The COVID19 Tripwire

“You better tuck that in. You’re gonna’ get that caught on a tripwire.” – Lieutenant Dan, Forrest Gump

There is a popular game called Jenga in which a tower of rectangular blocks is arranged to form a sturdy tower. The objective of the game is to take turns removing blocks without causing the tower to fall. At first, the task is as easy as the structure is stable. However, as more blocks are removed, the structure weakens. At some point, a key block is pulled, and the tower collapses. Yes, the collapse is a direct cause of the last block being removed, but piece by piece the structure became increasingly unstable. The last block was the catalyst, but the turns played leading up to that point had just as much to do with the collapse. It was bound to happen; the only question was, which block would cause the tower to give way?

A Coronavirus

Pneumonia of unknown cause first detected in Wuhan, China, was reported to the World Health Organization (WHO) on December 31, 2019. The risks of it becoming a global pandemic (formally labeled COVID-19) was apparent by late January. Unfortunately, it went mostly unnoticed in the United States as China was slow to disclose the matter and many Americans were distracted by impeachment proceedings, bullish equity markets, and other geopolitical disruptions.

The S&P 500 peaked on February 19, 2020, at 3393, up over 5% in the first two months of the year. Over the following four weeks, the stock market dropped 30% in one of the most vicious corrections of broad asset prices ever seen. The collapse erased all of the gains achieved during the prior 3+ years of the Trump administration. The economy likely entered a recession in March.

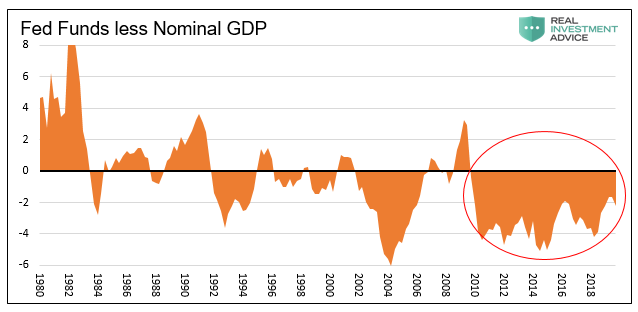

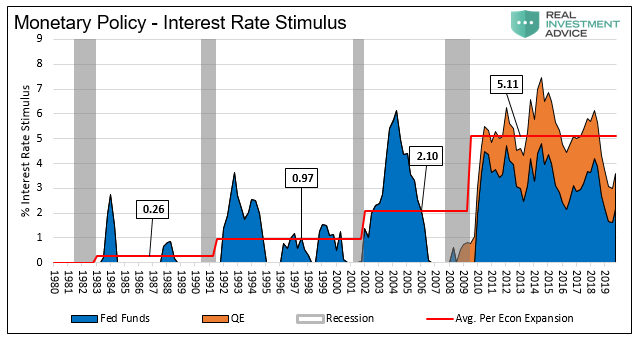

There will be much discussion and debate in the coming months and years about the dynamics of this stunning period. There is one point that must be made clear so that history can properly record it; the COVID-19 virus did not cause the stock and bond market carnage we have seen so far and are likely to see in the coming months. The virus was the passive triggering mechanism, the tripwire, for an economy full of a decade of monetary policy-induced misallocations and excesses leaving assets priced well beyond perfection.

