Democrats Should Start Worrying About The Deficit.

Democrats should start worrying about the level of debt and the increasing deficit. I previously discussed this issue when President Obama held the White House, when Marshall Auerback, via the Nation, wrote:

“Delivering on big progressive ideas like Medicare for All and the Green New Deal will never happen until Democrats get over their fear of red ink.”

While that article was a long and winding mess of convoluted ideas, the following excerpt was vital.

“In an environment increasingly characterized by slowing global economic growth, businesses are understandably hesitant to invest in a way that creates high-quality, high-paying jobs for the bulk of the domestic workforce. The much-vaunted Trump corporate ‘tax reform’ may have been sold to the American public on that basis, but corporations have largely used their tax cut bonanza to engage in share buybacks, which fatten executive compensation but have done nothing for the rest of us. At the same time, private households still face constraints on their consumption because of stagnant wages, rising health care costs, declining job security, poorer employment benefits, and rising debt levels.

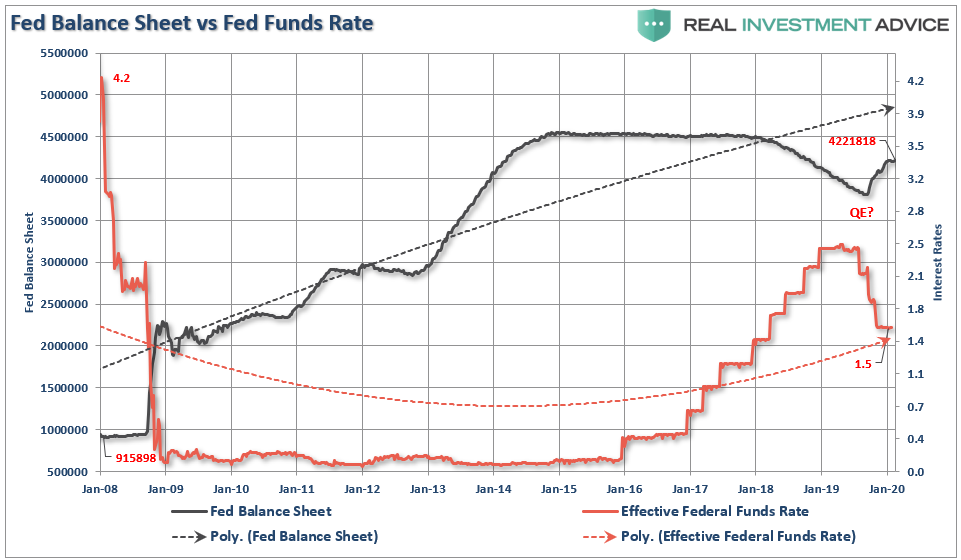

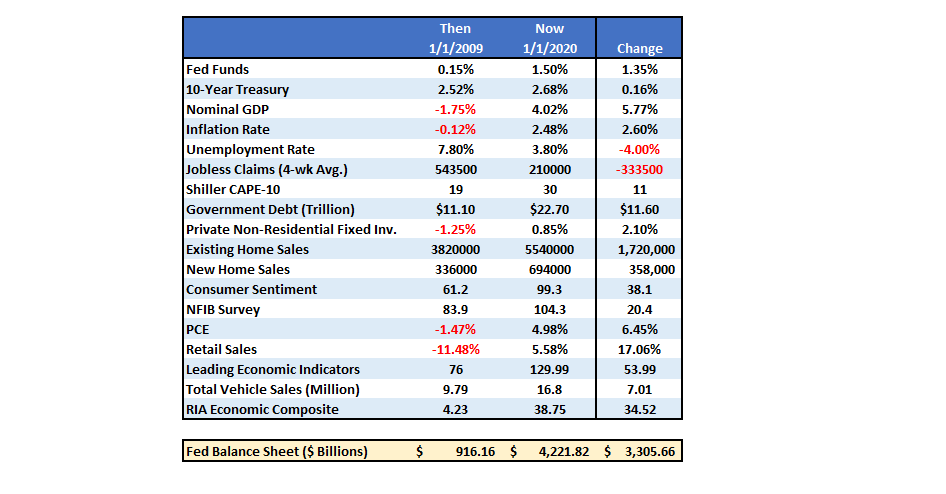

Instead of solving these problems, the reliance on extraordinary monetary policy from the Federal Reserve via programs such as quantitative easing has exacerbated them. In contrast to properly targeted fiscal spending, the Federal Reserve’s misguided monetary policies have fueled additional financial speculation and asset inflation in stock markets and real estate, which has made housing even less affordable for the average American.”

While there is truth in that statement, and it is the same issue I have railed against previously in this blog, Mr. Auerback’s solution was seemingly simple.

“Democrats should embrace the ‘extremist’ spirit of Goldwater and eschew fiscal timidity (which, in any case, is based on faulty economics). After all, Republicans do it when it suits their legislative agenda. Likewise, Democrats should go big with deficits—as long as they are used for the transformative programs that progressives have long talked about and now have the chance to deliver.”

As I noted then, such a solution was essentially the adoption of Modern Monetary Theory (MMT), which, as discussed previously, is the assumption debt and deficits “don’t matter” as long as there is no inflation.

“Modern Monetary Theory is a macroeconomic theory that contends that a country that operates with a sovereign currency has a degree of freedom in their fiscal and monetary policy, which means government spending is never revenue constrained, but rather only limited by inflation.” – Kevin Muir

However, fast forward to the present, we tried MMT; the Democrats went big with debts and deficits and funded social programs, and the result was a massive spike in inflation and no actual increase in broad economic prosperity.

So, what went wrong?

The Non-Solution

The problem with most Democratic spending ideas on social programs and welfare, like free healthcare or college, is the lack of a crucial ingredient. That ingredient is a “return on investment.” Dr. Woody Brock previously addressed this point in his book “American Gridlock;”

“Country A spends $4 Trillion with receipts of $3 Trillion. This leaves Country A with a $1 Trillion deficit. In order to make up the difference between the spending and the income, the Treasury must issue $1 Trillion in new debt. That new debt is used to cover the excess expenditures but generates no income leaving a future hole that must be filled.

Country B spends $4 Trillion and receives $3 Trillion income. However, the $1 Trillion of excess, which was financed by debt, was invested into projects, infrastructure, that produced a positive rate of return. There is no deficit as the rate of return on the investment funds the “deficit” over time.“

Let me be clear. There is no disagreement about the need for government spending. The debate is about the abuse and waste of it.

