#MacroView: Japan, The Fed, & The Limits Of QE

This past week saw a couple of interesting developments.

On Wednesday, the Fed released the minutes from their January meeting with comments which largely bypassed overly bullish investors.

“… several participants observed that equity, corporate debt, and CRE valuations were elevated and drew attention to high levels of corporate indebtedness and weak underwriting standards in leveraged loan markets. Some participants expressed the concern that financial imbalances-including overvaluation and excessive indebtedness-could amplify an adverse shock to the economy …”

“… many participants remarked that the Committee should not rule out the possibility of adjusting the stance of monetary policy to mitigate financial stability risks, particularly when those risks have important implications for the economic outlook and when macroprudential tools had been or were likely to be ineffective at mitigating those risks…”

The Fed recognizes their ongoing monetary interventions have created financial risks in terms of asset bubbles across multiple asset classes. They are also aware that the majority of the policy tools are likely ineffective at mitigating financial risks in the future. This leaves them being dependent on expanding their balance sheet as their primary weapon.

Interestingly, the weapon they are dependent on may not be as effective as they hope.

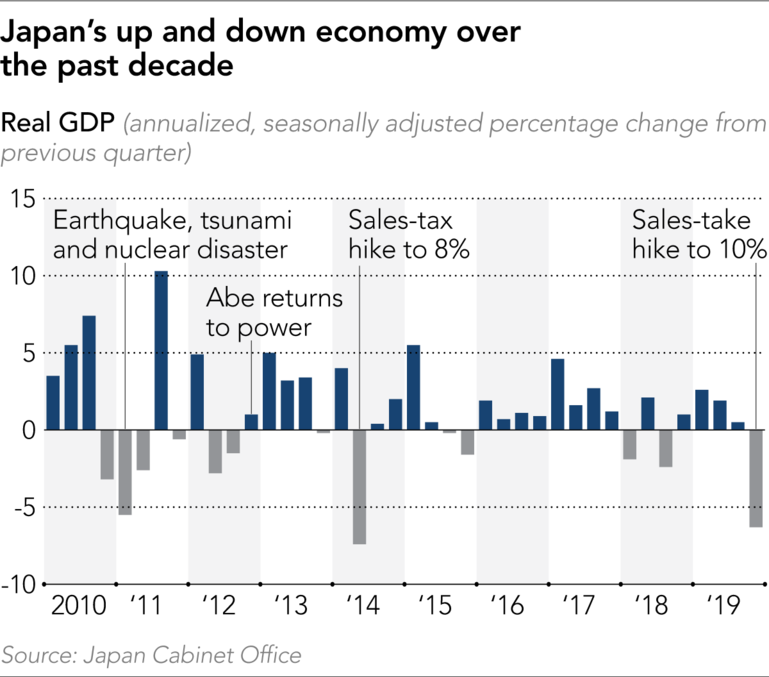

This past week, Japan reported a very sharp drop in economic growth in their latest reported quarter as a further increase in the sales-tax hit consumption. While the decline was quickly dismissed by the markets, this was a pre-coronovirus impact, which suggests that Japan will enter into an “official” recession in the next quarter.

There is more to this story.

