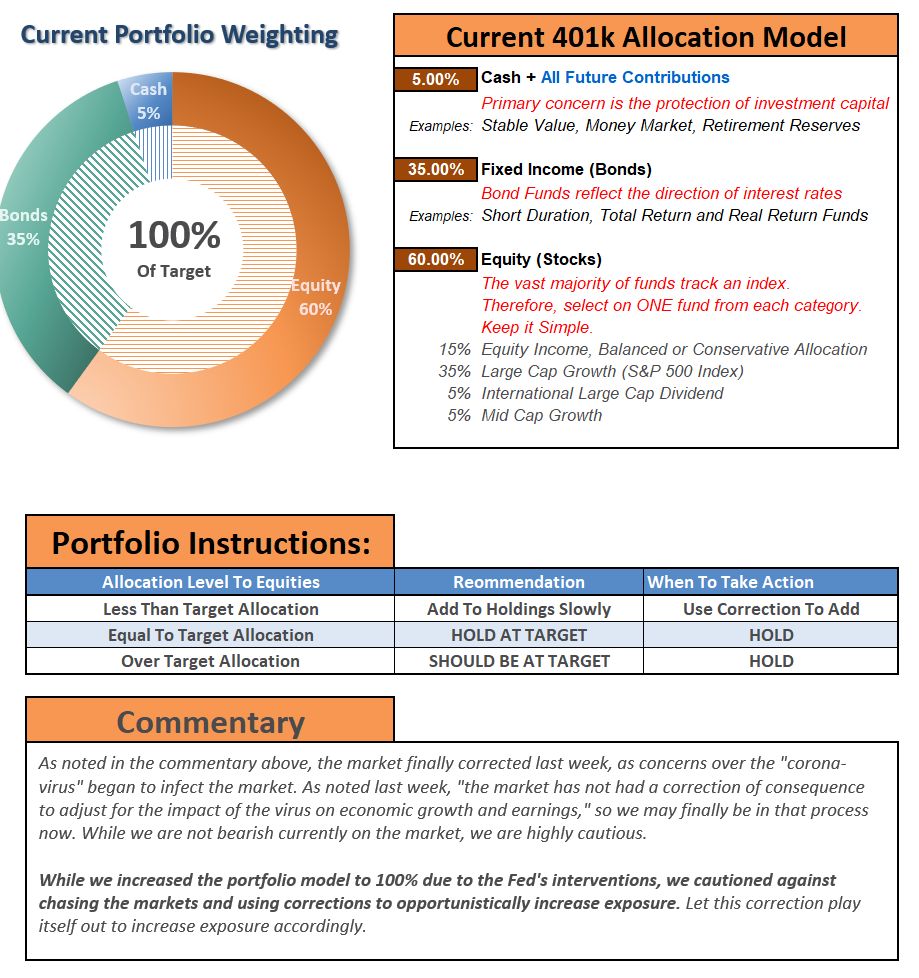

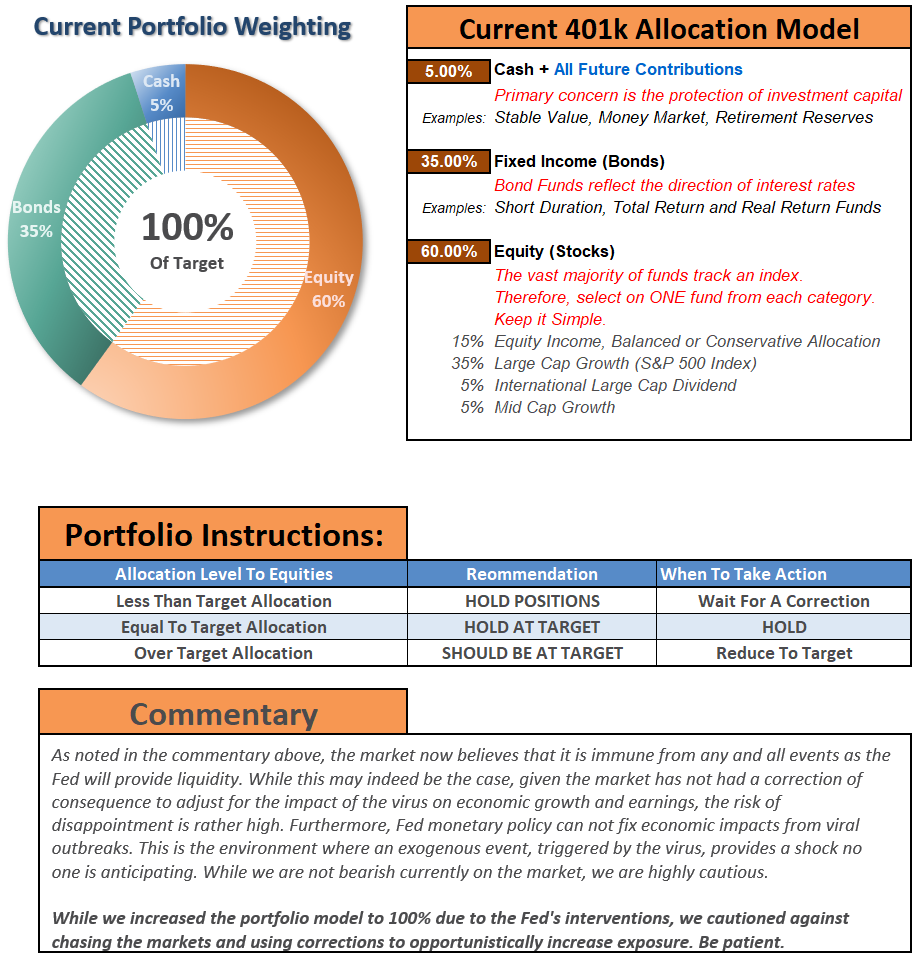

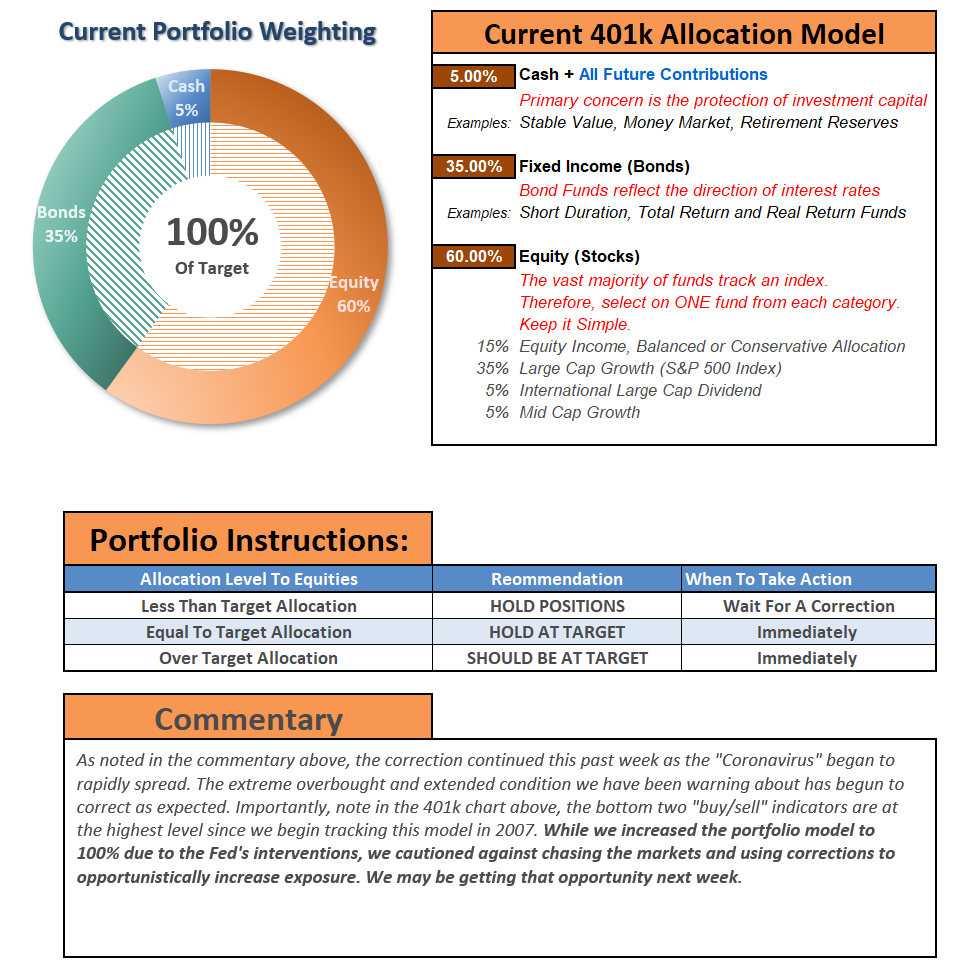

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber(You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

Name of the company

Plan Sponsor

A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

The “2020 SOCIALLY DISTANT INVESTMENT SUMMIT” is coming on Thursday, April 2nd.