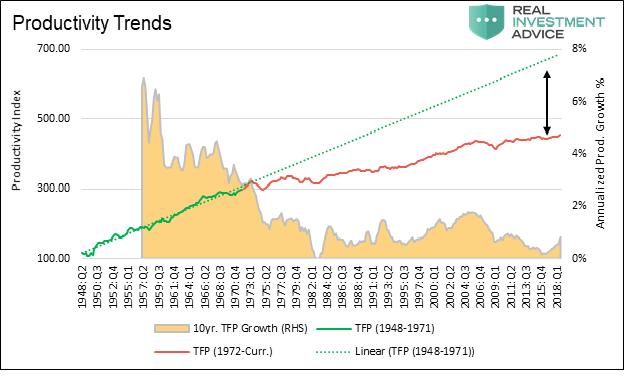

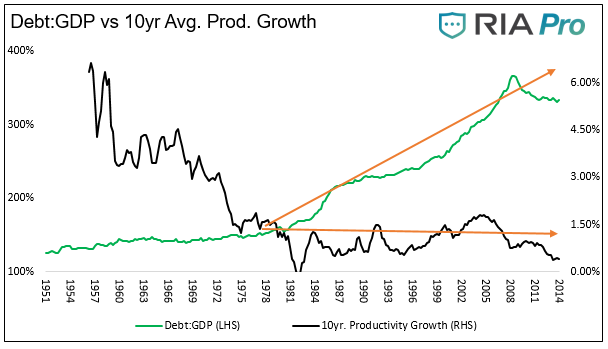

John Maynard Keynes’ was correct in his theory that for government “deficit” spending to be effective, the “payback” from investments made through debt must yield a higher rate of return than the debt used to fund it.

Currently, the U.S. is “Country A.”