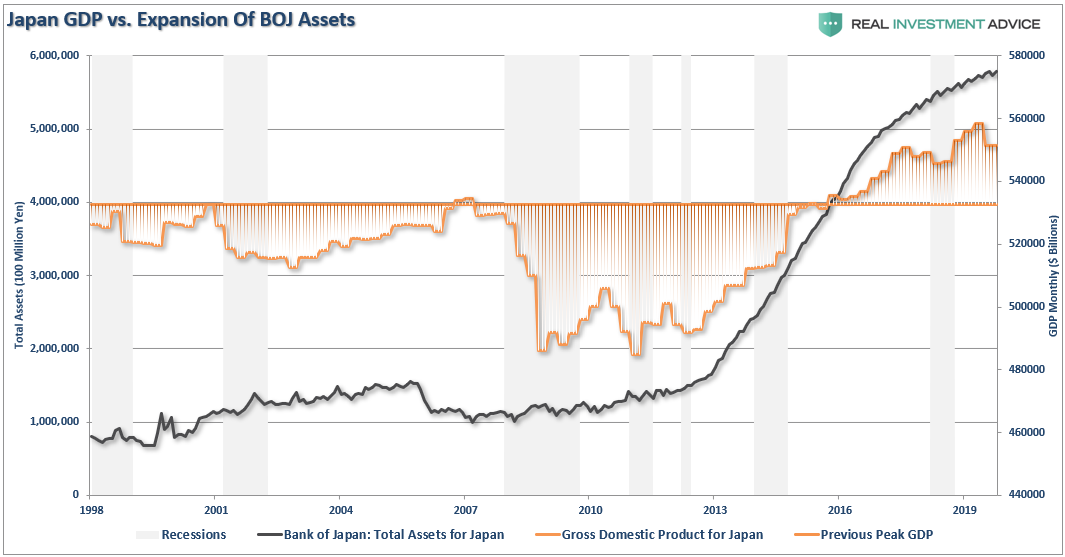

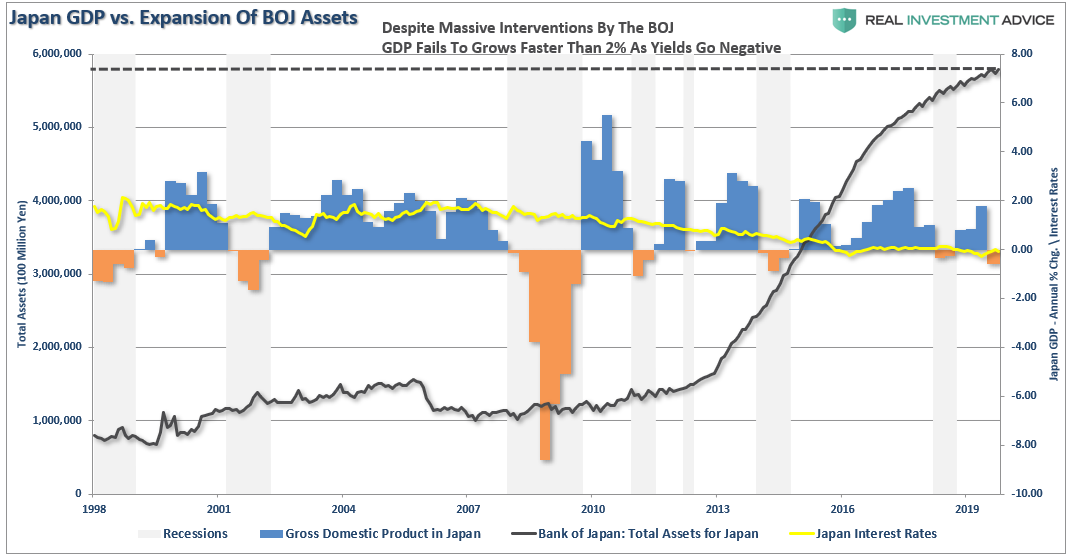

Since the financial crisis, Japan has been running a massive “quantitative easing” program which, on a relative basis, is more than 3-times the size of that in the U.S. However, while stock markets have performed well with Central Bank interventions, economic prosperity is only slightly higher than it was prior to the turn of century.

Furthermore, despite the BOJ’s balance sheet consuming 80% of the ETF markets, not to mention a sizable chunk of the corporate and government debt market, Japan has been plagued by rolling recessions, low inflation, and low-interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time in recent years.)

Why is this important? Because Japan is a microcosm of what is happening in the U.S. As I noted previously:

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.