Click the link below to receive an email with a special “invitation only” link when the summit goes “live.” (Current newsletter subscribers are already registered.)

“From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance.

Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Chart Updated Through Friday

Not surprisingly, here were the headlines, almost exactly as we wrote them:

Well, you get the idea.

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. More importantly, “bear markets” only end when “NO ONE wants to buy it.”

Fed Can’t Fix It

As noted above, the “bear market” will NOT be over until the credit market is fixed. We are a long way from that being done, given the blowout in yields currently occurring.

The Fed has cut rates by 150 basis points to near zero and run through its entire 2008 crisis handbook.

That wasn’t enough to calm markets, though — so the central bank also announced $1 trillion a day in repurchase agreements and unlimited quantitative easing, which includes a hard-to-understand $625 billion of bond-buying a week going forward. At this rate, the Fed will own two-thirds of the Treasury market in a year.

But it’s the alphabet soup of new programs that deserve special consideration, as they could have profound long-term consequences for the functioning of the Fed and the allocation of capital in financial markets. Specifically, these are:

CPFF (Commercial Paper Funding Facility) – buying commercial paper from the issuer.

PMCCF (Primary Market Corporate Credit Facility) – buying corporate bonds from the issuer.

SMCCF (Secondary Market Corporate Credit Facility) – buying corporate bonds and bond ETFs in the secondary market.

MSBLP (Main Street Business Lending Program) – Details are to come, but it will lend to eligible small and medium-sized businesses, complementing efforts by the Small Business Association.

To put it bluntly, the Fed isn’t allowed to do any of this.”

However, on Friday, the Federal Reserve ran into a problem, which could poses a risk for the markets going forward. As Jim noted, the mind-boggling pace of bond purchases quickly hit the limits of what was available to pledge for collateral.

Or rather, the Fed’s “unlimited QE,” may not be so “unlimited” after all.

The consequence is the Fed is already having to start cutting back on its QE program. That news fueled the late-day sell-off Friday afternoon. (Charts courtesy of Zerohedge)

While Congress did pass the “CARES” act on Friday, it will do little to backstop what is about to happen to the economy for two primary reasons:

The package will only support the economy for up to two months. Unfortunately, there is no framework for effective and timely deployment; firms are already struggling to pay rents, there are pockets of funding stress in credit markets as default risks build, and earnings guidance is abandoned.

The unprecedented uncertainty facing financial markets on the duration of social distancing, the depth of the economic shock and when the infection rate curve will flatten, and there are many unknowns which will further undermine confidence.

Both of these points are addressed in this week’s Macroview but here are the two salient points to support my statement:

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance, can be provided. This will lead to higher and longer-duration of, unemployment.”

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any type of disruption to their income going into the recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits leads to higher unemployment and lower asset prices until the cycle is complete.

The long term bull pattern that existed since the 3/9/09 is over. That means the pattern of investors confidently buying every decline is over.

The market became historically oversold on 3/23 using many metrics, and that oversold condition coincided with the long term support area of S&P 500 2110-2180.

The short-covering and rebalancing had a lot to do with the size and speed of the 3-day rally. Also, we know the lack of ETF liquidity played a huge role as well as algorithmic trading.

Technically the market can still go up 6.9% higher from here to hit the 50% retracement level (3386 – 2237 = 1149/2 = 574 + 2237 = 2811….2811/2630 = +6.9%.) I would not bet on it.

The market only sustains a rally once there is light at the Coronavirus tunnel.

I do not think the S&P 500 will hit a new high this year. Maybe not in 2021, either.

His analysis agrees with our own, which we discussed with you last week.

“The good news is the markets are now more extremely oversold on a variety of measures than at just about any other point in history.

Warning: Any reversal will NOT BE the bear market bottom. It will be a ‘bear market’ rally you will want to ‘sell’ into. The reason is there are still many investors trapped in ‘buy and hold’ and ‘passive indexing’ strategies that are actively seeking an exit. Any rallies will be met with redemptions.

Most importantly, all of our long-term weekly ‘sell signals’ have now been triggered. Such would suggest that a rally back to the ‘bullish trend line’ from 2009 will likely be the best opportunity to ‘sell’ before the ‘bear market’ finds its final low.”

Last week’s chart updated through Friday’s close.

While the recent lows may indeed turn out to be “the bottom,” I highly suspect they won’t. Given the sell signals have been registered at such high levels, the time, and distance, needed to reverse the excesses will require a deeper market draw.

As Jeff Hirsch from Stocktrader’s Alamanc noted:

“While we are all rooting for the market to find support here so much damage has been done. A great deal of uncertainty remains for the economy and health crisis. This looks like a bear market bounce.

History suggests that we are in for some tough sledding in the market this year with quite a bit of chop. When the January Barometer came in with a negative reading, our outlook for 2020 began to diminish as every down January since 1950 has been followed by a new or continuing bear market, a 10% correction, or a flat year. Then another warning sign flashed when DJIA closed below its December closing low on February 26, 2020 as the impact of this novel coronavirus began to take its toll on Wall Street.

In the March Outlook, we presented this graph of the composite seasonal pattern for the 22 years since 1950 when both the January Barometer as measured by the S&P 500 were down, and the Dow closed below its previous December closing low in the first quarter. Below is a graph of DJIA, S&P 500 and NASDAQ Composite for 2020 year-to-date as of the close on March 25. Comparing 2020 market action to these 22 years, suggests a choppy year ahead with the potential for several tests of the recent low.”

“The depth of this waterfall decline may be too deep for the market to rebound quickly. This bear market also put this year’s Best Six Months (November-April) at risk of being negative. The record of down Best Six Months is not encouraging and it reminds us of a salient quote from the Almanac from an old market sage,

‘If the market does not rally, as it should during bullish seasonal periods, it is a sign that other forces are stronger and that when the seasonal period ends those forces will really have their say.’— Edson Gould (Stock market analyst, Findings & Forecasts, 1902-1987)'”

On a short-term basis, the market is also suggesting some risk. The daily chart below shows the market rallied to, and failed at, the first level of the Fibonacci retracement we outlined last week, suggesting profits be taken at this level. While there are two remaining targets for the bear market rally, the probabilities weigh heavily against them. (This doesn’t mean they can’t be achieved, it is “possible,” just not “probable.”)

Furthermore, with the “Death Cross” triggering on Friday (the 50-dma crossing below the 200-dma), this will put further downside pressure on any “bear market” advance from current levels.

Given the magnitude, and multiple confirmations, of these signals, it is far too soon to assume the “bear market” is over. This is particularly the case, given the sell-off is less than one-month-old.

Bear markets, and recessions, tend to last 18-months on average.

The current bear market and recession are not the results of just the “coronavirus” shock. It is the result of many simultaneous shocks from:

Economic disruption

Surging unemployment

Oil price shock

Collapsing consumer confidence, and

Most importantly, a “credit event.”

We likely have more to go before we can safely assume we have turned the corner.

In the meantime, use rallies to raise cash. Don’t worry about trying to “buy the bottom.”There will be plenty of time to see “THE” bottom is in, and having cash will allow you to “buy stocks” from the last of the “weak hands.”

