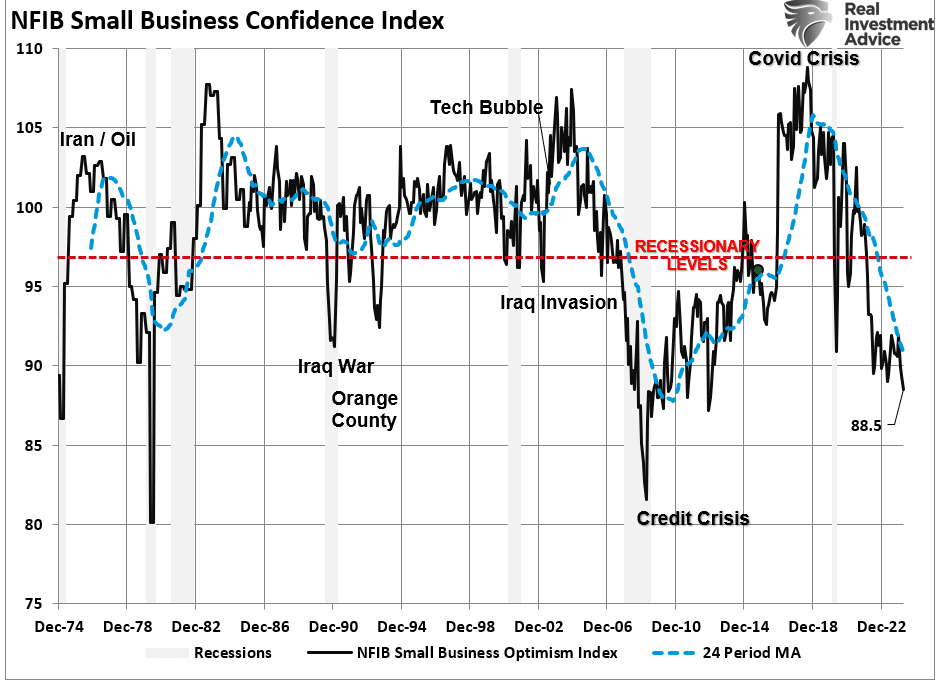

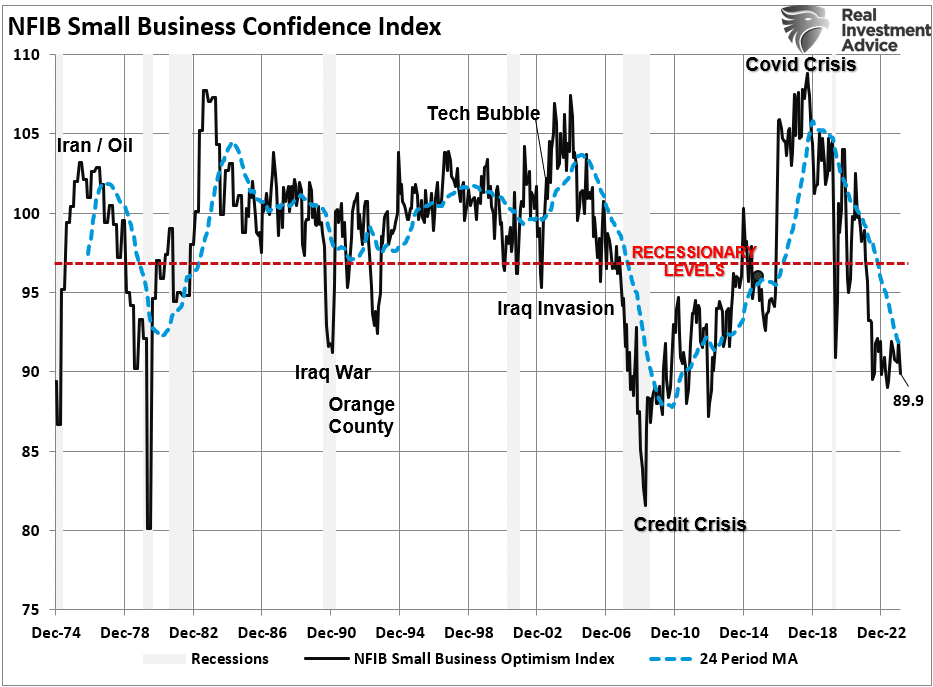

The latest National Federation of Independent Business (NFIB) survey was an economic warning that departed widely from more robust governmental reports. Ina recent analysis of small businesses, we discussed the importance those business owners play in the economy.

“It is crucial to understand that small and mid-sized businesses comprise a substantial percentage of the U.S. economy. Roughly 60% of all companies in the U.S. have less than ten employees.

Small businesses drive the economy, employment, and wages. Therefore, the NFIB’s statements are highly relevant to the economy’s current state compared to the headline economic data from Government sources.”

While recent government data on economic growth and employment remain robust, the NFIB small business confidence survey declined in its latest reading. Not only did it fall to the lowest level in 11 years, but, as far as an economic warning goes, it remained at levels historically associated with a recessionary economy.

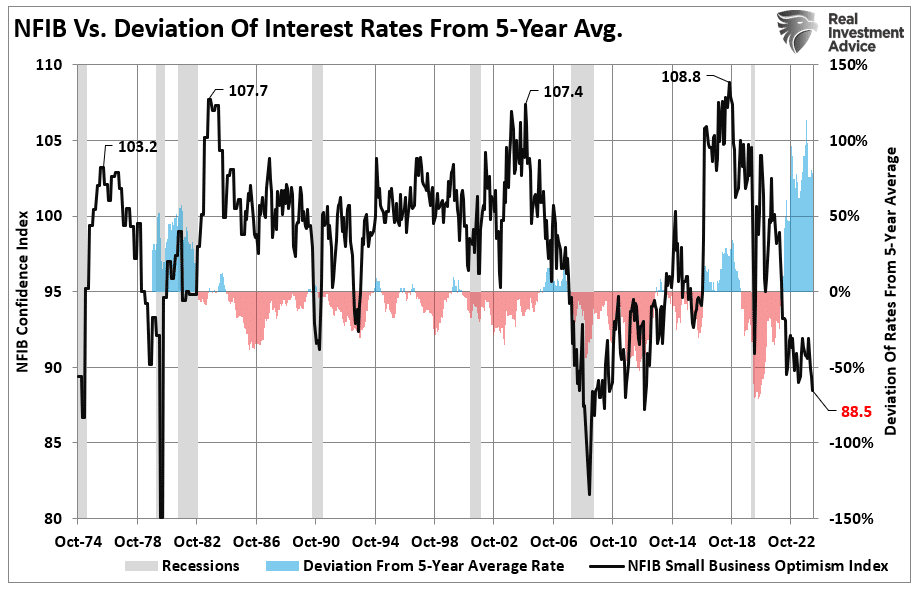

The decline in confidence should be unsurprising given the largest deviation of interest rates from their 5-year average since 1975. Higher borrowing costs impede business growth for small businesses, as they don’t have access to the bond market like major companies.

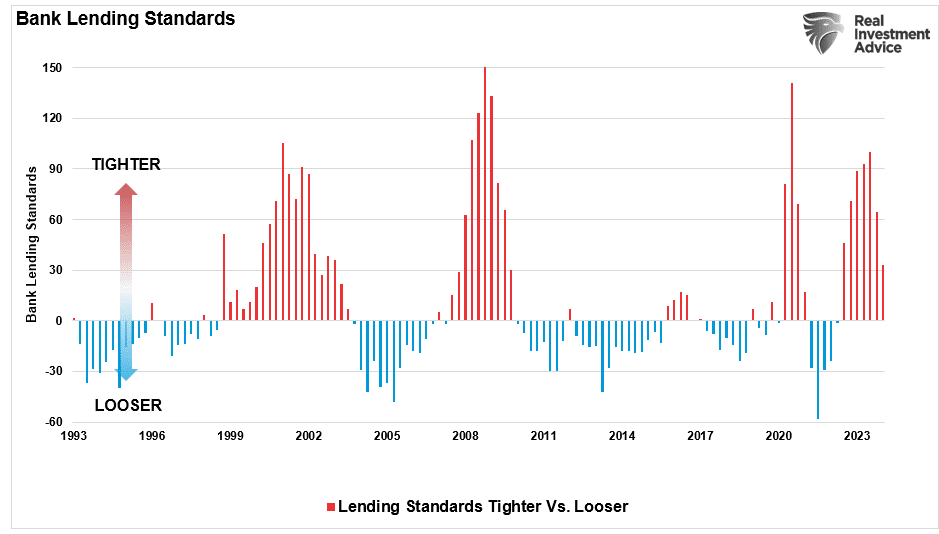

Therefore, as the economy slows and interest rates rise, small business owners turn to their local banks for operating loans. However, higher rates and tighter lending standards make access to capital more difficult.

Of course, given that capital is the lifeblood of any business, decisions on hiring, capital expenditures, and expansion hang in the balance.

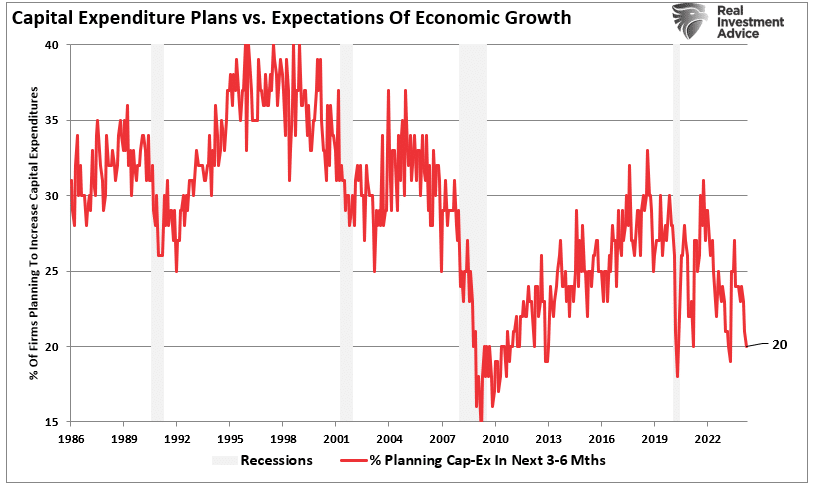

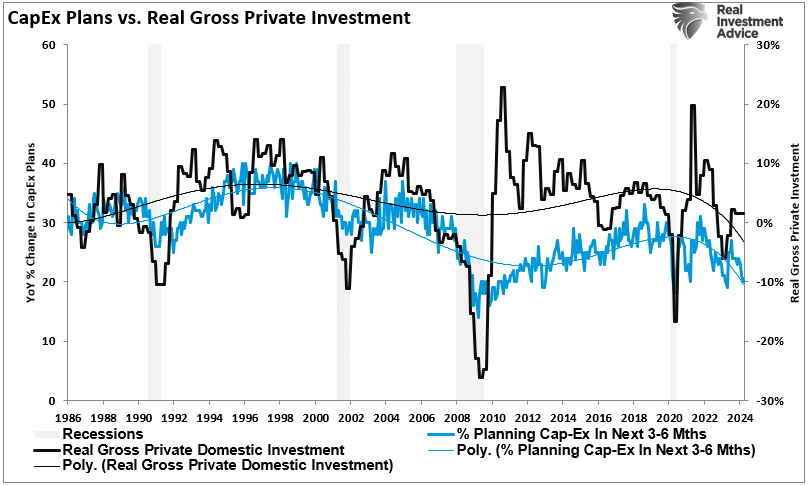

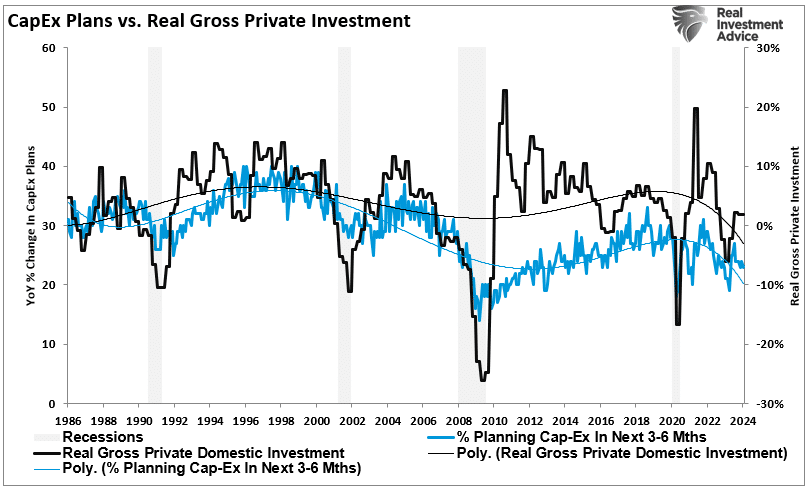

Economic Warning – Capital Expenditures

It should be unsurprising that if the economy were expanding as quickly as headline data suggests, business owners would be expending capital to increase capacity to meet rising demand. However, in the most recent NFIB report, the percentage of business owners planning capital expenditures over the 3-6 months dropped to the lowest level since the pandemic-driven shutdown.

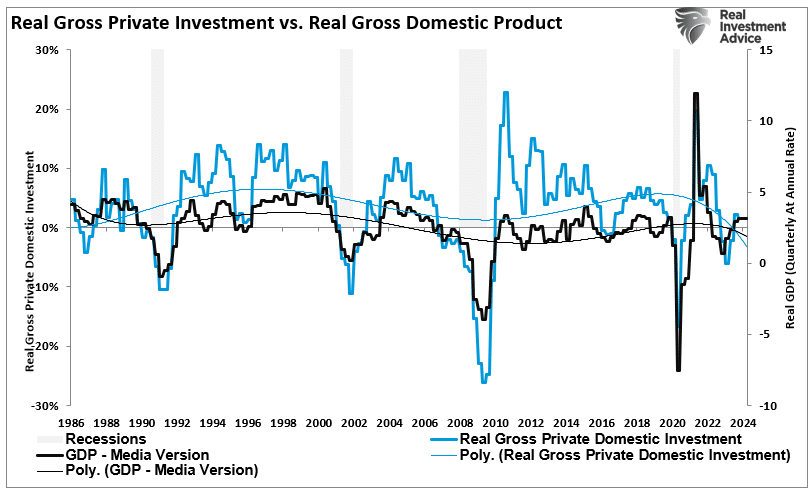

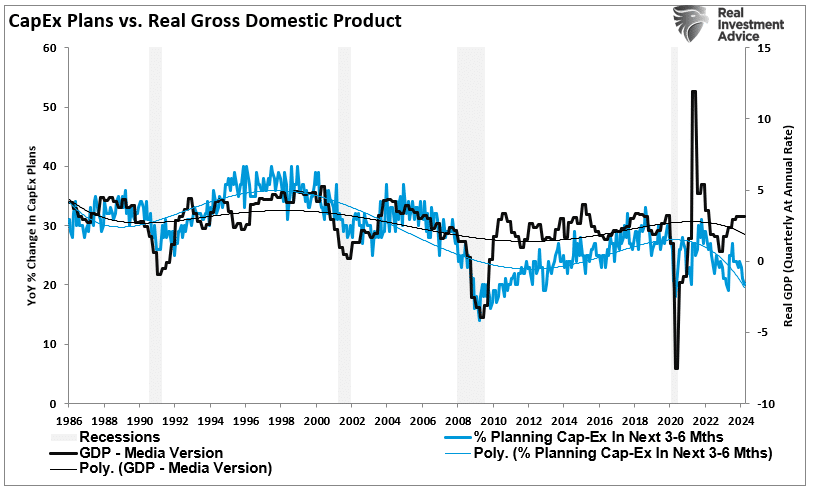

Again, given that small businesses comprise about 50% of the economy, there is more than just a casual relationship between their capital expenditure plans (CapEx) and real gross private investment, which is part of the GDP equation.

In other words, if small businesses cut back on CapEx, this will eventually translate into slower rates of private investment and, ultimately, economic growth in coming quarters.

As shown, the correlation between small business CapEx plans and economic growth should not be dismissed. While mainstream economists are becoming increasingly optimistic about an “economic reflation,” the economic warning between real GDP and CapEx suggests caution.

Of course, if small businesses are unwilling to increase CapEx, it is because there is a lack of demand to justify those expenditures. Therefore, if CapEx is falling, we should expect economic warnings from employment and sales.

Something Amiss With Sales

Many reasons feed into a small business owner’s decision NOT to invest in their business. As noted above, tighter bank lending standards and increased borrowing costs certainly weigh on that decision. However, if “business is booming,” business owners will find the capital needed to meet increased demand. However, looking deeper into the NFIB data, we find rising concerns about the “demand” side of the equation.

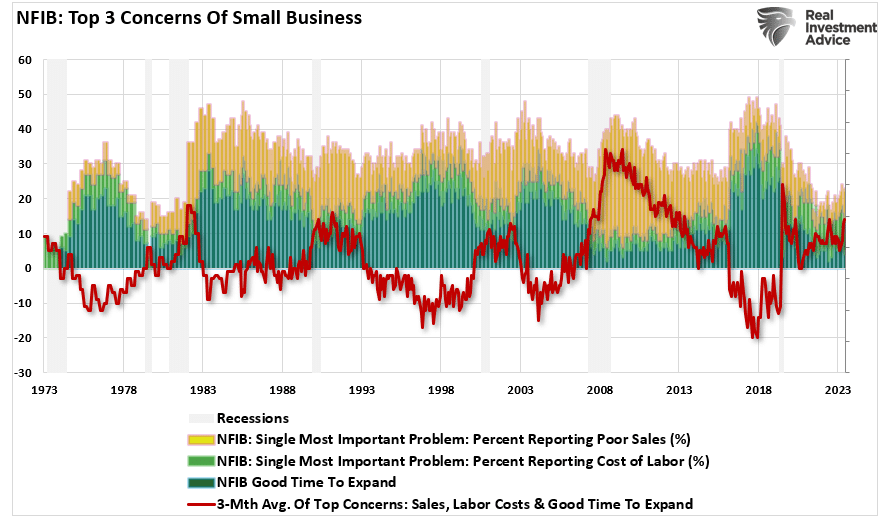

The NFIB publishes several data points from the survey concerning the “concerns” small business owners have. These cover many concerns, from government regulations to taxes, labor costs, sales, and other concerns confronting business owners. When it comes to the “demand” side of the equation, there are three crucial categories:

Poor sales (demand),

Cost of labor (the most significant expense to any business), and

Is it a “Good time to expand?”(Capex)

In the chart below, I have inverted “Good time to expand,” so it correlates with rising concerns about the cost of labor and poor sales. What should be obvious is that the average of these concerns escalates as economic growth weakens (recessionary periods) and falls during economic recoveries. Currently, these rising concerns should provide an economic warning to economists.

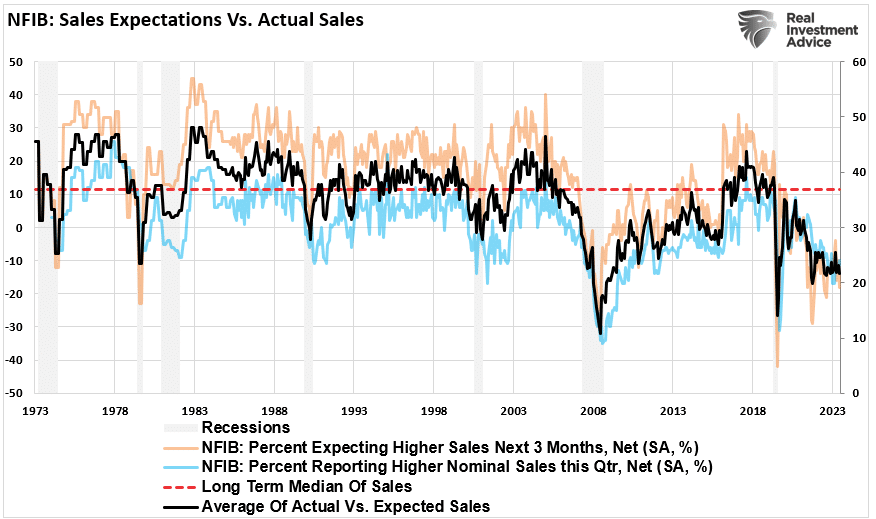

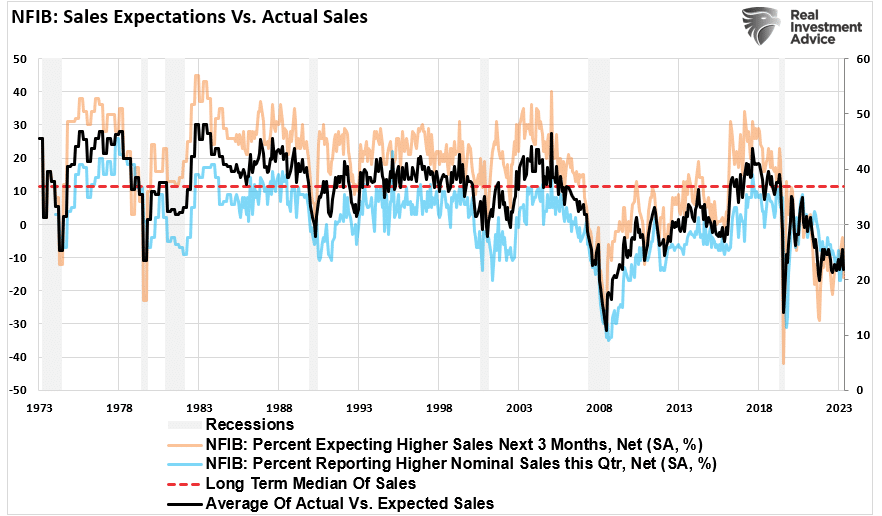

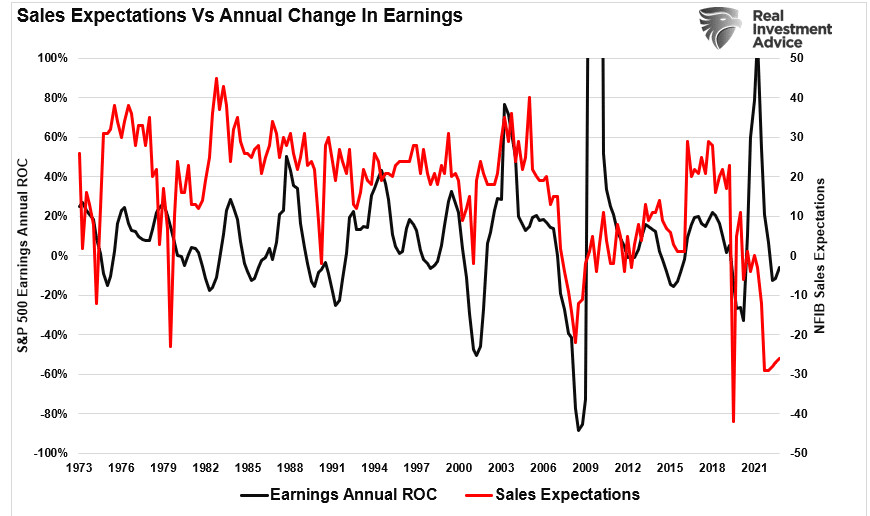

Examining sales and employment figures can help us understand why business owners remain pessimistic about the overall economy. The chart below shows the NFIB members’ sales expectations over the next quarter compared to the previous quarter. The black line is the average of both with a long-term median.

Unsurprisingly, business owners are always optimistic that sales will improve in the next quarter. However, actual sales tend to fall short of those expectations. The two have a very high correlation, which is why the average of both provides valuable information. Sales expectations and actual sales are well below levels typically witnessed during recessions. With sales (demand) weak, there is little need to increase production (supply) substantially.

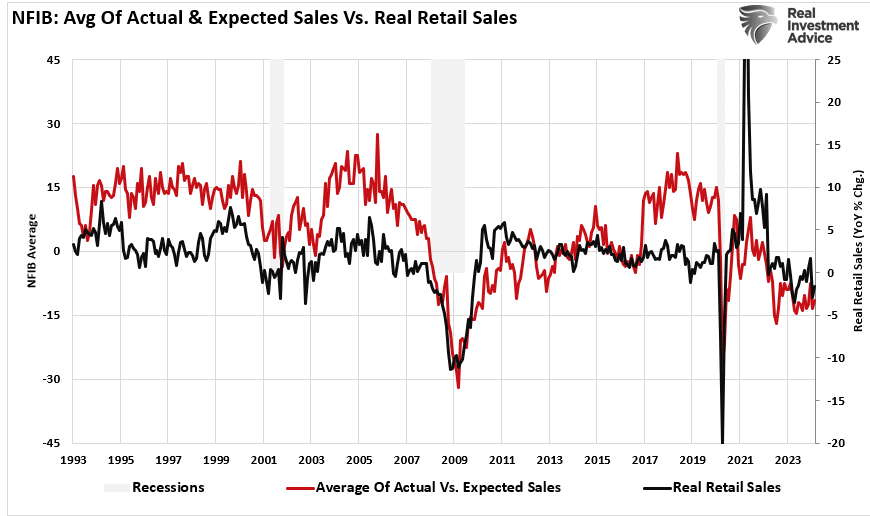

Here is the economic warning to pay attention to. Real retail sales comprise about 40% of personal consumption expenditures (PCE), roughly 70% of the economic growth rate. The decline in the average of actual and expected sales of small businesses suggests weaker retail sales and, by extension, a slower economic growth rate.

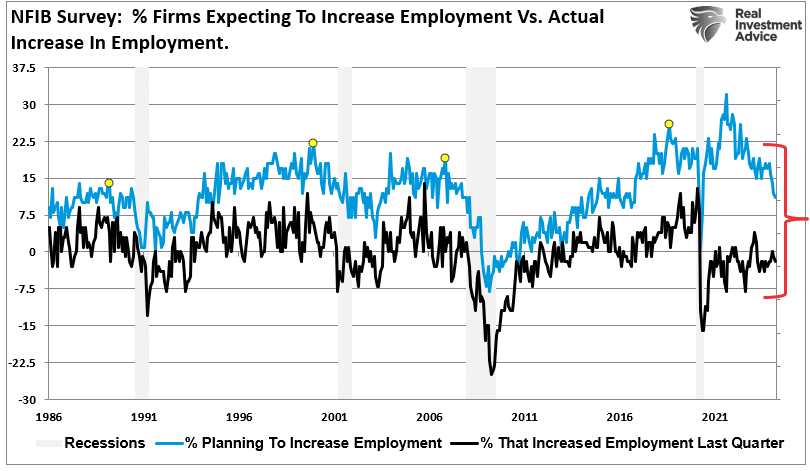

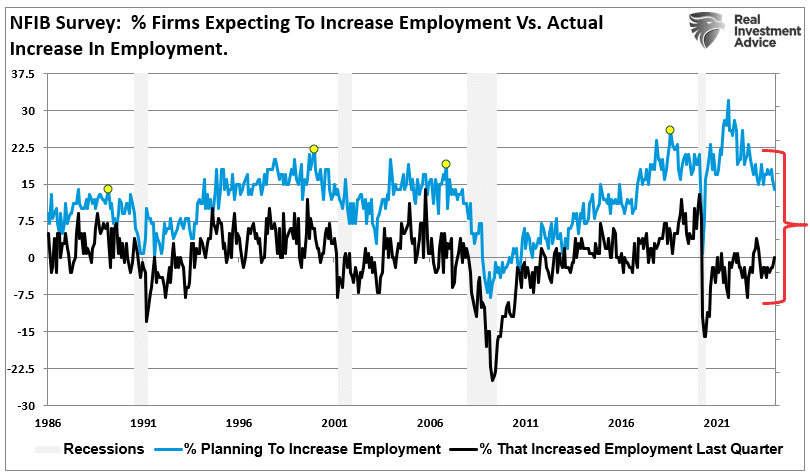

EmploymentWarning

The demand side of the economic equation is crucially important. If the demand for a business owner’s products or services declines, there is little need to increase employment. Therefore, if economic growth was as robust as headlines suggest, why are small businesses’ plans to increase employment declining sharply?

Furthermore, when demand falls, business owners look to cut operating costs to protect profitability. While cutting future employment is part of that equation, so are plans to raise worker compensation.

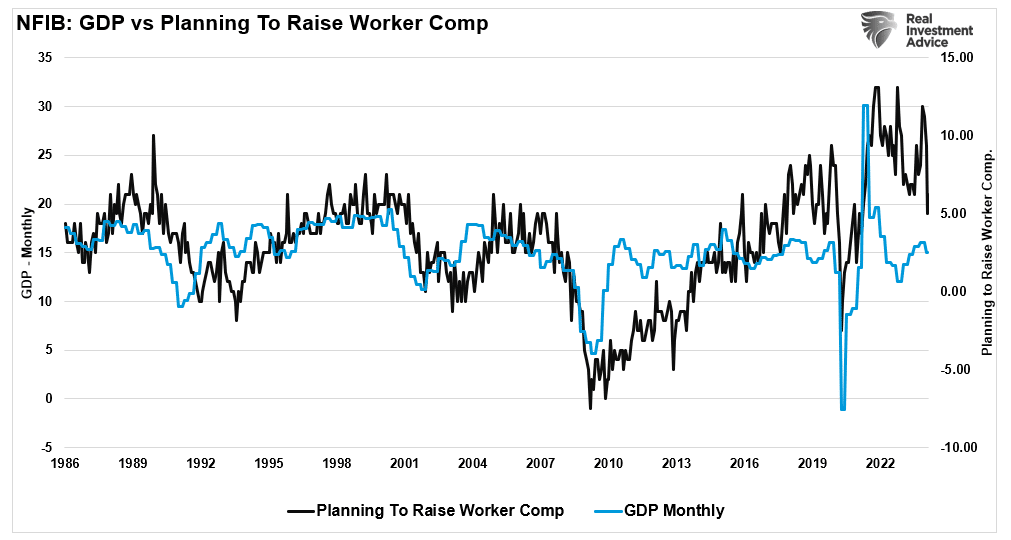

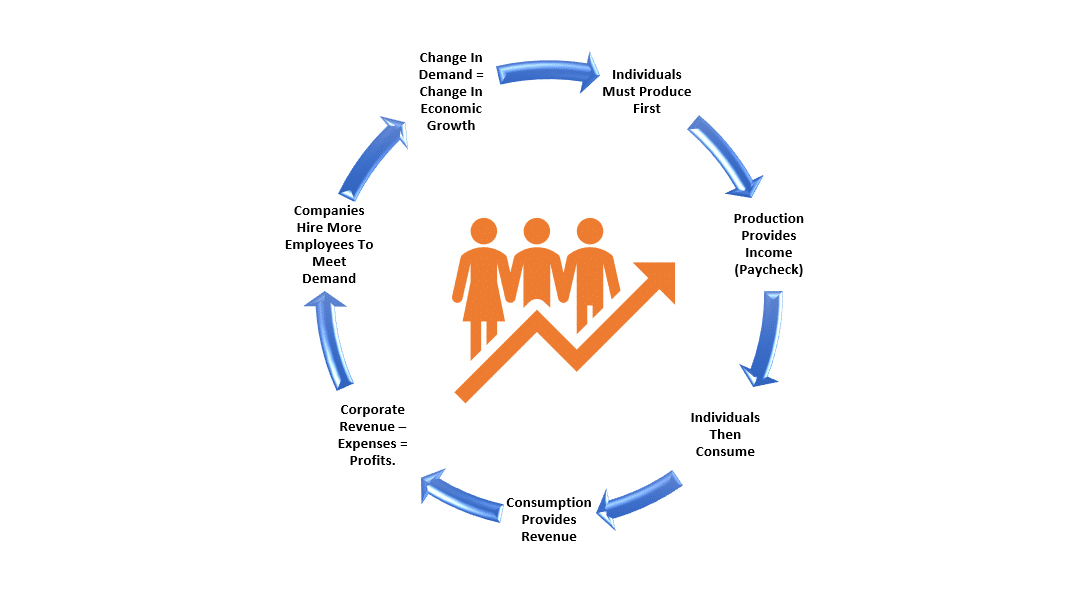

The last chart is crucial. The U.S. is a consumption-based economy. However, consumers can not consume without producing something first. Production must come first to generate the income needed for that consumption. The cycle is displayed below.

