Our interim global forecast is the second prepared in March and is much more pessimistic than our 17 March regularly scheduled outlook. It is based on major downgrades to forecasts of the US economy and oil prices. The risks remain overwhelmingly on the downside and further downgrades are almost assured.

IHS Markit now believes the COVID-19 recession will be deeper than the one following the global financial crisis in 2008-09. Real world GDP should plunge 2.8% in 2020 compared with a drop of 1.7% in 2009. Many key economies will see double-digit declines (at annualized rates) in the second quarter, with the contraction continuing into the third quarter.

It will likely take two to three years for most economies to return to their pre-pandemic levels of output. More troubling is the likelihood that, because of the negative effects of the uncertainty associated with the virus on capital spending, the path of potential GDP will be lower than before. This happened in the wake of the global financial crisis.

Six Key Points

Based on recent data and developments, IHS Markit has slashed the US 2020 forecast to a contraction of 5.4%.

Because of the deep US recession and collapsing oil prices, IHS Markit expects Canada’s economy to contract 3.3% this year, before seeing a modest recovery in 2021.

Europe, where the number of cases continues to grow rapidly and lockdowns are pervasive, will see some of the worst recessions in the developed world, with 2020 real GDP drops of approximately 4.5% in the eurozone and UK economies. Italy faces a decline of 6% or more. The peak GDP contractions expected in the second quarter of 2020 will far exceed those at the height of the global financial crisis.

Japan was already in recession, before the pandemic. The postponement of the summer Tokyo Olympics will make the downturn even deeper. IHS Markit expects a real GDP contraction of 2.5% this year and a very weak recovery next year.

China’s economic activity is expected to have plummeted at a near-double-digit rate in the first quarter. It will then recover sooner than other countries, where the spread of the virus has occurred later. IHS Markit predicts growth of just 2.0% in 2020, followed by a stronger-than-average rebound in 2021, because of its earlier recovery from the pandemic.

Emerging markets growth will also be hammered. Not only are infection rates rising rapidly in key economies, such as India, but the combination of the deepest global recession since the 1930s, plunging commodity prices, and depreciating currencies (compounding already dangerous debt burdens) will push many of these economies to the breaking point.

No V-Shaped Recovery

With that, Markit came around to my point of view all along. Those expecting a V-shaped recovery are sadly mistaken.

I have been amused by Goldman Sachs and Morgan Stanley predictions of a strong rebound in the third quarter.

It’s a list of projections from an excellent must see video presentation by Jim Bianco. I added my own thoughts on the key points.

The bottom line is don’t expect a v-shaped recovery. We will not return to the old way of doing business.

Globalization is not over, but the rush to globalize everything is. This will impact earnings for years to come.

Finally, stimulus checks are on the way, but there will be no quick return to buying cars, eating out, or traveling as much.

Boomers who felt they finally had enough retirement money just had a quarter of it or more wiped out.

It will take a long time, if ever, for the same sentiment to return. Spending will not recover. Boomers will die first, and they are the ones with the most money.

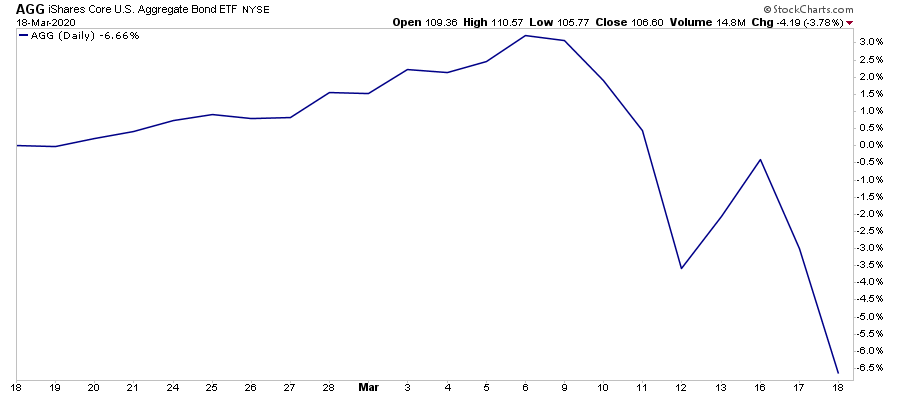

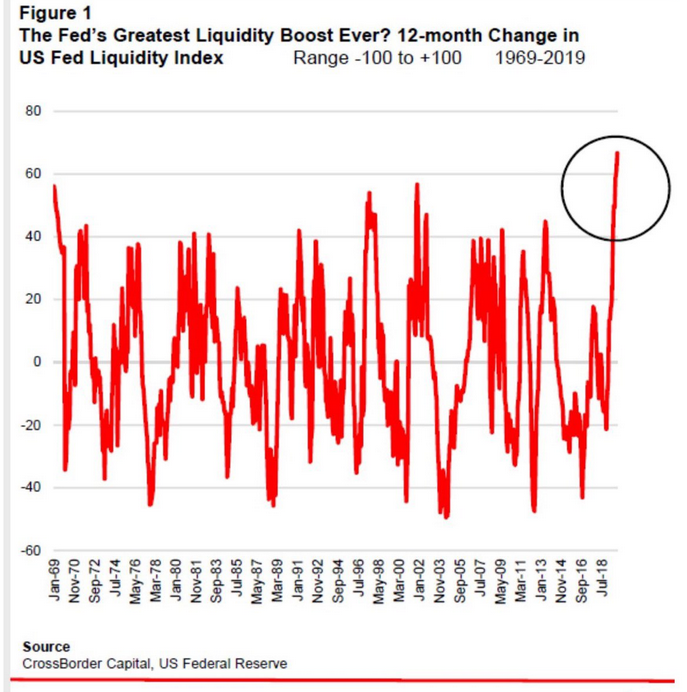

Shedlock: Fed Trying To Save The Bond Market As Unemployment Explodes

Bond market volatility remains a sight to behold, even at the low end of the curve.

Bond Market Dislocations Remain

The yield on a 3-month T-Bill fell to 1.3 basis points then surged to 16.8 basis points in a matter of hours. The yield then quickly crashed to 3 basis points and now sits at 5.1 basis points.

The Fed is struggling even with the low end of the Treasury curve.

$IRX 3-Month Yield

Stockcharts shows the 3-month yield ($IRX) dipping below zero but Investing.Com does not show the yield went below zero.

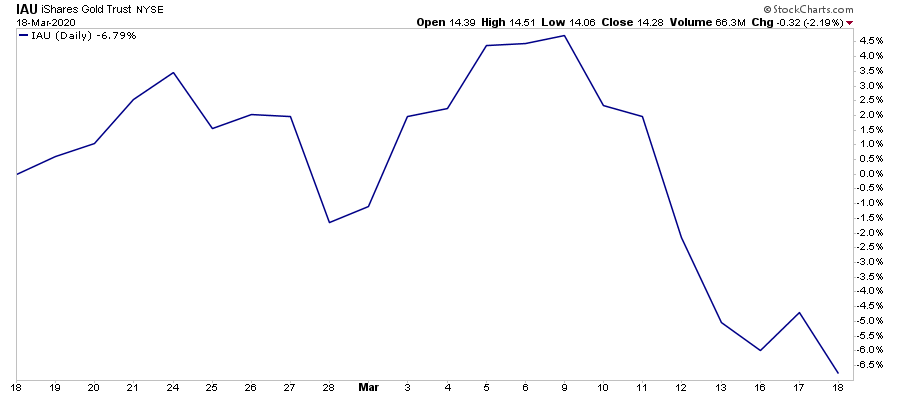

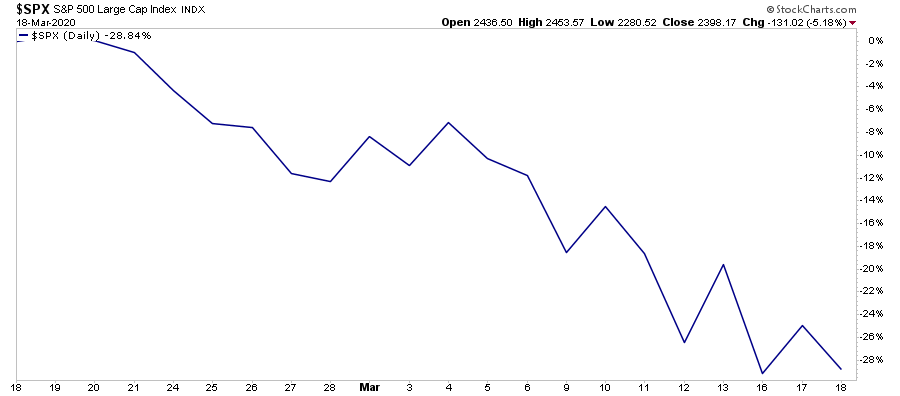

In a crisis, it is said, all correlations go to one. Threats get so overwhelming that everything reacts in unison. And the common thread running through all facets of financial markets and the real economy right now is simple: a global cash crunch of epic proportions.

Investors piled $137 billion into cash-like assets in the five days ending March 11, according to a Bank of America report citing EPFR Global data. Its monthly fund manager survey showed the fourth-largest monthly jump in allocations to cash ever, from 4% to 5.1%.

“Cash has become the king as the short-term government funds have had massive deposits, with ~$13 billion inflows last week (a 10-standard deviation move),” adds Maneesh Dehspande, head of equity derivatives strategy at Barclays.

4th Largest Jump in History

It’s quite telling that a jump of a mere 1.1 percentage point to 5.1% cash is the 4th largest cash jump in history.

Margin and Short Covering

“In aggregate, the market saw a large outflow, with $9 billion of long liquidation and $6 billion of short covering,” said Michael Haigh, global head of commodity research at Societe Generale. “This general and non-directional closure of money manager positions could be explained by a need for cash to pay margin calls on other derivatives contracts.”

The comment is somewhat inaccurate. Sideline cash did not change “in aggregate” although cash balances t various fund managers did.

This is what happens when leveraged longs get a trillion dollar derivatives margin call or whatever the heck it was.

Need a Better Hedge

With the S&P 500 down more than 12% in the five sessions ending March 17, the Japanese yen is weaker against the greenback, the 10-year Treasury future is down, and gold is too.

That’s another sign dollars are top of mind, and investors are selling not only what they want to, but also what they have to.

Dash to Cash

It’s one thing to see exchange-traded products stuffed full of relatively illiquid corporate bonds trade below the purported sum of the value of their holdings. It’s quite another to see such a massive discount develop in a more plain-vanilla product like the Vanguard Total Bond Market ETF (BND) as investors ditched the product to raise cash despite not quite getting their money’s worth.

The fund closed Tuesday at a discount of nearly 2% to its net asset value, which blew out to above 6% last week amid accelerating, record outflows. That exceeded its prior record discount from 2008.

It is impossible for everyone to go to cash at the same time.

Someone must hold every stock, every bond and every dollar.

The Fed said the swaps, in which the Fed accepts other currencies in exchange for dollars, will for at least the next six months allow the central banks of Australia, Brazil, South Korea, Mexico, Singapore, Sweden, Denmark, Norway and New Zealand to tap up to a combined total of $450 billion, money to ensure the world’s dollar-dependent financial system continues to function.

The new swap lines “like those already established between the Federal Reserve and other central banks, are designed to help lessen strains in global U.S. dollar funding markets, thereby mitigating the effects of these strains on the supply of credit to households and businesses, both domestically and abroad,” the Fed said in a statement.

The central banks of South Korea, Singapore, Mexico and Sweden all said in separate statements they intended to use them.

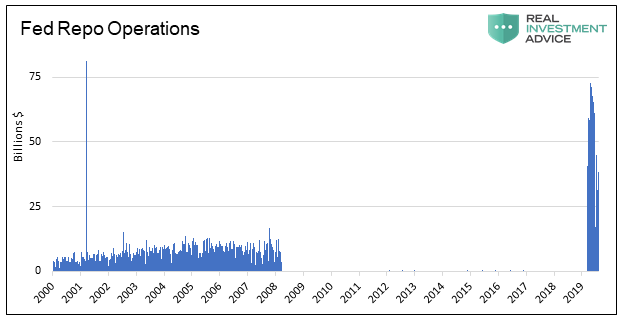

Fed Does Another Emergency Repo and Relaunches Commercial Paper Facility

The Fed blew three economic bubbles in succession. A deflationary bust has started. They blew bubbles trying to prevent “deflation” defined as falling consumer prices.