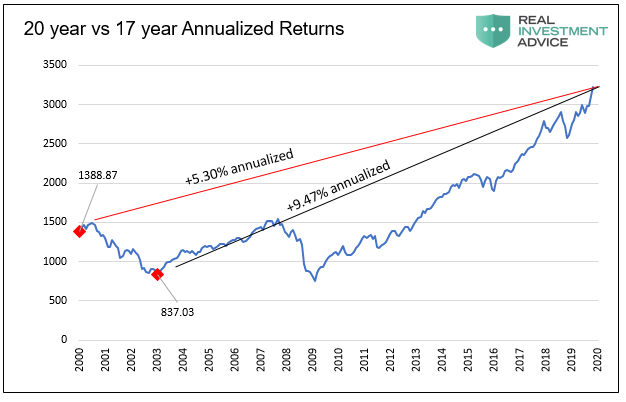

Never-Ending Gains

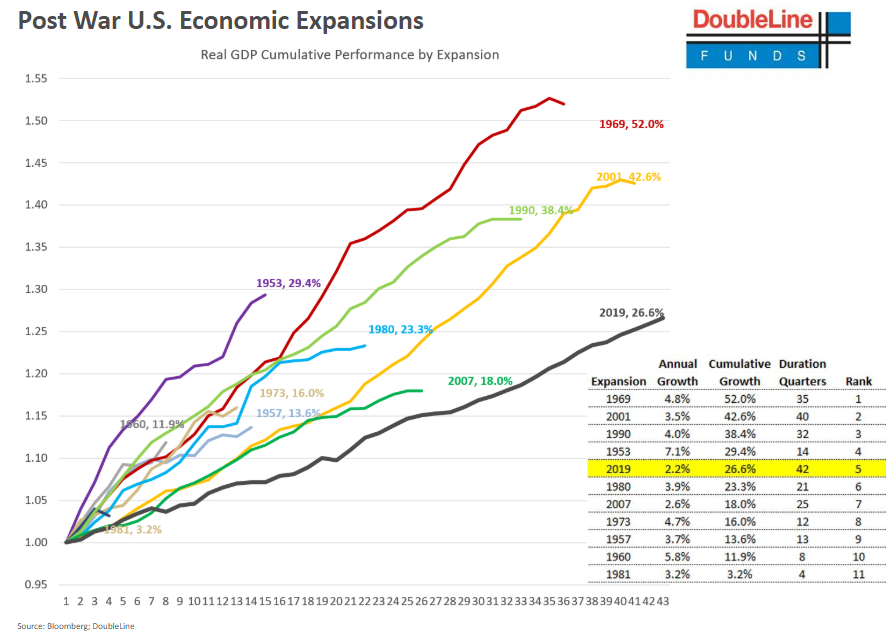

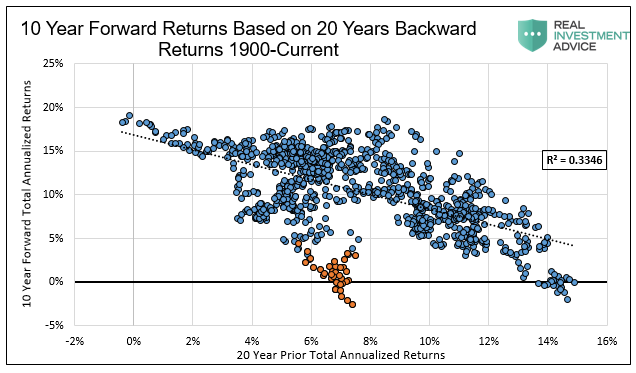

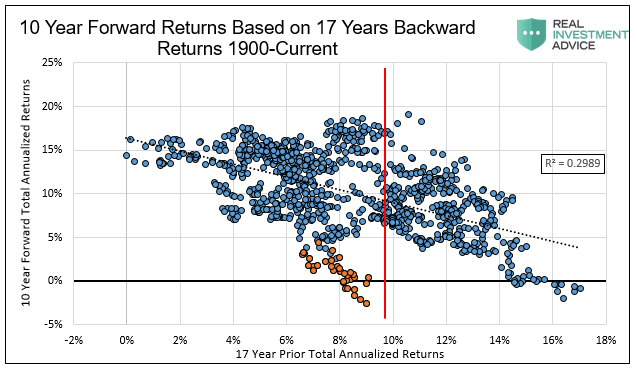

It is safe to say that the record-long economic expansion, to which no one saw an end, ended in February 2020 at 128 months. To suggest otherwise is preposterous given what we know about national economic shutdowns and the early look at record Initial Jobless Claims that surpassed three million. Between the trough in the S&P 500 from the financial crisis in March 2009 and the recent February peak, 3,999 days passed. The 10-year rally scored a total holding-period return of 528% and annualized returns of 18.3%. Although the longest expansion on record, those may be the most remarkable risk-adjusted performance numbers considering it was also the weakest U.S. economic expansion on record, as shown below.

