Over the last two weeks, the U.S. dollar index has risen by 6%. That may not seem like much to investors who are watching stocks rise and fall by that amount, and even more daily or bond yields falling in half and then doubling, but trust us; it is.

The dollar is unlike any other asset because it is the world’s reserve currency. When a Canadian tire company buys rubber from a Philippine rubber company, the payment occurs in U.S. dollars. Both countries have their own currencies, but neither currency has the liquidity, deep credit markets, and quite frankly, the world’s largest economy and military power backing it.

Because so many foreign countries and companies transact with dollars, they need to borrow in dollars, despite the fact their revenue is often not in dollars. This creates a mismatch between revenues and expenses as currency values fluctuate. If the mismatch is not hedged, as is frequently the case, foreign borrowers of U.S. dollars are subject to higher borrowing costs if the dollar rises versus their local currency. Simply the local currency depreciates versus the dollar; therefore, they need more of the local currency to make good on their debt. Because of this construct, a stronger dollar is effectively a tightening of financial conditions on the rest of the world.

This is what is occurring today as the virus is severely impacting the global economy. Revenues are deteriorating and the cost of dollar-denominated foreign debt is rising rapidly. As borrowers scramble to raise more dollars to meet their obligations, the situation worsens as the demand for dollars forces the dollar higher. In layman’s terms, there is a global run on the dollar and, in circular fashion, the run is pushing the dollar higher. Either the global economy will break or the dollar. Right now it seems that despite massive liquidity from the Fed the dollar does not want to back down.

How Far Can Stocks Fall?

The question repeatedly asked of us last week is how much more can the stock market fall? We don’t have a crystal ball and we cannot predict the future but we can take steps to prepare for it. Our analysis and understanding of history allow us to use many different fundamental and technical models to create a broad range of possible answers to the question. With that range of potential outcomes we adjust our risk tolerance as appropriate.

For example, in our daily series of RIA Pro charts and the weekly Newsletter, we lay out key technical, sentiment, and momentum measures for many markets, sectors, and stocks. In doing so, we provide a range of potential shorter-term outcomes. We also depend on feedback from other reliable independent services such as Brett Freeze at Global Technical Analysis. His work is exclusively and routinely featured every month in Cartography Corner on RIA Pro.

In this article, we move beyond technical analysis and share a simple fundamental valuation analysis to help provide more guidance as to where the market may trade in the coming months and even years. This analysis can be viewed as bullish or bearish. Our goal is not to persuade you towards one direction or the other, but to open your eyes to the wide range of possibilities.

CAPE

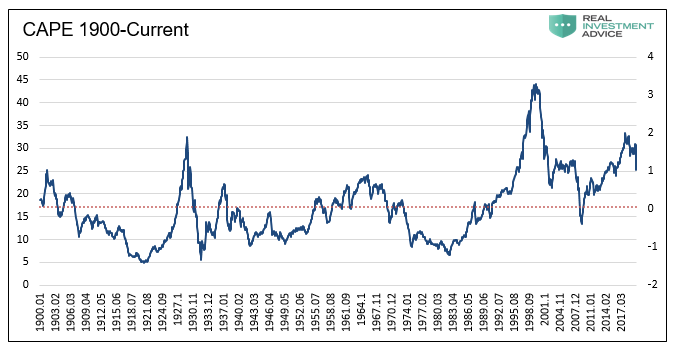

The data employed in this analysis is as of the market close on March 13, 2020.

Shiller’s Cyclically Adjusted Price to Earnings (CAPE 10) is one of our preferred valuation measures. Robert Shiller developed the CAPE 10 model to help investors assess valuations based on dependable, longer-term earnings trends. The most common CAPE analysis uses ten years of earnings data. The period is not too sensitive to transitory gyrations in earnings and it frequently includes a full economic cycle.

As shown below, monthly readings of CAPE fluctuate around the historical average (dotted line). The variance of valuations around the mean is put into further context with the right side y-axis, which shows how many sigma’s (standard deviations) each reading is from the average. The current CAPE of 25.36, or +1.10 sigma’s from the mean.

Data Courtesy Robert Shiller

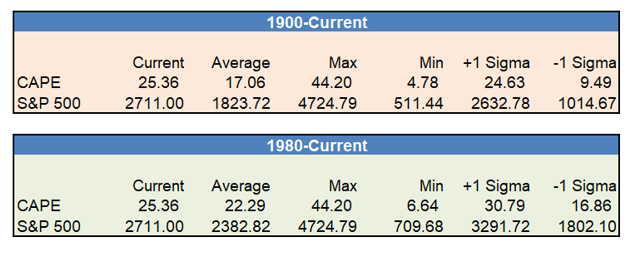

The average CAPE over the 120+ years is 17.06, the maximum was 44.20, and the minimum was 4.78.