As employees receive fewer compensation increases (raises, bonuses, etc.) amid rising living costs, they cut consumption, which translates into slower economic growth rates. In turn, business owners cut employment and compensation further. It is a virtual spiral that historically ends in recession.

While this time could certainly be different, the economic warnings from the NFIB survey should not be dismissed. The data could explain why the Fed is adamant about cutting rates.

Immigration And Its Impact On Employment

Is immigration why employment reports from the Bureau of Labor Statistics (BLS) continue defying mainstream economists’ estimates? Many are asking this question as the U.S. experiences a flood of immigrants across the southern border. Concurrently, many young college graduates continue to complain about the inability to receive a job offer. As noted recently by CNBC:

The job market looks solid on paper. According to government data, U.S. employers added 2.7 million people to their payrolls in 2023. Unemployment hit a 54-year low of 3.4% in January 2023 and ticked up just slightly to 3.7% by December.

But active job seekers say the labor market feels more difficult than ever. A 2023 survey from staffing agency Insight Global found that recently unemployed full-time workers had applied to an average of 30 jobs only to receive an average of four callbacks or responses.”

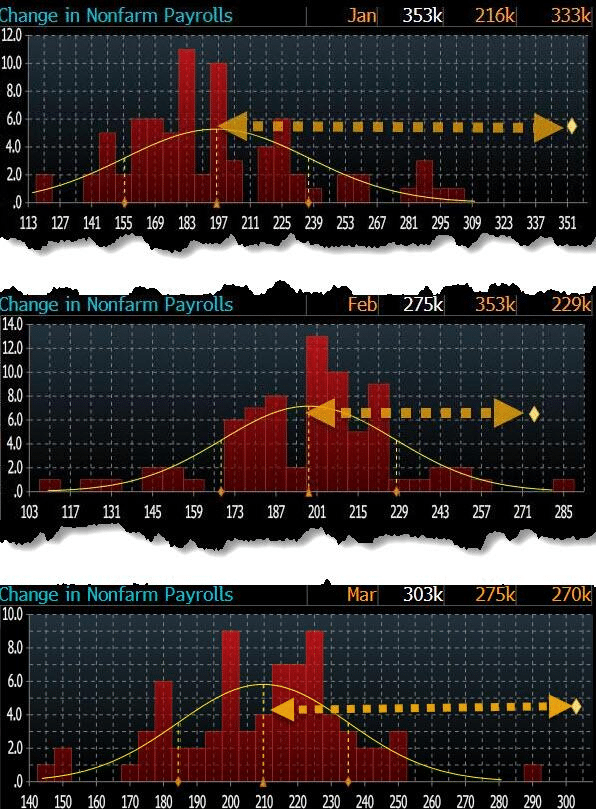

These stories are not unique. If you Google “Can’t find a job,” you will get many article links. Yet employment reports have been exceedingly strong for the past several months.In March, the U.S. economy added 303,000 jobs, exceeding every economist’s estimate by four standard deviations. In terms of statistics, a single four-standard deviation event should be rare. Three months in a row is a near statistical impossibility.

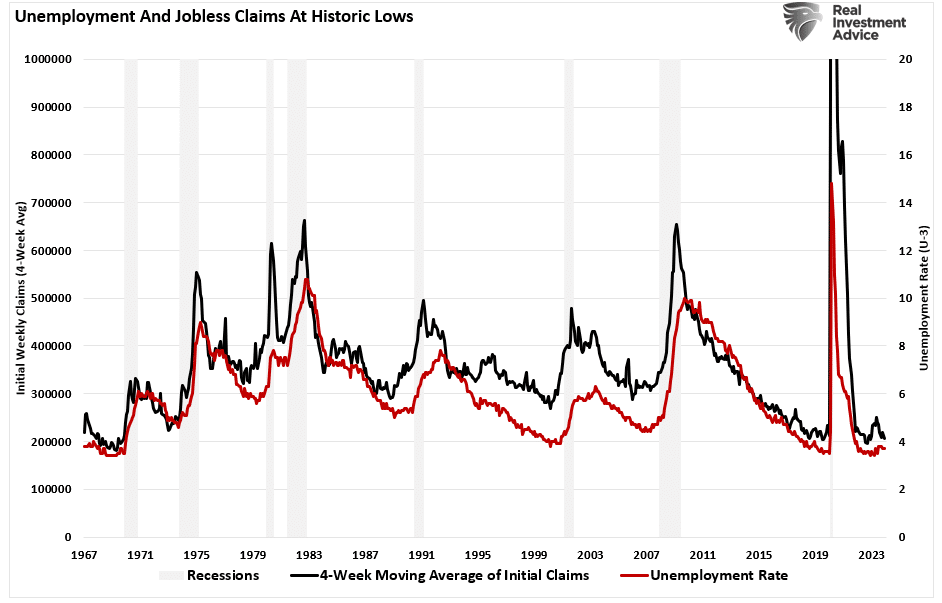

Despite weakness in manufacturing and services, with many companies recently announcing layoffs, we have near-record-low jobless claims and employment. According to official government data, the economy has rarely been more robust.

Such a situation begs an obvious question: How are college graduates struggling to find employment while the labor market remains so strong?

We may find the answer in immigration.

Immigrations Impact By The Numbers

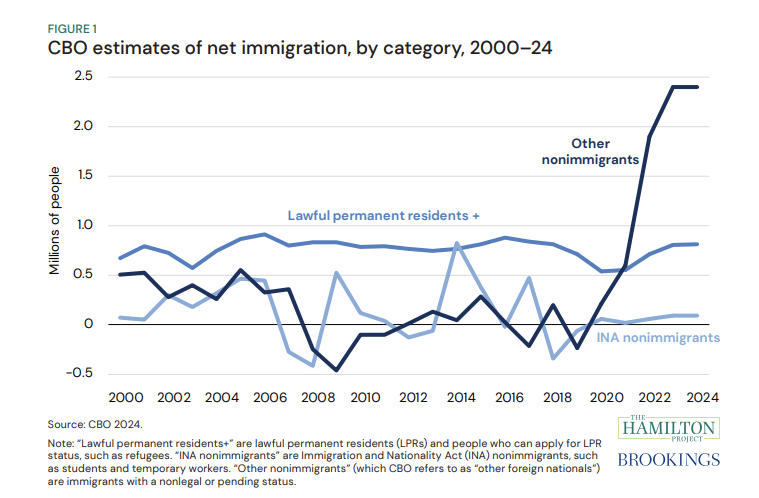

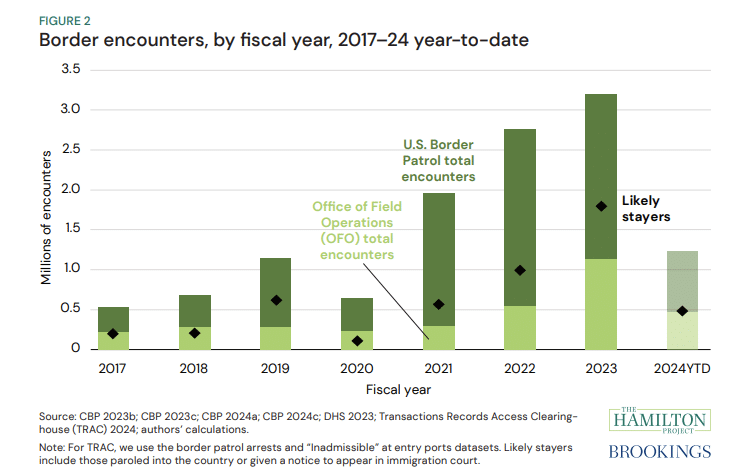

A recent study by Wendy Edelberg and Tara Watson at the Brookings Institution found that illegal immigrants in the country helped boost the labor market, steering the economy from a downturn. Data from the Congressional Budget Office shows a massive uptick of 2.4 million “other immigrants” who don’t fall into the category of lawful immigrants or those on temporary visas. The chart below shows how this figure has spiked from a level of less than 500,000 at the beginning of the 2020s.

The most significant change relative to the past stems from CBO’s other non-immigrant category, which includes immigrants with a nonlegal or pending status.

“We indicate our estimates of ‘likely stayers’ by diamonds in Figure 2. In FY 2023, almost a million people encountered at the border were given a ‘notice to appear,’ meaning they have permission to petition a court for asylum or other immigration relief. Most of these individuals are waiting in the U.S. for the asylum court queue, which has over a million case backlog. In addition, over 800,000 have been granted humanitarian parole (mostly immigrants from Ukraine, Haiti, Cuba, Nicaragua, and Venezuela). These 1.8 million ‘likely stayers’ in FY 2023 may or may not remain in the U.S. permanently, but most are currently living in the U.S. and participating in the economy. CBO estimates that there were 2 million such entries over the calendar year 2023, which is consistent with higher encounters at the end of the calendar year.”

According to the CBO’s estimates for 2023, the categories of lawful permanent resident migration, INA non-immigrant, and other non-immigrant equated to 3.3 million net entries. However, the number is likely much higher than estimates, subject to uncertainty about unencountered border crossings, visa overstays, and “got-aways.”

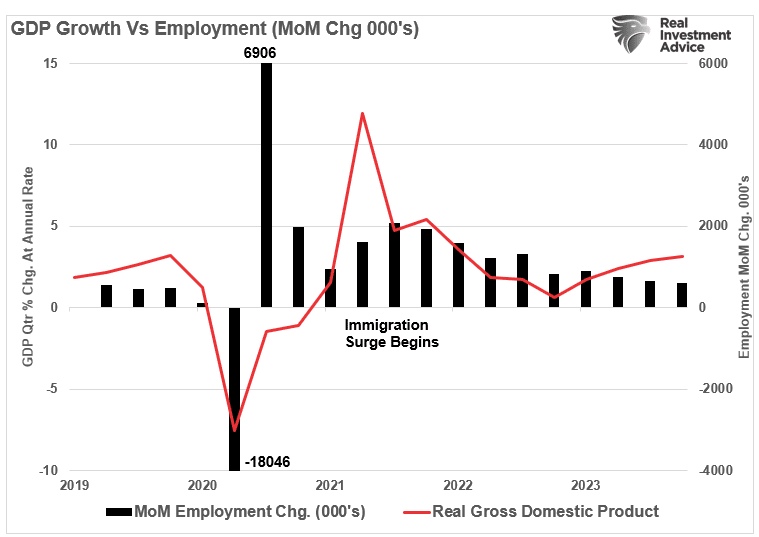

As such, this influx of immigrants has significantly added to payroll growth and has accounted for the uptick in economic growth starting in 2022. While the uptick in border encounters began in earnest in 2021, as the current Administration repealed previous border security actions, there is a “lag effect” of immigration on economic growth.

However, not all jobs are created equal.

Immigration’s Impact On Job Availability

Since 1980, the U.S. economy has shifted from a manufacturing-based economy to a service-oriented one. The reason is that the “cost of labor” in the U.S. to manufacture goods is too high. Domestic workers want high wages, benefits, paid vacations, personal time off, etc. On top of that are the numerous regulations on businesses from OSHA to Sarbanes-Oxley, FDA, EPA, and many others. All those additional costs are a factor in producing goods or services. Therefore, corporations must offshore production to countries with lower labor costs and higher production rates to manufacture goods competitively.

In other words, for U.S. consumers to “afford” the latest flat-screen television, iPhone, or computer, manufacturers must “export” inflation (the cost of labor and production) to import “deflation”(cheaper goods.) There is no better example of this than a previous interview with Greg Hays of Carrier Industries. Following the 2016 election, President Trump pushed for reshoring U.S. manufacturing. Carrier Industries was one of the first to respond. Mr. Hays discussed the reasoning for moving a plant from Mexico to Indiana.

“So what’s good about Mexico? We have a very talented workforce in Mexico. Wages are obviously significantly lower. About 80% lower on average. But absenteeism runs about 1%. Turnover runs about 2%. Very, very dedicated workforce.Which is much higher versus America. And I think that’s just part of these — the jobs, again, are not jobs on an assembly line that [Americans] really find all that attractive over the long term.“

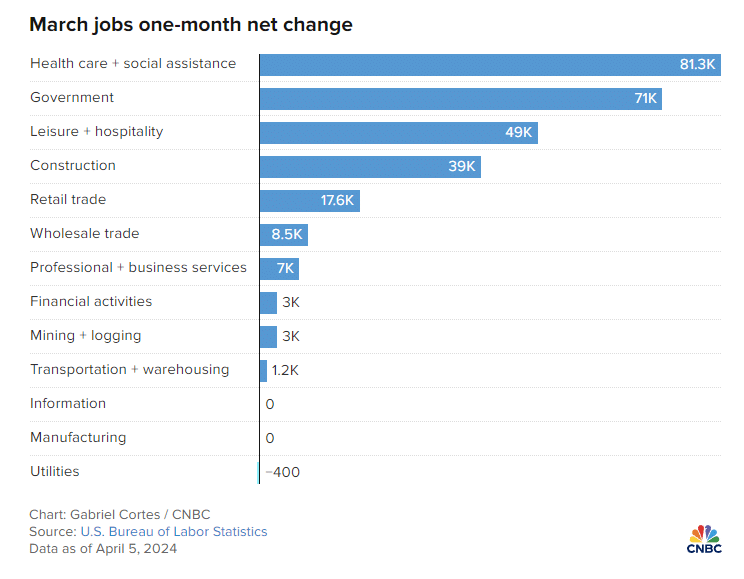

The need to lower costs by finding cheaper and plentiful sources of labor continues. While employment continues to increase, the bulk of the jobs created are in areas with lower wages and skill requirements.

“The continued rebound of these jobs, along with strong months for sectors like construction, could be a sign that immigration is helping the labor market grow without putting too much upward pressure on wages.”

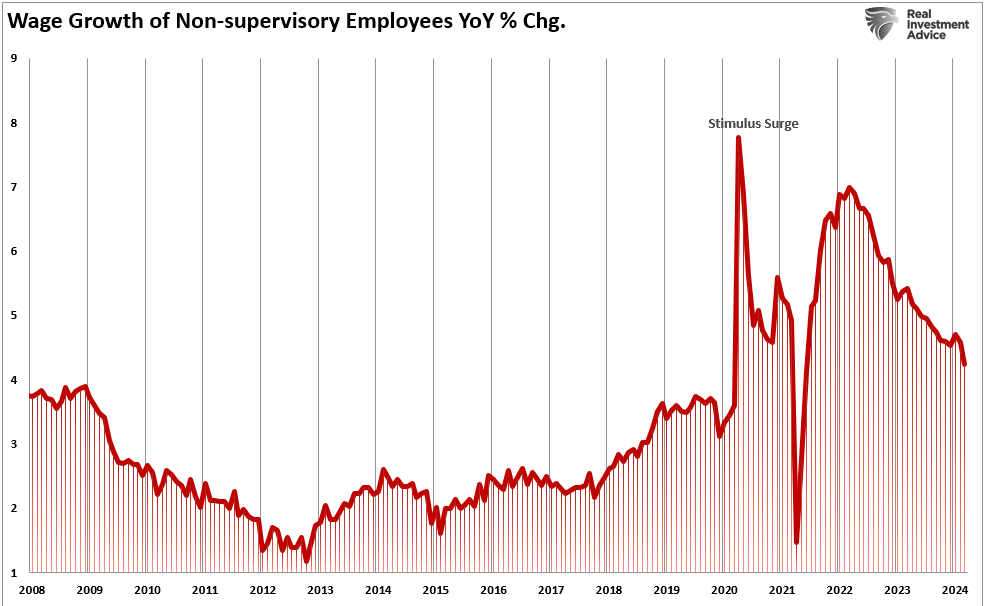

This is a crucial point. If there is strong employment growth, wages should increase commensurately as the demand for labor increases. However, that isn’t happening, as the cost of labor is suppressed by hiring workers willing to work for less compensation. In other words, the increase in illegal immigrants is lowering the “average” wage for Americans.

Nonetheless, in the last year, 50% of the labor force growth came from net immigration. The U.S. added 5.2 million jobs last year, which boosted economic growth without sparking inflationary pressures.

While immigration has positively impacted economic growth and disinflation, this story has a dark side.

FED CHAIR POWELL: Because, you know, immigrants come in, and they tend to work at a rate that is at or above that for non-immigrants. Immigrants who come to the country tend to be in the workforce at a slightly higher level than native Americans. But that’s primarily because of the age difference. They tend to skew younger.“

You should read that comment again carefully. As noted by Greg Hayes, immigrants tend to work harder and for less compensation than non-immigrants. That suppression of wages and increased productivity, which reduces the amount of required labor, boosts corporate profitability.

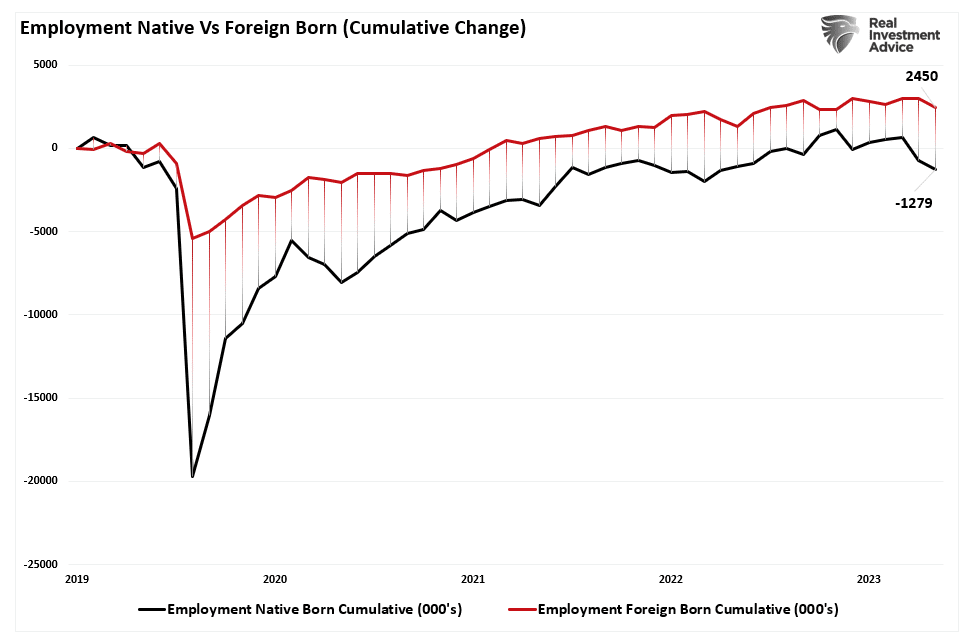

The move to hire cheaper labor should be unsurprising. Following the pandemic-related shutdown, corporations faced multiple threats to profitability from supply constraints, a shift to increased services, and a lack of labor. At the same time, mass immigration (both legal and illegal) provided a workforce willing to fill lower-wage paying jobs and work regardless of the shutdown. Since 2019, the cumulative employment change has favored foreign-born workers, who have gained almost 2.5 million jobs, while native-born workers have lost 1.3 million. Unsurprisingly, foreign-born workers also lost far fewer jobs during the pandemic shutdown.

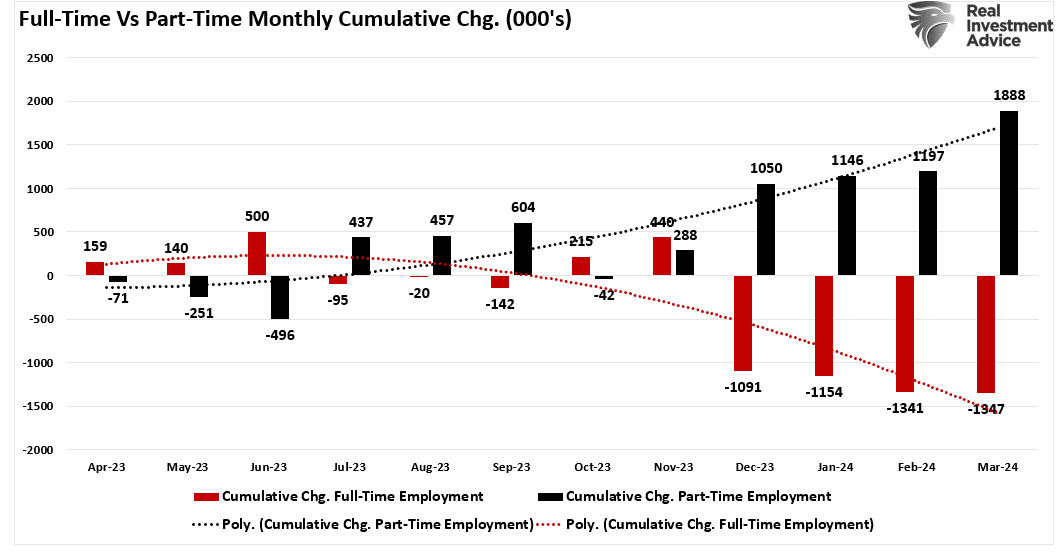

Given that the bulk of employment continues to be in lower-wage paying service jobs (i.e., restaurants, retail, leisure, and hospitality) such is why part-time jobs have dominated full-time in recent reports. Since last year, part-time jobs have risen by 1.8 million while full-time employment has declined by 1.35 million.

Not dismissing the implications of the shift to part-time employment is crucial.

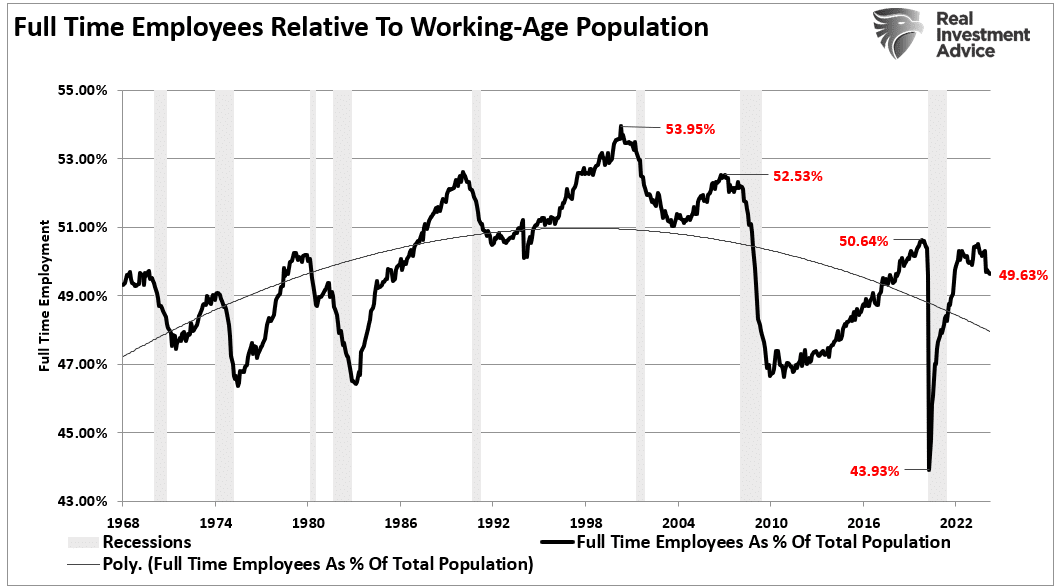

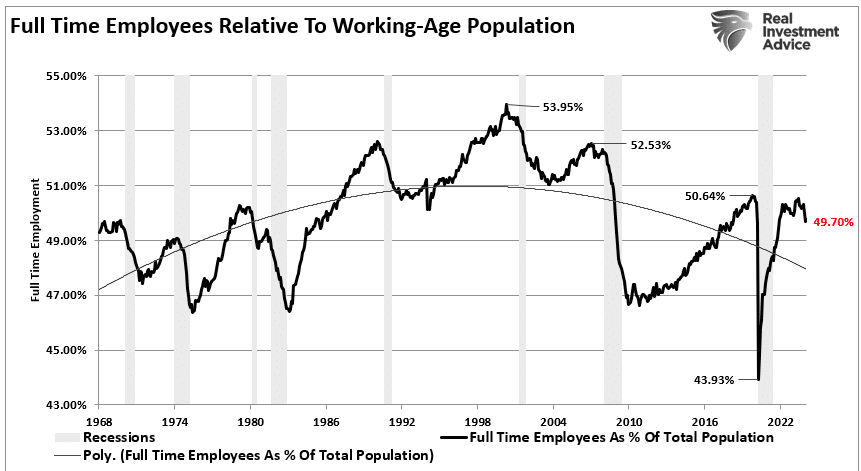

Personal consumption, what you and I spend daily, drives nearly 70% of economic growth in the U.S. Therefore, Americans require full-time employment to consume at an economically sustainable rate. Full-time jobs provide higher wages, benefits, and health insurance to support a family, whereas part-time jobs do not.

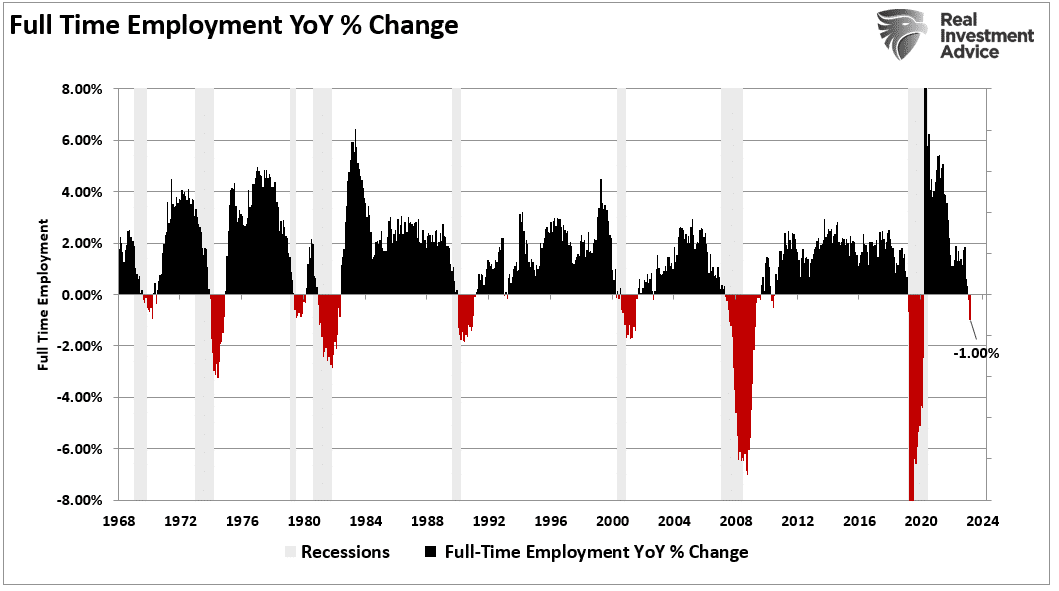

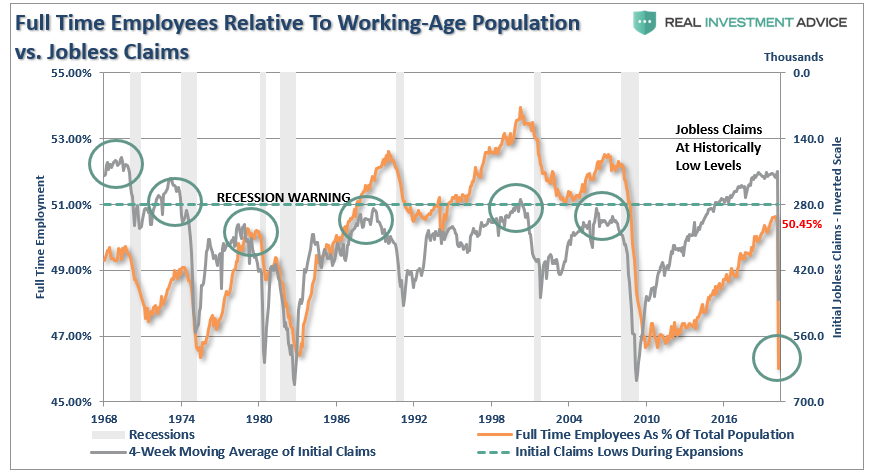

Notably, given the surge in immigration into the U.S. over the last few years, the all-important ratio of full-time employees relative to the population has dropped sharply. As noted, given that full-time employment provides the resources for excess consumption, that ratio should increase for the economy to continue growing strongly.

However, the reality is that the full-time employment rate is falling sharply. Historically, when the annual rate of change in full-time employment dropped below zero, the economy entered a recession.

While there is much debate over immigration, most of the arguments do not differentiate between legal and illegal immigration. There are certainly arguments that can be made on both sides. However, what is less debatable is the impact that immigration is having on employment and wages. Of course, as native-born workers continue to demand higher wages, benefits, and other tax-funded support, those costs must be passed on by the companies creating those products and services. At the same time, consumers are demanding lower prices.

That imbalance between input costs and selling price drives companies to aggressively seek options to reduce the highest cost to any business – labor.

Such is why full-time employment has declined since 2000 despite the surge in the Internet economy, robotics, and artificial intelligence. It is also why wage growth fails to grow fast enough to sustain the cost of living for the average American. These technological developments increased employee productivity, reducing the need for additional labor.

Unfortunately, college graduates expecting high-paying jobs will likely continue to find it increasingly frustrating. Such is particularly the case as “Artificial Intelligence” gains traction and displaces “white collar” work, further squeezing the demand for “native-born” workers.