They say “being early is wrong,” but the 30-day destruction of valuations erasing over three years of gains, argues that you could have been conservative for the past three years, kept a large allocation in cash, and are now sitting on small losses and a pile of opportunity with the market down 30%.

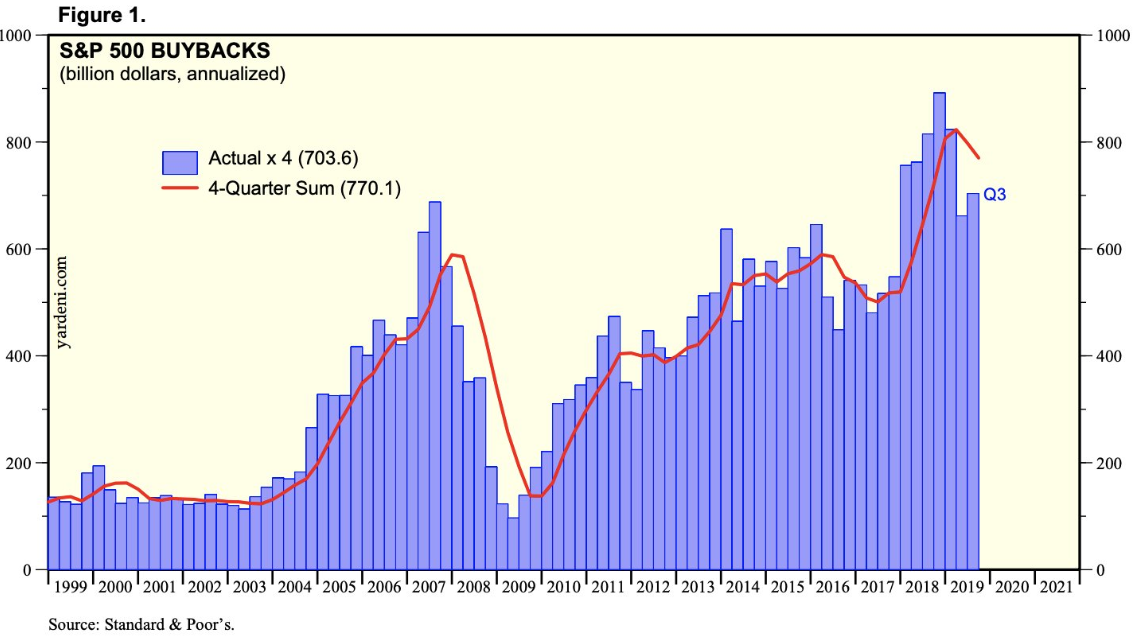

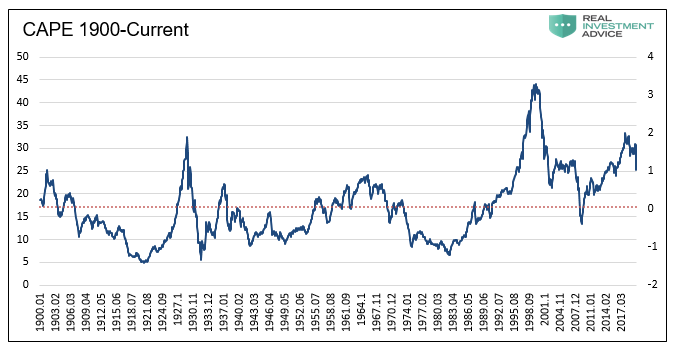

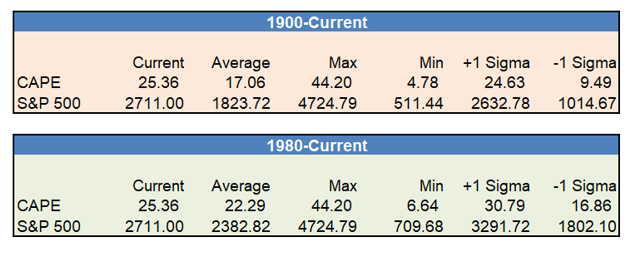

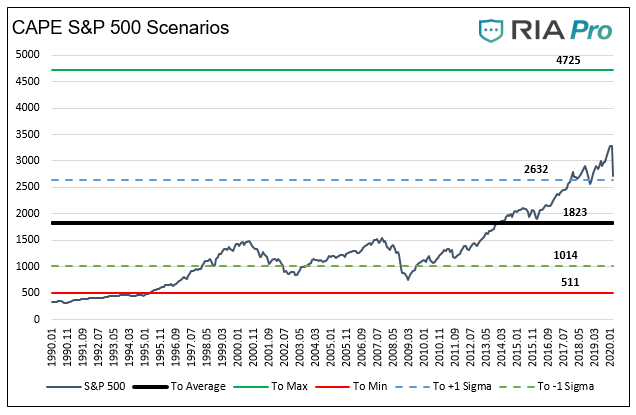

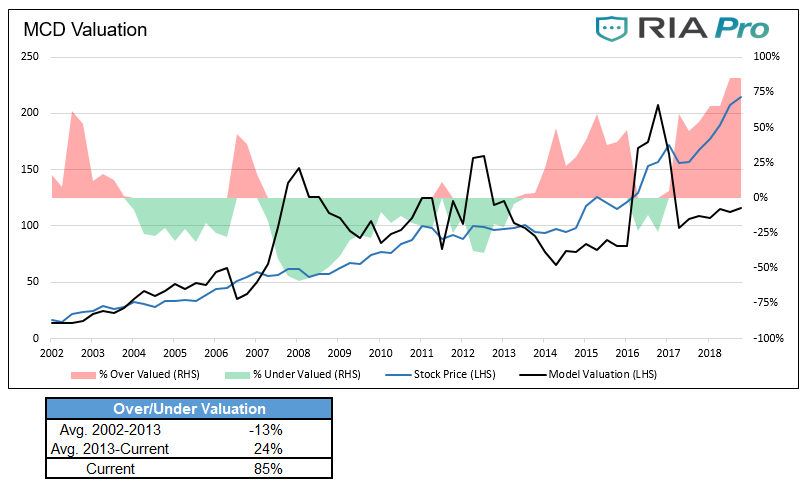

As we have documented time and again, the market for financial assets was a walking dead man, especially heading into 2020. Total corporate profits were stagnant for the last six years, and the optics of magnified earnings-per-share growth, thanks to trillions in share buybacks, provided the lipstick on the pig.