If we use more recent data, say from 1980 to current, the average CAPE is 22.29. Due to the higher average over the period, which includes the late 90s dot com bubble and the housing bubble, the current reading is only .36 sigma’s above its average.

The following tables, using both time frames, provide price guidance based on where the S&P 500 would need to be if CAPE were to move to its average, maximum, and minimum, as well as plus or minus one sigma from the mean.

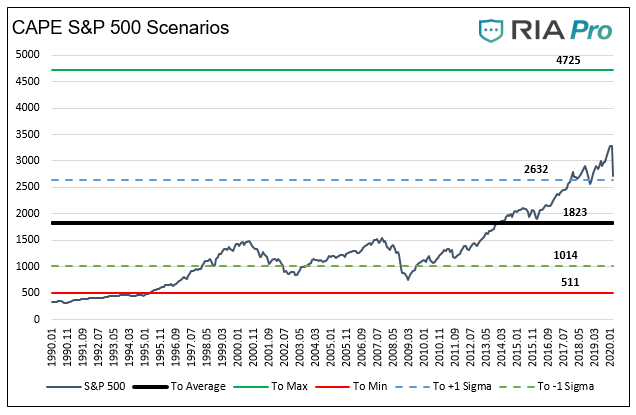

The graph below shows the S&P 500 price in relation to that which would occur if the CAPE ratio went to its average, maximum, minimum, and plus or minus one sigma from the last 120 years.

It is important to stress that the denominator, earnings, includes data from March 2010 to February 2020. That ten years did not include a recession, which, over the 120+ years in this analysis, only happened briefly one other time, the late 1990’s.

The Corona Virus will no doubt hurt earnings for at least a few quarters and could push the economy into a recession. Accordingly, the denominator in CAPE will likely be declining. Whether or not CAPE rises for falls depends on the price action of the index.

Summary

Stocks are not cheap. As shown, a reversion to the average of the last 120 years, would result in an additional 33% decline from current levels. While the massive range of outcomes may appear daunting, this analysis is designed to help better understand the bounds of the market.

The S&P 500 certainly has room to trade much lower. It can also double in price and stay within the bounds of history. Lastly, given the unprecedented nature of current circumstances, it may be different this time and write new history.

McDonald’s, Not A Shelter In The Coming Storm

The amount

of time and effort that investors spend assessing the risks versus the potential

returns of their portfolio should shift as the economy and markets cycle over

time. For example, when an economic recovery finally breaks the grip of a

recession, and asset prices and valuations have fallen to average or below-average

levels, price and economic risks are greatly diminished. That is not to say

there is no risk, just less risk.

Market and

economic troughs are akin to the aftermath of a forest fire. After a fire has

ravaged a forest, the risks for another fire are not zero, but they are below

average. Counter-intuitively, it is at these points in time when people are

most fearful of fire or, in the case of investing, most worried about losses. With

reduced risks, investors during these times should be more focused on the better

than average rewards offered by the markets and not as concerned with the risks

entailed in reaping those rewards.

Conversely,

in the ninth inning of a bull market when valuations are well above the norm, and

the economy has expanded for a long period, investors need to shift focus

heavily to the potential risks. That is not to say there are no more rewards to

come, but the overwhelming risks are substantial, and they can result in a permanent

loss of wealth. As human beings are prone to do, we often zig when we should

zag.

In January,

we wrote Gimme Shelter to highlight that risk can be hard to detect. Sure, high flying companies with

massive price gains and repeated net losses like Tesla or Netflix are easy to

spot. More difficult, though, are those tried and true value stocks of

companies that have flourished for decades. Specifically, we provided readers

with an in-depth analysis of Coca-Cola (KO). While KO is a name brand known

around the world with a long record of dependable earnings growth, its stock price

has greatly exceeded its fair value.

We did not

say that KO is a sure-fire short sale or even a sell. Instead, we conveyed that

when a significant market drawdown occurs, KO has a lot more risk than is likely

perceived by most investors. Simply, it

is not the place investors should seek shelter in a market storm as they may

have in the past.

We now take

the opportunity to discuss another “value” company that many investors may consider

a stock market shelter or safe haven.

We follow in

this series with a review of McDonald’s (MCD).

You Deserve a Break Today

Please note the models and

computations employed in this series use earnings per share and net income.