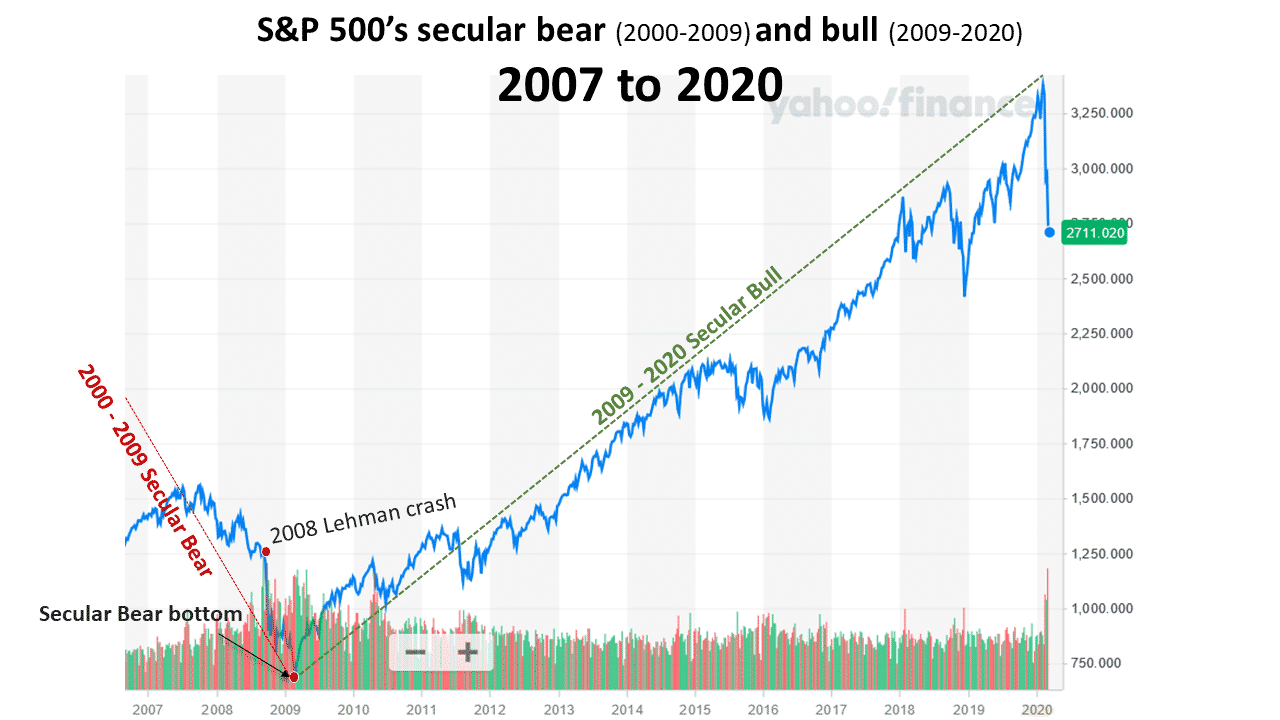

Market Corrections Matter More Than You Think

During running bull markets, much commentary is written on why this time is different and why investors should not worry about market corrections. One such piece was written recently by Fisher Investments. To wit:

“After the S&P 500’s 26% return last year and this year’s strong start, many investors are worried – understandably – that this bull run is getting ahead of itself.

They shouldn’t. The strange-but-true fact is that, statistically speaking, average returns — which have amounted to about 10% a year over nearly a century of trading — aren’t normal in the stock market for any given year. A second, surprisingly pleasant fact is that so-called “extreme” returns are far closer to what we’d call normal — and they’re mostly on the positive side.”

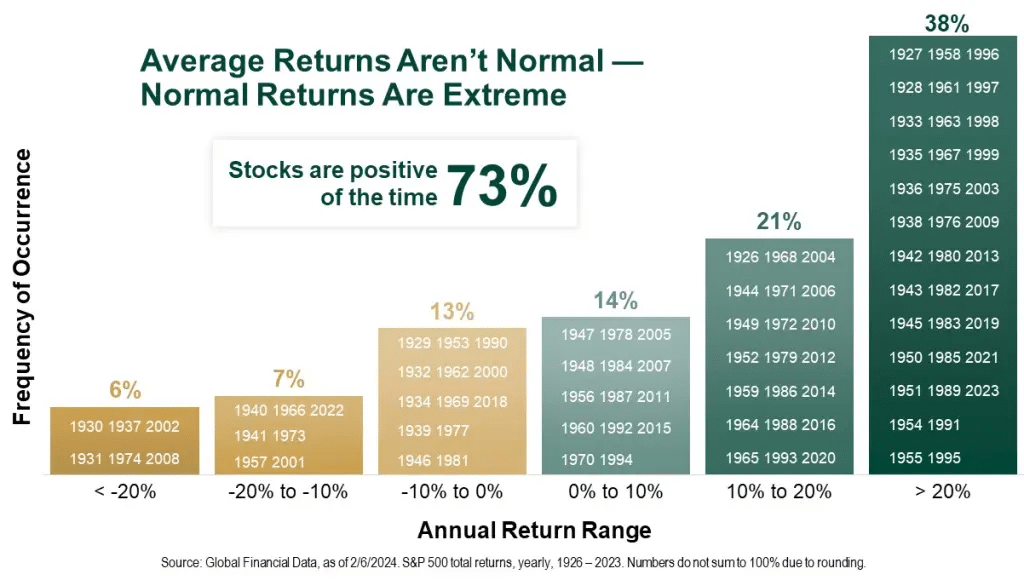

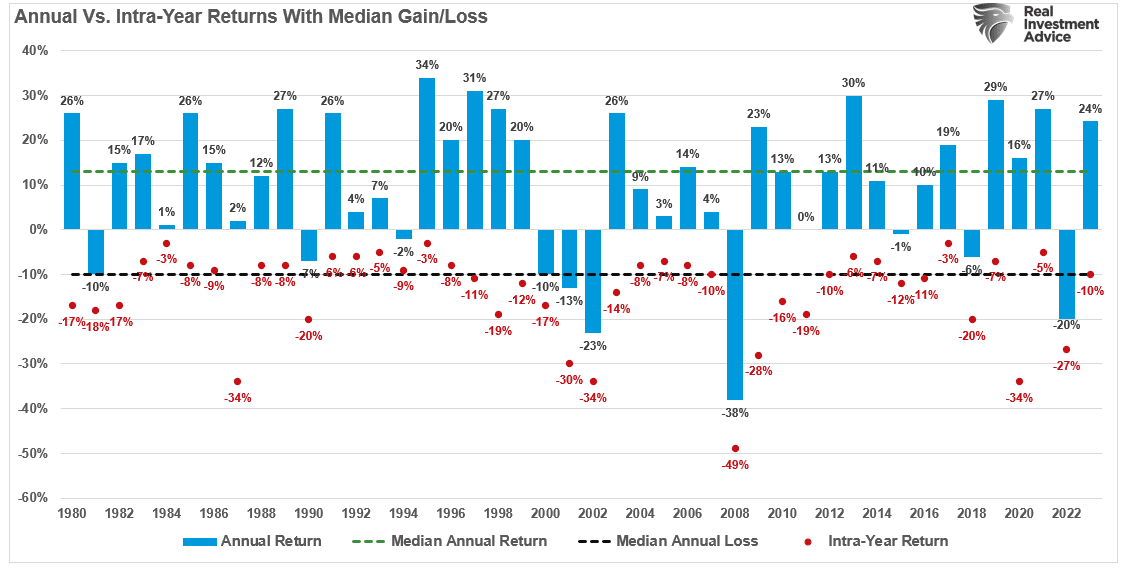

There are a lot of problems with that statement, which we will get into. However, there are some essential facts about markets that should be understood. First, indeed, stocks rise more often than they fall. Historically speaking, the stock market increases about 73% of the time. The other 27% of the time, market corrections are reversing the excesses of the previous advance. The table below shows the dispersion of returns over time.

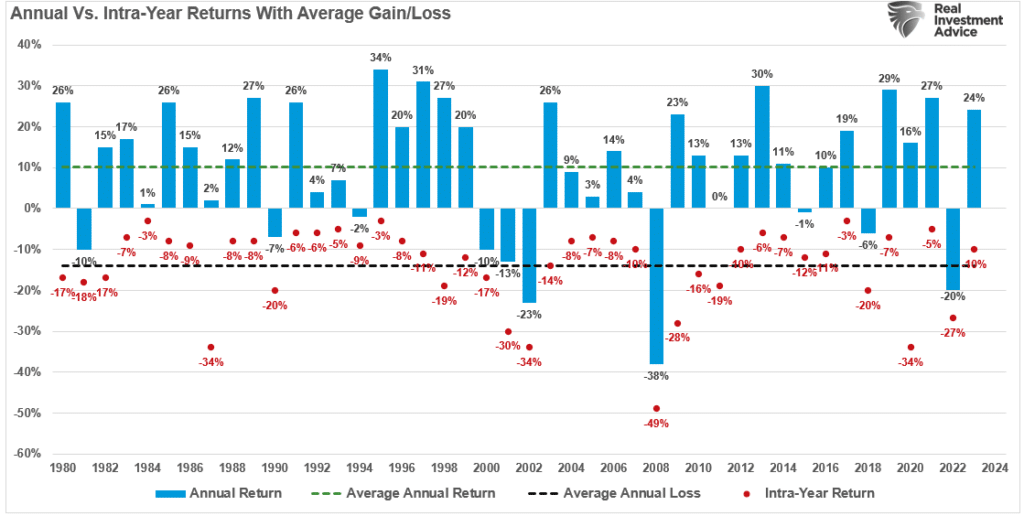

However, fairly substantial corrections have not been uncommon in those positive return years. As shown in the table below, intra-year corrections, which average roughly 10%, are common.

There is little to be concerned about as 38% of the time, the market is cranking out greater than 20% returns versus just 6% of 20% or more market corrections. As Mr. Fisher notes:

“The upshot? Big returns simply aren’t the rarity that “too far, too fast” bears claim. In bull markets, they are more normal than not. Why? The roughly 10% long-term annual average includes bear markets. Strip out the bears and you’ll find that during the 14 S&P 500 bull markets before this one, stocks annualized 23%.“

The problem with Mr. Fisher’s statement is that he doesn’t understand the math behind market corrections. As we will explain, a significant difference exists between a 20% advance and a 20% market correction. Such is particularly the case if you are in or approaching retirement.

Market Corrections And The Function Of Math

Notice that the table above uses percentage returns. As noted, that is a deceptive take if you don’t examine the issue beyond a cursory glance.

For example, assume an arbitrary stock market index that trades at 1000 points. Over the next 12 months, the index will increase by 20%. The index value is now 1200 points.

During the next 12 months, the index declines by one of those rare outliers of 20%. The index doesn’t just give up its gain of 200 points.

1200 x (-20%) = 240 points = 960 points

The investor now has an unrealized capital loss.

Let’s take this example further and assume the index goes from 1000 to 8000.

1000 to 2000 = 100% return

From 1000 to 3000 = 200% return

The next 1000 to 4000 = 300% return

…

The final 1000 to 8000 = 700% return

No one would argue that a 700% return on their money wasn’t fantastic. However, let’s do some math:

10% loss equals an 800-point decline, nearly wiping out the last 1000-point advance.

20% market correction is 1600 points

30% decline erases 2400 points.

40% loss equals 3200 points or nearly 50% of all the gains.

50% decline is 4000 points.

The problem with using percentages to measure an advance is that there is an unlimited upside. However,you can only lose 100%.

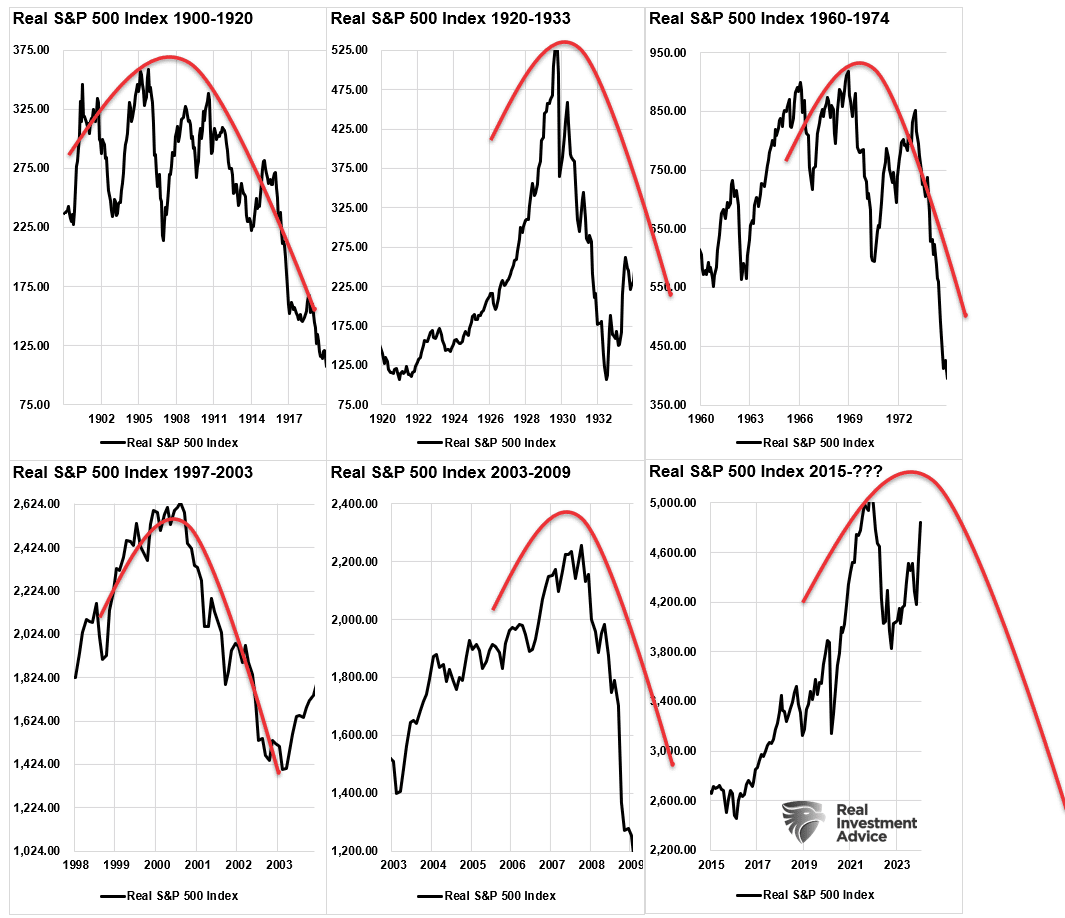

A Graphic Example

That is the problem of percentages. We can also show this graphically.

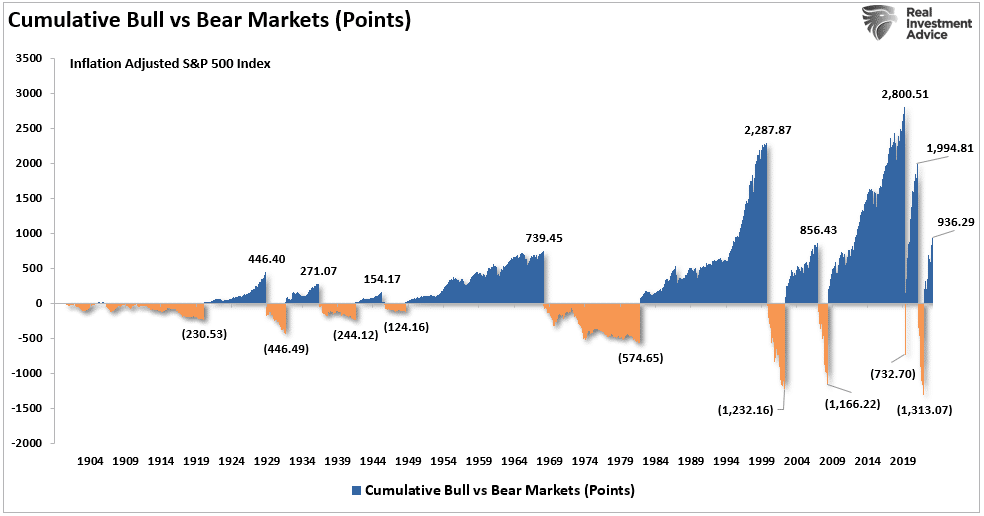

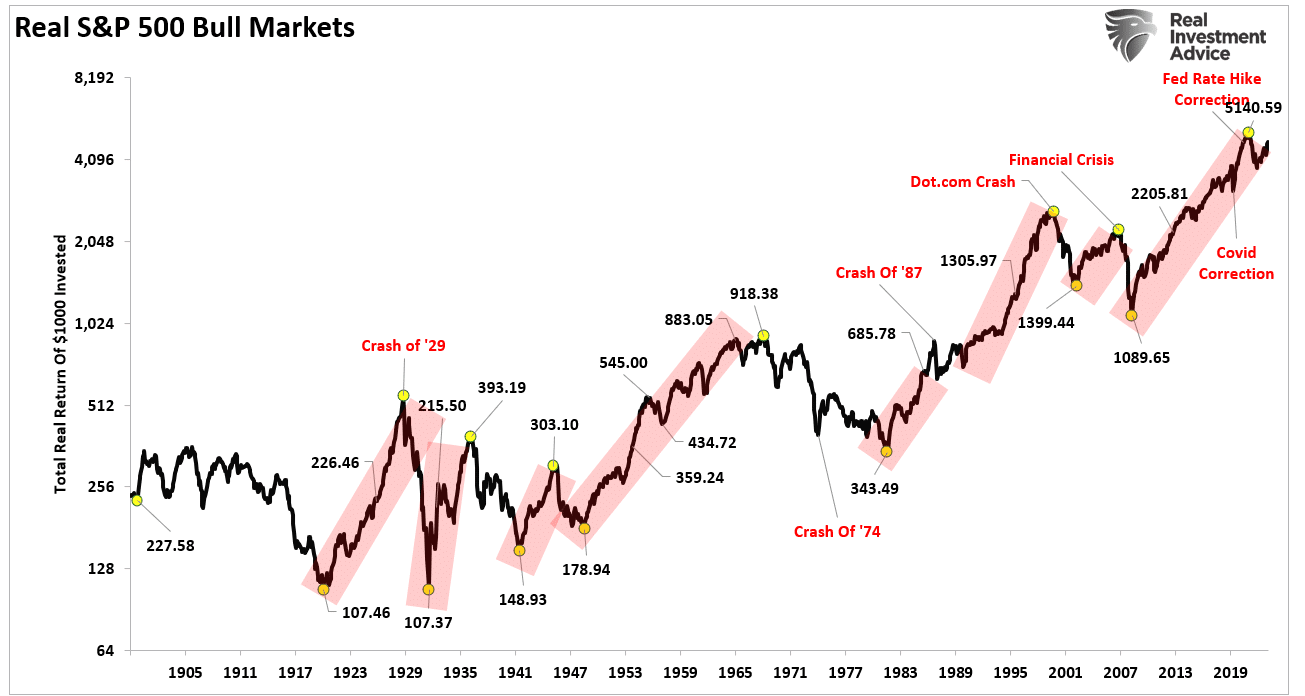

One of the charts often used by the “perma bulls” like Ken Fisher to coax individuals into not worrying about portfolio risk is measuring the cumulative advances and declines of the market in percentages. When presented this way, the bear market corrections are hardly noticeable. This chart is often used to convince individuals that bear markets don’t matter much over the long term.

However, as noted above, this presentation is very deceptive due to how math works. If we change from percentages to actual point changes, the devastation of market corrections becomes more evident. Historically, the subsequent declines wiped out huge chunks of the previous advances. Of course, at the bottom of these market corrections, investors generally sell due to the mounting losses’ psychological pressures.

This is why, after two of the most significant bull markets in history, most individuals have very little money invested in the financial markets.

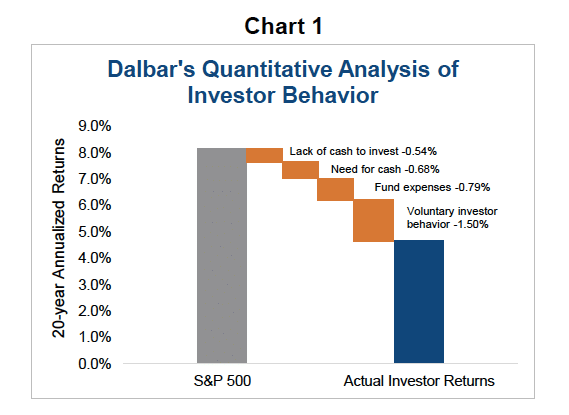

Average And Actual Returns Are Not The Same

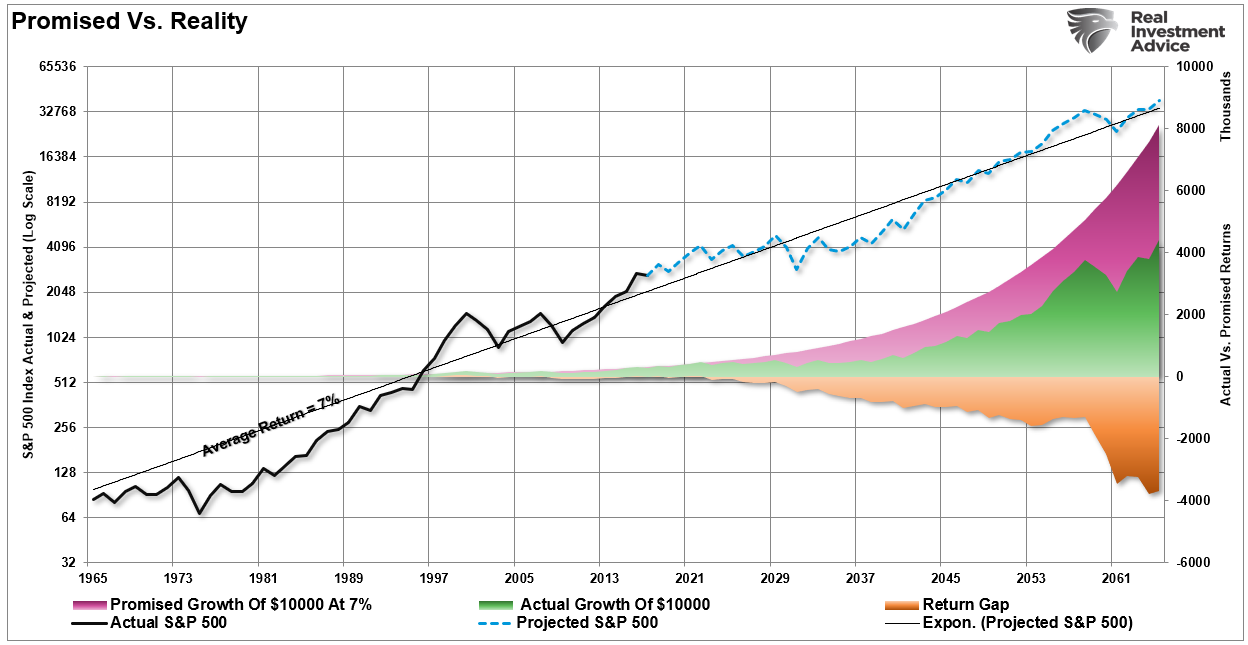

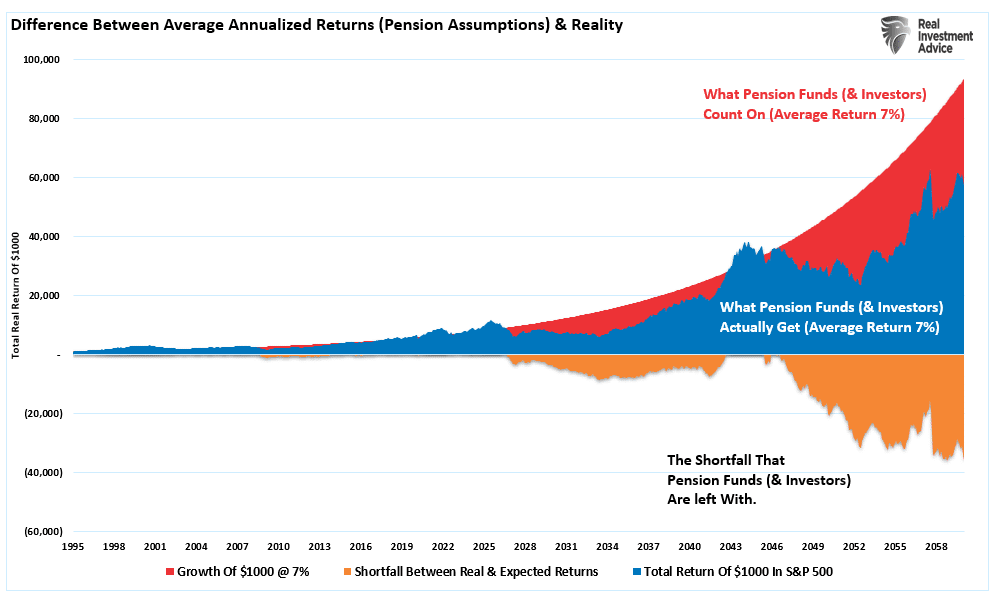

There is a massive difference between AVERAGE and ACTUAL returns on invested capital. Thus, in any given year, the impact of losses destroys the annualized “compounding” effect of money.

The chart below shows the difference between “actual” investment returns and “average” returns over time. See the problem? The purple-shaded area and the market price graph show “average” returns of 7% annually. However, the return gap in “actual returns,” due to periods of capital destruction, is quite significant.

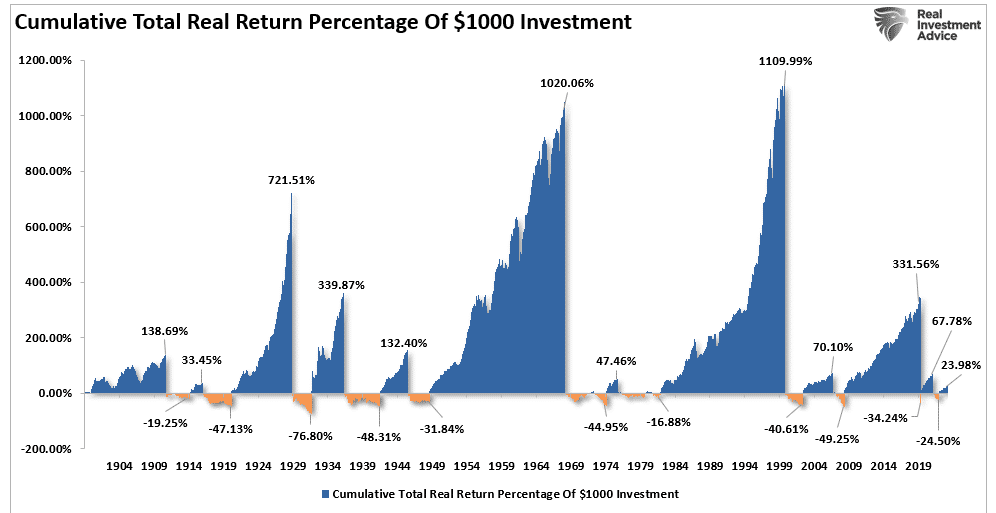

In the chart box below, I have taken a $1000 investment for each period and assumed the total return holding period until death. There are no withdrawals made. (Note: the periods from 1983 forward are still running as the investable life expectancy span is 40-plus years.)

The orange sloping line is the “promise” of 6% annualized compound returns. The black line represents what happened with invested capital from 35 years of age until death. At the bottom of each holding period, the bar chart shows the surplus, or shortfall, of the 6% annualized return goal.

At the point of death, the invested capital is short of the promised goal in every case except the current cycle starting in 2009. However, that cycle is yet to be complete, and the next significant downturn will likely reverse most, if not all, of those gains. Such is why using “compounded” or “average” rates of return in financial planning often leads to disappointment.

Three Key Considerations

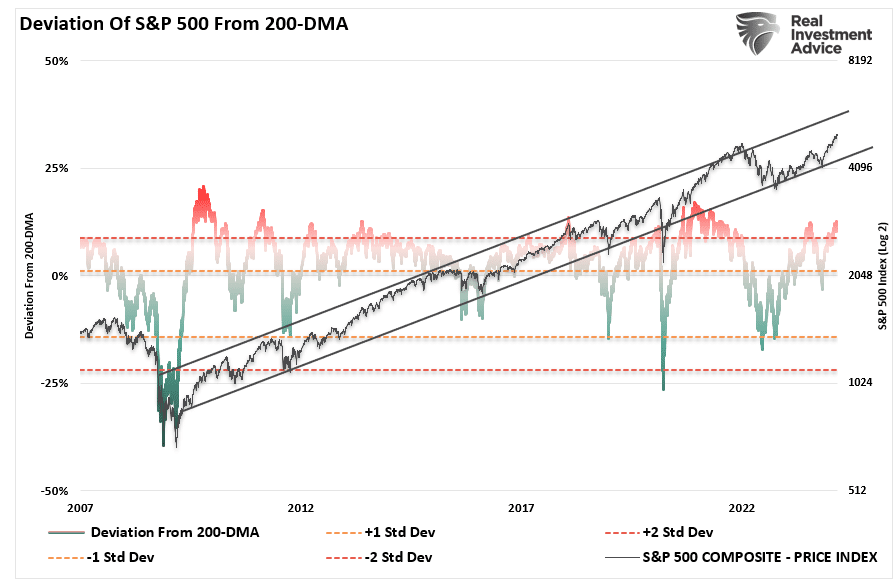

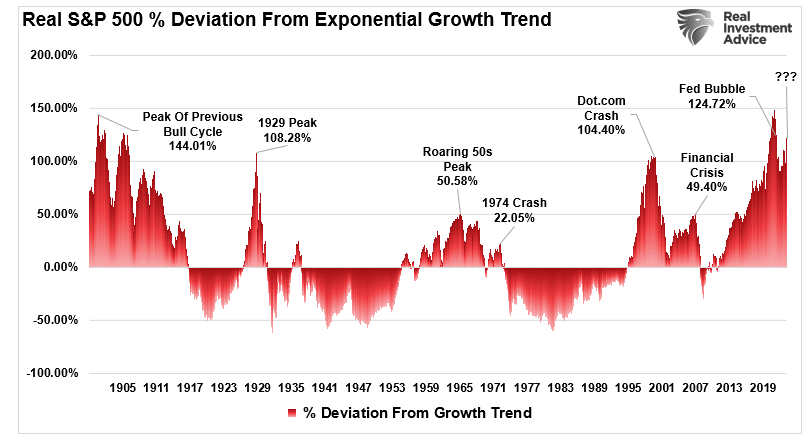

Over the next few months, the markets can extend the current deviations from the long-term mean even further. But that is the nature of every bull market peak and bubble throughout history as the seeming impervious advance lures the last stock market “holdouts” back into the markets.