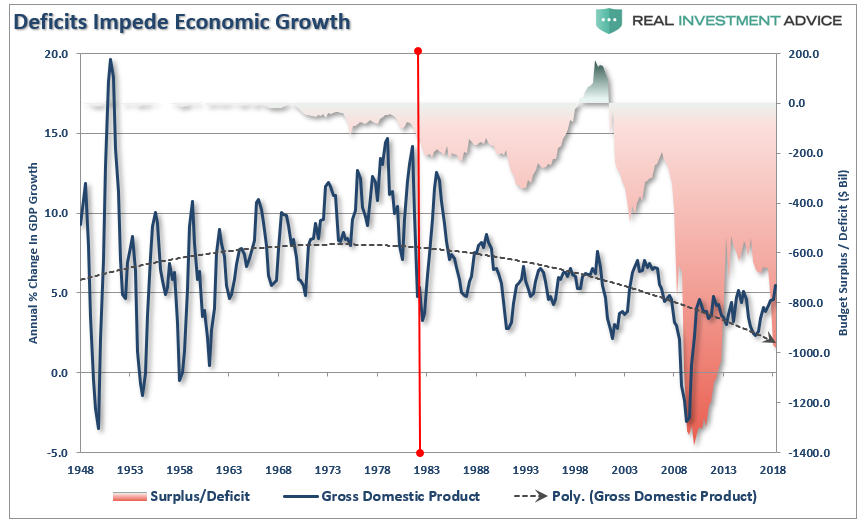

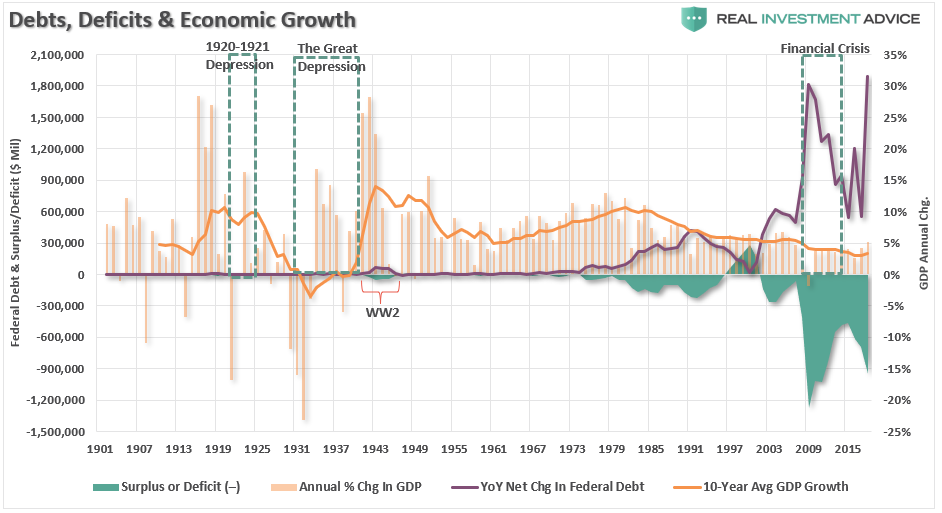

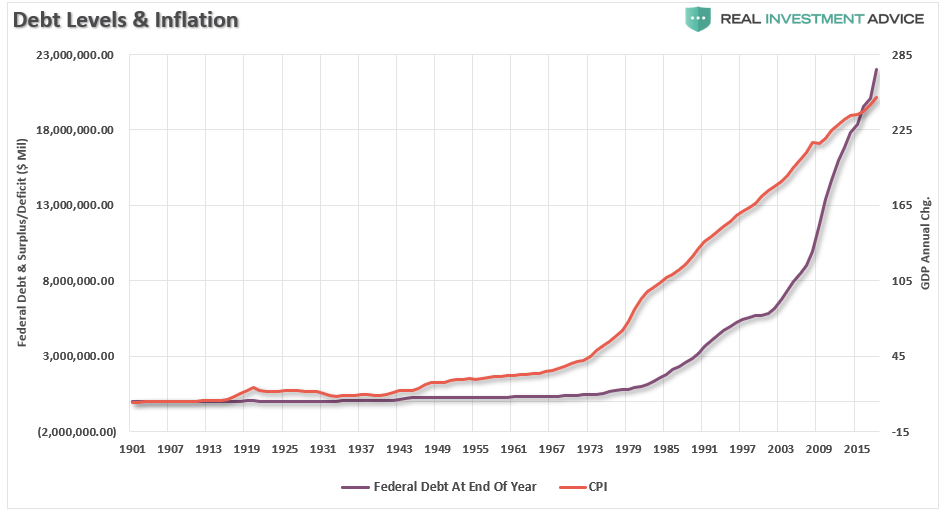

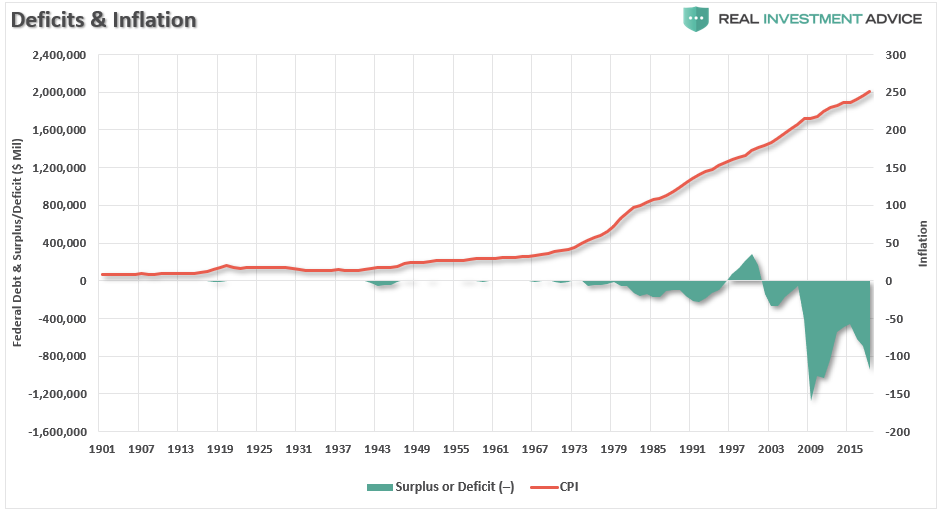

Most importantly, while there are many calling for an end of the ‘Great Bond Bull Market,’ this is unlikely the case. As shown in the chart below, interest rates are relative globally. Rates can’t increase in one country while a majority of economies are pushing negative rates. As has been the case over the last 30-years, so goes Japan, so goes the U.S.”

As my colleague Doug Kass recently noted, Japan is a template of the fragility of global economic growth.