Stock buybacks warp earnings per share (EPS), making earnings appear better than

they would have without buybacks. The more positive result is simply due to a

declining share count or denominator in the EPS equation. Net income and

revenue data are unaffected by share buybacks and therefore deliver a more accurate

appraisal of a company’s value.

Over the

last ten years, the price of MCD has grown at a 13% annual rate, more than double

its EPS, and over five times the rate of growth of its net income. The pace at

which the growth of its stock price has surpassed its fundamentals has

increased sharply over the last three years. During this period, the stock

price has increased 46% annually, which is almost four times its EPS growth and

more than six times the growth of its net income.

Of further

concern, revenues have declined 5% annually over the last three years,

and the most recently reported annual revenues are now less than they were ten

years ago when the U.S. and global GDP were only about 60% the size they are

today. To pile on, the amount of debt MCD has incurred over the last ten years

has increased by 355%.

MCD is a good company and, like KO, is one of the most well-known brands on the globe. Rated at BBB+, default or bankruptcy risk for MCD is remote, and because of its product line, it will probably see earnings hold up well during the next recession. For many, it is cheaper to eat at a McDonald’s restaurant than to cook at home. Although their operating business is valuable and dependable, those are not reasons to acquire or hold the stock. The issue is what price I am willing to pay in order to try to avoid a loss and secure a reasonable return.

Valuations

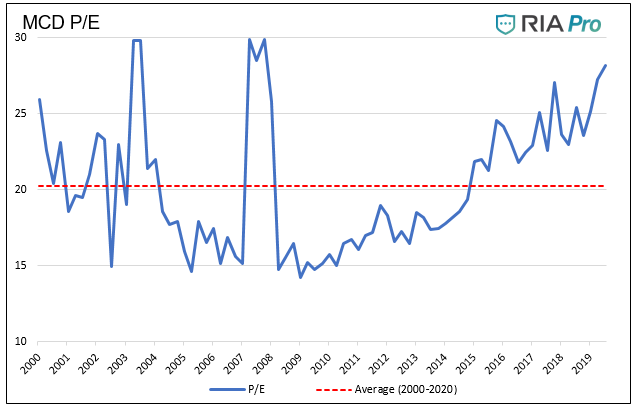

Using a simple price to earnings (P/E) valuation, as shown below, MCD’s current P/E for the trailing twelve months is 28, which is about 40% greater than its average over the last two decades.

The

following graphs, tables, and data use the same models and methods we used to evaluate

KO. For a further description, please read Gimme Shelter.

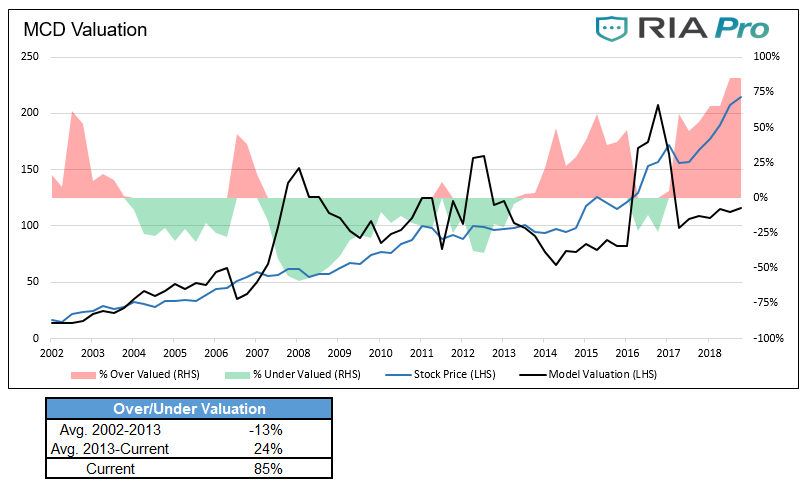

Currently, as shown below, MCD is trading 85% above its fair value using our earnings growth model. It is worth noting that MCD, as shown with green shading, was typically valued as cheap using this model. The table below the graph shows that, on average, from 2002-2013, the stock traded 13% below fair value.

We support the

graph and table above with a cash flow analysis. We assumed McDonald’s 5.6%

long-run income growth rate to forecast earnings for the next 30 years. When

these forecasted earnings are then discounted at the appropriate discounting

rate of 7%, representing longer-term equity returns, MCD is currently overvalued by 72%.

Lastly, as we did in Gimme Shelter, we asked our friend David Robertson from Arete Asset Management to evaluate MCD’s intrinsic value. His cash flow-based model assigns an intrinsic share price value of 97.27. Based on his work, MCD is currently overvalued by 124%.