BIS Deflation Study

The BIS did a historical study and found routine price deflation was not any problem at all.

“Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive,” stated the BIS study.

Deflation is not really about prices. It’s about the value of debt on the books of banks that cannot be paid back by zombie corporations and individuals.

Blowing bubbles in absurd attempts to arrest “price deflation” is crazy. The bigger the bubbles the bigger the resultant “asset bubble deflation”. Falling consumer prices do not have severe negative repercussions. Asset bubble deflations are another matter.

Assessing the Blame

Central banks are not responsible for the coronavirus. But they are responsible for blowing economic bubbles prone to crash.

The equities bubbles before the coronavirus hit were the largest on record.

Dollar Irony

The irony in this madness is the US will be printing the most currency and have the biggest budget deficits as a result. Yet central banks can’t seem to get enough dollars. In that aspect, the dollar ought to be sinking.

But given the US 10-year Treasury yield at 1.126% is among the highest in the world, why not exchange everything one can for dollars earning positive yield.

This is all such circular madness, it’s hard to say when or how it ends.

Unemployment Set To Explode

A SurveyUSA poll reveals 9% of the US is out of a job due to the coronavirus.

9% of Working Americans (14 Million) So Far Have Been Laid Off As Result of Coronavirus; 1 in 4 Workers Have Had Their Hours Reduced;

2% Have Been Fired; 20% Have Postponed a Business Trip; Shock Waves Just Now Beginning to Ripple Through Once-Roaring US Economy:

Early markers on the road from recession to depression as the Coronavirus threatens to stop the world from spinning on its axis show that 1 in 4 working Americans have had their hours reduced as a result of COVID-19, according to SurveyUSA’s latest time-series tracking poll conducted 03/18/20 and 03/19/20.

Approximately 160 million Americans were employed in the robust Trump economy 2 months ago. If 26% have had their hours reduced, that translates to 41 million Americans who this week will take home less money than last, twice as many as SurveyUSA found in an identical poll 1 week ago. Time-series tracking graphs available here.

9% of working Americans, or 14 million of your friends and neighbors, will take home no paycheck this week, because they were laid off, up from 1% in an identical SurveyUSA poll 1 week ago. Time-series tracking graphs available here.

Unlike those laid-off workers who have some hope of being recalled once the worst of the virus has past, 2% of Americans say they have lost their jobs altogether as a result of the virus, up from 1% last week.

Of working Americans, 26% are working from home either some days or every day, up from 17% last week. A majority, 56%, no longer go to their place of employment, which means they are not spending money on gasoline or transit tokens.

About: SurveyUSA interviewed 1,000 USA adults nationwide 03/18/20 through 03/19/20. Of the adults, approximately 60% were, before the virus, employed full-time or part-time outside of the home and were asked the layoff and reduced-hours questions. Approximately half of the interviews for this survey were completed before the Big 3 Detroit automakers announced they were shutting down their Michigan assembly lines. For most Americans, events continue to unfold faster than a human mind is able to process the consequences.

If we assume the SurveyUSA numbers are accurate and will not get worse, we can arrive at some U3 and U6 unemployment estimates.

Baseline Unemployment Estimate (U3)

Unemployed: 5.787 million + 14 million = 19.787 million unemployed

Civilian Labor Force: 164.546 million (unchanged)

Unemployment Rate: 19.787 / 164.546 = 12.0%

That puts my off the top of the head 15.0% estimate a few days in the ballpark.

Underemployment Estimate (U6)

Employed: 158.759 million.

26% have hours reduced = 41.277 million

Part Time for Economic Reasons: 4.318 million + 41.277 million = 45.595 million underemployed

45.595 million underemployed + 19.787 million unemployed = 65.382 million

Civilian Labor Force: 164.546 million (unchanged)

U6 Unemployment Rate: 65.382 / 164.546 = 39.7%

Whoa Nellie

Wow, that’s not a recession. A depression is the only word.

Note that economists coined a new word “recession” after the 1929 crash and stopped using the word depression assuming it would never happen again.

Prior to 1929 every economic slowdown was called a depression. So if you give credit to the Fed for halting depressions, they haven’t. Ity’s just a matter of semantics.

Depression is a very fitting word if those numbers are even close to what’s going to happen.

The Fed blew three economic bubbles in succession. A deflationary bust has started. They blew bubbles trying to prevent “deflation” defined as falling consumer prices.

BIS Deflation Study

The BIS did a historical study and found routine price deflation was not any problem at all.

“Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive,” stated the BIS study.

Deflation is not really about prices. It’s about the value of debt on the books of banks that cannot be paid back by zombie corporations and individuals.

Blowing bubbles in absurd attempts to arrest “price deflation” is crazy. The bigger the bubbles the bigger the resultant “asset bubble deflation”. Falling consumer prices do not have severe negative repercussions. Asset bubble deflations are another matter.

Assessing the Blame

Central banks are not responsible for the coronavirus. But they are responsible for blowing economic bubbles prone to crash.

The equities bubbles before the coronavirus hit were the largest on record.

Dollar Irony

The irony in this madness is the US will be printing the most currency and have the biggest budget deficits as a result. Yet central banks can’t seem to get enough dollars. In that aspect, the dollar ought to be sinking.

But given the US 10-year Treasury yield at 1.126% is among the highest in the world, why not exchange everything one can for dollars earning positive yield.

This is all such circular madness, it’s hard to say when or how it ends.

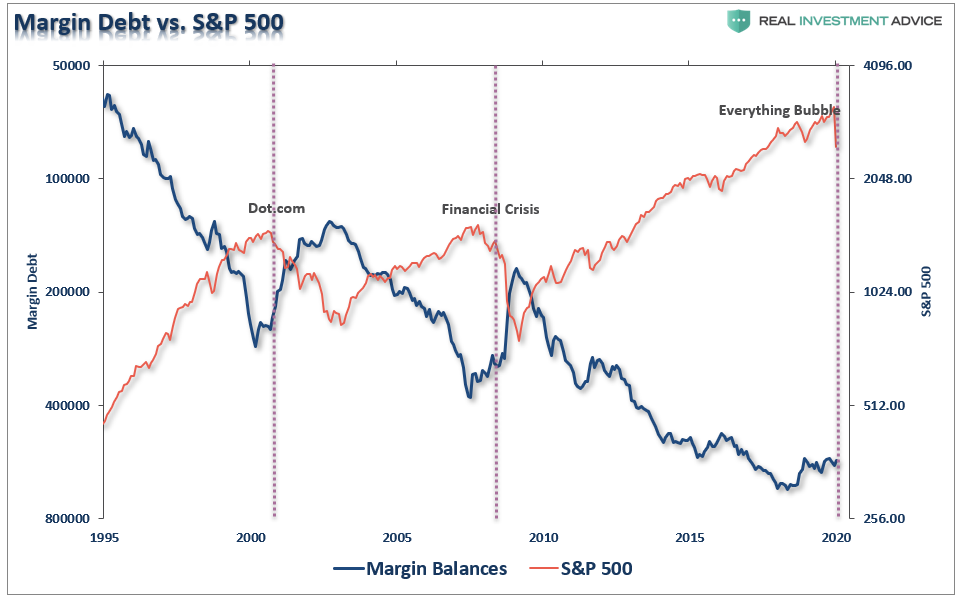

Margin Call: You Were Warned Of The Risk

I have been slammed with emails over the last couple of days asking the following questions:

“What just happened to my bonds?”

“What happened to my gold position, shouldn’t it be going up?”

“Why are all my stocks being flushed at the same time?”

“Stocks down, Bonds down, credit down, gold down, oil down, copper down, crypto down, global systemically important banks down, and liquidity down…

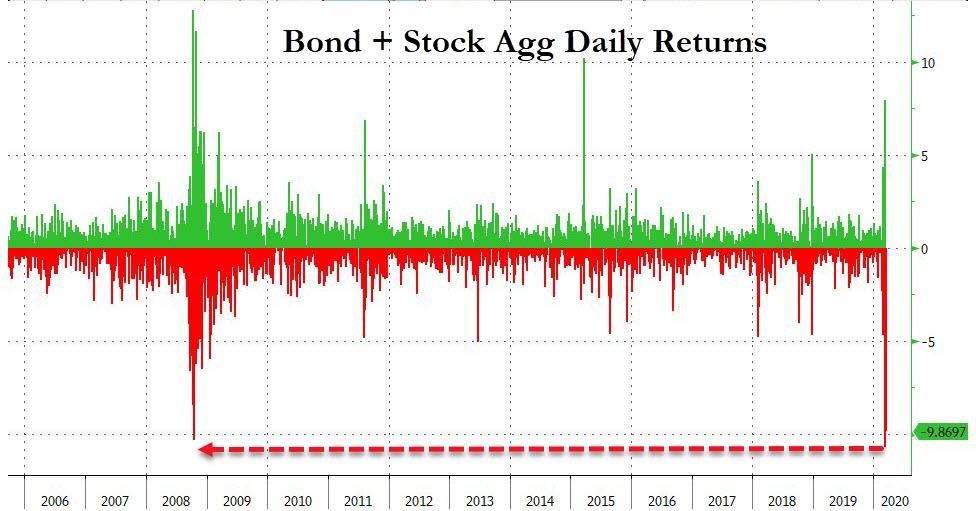

Today was the worst day for a combined equity/bond portfolio… ever…”

This Is What A “Margin Call,” Looks Like.

In December 2018,we warned of the risk. At that time, the market was dropping sharply, and Mark Hulbert wrote an article dismissing the risk of margin debt. To wit:

“Plunging margin debt may not doom the bull market after all, reports to the contrary notwithstanding.

According to research conducted in the 1970s by Norman Fosback, then the president of the Institute for Econometric Research, there is an 85% probability that a bull market is in progress when margin debt is above its 12-month moving average, in contrast to just a 41% probability when it’s below.

Why, then, do I suggest not becoming overly pessimistic? For several reasons:

1) The margin debt indicator issues many false signals

2) There is insufficient data

3) Margin debt is a strong coincident indicator.”

I disagreed with Mark on several points at the time. But fortunately the Federal Reserve’s reversal on monetary policy kept the stock market from sinking to levels that would trigger “margin calls.”

As I noted then, margin debt is not a technical indicator that can be used to trade markets. Margin debt is the “gasoline,” which drives markets higher as the leverage provides for the additional purchasing power of assets. However, that “leverage” also works in reverse as it provides the accelerant for larger declines as lenders “force” the sale of assets to cover credit lines without regard to the borrower’s position.

That last sentence is the most important and is what is currently happening in the market.

The issue with margin debt, in terms of the biggest risk, is the unwinding of leverage is NOT at the investor’s discretion.

It is at the discretion of the broker-dealers that extended that leverage in the first place. (In other words, if you don’t sell to cover, the broker-dealer will do it for you.)

When lenders fear they may not be able to recoup their credit-lines, they force the borrower to either put in more cash or sell assets to cover the debt. The problem is that “margin calls” generally happen all at once as falling asset prices impact all lenders simultaneously.

Margin debt is NOT an issue – until it is.

When an “event” occurs that causes lenders to “panic” and call in margin loans, things progress very quickly as the “math” becomes a problem. Here is a simple example.

“If you buy $100,000 of stock on margin, you only need to pay $50,000. Seems like a great deal, especially if the stock price goes up. But what if your stock drops to $60,000? Suddenly, you’ve lost $40,000, leaving you with only $10,000 in your margin account. The rules state that you need to have at least 25 percent of the $60,000 stock value in your account, which is $15,000. So not only do you lose $40,000, but you have to deposit an additional $5,000 in your margin account to stay in business.“

However, when margin calls occur, and equity is sold to meet the call, the equity in the portfolio is reduced further. Any subsequent price decline requires additional coverage leading to a “death spiral” until the margin line is covered.

Example:

$100,000 portfolio declines to $60,000. Requiring a margin call of $5000.

You have to deposit $5000, or sell to cover.