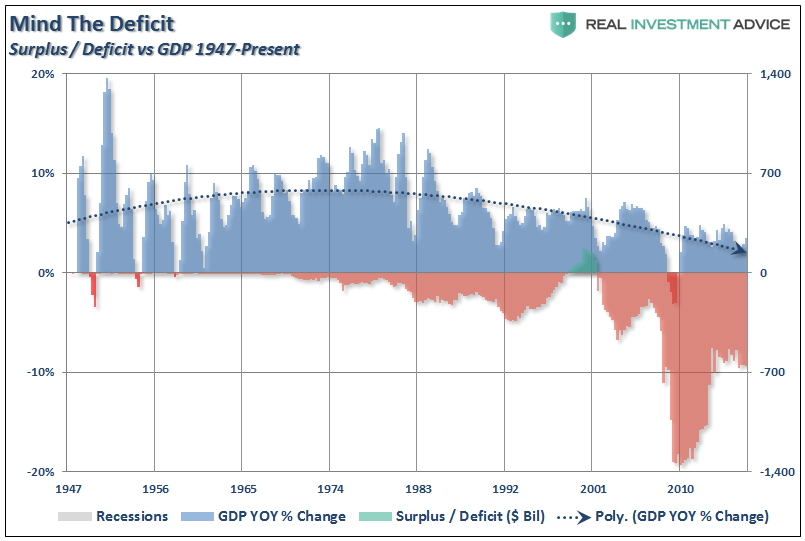

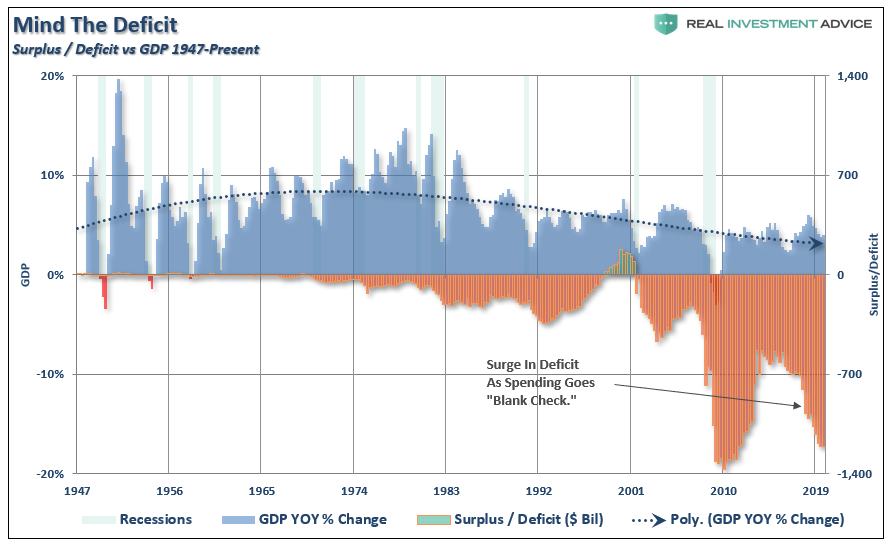

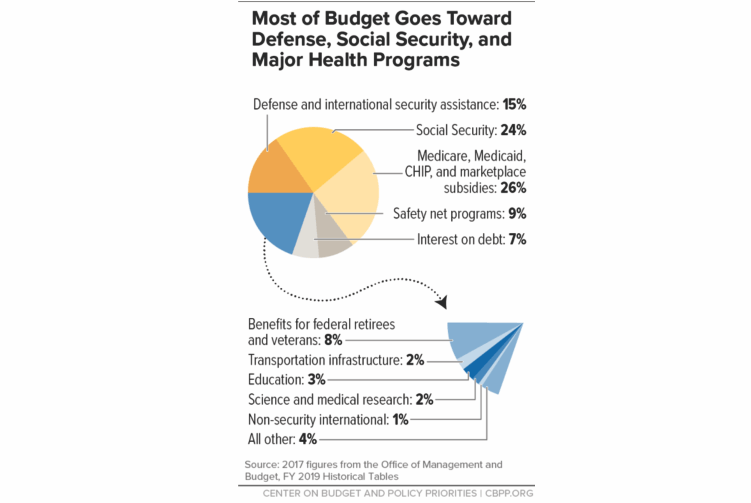

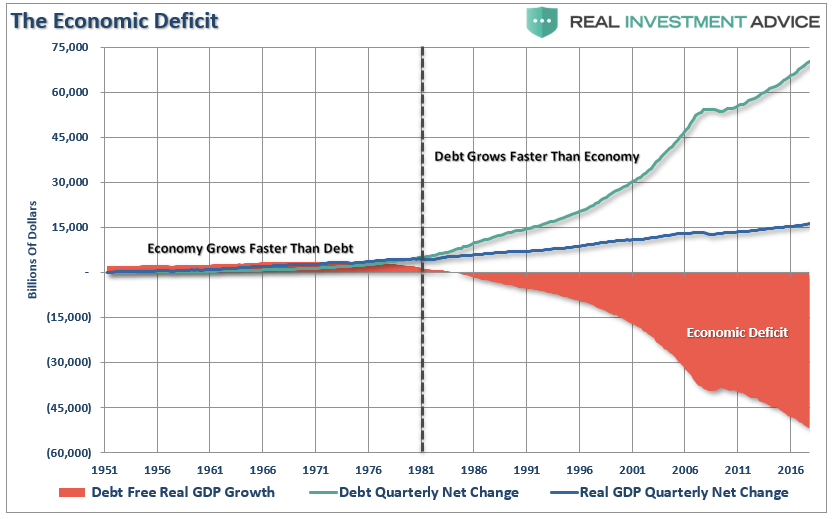

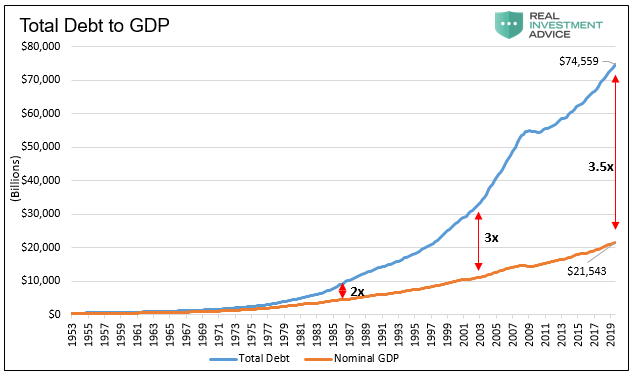

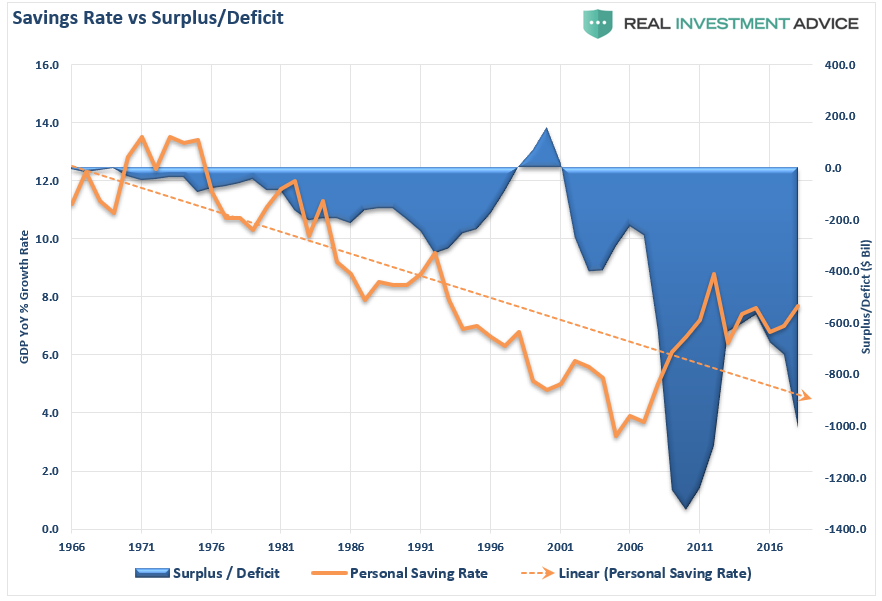

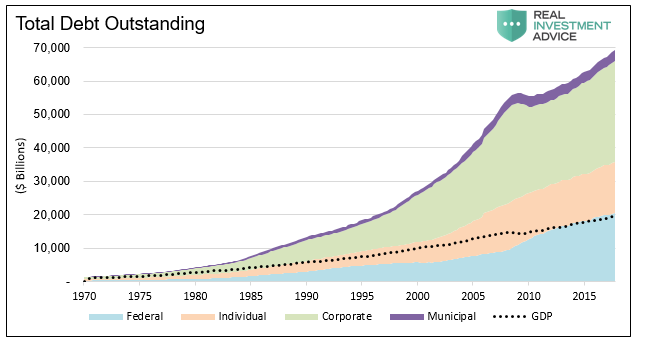

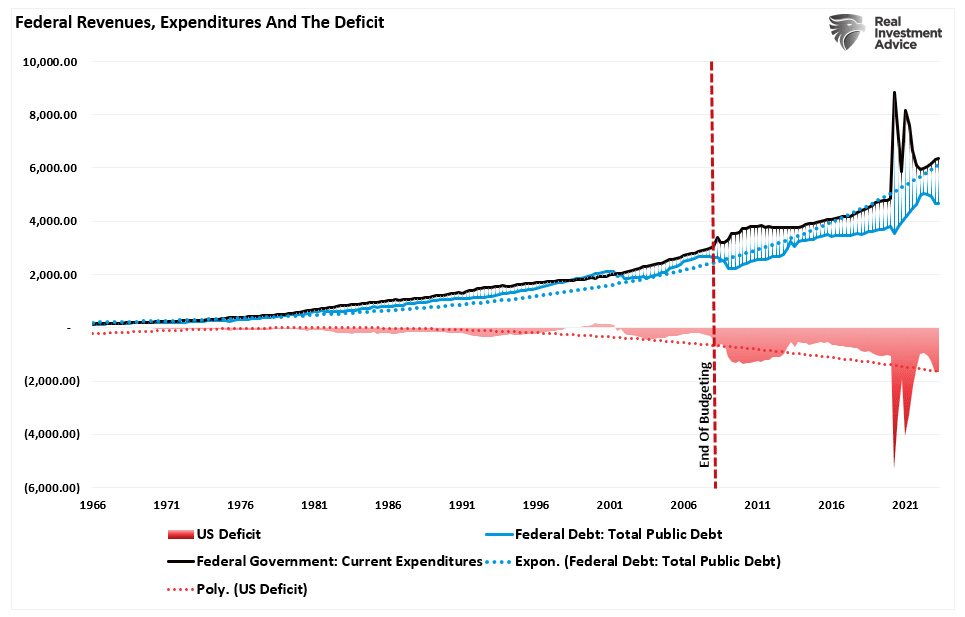

The problem with the more socialistic programs that Democrats continue to pursue with deficit spending is that it exacerbates the problem. The Center On Budget & Policy Priorities data can help visualize the issue.