Summary

Like KO, we

are not making a recommendation on MCD as a short or a sell candidate, but by

our analysis, MCD stock appears to be trading at a very high valuation. Much

of what we see in large-cap stocks today, MCD included, is being driven by

indiscriminate buying by passive investment funds. Such buying can certainly continue,

but at some point, the gross overvaluations will correct as all extremes do.

Even if MCD

were to “only” decline back to a normal valuation, the losses could be

significant and might even exceed those of the benchmark index, the S&P

500. Now consider that MCD may correct beyond the average and could once again

trade below fair value. Even assuming

MCD earnings are not hurt during a recession, the correction in its stock price

to more reasonable levels could be painful for shareholders.

Quick Take: The Great “Tesla” Hysteria Of 2020

“Let us see how high we can fly

before the sun melts the wax in our wings.” – E. O. Wilson

Since January 1, 2020, Tesla’s (TSLA) stock price has risen by $462 or 110%. TSLA’s market cap now exceeds every automaker except for Toyota. In fact, it exceeds not only the combined value of the “big three” automakers GM, Ford, and Chrysler/Fiat, but also companies like Charles Schwab, Target, Deere, Eli Lily, and Marriot to name a few large companies.

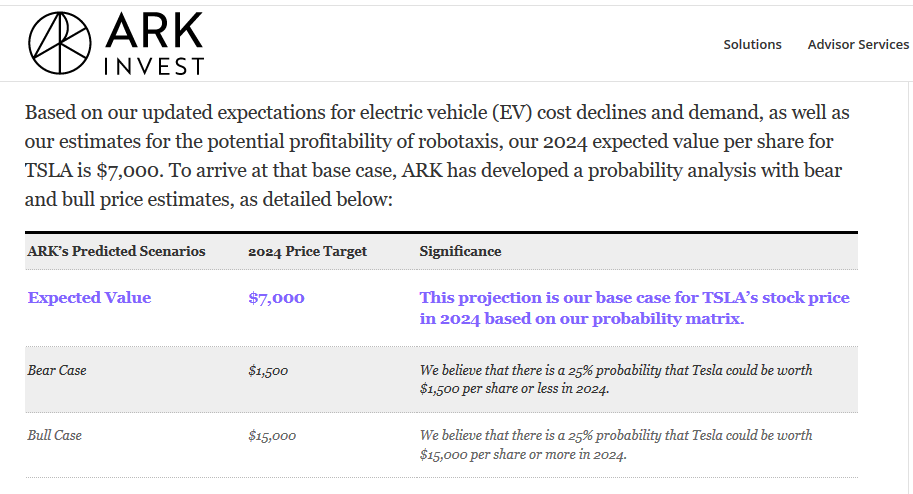

Seem crazy? Not as crazy as what comes next. Crazy are the expectations of Catherine Wood of ARK Invest. This well-known “disruptive innovation” based investor put out the following chart showing an expected price of $7,000 in 2024 with a $15,000 upside target.

Siren songs

such as the one shown above encourage investors to chase the stock higher with

reckless abandon, and maybe that is ARK’s intent. Given their large holding of

TSLA, it certainly makes more sense than their price targets. Instead of taking

her recommendations with blind faith, here are some statistics to illustrate

what is required for TSLA to reach such lofty goals.

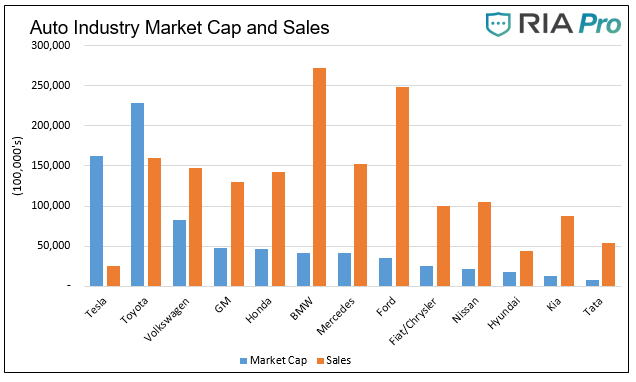

To start, let’s compare TSLA to their peer group, the auto industry. The chart below shows that TSLA has the second largest market cap in the auto industry, only behind Toyota. Despite the market cap, its sales are the lowest in the industry and by a lot. According to figures published on their website, TSLA sold 367,500 cars in 2019. General Motors sold 2.9 million and Ford sold 2.4 million.

Clearly investors

are betting on the future, so let’s put ARK’s forecast into context.