However, if you don’t have the cash, then a problem arises. The sell of equity reduces the collateral requirement requiring a larger transaction: $5000/.25% requirement = $20,000

With the margin requirement met, a balance of $40,000 remains in the account with a $10,000 margin requirement.

The next morning, the market declines again, triggering another margin call.

Wash, rinse, repeat until broke.

This is why you should NEVER invest on margin unless you always have the cash to cover.

Just 20%

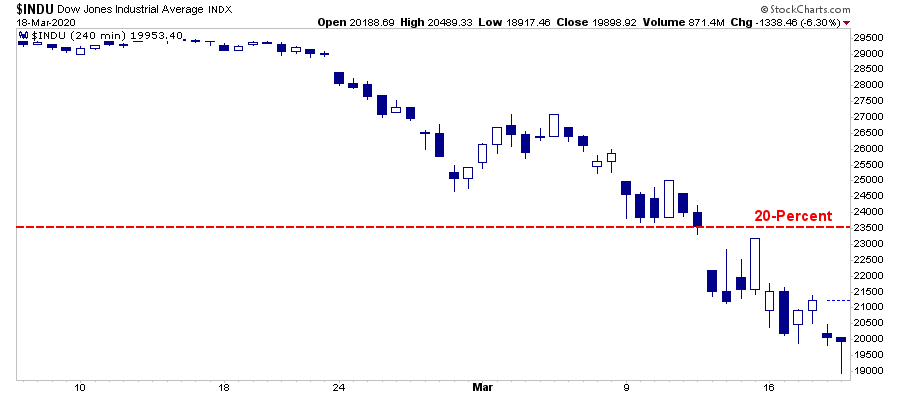

As I discussed previously, the level we suspected would trigger a margin event was roughly a 20% decline from the peak.

“If such a decline triggers a 20% fall from the peak, which is around 2340 currently, broker-dealers are likely going to start tightening up margin requirements and requiring coverage of outstanding margin lines.

This is just a guess…it could be at any point at which “credit-risk” becomes a concern. The important point is that ‘when’ it occurs, it will start a ‘liquidation cycle’ as ‘margin calls’ trigger more selling which leads to more margin calls. This cycle will continue until the liquidation process is complete.

The Dow Jones provided the clearest picture of the acceleration in selling as “margin calls” kicked in.

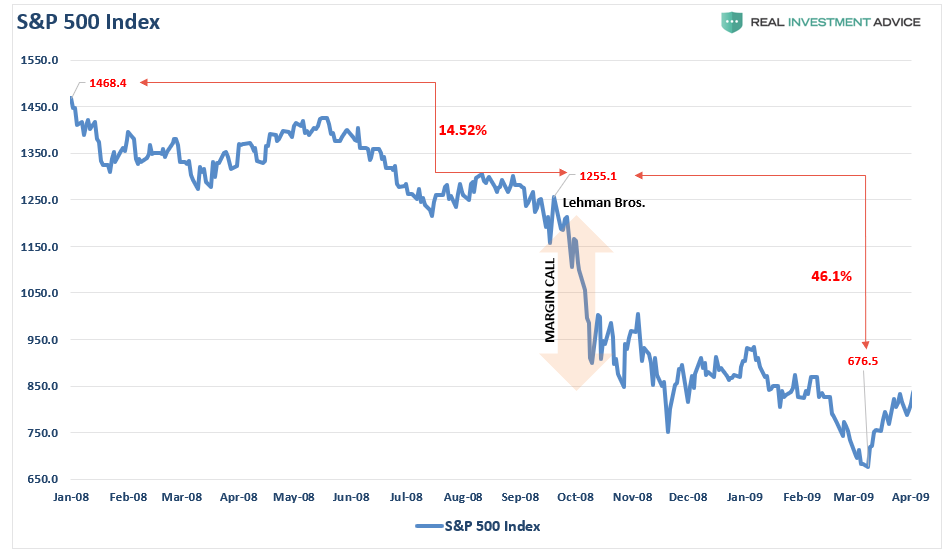

The last time we saw such an event was in 2008.

How Much More Is There To Go?

Unfortunately, FINRA only updates margin debt with about a 2-month lag.

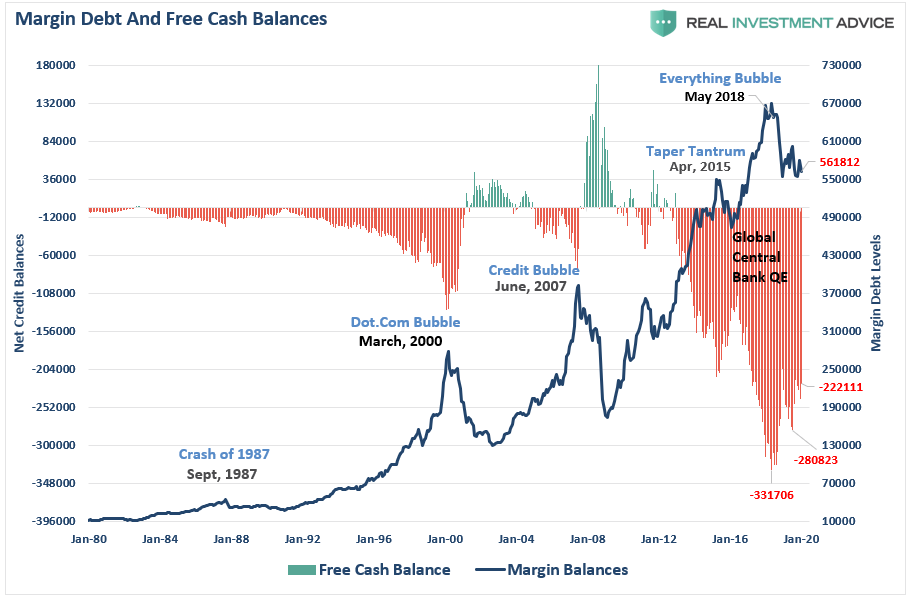

Mark’s second point was a lack of data. This isn’t actually the case as margin debt has been tracked back to 1959. However, for clarity, let’s just start with data back to 1980. The chart below tracks two things:

The actual level of margin debt, and;

The level of “free cash” balances which is the difference between cash and borrowed funds (net cash).

As I stated above, since the data has not been updated since January, the current level of margin, and negative cash balances, has obviously been reduced, and likely sharply so.

However, previous “market bottoms,” have occurred when those negative cash balances are reverted. Given the extreme magnitude of the leverage that was outstanding, I highly suspect the “reversion” is yet complete.

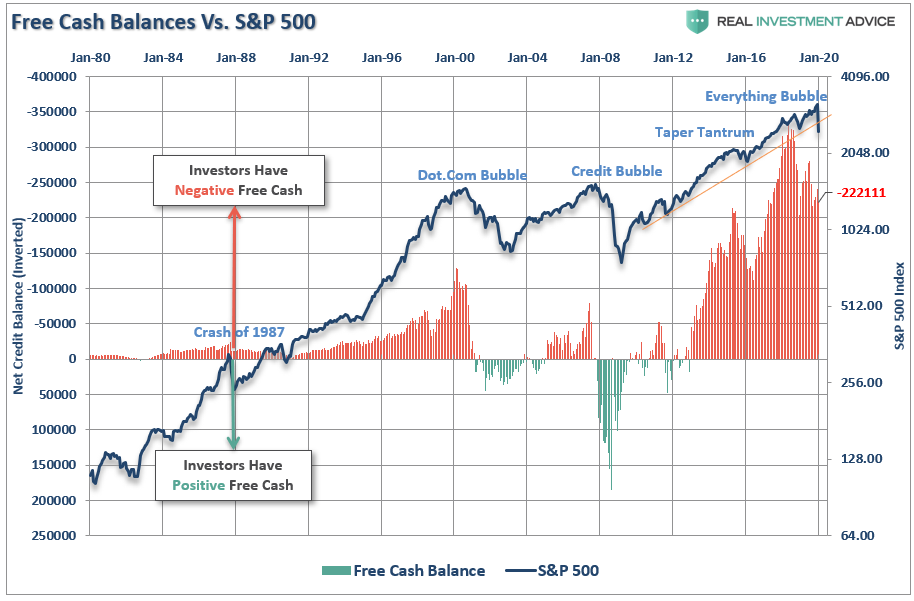

The relationship between cash balances and the market is better illustrated in the next chart. I have inverted free cash balances, to show the relationship between reversals in margin debt and the market. Given the market has only declined by roughly 30% to date, there is likely more to go. This doesn’t mean a fairly sharp reflexive bounce can’t occur before a further liquidation ensues.

If we invert margin debt to the S&P 500, you can see the magnitude of both previous market declines and margin liquidation cycles. As stated, this data is as of January, and margin balances will be substantially lower following the recent rout. I am just not sure we have “squeezed” the last bit of blood out of investors just yet.

You Were Warned

I warned previously, the idea that margin debt levels are simply a function of market activity, and have no bearing on the outcome of the market, was heavily flawed.

“By itself, margin debt is inert.

Investors can leverage their existing portfolios and increase buying power to participate in rising markets. While ‘this time could certainly be different,’ the reality is that leverage of this magnitude is ‘gasoline waiting on a match.’

When an event eventually occurs, it creates a rush to liquidate holdings.The subsequent decline in prices eventually reaches a point that triggers an initial round of margin calls. Since margin debt is a function of the value of the underlying ‘collateral,’ the forced sale of assets will reduce the value of the collateral, triggering further margin calls. Those margin calls will trigger more selling, forcing more margin calls, so forth and so on.

That event was the double-whammy of collapsing oil prices and the economic shutdown in response to the coronavirus.

While it is certainly hoped by many that we are closer to the end of the liquidation cycle, than the beginning, the dollar funding crisis, a blowout in debt yields, and forced selling of assets, suggests there is likely more pain to come before we are done.

It’s not too late to take actions to preserve capital now, so you have capital to invest later.

“With our risk limits hit, and in order to protect our clients from both financial and emotional duress, we made the decision that even the reduced risk we were carrying was still too much.

The good news is that a great ‘buying’ opportunity is coming. Just don’t be in a ‘rush’ to try and buy the bottom.

I can assure you, when we ultimately see a clear ‘risk/reward’ set up to start taking on equity risk again, we will do so ‘with both hands.’

And we are sitting on a lot of cash just for that reason.”

You can’t “buy low,” if you don’t have anything to “buy with.”

The Problem With Pragmatism… and Inflation

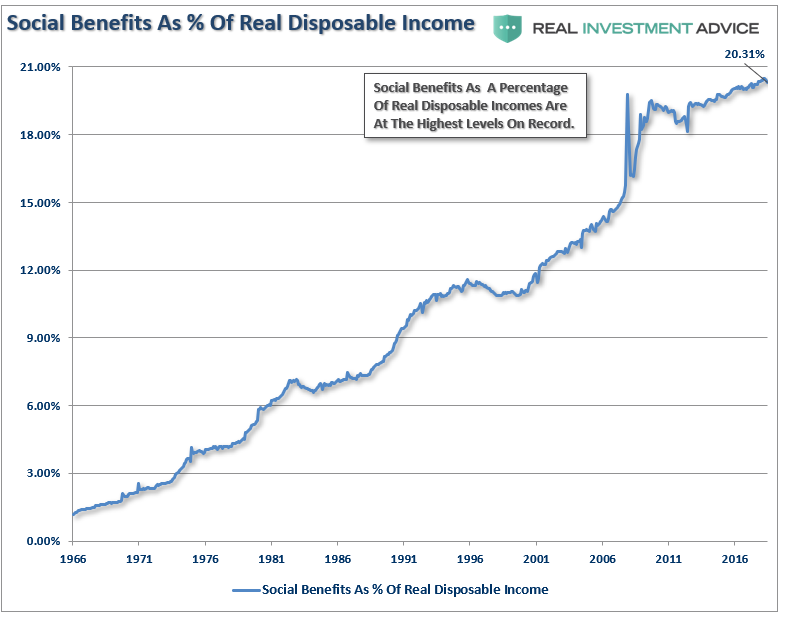

Pragmatism is seeking immediate solutions with little to no consideration for the longer-term benefits and consequences. An excellent example of this is the Social Security system in the United States. In the Depression-era, a government-sponsored savings plan was established to “solve” for lack of retirement savings by requiring contributions to a government-sponsored savings plan. At the time, the idea made sense as the population was greatly skewed towards younger people. No one seriously considered whether there would always be enough workers to support benefits for retired people in the future. Now, long after those policies were enacted and those that pushed the legislation are long gone, the time is fast approaching when Social Security will be unable to pay out what the government has promised.