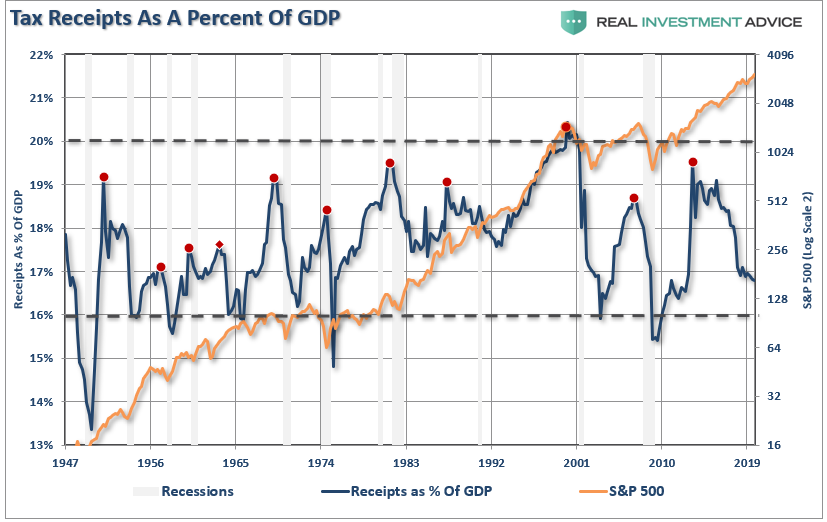

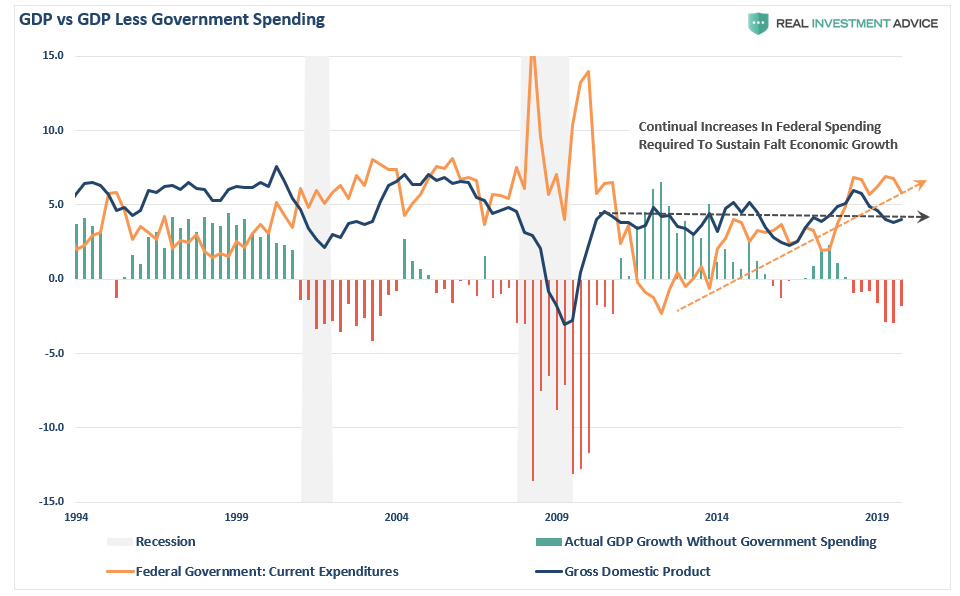

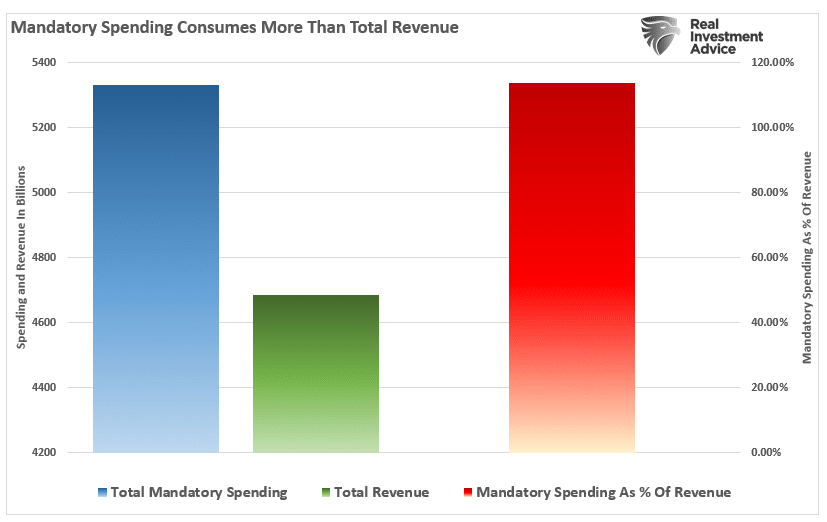

As of the latest annual data, through the end of Q2-2023, the Government spent $6.3 Trillion, of which $5.3 Trillion went to mandatory expenses. In other words, it currently requires 113% of every $1 of revenue to pay for social welfare and interest on the debt. Everything else must come from debt issuance.