As such, three key considerations exist for individuals currently invested in the stock market.

Time horizon (retirement age less starting age)

Valuations at the beginning of the investment period.

Rate of return required to achieve investment goals.

Suppose valuations are high at the beginning of the investment journey. In that case, if the time horizon is too short or the required rate of return is too high, the outcome of a “buy and hold” strategy will most likely disappoint expectations.

Mean reverting events expose the fallacies of “buy-and-hold” investment strategies. The “stock market” is NOT the same as a “high yield savings account,” and losses devastate retirement plans. (Ask any “boomer” who went through the dot.com crash or the financial crisis.”)

Therefore, during excessively high valuations, investors should consider opting for more “active” strategies with a goal of capital preservation.

As Vitaliy Katsenelson once wrote:

“Our goal is to win a war, and to do that we may need to lose a few battles in the interim. Yes, we want to make money, but it is even more important not to lose it.”

I agree with that statement, so we remain invested but hedged within our portfolios.

Unfortunately, most investors do not understand market dynamics and how prices are “ultimately bound by the laws of physics.” While prices can certainly seem to defy the law of gravity in the short term, the subsequent reversion from extremes has repeatedly led to catastrophic losses for investors who disregard the risk.

Just remember, in the market, there is no such thing as “bulls” or “bears.”

There are only those who “succeed” in reaching their investing goals and those who “fail.”

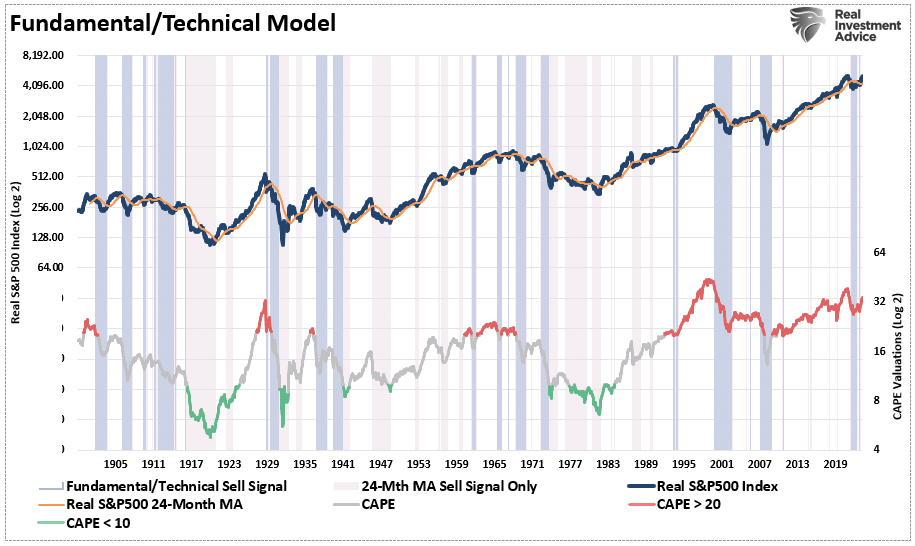

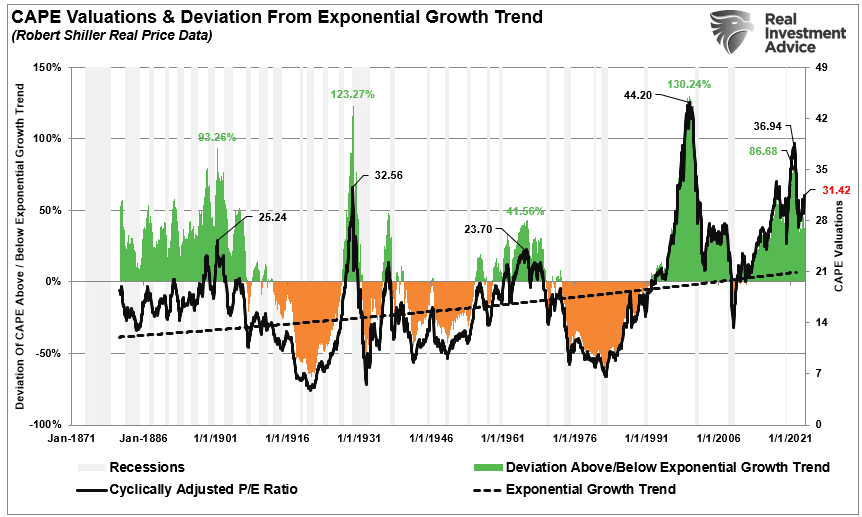

Technical Measures And Valuations. Does Any Of It Matter?

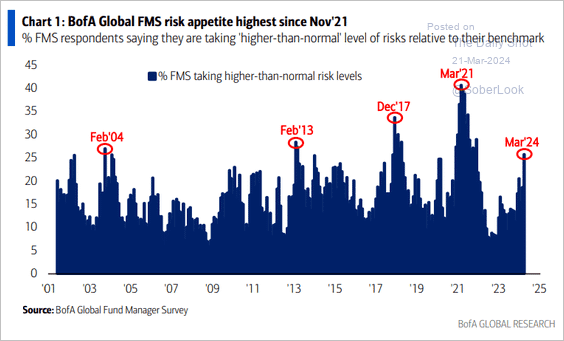

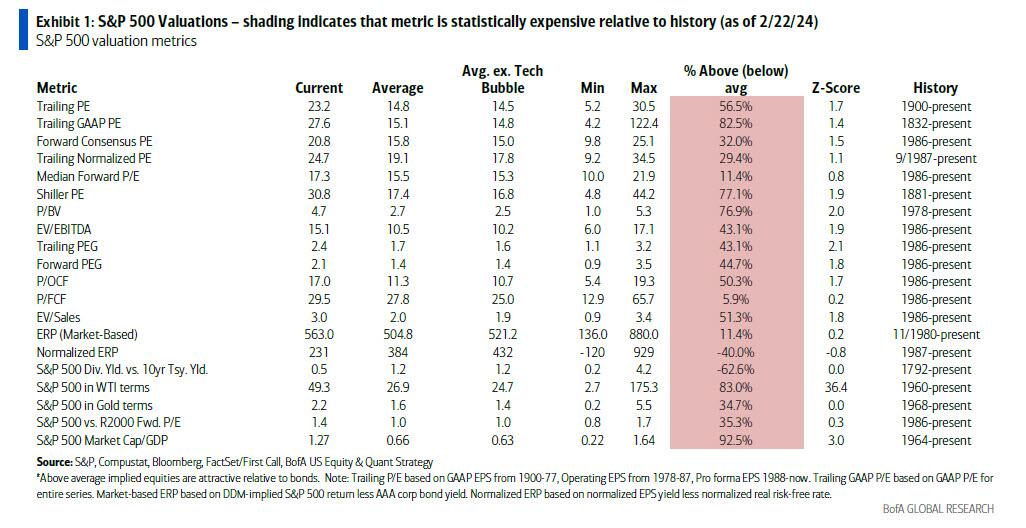

Technical measures and valuations all suggest the market is expensive, overbought, and exuberant. However, none of it seems to matter as investors pile into equities to chase risk assets higher. A recent BofA report shows that the increase in risk appetite has been the largest since March 2021.

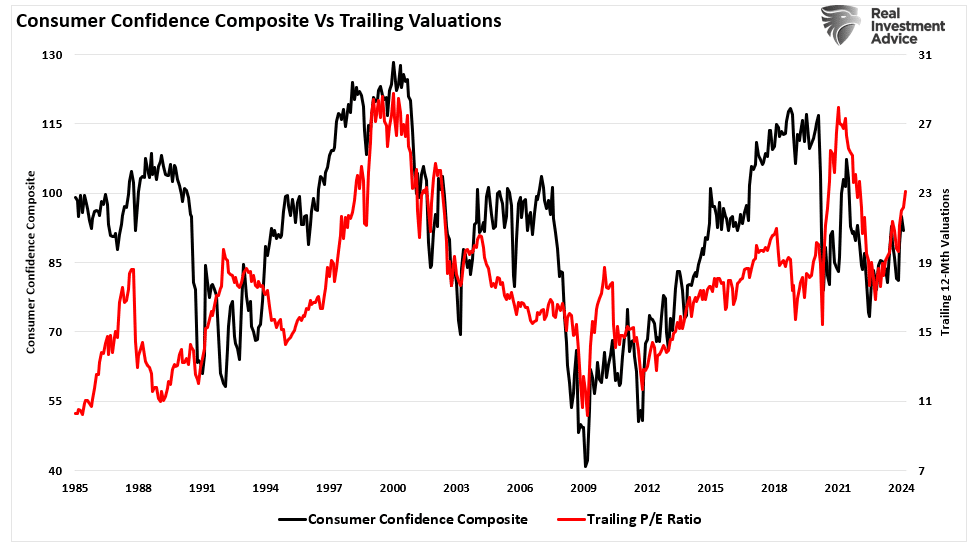

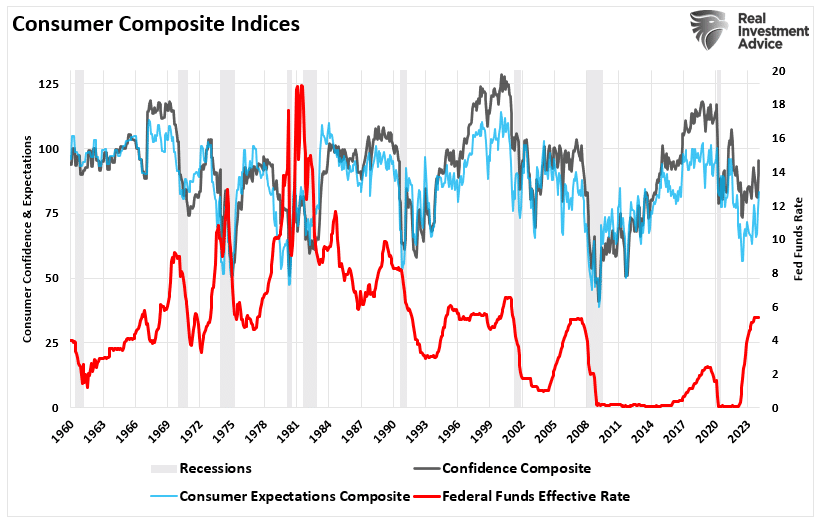

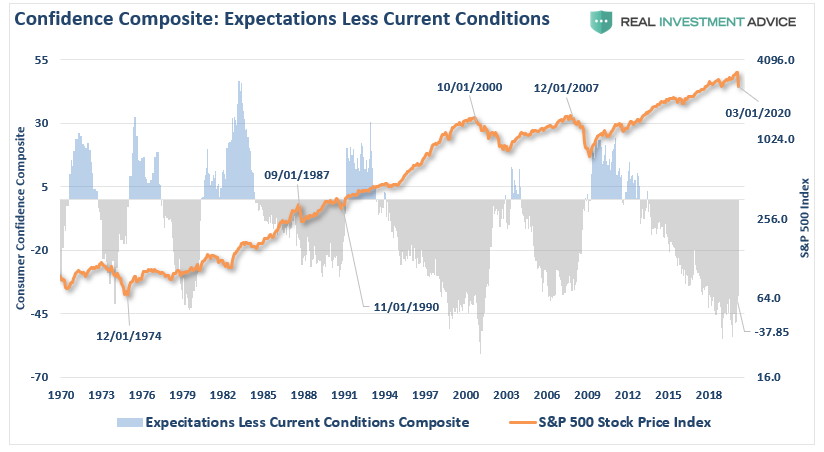

Of course, as prices increase faster than underlying earnings growth, valuations also increase. However, as discussed in “Valuations Suggest Caution,” valuations are a better measure of psychology in the short term. To wit:

“Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of ‘investor psychology’ and the manifestation of the ‘greater fool theory.’ As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.”

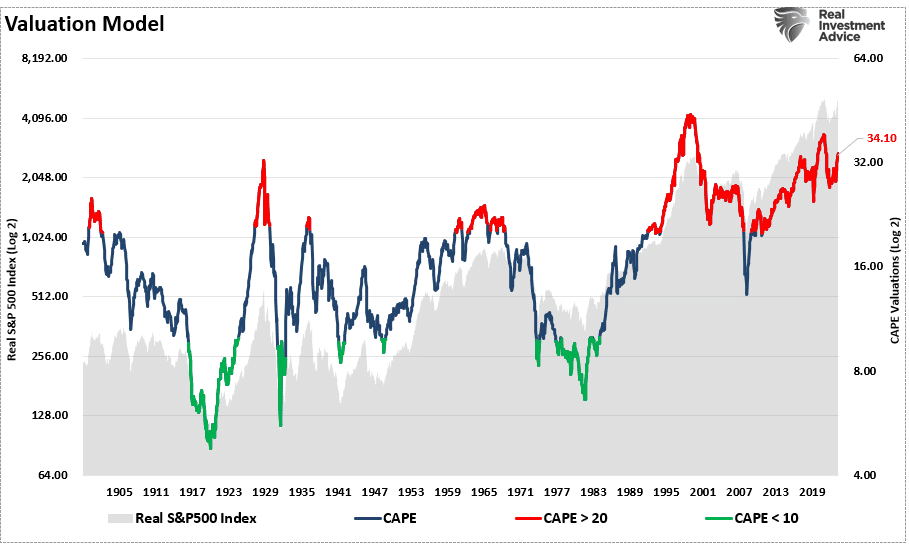

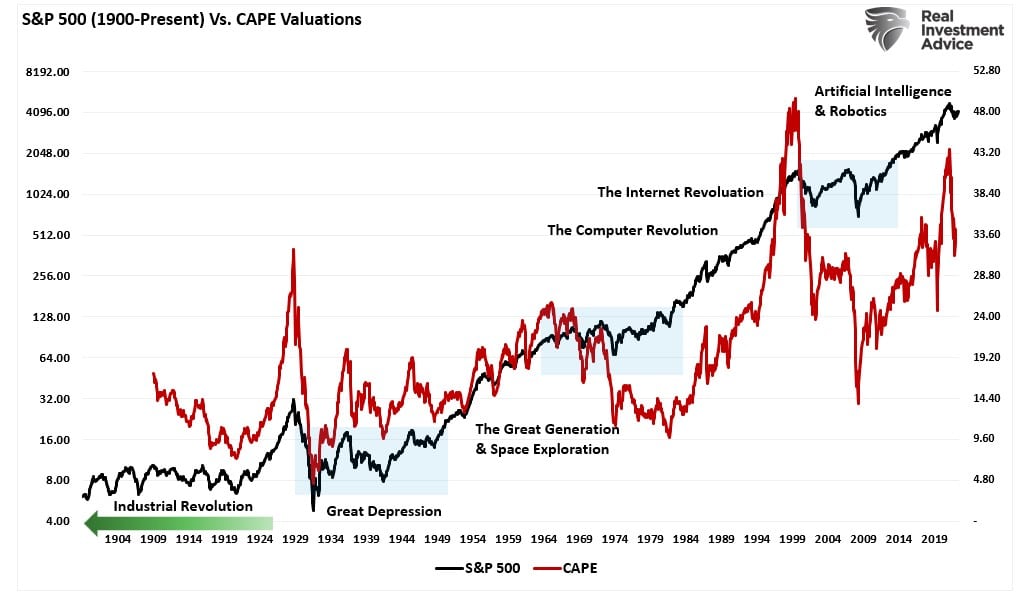

When investors are exuberant and willing to overpay for future earnings growth, valuations increase. The increase in valuations, also known as “multiple expansion,” is a crucial support for bull markets. As shown, the increase in multiples coincides with rising markets. Of course, the opposite, known as “multiple contractions,” is also true. With a current Shiller CAPE valuation multiple of 34x earnings, such suggests that investor confidence is elevated.

As noted, valuations are terrible market timing indicators and should not be used for such. While valuations provide the basis for calculating future returns, technical measures are more critical for managing near-term portfolio risk.

Technical Measures Are Getting Extreme

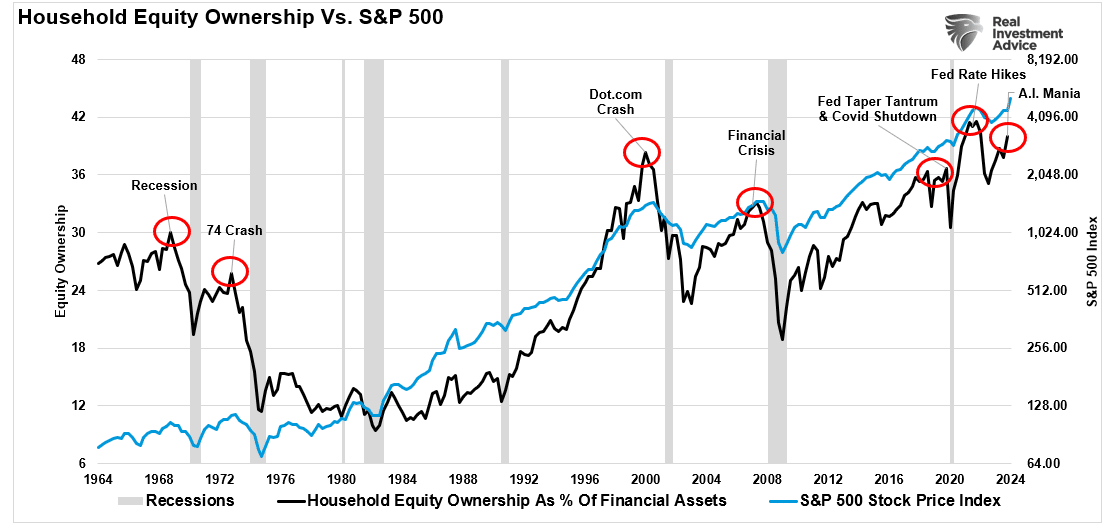

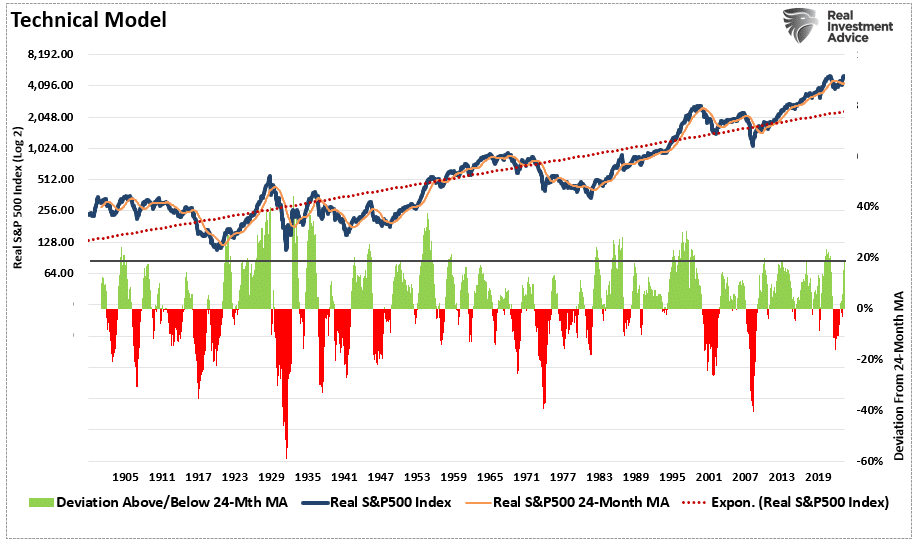

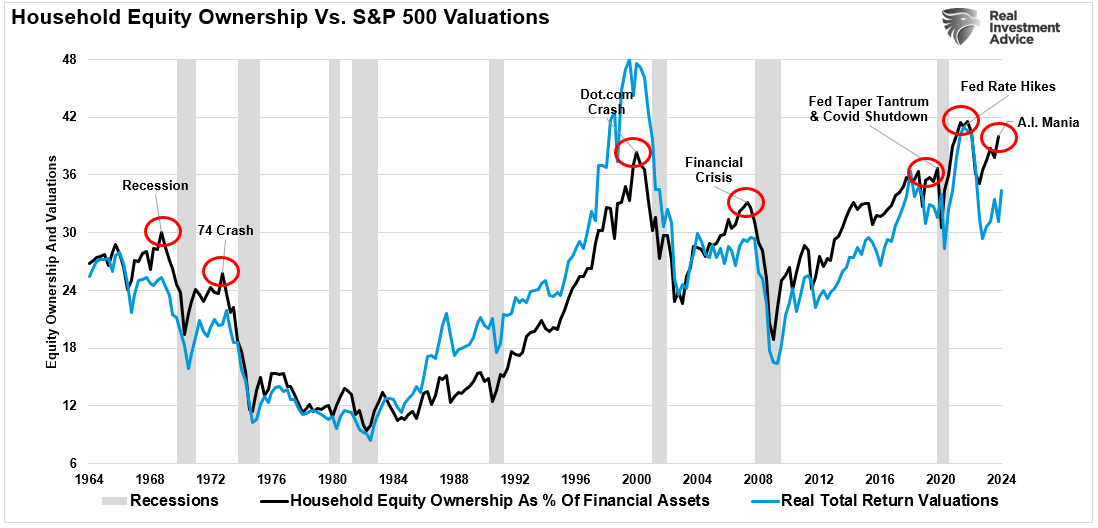

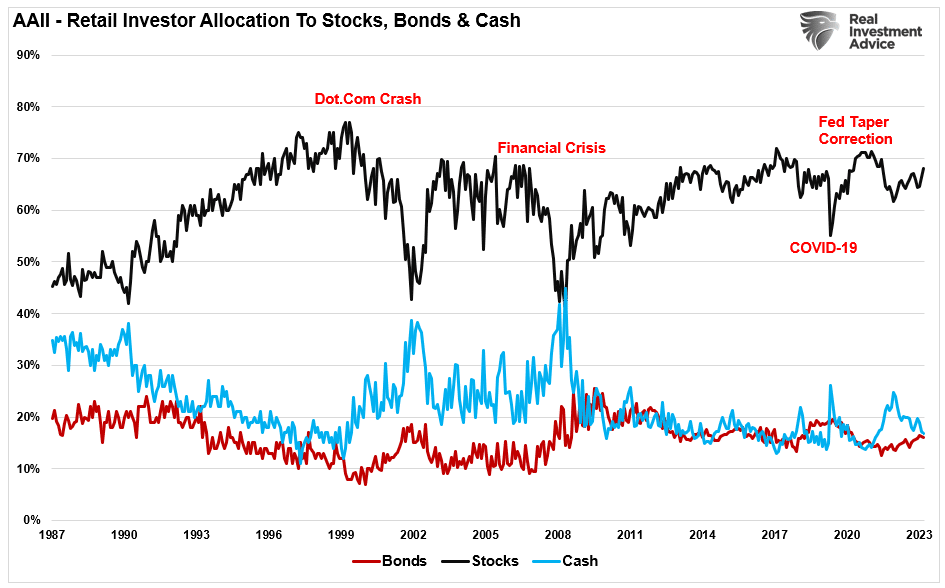

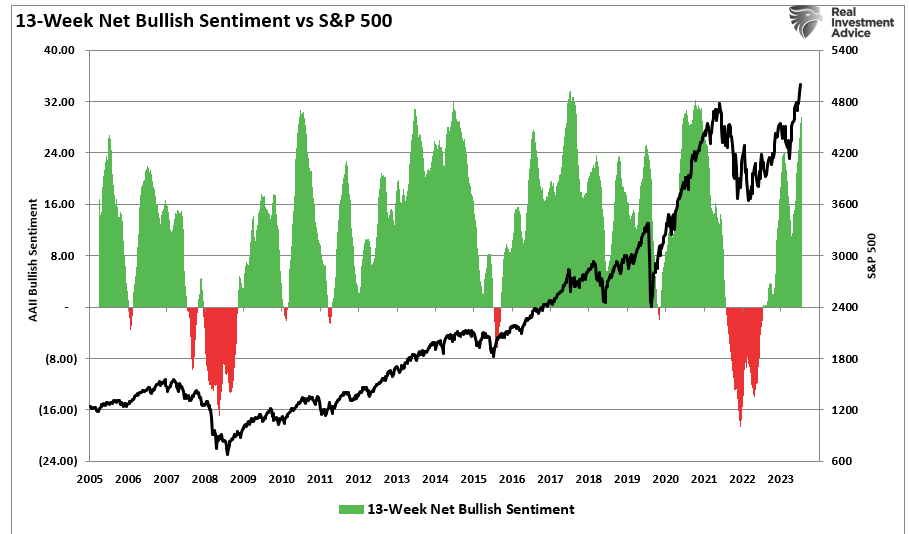

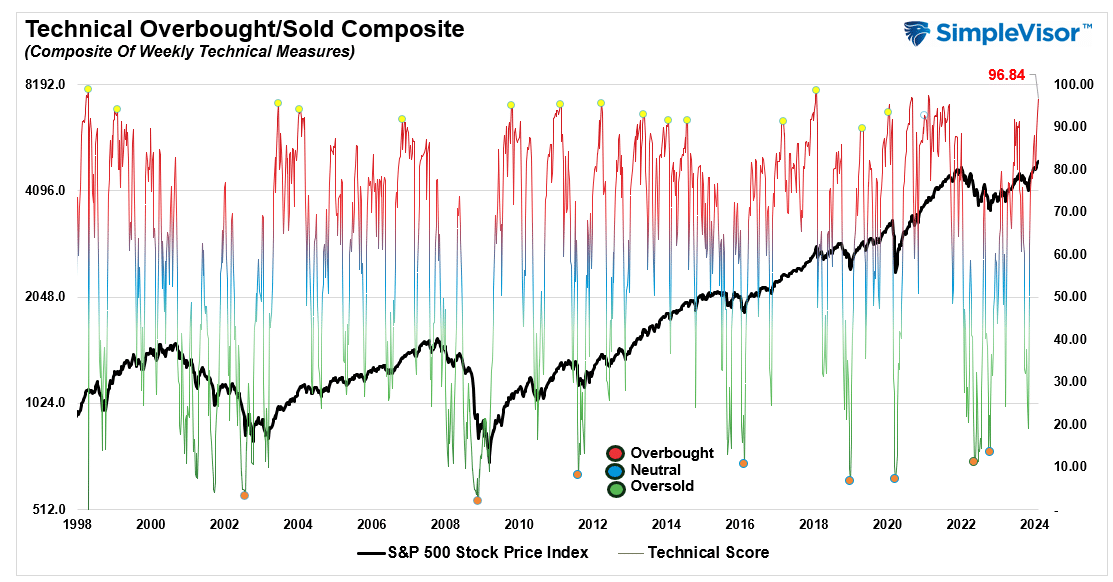

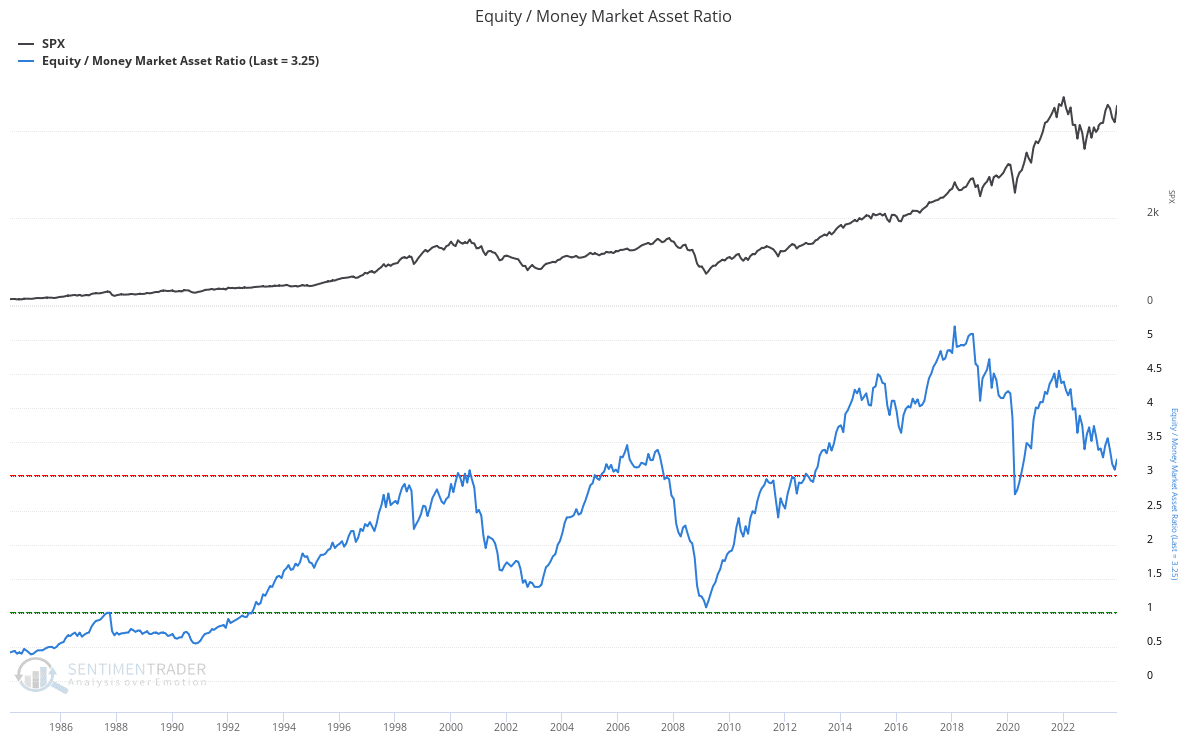

As noted, investors are again becoming exuberant over stock ownership. Such is vital to creating multiple expansions and fueling bull market advances. High valuations, bullish sentiment, and leverage are meaningless if the underlying equities are not owned. As discussed in “Household Equity Allocations,” the current levels of household equity ownership have reverted to near-record levels. Historically, such exuberance has been the mark of more important market cycle peaks.