Pragmatism is the common path of governments, led by politicians seeking re-election and the retention of power. Instead of considering the long-term implications of their policies, they focus on satisfying an immediate desire of their constituents.

In his book Economics in One Lesson, Henry Hazlitt made this point very clear by elaborating on the problems that eventually transpire from imprudent monetary and fiscal policy.

“The art of economics consists in looking not merely at the immediate but at the longer effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups.

Nine-tenths of the economic fallacies that are working such dreadful harm in the world today are the result of ignoring this lesson.”

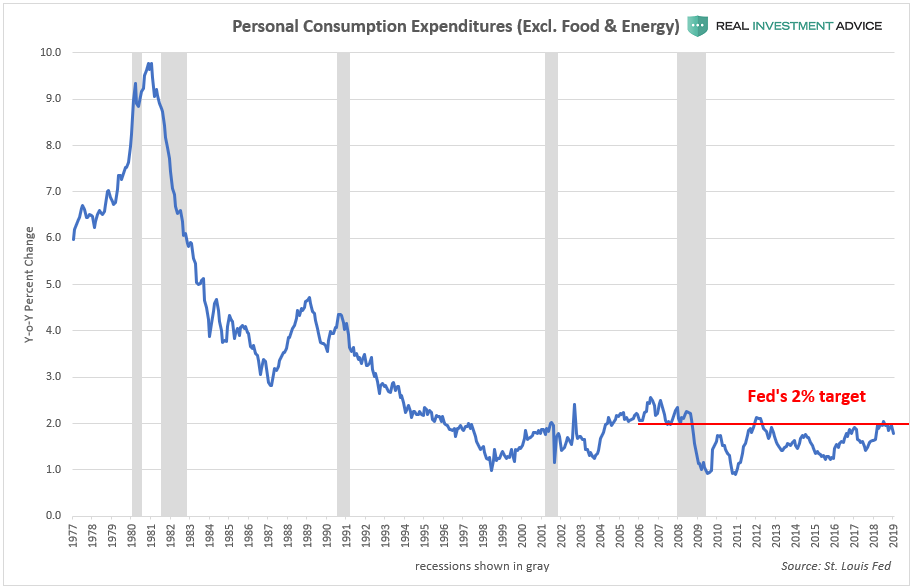

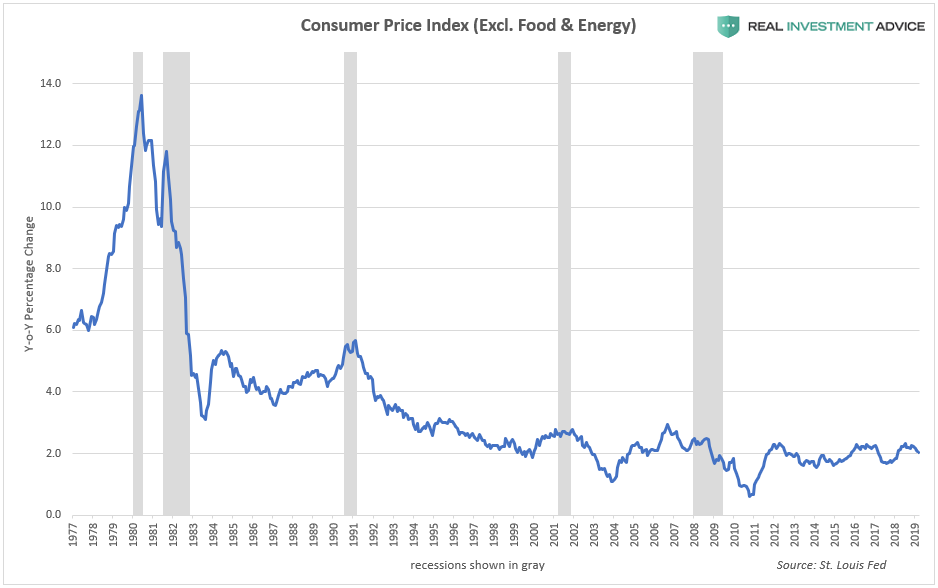

Inflation

One of the most pernicious of these issues in our “modern and sophisticated” intellectual age is that of inflation. When asked to define inflation, most people say “rising prices,” with no appreciation for the fact that price movements are an effect, not a cause. They are a symptom of monetary circumstances. Inflation is a disequilibrium between the amounts of currency entering an economic system relative to the productive output of that same system.

In today’s world, there is only fiat (“by decree”) currencies. In other words, the value of currencies are not backed by some physical commodity such as gold, silver, or oil. Currencies are only backed by the perceived productive capacity of the nation and the stability of the issuing government. If a government takes unreasonable measures in managing its fiscal and monetary affairs, then the standard of living in that society will deteriorate, and confidence in it erodes.

Put another way, when the people of a nation or its global counterparts lose confidence in the fiscal and monetary policy-makers, the result is a loss of confidence in the medium of exchange, and a devaluation of the currency ensues. The influence of those in power will ultimately prove to be unsustainable.

Inflation is an indicator of confidence in the currency as a surrogate of confidence in the policies of a government. It is a mirror. This is why James Grant is often quoted as saying, “The gold price is the reciprocal of the world’s faith in central banking.”

Confidence in a currency may be lost in a variety of ways. The one most apparent today is creating too many dollars as a means of subsidizing the spending habits of politicians and the borrowing demands of corporations and citizens.

Precedent

There is plenty of modern-day historical precedent for a loss of confidence from excessive debt creation and the inevitable excessive currency creation. Weimar Germany in the 1920s remains the modern era poster child, but Zimbabwe, Argentina, and Venezuela also offer recent examples.

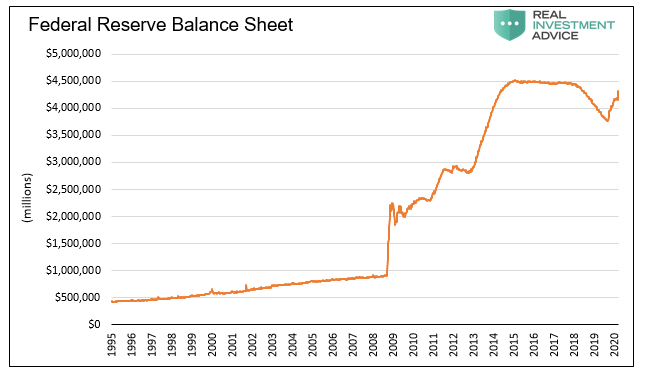

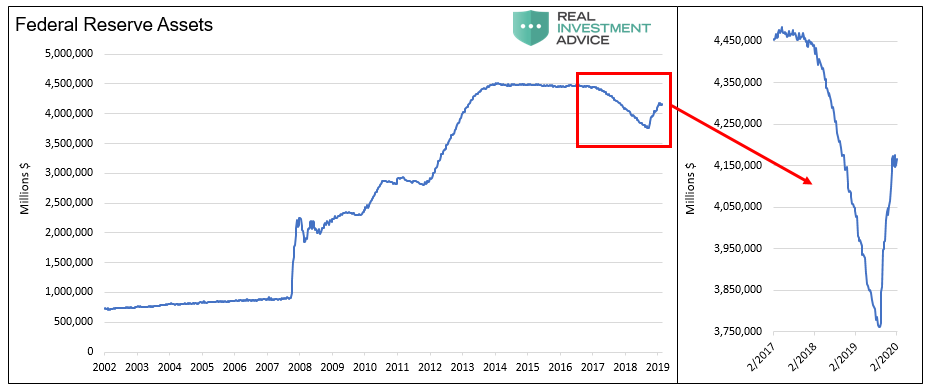

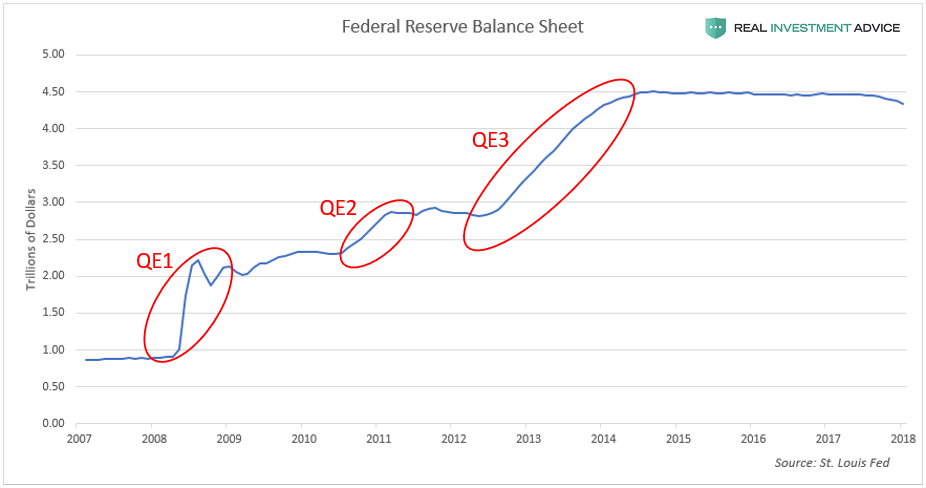

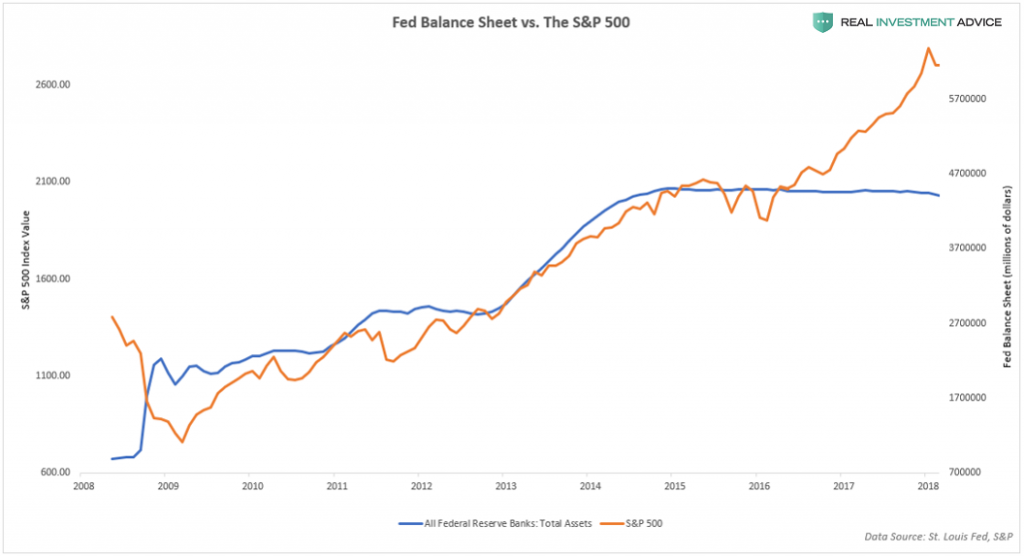

Following the 2008 financial crisis, many believed that the actions of the Federal Reserve were “heroic.” Despite failing to see the warning signs of a housing bubble in the months and even years leading up to the crisis, the Fed’s perspective was that it exists to provide liquidity. As the chart below illustrates, that is precisely what they did.

Data Courtesy Bloomberg

That pragmatic response failed to heed Hazlitt’s warning. What are the longer-term effects for the economy, the bailed-out banking system, and all of us? How would these policies affect the economy, markets, society, and the wealth of the nation’s citizens in five, ten, or twenty years?

Keeping interest rates at a low level for many years following the financial crisis while the economy generally appears to have recovered raises other questions. The Fed continues to argue that inflation remains subdued. That argument goes largely undisputed despite credible evidence to the contrary. Further, it provides the Fed a rationalization for keeping rates well below normal.