“Global growth continues to slow and the negative impact on demand and the broad supply interruptions will likely expose the weakness of the foundation and trajectory of worldwide economic growth. This is particularly dangerous as the monetary ammunition has basically been used up.

As we have observed, monetary growth (and QE) can mechanically elevate and inflate the equity markets. For example, now in the U.S. market, basic theory is that in practice a side effect is that via the ‘repo’ market it is turned into leveraged trades into the equity markets. But, again, authorities are running out of bullets and have begun to question the efficacy of monetary largess.

Bigger picture takeaway is beyond the fact that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.

While financial engineering clearly props up asset prices, I think Japan is a very good example that financial engineering not only does nothing for an economy over the medium to longer-term, it actually has negative consequences.”

This is a key point.

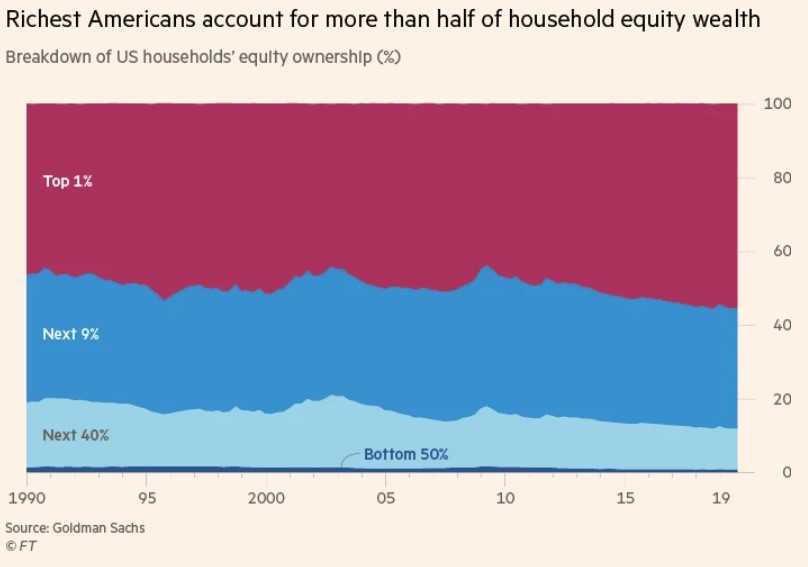

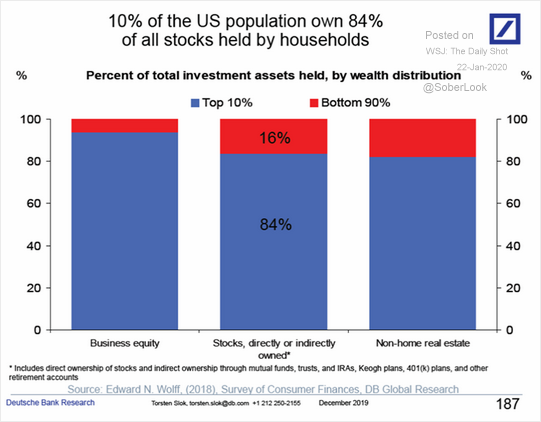

The “Stock Market” Is NOT The “Economy.”

Roughly 90% of the population gets little, or no, direct benefit from the rise in stock market prices.