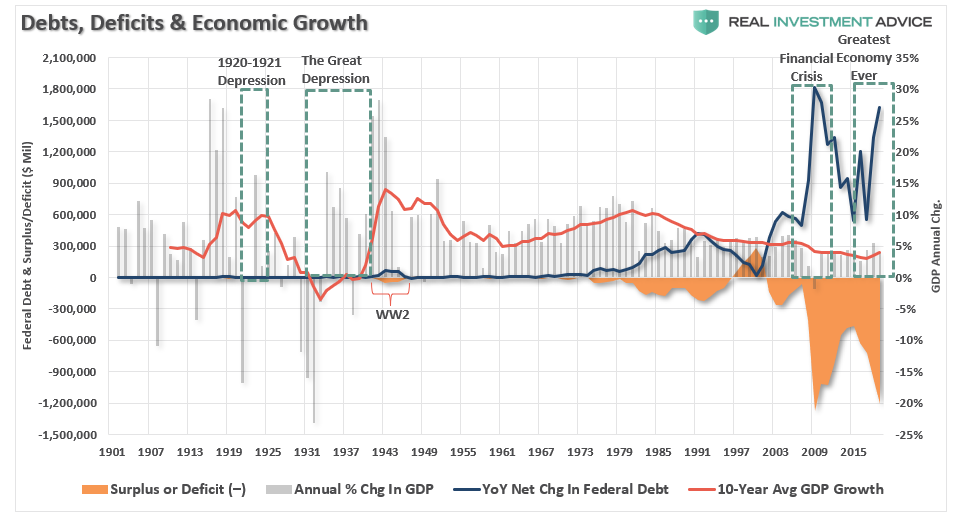

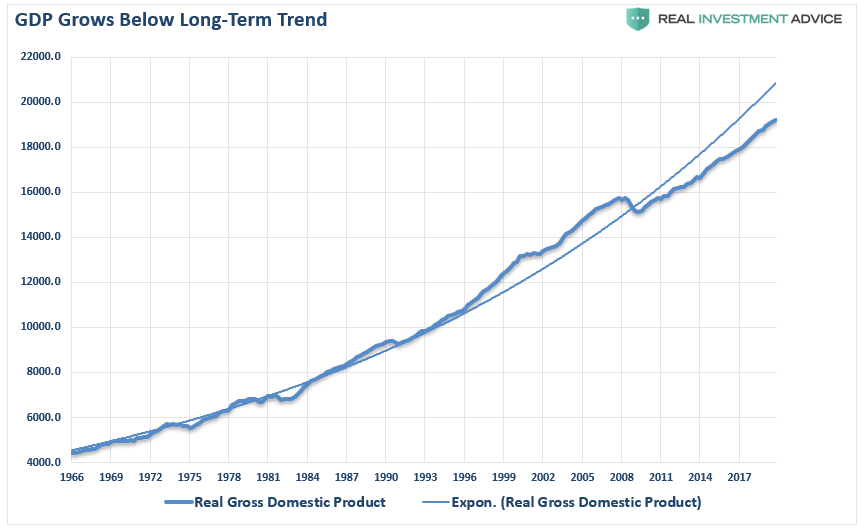

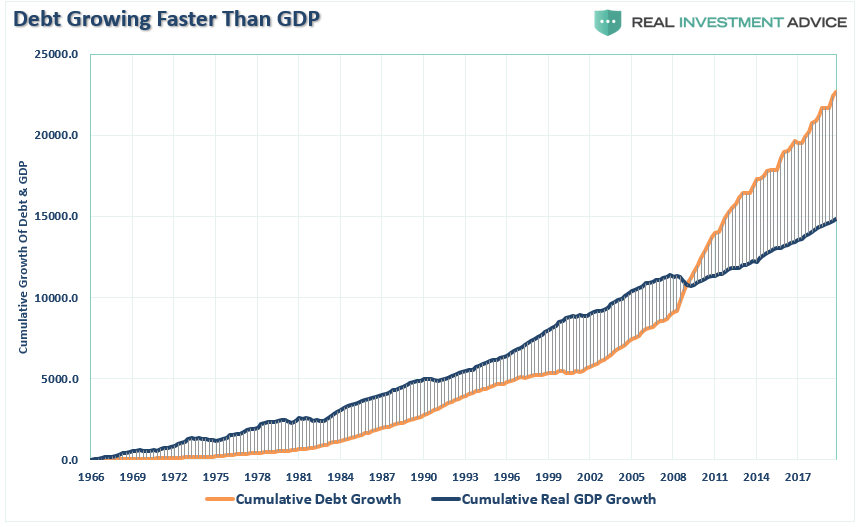

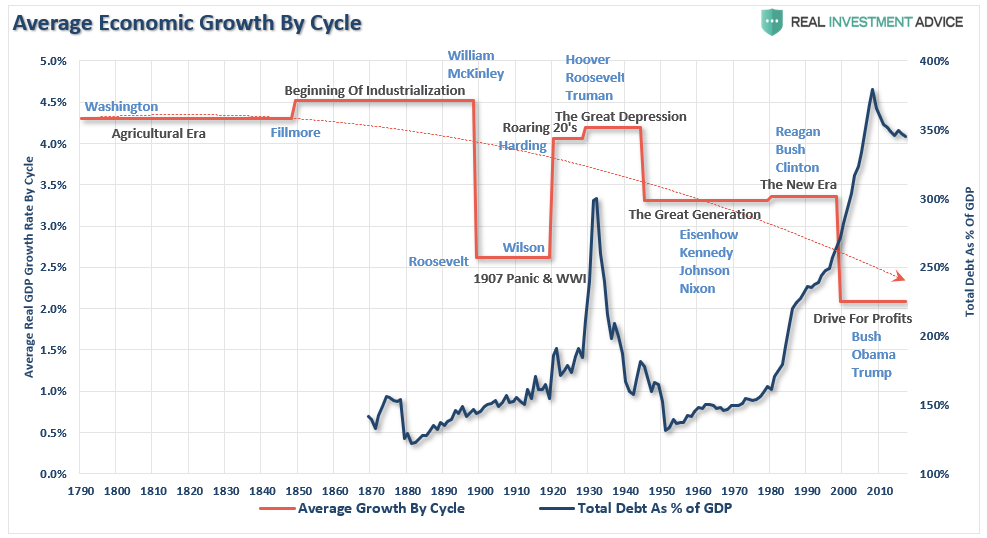

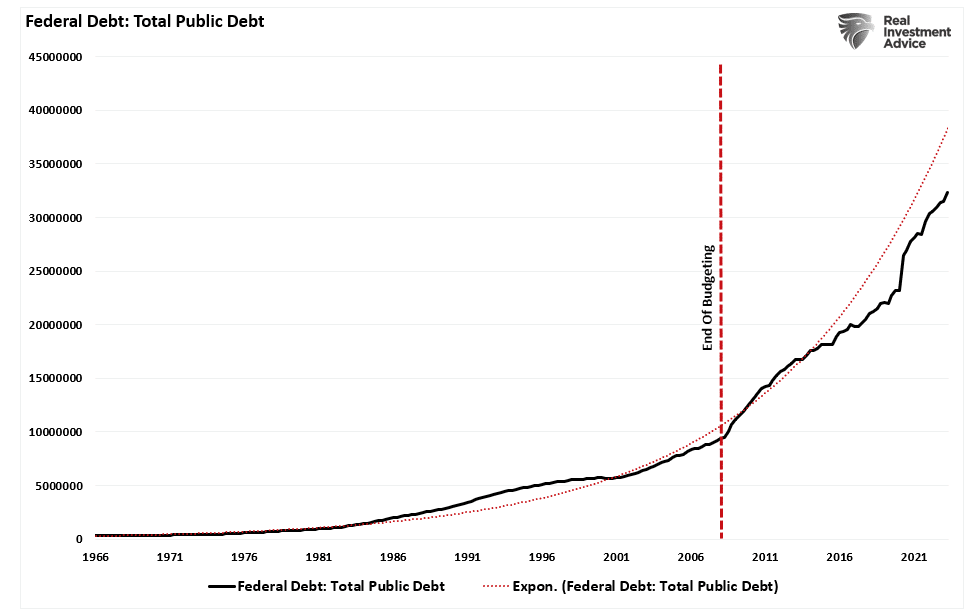

This is why debt issuance has surged since 2008 when Congress quit using the budgeting process to allow for rampant spending.

