Hope For The Best, Plan For The Worst

Around 46 BC, Cicero wrote to a friend saying, “you must hope for the best.” To be happy in life we must always have “hope.” It is “hope” which is the beacon that lights the pathway from the darkness that eventually befalls everyone at one point or another in their life.

However, when it comes to financial planning and investing we should consider Benjamin Disraeli’s version from “The Wondrous Tale Of Alroy:”

“I am prepared for the worst, but hope for the best.”

During very late stage bull markets, the financial press is lulled into a sense of complacency that markets will only rise. It is during these late stage advances you start seeing a plethora articles suggesting simple ways to create wealth. Here are a few of the most recent ones I have seen:

- The Power Of Compounding

- The New Math Of Retirement: Save 10%.

- 3-Easy Steps To Retire Early

It’s easy.

Just stick your money in an index fund and “viola” you will be rich.

It reminds me of the old Geico commercials: “It’s so easy a cave man can do it.”

The problem is that these articles are all written by individuals who have never seen, must less survived, a bear market. Bear markets change your way of thinking.

For instance, Grant Sabatier has been in the media a good bit as of late with his success story of going from a net worth of $2.26 to $1 million in 5-years. It is quite an accomplishment. So what was his secret? Save like crazy and invest in index funds, stocks and REIT’s. It’s simple, as long as you have the benefit of a liquidity driven stock market make it all work. (As is always the case, the best way to become a millionaire is to write a book about how to become a millionaire.)

This is all a symptom of the decade-long bull market which has all but erased the memories of the financial crisis.

Following the financial crisis, you didn’t see stories like these. The brutal reality of what happened to individual’s life savings, and lives, was too brutal to discuss. No longer were there mentions of “buy and hold” investing, “dollar cost averaging,” and “buying dips.”

10-years, and 300% gains later, those brutal lessons have been forgotten as the “Wall Street Casino” has finally reignited the “animal spirits” of individuals.

Animal spirits came from the Latin term “spiritus animalis” which means the breath that awakens the human mind. Its use can be traced back as far as 300BC where the term was used in human anatomy and physiology in medicine. It referred to the fluid or spirit that was responsible for sensory activities and nerves in the brain. Besides the technical meaning in medicine, animal spirits was also used in literary culture and referred to states of physical courage, gaiety, and exuberance.

It’s more modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money,” wherein he used the term to describe the human emotions driving consumer confidence. Ultimately, the “breath that awakens the human mind,” was adopted by the financial markets to describe the psychological factors which drive investors to take action in the financial markets.

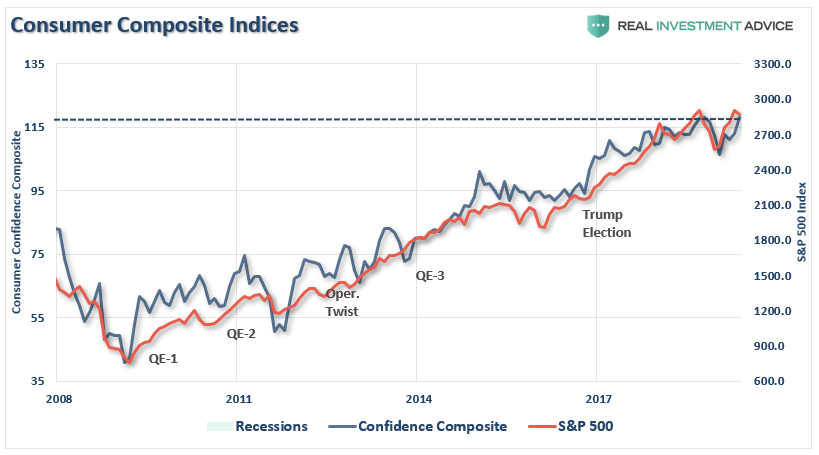

The 2008 financial crisis revived the interest in the role that “animal spirits” could play in both the economy and the financial markets. The Federal Reserve, then under the direction of Ben Bernanke, believed it to be necessary to inject liquidity into the financial system to lift asset prices in order to “revive” the confidence of consumers. The result of which would evolve into a self-sustaining environment of economic growth.