If the TSLA share price were to rise to their baseline forecast of 7,000, the market cap would increase to $1.26 trillion. Currently, the auto industry, as shown above, and including TSLA, aggregates to $772 billion. At the upside scenario of 15,000, the market cap of TSLA ($2.7 trillion) would be almost four times the current market cap of the entire auto industry. More stunning, it would be greater than the combined value of Apple and Microsoft.

Even if we make

the ridiculous assumption that TSLA will be the world’s only automaker, a price

of 15,000 still implies a valuation that is three to four times the current industry

average based on price to sales and price to earnings. At 7,000, its valuation

would be 1.6 times the industry average. Again,

and we stress, that is if TSLA is the world’s only automaker.

Summary

Tesla is one

of a few poster children for the latest surge in the current bull market. That

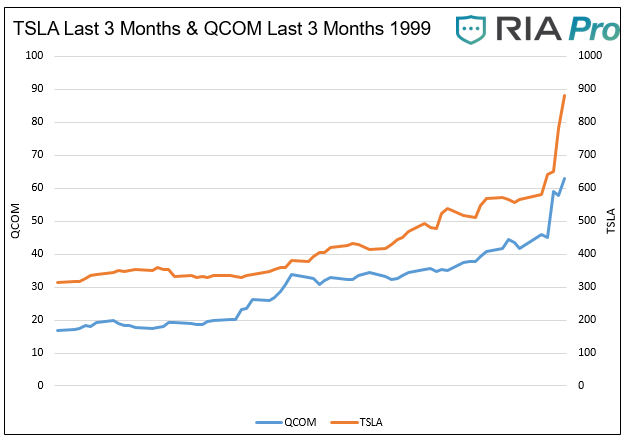

said, it’s worth remembering some examples from the past. For instance, Qualcomm

(QCOM) was a poster child for the tech boom in the late 1990s. Below is a chart

comparing the final surge in QCOM (Q4 1999) to the last three months of trading

for TSLA.

In the last quarter of 1999, QCOM’s price rose by 277%. TSLA is only up 181% in the last three months and may catch up to QCOM’s meteoric rise. However, if history is any guide, QCOM likely offers what a textbook example of a blow-off top is. By 2003 QCOM lost 90% of its value and would not recapture the 1999 highs for 15 years.

Tesla may be

the next great automaker and, in doing so, own a sizeable portion of market

share. However, to have estimates as high as those proposed by ARK, they must

be the only automaker and assume fantastic growth in the number of cars bought worldwide. Given their

technology is replicable and given the enormous incentives for competitors, we

not only find ARK’s wild forecast exceedingly optimistic, but we believe it is

already trading near a best-case scenario level.

One final

factor that ARK Invest also seems to have neglected is the risk of an economic

downturn. Although they do highlight a “Bear Case” price target of $1,500, that

too seems incoherent. Given that TSLA is still losing money and is also heavily

indebted, an economic slowdown would raise the risk of their demise. In such an

instance, TSLA would probably become the property of one of the major car

companies for less than $50 per share.

TSLA’s stock may run higher. Its price is now a function of all the key speculative ingredients – momentum, greed, FOMO, and of course, short covering. The sky always seems to be the limit in the short run, but as Icarus found out, be careful aiming for the sun.

**As we published the article Tesla was up 20% on the day. The one day jump raised their market cap by an amount greater than the respective market caps of KIA, Hyundai, Nissan, and Fiat/Chrysler!!