Of course, given the massive surge in spending, revenues cannot keep up the pace, leading to a rapid increase in debt issuance and a trending deficit.

However, while Democrats keep pushing for more socialistic programs, which garners votes in election cycles, they are now faced with a problem that may be their undoing.

Debt Diverts Productive Capital

Ben Ritz for the WSJ recently penned:

“Deficits are undermining the Biden economy. In the past year, the real federal budget deficit more than doubled, from $933 billion to $2 trillion. Democrats rightly argued that spending borrowed money was a critical economic support during the Covid pandemic. But the unemployment rate the over past year has been consistently lower than any point since the 1950s.

Economists, even those on the far left who subscribe to ‘modern monetary theory,’ agree that increasing deficits in a tight labor market fuels inflation. Voters’ frustrations with inflation and the interest-rate hikes implemented to bring it under control exceed their appreciation for low unemployment, fueling disapproval of President Biden’s economic record. Deficit reduction is more important than it has been at any other time in the 21st century.”

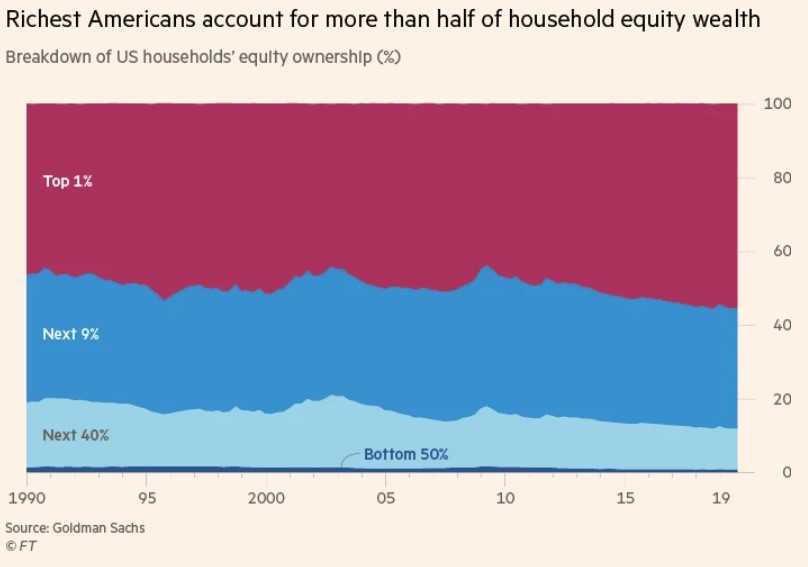

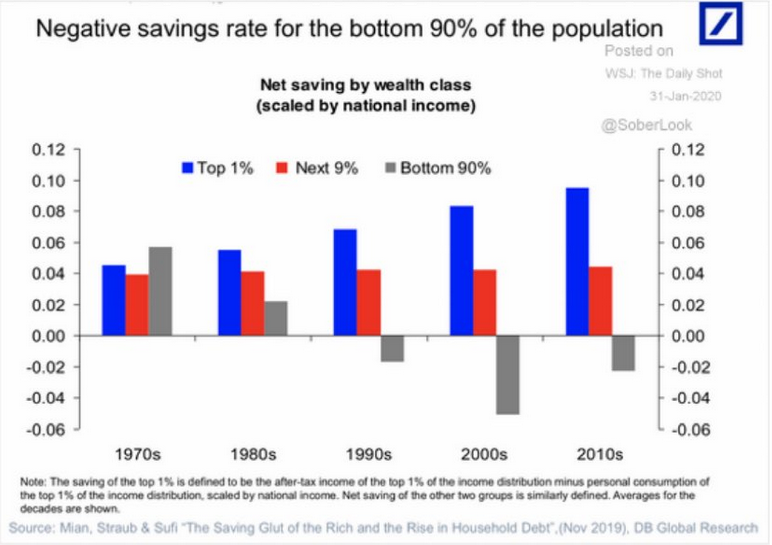

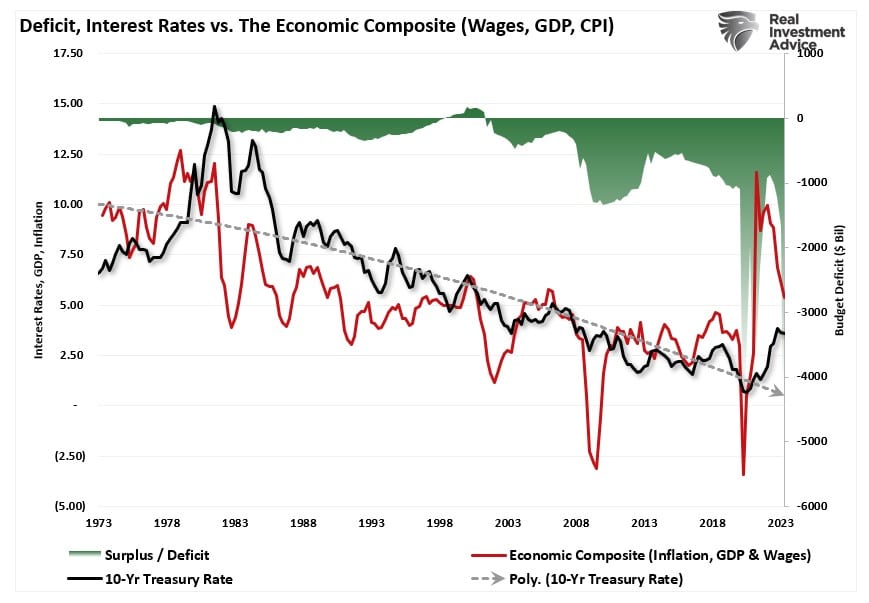

The problem with the analysis is that while the “unemployment rate” may be low, economic disparity is high. While the massive surge in pandemic-era spending boosted economic inflation, it also created an enormous rise in inflation, unsurprisingly. That inflation surge spurred the Fed to aggressively hike rates on the short end of the yield curve, while inflation and economic growth pushed long-term rates higher.