Ben Bernanke & Co. were successful in fostering a massive lift to equity prices since 2009 which, in turn, did correspond to a lift in the confidence of consumers. (The chart below is a composite index of both the University of Michigan and Conference Board surveys.)

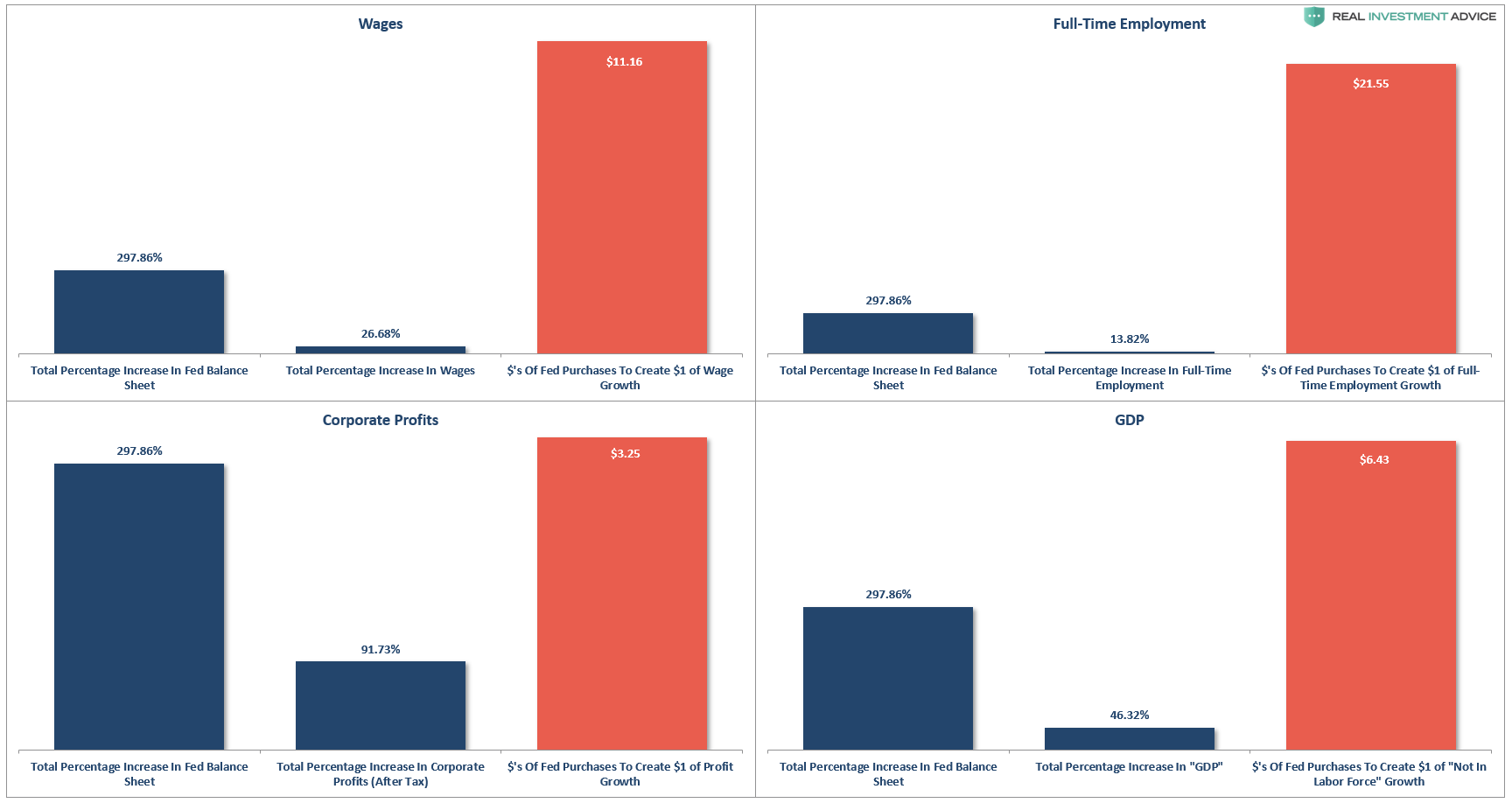

Unfortunately, despite the massive expansion of the Fed’s balance sheet and the surge in asset prices, there was relatively little translation into wages, full-time employment, or corporate profits after tax which ultimately triggered very little economic growth.

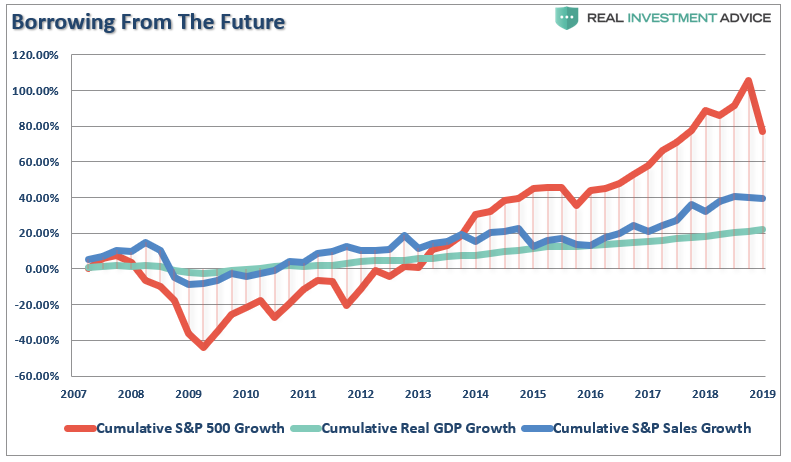

The problem, of course, is the surge in asset prices remained confined to those with “investible wealth” but failed to deliver a boost to the roughly 90% of American’s who have experienced little benefit. In turn, this has pushed asset prices, which should be a reflection of underlying economic growth, well in advance of the underlying fundamental realities. Since 2009, the S&P has risen by roughly 300%, while economic and earnings per share growth (which has been largely fabricated through share repurchases, wage and employment suppression and accounting gimmicks) have lagged.

The stock market has returned almost 80% since the 2007 peak which is more than twice the growth in GDP and nearly 4-times the growth in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not as subject to manipulation.) The all-time highs in the stock market have been driven by the $4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, PE expansion, and ZIRP. With Price-To-Sales ratios and median stock valuations not the highest in history, one should question the ability to continue borrowing from the future?