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

S&P 500 Tear Sheet

Performance Analysis

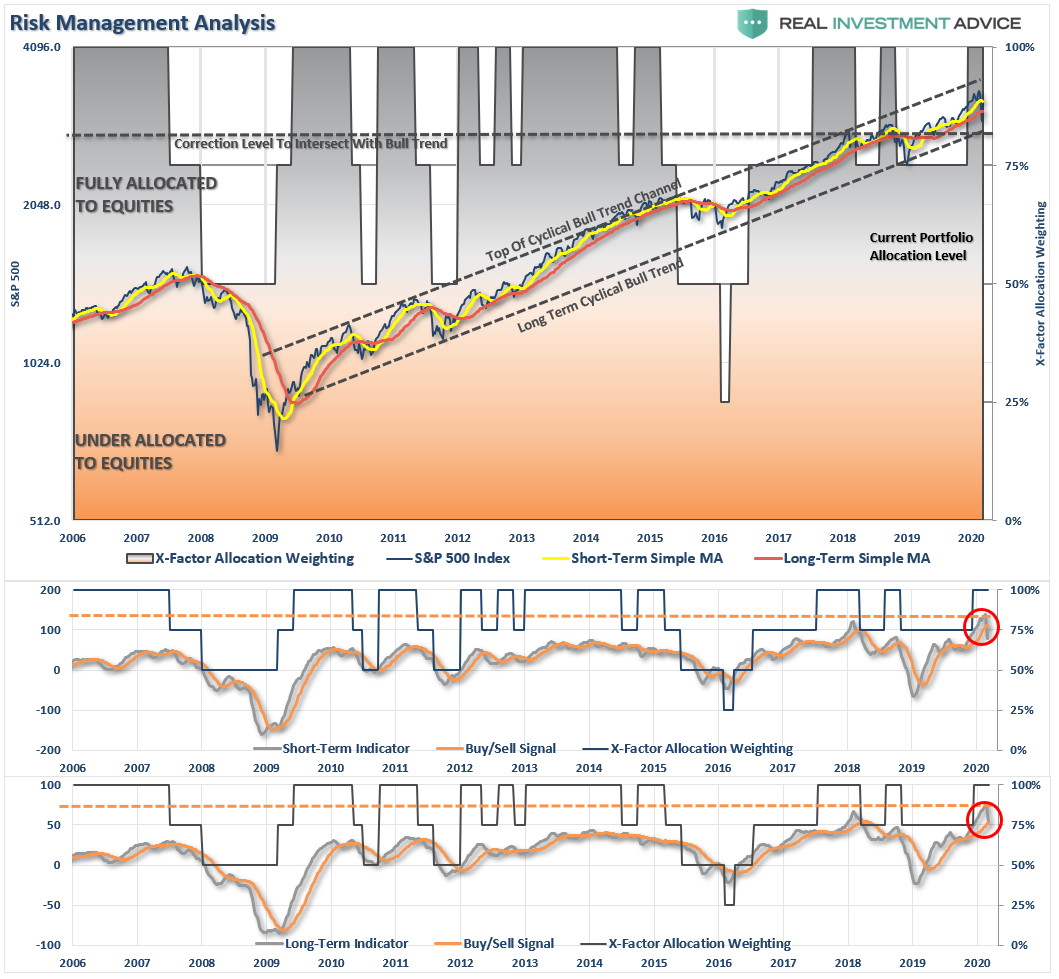

Technical Composite

Note: The technical gauge bounced from the lowest level since both the “Dot.com” and “Financial Crisis.” However, note the gauge bottoms BEFORE the market bottoms. In 2002, lows were retested. In 2008, there was an additional 22% decline in early 2009.

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

Finally, the markets bounced this past week.

However, don’t get too excited; there has been a tremendous amount of technical damage done which keeps us on the sidelines for now.

Improving – Discretionary (XLY), and Real Estate (XLRE)

We previously reduced our weightings to Real Estate and liquidated Discretionary entirely over concerns of the virus and impact on the economy. No change this week. We are getting more interested in REITs again, but are going to select individual holdings versus the ETF due to leverage concerns in the REITs.

Discretionary is going to remain under pressure due to people being able to go out and shop. This sector will eventually get a bid, so we are watching it, but we need to see an eventual end to the isolation of consumers.

Early last week, we shifted exposures in portfolios and added to our Technology and Communications sectors, bringing them up to weight. We also added QQQ, which was closed out on Friday.

Current Positions: XLK, XLC, 1/2 weight XLP, XLV

Weakening – None

No sectors in this quadrant.

Current Position: None

Lagging – Industrials (XLI), Financials (XLF), Materials (XLB), and Energy (XLE)

No change from last week, with the exception that performance continued to be worse than the overall market.

These sectors are THE most sensitive to Fed actions (XLF) and the shutdown of the economy. We eliminated all holdings in late February and early March.

Current Position: None

Market By Market

Small-Cap (SLY) and Mid Cap (MDY) – Four weeks ago, we sold all small-cap and mid-cap exposure over concerns of the impact of the coronavirus. We remain out of these sectors for now.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Same as small-cap and mid-cap. Given the spread of the virus and the impact on the global supply chain. Trading opportunities only.

Current Position: None

S&P 500 Index (Core Holding) – Given the rapid deterioration of the broad market, we sold our entire core position holdings for the safety of cash. We did add a small trading position in QQQ on Monday afternoon, and sold it on Friday.

Current Position: None

Gold (GLD) – We added a small position in GDX recently, and increased our position in IAU early this week. With the Fed going crazy with liquidity, this will be good for gold long-term, so we continue to add to our holdings on corrections.

Bonds regained their footing this week, as the Fed became the “buyer” of both “first” and “last” resort. Simply, “bonds will not be allowed to default,” as the Fed will guarantee payments to creditors. We have now reduced our total bond exposure to 20% of the portfolio from 40% since we are only carrying 10% equity currently. (Rebalanced our hedge.)

Current Positions: SHY, IEF, BIL

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

Despite the headlines of the “biggest rally in history” this past week, it’s easy to get sucked into the “Media headline” hype. However, let’s put this into some perspective:

Over the last “X” days the S&P 500 is:

5-days: +10.2%

6-days: +5.4%

10-days: -6.25%

It is much less exciting when compared to the fastest 30% plunge in history.

Keeping some perspective on where we are currently is very important. It’s easy to get swayed by the media headlines, which can lead us into making emotional investment mistakes. More often than not, emotional decisions turn out poorly.

We are continuing our process of blending the Equity and ETF models. As we head out of this bear market, ETF’s will have much less value relative to our selective strategies.

This doesn’t mean we won’t use ETF’s at all, but we will selectively use them to fill in gaps to our individual equity selection, or for short-term trading opportunities.

Such was the case on Monday when we took on a position in QQQ for a bounce, and was subsequently closed out on Friday.

We also added small holdings of CLX and MRK to our long-term portfolio, as well as increased our exposure to IAU.

We continue to remain very defensive, and are in an excellent position with plenty of cash, reduced bond holdings, and minimal equity exposure in companies we want to own for the next 10-years.

We are just patiently waiting for the right opportunity to buy large chunks of these holdings with both stable, and higher yields.

Let me repeat from last week:

The ONLY people who care more about your money than you, is all of us at RIA Advisors.

We will NOT “buy the bottom” of the market. We will buy when we SEE the bottom of the market is in and risk/reward ratios are clearly in our favor.

This has been THE fastest bear market in history. We are doing our best to preserve your capital so that you meet your financial goals. Bear markets are never fun, but they are necessary for future gains.

We’ve got this.

Please don’t hesitate to contact us if you have any questions, or concerns.

Lance Roberts

CIO

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber(You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

Name of the company

Plan Sponsor

A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

Technically Speaking: The One Thing – Playing The “Bear Market” Rally.

Let’s flashback to a time not so long ago, May 2019.

“It was interesting to see Federal Reserve Chairman Jerome Powell, during an address to the Fernandina Beach banking conference, channel Ben Bernanke during his speech on corporate ‘sub-prime’ debt (aka leveraged loans.)

‘Many commentators have observed with a sense of déjà vu the buildup of risky business debt over the past few years. The acronyms have changed a bit—’CLOs’ (collateralized loan obligations) instead of ‘CDOs’ (collateralized debt obligations), for example—but once again, we see a category of debt that is growing faster than the income of the borrowers even as lenders loosen underwriting standards. Likewise, much of the borrowing is financed opaquely, outside the banking system. Many are asking whether these developments pose a new threat to financial stability.

In public discussion of this issue, views seem to range from ‘This is a rerun of the subprime mortgage crisis’ to ‘Nothing to worry about here.’ At the moment, the truth is likely somewhere in the middle. To preview my conclusions, as of now, business debt does not present the kind of elevated risks to the stability of the financial system that would lead to broad harm to households and businesses should conditions deteriorate.’ – Jerome Powell, May 2019

“Unfortunately, while Jerome Powell may be currently channeling Ben Bernanke to keep markets stabilized momentarily, the real risk is some unforeseen exogenous event, such as Deutsche Bank going bankrupt, that triggers a global credit contagion.”