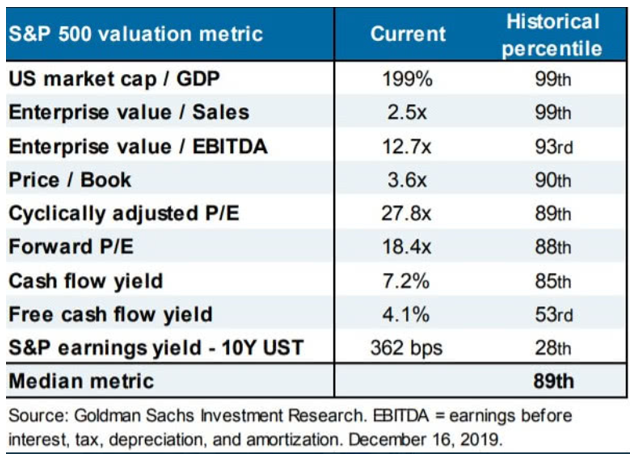

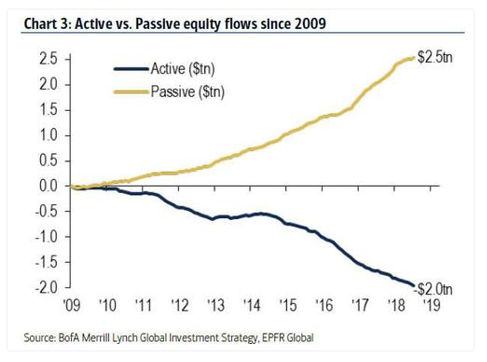

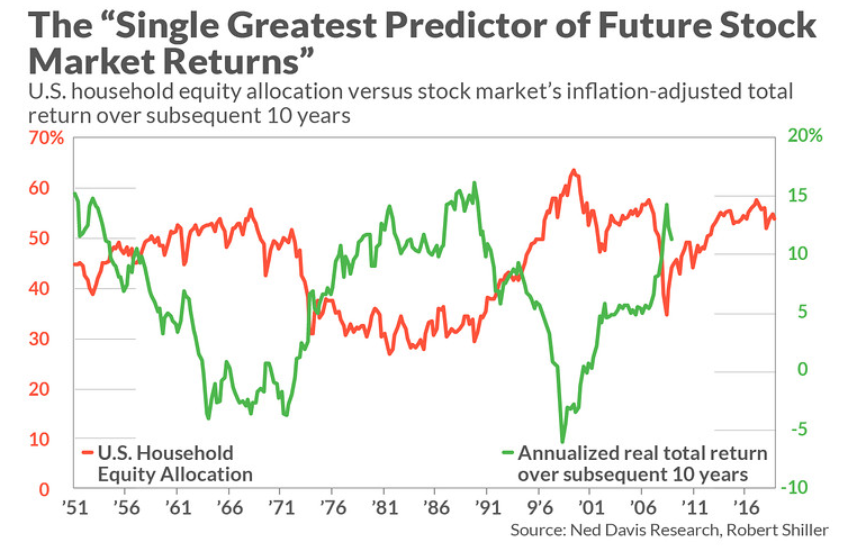

Passive investors indiscriminately and in most cases, unknowingly, bought $1.5 trillion in over-valued stocks and bonds, helping further push the market to irrational levels. Even Goldman Sachs’ assessment of equity market valuations at the end of 2019, showed all of their valuation measures resting in the 90-99th percentile of historical levels.