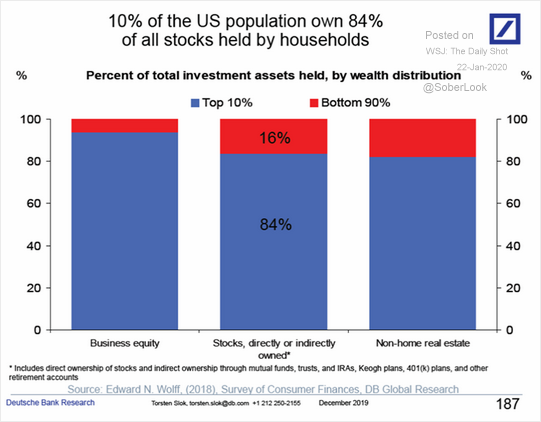

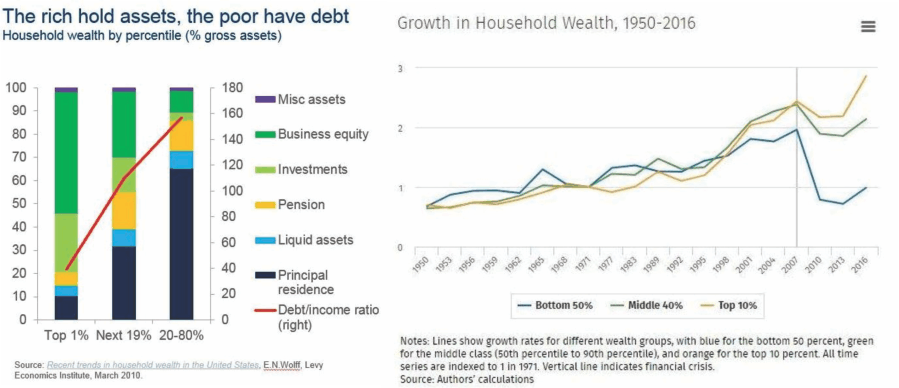

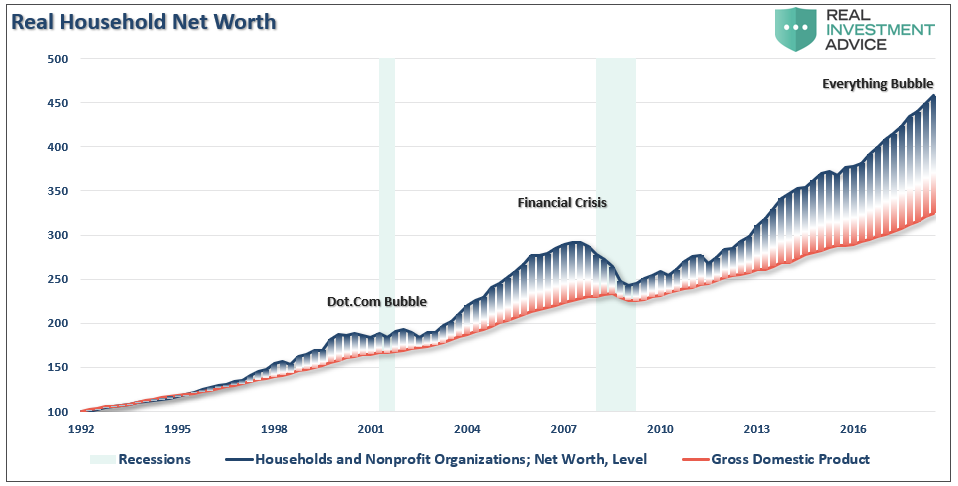

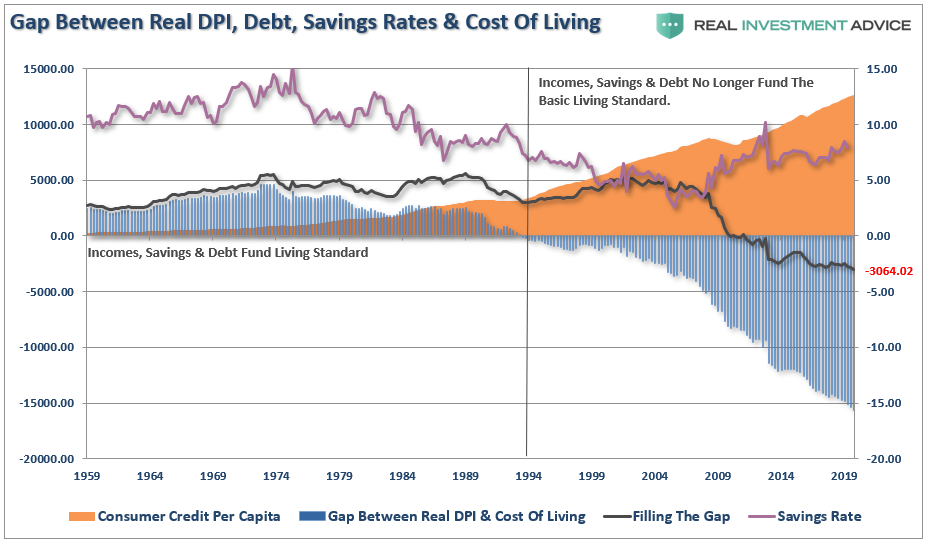

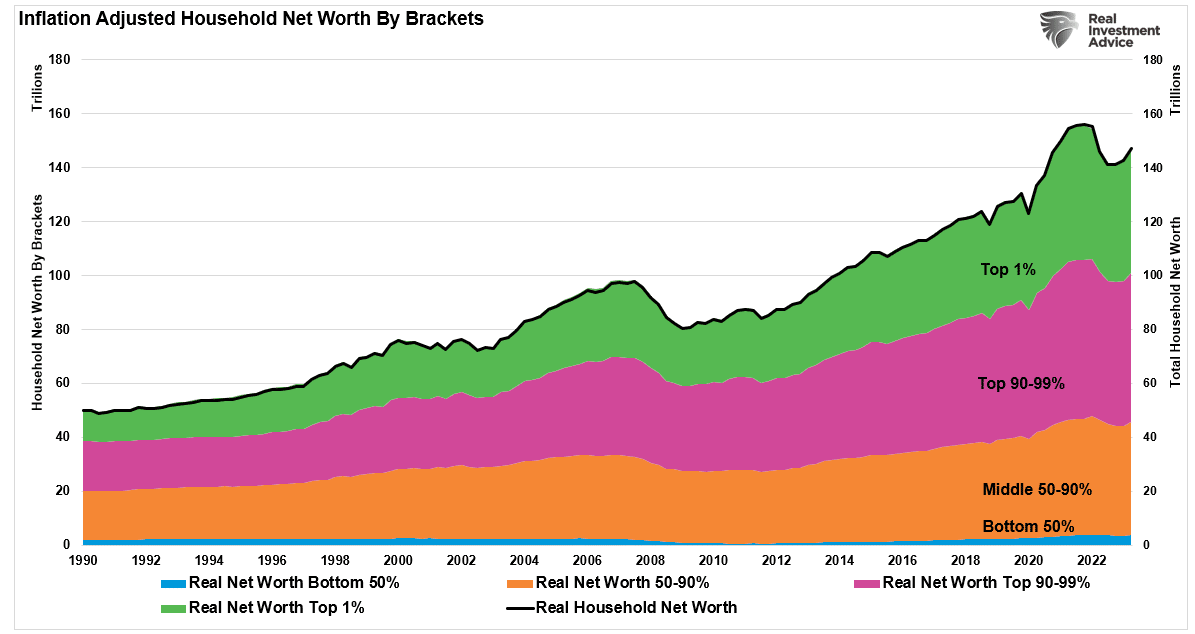

Subsequently, higher inflation and higher borrowing costs priced out wage increases with substantially higher living costs. Unsurprisingly, the net worth of the bottom 90% of Americans has failed to improve.