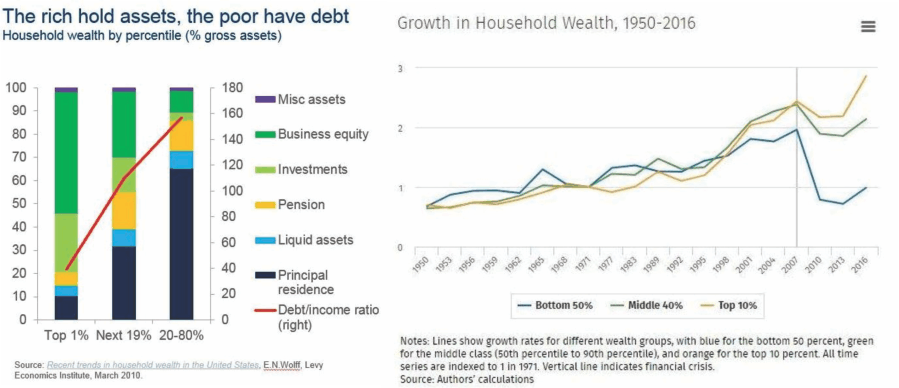

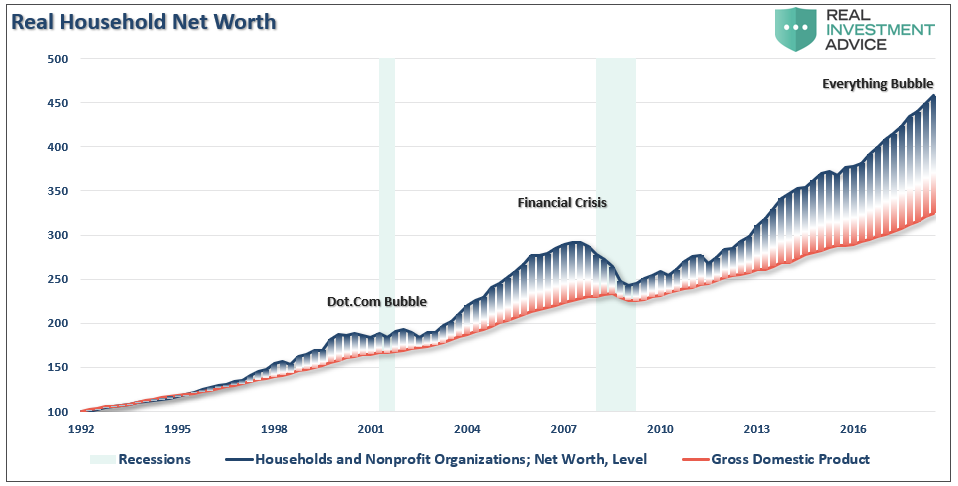

Another way to view this issue is by looking at household net worth growth between the top 10% to everyone else.

Since 2007, the ONLY group that has seen an increase in net worth is the top 10% of the population.

“This is not economic prosperity.

This is a distortion of economics.”

