Energy Sector Analysis: 1-09-2020

We have been discussing the opportunity that may be presenting itself in the Energy sector. With oil prices rising, and valuations better than other areas of the market, there are some trading opportunities starting to appear.

While the portfolios are designed to have longer-term holding periods, we understand that things do not always go the way we plan. We are entering the energy sector on a trading basis only, which could be very short-term, until both the positions and the overall thesis begins to mature.

While there are a LOT of energy companies to choose from, we have eliminated all companies which are NOT PROFITABLE from our analysis. All candidates must also pay a dividend to comply with our total return thesis and portfolio strategy.

Sector ETF’s

XLE – Energy Select Sector SPDR

- With the broad energy sector on a buy signal, we are looking to add exposure to our portfolios.

- We have been reluctant to move too quickly as previous rally attempts to the 200-dma have been selling opportunities.

- With the sector very overbought short-term, we are looking for a pullback in the broader energy sector to add 1/2 position to the Equity and ETF portfolios.

- Stop is will be set at $58 after entry.

IEO – iShares U.S. Oil & Gas Exploration

- As with the broader energy space, Oil & Gas exploration has also broken about the 200-dma and is on a buy signal.

- As with XLE, IEO is very overbought and needs a correction to work off the overbought position before positions can be added.

- The stop is set at $53 after entry.

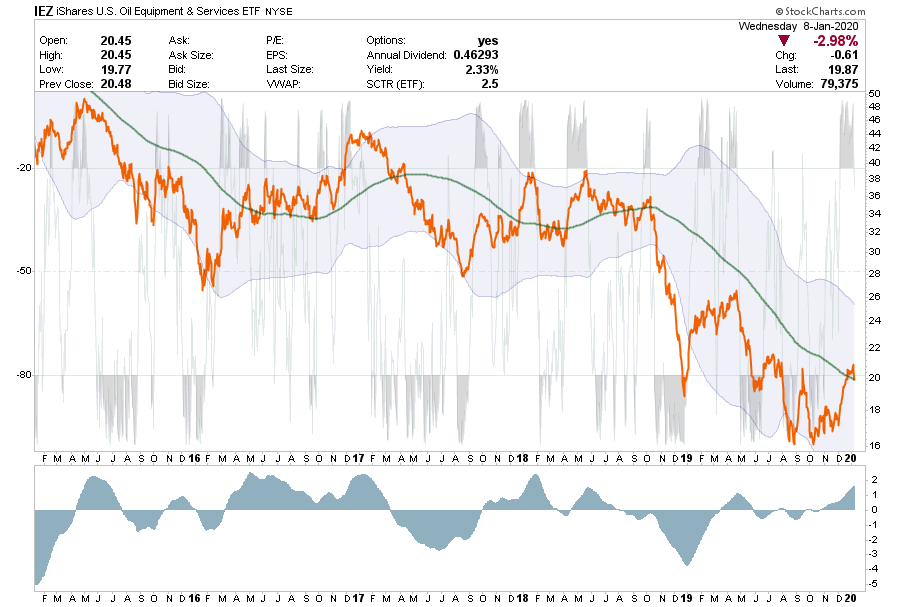

IEZ – iShares U.S. Oil Equipment & Services

- Oil & Equipment Services doesn’t look as convincing as the refining and major oil companies look.

- While IEZ is very overbought it is just now making an attempt to break above the 200-dma. It is too early to consider this space as most of the companies in the sector are not profitable and are carrying a lot of debt.

Individual Securities

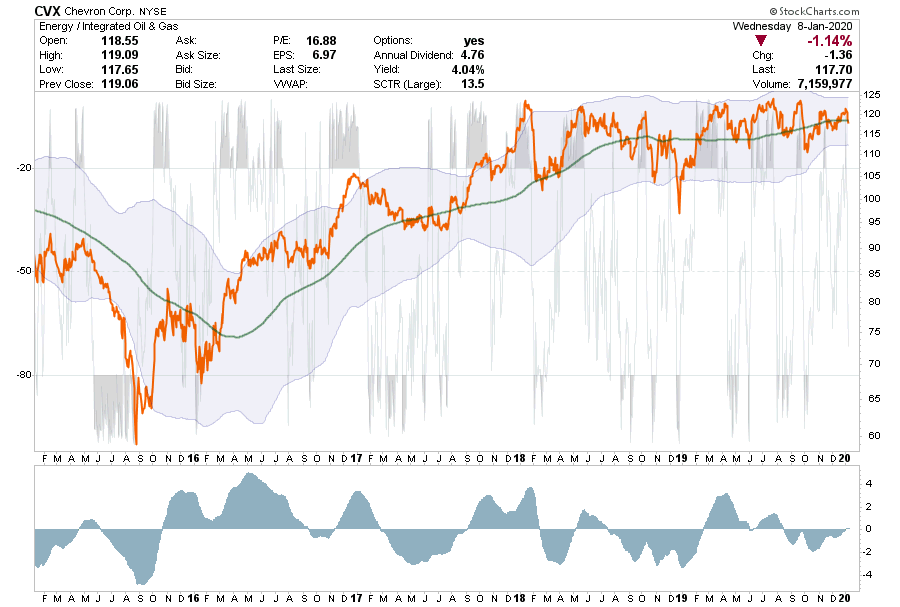

CVX – Chevron Corp.