Politicians who oversee the Fed and want to retain power, consent to low-rate policies believing it will foster economic growth. While that may make sense to some, it is short-sighted and, therefore, pragmatic. The assessment does not account for a variety of other complicating factors, namely, what may transpire in the future as a result? Are seeds of excess being sown as was the case in the dot-com bubble and the housing bubble? If so, can we gauge the magnitude?

Policy Imposition

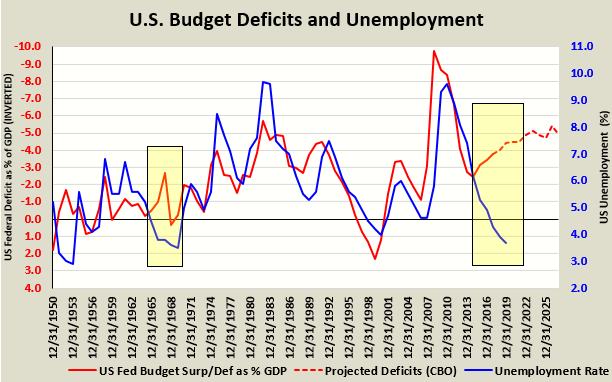

In the mid-1960s, President Lyndon Johnson sought to escalate U.S. involvement in the Vietnam War. In doing so, he knew he would need the help of the Fed to hold interest rates down to run the budget deficits required to fund that war. Although then-Fed Chairman William McChesney Martin was reluctant to ease monetary policy, he endured various forms of abuse from the Oval Office and finally acquiesced.

The bullying these days comes from President Trump. Although his arguments for easier policy contradict what he said on the campaign trail in 2016, Jerome Powell is compliant. Until recently, the economy appeared to be running at full employment and all primary fundamental metrics were well above the prior peaks set in 2007.

Additionally, Congress, at Trump’s behest and as the chart below illustrates, has deployed massive fiscal stimulus that created a yawning gap (highlighted) between fiscal deficits and the unemployment picture. This is a divergence not seen since the Johnson administration in the 1960s (also highlighted) and one of magnitude never seen. As is very quickly becoming clear, those actions both monetary and fiscal, were irresponsible to the point of negligence. Now, when we need it most as the economy shuts down, there is little or no “dry powder”.

Data Courtesy Bloomberg

President Johnson got his way and was able to fund the war with abnormally low interest rates. However, what ensued over the next 15 years was a wave of inflation that destroyed the productive capacity of the economy well into the early 1980s. Interest rates eventually rose to 18%, and economic dynamism withered as did the spirits of the average American.

The springboard for that scenario was a pragmatic policy designed to solve an immediate problem with no regard for the future. Monetary policy that suppressed interest rates and fiscal policy that took advantage of artificially low interest rates to accumulate debt at a relatively low cost went against the American public best interests. The public could not conceive that government “of, by and for the people” would act in such a short-sighted and self-serving manner.

Data Courtesy Bloomberg

The Sequel

Before the COVID-19 pandemic, the Congressional Budget Office (CBO) projections for U.S. budget deficits exceeded $1 trillion per year for the next 10-years. According to the CBO, the U.S. Treasury’s $22.5 trillion cumulative debt outstanding was set to reach $34.5 trillion by 2029, and that scenario assumed a very optimistic GDP growth of 3% per year. Further, it laughably assumed no recession will occur in the next decade, even though we are already in the longest economic expansion since the Civil War. In the event of a recession, a $1.8 trillion-dollar annual deficit would align with average historical experience. Given the severity of what is evident from the early stages of the pandemic, that forecast may be very much on the low end of reality.

The 1960s taught us that monetary and fiscal policy is always better erring on the side of conservatism to avoid losing confidence in the currency. Members of the Fed repeatedly tell the public they know this. Yet, if that is the case, why would they be so influenced by a President focused on marketing for re-election purposes? Alternatively, maybe the policy table has been set over the past ten years in a way that prevents them from taking proper measures? Do they assume they would be rejected despite the principled nature of their actions?

Summary

Inflation currently seems to be the very least of our worries. Impeachment, Iran, North Korea and climate change were all crisis head fakes.

The Fed was also distracted by what amounted to financial dumpster fires in the fall of 2019. After a brief respite, the Fed’s balance sheet began surging higher again and they cut the Fed Funds rate well before there was any known threat of a global pandemic. What is unclear is whether imprudent fiscal policies were forcing the Fed into imprudent monetary policy or whether the Fed’s policies, historical and current, are the enabler of fiscal imprudence. Now that the world has changed, as it has a habit of doing sometimes even radically, policymakers and the collective public are in something of a fine mess to understate the situation.

Now we are contending with a real global financial, economic, and humanitarian threat and one that demands principled action as opposed to short-sighted pragmatism.

The COVID-19 pandemic is clearly not a head fake nor is it a random dumpster fire. Neither is it going away any time soon. Unlike heads of state or corporate CEOs, biological threats do not have a political agenda and they do not care about the value of their stock options. There is nothing to negotiate other than the effectiveness of efforts required to protect society.

Given the potential harm caused by the divergence between stimulus and economic fundamentals, it would be short-sighted and irresponsibly pragmatic to count out the prospect of inflation. Given the actions of the central bankers, it could also be the understatement of this new and very unusual decade.

Shedlock: Supply And Demand Shocks Coming Up

Dual economic shocks are underway simultaneously. There are shortages of some things and lack of demand for others.

The coronavirus is delivering a one-two punch to the world economy, laying it low for months to come and forcing investors to reprice equities and bonds to account for lower company earnings.

From one side, the epidemic is hammering the capacity to produce goods as swathes of Chinese factories remain shuttered and workers housebound. That’s stopping production of goods there and depriving companies elsewhere of the materials they need for their own businesses.

With the virus no longer contained to China, increasingly worried consumers everywhere are reluctant to shop, travel or eat out. As a result, companies are likely not only to send workers home, but to cease hiring or investing — worsening the hit to spending.

How the two shocks will reverberate has sparked some debate among economists, with Harvard University Professor Kenneth Rogoff writing this week that a 1970s style supply-shortage-induced inflation jolt can’t be ruled out. Others contend another round of weakening inflation is pending.

Some economists argue that what’s happened is mostly a supply side shock, others have highlighted the wallop to demand as well, to the degree that the distinction matters.

Slowest Since the Financial Crisis

Inflationary or Deflationary?

In terms of prices, it’s a bit of both, but mostly the latter.

There’s a run on sanitizers, face masks, toilet paper ect. Prices on face masks, if you can find them, have gone up.

But that is dwarfed by the demand shock coming from lack of wages for not working, not traveling, not eating out etc.

The lost wages for 60 million people in China locked in will be a staggering hit alone.

That has also hit Italy. It will soon hit the US.

Next add in the fear from falling markets. People, especially boomers proud of their accounts (and buying cars like mad) will stop doing so.

It will be sudden.

Bad Timing

COVID-19 comes at a tricky time for the global economy. Take Japan. The Oct sales tax hike saw GDP fall 1.6% q/q in Q4, taking year-over-year growth negative (black). That's a weak base even before factoring in Q1 deterioration in the manufacturing (blue) & services (red) PMIs… pic.twitter.com/iUZwQ1U2LA

'The stockpiling crisis that has hit supermarkets across Asia has spread to Europe as consumers start hoarding groceries and hygiene products amid fears of a coronavirus pandemic.' https://t.co/uV5OK1zLJj

Like in many other places, Euro zone is vulnerable to COVID-19 because its starting point is so weak. Growth in Q4 was just 0.1% q/q and it's hard to see how 2020 will be much better than 0.5% overall, far below the ECB forecast of 1.1% (as of Dec). Deflation risk is rising… pic.twitter.com/oLUbIKwHLg

The COVID-19 shock is likely to accelerate the structural shift away from brick & mortar retail in the US. Growth in core retail sales was already weak through Jan, even before virus anxiety built (top lhs). COVID-19 is, unfortunately, another reason to order online (top rhs)… pic.twitter.com/feu30pC4pW

There's a debate if COVID-19 is a supply or demand shock. There's evidence of supply disruption in longer delivery times in manufacturing. But we don't for a second worry that prices will rise, because weak demand swamps all that. Net net: negative demand shock dominates by far. pic.twitter.com/OtyMoJHTDT

Deflation is not really about prices. It’s about the value of debt on the books of banks that cannot be paid back by zombie corporations and individuals.

That is what the Fed fears. It takes lower and lower yields to prevent a debt crash. But it is entirely counterproductive and it does not help the consumer, only the asset holders. Fed (global central bank) policy is to blame.

These are the important point all the inflationistas miss.

Our Triple-C Rated Economy: Complacency, Contradictions, and Corona

“I got my toes in the water, ass in the sand

Not a worry in the world, a cold beer in my hand

Life is good today, life is good today” – Toes, Zac Brown Band

The economic

and social instabilities in the U.S. are numerous and growing despite the fact

that many of these factors have been in place and observable for years.

Overvaluation of equity markets

Weak GDP Growth

High Debt to GDP levels

BBB Corporate Debt at Record Levels

High Leverage and Margin Debt

Weak Productivity

Growing Fiscal Deficits

Geopolitical uncertainty

Acute Domestic Political Divisiveness

Rising Populism

Trade Wars

Corona Virus

As we know, this list could be extended for pages, however, the one thing that will never show up on this list is…?

Inflation.

Inflation

As reported

by the Bureau of Labor Statistics (BLS) and the Bureau of Economic Analysis

(BEA), inflation has been running above 2% for the better part of the last few

years. Despite CPI being greater than their 2% target, the Federal Reserve

(Fed) has been wringing their hands about the lack of inflation. They insist

that inflation, as currently measured, is too low. We must disclaim, this all

assumes we should have confidence in these measurements.

At his

January 29, 2020 press conference, Chairman Powell stated:

“…inflation

that runs persistently below our objective can lead longer-term inflation

expectations to drift down, pulling actual inflation even lower. In turn,

interest rates would be lower, as well, closer to their effective lower bound.

As a

result, we would have less room to reduce interest rates to support the economy

in a future downturn to the detriment of American families and businesses. We

have seen this dynamic play out in other economies around the world and we’re

determined to avoid it here in the United States.”

Contradictions

There are a couple of inconsistencies in Powell’s comments

from the most recent January 2020 post-FOMC press conference. These are issues

we have become increasingly interested in exploring because of the seeming

incoherence of Fed policy. Further, as investors, high valuations and PE

multiple expansion appear predicated upon “favorable” monetary policy. If

investors are to rely on the Fed, they would be well-advised to understand them and properly judge their coherence.

As discussed in Jerome

Powell & the Fed’s Great Betrayal,

Powell states that the supply of money that the Fed provides to the system is

to be based on the demand for money – not the economic growth rate. That is a

major departure from orthodox monetary policy. If investors had been paying

attention, the bond market should have melted down on that one sentence. It did

not because the market pays attention to the current implications for the Fed’s

actions, not the future shock of such a policy. It is a myopic curse that

someday could prove costly to investors.

As for Powell’s quote above, the first inconsistency is that

the circumstances they have seen “play

out in other countries” have not shown itself in the U.S. To front-run

something that has not occurred assumes you are correct to anticipate it

occurring in the future. It is pure speculation and quite a leap even for those smart PhDs at the

Fed.

“Overall, the U.S. economy appears likely

to expand at a moderate pace over the second half of 2007, with growth then

strengthening a bit in 2008 to a rate close to the economy’s underlying trend.” – Ben Bernanke, Testimony to Senate Banking

Committee, July 2007

Although we

have not actually seen this “dynamic” play out in the U.S. since the great

depression, Fed officials are so concerned about deflation that they have begun

telegraphing their intent to allow inflation to overshoot their 2% target. Based

on current Fed guidance, periods of lesser inflation would be offset by periods

of higher inflation.

Our question

is, how do they come to that conclusion and based on what analytical rigor and evidence? There is, by the way, evidence from other countries throughout

the history of humanity, that when money is printed to accommodate the spending

incontinence of politicians, people lose confidence in the domestic currency.

That would be devastatingly inflationary, and it is, without question of

measurements, where we are headed.