A Late Stage Event

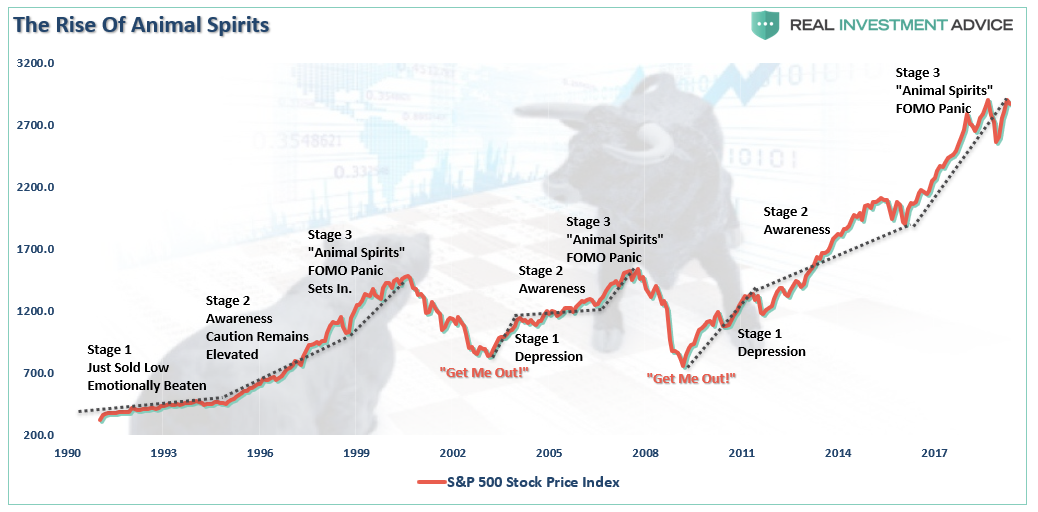

Here’s a little secret, “Animal Spirits” is simply another name for “Irrational Exuberance,” as it is the manifestation of the capitulation of individuals who are suffering from an extreme case of the “FOMO’s” (Fear Of Missing Out). The chart below shows the stages of the previous bull markets and the inflection points of the appearance of “Animal Spirits.”

Not surprisingly, the appearance of “animal spirits” has always coincided with the latter stages of a bull market advance and has been coupled with over valuation, high levels of complacency, and high levels of equity ownership.

As we wrote in detail just recently, valuations are problematic for investors going forward. When high valuations are combined with an extremely long economic expansion, the risk to the “bull market” thesis is an economic slowdown, or contraction, that derails the lofty expectations of continued earnings growth.

The rise in “animal spirits” is simply the reflection of the rising delusion of investors who frantically cling to data points which somehow support the notion “this time is different.” As David Einhorn once stated:

“The bulls explain that traditional valuation metrics no longer apply to certain stocks. The longs are confident that everyone else who holds these stocks understands the dynamic and won’t sell either. With holders reluctant to sell, the stocks can only go up – seemingly to infinity and beyond. We have seen this before.

There was no catalyst that we know of that burst the dot-com bubble in March 2000, and we don’t have a particular catalyst in mind here. That said, the top will be the top, and it’s hard to predict when it will happen.”

This is a crucially important point.

There is nothing wrong with “hoping” for the best possible outcome. However, taking actions to prepare for a negative consequence removes a good deal of the risk with very low short-term costs.

Rules Of The Road

While investing in the markets over the last decade has generated a good deal of wealth for those that have been fortunate enough to have liquid assets to invest, the next bear market will also take much, if not all of it, away.

As the last two decades should have taught the financial media by now, the stock market is not a “get wealthy for retirement” scheme. You cannot continue to under save for your retirement hoping the stock market will make up the difference. This is the same trap that pension funds all across this country have fallen into and are now paying the price for.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you most likely want. Two massive bear markets have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to prepare properly for retirement.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean that you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

- The only way to ensure you will be adequately prepared for retirement is to “save more and spend less.” It ain’t sexy, but it will absolutely work.

- You Will Be WRONG. The markets cycle, just like the economy, and what goes up will eventually come down. More importantly, the further the markets rise, the bigger the correction will be. RISK does NOT equal return. RISK = How much you will lose when you are wrong, and you will be wrong more often than you think.

- Don’t worry about paying off your house. A paid off house is great, but if you are going into retirement being “house rich” and “cash poor” will get you in trouble. You don’t pay off your house UNTIL your retirement savings are fully in place and secure.

- In regards to retirement savings – have a large CASH cushion going into retirement. You do not want to be forced to draw OUT of a pool of investments during years where the market is declining. This compounds the losses in the portfolio and destroys principal which cannot be replaced.

- Hope for the best, but plan for the worst. You should want a happy and secure retirement – so plan for the worst. If you are banking solely on Social Security and a pension plan, what would happen if the pension was cut? Corporate bankruptcies happen all the time and to companies that most never expected. By planning for the worst, anything other outcome means you are in great shape.

Most likely what ever retirement planning you have done, is wrong.

Change your assumptions, ask questions, and plan for the worst.

There is no one more concerned about YOUR money than you and if you don’t take an active interest in your money – why should anyone else?