- CVX hasn’t done much in the last couple of years either good or bad.

- Currently, CVX is on a sell signal, which is improving and close to turning positive, and the position is currently holding the 200-dma.

- With a near 5% yield, the return has almost solely come from the dividend over the last couple of years.

- We like this company and will look to add a position if the buy signal turns positive and support holds.

- Stop is set at $112.50 after entry.

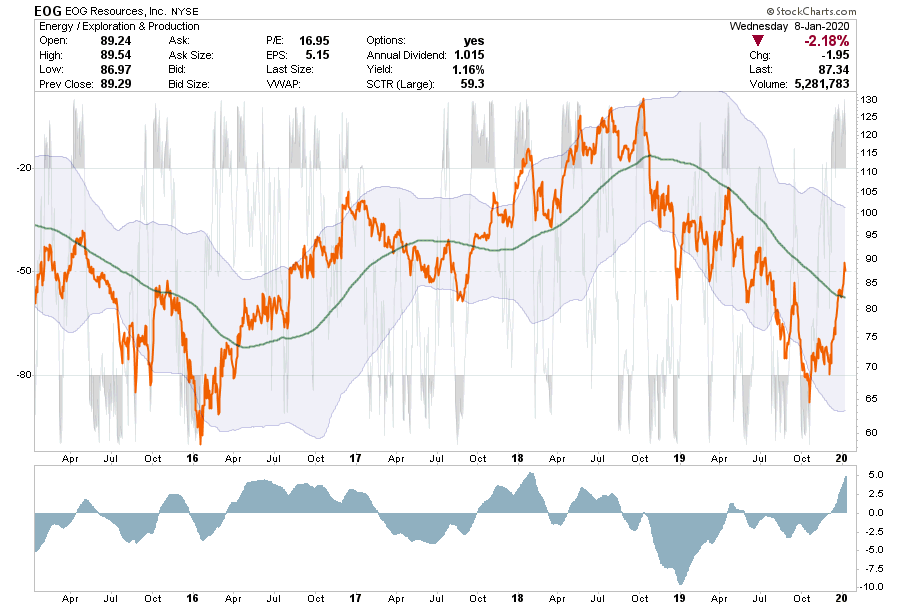

EOG – EOG Resources

- EOG has had an extremely sharp move and is overbought with a very extended buy signal currently.

- EOG needs to correct, work off the overbought condition, and reduce the buy signal before an entry can be made.

- Take profits if you are long currently,

- Stop is set at $70

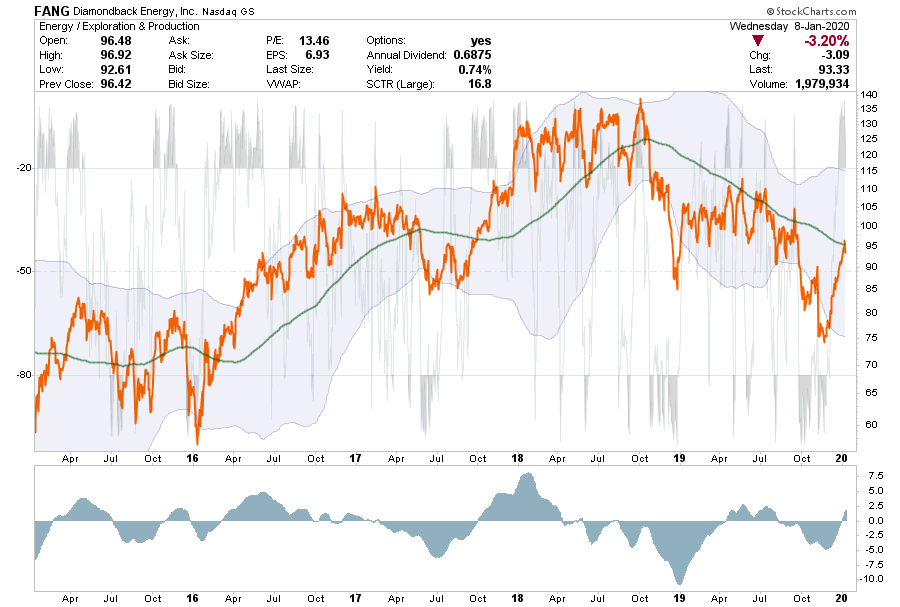

FANG – Diamond Back Drilling

- FANG is currently testing its 200-dma which has been the downtrend resistance point for the stock.