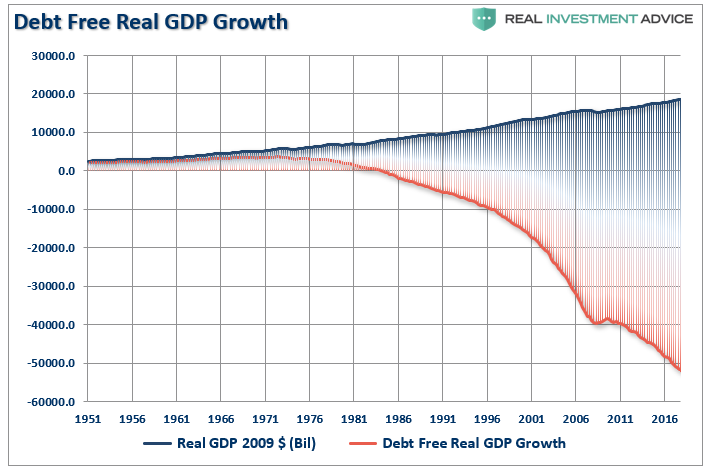

The problem for the Democrats is that continuing to push socialistic programs only makes the situation worse. Yes, more “free money” to individuals sounds excellent in theory, but prices ultimately increase more. The problem is exacerbated as non-productive debt erodes economic growth, and more debt diverts productive capital into interest payments.

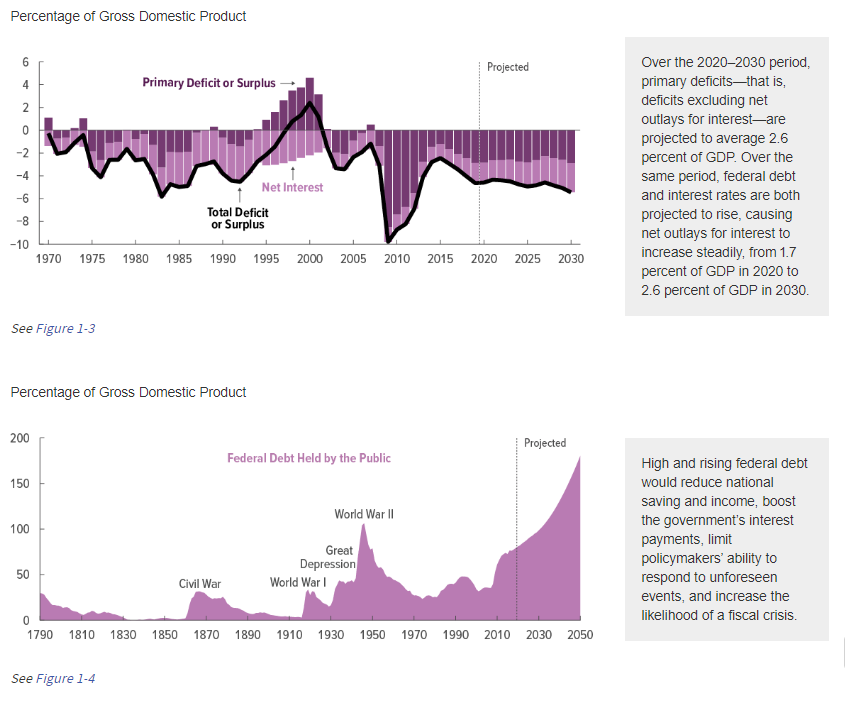

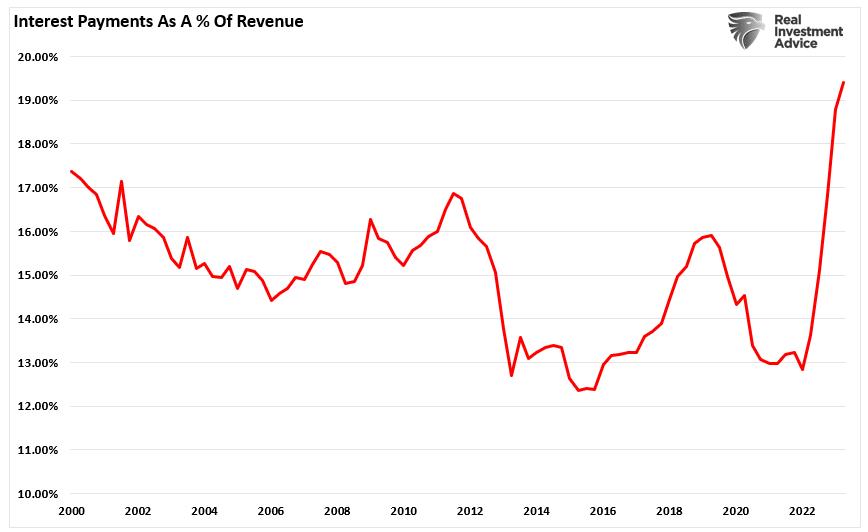

“Annual interest payments are already at their highest level as a percentage of gross domestic product since the 1990s. By 2028 the government is projected to spend more than $1 trillion on interest payments each year—more than it spends on Medicaid or national defense. Worse, the U.S. may be entering a vicious circle whereby higher deficits increase debt and fuel inflation, which the Federal Reserve must combat by raising interest rates, causing debt-service costs to balloon further.” – Ben Ritz

While the Democrats continue to push for more social spending programs, we have potentially reached the point where that may be no longer feasible. I agree with Ben’s view that it may be time for both Democrats and Republicans to start taking steps to restore fiscal responsibility in Washington.

The average American family is no longer supportive of new progressive policies when they believe we can’t even pay for the promises already made.

Of course, if the economy slips into a recession before the 2024 election, we could see a political rout in Washington, D.C.