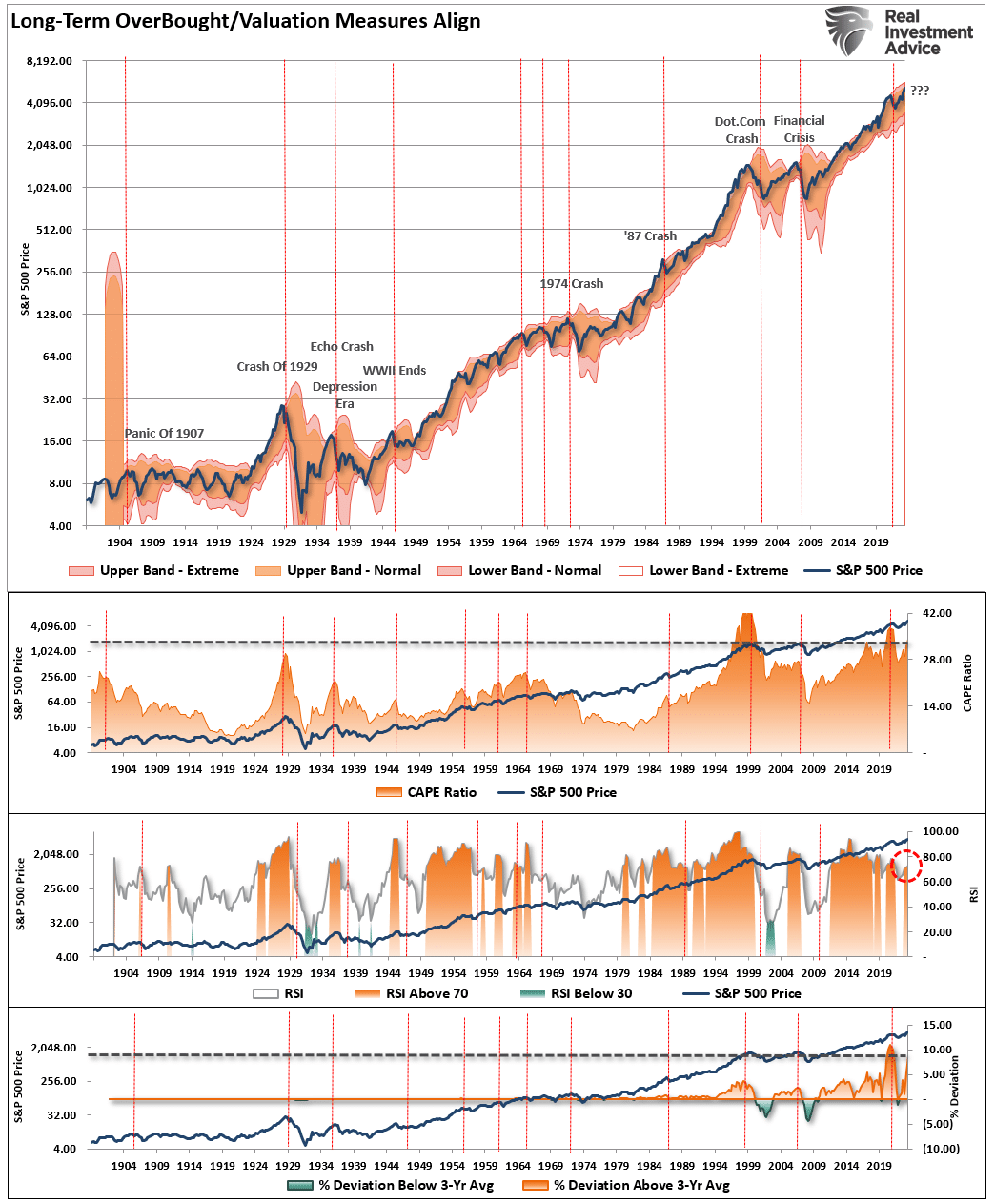

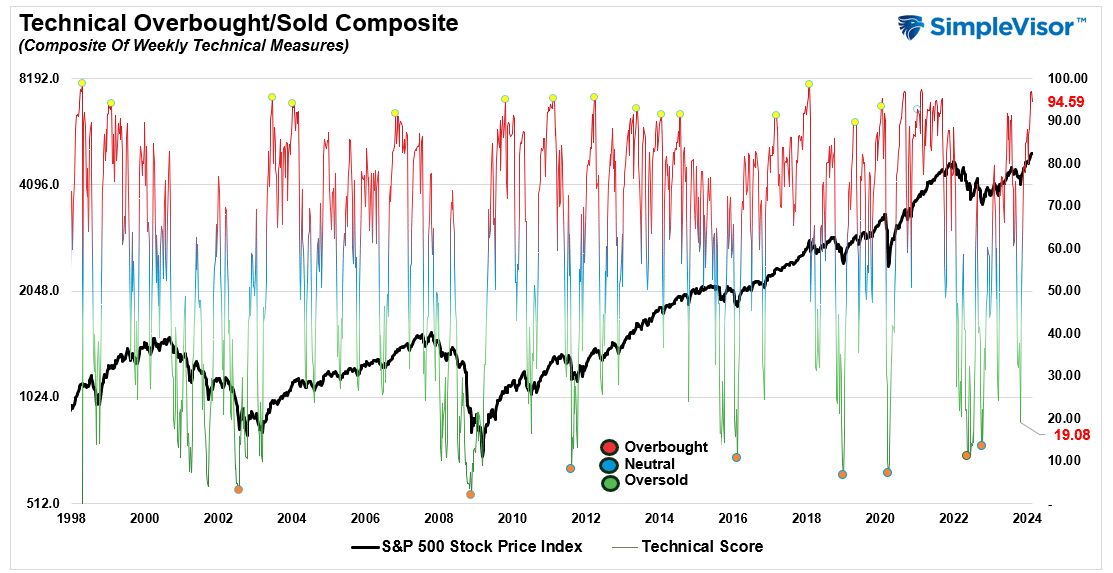

While household equity ownership is critical to expanding the bull market, the technical measures provide an understanding of when excesses are reached. One measure we focus on is the deviation of price from long-term means. The reason is that markets are bound to long-term means over time. For a “mean” or “average” to exist, prices must trade above and below that price over time. Therefore, we can determine when deviations are approaching more extreme levels by viewing past deviations. Currently, the deviation of the market from its underlying 2-year average is one of the largest in history. Notably, there have certainly been more significant deviations in the past, suggesting the current deviation from the mean can grow further. However, such deviations have crucially been a precursor to an eventual mean-reverting event.

The following analysis uses quarter data and evaluates the market using valuation and technical measures. From a long-term perspective, the market is trading at more extreme levels. The quarterly Relative Strength (RSI) measure is above 70, the deviation is close to a historical record, and the market trades nearly 3 standard deviations above its quarterly mean. As noted, while these valuation and technical measures can undoubtedly become more extreme, the ingredients for an eventual mean reverting event are present.

Of course, the inherent problem with long-term analysis is that while valuations and long-term technical measures are more extreme, they can remain that way for much longer than logic suggests. However, we can construct a valuation and technical measures model using the data above. As shown, the model triggered a “risk off” warning in early 2022 when high valuations collided with an extreme deviation of the market above the 24-month moving average. That signal was reversed in January 2023, as the market began to recover. While a new signal has not yet been triggered, the ingredients of valuations and deviations are present.

The Ingredients Are Missing A Catalyst

The problem with long-term technical measures and valuations is that they move slowly. Therefore, the general assumption is that if high valuations do not lead to an immediate market correction, the measure is flawed.

In the short term, “valuations” have little relevance to what positions you should buy or sell. It is only momentum, the direction of the price, that matters. Managing money, either “professionally” or “individually,” is a complicated process over the long term. It seems exceedingly easy in the short term, particularly amid a speculative mania. However, as with every bull market, a strongly advancing market forgives investors’ many investing mistakes. The ensuing bear market reveals them in the most brutal and unforgiving of outcomes.

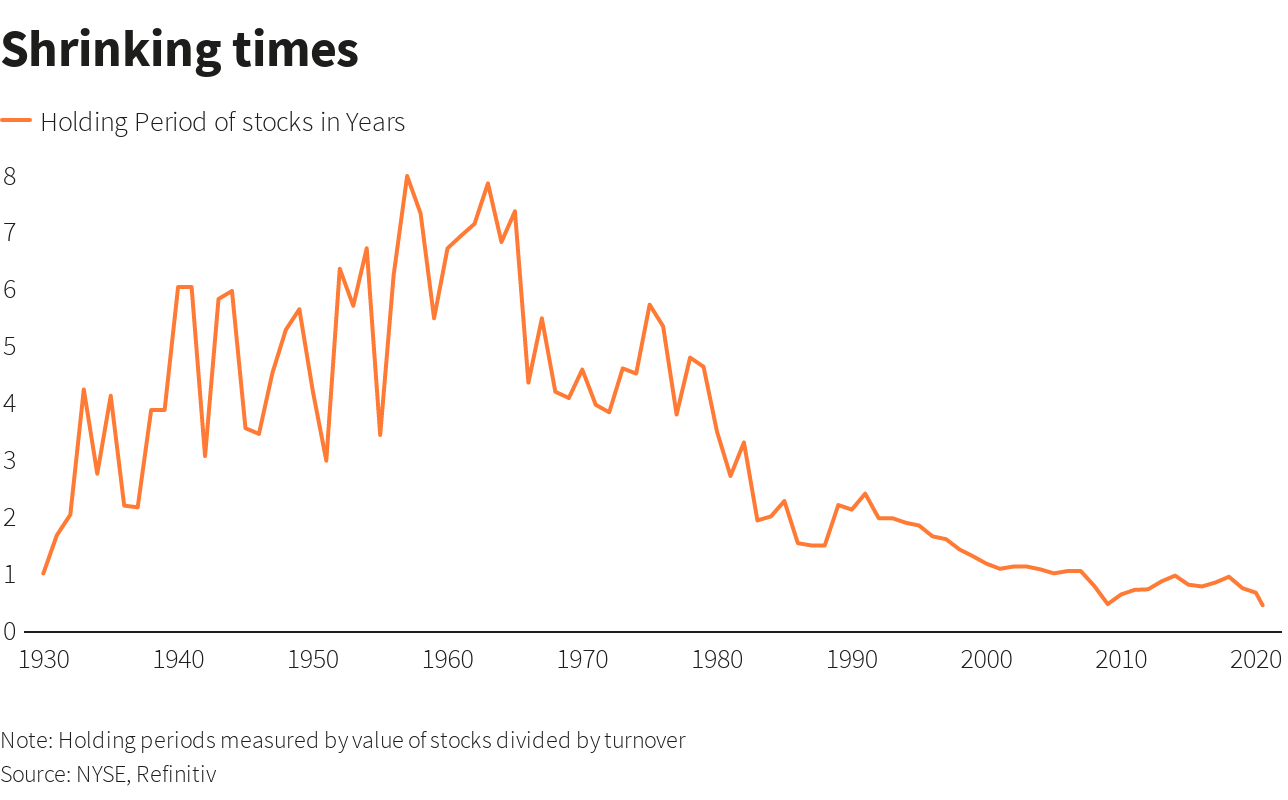

There is a clear advantage to providing risk managementto portfolios over time. The problem is that most individuals cannot manage their own money because of “short-termism.” As shown by shrinking holding periods.

While “short-termism” currently dominates the investor mindset, the ingredients for a reversion exist. However, that does not mean one will happen tomorrow, next month, or even this year.

Think about it this way. If I gave you a bunch of ingredients such as nitrogen, glycerol, sand, and shell, you would probably stick them in the garbage and think nothing of it. They are innocuous ingredients and pose little real danger by themselves. However, you make dynamite using a process to combine and bind them. However, even dynamite is safe as long as it is stored properly. Only when dynamite comes into contact with the appropriate catalyst does it become a problem.

“Mean reverting events,” bear markets, and financial crises result from a combined set of ingredients to which a catalyst ignites. Looking back through history, we find similar elements every time.

Like dynamite, the individual ingredients are relatively harmless but dangerous when combined.

Importantly, this particular formula remains supportive of higher asset prices in the short term. Of course, the more prices rise, the more optimistic investors become.

While the combination of ingredients is dangerous, they remain “inert” until exposed to the right catalyst.

What causes the next “liquidation cycle” is currently unknown. It is always an unexpected, exogenous event that triggers a “rush for the exits.”

Many believe that “bear markets” are now a relic of the past, given the massive support provided by Central Banks. Maybe that is the case. However, remembering that such beliefs were always present before more severe mean-reverting events is worth remembering.

To quote Irving Fisher in 1929, “Stocks are at a permanently high plateau.”

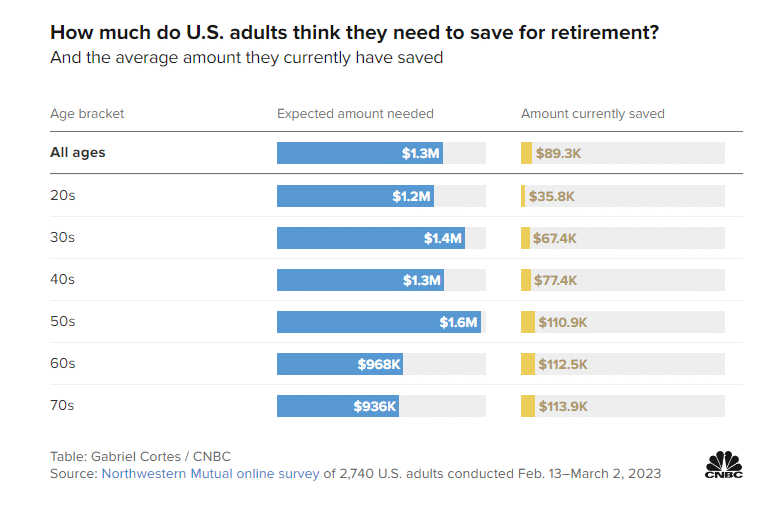

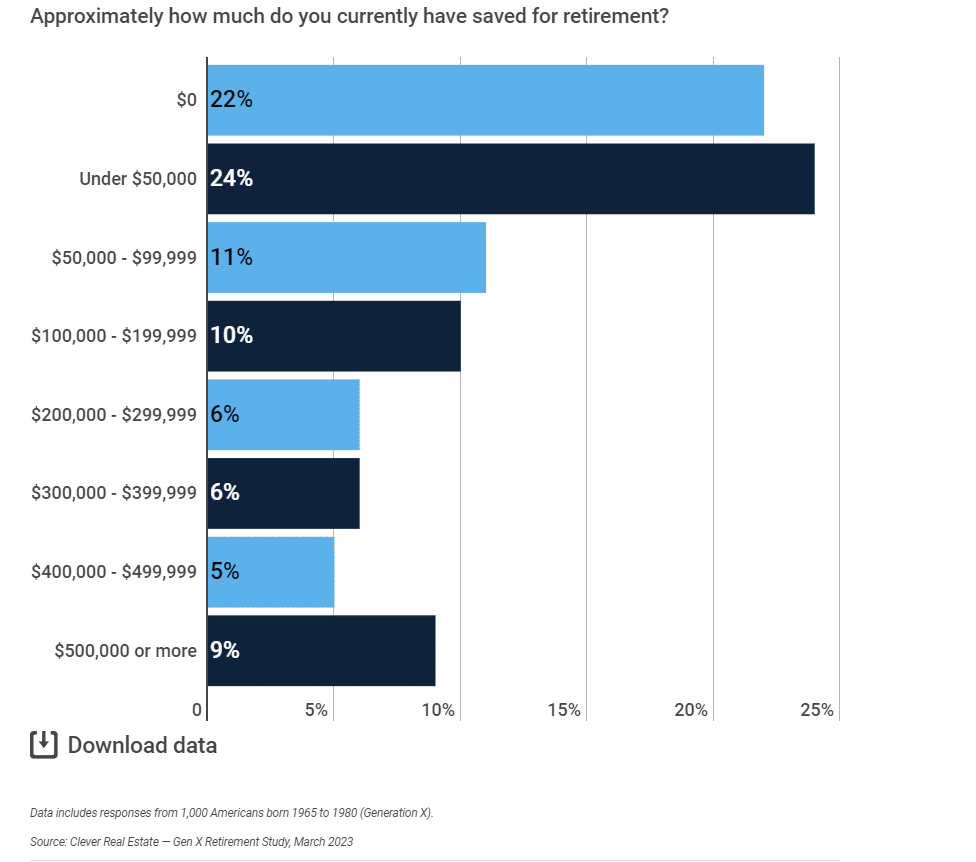

Retirement Crisis Faces Government And Corporate Pensions

It is long past the time that we face the fact that “Social Security” is facing a retirement crisis. In June 2022, we touched on this issue, discussing the stark realities confronting Social Security.

“The program’s payouts have exceeded revenue since 2010, but the recent past is nowhere near as grim as the future. According to the latest annual report by Social Security’s trustees, the gap between promised benefits and future payroll tax revenue has reached a staggering $59.8 trillion. That gap is $6.8 trillion larger than it was just one year earlier. The biggest driver of that move wasn’t Covid-19, but rather a lowering of expected fertility over the coming decades.” – Stark Realities

Note the last sentence.

When President Roosevelt first enacted social security in 1935, the intention was to serve as a safety net for older adults. However, at that time, life expectancy was roughly 60 years. Therefore, the expectation was that participants would not be drawing on social security for very long on an actuarial basis. Furthermore, according to the Social Security Administration, roughly 42 workers contributed to the funding pool for each welfare recipient in 1940.

Of course, given that politicians like to use government coffers to buy votes, additional amendments were added to Social Security to expand participation in the program. This included adding domestic labor in 1950 and widows and orphans in 1956. They lowered the retirement age to 62 in 1961 and increased benefits in 1972. Then politicians added more beneficiaries, from disabled people to immigrants, farmers, railroad workers, firefighters, ministers, federal, state, and local government employees, etc.

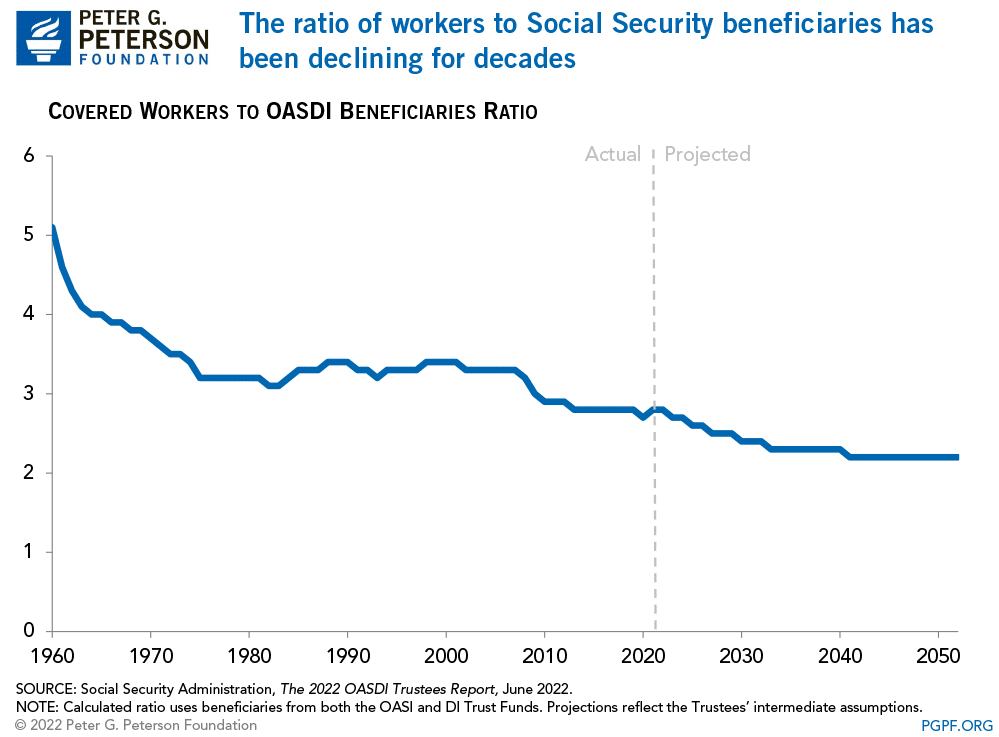

While politicians and voters continued adding more beneficiaries to the welfare program, workers steadily declined. Today, there are barely 2-workers for each beneficiary. As noted by the Peter G. Peterson Foundation:

“Social Security has been a cornerstone of economic security for almost 90 years, but the program is on unsound footing. Social Security’s combined trust funds are projected to be depleted by 2035 — just 13 years from now. A major contributor to the unsustainability of the current Social Security program is that the number of workers contributing to the program is growing more slowly than the number of beneficiaries receiving monthly payments. In 1960, there were 5.1 workers per beneficiary; that ratio has dropped to 2.8 today.”

As we will discuss, the collision of demographics and math is coming to the welfare system.

A Massive Shortfall

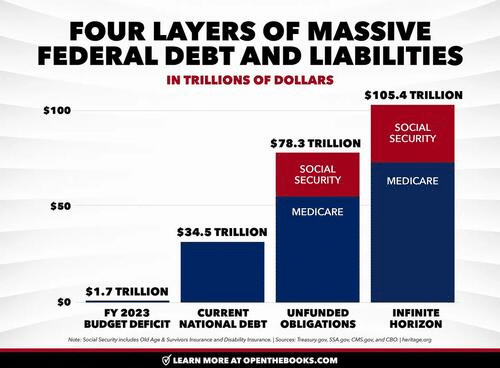

The new Financial Report of the United States Government (February 2024) estimates that the financial position of Social Security and Medicare are underfunded by roughly $175 Trillion. Treasury Secretary Janet Yellin signed the report, but the chart below details the problem.

The obvious problem is that the welfare system’s liabilities massively outweigh taxpayers’ ability to fund it. To put this into context, as of Q4-2023, the GDP of the United States was just $22.6 trillion. In that same period, total federal revenues were roughly $4.8 trillion. In other words, if we applied 100% of all federal revenues to Social Security and Medicare, it would take 36.5 years to fill the gap. Of course, that is assuming that nothing changes.

However, therein lies the actuarial problem.

All pension plans, whether corporate or governmental, rely on certain assumptions to plan for future obligations. Corporate pensions, for example, rely on certain portfolio return assumptions to fund planned employee retirements. Most pension plans assume that portfolios will return 7% a year. However, a vast difference exists between “average returns” and “compound returns” as shown.

Social Security, Medicare, and corporate pension plans face a retirement crisis. A shortfall arises if contributions and returns don’t meet expectations or demand increases on the plans.

For example, given real-world return assumptions, pension funds SHOULD lower their return estimates to roughly 3-4% to potentially meet future obligations and maintain some solvency. However, they can’t make such reforms because “plan participants” won’t let them. Why? Because:

It would require a 30-40% increase in contributionsby plan participants they can not afford.

Given many plan participants will retire LONG before 2060, there isn’t enough time to solve the issues and;

Any bear market will further impede the pension plan’s ability to meet future obligations without cutting future benefits.

Social Security and Medicare face the same intractable problem. While there is ample warning from the Trustees that there are funding shortfalls to the plans, politicians refuse to make the needed changes and instead keep adding more participants to the rolls.

However, all current actuarial forecasts depend on a steady and predictable pace of age and retirement. But that is not what is currently happening.

A Retirement Crisis In The Making

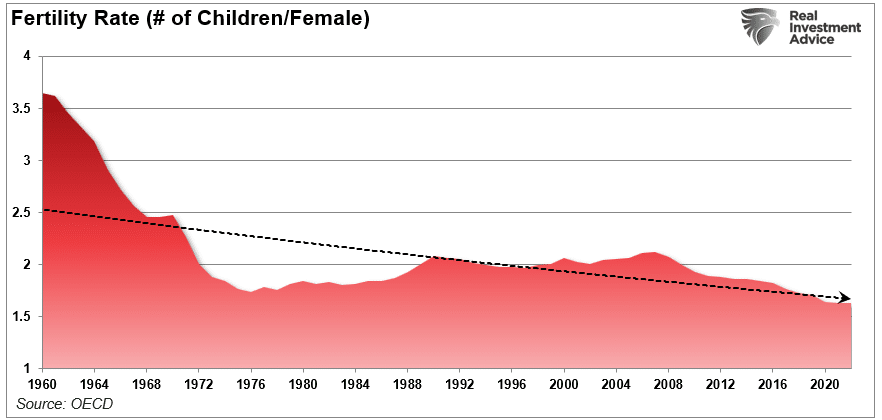

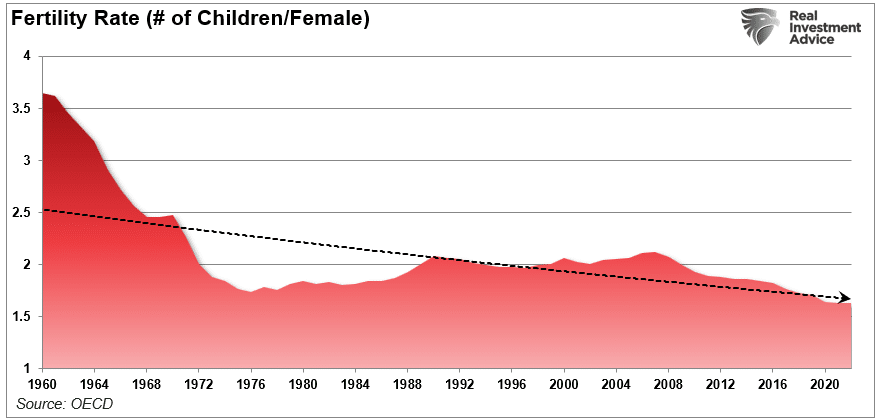

The single biggest threat that faces all pension plans is demographics. That single issue can not be fixed as it takes roughly 25 years to grow a taxpayer. So, even if we passed laws today that required all women of birthing age to have a minimum of 4 children over the next 5 years, we would not see any impact for nearly 30 years. However, the problem is running in reverse as fertility rates continue to decline.

Interestingly, researchers from the Center For Sexual Health at Indiana University put forth some hypotheses behind the decline in sexual activity:

Less alcohol consumption (not spending time in bars/restaurants)

More time on social media and playing video games

Lower wages lead to lower rates of romantic relationships

Non-heterosexual identities

The apparent problem with less sex and non-heterosexual identities is fewer births.

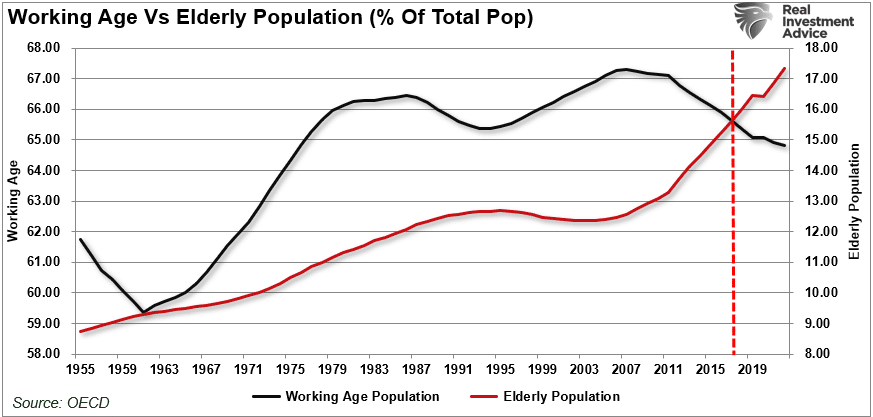

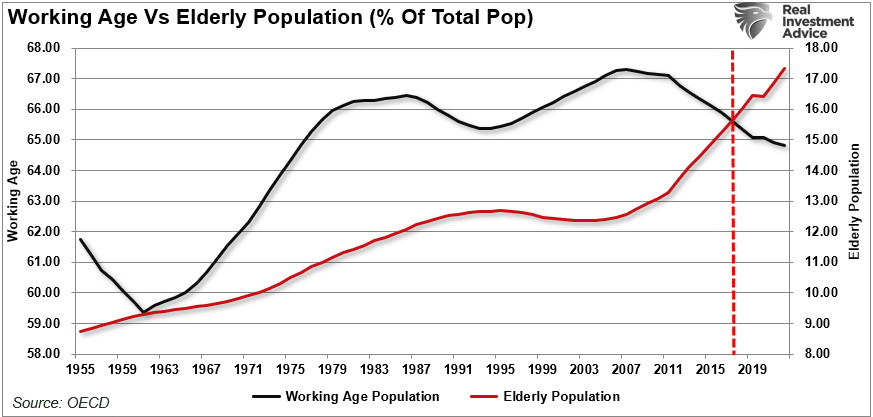

No matter how you calculate the numbers, the problem remains the same. Too many obligations and a demographic crisis. As noted by official OECD estimates, the aging of the population relative to the working-age population has already crossed the “point of no return.”

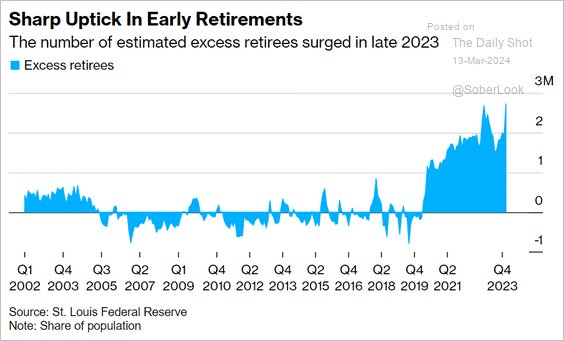

To compound that situation, there has been a surge in retirees significantly higher than estimates. As noted above, actuarial tables depend on an expected rate of retirees drawing from the system. If that number exceeds those estimates, a funding shortfall increases to provide the required benefits.

The decline in economic prosperity discussed previously is caused by excessive debt and declining income growth due to productivity increases. Furthermore, the shift from manufacturing to a service-based society will continue to lead to reduced taxable incomes.

This employment problem is critical.

By 2025, each married couple will pay Social Security retirement benefits for one retiree and their own family’s expenses. Therefore, taxes must rise, and other government services must be cut.

Back in 1966, each employee shouldered $555 of social benefits. Today, each employee has to support more than $18,000 in benefits. The trend is unsustainable unless wages or employment increases dramatically, and based on current trends, such seems unlikely.

The entire social support framework faces an inevitable conclusion where wishful thinking will not change that outcome. The question is whether elected leaders will make needed changes now or later when they are forced upon us.

For now, we continue to “Whistle past the graveyard” of a retirement crisis.