- The stock is currently very overbought, but is just registering a “buy signal.”

- We are going to watch this stock closely, it needs more work before becoming a potential trade.

- If long currently, take profits.

- Stop is set at $75

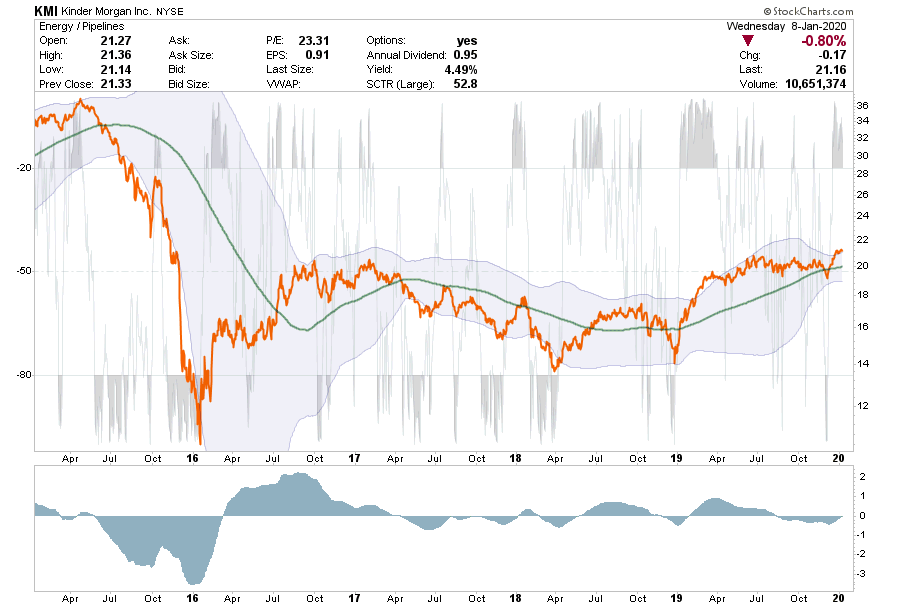

KMI – Kinder Morgan

- KMI has had a lot of problems since their acquisition of El Paso Energy.

- The stock is currently very overbought, but is close to registering a “buy signal” after holding support at the 200-dma.

- KMI needs to correct a little, and hold support at the 200-dma, to provide for a decent entry point. If oil prices correct, that entry point will be come likely.

- If long the position, take profits.

- Stop loss is set at $20

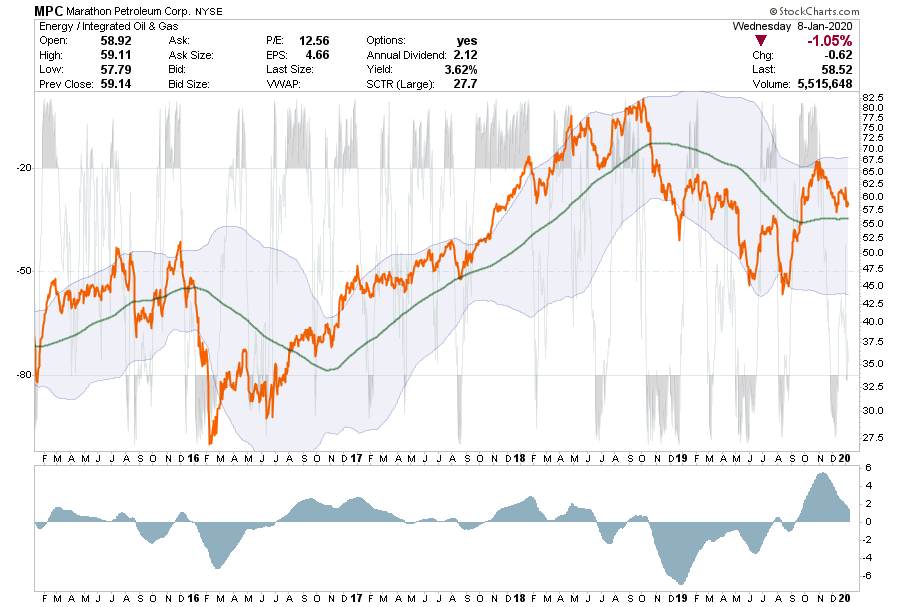

MPC – Marathon Petroleum Corp.