The next inconsistency

is that the Fed’s protracted engagement in quantitative easing (QE) over the

past ten years has created precisely the circumstances about which Powell warns

here – “less room to reduce interest rates… to the detriment of American

families and businesses.”

The Chairman

of the U.S. Fed, Jerome Powell, should understand how supply and demand works,

but as a reminder, the less available something is, everything else constant,

the more it is worth. Mr. Chairman, your predecessors removed $3.5 trillion of

bonds from the market, what did you think would happen to bond prices and

therefore yields?

Powell stumbled

head-first into that self-contradiction, especially after watching the

fantastic failure to normalize rates through rate hikes and quantitative

tightening (QT) earlier in 2019, which caused him to perform a hasty 180-degree

policy reversal in the fall of 2019.

We think this is a workable plan, and

it will, as one of my colleagues, President Harker, described it, it will be

like watching paint dry, that this will just be something that runs quietly in

the background. –

Janet Yellen, Federal Reserve Chairman, June 14, 2017, FOMC Press Conference

Contrary to the

reassurances of Janet Yellen and many other Fed members, it (QT) was a lot more

exciting than watching paint dry. That too is troubling.

Wise Owl

In a recent

interview on RealVision TV, James Grant, publisher of Grants Interest Rate

Observer said:

“Is

inflation a thing of the past?… are forces in place today that could

reproduce [the great inflation of the 1970s? Inflation by definition,

represents a loss of confidence in money. How do you lose confidence in money?

Well, you create too much of it to subsidize the spending habits of the

politicians. That’s one possible cause and are we on the way to something like

that? Well, possibly. In this splendid economy, we’re generating a

trillion-dollar budget deficit.”

Grant

continues:

“Then

two, there is the physical structure of the economy. We live in a world of

expedited delivery of just in time rather than just in case. We live in a world

of ubiquitous information about supply chains, but maybe if push comes to shove

in the world of geopolitics, the supply chains might break. Lo and behold, we

might be on our own in America for things we now import, and if we are, those

prices would not be so low, they would be much higher.”

Again,

pointing back to our recent article referenced above, Jerome Powell &

the Fed’s Great Betrayal, there are other indicators of inflation that

contradict what the Fed believes. In that article, we discussed real-world

examples such as M2 growth, and auto and housing prices, to contrast with the BLS

and Fed engineered metrics. Despite a plethora of readily available data to the

contrary, we are continually reminded by the Fed of the absence of inflation.

As we know,

the Fed just began another round of radical policy accommodation to incite higher

inflation. If you pre-suppose a confluence of circumstances that begins to

constrict global supply chains, then the inflation Grant theorizes might not be

so far-fetched. The Fed, as has historically been the case, would be caught looking

the wrong way, and given their proclivity toward wanting more inflation, it would

almost certainly be too late to respond.

“Moreover, the agencies have made

clear that no bank is too-big-too-fail, so that bank management, shareholders,

and un-insured debt holders understand that they will not escape the

consequences of excessive risk-taking. In short, although vigilance is

necessary, I believe the systemic risk inherent in the banking system is

well-managed and well-controlled.” – Benjamin S. Bernanke Fed Chairman confirmation hearing

November 15, 2005

“Rather than making management,

shareholders, and debt holders feel the consequences of their risk-taking, you

bailed them out. In short, you are the definition of moral hazard.” – Senator Jim Bunning at Bernanke

second confirmation hearing December 3, 2009

In the same way, there were recorded levels of laughter

in FOMC meetings at the absurd incentives homebuilders were offering to sell houses

in 2004, 2005, and 2006. The Fed is now equally blind, neglect, and arrogant concerning

the perceived absence of inflation. The laughter in the Eccles Building

boardroom stopped abruptly in mid-2007 as the housing market stalled. The Coronavirus

may be a similar wake-up call with serious economic consequences.

Here and

Now

The

situation that is developing illustrates the one-dimensional nature of Fed

thinking. Despite having the latest news

on the spread of the Corona Virus at the January 29, 2020 Federal Open Market

Committee (FOMC) meeting, the Fed’s concern was for a slowdown in global growth

and failed attempts to prime inflation. There was no consideration for

possible second and third-order effects of the virus.

What are the

possible second and third-order effects? They are the things that follow after

the obvious occurs. In this case, there is no question that China’s growth is

going to be hurt by the virus and quarantines, the restrictions on flight and

travel, and factory shutdowns. That is obvious.

Consider the

virus is now spreading rapidly to other suppliers of U.S. goods and services

such as Korea, Japan, and Italy. What might not be obvious is that the growing

problem will impede global commerce and cause fractures in the extensive and

complex network of global supply chains. Goods and services we are accustomed

to finding on the shelves of the local Wal-Mart or via the internet may not be

available to us, or if they are, they may come at a cost well above the price

we paid before the pandemic. If that occurs, those changes in prices will eventually

find their way to the BLS inflation data collectors, and then, as the old

saying goes, all bets are off.

Summary

There are

plenty of uncertainties in the world. Individuals have the decision-making

ability to evaluate those uncertainties and the risks they pose. That said, it

is difficult to remember a time when the potential turbulence we face has been

so broadly ignored by the “market” and so overlooked by the Fed and politicians.

It is as though we have been tranquilized by the ever-rising stock market and

net worth as an artifact of that fallacious indicator of security.

By all

appearances, stock index levels convey not a worry in the world. Indeed, life

is good today. We are just not so sure about tomorrow.

Why “Not-QE” is QE: Deciphering Gibberish

“I guess I should warn you, if I turn out to be particularly clear, you’ve probably misunderstood what I’ve said.” – Alan Greenspan

Imagine if Federal Reserve (Fed)

Chairman Jerome Powell told the American people they must pay more for the goods

and services they consume.

How long would it take for mobs with pitchforks

to surround the Mariner Eccles building?

However, Jerome Powell and every other member of the Fed routinely and consistently

convey pro-inflationary ideals, and there is nary a protest, which seems odd.

The reason for the American public’s complacency is that the Fed is not that direct

and relies on carefully crafted language and euphemisms to describe the desire

for higher inflation.

To wit, the following statements from past

and present Fed officials make it all but clear they want more inflation:

“That is why it is essential that we at the

Fed use our tools to make sure that we do not permit an unhealthy downward

drift in inflation expectations and inflation,” – Jerome Powell November

2019

“In order to move rates up, I would want to

see inflation that’s persistent and that’s significant,” -Jerome Powell

December 2019

“Been very challenging to get inflation back

to 2% target” -Jerome Powell December 2019

“Ms. Yellen also said that continuing low

inflation, regarded as a boon by many, could be “dangerous” – FT – November

2017

“One way to increase the scope for monetary

policy is to retain the Fed’s current focus on hitting a targeted value of

inflation, but to raise the target to, say, 3 or 4 percent.” –Ben

Bernanke October 2017

“Further weakness in inflation could prompt

the U.S. Federal Reserve to cut interest rates, even if economic growth

maintains its momentum” -James

Bullard, President of the Federal Reserve Bank of St. Louis May 2019

“Fed Evans Says Low Inflation Readings

Elevating His Concerns” -Bloomberg May 2019

“I believe an aggressive policy

action such as this is required to re-anchor inflation expectations at our

target.” Neel Kashkari, President Minneapolis Fed June

2019

As an aside, it cannot be overemphasized

the policies touted in the quotes above actually result in deflation, an

outcome the Fed desperately fears.

The Fed, and all central banks for

that matter, have a long history of using confusing economic terminology.

Economics is not as complicated as the Fed makes it seem. What does make economics

hard to grasp is the technical language and numerous contradictions the Fed uses

to explain economics and justify unorthodox monetary policy. It is made even

more difficult when the Fed’s supporting cast – the media, Wall Street and other

Fed apologists – regurgitate the Fed’s gibberish.

The Fed’s fourth installment of

quantitative easing (“QE4”, also known as “Not-QE QE”) is vehemently denied as

QE by the Fed and Fed apologists. These

denials, specifically a recent article in the Financial Times (FT), provide us

yet another opportunity to show how the Fed and its minions so blatantly

deceive the public.

What is QE?

QE is a transaction in which the Fed purchases

assets, mainly U.S. Treasury securities and mortgage-backed-securities, via their

network of primary dealers. In exchange for the assets, the Fed credits the participating

dealers’ reserve account at the Fed, which is a fancy word for a place for

dormant money. In this transaction, each dealer receives payment for the assets

sold to the Fed in an account that is essentially the equivalent of a

depository account with the Fed. Via QE, the Fed has created reserves that sit

in accounts maintained by it.

Reserves are the amount of funds required

by the Fed to be held by banks (which we are using interchangeably with

“primary dealer” for the remainder of this discussion) in their Fed account or

in vault cash to back up a percentage of specified deposit liabilities. While

QE is not directly money printing, it enables banks to create loans at a

multiple of approximately ten times the reserves available, if they so choose.

Notice that “Quantitative Easing” is the

preferred terminology for the operations that create additional reserves, not

something easier to understand and more direct like money/reserve printing, Fed

bond buying program, or liquidity injections. Consider the two words used to describe

this policy – Quantitative and Easing. Easing is an accurate descriptor of the

Fed’s actions as it refers to an action that makes financial conditions easier,

e.g., lower interest rates and more money/liquidity. However, what does

quantitative mean? From the Oxford Dictionary, “quantitative” is “relating to, measuring, or measured by the

quantity of something rather than its quality.”

So, QE is a measure of the amount of

easing in the economy. Does that make sense to you? Would the public be so

complacent if QE were called BBMPO (bond buying and money printing operations)?

Of course not. The public’s acceptance of QE without much thought is a victory

for the Fed marketing and public relations departments.

Is “Not-QE” QE?

The Fed and media are vehemently

defending the latest round of repurchase market (“repo”) operations and T-bill

purchases as “not QE.” Before the Fed even implemented these new measures,

Jerome Powell was quick to qualify their actions accordingly: “My colleagues and I will soon announce

measures to add to the supply of reserves over time,” “This is not QE.”

This new round of easing is QE, QE4, to be

specific. We dissect a recent article from the

FT to debunk the nonsense commonly used to differentiate these recent actions

from QE.

The article presents three factors

that must be present for an action to qualify as QE, and then it rationalizes

why recent Fed operations are something else. Here are the requirements, per

the article:

“increasing the volume of reserves in the

banking system”

“altering the mix of assets held by investors”

“influence investors’ expectations about

monetary policy”

Simply:

providing

banks the ability to make more money

forcing

investors to take more risk and thereby push asset prices higher

steer

expectations about future Fed policy.

Point 1

In the article, White argues “that the US banking system has not

multiplied up the Fed’s injection of reserves.”

That is an objectively false

statement. Since September 2019, when repo and Treasury bill purchase operations

started, the assets on the Fed’s balance sheet have increased by approximately

$397 billion. Since they didn’t pay for those assets with cash, wampum, bitcoin,

or physical currency, we know that $397 billion in additional reserves have

been created. We also know that excess reserves, those reserves held above the

minimum and therefore not required to backstop specified deposit liabilities,

have increased by only $124 billion since September 2019. That means $273

billion (397-124) in reserves were employed (“multiplied up”) by banks to

support loan growth.

Regardless of whether these reserves

were used to back loans to individuals, corporations, hedge funds, or the U.S.

government, banks increased the amount of debt outstanding and therefore the

supply of money. In the first half of 2019, the M2 money supply rose at a 4.0%

to 4.5% annualized rate. Since September, M2 has grown at a 7% annualized rate.

Point 2

White’s second argument against the

recent Fed action’s qualifying as QE is that, because the Fed is buying Treasury

Bills and offering short term repo for this round of operations, they are not

removing riskier assets like longer term Treasury notes and mortgage-backed securities

from the market. As such, they are not causing investors to replace safe investments

with riskier ones. Ergo, not QE.

This too is false. Although by purchasing

T-bills and offering repo the Fed has focused on the part of the bond market

with little to no price risk, the Fed has removed a vast amount of assets in a

short period. Out of necessity, investors need to replace those assets with other

assets. There are now fewer non-risky assets available due to the Fed’s actions,

thus replacement assets in aggregate must be riskier than those they replace.