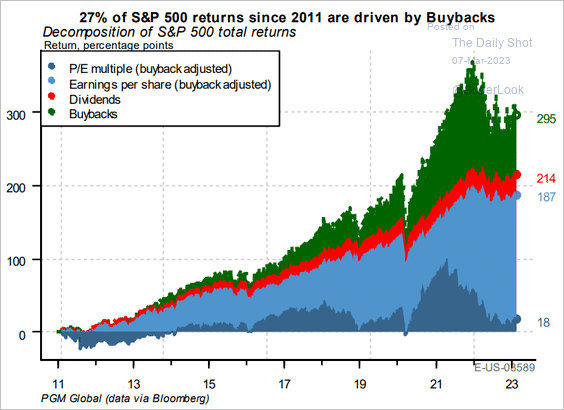

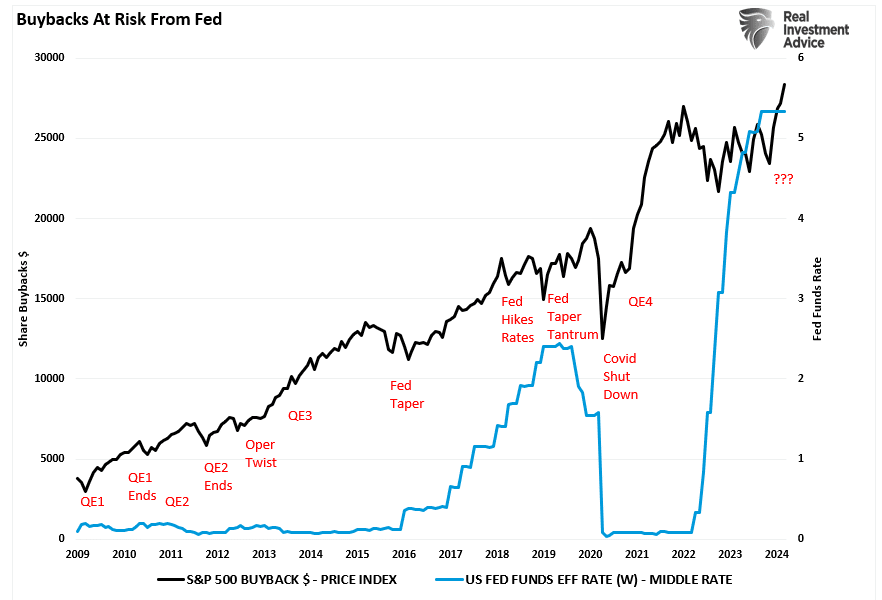

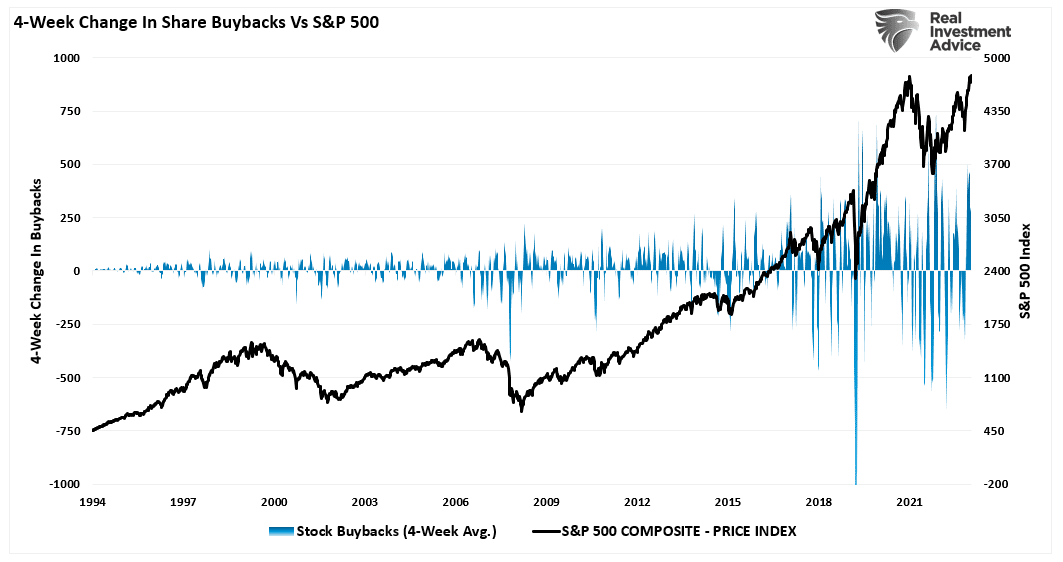

Blackout Of Buybacks Threatens Bullish Run

With the last half of March upon us, the blackout of stock buybacks threatens to reduce one of the liquidity sources supporting the bullish run this year. If you don’t understand the importance of corporate share buybacks and the blackout periods, here is a snippet of a 2023 article I previously wrote.

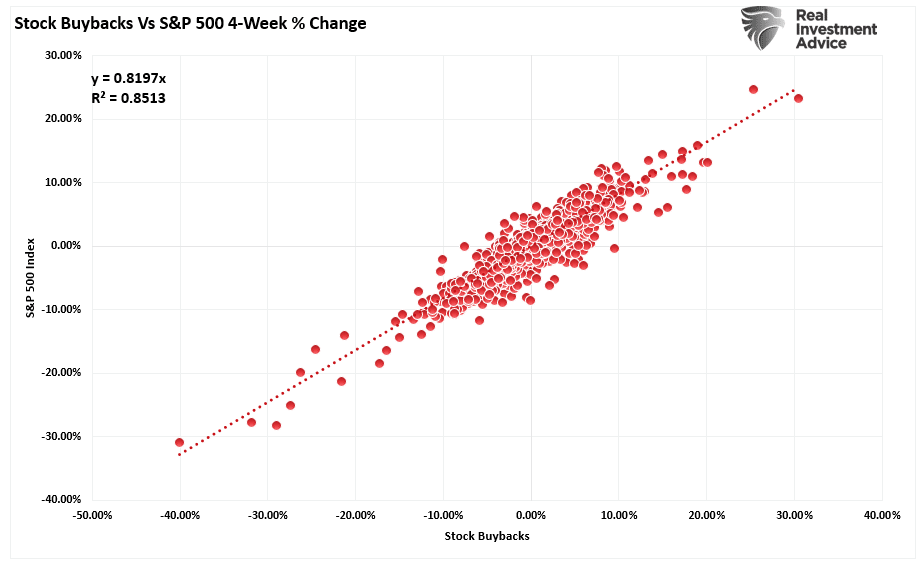

“The chart below via Pavilion Global Markets shows the impact stock buybacks have had on the market over the last decade. The decomposition of returns for the S&P 500 breaks down as follows:“

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting massive liquidity into the financial markets and corporations buying back their shares, there have been no other real buyers in the market.

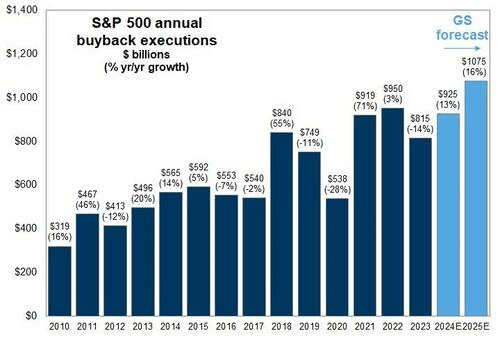

Given the increasing amount of corporate share buybacks, with 2024 expected to set a record, the importance of that activity has been a critical support for asset prices. As we noted in October 2023, near the bottom of the summer correction:

“Three primary drivers will likely drive markets from the middle of October through year-end. The first is earnings season, which kicks off in two weeks, negative short-term sentiment, and the corporate share buyback window reopens from blackout in November.”

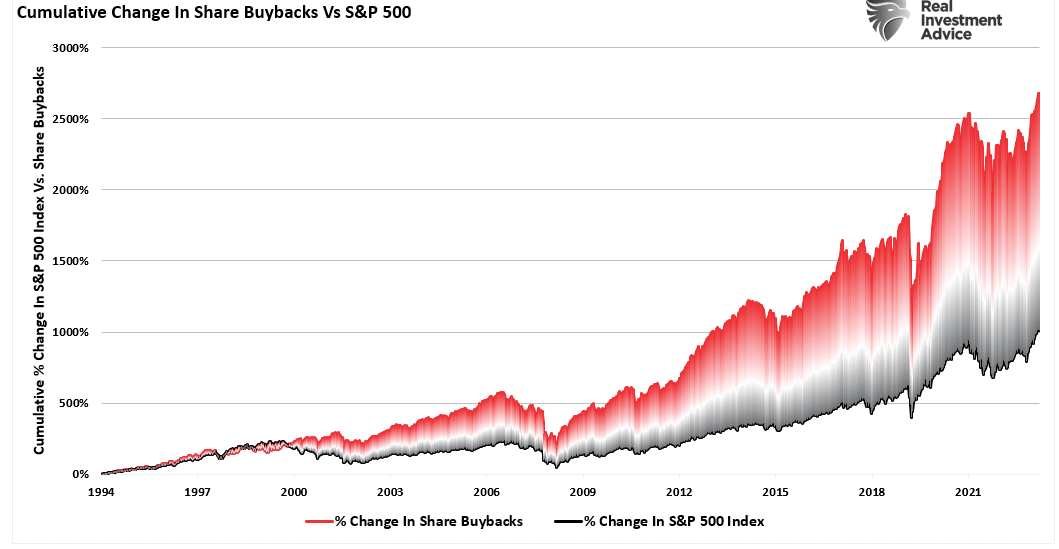

Notably, since 2009, and accelerating starting in 2012, the percentage change in buybacks has far outstripped the increase in asset prices.

As we will discuss, it is more than just a casual correlation, and the upcoming blackout window may be more critical to the rally than many think.

A High Correlation

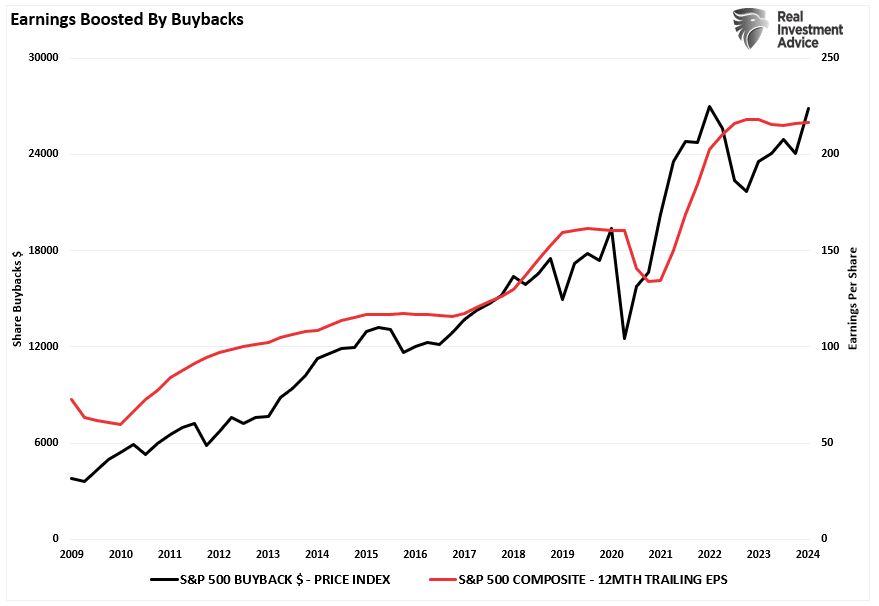

Unsurprisingly, the market rally that began in November correlated with a strong surge in corporate share repurchases. Interestingly, while the media touts the strong earnings growth shown in the recent reporting period, such would not have been the case without the surge in buybacks.

The result is not surprising given that the majority of earnings growth for the quarter came from the companies that are the most aggressive with share repurchases. However, given current valuation levels, it should make one question precisely what you are paying for.

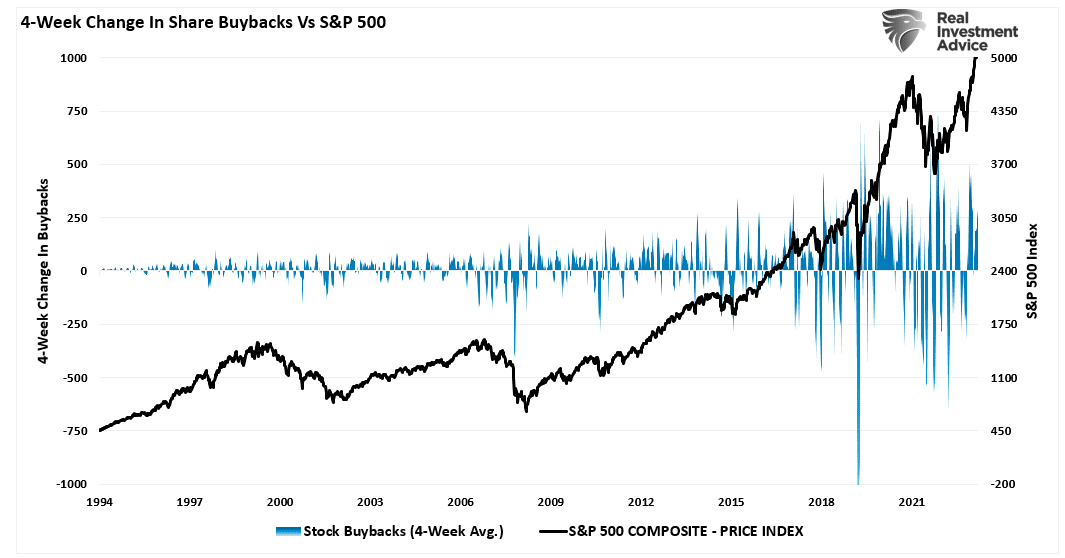

Nonetheless, the buyback surge has supported the market surge since the October 2023 lows. We saw the same at the bottom of the market in October 2022. The chart shows the 4-week percentage change in share buybacks versus the S&P 500.

The end of October tends to be the inflection point for the market, particularly over the last few years, because that is when the blackout period for share buybacks fully ends. While many argue that buybacks have little to do with market movements, a high correlation exists between the 4-week percentage change in buybacks versus the stock market. More importantly, since the act of share repurchases provides a buyer for those shares, the .85 correlation between the two suggests this is more than just a casual relationship.

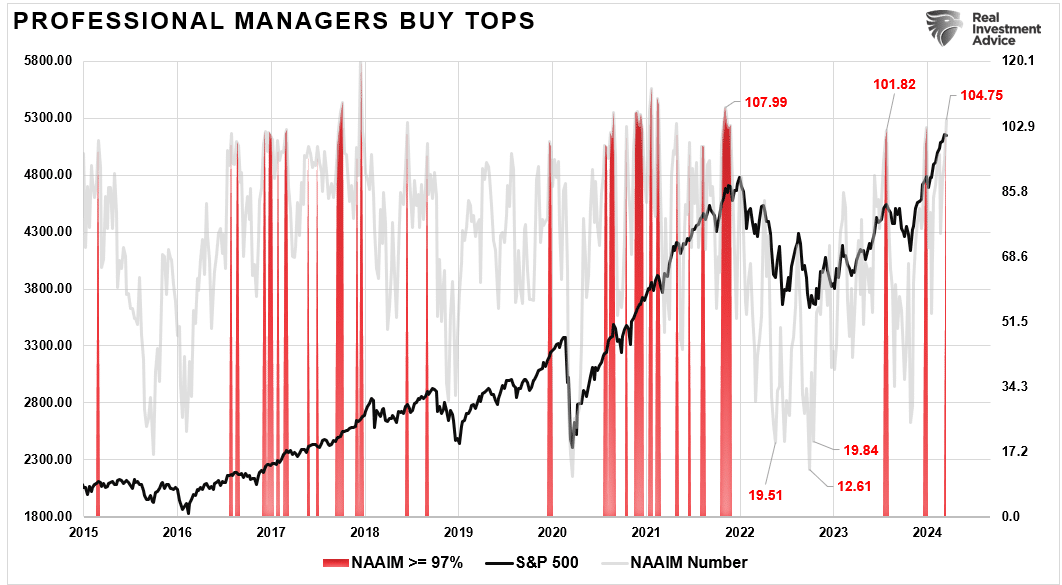

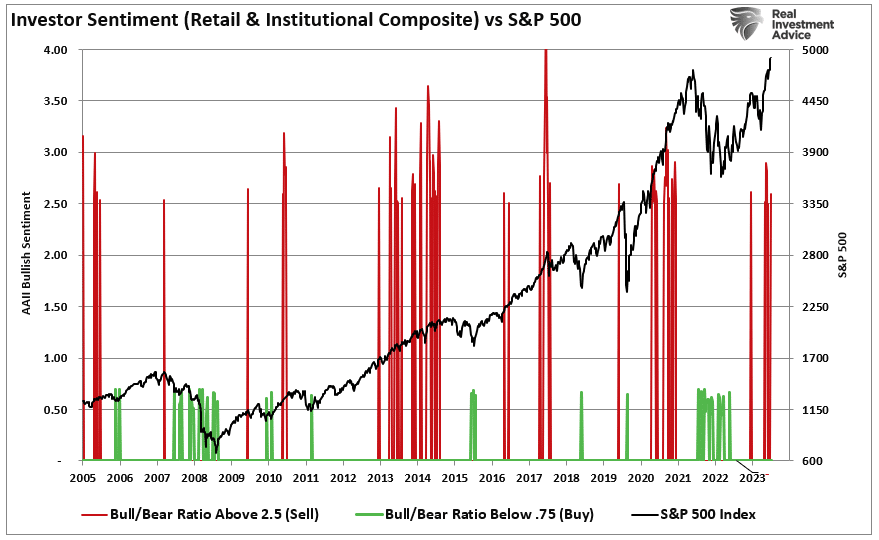

Investors Are Really Bullish

Currently, investors are very exuberant about the current investing environment. As discussed in “Market Top or Bubble?”, little seems to deter investor enthusiasm.

Investor sentiment is once again very bullish. Historically, when retail investor sentiment is exceedingly bullish combined with low volatility, such has generally corresponded to short-term market peaks.

At the same time, professional managers are also very bullish and are leveraging portfolios to chase returns. When professional investor allocations exceed 97%, such has historically been close to short-term market peaks.

The risk to these more optimistic investors is that with the blackout period beginning, corporate demand, the largest buyers of equities, will drop by 35%. Therefore, given the correlation between buybacks and the market, a reversal of that corporate demand could lead to a market decline. Any decline will likely lead to a reversal of positioning by investors, further exacerbating that correction process.

While there is no guarantee of anything in the markets, it is likely a short-term risk worth paying attention to.

The Fed Will Support Buybacks

While the blackout of share buybacks may lead to a short-term market correction, the Federal Reserve may provide additional support over the long term.

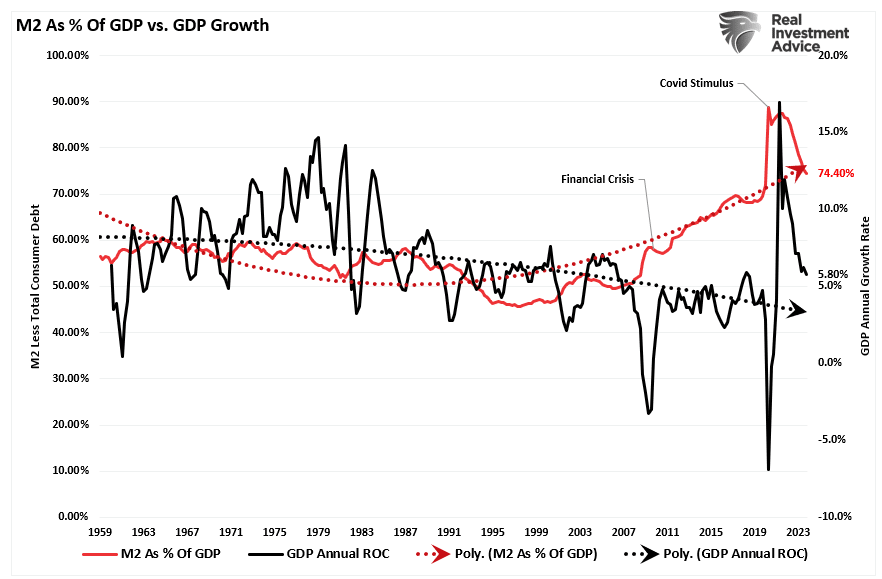

The Federal Reserve has been transparent and likely done with hiking interest rates for this cycle. Given the massive surge in the Fed funds rate, the economy has withstood that impact quite well. Of course, the reason was the enormous surge in fiscal support through deficit spending and a massive increase in the M2 money supply as a percentage of GDP.

However, if the Federal Reserve lowers interest rates, it will reduce corporate borrowing costs, which has historically been a boon for share buybacks. Such is particularly the case for large corporations like Apple (AAPL), which can borrow several billion dollars at low rates and buy back outstanding shares. As shown, share buybacks rose sharply following the “Financial Crisis” but slowed during periods of higher rates. Corporations are now “front-running” the Federal Reserve in anticipation of increased monetary accommodation.

With corporate buybacks on track to set a new record this year, exceeding $1 Trillion, corporations will need lower rates to finance the purchases.

Conclusion

As we have discussed for the last month, the market is exceptionally bullish, extended, and deviated from long-term means. With the beginning of the “buyback blackout,” removing an essential buyer of equities is a risk worth watching.

Even if you are incredibly bullish on the markets, healthy bull markets must occasionally be corrected. Without such corrections, excesses are built, leading to more destructive outcomes.

What causes such a correction is always unknown. While the removal of buybacks temporarily may lead to a price reversal, those buybacks will return soon enough. And with $1 trillion in anticipated purchases, that is a lot of support for asset prices this year.

Does this mean the market will never face another “bear market?”

“The math isn’t complicated: When the share count goes down, your interest in our many businesses increases. Every small bit helps if repurchases are made at value-accretive prices.

Just as surely, when a company overpays for repurchases, the continuing shareholders lose. At such times, gains flow only to the selling shareholders and to the friendly, but expensive, investment banker who recommended the foolish purchases.“

Eventually, the detachment of the financial markets from underlying economic realities will be reverted.

However, that is not likely a problem we will face between now and year-end.

Household Equity Allocations Suggests Caution

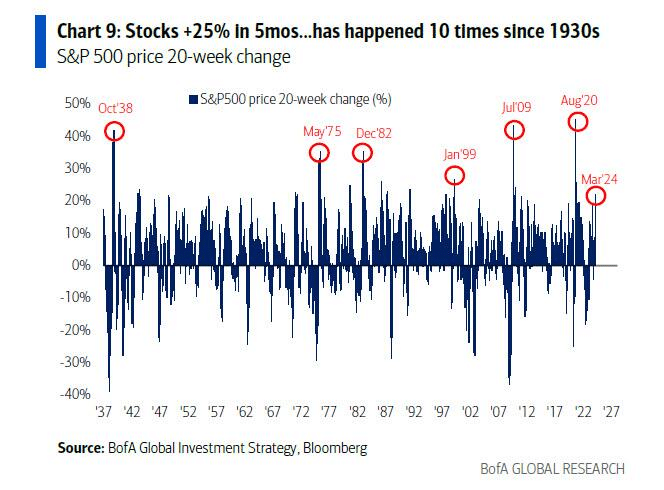

Household equity allocations are again sharply rising, as the “Fear Of Missing Out” or “F.O.M.O.” fuels a near panic mentality to chase markets higher. As Michael Hartnett from Bank of America recently noted:

“Stocks are up a ferocious +25% in 5 months, which has happened just 10 times since the 1930s. Normally, such surges occur from recession lows (1938, 1975, 1982, 2009, 2020), but, of course, we did not have a recession in 2023, according to the Biden administration. These surges also occur at the start of bubbles (Jan’99).”

As discussed in the recent Bull Bear Report, we can only identify bubbles in hindsight. Such is the problem with trying to “time” a market top, as they can last much longer than logic would predict. George Soros explained this well in his theory of reflexivity.

“Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time. Sometimes it’s quite insignificant, at other times it is quite pronounced. When there is a significant divergence between market prices and the underlying reality, the markets are far from equilibrium conditions.“

Every bubble has two components:

An underlying trend that prevails in reality and;

A misconception relating to that trend.

“When positive feedback develops between the trend and the misconception, a boom-bust process gets set into motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception get reinforced. Eventually, market expectations become so far removed from reality that people get forced to recognize that a misconception is involved. A twilight period ensues during which doubts grow, and more people lose faith, but the prevailing trend gets sustained by inertia.” – George Soros

In simplistic terms, Soros says that once the bubble inflates, it will remain inflated until some unexpected, exogenous event causes a reversal in the underlying psychology. That reversal then reverses psychology from “exuberance” to “fear.”

What will cause that reversion in psychology? No one knows.

However, the important lesson is that market tops and bubbles are a function of “psychology.” The manifestation of that “psychology” manifests itself in asset prices and valuations that exceed economic growth rates.

Once again, investors are piling into equities and “writing checks that the economy can’t cash.”

An Economic Underpinning

To understand the problem, we must first realize from which capital gains are derived.

Capital gains from markets are primarily a function of market capitalization, nominal economic growth, plus dividend yield. Using John Hussman’s formula, we can mathematically calculate returns over the next 10-year period as follows:

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1

Therefore, IF we assume that GDP could maintain 2% annualized growth in the future, with no recessions ever, AND IF current market cap/GDP stays flat at 2.0, AND IF the dividend yield remains at roughly 2%, we get forward returns of:

(1.02)*(1.2/1.5)^(1/10)-1+.02 = -(1.08%)

But there are a “whole lotta ifs” in that assumption. Most importantly, we must also assume the Fed can get inflation to its 2% target, reduce current interest rates, and, as stated, avoid a recession over the next decade.

Yet, despite these essential fundamental factors, retail investors again throw caution to the wind. As shown, the current levels of household equity ownership have reverted to near-record levels. Historically, such exuberance has been the mark of more important market cycle peaks.

If economic growth is reversed, the valuation reduction will be quite detrimental. Again, such has been the case at previous peaks where expectations exceed economic realities.

Bob Farrell once quipped investors tend to buy the most at the top and the least at the bottom. Such is simply the embodiment of investor behavior over time. Our colleague, Jim Colquitt, previously made an important observation.

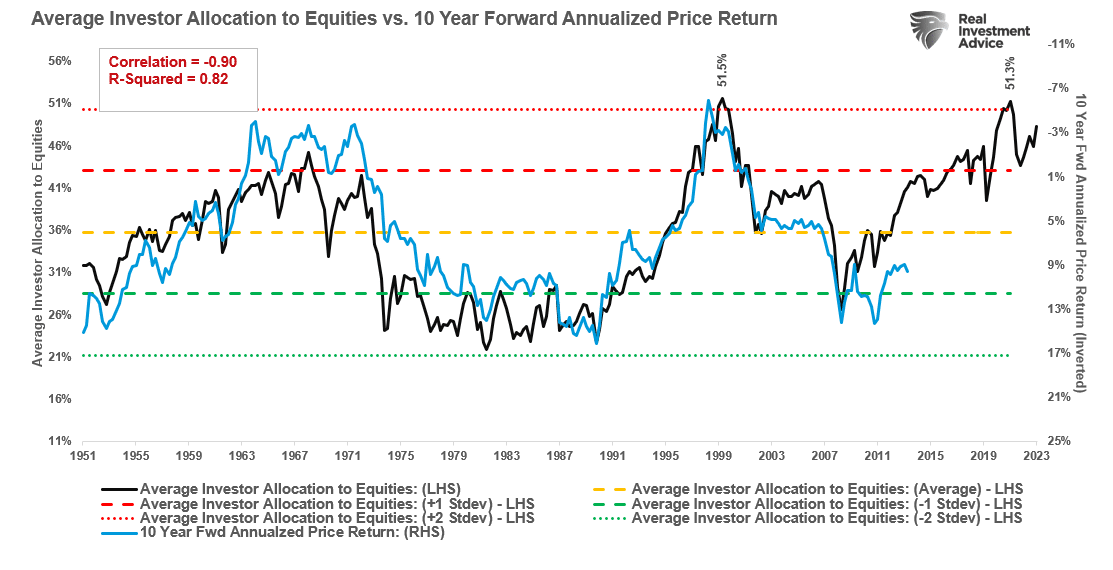

“The graph below compares the average investor allocation to equities to S&P 500 future 10-year returns. As we see, the data is very well correlated, lending credence to Bob Farrell’s Rule #5. Note the correlation statistics at the top left of the graph.”

The 10-year forward returns are inverted on the right scale. This suggests that future returns will revert toward zero over the next decade from current levels of household equity allocations by investors.

The reason is that when investor sentiment is extremely bullish or bearish, such is the point where reversals have occurred. As Sam Stovall, the investment strategist for Standard & Poor’s, once stated:

“If everybody’s optimistic, who is left to buy? If everybody’s pessimistic, who’s left to sell?”

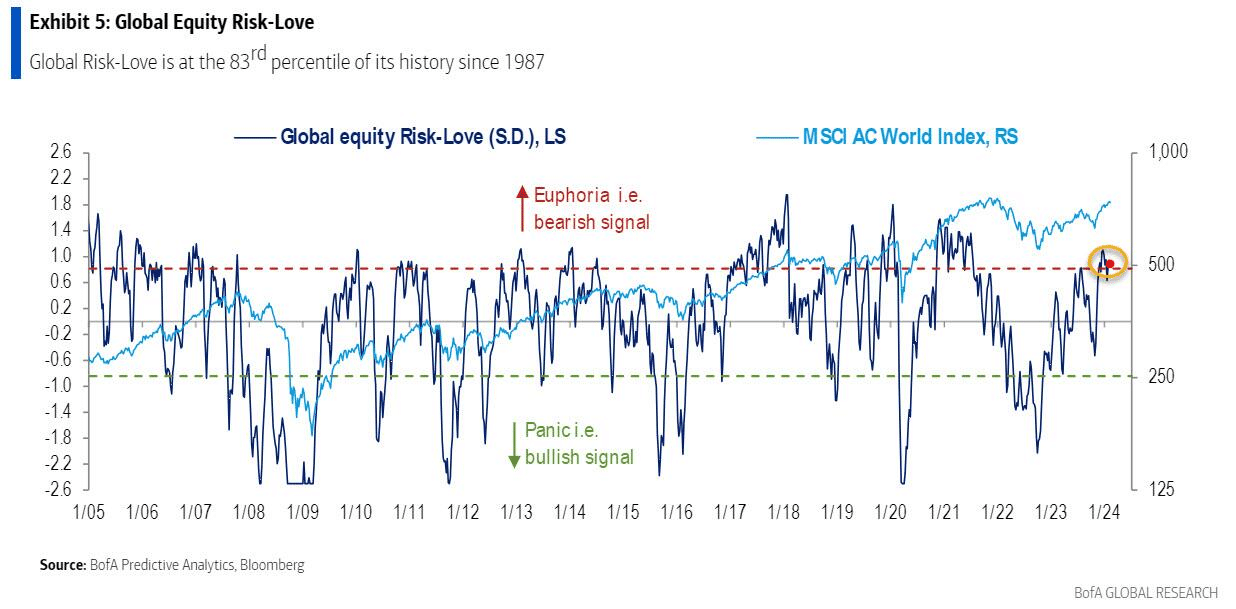

Everyone is very optimistic about the market. Bank of America, one of the world’s largest asset custodians, monitors risk positioning across equities. Currently, “risk love” is in the 83rd percentile and at levels that have generally preceded short-term corrective actions.

The only question is what eventually reverses that psychology.