- MPC is a little different picture than the others

- MPC had a very strong rally, got very extended, and is now correcting that extension.

- With the position holding support at the 200-dma, there is a decent trading setup to add to portfolios. We also like the 3.6% yield.

- Buy 1/2 position at current levels.

- Stop is tight at the 200-dma or $56.

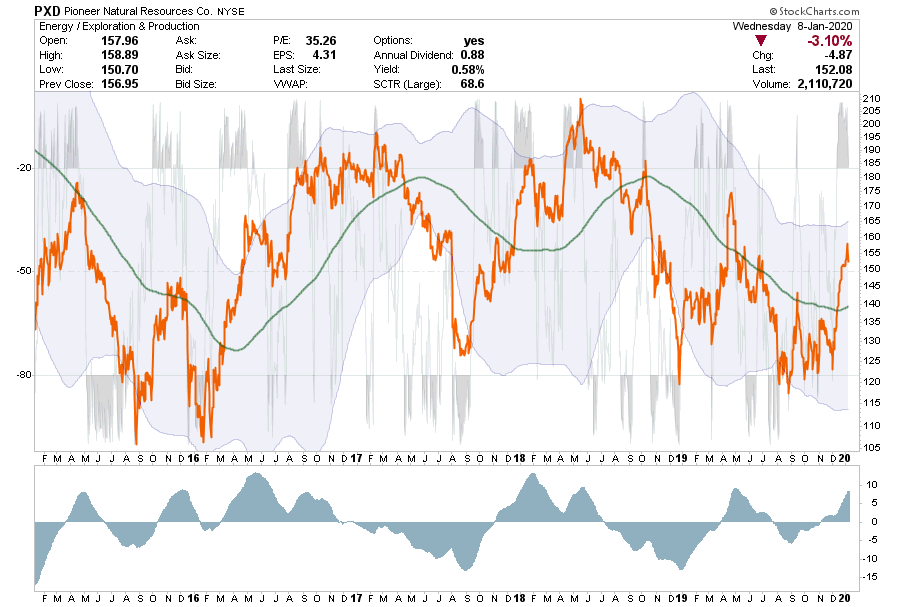

PXD – Pioneer Natural Resources

- PXD has had a very strong run over and is both extended on its buy signal and very overbought.

- Wait for a correction which holds support at the 200-dma and works off the overbought and extended condition.

- Take profits if long the position currently.

- Stop loss is set at $140

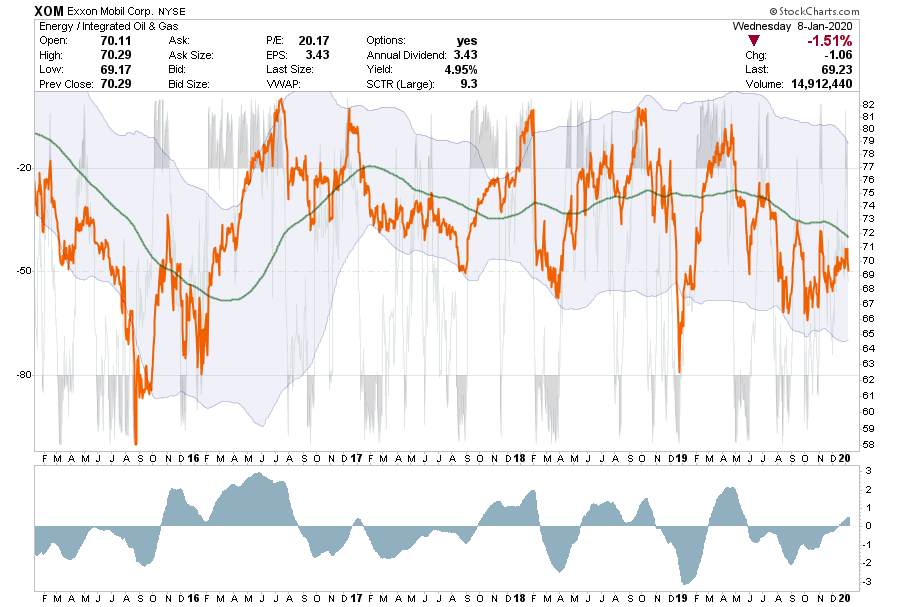

XOM – Exxon Mobil

- XOM has rallied off of lows where we added to our existing position last year.

- However, while it has failed at the 200-dma it has registered a short-term buy signal.

- While we are roughly flat in the position currently, performance has been disappointing while we are collecting the 5% yield.

- We will continue to hold the position for now, but may look to reduce it on any rally in the near future.

- Stop loss remains at $66