Additionally, the Fed is offering repo

funding to the market. Repo is largely used by banks, hedge funds,

and other investors to deploy leverage when buying financial assets. By cheapening

the cost of this funding source and making it more readily available, institutional

investors are incented to expand their use of leverage. As we know, this alters

the pricing of all assets, be they stocks, bonds, or commodities.

By way of example, we know that two

large mortgage REITs, AGNC and NLY, have dramatically increased the leverage

they utilize to acquire mortgage related assets over the last few months. They

fund and lever their portfolios in part with repo.

Point 3

White’s third point states, “the Fed is not using its balance sheet to

guide expectations for interest rates.”

Again, patently false. One would have

to be dangerously naïve to subscribe to White’s logic. As described below,

recent measures by the Fed are gargantuan relative to steps they had taken over

the prior 50 years. Are we to believe

that more money, more leverage, and fewer assets in the fixed income universe is

anything other than a signal that the Fed wants lower interest rates? Is

the Fed taking these steps for more altruistic reasons?

Bad Advice

After pulling the wool over his reader’s

eyes, the author of the FT article ends with a little advice to investors:“Rather than obsessing about fluctuations in

the size of the Fed’s balance sheet, then, investors might be better off

focusing on those things that have changed more fundamentally in recent

months.”

After a riddled and generally incoherent explanation about why QE is not QE, White has the chutzpah to follow up with advice to disregard the actions of the world’s largest central bank and the crisis-type operations they are conducting. QE 4 and repo operations were a sudden and major reversal of policy. On a relative basis using a 6-month rate of change, it was the third largest liquidity injection to the U.S. financial system, exceeded only by actions taken following the 9/11 terror attacks and the 2008 financial crisis. As shown below, using a 12-month rate of change, recent Fed actions constitute the single biggest liquidity injection in 50 years of data.

Are we to believe that the latest

round of Fed policy is not worth following? In what is the biggest “tell” that

White is not qualified on this topic, every investment manager knows that money

moves the markets and changes in liquidity, especially those driven by the

central banks, are critically important to follow.

The graph below compares prior balance

sheet actions to the latest round.

Data Courtesy St. Louis Federal Reserve

This next graph is a not so subtle

reminder that the current use of repo is simply unprecedented.

Data Courtesy St. Louis Federal Reserve

Summary

This is a rebuttal to the FT article and

comments from the Fed, others on Wall Street and those employed by the

financial media. The wrong-headed views in the FT article largely parrot those

of Ben Bernanke. This past January he stated the following:

“Quantitative easing works through two

principal channels: by reducing the net supply of longer-term assets, which

increases their prices and lower their yields; and by signaling policymakers’

intention to keep short rates low for an extended period. Both channels helped

ease financial conditions in the post-crisis era.” -LINK

Bourbon, tequila, and beer offer

drinkers’ very different flavors of alcohol, but they all have the same effect. This round of QE may be a slightly

different cocktail of policy action, but it is just as potent as QE 1, 2, and 3

and will equally intoxicate the market as much, if not more.

Keep in mind that QE 1, 2, and 3 were

described as emergency policy actions designed to foster recovery from

an economic crisis. Might that fact be the rationale for claiming this round of

liquidity is far different from prior ones? Altering words to describe clear

emergency policy actions is a calculated effort to normalize those actions.

Normalizing them gives the Fed greater latitude to use them at will, which appears

to be the true objective. Pathetic though it may be, it is the only rationale that

helps us understand their obfuscation.

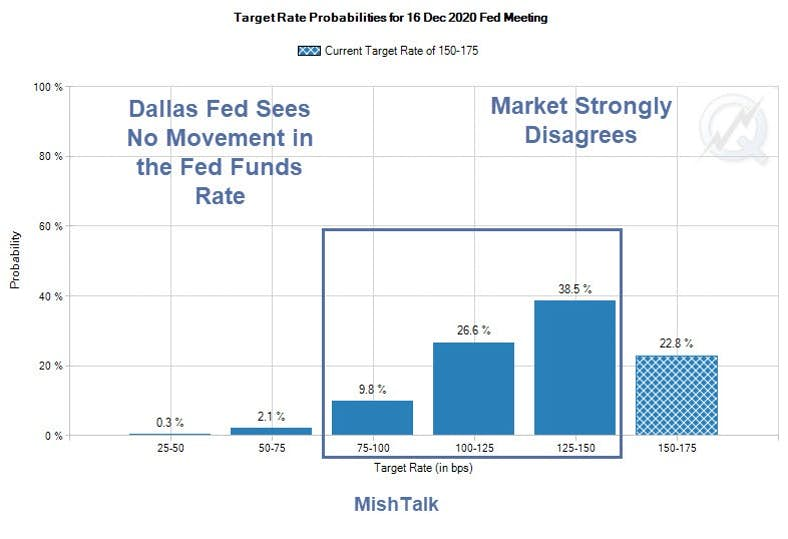

Dallas Fed President Sees “No Move” In Fed Funds Rate

Dallas Fed President Robert Kaplan made some interesting comments today on interest rates, repos, and the coronavirus.

Dallas Fed President Robert Kaplan was on panel discussion today at the University of Texas McCombs School of Business on the “2020 Business Outlook: Real Estate and the Texas Economy” in Austin, Texas.

Bloomberg Econoday Synopsis

Dallas Fed President Robert Kaplan is neutral right now on monetary policy, saying neither a rate cut nor a rate hike are necessary in the medium term. “My base case is no movement up or down in the Fed funds rate [in 2020], but I’ll be monitoring [things] carefully … this year,” Kaplan said in a panel discussion.

Kaplan believes the outlook for the economy has stabilized and if anything has “firmed”, and though he now has “a more confident outlook” he isn’t ready to commit to a rate hike saying it’s “too soon to judge if a hike is coming, and you’ve got a number of [risky] factors going on.”

Regarding a so-called “coronavirus cut” to reassure markets, Kaplan doesn’t see justification yet adding, however, that he is carefully watching how the virus unfolds and that he will have a better sense of its effects over the next few months. Kaplan also noted that he will be watching the first-half impact of the Boeing 737 production shutdown.

On repo operations, Kaplan described the rise in the Fed’s balance sheet through year-end as “substantial” but he sees slowing growth through June. “I’d be hopeful and expect that as we continue bill purchases during the second quarter, the repo usage will begin to decline and the headline net balance-sheet growth for the Fed will moderate – certainly far more moderate than what’s we’ve seen to this period.”

On inflation, Kaplan’s base case is an upward trend toward 2 percent in the medium term. Kaplan said the Fed is debating whether to lengthen out its look at inflation from a one-year average to perhaps a two-year average. “We look at a variety of factors to make our judgment.”

Regarding no interest rate movement, the market disagrees, and so do I.

On inflation, the entire fed is clueless about what it is.

“Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.”

John Maynard Keynes – The Economic Consequences of Peace 1920

“And when we see that we’ve reached that level we’ll begin to gradually reduce our asset purchases to the level of the underlying trend growth of demand for our liabilities.” –Jerome Powell January 29, 2020.

With that one seemingly innocuous statement, Chairman Powell revealed an alarming admission about the supply of money and your wealth. The current state of monetary policy explains why so many people are falling behind and why wealth inequality is at levels last seen almost 100 years ago.

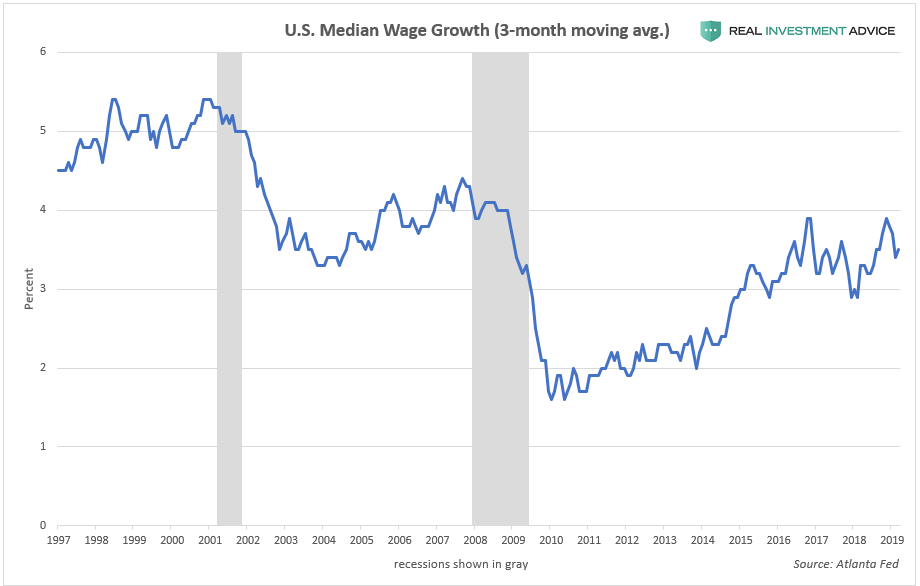

REALity

“Real” is a very important concept in the field of economics. Real generally refers to an amount of something adjusted for the effects of inflation. This allows economists to measure true organic growth or decline.

Real is

equally important for the rest of us. The size of our paycheck or bank account

balance is meaningless without an understanding of what money can buy. For

instance, an annual income of $25,000 in 1920 was about eight times the

national average. Today that puts a family of four below the Federal Poverty

Guideline. As your grandfather used to say, a dollar doesn’t go as far as it

used to.

Real wealth and

real wage growth are important for assessing your economic standing and that of

the nation.

Here are two

facts:

Wealth is largely a function of the wages we earn

The wages we earn are predominately a function of the growth rate of the economy

These facts

establish that the prosperity and wealth of all citizens in aggregate is meaningfully

tied to economic growth or the output of a nation. It makes perfect sense.

Now, let us consider

inflation and the role it plays in determining our real wages and real wealth.

If the rate

of inflation is less than the rate of wage growth over time, then our real

wages are rising and our wealth is increasing. Conversely, if inflation rises

at a pace faster than wages, wealth declines despite a larger paycheck and more

money in the bank.

With that understanding of “real,” let’s discuss inflation.

What is Inflation?

Borrowing

from an upcoming article, we describe inflation in the following way:

“One of the most pernicious of these issues in our “modern and sophisticated” intellectual age is that of inflation. Most people, when asked to define inflation, would say “rising prices” with no appreciation for the fact that price movements are an effect, not a cause. They are a symptom of monetary circumstances. Inflation defined is, in fact, a disequilibrium between the amount of currency entering an economic system relative to the productive output of that same system.”

The price of

cars, cheeseburgers, movie tickets, and all the other goods and services we

consume are chiefly based on supply and demand. Demand is a function of both

our need and desire to own a good and, equally importantly, how much money we

have. The amount of money we have in aggregate, known as money supply, is

governed by the Federal Reserve. Therefore, the supply of money is a key

component of demand and therefore a significant factor affecting prices.

With the

linkage between the supply of money and inflation defined, let us revisit

Powell’s recent revelation.

“And when we see that we’ve reached that level we’ll begin to gradually reduce our asset purchases to the level of the underlying trend growth of demand for our liabilities.”

In plain English, Powell states that the supply of money is based on the demand for money and not the economic growth rate. To clarify, one of the Fed’s largest liabilities currently are bank reserves. Banks are required to hold reserves for every loan they make. Therefore, they need reserves to create money to lend. Ergo, “demand for our liabilities,” as Powell states, actually means bank demand for the seed funding to create money and make loans.

The

relationship between money supply and the demand for money may, in fact, be

aligned with economic growth. If so, then the supply of money should rise with

the economy. This occurs when debt is predominately employed to facilitate

productive investments.

The problem occurs

when money is demanded for consumption or speculation. For example:

When hedge funds demand billions to leverage their trading activity

When Apple, which has over $200 billion in cash, borrows money to buy back their stock

When you borrow money to buy a car, the size of the economy increases but not permanently as you are not likely to buy another car tomorrow and the next day

Now ask,

should the supply of money increase because of those instances?

The

relationship between the demand for money and economic activity boils down to

what percentage of the debt taken on is productive and helps the economy and

the populace grow versus what percentage is for speculation and consumption.

While there

is no way to quantify how debt is used, we do know that speculative and

consumptive debt has risen sharply and takes up a much larger percentage of all

debt than in prior eras. The glaring

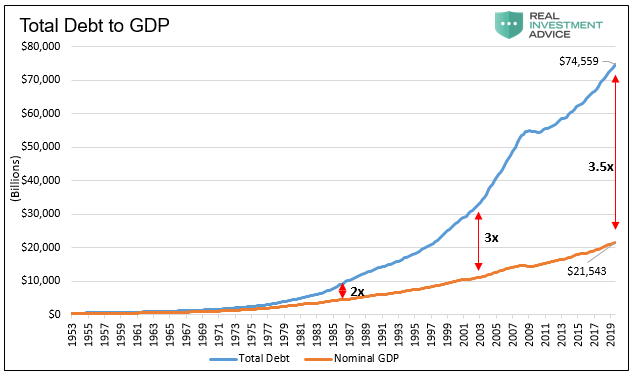

evidence is the sharp rise of debt to GDP.

Data Courtesy St. Louis Federal

Reserve

If most of

the debt were used productively, then the level of debt would drop relative to

GDP. In other words, the debt would not only produce more economic growth but

would also pay for itself. The exact

opposite is occurring as growth languishes despite record levels of debt

accumulation.

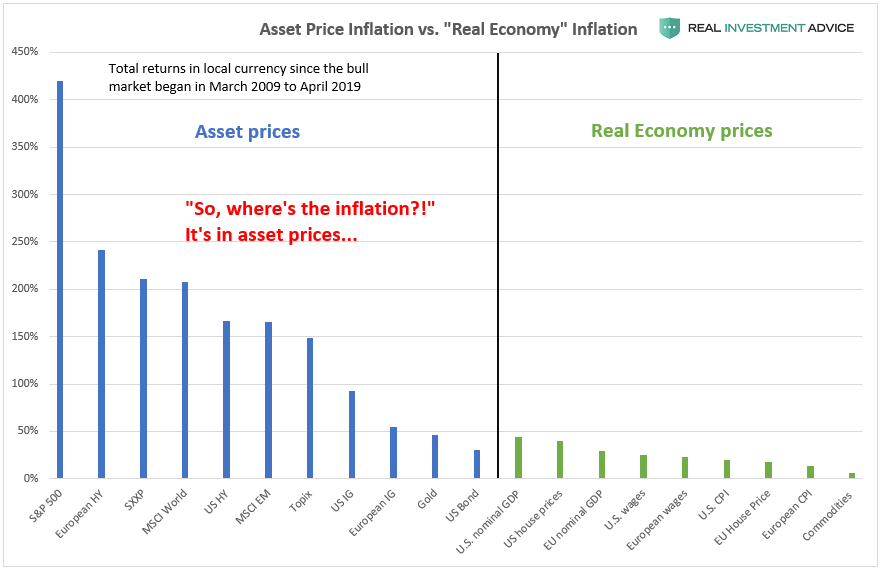

The

speculative markets provide further evidence. Without presenting the long list

of asset valuations that stand at or near record levels, consider that since

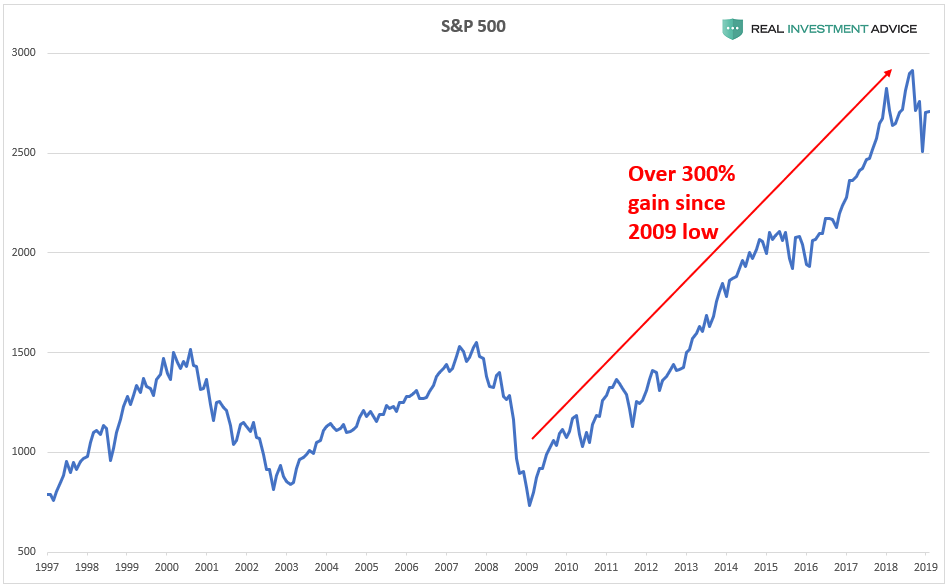

the last time the S&P 500 was fairly valued in 2009, it has grown 375%. Meanwhile,

total U.S. Treasury debt outstanding is up by 105% from $11 trillion to $22.5

trillion and corporate debt is up 55% from $6.5 trillion to $10.1 trillion. Over

that same period, nominal GDP has only grown 46% and Average Hourly Earnings by

29%.

When the money supply is increased

for consumptive and speculative purposes, the Fed creates dissonance between

our wages, wealth, and the rate of inflation. In other words, they generate

excessive inflation and reduce our real wealth.

If this is the case, why is the stated rate of inflation less than economic growth and wage growth?

The Wealth Scheme

This scheme

works like all schemes by keeping the majority of people blind to what is truly

occurring. To perpetuate such a scheme, the public must be convinced that inflation

is low and their wealth is increasing.

In 2000, a

brand new Ford Taurus SE sedan had an original MSRP of $18,935. The 2019 Ford

Taurus SE has a starting price of $27,800.

Over the last 19 years, the base price of the Ford Taurus has risen by

2.05% a year or a total of 47%. According to the Bureau of Labor Statics (BLS),

since the year 2000, the consumer price index for new vehicles has only risen

by 0.08% a year and a total of 1.68% over the same period.

For another instance of how inflation is grossly underreported, we highlighted flaws in the reporting of housing prices in MMT Sounds Great in Theory But… To wit:

“Since then, inflation measures have been tortured, mangled, and abused to the point where it scarcely equates to the inflation that consumers deal with in reality. For example, home prices were substituted for “homeowners equivalent rent,” which was falling at the time, and lowered inflationary pressures, despite rising house prices.

Since 1998, homeowners equivalent rent has risen 72% while house prices, as measured by the Shiller U.S. National Home Price Index has almost doubled the rate at 136%. Needless to say, house prices, which currently comprise almost 25% of CPI, have been grossly under-accounted for. In fact, since 1998 CPI has been under-reported by .40% a year on average. Considering that official CPI has run at a 2.20% annual rate since 1998, .40% is a big misrepresentation, especially for just one line item.”

Those two obscene examples highlight that the government reported inflation is not the same inflation experienced by consumers. It is important to note that we are not breaking new ground with the assertion that the government reporting of inflation is low. As we have previously discussed, numerous private assessments quantify that the real inflation rate could easily be well above the average reported 2% rate. For example, Shadow Stats quantifies that inflation is running at 10% when one uses the official BLS formula from 1980.

Despite what

we may sense and a multitude of private studies confirming that inflation is

running greater than 2%, there are a multitude of other government-sponsored

studies that argue inflation is actually over-stated. So, the battle is in the

trenches, and the devil is in the details.

As defined

earlier, inflation is “a disequilibrium

between the amount of currency entering an economic system relative to the

productive output of that same system.”

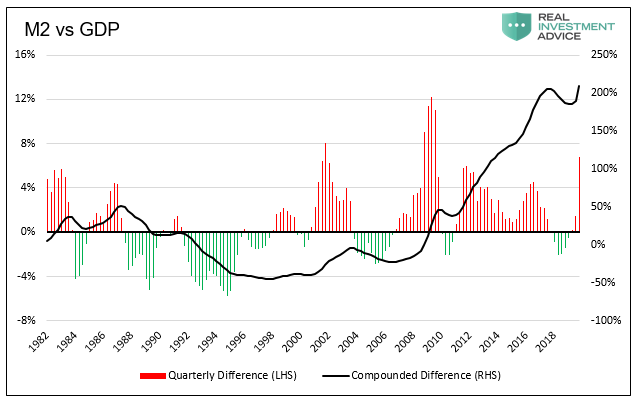

The

following graph shows that the supply of money, measured by M2, has grown far more

than the rate of economic growth (GDP) over the last 20 years.

Data St. Louis Federal Reserve

Since 2000,

M2 has grown 234% while GDP has grown at half of that rate, 117%. Over the same

period, the CPI price index has only grown by 53%. M2 implies an annualized

inflation rate over the last 20 years of 6.22% which is three times that of

CPI.

Dampening

perceived inflation is only part of the cover-up. The scheme is also

perpetuated with other help from the government. The government borrows to

boost temporary economic growth and help citizens on the margin. This further limits

people’s ability to detect a significant decline in their standard of living.

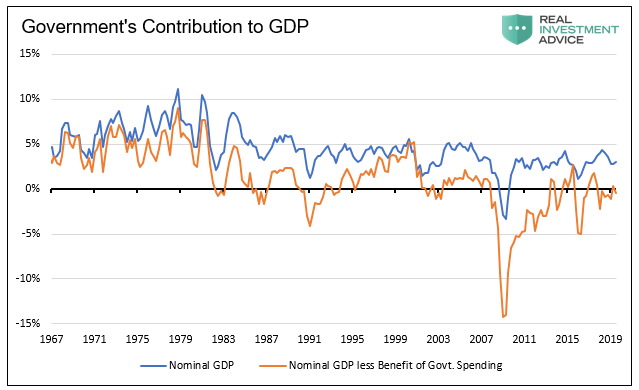

As shown

below, when one strips out the change in government debt (the actual increase

in U.S. Treasury debt outstanding) from the change in GDP growth, the organic economy

has shrunk for the better part of the last 20 years.

Data St. Louis Federal Reserve

It doesn’t

take an economist to know that a 6.22% inflation rate (based on M2) and decade

long recession would force changes to our monetary policy and send those

responsible to the guillotines. If someone suffering severe headaches is

diagnosed with a brain tumor, the problem does not go away because the doctor

uses white-out to cover up the tumor on the x-ray film.

Despite crystal clear evidence, the mirages

of economic growth and low inflation prevent us from seeing reality.

Summary

Those

engaging in speculative ventures with the benefit of cheap borrowing costs are

thriving. Those whose livelihood and wealth are dependent on a paycheck are

falling behind. For this large percentage of the population, their paychecks may

be growing in line with the stated government inflation rate but not the true inflation

rate they pay at the counter. They fall further behind day by day as shown

below.

While this

may be hard to prove using government inflation data, it is the reality.

If you think otherwise, you may want to ask why a political outsider like

Donald Trump won the election four years ago and why socialism and populism are

surging in popularity. We doubt that it is because everyone thinks their wealth

is increasing. To quote Bill Clinton’s 1992 campaign manager James Carville, “It’s the economy, stupid.”

That brings

us back to Jerome Powell and the Fed. The U.S. economy is driven by millions of

individuals making decisions in their own best interests. Prices are best

determined by those millions of people based on supply and demand – that

includes the price of money or interest rates. Any governmental interference

with that natural mechanism is a recipe for inefficiency and quite often failure.

If monetary policy is to be set by a small number of people in a conference room in the Eccles Building in Washington, D.C. who think they know what is best for us based on flawed data, then they should prepare themselves for even more radical social and political movements than we have already seen.

Retired Or Retiring Soon? Yes, Worry About A Correction

When I was growing up, my father used to tell me I should “never take advice from anyone who hasn’t succeeded at what they are advising.”

The most truth of that statement is found in the financial press, which consists mostly of people writing articles and giving advice on topics where they have little experience, and in general, have achieved no success.

The best example came last week in an email quoting:

“You recently suggested that you took profits from your portfolios; however, I read an article saying retirees shouldn’t change their strategies. ‘If you’ve got a thoughtful financial plan and a diversified investment portfolio, the general rule is to leave everything alone.'”

This seems to be an entirely different approach to what you are suggesting. Also, since corrections can’t be predicted, it seems to make sense.”