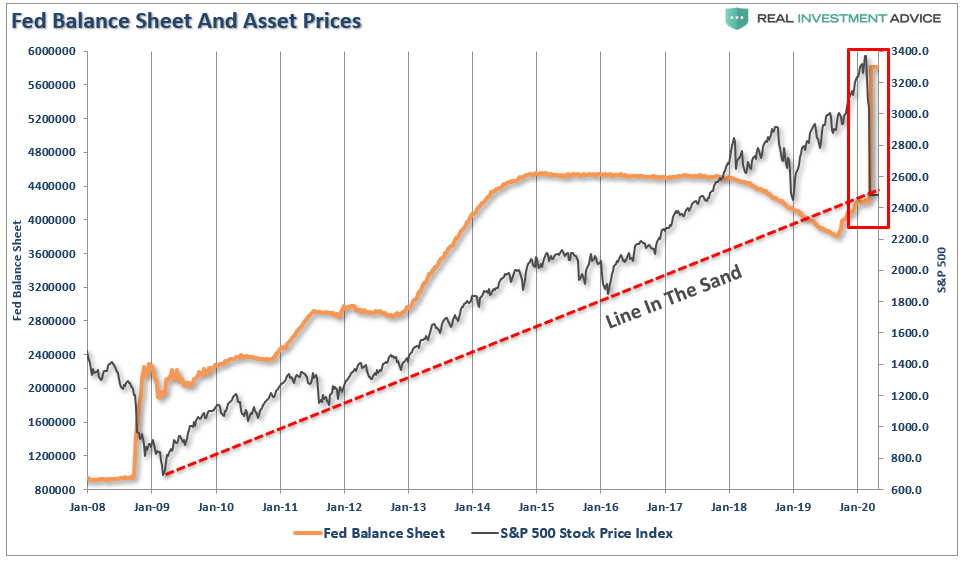

While the “exogenous event” was a “virus,” it led to a “credit event” which has crippled markets globally, leading the Federal Reserve to throw everything possible at trying to stem the crisis. With the Fed’s balance sheet set to expand towards $10 Trillion, the Federal deficit to balloon to $4 trillion, it is “all hands on deck” to stop the next “Great Depression” before it takes hold.

However, this is what we have been warning about:

“Pay attention to the market. There action this year is very reminiscent of previous market topping processes. Tops are hard to identify during the process as ‘change happens slowly.’The mainstream media, economists, and Wall Street will dismiss pickup in volatility as simply a corrective process. But when the topping process completes, it will seem as if the change occurred ‘all at once.’

The same media which told you ‘not to worry,’ will now tell you ‘no one could have seen it coming.’”

The only question which remains to be answered is whether the MORE debt and monetary stimulus can fix a debt and monetary stimulus bubble?

In other words, can the Fed inflate the fourth bubble to offset the implosion of the third?

Think about the insanity of that statement, but that is what the markets, and the economy, are banking on.

We do expect that with the flood of fiscal and monetary stimulus, a “bear market rally” becomes a real probability, at least in the short-term.

How big of a rally? What should you do? These are the important points in today’s missive.

The One Thing

The “ONE Thing” you need to do TODAY, right now, is “accept” where you are.

What you had, what was lost, and the mistakes you made, CAN NOT be corrected. They are in the past. However, by hanging on to those “emotions,” we lock ourselves out of the ability to take actions that will begin the corrective process.

Let me dispel some myths:

“Hope” is not an investment strategy. Hanging on to some stock you lost money in waiting for it to “get back to even,” costs you opportunity.

You aren’t a loser. Whatever happened previously is over, and it doesn’t make you a “loser.” However, staying in losing positions or strategies will continue to cost you.

Selling does NOT lock in losses. The losses have already occurred. Selling, however, gives you the ability to take advantage of “opportunity” to begin the recovery process.

Okay, now that we have the right “mindset,” let’s take an educated guess on what happens next.

The current bear market is exhibiting many of the same “technical traits” as seen in both the “Dot.com” and “Financial Crisis.”

In each previous case, the market experienced a parabolic advance to the initial peak. A correction ensued, which was dismissed by the mainstream media, and investors alike, as just a “pause that refreshes.” They were seemingly proved correct as the markets rebounded shortly thereafter and even set all-time highs. Investors, complacent in the belief that “this time was different” (1999 – a new paradigm, 2007 – Goldilocks economy), continued to hold out hopes the bull market was set to continue.

That was a mistake.

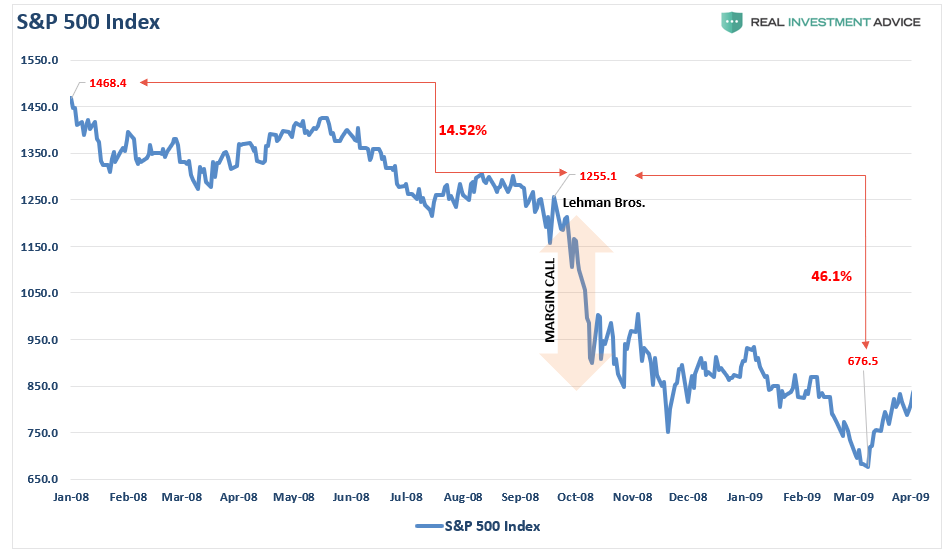

Also, in each period, once the monthly “sell signal” was triggered from a high level, the ensuing correction process took months to complete. This not only reset the market, but valuations as well. In both previous periods, reflexive rallies occurred, which eventually failed. While the 2008 plunge following the Lehman crisis was most similar to the current environment, there was a brief rally following the passage of TARP, which sucked investors in before the additional 22% decline in the first two months of 2009.

Most importantly, the market got very oversold early in both previous bear markets, and stayed that way for the entirety of the bear market. Currently, the market has only just now gotten to a similar oversold condition.

What all the indicators currently suggest is that while the current correction has been swift and brutal, bear markets are not resolved in a single month.

This is going to take some time.

Bear Market Rally

Over the past couple of week’s, we have been talking about a potential reflexive bounce.

From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance. Such an advance will “lure” investors back into the market, thinking the “bear market” is over.

This is what “bear market rallies” do, and generally inflict the most pain possible on unwitting investors. The reasons for this are many, but primarily investors who were trapped in the recent decline will use the rally to “flee” the markets permanently.

Chart Updated Through Monday

More importantly, as noted above, “bear markets” are not resolved in a single month. Currently, there are too many investors trying to figure out where “the bottom” is, so they can “buy” it.

Bear markets do not end in optimism; they end in despair.

Looking back at 2008, numerous indicators suggest the “bear market” has only just begun. While this does NOT rule out a fairly strong reflexive rally, it suggests that any rally will ultimately fail as the bear market completes its cycle.