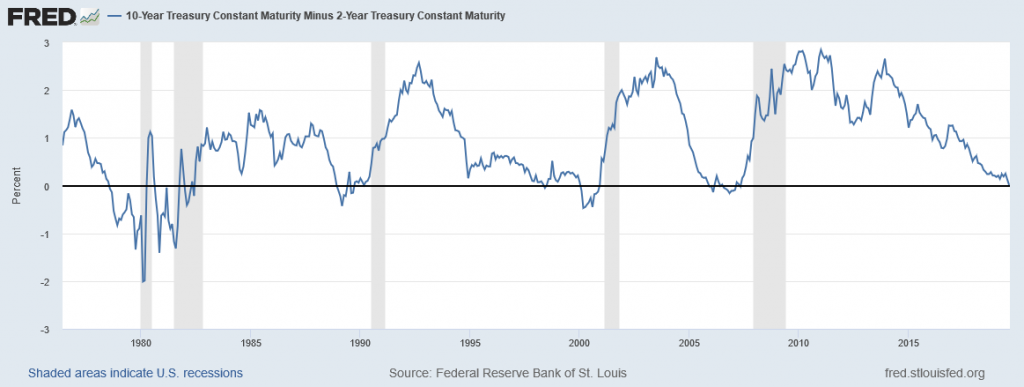

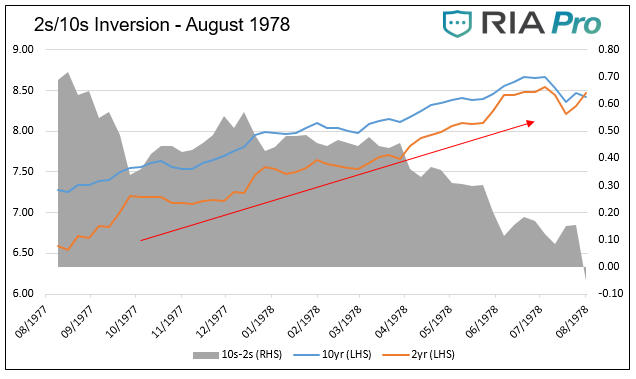

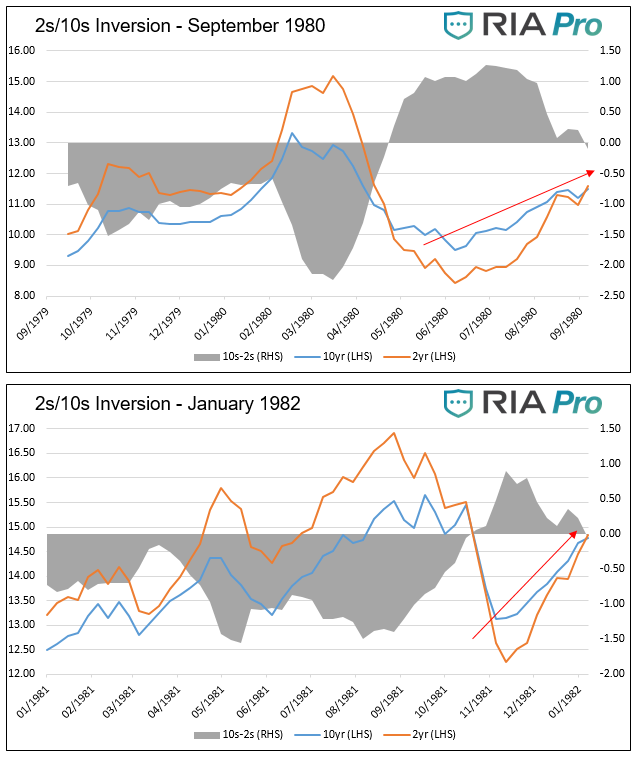

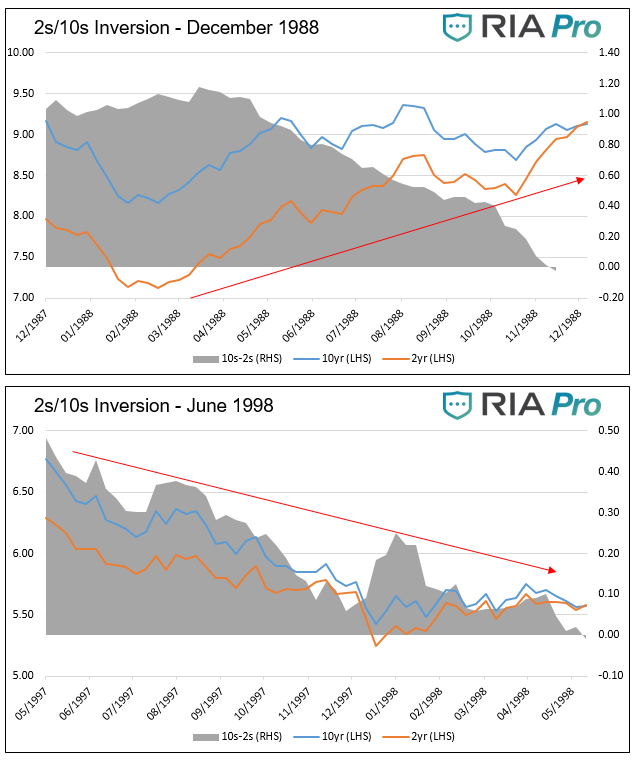

Comparing Yield Curves

Since August

of 1978, there have been seven instances where the yields on ten-year Treasury

Notes were lower than those on two-year Treasury Notes, commonly referred to as

“yield curve inversion.” That count includes the current episode which only

just occurred. In all six prior instances a recession followed, although in

some cases with a lag of up to two years.

Given the yield

curve’s impeccable 30+ year track record of signaling recessions, we think it

is appropriate to compare the current inversion to those of the past. In doing

so, we can further refine our economic and market expectations.