Blind Bond Markets

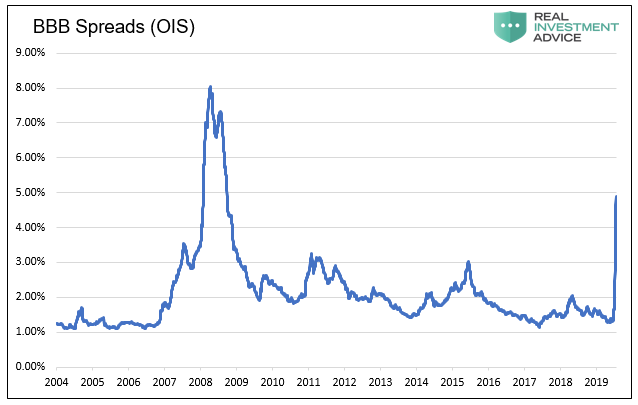

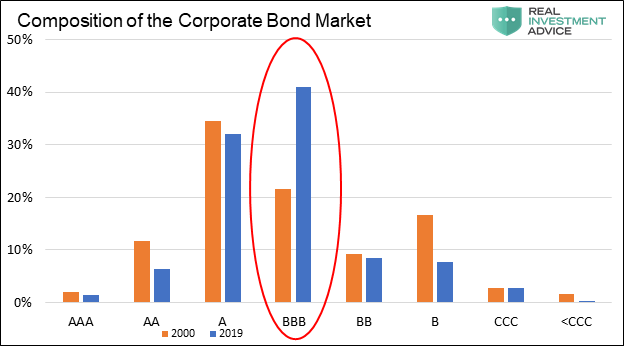

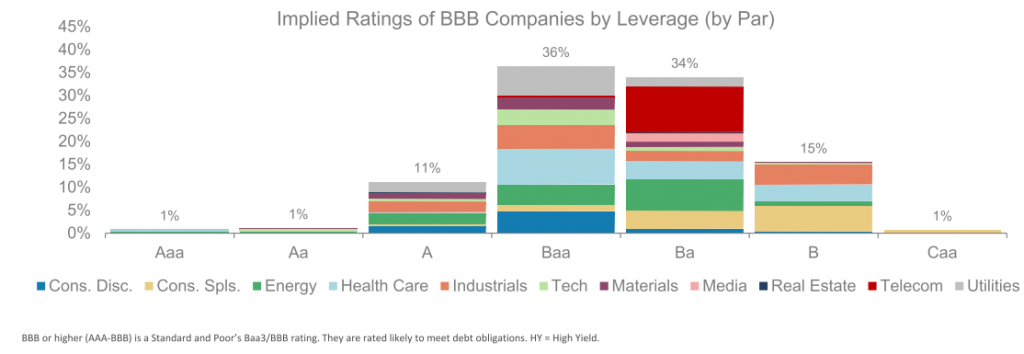

The fixed income markets were also swarming with indiscriminate buyers. The corporate bond market was remarkably overvalued with tight spreads and low yields that in no way offered an appropriate return for the risk being incurred. Investment-grade bonds held the highest concentration of BBB credit in history, most of which did not qualify for that rating by the rating agencies’ own guidelines. The junk bond sector was full of companies that did not produce profits, many of whom were zombies by definition, meaning the company did not generate enough operating income to cover their debt servicing costs. The same held for leveraged loans and collateralized loan obligations with low to no covenants imposed. And yet, investors showed up to feed at the trough. After all, one must reach for extra yield even if it means forgoing all discipline and prudence.

To say that no lessons were learned from 2008 is an understatement.