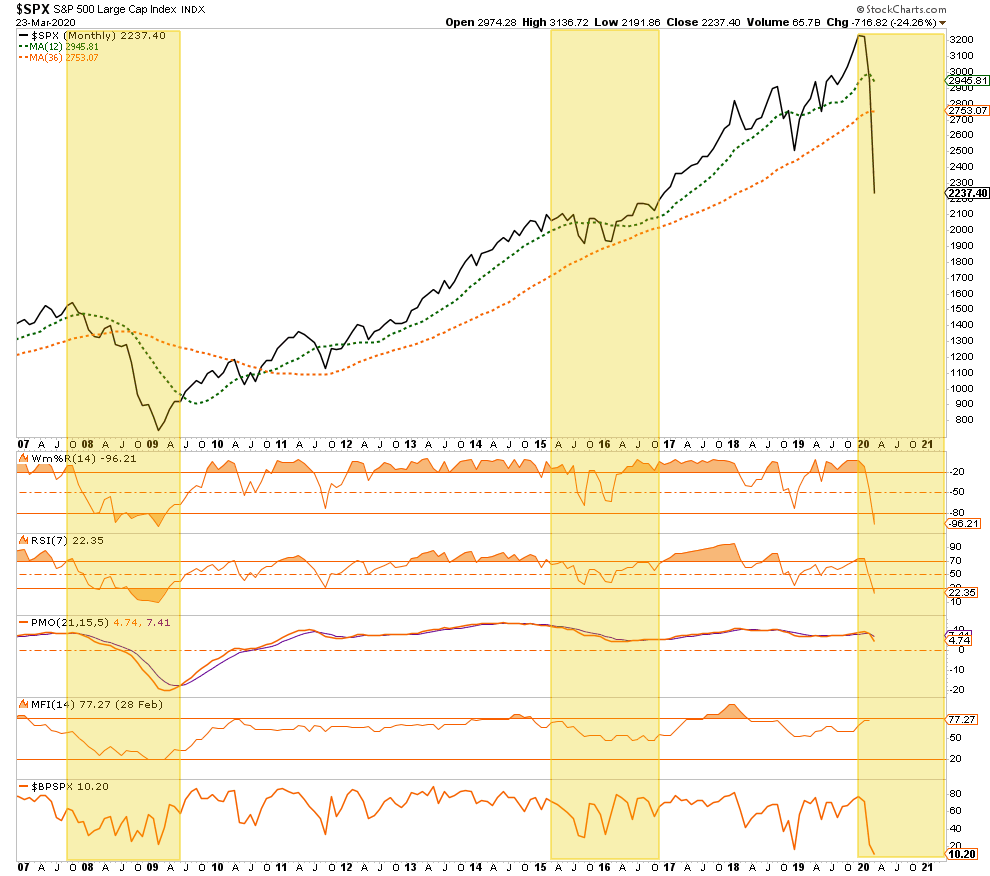

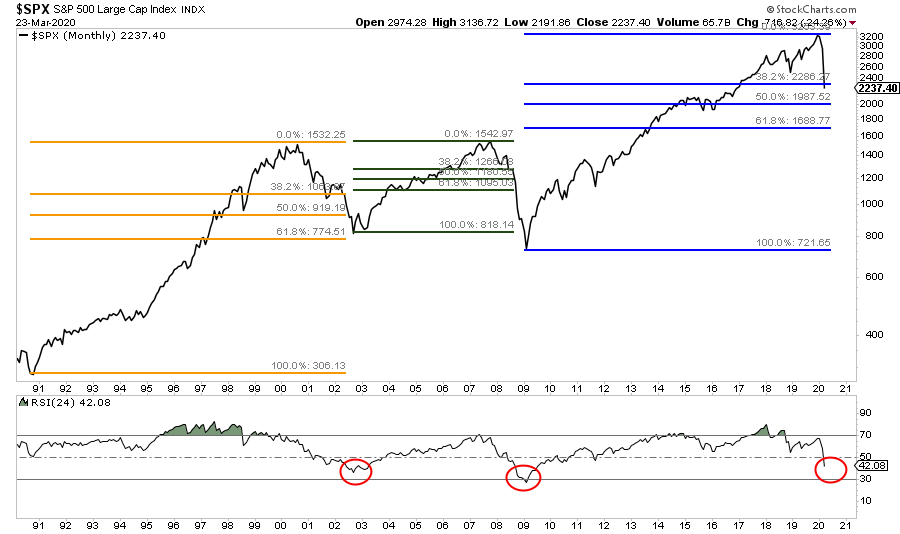

This can be seen more clearly in the monthly chart below, which looks at both previous bull and bear markets using a Fibonacci retracement. As shown, from the peak of both previous bull market “bubbles,” the market reversed 61.8% of the advance during the “Dot.com” crash, and more than 100% of the advance during the “Financial Crisis.”

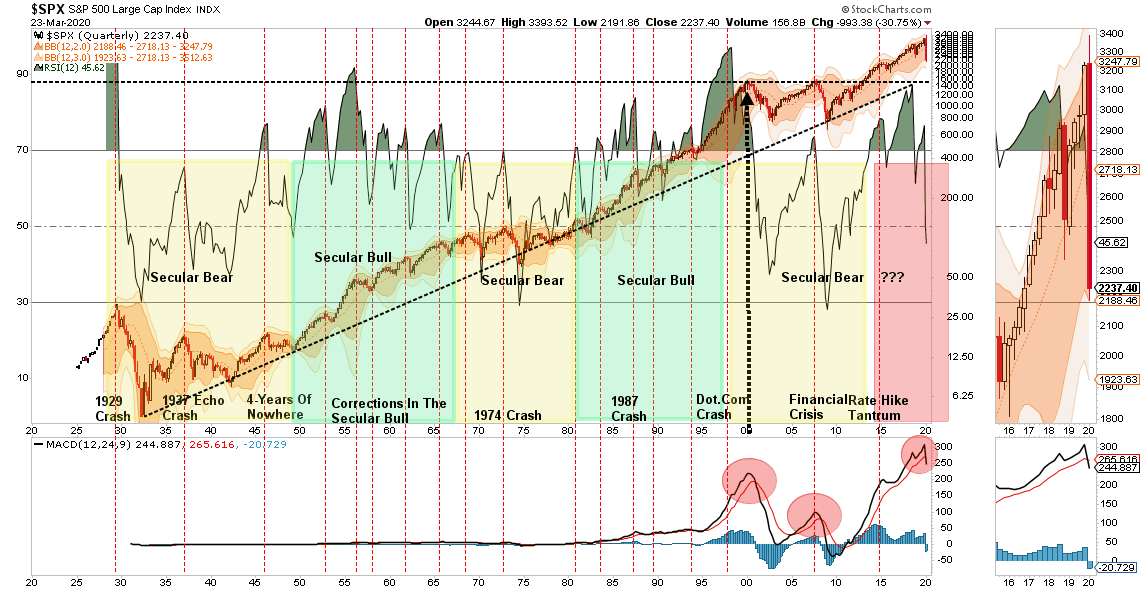

Given the current bull market cycle was longer, more levered, and more extended than both previous bull markets, a 38.2% decline is unlikely to fulfill the requirements of this reversion. Our ultimate target of 1600-1800 on the S&P 500 remains confirmed by the quarterly chart below.

The current correction process has only just triggered a quarterly sell signal combined with a break from an extreme deviation of the long-term bull-trend back to the 1930’s. Both previous bull market peaks coincide with the long-term bull trend at about 1600 on the S&P currently. Given all the stimulus being infused into the markets currently, we broaden our bear market bottom target to 1600-1800, as noted.

The technical signals, which do indeed lag short-term turns in the market, all confirm the “bear market” is only just awakening. While bullish reflexive rallies are very likely, and should be used to your advantage, this is a “traders” market for the time being.

In other words, the new mantra for the market, for the time being, will be to “Sell Rallies” rather than “Buy The Dip.”

As I have noted many times previously:

“This ‘time is not different,’ and there will be few investors that truly have the fortitude to ‘ride out’ the next decline.

Everyone eventually sells. The only difference is ‘selling when you want to,’ versus ‘selling when you have to.’”

Yes, the market will rally, and likely substantially so. Just don’t forget to take action, make changes, and get on the right side of the trade, before the “bear returns.”

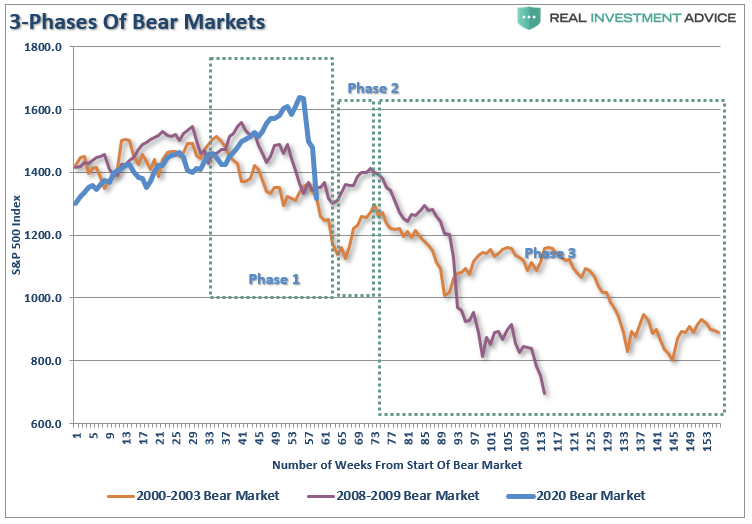

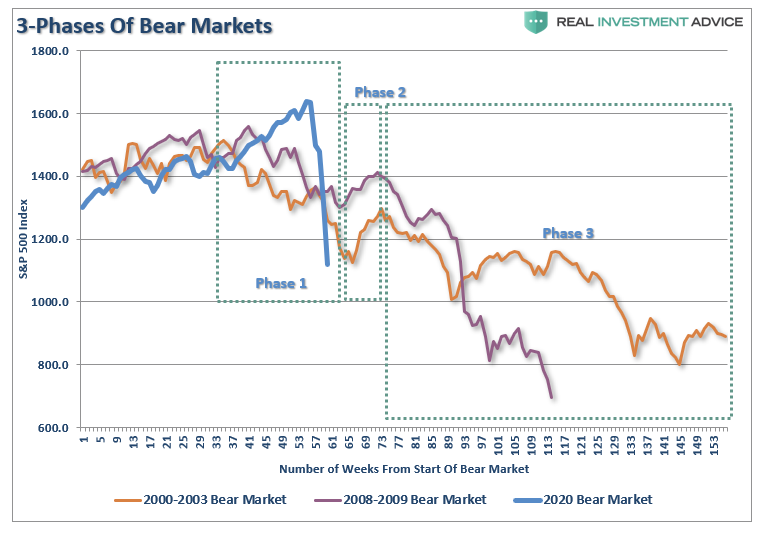

Bear markets have three stages – sharp down, reflexive rebound and a drawn-out fundamental downtrend

Bear markets often START with a sharp and swift decline.