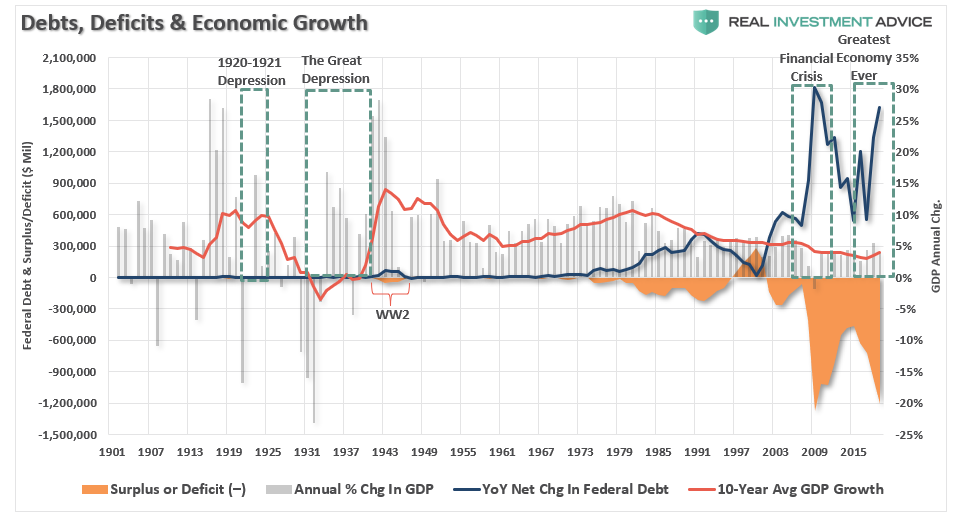

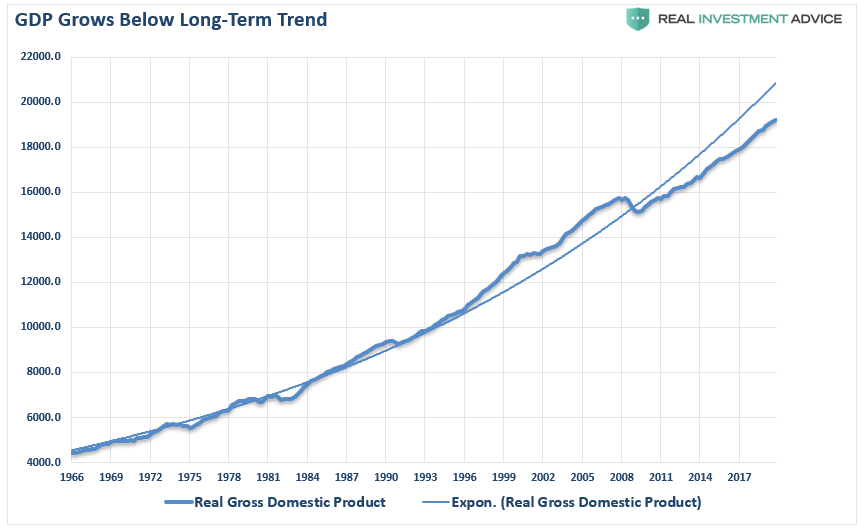

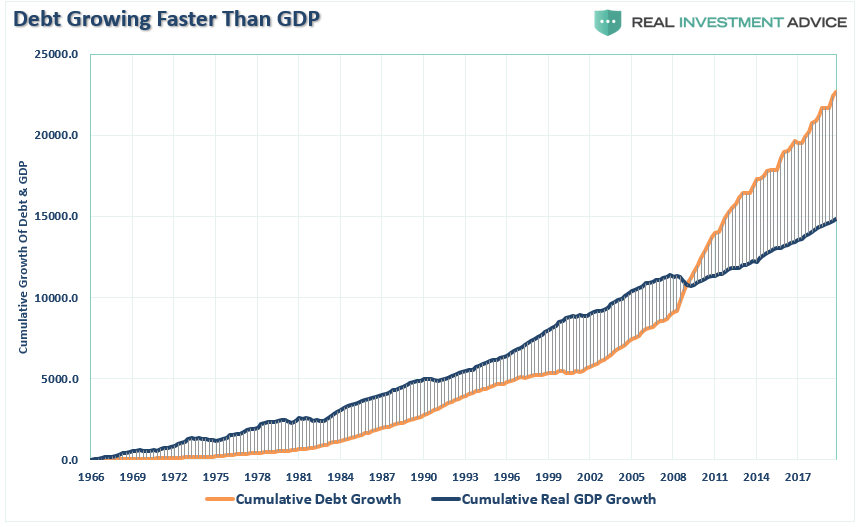

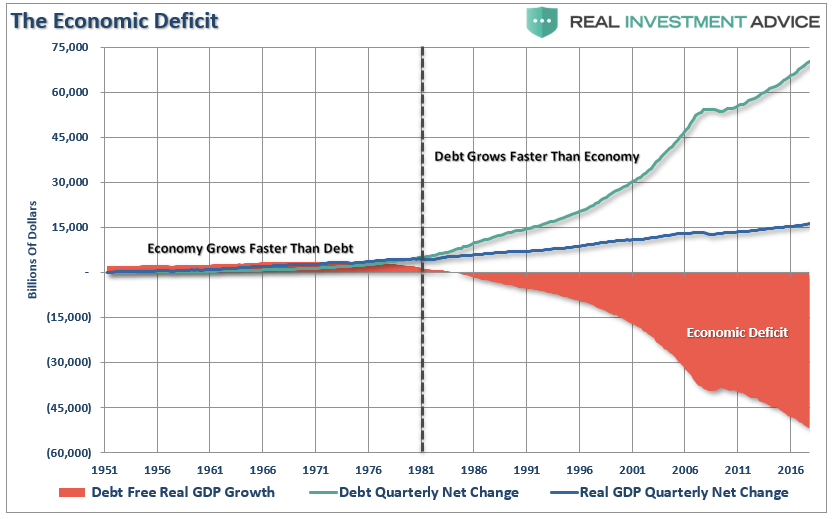

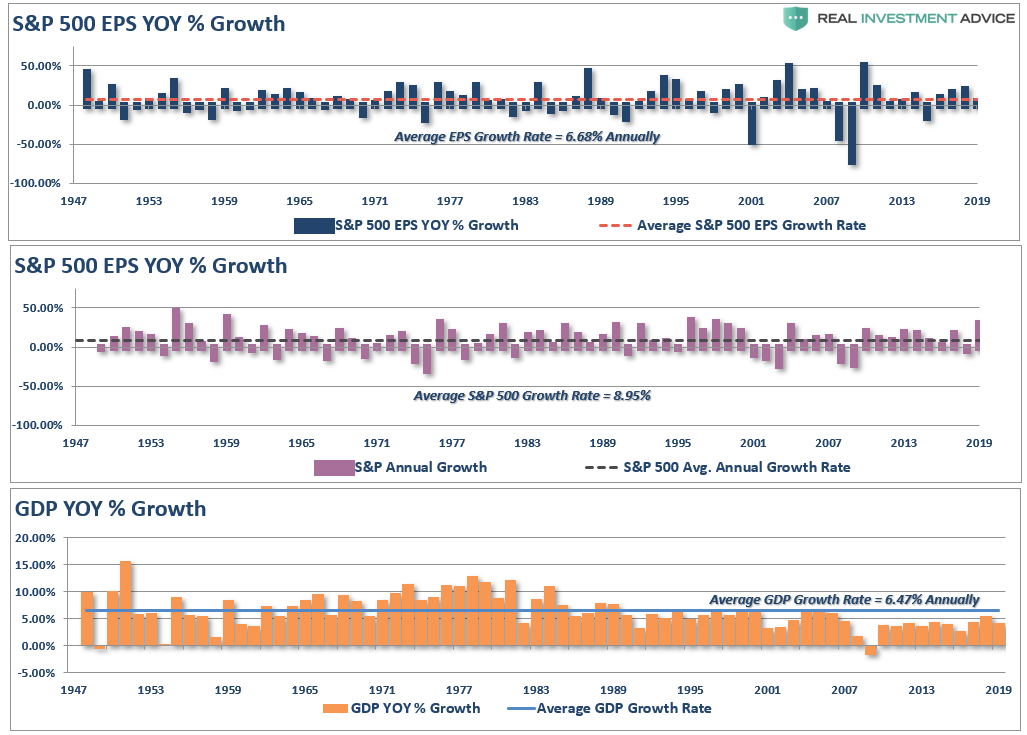