Bull or Bear Flattening

In this

section, we graph the seven yield curve inversions since 1978, showing how ten-year

U.S. Treasuries (UST), two-year UST and the 10-year/2 year curve performed in

the year before the inversion.

Before

progressing, it is worth defining some bond trading lingo:

Steepener-

Describes a situation in which the difference between the yield on the 10-year UST and the yield on the 2y-year UST is

increasing. Steepeners can occur when both securities are trending up or down

in yield or when the 2-year yield declines while the 10-year yield increases.

Flattener-

A flattener is the opposite of a steepener, and the difference between yields

is declining. As shown in the graph

above, the slope of the curve has been in a flattening trend for the last five

years.

Bullish/Bearish-

The terms steepener and flattener are typically preceded with the descriptor

bullish or bearish. Bullish means yields are declining (bond prices are rising)

while bearish means yields are rising (bond prices are falling). For instance,

a bullish flattener means that both 2s and 10s are declining in yield but 10s

are declining at a quicker pace. A bearish flattener implies that yields for 2s

and 10s are rising with 2s increasing at a faster pace. Currently, we are witnessing a bullish

flattener. All inversions, by definition, are preceded by a flattening trend.

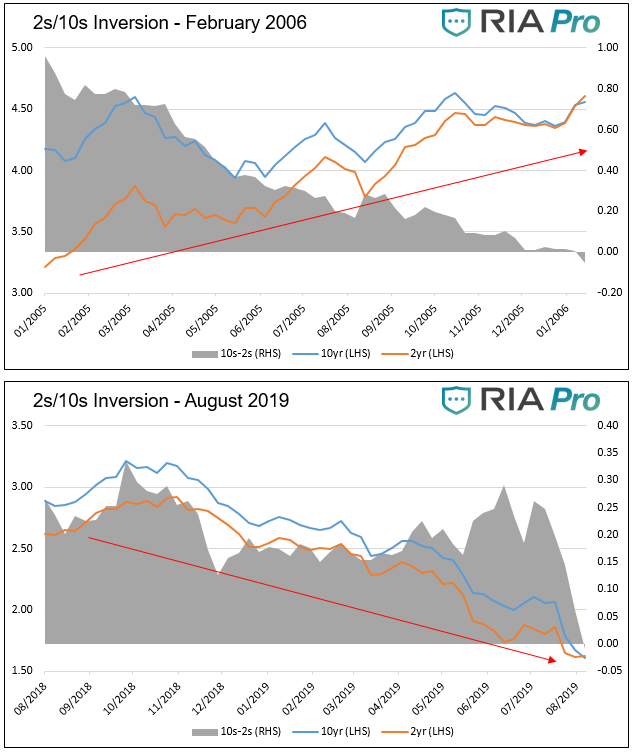

As shown in

the seven graphs below, there are two distinct patterns, bullish flatteners and

bearish flatteners, which emerged before each of the last seven inversions. The

red arrows highlight the general trend of yields during the year leading up to

the curve inversion.

Data for all graphs courtesy St.

Louis Federal Reserve

Five of the

seven instances exhibited a bearish flattening before inversion. In other

words, yields rose for both two and ten year Treasuries and two year yields

were rising more than tens. The exceptions are 1998 and the current period.

These two instances were/are bullish flatteners.

Bearish Flattener

As the

amount of debt outstanding outpaces growth in the economy, the reliance on debt

and the level of interest rates becomes a larger factor driving economic

activity and monetary and fiscal policy decisions. In five of the seven

instances graphed, interest rates rose as economic growth accelerated and consumer

prices perked up. While the seven periods are different in many ways, higher interest

rates were a key factor leading to recession. Higher interest rates reduce the

incentive to borrow, ultimately slowing growth and in these cases resulted in a

recession.

Bullish Insurance Flattener

As noted,

the current period and 1998 are different from the other periods shown. Today, as

in 1998, yields are falling as the 10-year

Treasury yield drops faster than the 2-year Treasury yield. The curve thus flattens

and ultimately inverts.

Seven years

into the economic expansion, during the fall of 1998, the Fed cut rates in

three 25 basis point increments. Deemed “insurance cuts,” the purpose was to

counteract concerns about sluggish growth overseas and financial market concerns

stemming from the Asian crisis, Russian default, and the failure of hedge fund giant

Long Term Capital. The yield curve inversion was another factor driving the

Fed. The domestic economy during the period was strong, with real GDP staying

above 4%, well above the natural growth rate.