After this decline, there is an oversold bounce that retraces a portion of that decline.

The longer-term decline then continues, at a slower and more grinding pace, as the fundamentals deteriorate.

Dow Theory also suggests that bear markets consist of three down legs with reflexive rebounds in between.

The chart above shows the stages of the last two primary cyclical bear markets versus today (the 2020 scale has been adjusted to match.)

As would be expected, the “Phase 1” selloff has been brutal.

That selloff sets up a “reflexive bounce.” For many individuals, they will “feel like” they are “safe.” This is how “bear market rallies” lure investors back in just before they are mauled again in “Phase 3.”

Just like in 2000, and 2008, the media/Wall Street will be telling you to just “hold on.” Unfortunately, by the time “Phase 3” was finished, there was no one wanting to “buy” anything.

America: WILL WE FINALLY LEARN A LESSON?

“Much of what passes for orthodoxy in economics and finance proves, on closer examination, to be shaky business.” The Misbehavior of Markets – by Benoit Mandelbrot & Richard L. Hudson.

If as households we do crumble financially yet another time, will this ‘outlier’ event finally teach us a valuable lesson? One we’ll never forget (again)? I mean, how many Black Swans or events that create wholesale economic and financial devastation must we endure to work diligently, effortlessly, to shore up our family’s finances?

Unfortunately, as humans, we focus on risk and financial stability too late. Always. Too. Late. We are creatures of complacency and mainstream financial advice does nothing but fuel our overconfidence bias. Only when a storm is upon us, wreaking havoc, do we seek to board the windows and secure what’s important to us.

We’re cajoled by ‘experts’ during good times. We’re taught how outlier events occur every 1,000 years. Strange how rare occurrences aren’t so rare. They seem to happen every decade. So, let me ask you – How many times do these so-called ‘rare’ events need to occur before fiscal discipline becomes a priority for all of us?

Over the last three years, at RIA we have created several financial tenets to guard against financial vulnerability. I don’t mean to preach; I mean to teach.

I hope over the next few years, once this pandemic is past and we rummage through the economic rubble, we’ll take it upon ourselves to remain vigilant through the complacency and take the following rules to heart.

1. A painful reminder about the ‘buy and hold’ investment philosophy or whatever horrid expletive you’re probably calling it right now.

Never forget that convincing words, piles of academic studies and mined data from big-box financial retailers in pretty packages make it easy to share convincing stories to push stocks. Hopefully, investors who spent most of their time and money getting back to even remain comforted by the narratives. They’ll now do it again.

I’ll admit – I’m nonplussed by the appeal of buy-and-hold to the purists. I truly envy them.

It seems to be a “What Me Worry?” kind of existence. There seems to be an eerie comfort to throwing money into a black hole of overvalued investments and hoping that it transforms into a white light of wealth 20 years down the road (even if it’s a very dim bulb). I truly wish I could be convinced that a blind buy-and-hold fable is truth.

I so passionately want investors to achieve returns and exceed their financial life benchmarks or goals; it’s good for me too. I also would like to minimize the damage from bears. Is that too much to ask?

At Real Investment Advice we think it’s one of a money manager’s primary responsibilities.

Buy-and-hold at the core wrapped in rules of risk management is a healthy, long-term strategy to build and protect wealth. That’s what we’re doing at this juncture.

If you’re completely out of the market for an extended period, I mean zilch, zero, then stock investing may not be appropriate for you. Hey, it isn’t for everyone, especially today when the flood of central bank liquidity (I’ve never witnessed anything like it), algos (the robots), probably $4 trillion in fiscal stimulus coming, tries to stem the devastation. The bull market is dead, a bear is tricky to navigate. I am grateful to be a partner at a firm where all members understand the devastation of bear markets and are not ‘deer in headlights’ as this crisis is upon us. Take heart – the bear will die; the bull will run again. As investors we will bleed. The key is not to hemorrhage. There is a difference.

It’s not too late to undertake a quick gut check – Realize that an allocation of 10-20% to domestic and international stocks can drop 40% on average in bear markets. Investors fail to realize that diversifying between foreign and U.S. stocks doesn’t manage the risk they care about most – risk of principal loss. We are witnessing this now – one more time on the disaster hit parade. The world has become increasingly an Irwin Allen (The Poseidon Adventure; The Towering Inferno), film and we are the actors.

Let’s say your retirement plan balance is $90,000. In a conservative allocation, $18,000 (20%), may be allocated to stocks. If a bear cycle takes the stock balance down to $10,800 and makes you a bit queasy, then certainly the market doesn’t fit into your overall investment philosophy.

If you do have the intestinal fortitude to maintain an allocation to stocks, your financial partner is a buy-and-hold zealot (highly likely), and you haven’t taken profits (a tenet of risk management) or rebalanced this year, then there’s still an opportunity to do so on rallies. It’s acceptable to maintain additional cash as much as buy-and-hold purists abhor cash.

You’re not the ‘idiot’ who sells at the bottom just because you adhere to rules of risk management.

Granted, investors can be their worst emotional enemies. If risk management rules are employed as an integration to an overall investment process, then selling at the very bottom may be avoided. From my experience, the dumbest actions of those who did sell at the bottom in March 2009, rest almost solely on their brokers.

You see, if financial professionals would have empathized with their clients and took enough (any) action to preserve capital as clients were calling with concern in late 2007, maybe, just maybe, those distressed investors wouldn’t have sold out of everything pretty much at the bottom.

The advice “not to worry, markets always come back,” regurgitated repeatedly did nothing to allay concerns; frankly hollow words made brokers appear as if they employed market blinders or were in a state of denial. They appeared ignorant, not aware of the severity of the crisis.

I listened enough to begin surgically trimming positions (I explained to clients we sought to take a scalpel, not a machete to reducing stock exposure in portfolios), and was proactive to sell clients out of a Charles Schwab bond fund described as “stable in price,” an “alternative to cash,” in November 2007 when the mutual fund share price was doing nothing but faltering.

Although Schwab portfolio management assured us in the field repeatedly that there was “nothing wrong with the fund,” and it wasn’t suffering mass redemptions, it did eventually go bust and Schwab was held accountable for lack of oversight.

Unfortunately, the company got off easy as the settlement with the SEC was nothing but a financial slap on the wrist when the fund held $13.5 billion at its peak.

You tell me this stuff isn’t rigged against retail investors? I believe differently. I always will.

Proactive behavior allowed me to maintain a semblance of stock ownership and then begin to increase exposure through the summer of 2009. I deemed it buy-and-hold with a “protective twist.”

If your broker isn’t actively listening and is discounting concerns, it’s time to replace him or her. Answers received should be thorough and backed by analysis.

If you must invest today, consider dollar-cost averaging.

Usually, dollar-cost averaging where you add a fixed dollar amount to variable investments on a regular schedule, underperforms value or lump-sum investing. Unless the cyclically adjusted price-to-earnings ratio or CAPE exceeds 18.6 (today, it exceeds 25).

The other side of the coin of buy-and-hold isn’t active trading.

Cop out. Lame excuse. I can’t be clearer. Not only are you branded a ‘bear’ if you employ a sell discipline, it appears that the buy-and-hold purists can’t think outside of extremes. They tend to associate selling with active trading. It’s a clever ploy designed to avoid the conversation or even the thought of a sell process. It’s just impossible.

Not it isn’t. And it isn’t active trading either. Active trading isn’t going to generate returns, just activity. Plus, if you consider that trades cost ZERO at most big-box financial retailers, transaction costs aren’t a concern anymore.

For years, the investment industry has tried to scare clients into staying fully invested in the stock market, no matter how high stocks go or what’s going on in the economy. Investors are repeatedly warned that doing anything otherwise is simply foolish because “you can’t time the market.”

Here’s why per Lance Roberts:

“Wall Street firms, despite what the media advertising tells you, are businesses. As a business, their job is to develop and deliver products to investors in whatever form investor appetites demand…Wall Street is always happy to provide ‘products’ to the consumers they serve.

As Wall Street quickly figured out that it was far more lucrative to collect ongoing fees rather than a one-time trading commission…The mutual fund business was booming, and business was ‘brisk’ on Wall Street as profits surged.”

I’ll add:

Frankly, it’s too much work. Financial experts are primarily peddlers of managed products. They’re hired to regurgitate sell-side biased data mined from their employer’s research department. What they’re implying is they’re too busy meeting sales goals to consider risk management (the way you define it as an investor), important.