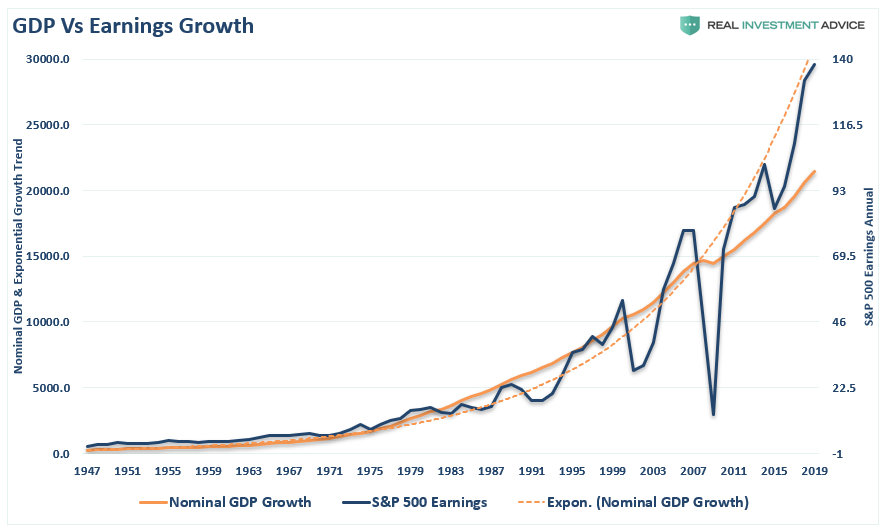

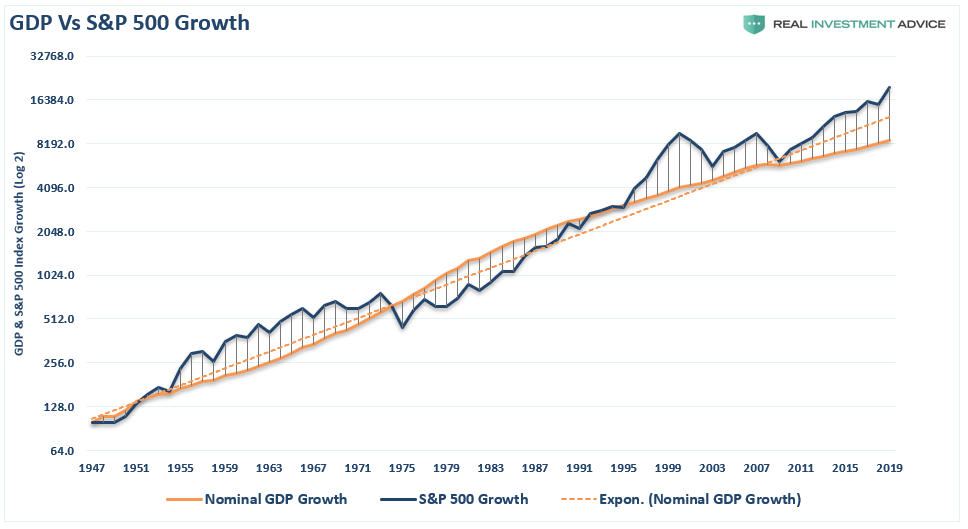

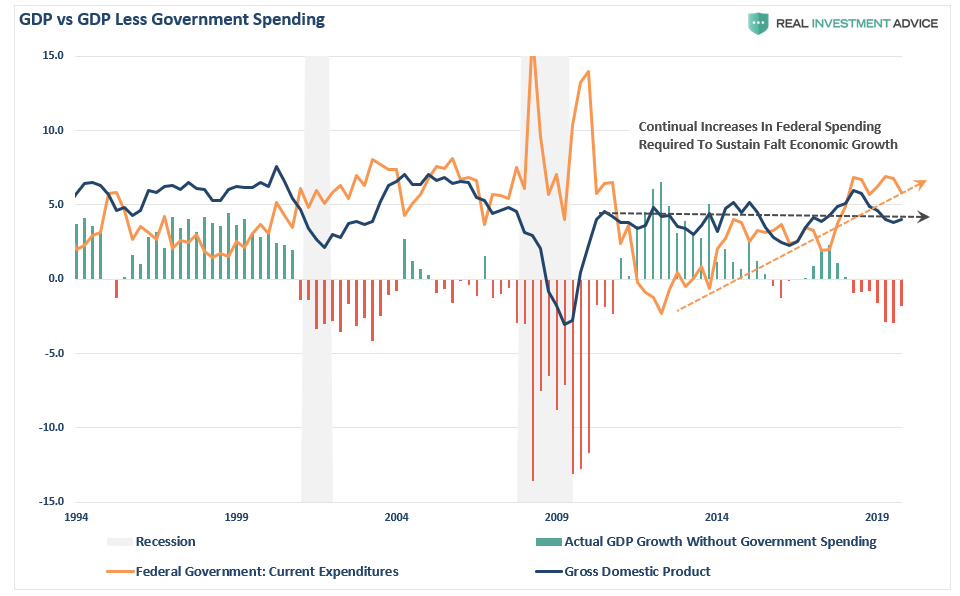

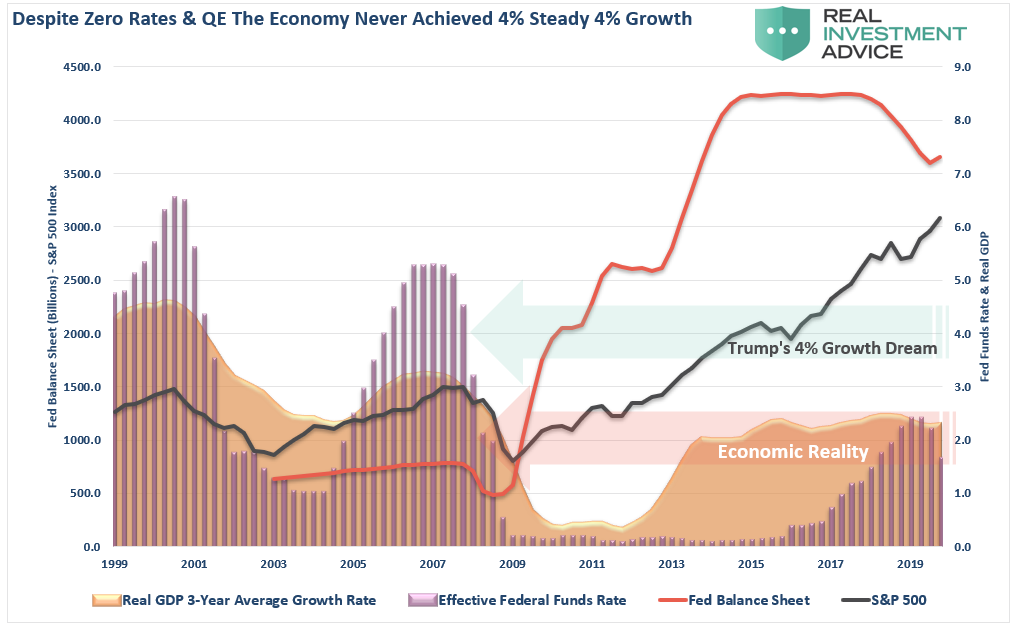

From 2009-2016, the Federal Reserve held rates at 0%, and