The current

period is somewhat similar. The U.S. economy, while not nearly as strong as the

’98 experience, has registered above-trend economic growth for the last two

years. Also similar to 1998, there are exogenous factors that are concerning for

the Fed. At the top of the list are the trade war and sharply slowing economic

activity in Europe and China. Like in 1998, we can add the newly inverted yield

curve to the list.

The Fed

reduced rates by 25 basis points on July 31, 2019. Chairman Powell characterized

the cut as a “mid-cycle adjustment” designed to ensure solid economic growth

and support the record-long expansion. Some Fed members are describing the cuts

as an insurance measure, similar to the language employed in 1998.

If 1998-like

“insurance” measures are the Fed’s game plan to counteract recessionary

pressures, we must ask if the periods are similar enough to ascertain what may

happen this time.

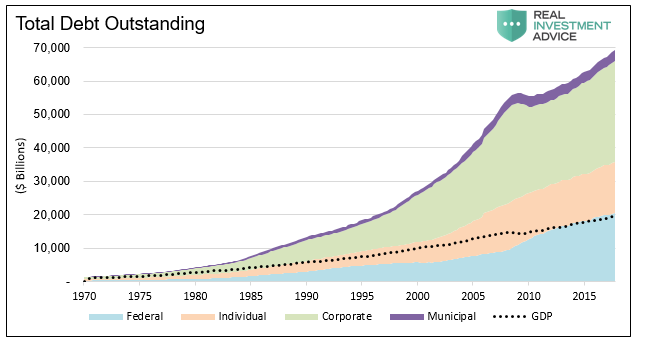

A key

differentiating factor between today and the late 1990s is not only the amount

of debt but the dependence on it. Over

the last 20 years, the amount of total debt as a ratio to GDP increased from

2.5x to over 3.5x.

Data Courtesy St. Louis Federal

Reserve

In 1998, believe

it or not, the U.S. government ran a fiscal surplus and Treasury debt issuance was

declining. Today, the reliance on debt for new economic activity and the burden

of servicing old debt has never been greater in the United States. Because

rates are already at or near 300-year lows, unlike 1998, the marginal benefits

from borrowing and spending as a result of lower rates are much less

economically significant currently.

In 1998, the

internet was in its infancy and its productive benefits were just being

discovered. Productivity, an essential element for economic growth, was

booming. By comparison, current productivity growth has been lifeless for well

over the last decade.

Demographics,

the other key factor driving economic activity, was also a significant

component of economic growth. Twenty years ago, the baby boomers were in their

spending and investing prime. Today they are retiring at a rate of 10,000 per

day, reducing their consumption and drawing down their investment accounts.

The key

point is that lower rates are far less likely to spur economic activity today than

in 1998. Additionally, the natural rate of economic growth is lower today, so the

economy is more susceptible to recession given a smaller decline in economic

activity than it was in 1998.

The 1998

rate cuts led to an explosion of speculative behavior primarily in the tech

sectors. From October of 1998 when the Fed first cut rates, to the market peak

in March of 2000, the NASDAQ index rose over 300%. Many equity valuation ratios

from the period set records.

We have

witnessed a similar but broader-based speculative fervor over the last five

years. Valuations in some cases have exceeded those of the late 1990s and in

other cases stand right below them. While the economic, productivity, and

demographic backdrops are not the same, we cannot rule out that Fed cuts might

fuel another explosive rally. If this were to occur, it will further reduce

expected returns and could lead to a crushing decline in the years following as

occurred in the early 2000s.

Summary

A yield

curve inversion is the bond market’s way of telegraphing concern that economic

growth will slow in the coming months. Markets do not offer guarantees, but the

2s-10s yield curve has been right every time in the last 30 years it voiced

this concern. As the book of Ecclesiastes reminds us, “the race does not always

go to the swift nor the battle to the strong…”, but that’s the way to bet.

Insurance rate

cuts may buy the record-long economic expansion another year or two as they did

20 years ago, but the marginal benefit of lower rates is not nearly as powerful

today as it was in 1998.

Whether the

Fed combats a recession in the months ahead as the bond market warns or in a

couple of years, they are very limited in their abilities. In 2000 and 2001,

the Fed cut rates by a total of 575 basis points, leaving the Fed Funds rate at

1.00%. This time around, the Fed can only cut rates by 225 basis points until

it reaches zero percent. When we reach that point, and historical precedence

argues it will be quicker than many assume, we must then ask how negative

rates, QE, or both will affect the economy and markets. For this there is no

prescriptive answer.

We respect your privacy and will only send you email that is related to what you subscribed to and why you subscribed. You can unsubscribe whenever you want with just a click of your mouse. For more information please see... Disclosure & Privacy Policy.