With that being said, consider other rules to protect your household for when the next ‘outlier’ event occurs (I mean, after this one).

2. The FVC – The Financial Vulnerability Cushion.

The main purpose of the Financial Vulnerability Cushion is to fortify the foundation of a financial house. You’ve heard about maintaining three to six months of living expenses in cash for emergencies. Well, define an emergency. The car breaks down, sure. The A/C goes out? Right. Expenses such as these fit well into a three to six-month cash cushion. However, Black Swan events remind us this cushion isn’t enough. We must finally learn to separate emergency from crisis.

Over the last six months we’ve been discussing on the radio how important it is to build a cash war chest of one to two years’ worth of living expenses and maintain it above everything else. These reserves are for crisis. A sudden job loss; major illness. Unfortunately, millions will be out of work here. Some, long term. I’m increasingly concerned about those who work in the energy sector. Never forget. Don’t listen to mainstream financial media again. Remember this time and work diligently to build a FVC.

3. Create financial rules around debt control and savings. Then stick to them. No matter what. Good times or bad.

Consider strict debt management and savings habits as the blend of robust soil which allows opportunities to be realized. Excessive debt and limited ability to buffer against financial emergencies and crisis can limit a person’s ability to take on riskier but rewarding ventures like career change, entrepreneurial endeavors and risks that may lead to significant, long-term wealth.

Student loan debt: Limited to one year’s worth of total expense, tuition, room & board, expenses.

Personal, unsecured debt (credit card, auto): No more than 25% of gross monthly household income.

4. Be smarter with credit.

Today, credit cards are used for various reasons – convenience, cash back, travel reward points and the most unfortunate, to meet ongoing living expenses in the face of structural wage stagnation. So, consider the following.

Credit Card Debt = No greater than 4% of monthly gross income.

If your household gross income is $50,000 then credit card debt shouldn’t exceed $2,000. Per WalletHub, Texas ranks 46 with $2,848 in average credit card debt.

Survival tip: Take control of your money. Contact your credit card provider today and request a lower interest rate, perhaps the favorable balance transfer rate along with delayed payments. We are in this catastrophe together and it’s the least they can do for at least the rest of the year.

Car Loan Debt-to-Income Ratio:

Cars are required like breathing here in Houston and Texas, overall. However, they are not investments. Their values do not appreciate. If anything, auto values decrease as soon as you drive away from the dealership.

Car Loan Obligation = No greater than 25% of monthly gross income.

For example, a household bringing in $60,000 a year shouldn’t have more than $15,000 in outstanding auto loan debt. In my household, the ratio is less than 10%. I drive a Toyota RAV4. Put your ego aside; consider reliability first.

As I complete interviews with media and news outlets in Houston and across the country, my heart is overwhelmed with sorrow for those who are suffering through this, yet another ‘rare’ historical episode.

Please reach out to our team with questions and for guidance.

Every question is a good question.

Never be afraid to ask.

Everyone Wanting To Buy Suggests The Bear Still Prowls (Full Report)

Everyone Wanting To Buy Suggests The Bear Still Prowls

NOTE: During these tumultuous times, we are unlocking our full newsletter to help you navigate the markets safely. Make sure you subscribe to RIAPRO.NET (Free 30-Day Trial) if you want to keep receiving the full report after the storm passes.

Everyone Wanting To Buy Suggests The Bear Still Prowls

“If you own 10% equities, as we do, and the market falls 100%, you will lose 10%. That said, you have 90 cents on the dollar to buy equities for free.” – Michael Lebowitz

For the last several months, we have been issuing repeated warnings about the market. While such comments are often mistaken for “being bearish,” we have often stated it is our process of managing “risk,” which is most important.

Beginning in mid-January, we began taking profits out of our portfolios and reducing risk. To wit:

‘On Friday, we began the orderly process of reducing exposure in our portfolios to take in profits, reduce portfolio risk, and raise cash levels.’

Importantly, we did not ‘sell everything’ and go to cash.

Since then, we took profits and rebalanced risk again in late January and early February as well.

On Friday/Monday, our ‘limits’ were breached, which required us to sell more.”

There are a couple of important things to understand about our current equity exposure.

To begin with, we never go to 100% cash. The reason is that “psychologically” it is too difficult for clients to start “buying” when the market finally bottoms. Seeing the market begin to recover, along with their portfolio, makes it easier to fight the fear the market is “going to zero.”

Secondly, and most importantly, at just 10% in current equity exposure, the market could literally fall 100% and our portfolios would only decline by 10%.(Of course, given we still have 90% of our capital left, we can buy a tremendous amount of “free assets.”)

Of course, the market isn’t going to zero.

However, let’s map out a more realistic example.

In this week’s MacroView, we discussed the “valuation” issue

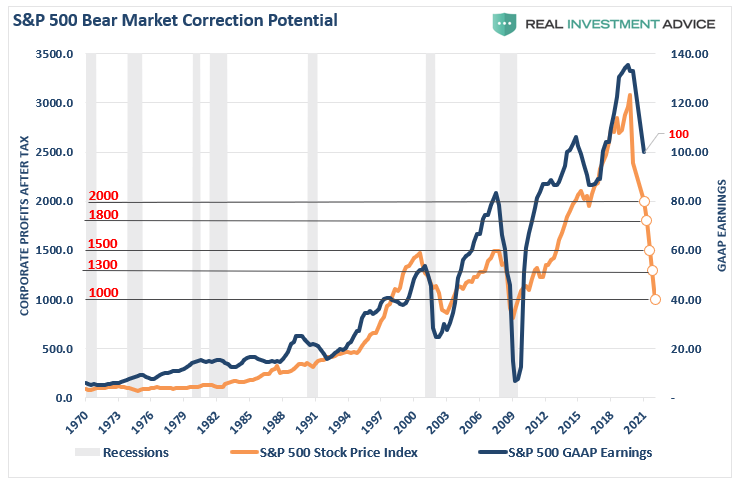

“If our, and Mr. Rosenberg’s, estimates are correct of a 5-8% recessionary drag in the second quarter of 2020, then an average reduction in earnings of 30% is most likely overly optimistic.

However, here is the math:

Current Earnings = 132.90

30% Reduction = $100 (rounding down for easier math)

At various P/E multiples, we can predict where “fair value” for the market is based on historical assumptions:

20x earnings: Historically high but markets have traded at high valuations for the last decade.

18x earnings: Still historically high.

15x earnings: Long-Term Average

13x earnings: Undervalued

10x earnings: Extremely undervalued but aligned with secular bear market bottoms.

You can pick your own level where you think P/E’s will account for the global recession but the chart below prices it into the market.”

So, let’s assume our numbers are optimistically in the “ballpark” of a valuation reversion, and earnings are only cut by 30% while the market bottoms at 1800, or 18x earnings.(I say optimistically because normal valuation reversions are 15x earnings or less.)

Here’s the math:

For a “buy and hold” investor (who is already down 20-30% from the peak)will lose an additional 22%.

For a client with 10% equity exposure, they will lose an additional 2.2%.

When the market does eventually bottom, and it will, it will be far easier for our clients to recover 10% of their portfolio versus 50% for most “buy and hold” strategies.

As we have often stated, “getting back to even is not an investment strategy.”

Is The Bear Market Over?

This is THE QUESTION for investors. Here are a few articles from the past couple of days:

Bear markets have three stages – sharp down, reflexive rebound and a drawn-out fundamental downtrend – Rule #8

Bear markets often START with a sharp and swift decline.

After this decline, there is an oversold bounce that retraces a portion of that decline.

The longer-term decline then continues, at a slower and more grinding pace, as the fundamentals deteriorate.

Dow Theory also suggests that bear markets consist of three down legs with reflexive rebounds in between.

The chart above shows the stages of the last two primary cyclical bear markets versus today (the 2020 scale has been adjusted to match.)

The answer to the question is simply this:

“When is it time to start buying the market? When you do NOT want to.”

Bond Market Implosion

At the moment, the Federal Reserve is fighting a potentially losing battle – the bond market.

After cutting rates to zero and launching QE of $700 billion – the markets crashed.

The ECB starts an $800 billion QE program, and the markets fail to move.

The Fed injected liquidity into money markets, the credit market, and is buying municipal bonds.

And the market crashed more.

The Fed has literally turned on a “garden hose” to extinguish a literal “bon(d)fire.”

This was no more evident than their action this past week to revive a program from the financial crisis called the Primary Dealer Credit Facility (PDCF) to bailout hedge funds and banks. Via Mike Witney:

“The Fed is reopening its most controversial and despised crisis-era bailout facility, the Primary Dealer Credit Facility. The facility’s real purpose is to transfer the toxic bonds and securities from failing financial institutions and corporations (through an intermediary) onto the Fed’s balance sheet.