A Disappointment Of Hopes

In January 2022, Jeremy Grantham made headlines with his market outlook titled “Let The Wild Rumpus Begin.” The crux of the article is summed up in the following paragraph.

“All 2-sigma equity bubbles in developed countries have broken back to trend. But before they did, a handful went on to become superbubbles of 3-sigma or greater: in the U.S. in 1929 and 2000 and in Japan in 1989. There were also superbubbles in housing in the U.S. in 2006 and Japan in 1989. All five of these superbubbles corrected all the way back to trend with much greater and longer pain than average.

Today in the U.S. we are in the fourth superbubble of the last hundred years.”

While the market corrected in 2022, the reversion needed to reverse the excess deviation from the long-term growth trends was not achieved. Therefore, unless the Federal Reverse is committed to a never-ending program of zero interest rates and quantitative easing, the eventual reversion of returns to their long-term means remains inevitable.

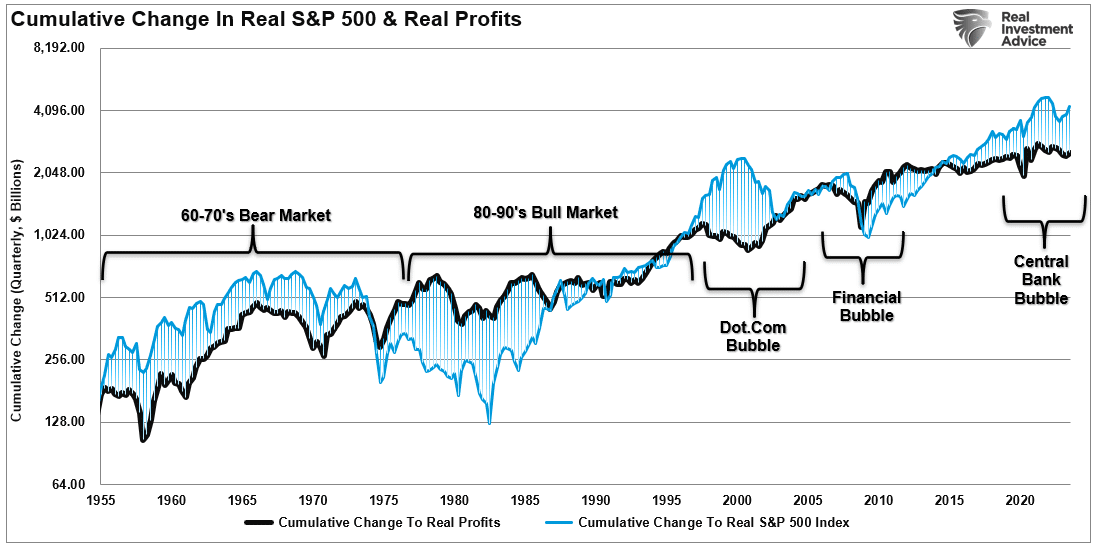

Such will result in profit margins and earnings returning to levels that align with actual economic activity. As Jeremy Grantham once noted:

“Profit margins are probably the most mean-reverting series in finance. And if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.” – Jeremy Grantham

Historically, real profits have always eventually reverted to underlying economic realities.

Many things can go wrong in the months and quarters ahead. Such is particularly the case at a time when deficit spending is running amok, and economic growth is slowing.

While investors cling to the “hope” that the Fed has everything under control, there is a reasonable chance they don’t.

The reality is that the next decade could be a disappointment to overly optimistic expectations.

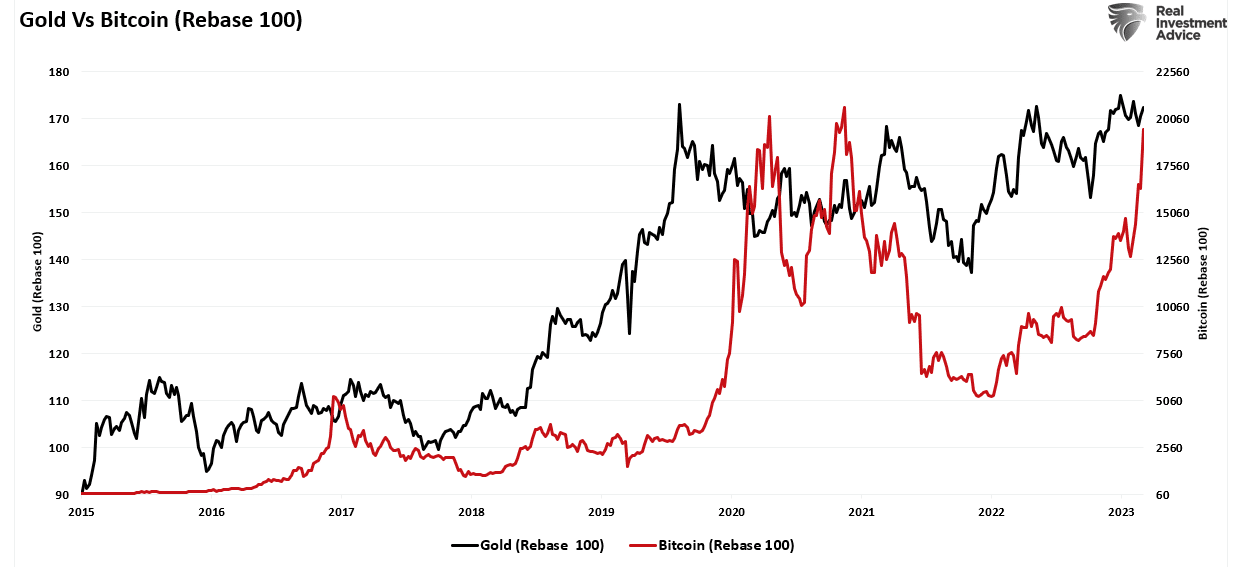

Digital Currency And Gold As Speculative Warnings

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite. Such isn’t surprising given the evolution of the market into a “casino” following the pandemic, where retail traders have increased their speculative appetites.

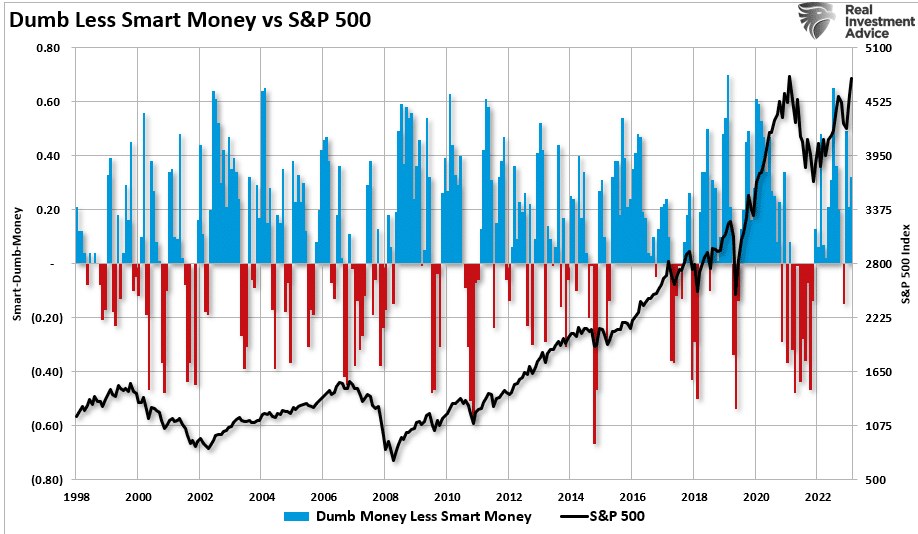

“Such is unsurprising, given that retail investors often fall victim to the psychological behavior of the “fear of missing out.” The chart below shows the “dumb money index” versus the S&P 500. Once again, retail investors are very long equities relative to the institutional players ascribed to being the “smart money.””

“The difference between “smart” and “dumb money” investors shows that, more often than not, the “dumb money” invests near market tops and sells near market bottoms.”

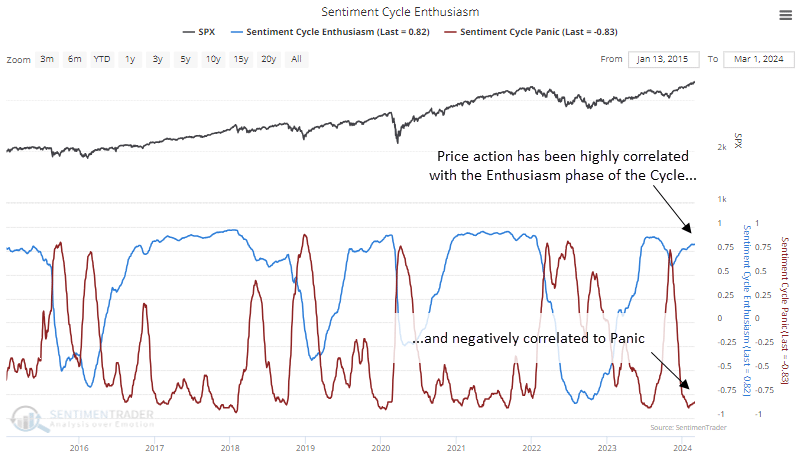

That enthusiasm has increased sharply since last November as stocks surged in hopes that the Federal Reserve would cut interest rates. As noted by Sentiment Trader:

“Over the past 18 weeks, the straight-up rally has moved us to an interesting juncture in the Sentiment Cycle. For the past few weeks, the S&P 500 has demonstrated a high positive correlation to the ‘Enthusiasm’ part of the cycle and a highly negative correlation to the ‘Panic’ phase.”

That frenzy to chase the markets, driven by the psychological bias of the “fear of missing out,” has permeated the entirety of the market. As noted in “This Is Nuts:”

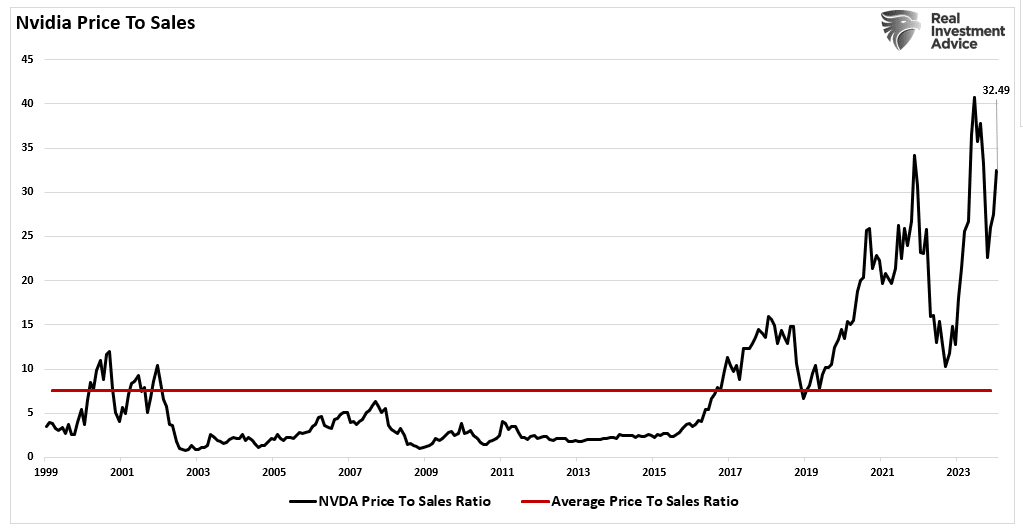

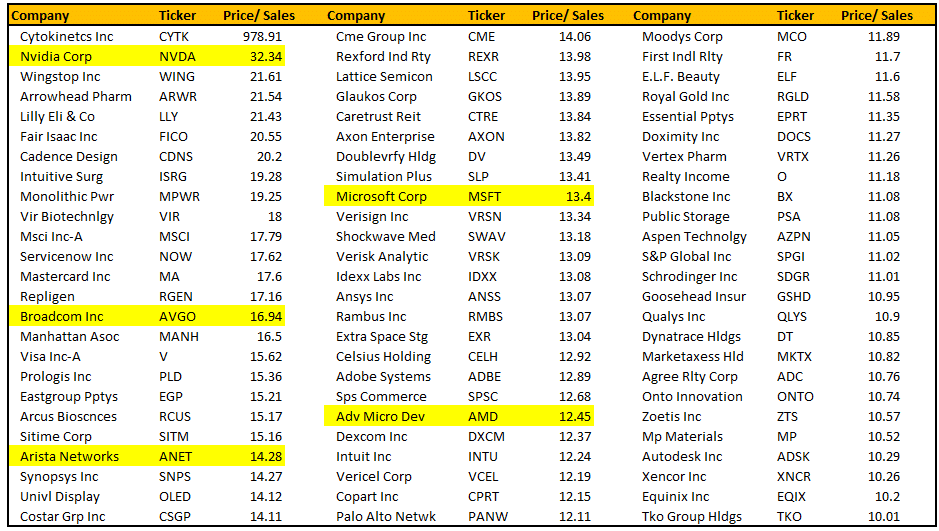

“Since then, the entire market has surged higher following last week’s earnings report from Nvidia (NVDA). The reason I say “this is nuts” is the assumption that all companies were going to grow earnings and revenue at Nvidia’s rate. There is little doubt about Nvidia’s earnings and revenue growth rates. However, to maintain that growth pace indefinitely, particularly at 32x price-to-sales, means others like AMD and Intel must lose market share.”

Of course, it is not just a speculative frenzy in the markets for stocks, specifically anything related to “artificial intelligence,” but that exuberance has spilled over into gold and cryptocurrencies.

Birds Of A Feather

There are a couple of ways to measure exuberance in the assets. While sentiment measures examine the broad market, technical indicators can reflect exuberance on individual asset levels. However, before we get to our charts, we need a brief explanation of statistics, specifically, standard deviation.

“Like a rubber band that has been stretched too far – it must be relaxed in order to be stretched again. This is exactly the same for stock prices that are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average.”

The idea of “stretching the rubber band” can be measured in several ways, but I will limit our discussion this week to Standard Deviation and measuring deviation with “Bollinger Bands.”

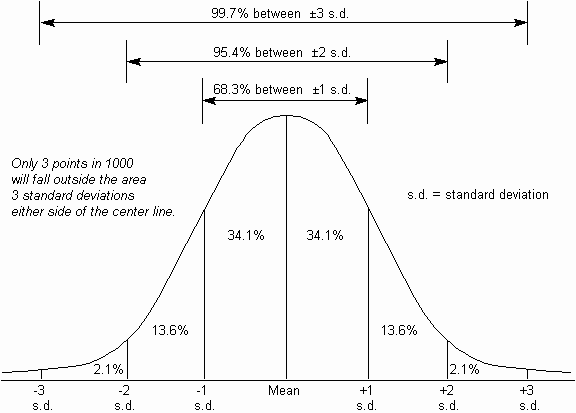

“Standard Deviation” is defined as:

“A measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is calculated as the square root of the variance.”

In plain English,this meansthat the further away from the average that an event occurs, the more unlikely it becomes. As shown below, out of 1000 occurrences, only three will fall outside the area of 3 standard deviations. 95.4% of the time, events will occur within two standard deviations.

A second measure of “exuberance” is “relative strength.”

“In technical analysis, the relative strength index (RSI) is a momentum indicator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The RSI is displayed as an oscillator (a line graph that moves between two extremes) and can read from 0 to 100.

Traditional interpretation and usage of the RSI are that values of 70 or above indicate that a security is becoming overbought or overvalued and may be primed for a trend reversal or corrective pullback in price. An RSI reading of 30 or below indicates an oversold or undervalued condition.” – Investopedia

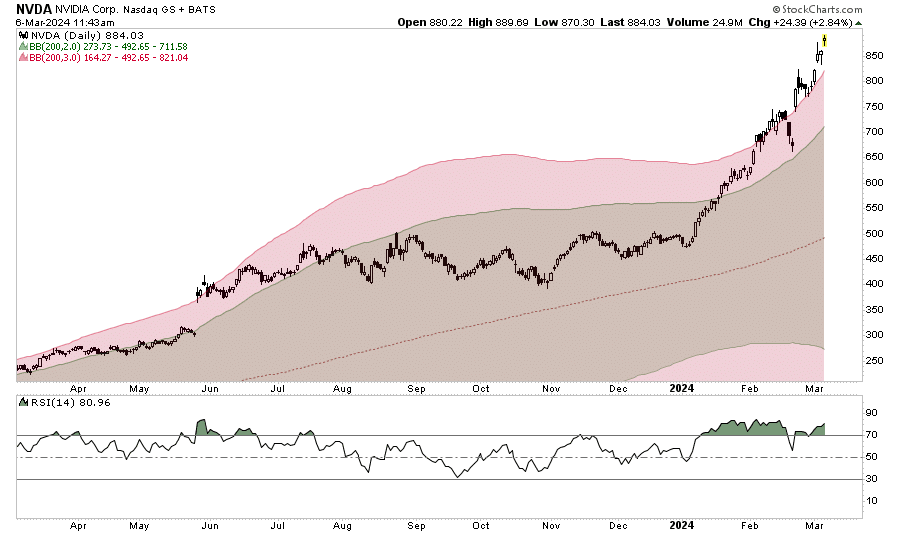

With those two measures, let’s look at Nvidia (NVDA), the poster child of speculative momentum trading in the markets. Nvidia trades more than 3 standard deviations above its moving average, and its RSI is 81. The last time this occurred was in July of 2023 when Nvidia consolidated and corrected prices through November.

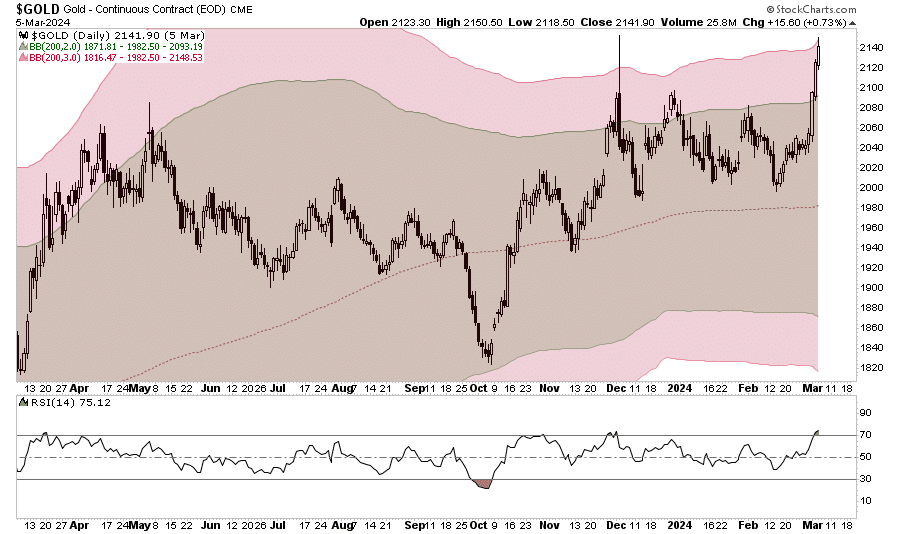

Interestingly, gold also trades well into 3 standard deviation territory with an RSI reading of 75. Given that gold is supposed to be a “safe haven” or “risk off” asset, it is instead getting swept up in the current market exuberance.

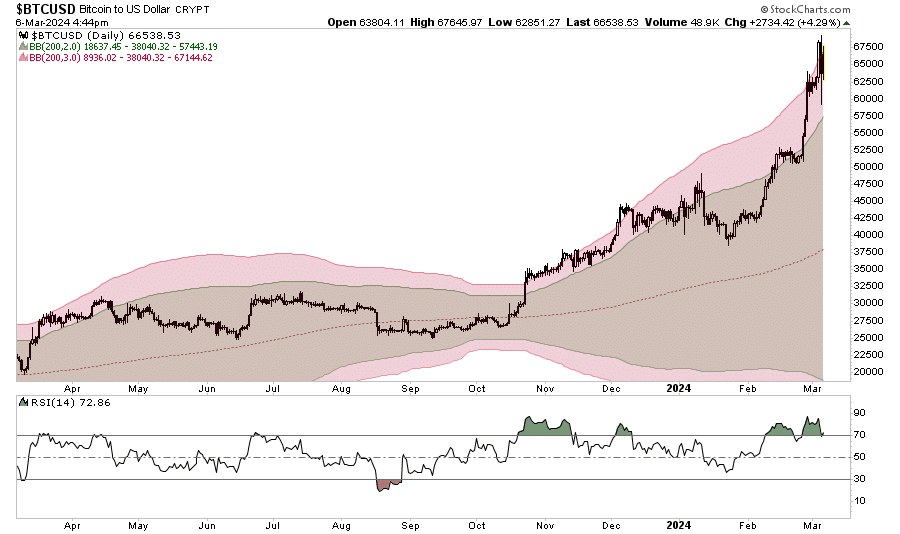

The same is seen with digital currencies. Given the recent approval of spot, Bitcoin exchange-traded funds (ETFs), the panic bid to buy Bitcoin has pushed the price well into 3 standard deviation territory with an RSI of 73.

In other words, the stock market frenzy to “buy anything that is going up” has spread from just a handful of stocks related to artificial intelligence to gold and digital currencies.

It’s All Relative

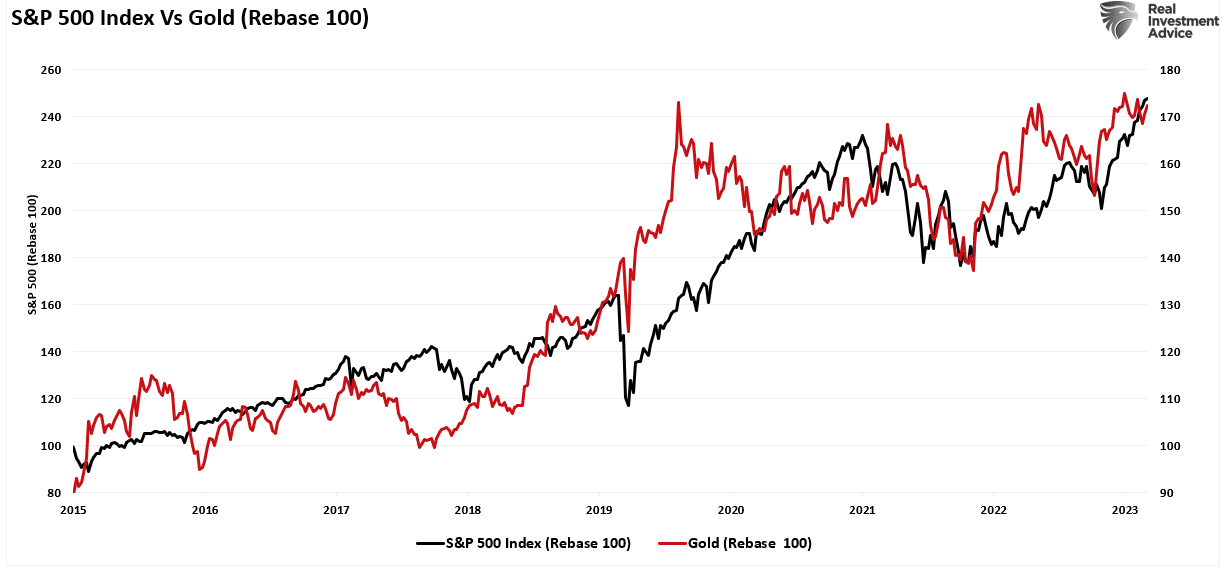

We can see the correlation between stock market exuberance and gold and digital currency, which has risen since 2015 but accelerated following the post-pandemic, stimulus-fueled market frenzy. Since the market, gold and cryptocurrencies, or Bitcoin for our purposes, have disparate prices, we have rebased the performance to 100 in 2015.

Gold was supposed to be an inflation hedge. Yet, in 2022, gold prices fell as the market declined and inflation surged to 9%. However, as inflation has fallen and the stock market surged, so has gold. Notably, since 2015, gold and the market have moved in a more correlated pattern, which has reduced the hedging effect of gold in portfolios. In other words, during the subsequent market decline, gold will likely track stocks lower, failing to provide its “wealth preservation” status for investors.

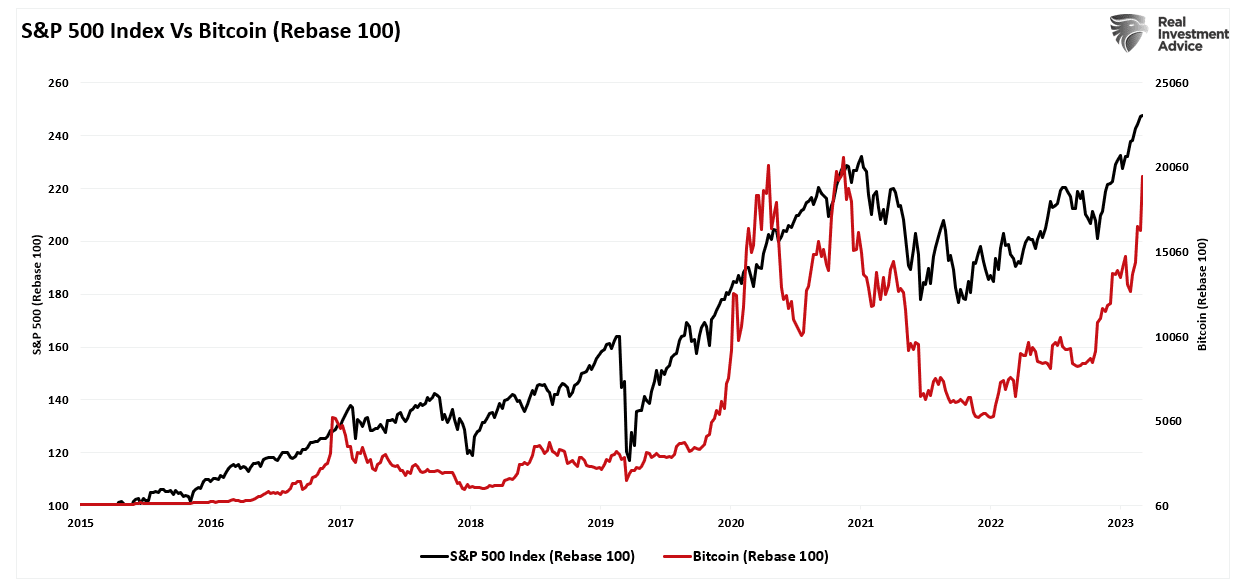

The same goes for cryptocurrencies. Bitcoin is substantially more volatile than gold and tends to ebb and flow with the overall market. As sentiment surges in the S&P 500, Bitcoin and other cryptocurrencies follow suit as speculative appetites increase. Unfortunately, for individuals once again piling into Bitcoin to chase rising prices, if, or when, the market corrects, the decline in cryptocurrencies will likely substantially outpace the decline in market-based equities. This is particularly the case as Wall Street can now short the spot-Bitcoin ETFs, creating additional selling pressure on Bitcoin.

Just for added measure, here is Bitcoin versus gold.

Not A Recommendation

There are many narratives surrounding the markets, digital currency, and gold. However, in today’s market, more than in previous years, all assets are getting swept up into the investor-feeding frenzy.

Sure, this time could be different. I am only making an observation and not an investment recommendation.

However, from a portfolio management perspective, it will likely pay to remain attentive to the correlated risk between asset classes. If some event causes a reversal in bullish exuberance, cash and bonds may be the only place to hide.

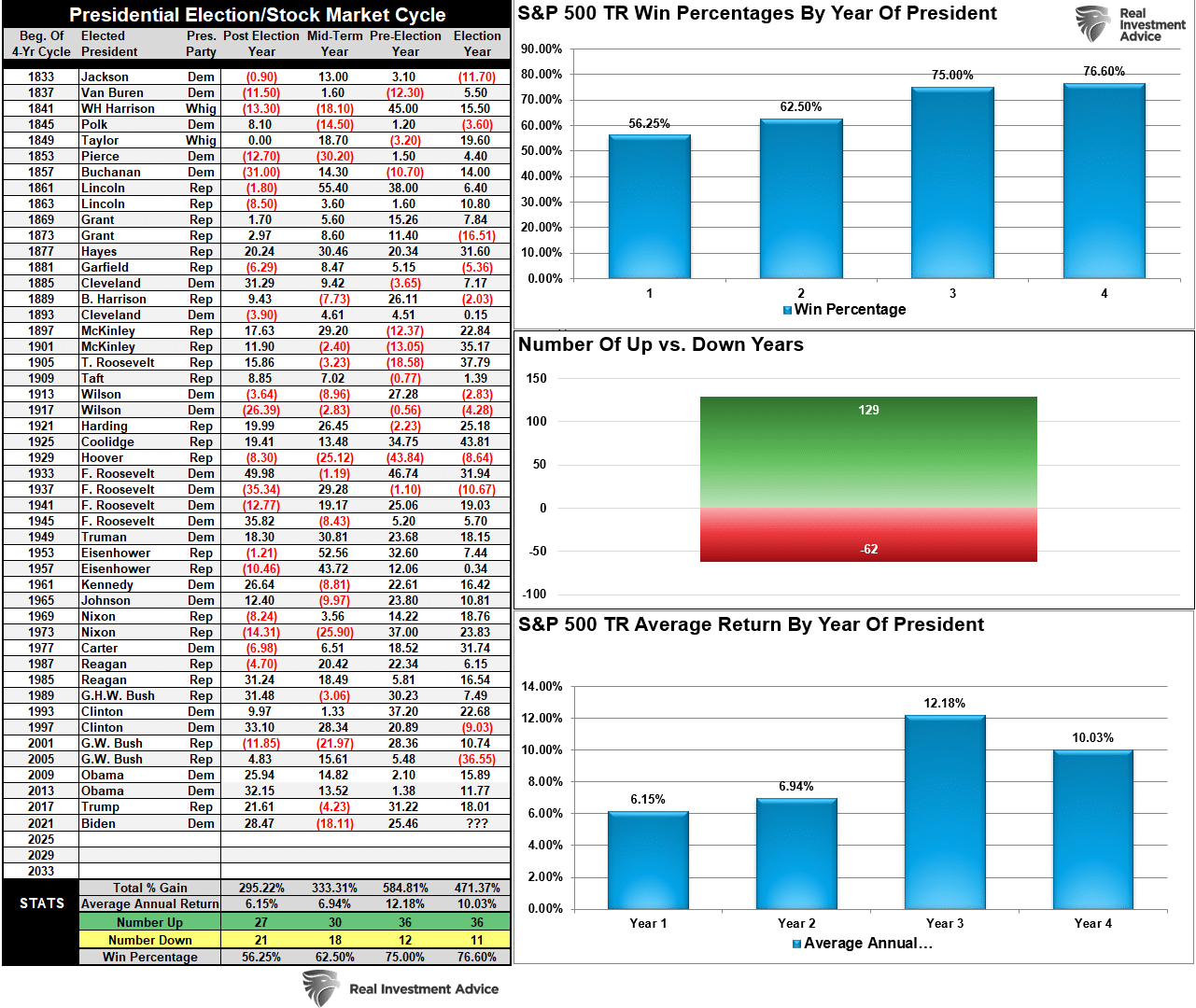

Presidential Elections And Market Corrections

Presidential elections and market corrections have a long history of companionship. Given the rampant rhetoric between the right and left, such is not surprising. Such is particularly the case over the last two Presidential elections, where polarizing candidates trumped policies.