Black Swan

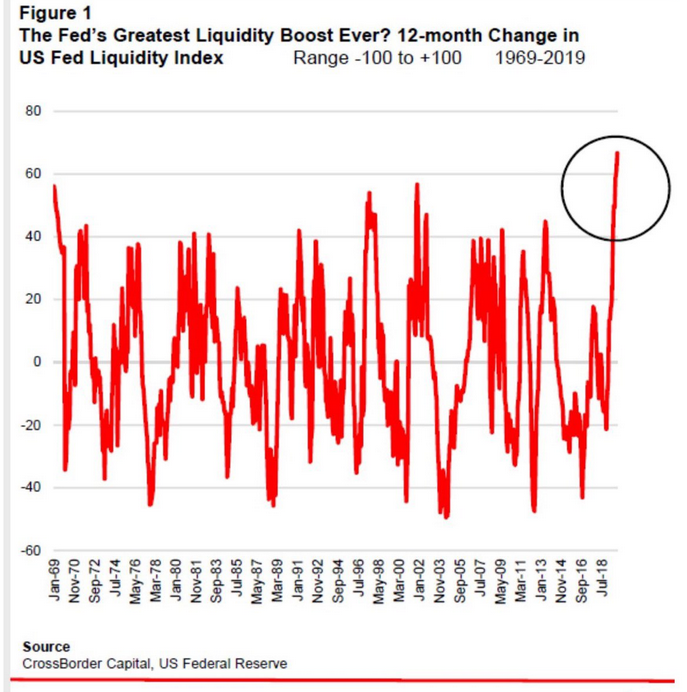

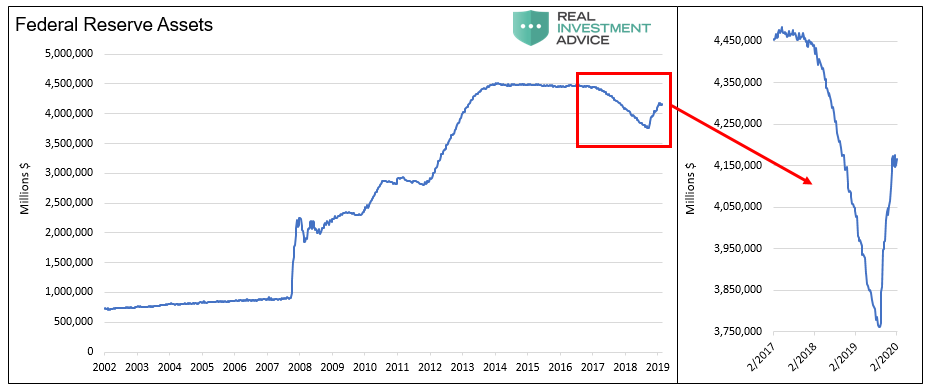

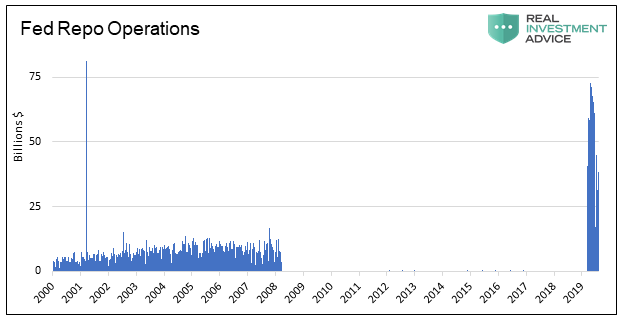

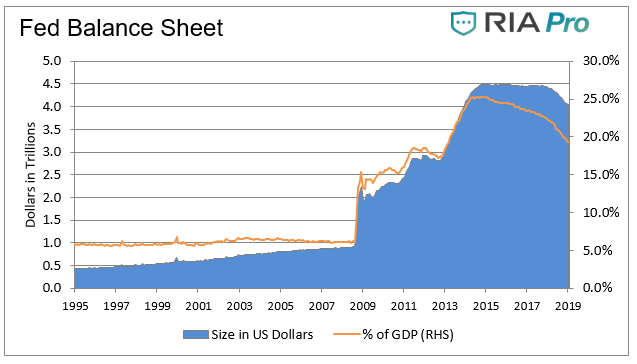

Meanwhile, as the markets priced to ridiculous valuations, corporate executives and financial advisors got paid handsomely, encouraging shareholders and clients to throw caution to the wind and chase the market ever higher. Thanks also to imprudent monetary policies aimed explicitly at propping up indefensible valuations, the market was at risk due to any disruption.

What happened, however, was not a slow leaking of the market as occurred leading into the 2008 crisis, but a doozy of a gut punch in the form of a pandemic. Markets do not correct by 30% in 30 days unless they are extremely overvalued, no matter the cause. We admire the optimism of formerly super-intelligent bulls who bought every dip on the way down. Ask your advisor not just to tell you how he is personally invested at this time, ask him to show you. You may find them to be far more conservative in their investment posture than what they recommend for clients. Why? Because they get paid on your imprudently aggressive posture, and they do not typically “eat their own cooking”. The advisor gets paid more to have you chasing returns as opposed to avoiding large losses.

Summary

We are facing a new world order of DE-globalization. Supply chains will be fractured and re-oriented. Products will cost more as a result. Inflation will rise. Interest rates, therefore, also will increase contingent upon Fed intervention. We have become accustomed to accessing many cheap foreign-made goods, the price for which will now be altered