The objective of this sleight of hand is to recapitalize big investors who, through their own bad bets, are now either underwater or in deep trouble. Just like 2008, the Fed is now doing everything in its power to save its friends and mop up the ocean of red ink that was generated during the 10-year orgy of speculation that has ended in crashing markets and a wave of deflation. Check out this excerpt from an article at Wall Street on Parade. Here’s an excerpt:

“Veterans on Wall Street think of the PDCF as the cash-for-trash facility, where Wall Street’s toxic waste from a decade of irresponsible trading and lending, will be purged from the balance sheets of the Wall Street firms and handed over to the balance sheet of the Federal Reserve – just as it was during the last financial crisis on Wall Street.”

In other words, the PDCF is a landfill for distressed assets that have lost much of their value and for which there is little or no demand. And, as bad as that sounds, the details about the resuscitated PDCF are much worse.”

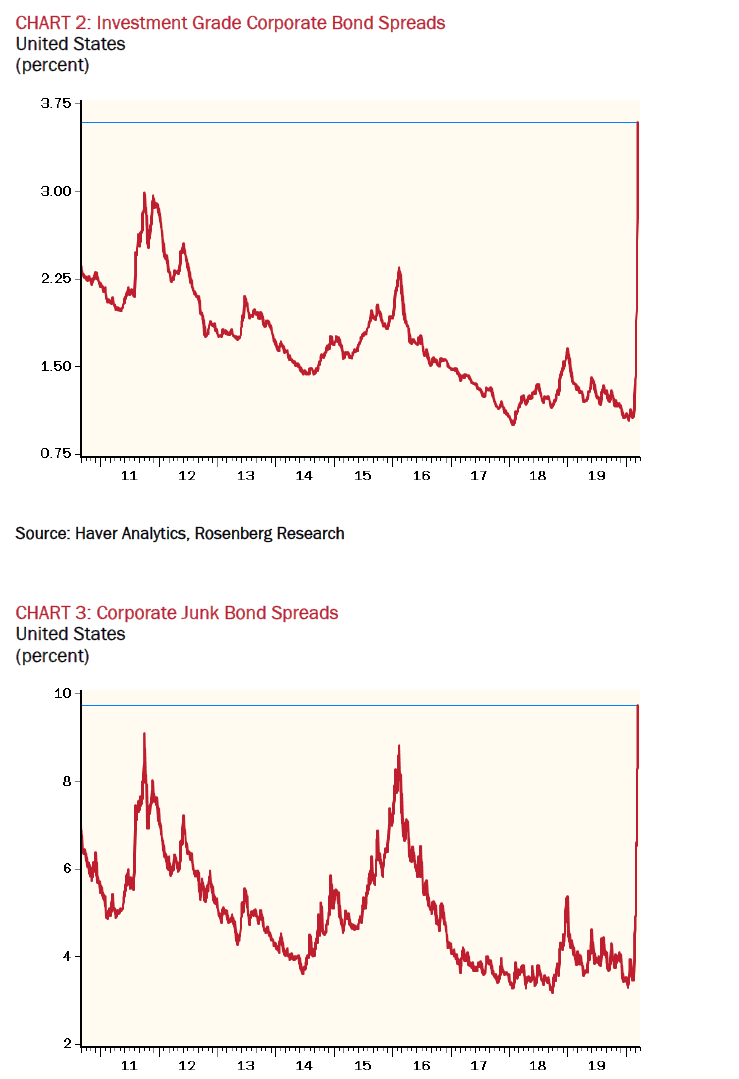

If you have any doubt how bad it is in the bond market, just take a look at what happened to both investment grade and junk bond spreads. (Charts courtesy of David Rosenberg)

As they say: “That clearly ain’t normal.”

More importantly, the “Bear Market” won’t be over until the credit markets get fixed.

Hunting The Bear

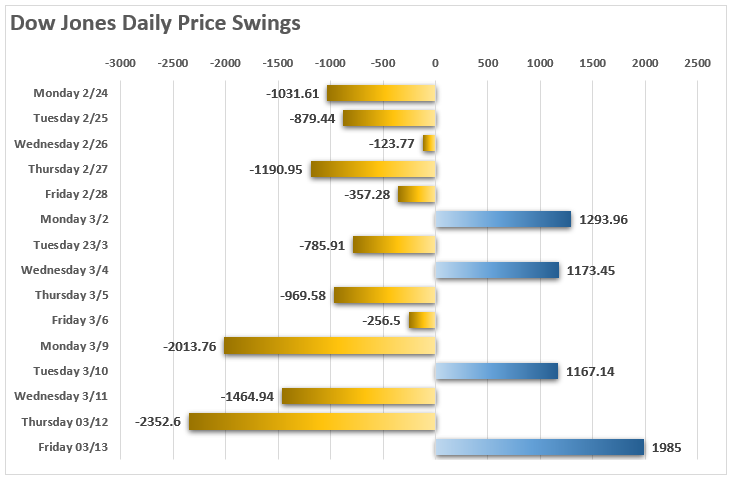

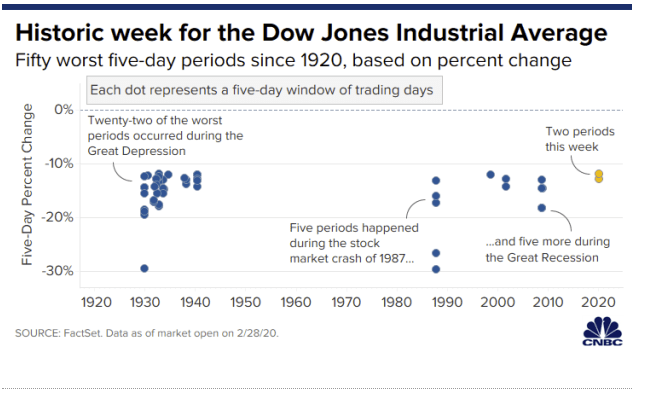

It was a pretty stunning week in the market. Over the last 5-days, the market declined an astonishing, or should I say breathtaking, 15%. The last time we saw a one week decline of that magnitude was during the “Lehman” crisis. (Of course, with hedge funds blowing up all week, this is precisely what the Fed has been bailing out.)

Since the peak of the market at the end of February, the market is now down a whopping 32%.

Surely, we are close to a bottom?

Let’s revisit our daily and weekly charts for some clues as to where we are, what could happen next, and what actions to take.

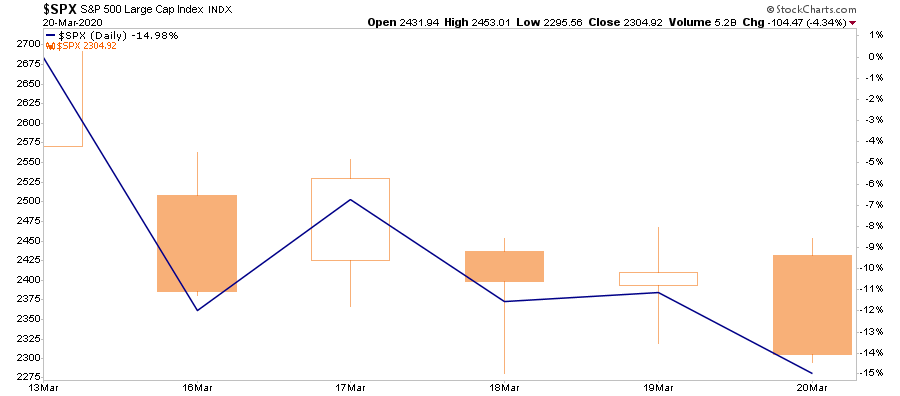

On a daily basis, the market is extremely stretched and deviated to the downside. Friday’s selloff smacked of an “Oriental Rug Company” where it was an “Everything Must Go Liquidation Event.”

Remember all those headlines from early this year:

Well….

This selloff completely reversed the entire advance from the 2018 lows. That’s the bad news.

The good news is the markets are now more extremely oversold on a variety of measures than at just about any other point in history.

Such a reversal, particularly given the “speed and magnitude” of the decline, argues for a “reversal” of some sort.

Warning: Any reversal will NOT BE the bear market bottom. It will be a “bear market” rally you will want to “sell” into. The reason is there are still many investors trapped in “buy and hold” and “passive indexing” strategies which are actively seeking an exit. Any rallies will be met with redemptions.

As noted above, bear markets do not end with investors wanting to “buy” the market. They end when “everyone wants to sell.”

And, NO, investors are “not different this time.”

This “bear market” rally scenario becomes more evident when we view our longer-term weekly “sell signals.” As we warned last week: