Pulling Forward versus Paying Forward

Debt allows a consumer (household, business, or government) to pull consumption forward or acquire something today for which they otherwise would have to wait. When the primary objective of fiscal and monetary policy becomes myopically focused on incentivizing consumers to borrow, spend, and pull consumption forward, there will eventually be a painful resolution of the imbalances that such policy creates. The front-loaded benefits of these tactics are radically outweighed by the long-term damage they ultimately cause.

Due to the overwhelming importance that the durability of economic growth has on future asset returns, we take a new approach in this article to drive home a message from our prior article The Death of the Virtuous Cycle. In this article, we use two simple examples to demonstrate how the Virtuous Cycle (VC) and Un-Virtuous Cycle (U-VC) have benefits and costs to society that play out over time.

The Minsky Moment

Before walking you through the examples contrasting the two economic cycles, it is important to put debt into its proper context. Debt can be used productively to benefit the economy in the long term, or it can be used to fulfill materialistic needs and to temporarily stimulate economic growth in the short term. While both uses of debt look the same on a balance sheet, the effect that each has on the borrower and the economy over time is remarkably different.

In the course of his life’s work as an economist, Hyman Minsky focused on the factors that cause financial market fragility and how extreme circumstances eventually resolve themselves. Minsky, who died in 1996, only recently became “famous” as a result of the sub-prime mortgage debacle and ensuing financial crisis in 2008.

Minsky elaborated on his “stability breeds instability” theory by identifying three types of borrowers and how they evolve to contribute to the accumulation of insolvent debt and inherent instability.

- Hedge borrowers can make interest and principal payments on debt from current cash flows generated from existing investments.

- Speculative borrowers can cover the interest on the debt from the investment cash flows but must regularly refinance, or “roll-over,” the debt as they cannot pay off the principal.

- Ponzi borrowers cannot cover the interest payments or the principal on debt from the investment cash flows, but believe that the appreciation of the investments will be sufficient to refinance outstanding debt obligations when the investment is sold.

Over the past 20 years, investors have been witness to a remarkable sequence of bubbles. The first culminated when an abundance of Ponzi borrowers concentrated their investments in the equity markets and technology stocks in particular. Technology companies, frequently with operating losses, raised capital through stock and debt offerings from investors who believed excessive valuations could expand indefinitely.

The second bubble emerged in housing. Many home buyers acquired houses via mortgages payments they could in no way afford, but believed house prices would rise indefinitely allowing them to service their mortgage obligations via the extraction of equity.

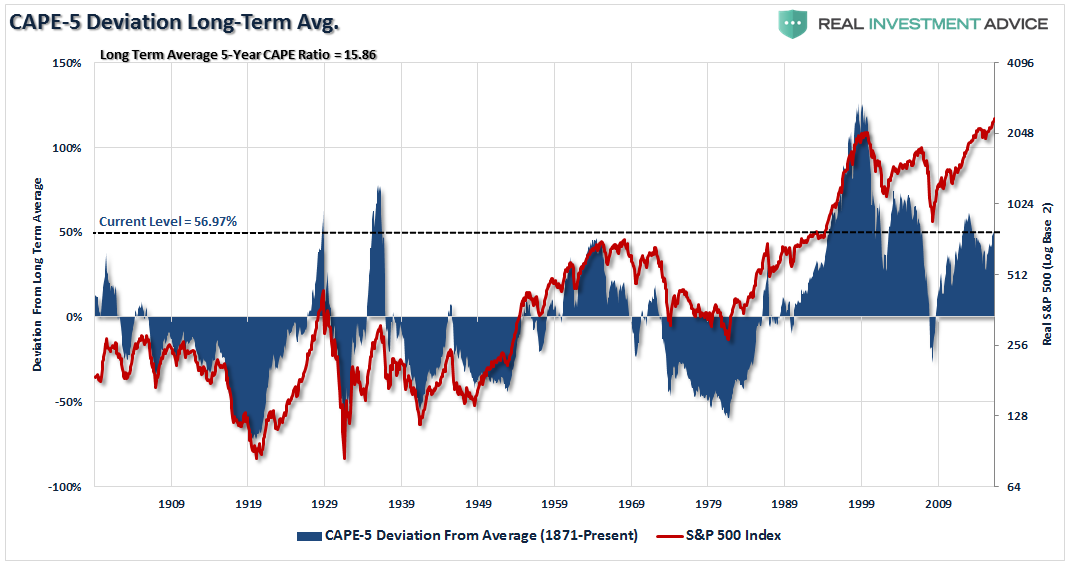

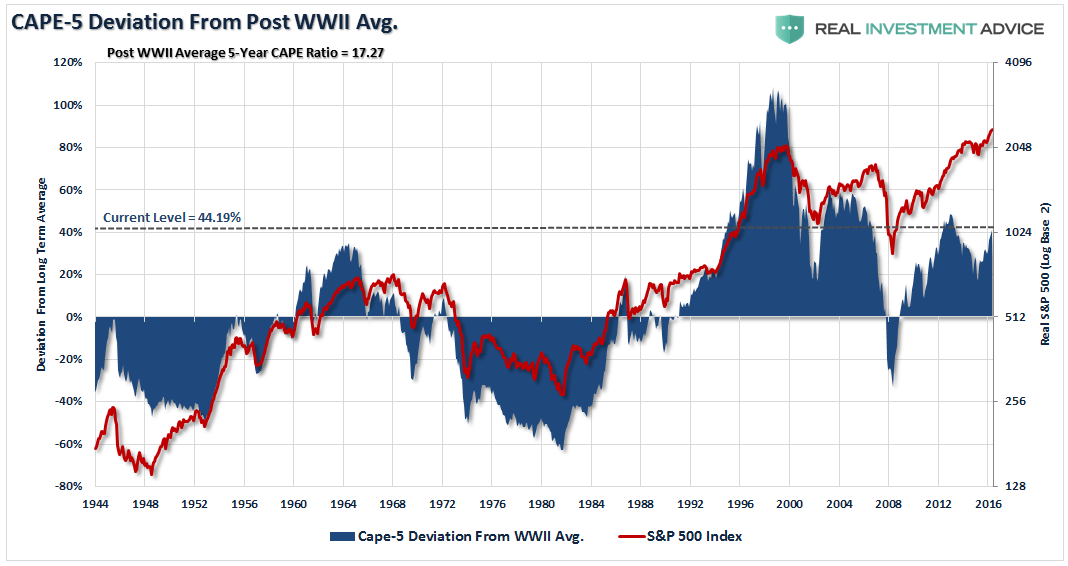

Today, we are witnessing a broader asset price inflation driven by a belief that central banks will engage in extraordinary monetary policy indefinitely to prop up valuations in the hope for the always “just around the corner” wealth effect. Equity markets are near all-time highs and at extreme valuations despite weak economic growth and limited earnings growth. Bond yields are near the lowest levels (highest prices) human civilization has ever seen. Commercial real estate is back at 2007 bubble valuations and real assets such as art, wine, and jewelry are enjoying record-setting bidding at auction houses.

These financial bubbles could not occur in an environment of weak domestic and global economic growth without the migration of debt borrowers from hedge to speculative to Ponzi status.

Compare and Contrast

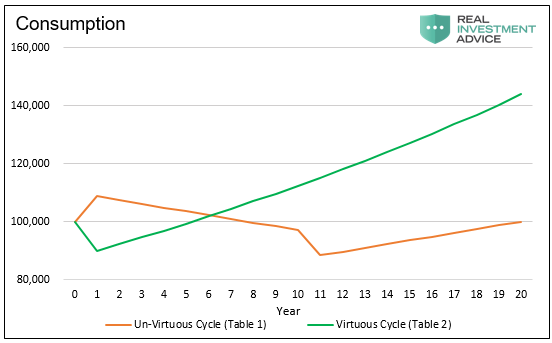

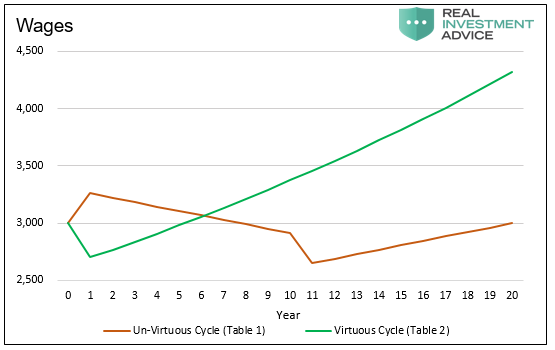

The tables below summarize two extreme economic models to exhibit how an economy dependent upon “Ponzi” financing compares to one in which savings are prioritized. In both cases, we show how the respective financial decisions influence consumption, profits, and wages.

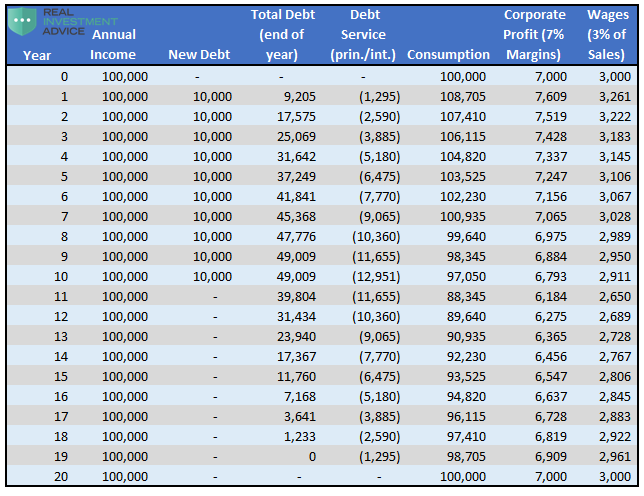

Table 1, below, is based on the assumption that consumers spend 100% of their wages and borrow an additional amount equivalent to 10% of their income annually for ten years straight. The debt amortizes annually and is therefore retired in full in 20 years.

Assumptions: Debt is borrowed each year for the first ten years at a 5% interest rate and ten year term, corporate profits and employee wages are 7% and 3% of consumption respectively, annual income is constant at $100,000 per year.

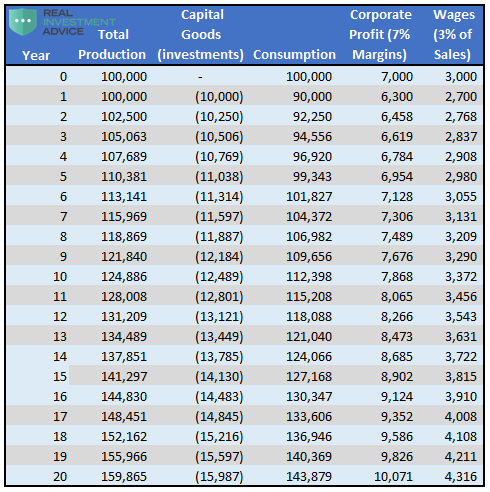

Table 2, below, assumes consumers spend 90% of wages, save and invest 10% a year, and do not borrow any money. The table is based on the work of Henry Hazlitt from his book Economics in One Lesson.

Assumptions: Productivity growth is 2.5% per year, corporate profits and employee wages are 7% and 3% of consumption respectively.

Table 1 is the U-VC and Table 2 is the VC. The tables illustrate that there are immediate economic benefits of borrowing and economic costs of saving. For example, in year one, consumption in Table 1 rises as a result of the new debt ($100,000 to $108,705) and wages and corporate profits follow proportionately. Conversely, table 2 exhibits an initial $10,000 decline in consumption to $90,000, and a similar decline in wages and corporate profits as a result of deferring consumption on 10% of the income that was designated for saving and investing.

After year one, however, the trends begin to reverse. In the U-VC example (Table 1), when new debt is added, debt servicing costs rise, and the marginal benefits of additional debt decline. By year eight, debt service costs ($10,360) are larger than the additional new debt ($10,000). At that point, without lower interest rates or larger borrowings, consumption will fall below the income level.

Conversely, in the VC example (Table 2), savings and investments engender productivity growth, which drives wages, profits, and consumption higher.

The graphs below highlight the consumption and wage trends from both tables.

As illustrated in both graphs, the short term justification for promoting the U-VC is prompt economic growth. Equally important, the reason that savings and investments in the VC are admonished is that they require discipline and a period of lesser growth, profits, and wages.

Debt-fueled consumption is an expedient measure to take when economic growth stalls and immediate economic recovery is demanded. While the marginal benefits of such action fade quickly, a longer-term policy that consistently encourages greater levels of debt and lower debt servicing costs can extend the beneficial economic effects for years, fooling many consumers, economists and business leaders into believing these activities are sustainable.

In the tables above, it takes almost seven years before consumption in the VC (Table 2) is greater than in U-VC (Table 1). However, after that breakeven point, the benefits of a VC become evident as economic growth compounds at an increasing rate, quickly surpassing the stagnating trends occurring under the U-VC.

In the real world, VC or U-VC economies do not exist. Economies tend to exhibit characteristics of both cycles. In the United States, for example, some consumers and corporations are saving, investing, and generating productive economic gains. Productivity gains from years past are still providing benefits as well. However, over the past 30 years, consumers have increasingly opted to borrow and consume in a Ponzi-like manner and neglect savings. In other words, the U.S. economy has increasingly favored “Ponzi” debt-fueled consumption and denied the benefits of savings and the VC. Then again, U.S. leadership has only encouraged these behavioral patterns through imprudent fiscal and monetary policies.

The U.S. and many other countries are once again approaching what has been deemed the Minsky Moment. Similar to 2008, this is the point when debt becomes unserviceable and a sharp increase in defaults is unavoidable. Will the Federal Reserve be able to once again reignite “Ponzi” borrowing to suspend that outcome?

Summary

The U.S. and many other countries are forced to deal with the consequences of economic policy actions, borrowing, and consumption behaviors from years past. While the present economic situation is troubling, leadership is obligated to reflect on past choices and move forward with changes that are in the best interest of the country and its entire population. As our title suggests, we can continue to try to pull consumption forward and further harm future growth, or we can save and reward future generations with productivity gains resulting in greater economic growth and prosperity.

Shifting direction, and “paying forward,” via more savings and investments and the deferral of some consumption, comes with immediate negative consequences to wages, profits, and economic growth. Nothing worth having is easy, as the saying goes. However, over time, the discipline is rewarded, and the economy can be on a more sustainable, prosperous path.

These economic concepts, tables, and graphs extend an accurate diagnosis of the “Death of the Virtuous Cycle.” They are intended to help investment managers better understand the costs and benefits of saving versus borrowing from a macroeconomic perspective. If successful in that endeavor, the substance of this article will afford managers better ideas about how to navigate a very uncertain investment landscape. The implications for the sustainability of economic growth and therefore long term asset returns are profound and the bedrock of all investment decisions.