From a portfolio management perspective, we must understand what happens during election years concerning the stock market and investor returns.

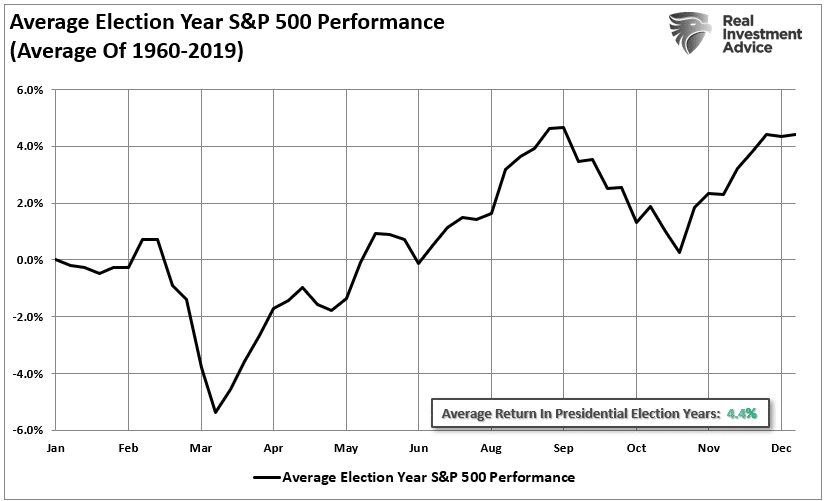

Since 1833, the S&P 500 index has gained an average of 10.03% in the year of a presidential election. By contrast, the first and second years following a Presidential election see average gains of 6.15% and 6.94%, respectively. There are notable exceptions to positive election-year returns, such as in 2008, when the S&P 500 sank nearly 37%. (Returns are based on price only and exclude dividends.) However, overall, the win rate of Presidential election years is a very high 76.6%

Since President Roosevelt’s victory in 1944, there have only been two losses during presidential election years: 2000 and 2008. Those two years corresponded with the “Dot.com Crash” and the “Financial Crisis.” On average, the second-best performance years for the S&P 500 are in Presidential election years.

For investors, with a “win ratio” of 76%, the odds are high that markets will most likely finish the 2024 Presidential election year higher. However, given the current economic underpinnings, I would caution completely dismissing the not-so-insignificant 24% chance that a more meaningful correction could reassert itself. Given the recent 15-year duration of the ongoing bull market, the more extreme deviations from long-term means, and ongoing valuation issues, a “Vegas handicapper” might increase those odds a bit.

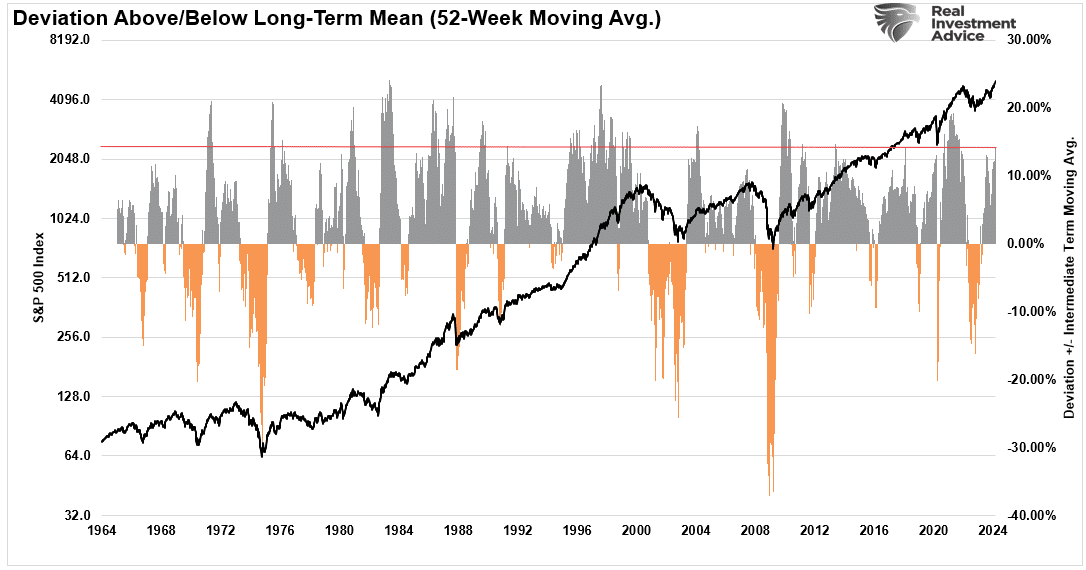

That deviation is more significant when looking at the 1-year moving average. Current deviation levels from the 52-week moving average have generally preceded short-term market corrections or worse.

However, as stated, while the market will likely end the year higher than where it started, Presidential election years have a correctional bias to them during the summer months.

Will Policies Matter

The short answer is “Yes.” However, not in the short term.

Presidential platforms are primarily “advertising” to get your vote. As such, a politician will promise many things that, in hindsight, rarely get accomplished. Therefore, while there is much debate about whose policies will be better, it doesn’t matter much as both parties have an appetite for “providing bread and games to the masses” through continuing increases in debt.

However, regarding the financial markets, Wall Street tends to abhor change. With the incumbent President, Wall Street understands the “horse the riding.” The risk to elections is a policy change that may undermine current trends. Those policy changes could be an increase in taxes, restrictive trade policies, cuts to spending, etc., which would potentially be unfriendly to financial markets in the short term.

This is why markets tend to correct things before the November elections. A look at all election years since 1960 shows that markets did rise during election years. However, notice that the market tends to correct during September and October.

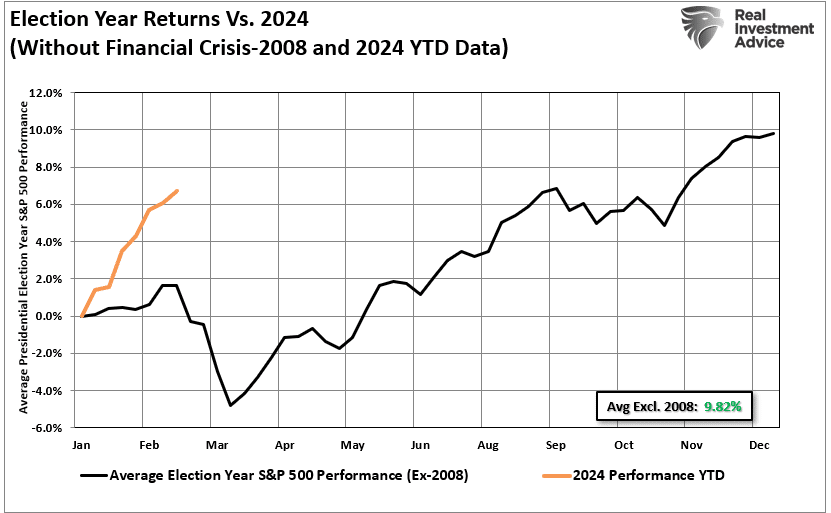

Notably, that data is heavily skewed by the decline during the 2008 “Financial Crisis,” also a Presidential election year. If we extract that one year, returns jump to 7.7% annually in election years. However, in both cases, returns still slump during September and October. The chart below shows that 2024 is running well ahead of historical norms.

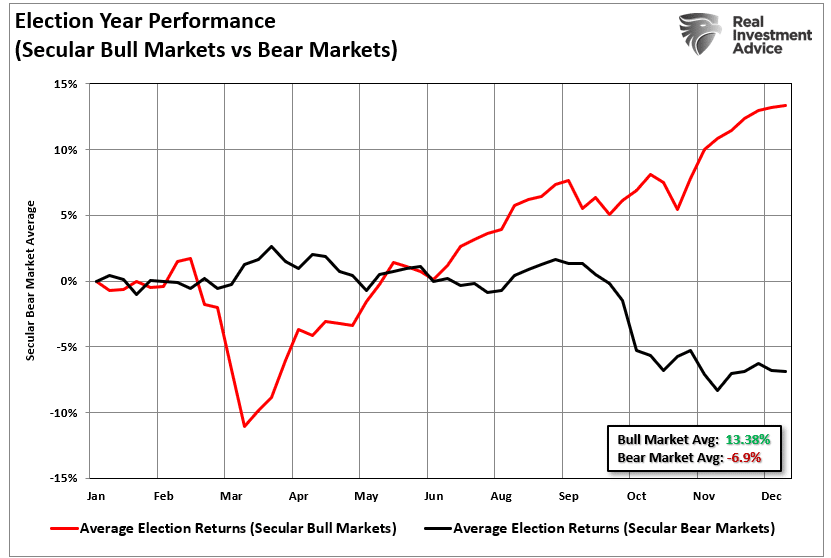

Lastly, while policies matter over a longer-term period, as changes to spending and regulation impact economic outcomes, market performance during SECULAR market periods varies greatly. During secular (long-term) bull markets, as we have now since 2009, Presidential election years tend to average almost 14% annually. That is opposed to secular bear markets, which tend to decline by 7% on average.

However, one risk that has taken shape since the “Financial Crisis” could have an outside effect on the markets in 2024.

The Great Divide

While you may feel strongly about one party or the other regarding politics, it doesn’t matter much regarding your money.

Such is particularly the case today. As we head into November, for the third election in a row, voters will cast ballots for the candidate they dislike less, not whose policies they like more. More importantly, most voters are going to the polls with large amounts of misinformation from social media commentators pushing political agendas.

Notably, the market already understands that with the parties more deeply dividedthan at any other point in history, the likelihood of any policies getting passed is slim. (2017 was the latest data from a 2019 report. Currently, that gap is even more significant as Social Media continues to fuel the divide.)

The one thing markets do seem to prefer – “political gridlock.”

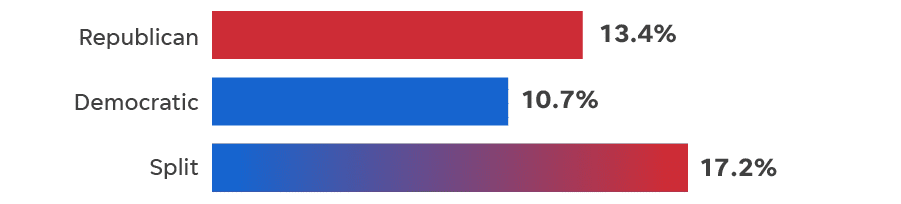

“A split Congress historically has been better for stocks, which tend to like that one party doesn’t have too much sway. Stocks gained close to 30% in 1985, 2013 and 2019, all under a split Congress, according to LPL Financial. The average S&P 500 gain with a divided Congress was 17.2% while GDP growth averaged 2.8%.” – USA Today

What we can derive from the data is the odds suggest the market will end this year on a positive note. However, such says little about next year. If you go back to our data table above, the 1st year of a new Presidential cycle is roughly a 50/50 outcome. It is also the lowest average return year, going back to 1833.

Furthermore, from the election to 2025, outcomes have been overly dependent on many things continuing to go “right.”

Avoidance of a “double-dip” recession. (Without more Fiscal stimulus, this is a plausible risk.)

The Fed drastically expands monetary policy.(Such won’t come without a recession.)

The consumer will need to expand their current debt-driven consumption. (This is a risk without more fiscal stimulus or sustainable economic growth.)

There is a marked improvement in both corporate earnings and profitability. (This will likely be the case as mass layoffs benefit bottom-line profitability. However, top-line sales remain at risk due to items #1 and #3.)

Multiple expansions continue. (The problem is that a lack of earnings growth in the bottom 490 stocks eventually disappoints)

These risks are all undoubtedly possible.

However, when combined with the longest-running bull market in history, high valuations, and excessive speculation, the risks of something going wrong have risen.

So, how do you position your portfolio for the election?

Portfolio Positioning For An Unknown Election Outcome

Over the last few weeks, we have repeatedly discussed reducing risk, hedging, and rebalancing portfolios. Part of this was undoubtedly due to the exaggerated rise from the November lows and the potential for an unexpected election outcome. As we noted in “Tending The Garden:”

“Taking these actions has TWO specific benefits depending on what happens in the market next.

If the market corrects, these actions clear out the ‘weeds’ and allow for protection of capital against a subsequent decline.

If the market continues to rally, then the portfolio has been cleaned up, and new positions can be added to participate in the next leg of the advance.

No one knows for sure where markets are headed in the next week, much less the next month, quarter, year, or five years. What we do know is not managing ‘risk’ to hedge against a decline is more detrimental to the achievement of long-term investment goals.”

That advice continues to play well in setting up your portfolio for the election. As outlined, the historical odds suggest that markets will rise regardless of the electoral outcome. However, those are averages. In 2000 and 2008, investors didn’t get the “average.”

Such is why it is always important to prepare for the unexpected. While you certainly wouldn’t speed down a freeway “blindfolded,” it makes little sense not to be prepared for an unexpected outcome.

Holding a little extra cash, increasing positioning in Treasury bonds, and adding some “value” to your portfolio will help reduce the risk of a sharp decline in the months ahead. Once the market signals an “all clear,” you can take “your foot off the brake” and speed to your destination.

Of course, it never hurts to always “wear your seatbelt.”

Valuation Metrics And Volatility Suggest Investor Caution

Valuation metrics have little to do with what the market will do over the next few days or months. However, they are essential to future outcomes and shouldn’t be dismissed during the surge in bullish sentiment. Just recently, Bank of America noted that the market is expensive based on 20 of the 25 valuation metrics they track. As BofA’s Chief Equity Strategist stated:

“The S&P 500 is egregiously expensive vs. history. It’s hard to be bullish based on valuation“

Since 2009, repeated monetary interventions and zero interest rate policies have led many investors to dismiss any measure of “valuation.” Therefore, investors reason the indicator is wrong since there was no immediate correlation.

The problem is that valuation models are not, and were never meant to be, “market timing indicators.” The vast majority of analysts assume that if a measure of valuation (P/E, P/S, P/B, etc.) reaches some specific level, it means that:

The market is about to crash, and;

Investors should be in 100% cash.

Such is incorrect. Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of “investor psychology” and the manifestation of the “greater fool theory.” As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.

What valuations do provide is a reasonable estimate of long-term investment returns. It is logical that if you overpay for a stream of future cash flows today, your future return will be low.

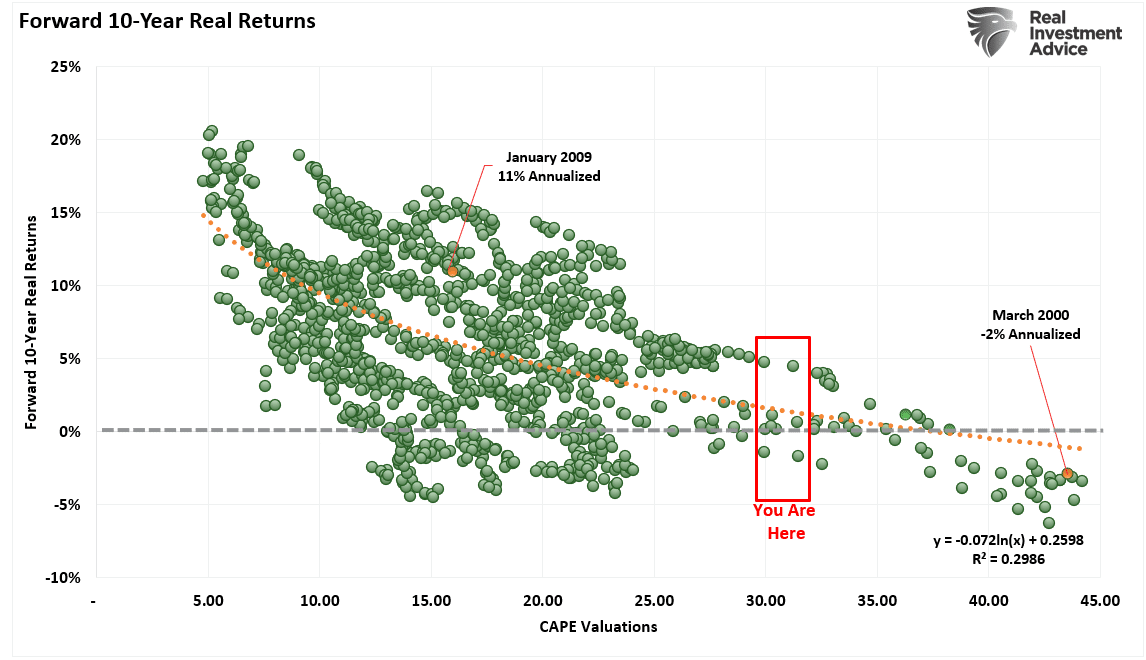

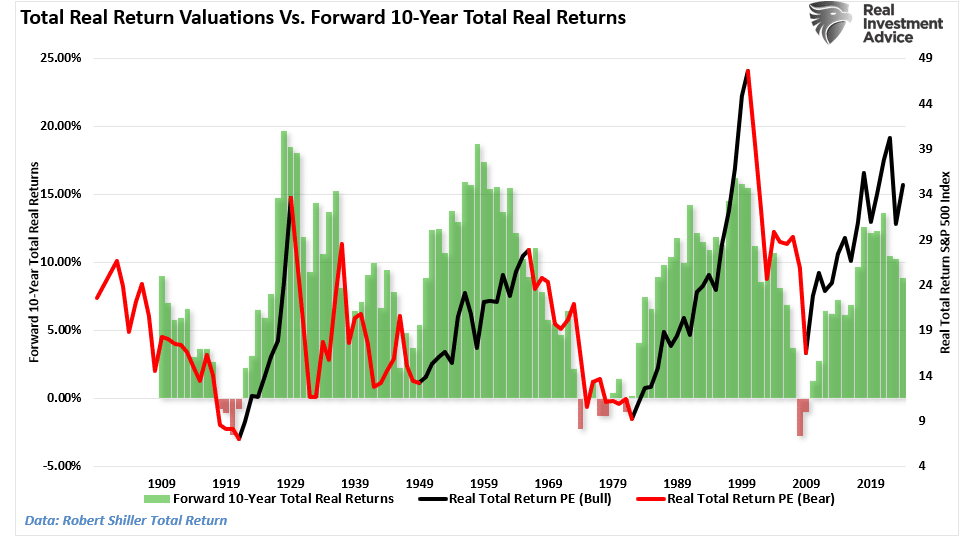

“Ten-year forward average returns fall nearly monotonically as starting Shiller P/E’s increase. Also, as starting Shiller P/E’s go up, worst cases get worse and best cases get weaker.

If today’s Shiller P/E is 22.2, and your long-term plan calls for a 10% nominal (or with today’s inflation about 7-8% real) return on the stock market, you are basically rooting for the absolute best case in history to play out again, and rooting for something drastically above the average case from these valuations.”

We can prove that by looking at forward 10-year total returns versus various levels of PE ratios historically.

Asness continues:

“It [Shiller’s CAPE] has very limited use for market timing (certainly on its own) and there is still great variability around its predictions over even decades. But, if you don’t lower your expectations when Shiller P/E’s are high without a good reason — and in my view, the critics have not provided a good reason this time around — I think you are making a mistake.”

Which brings me to Warren Buffett.

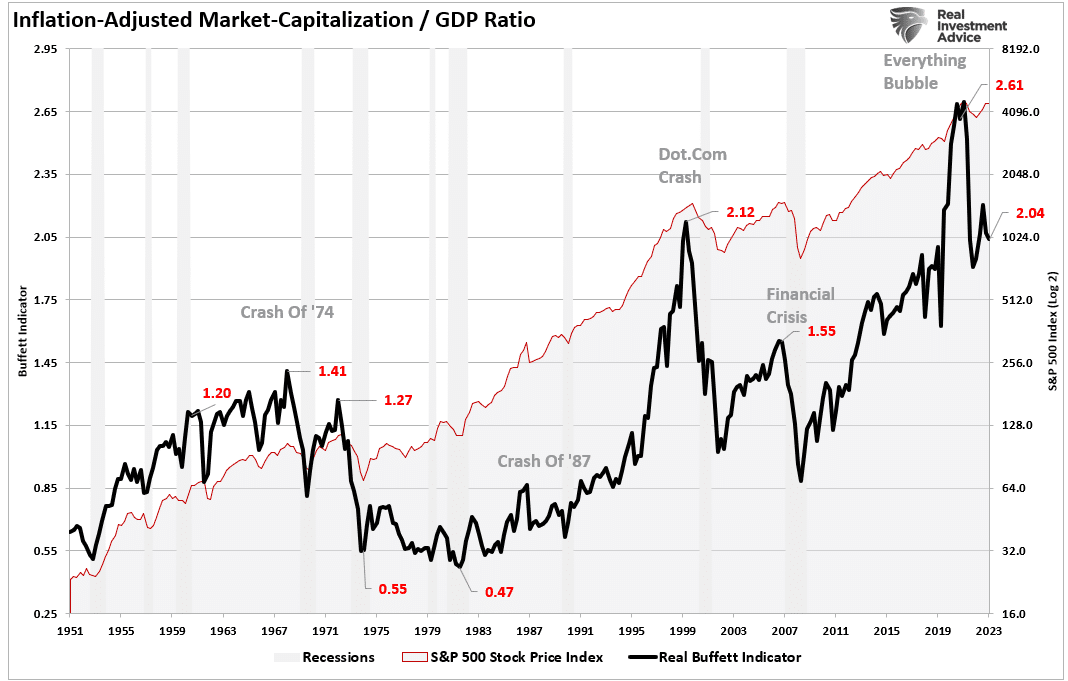

Market Cap To GDP

In our most recent newsletter, I discussed Warren Buffet’s dilemma with his $160 billion cash pile.

The problem with capital investments is that they take time to generate a profitable return that accretes to the business’s bottom line. The same goes for acquisitions. More importantly, concerning acquisitions, they must both be accretive to the company and reasonably priced. Such is Berkshire’s current dilemma.

“There remain only a handful of companies in this country capable of truly moving the needle at Berkshire, and they have been endlessly picked over by us and by others. Some we can value; some we can’t. And, if we can, they have to be attractively priced.”

This was an essential statement. Here is one of the most intelligent investors in history, suggesting that he cannot deploy Berkshire’s massive cash hoard in meaningful size due to an inability to find acquisition targets that are reasonably priced. With a $160 war chest, there are plenty of companies that Berkshire could either acquire outright, use a stock/cash offering, or acquire a controlling stake in. However, given the rampant increase in stock prices and valuations over the last decade, they are not reasonably priced.

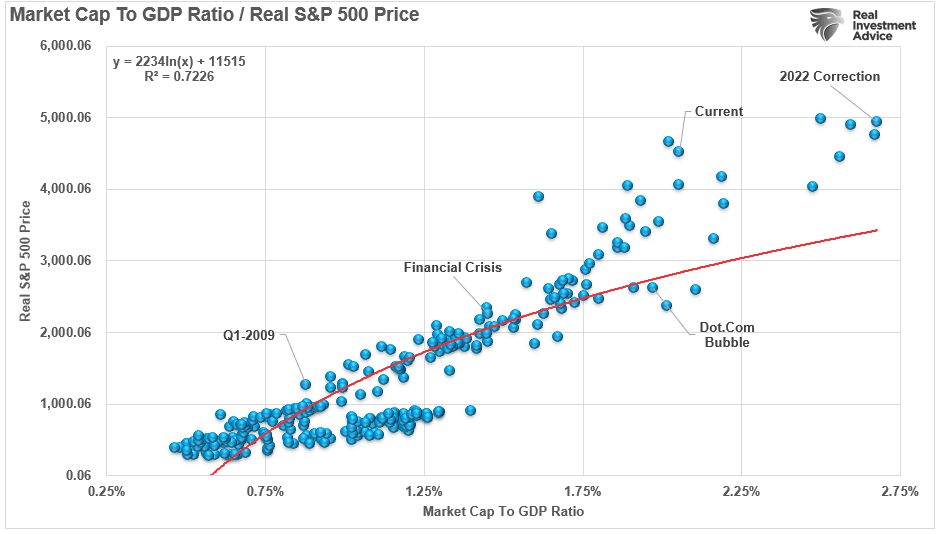

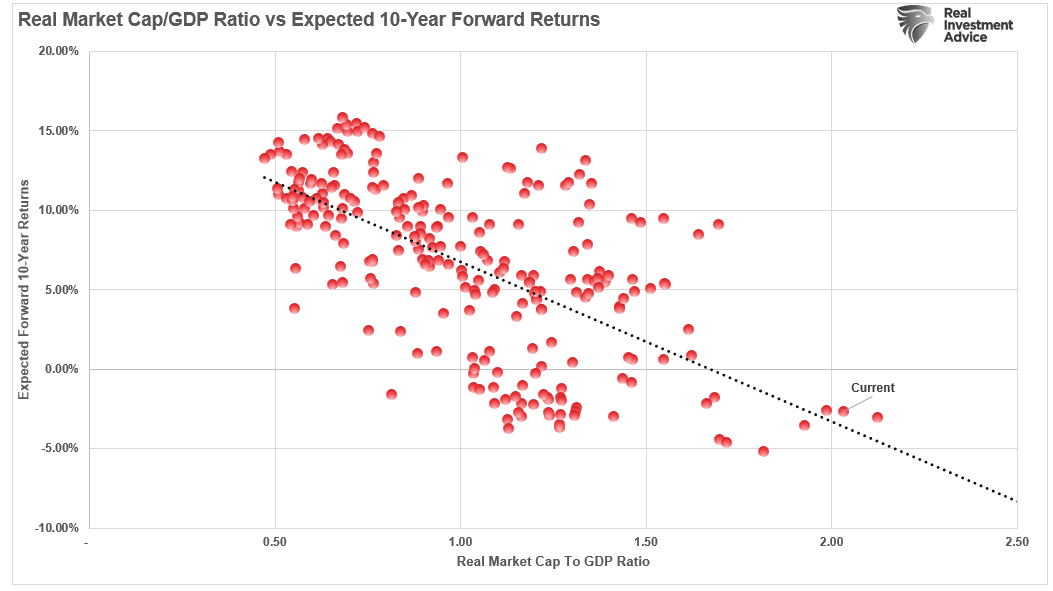

One of Warren Buffett’s favorite valuation measures is the market capitalization to GDP ratio. I have modified it slightly to use inflation-adjusted numbers. The simplicity of this measure is that stocks should not trade above the value of the economy. This is because economic activity provides revenues and earnings to businesses.

The “Buffett Indicator” confirms Mr. Asness’ point. The chart below uses the S&P 500 market capitalization versus GDP and is calculated on quarterly data.

Not surprisingly, like every other valuation measure, forward return expectations are substantially lower over the next ten years than in the past.

None of this should be surprising. Logics suggests that overpaying for any asset in the present inherently will generate lower future expected returns versus buying assets at a discount. Or, as Warren Buffett stated:

“Price is what you pay. Value is what you get.”

F.O.M.O. Trumps Fundamentals

In the “heat of the moment,” fundamentals don’t matter. In a market where momentum drives participants due to the “Fear Of Missing Out (F.O.M.O.),” fundamentals are displaced by emotional biases. Such is the nature of market cycles and one of the primary ingredients necessary to create the proper environment for an eventual reversion.

Notice, I said eventually.

As David Einhorn once stated:

“The bulls explain that traditional valuation metrics no longer apply to certain stocks. The longs are confident that everyone else who holds these stocks understands the dynamic and won’t sell either. With holders reluctant to sell, the stocks can only go up – seemingly to infinity and beyond. We have seen this before.

There was no catalyst that we know of that burst the dot-com bubble in March 2000, and we don’t have a particular catalyst in mind here. That said, the top will be the top, and it’s hard to predict when it will happen.”

Furthermore, as James Montier previously stated:

“Current arguments as to why this time is different are cloaked in the economics of secular stagnation and standard finance workhorses like the equity risk premium model. Whilst these may lend a veneer of respectability to those dangerous words, taking arguments at face value without considering the evidence seems to me, at least, to be a common link with previous bubbles.“

As BofA noted in its analysis, stocks are far from cheap. Based on Buffett’s preferred valuation model and historical data, return expectations for the next ten years are as likely to be close to zero or negative. Such was the case for ten years following the late ’90s.

Investors would do well to remember the words of the then-chairman of the SEC, Arthur Levitt. In a 1998 speech entitled “The Numbers Game,” he stated:

“While the temptations are great, and the pressures strong, illusions in numbers are only that—ephemeral, and ultimately self-destructive.”

Regardless, there is a straightforward truth.

“The stock market is NOT the economy.But the economy is a reflection of the very thing that supports higher asset prices: earnings.”

The economy is slowing down following the pandemic-related spending spree. It is also doubtful the Government can continue spending at the same clip over the next decade as it did in the last.

While current valuations are expensive, it does NOT mean the markets will crash tomorrow, next quarter, or even next year.

However, there is a more than reasonable expectation of disappointment in future market returns.

That is probably something investors need to come to grips with sooner rather than later.

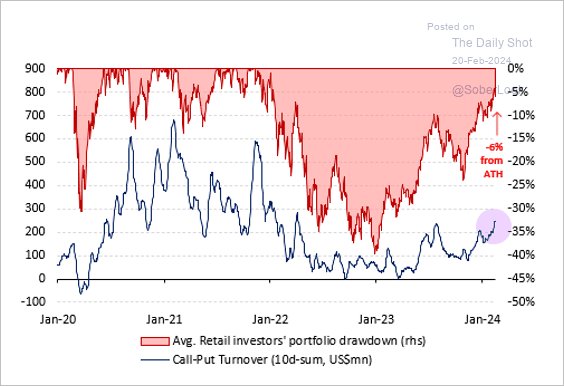

Dumb Money Almost Back To Even, Making The Same Mistakes

After over two years, retail investors, also known as the “dumb money,” are almost back to breakeven. A recent chart by Vanda Research shows that the average retail “dumb money” investor portfolio still sports a drawdown despite the markets making new all-time highs.

Such is unsurprising, given that retail investors often fall victim to the psychological behavior of the “fear of missing out.” The chart below shows the “dumb money index” versus the S&P 500. Once again, retail investors are very long equities relative to the institutional players ascribed to being the “smart money.”

The difference between “smart” and “dumb money” investors shows that, more often than not, the “dumb money” invests near market tops and sells near market bottoms.