higher or altogether beyond our reach. For most people, these events and outcomes remain inconceivable. The widespread expectation is that at some point in the not too distant future, we will return to the relative stability and tranquility of 2019. That assuredly will not be the case.

Society as a whole does not yet grasp what this will mean, but as we are fond of saying, “you cannot predict, but you can prepare.” That said, we need to be good neighbors and good stewards and alert one another to the rapid changes taking place in our communities, states, and nation. Neither investors nor Americans, in general, can afford to be intellectually lazy.

The COVID-19 virus triggered these changes, and they will have an enormous and lasting impact on our lives much as 9-11 did. Over time, as we experience these changes, our brains will think differently, and our decision-making will change. Given a world where resources are scarce and our proclivity to – since it is made in China and “cheap” – be wasteful, this will probably be a good change. Instead of scoffing at the frugality of our grandparents, we just might begin to see their wisdom. As a nation, we may start to understand what it means to “save for a rainy day.”

Save, remember that forgotten word.

As those things transpire – maybe slowly, maybe rapidly – people will also begin to see the folly in the expedience of monetary and fiscal policy of the past 40 years. Expedience such as the Greenspan Put, quantitative easing, and expanding deficits with an economy at full employment. Doing “what works” in the short term often times conflicts with doing what is best for the most people over the long term.

{kind=link}