flooded the financial system with 3-consecutive rounds of “Quantitative Easing” or “Q.E.” During that period, average real rates of economic growth rates never rose much above 2%.

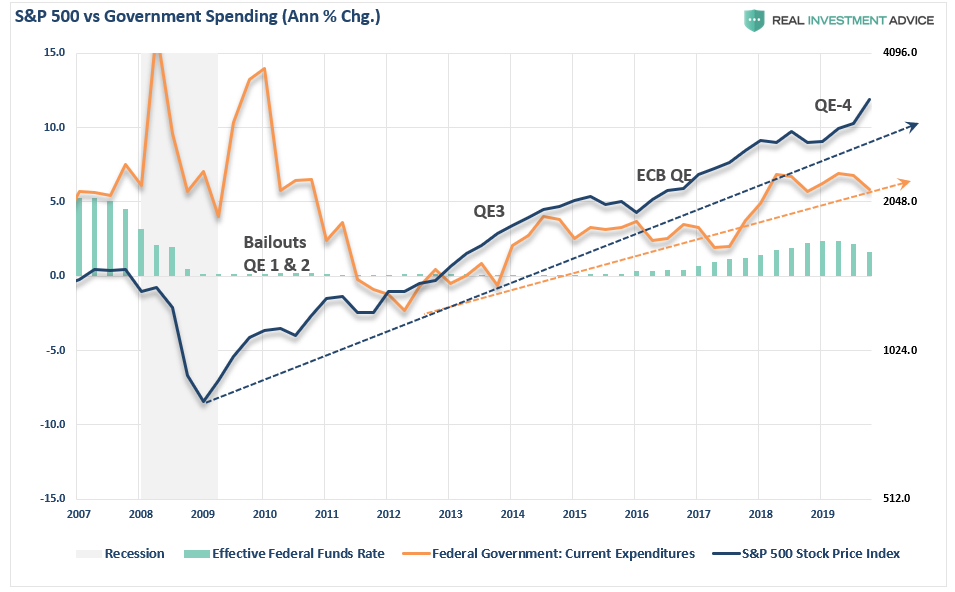

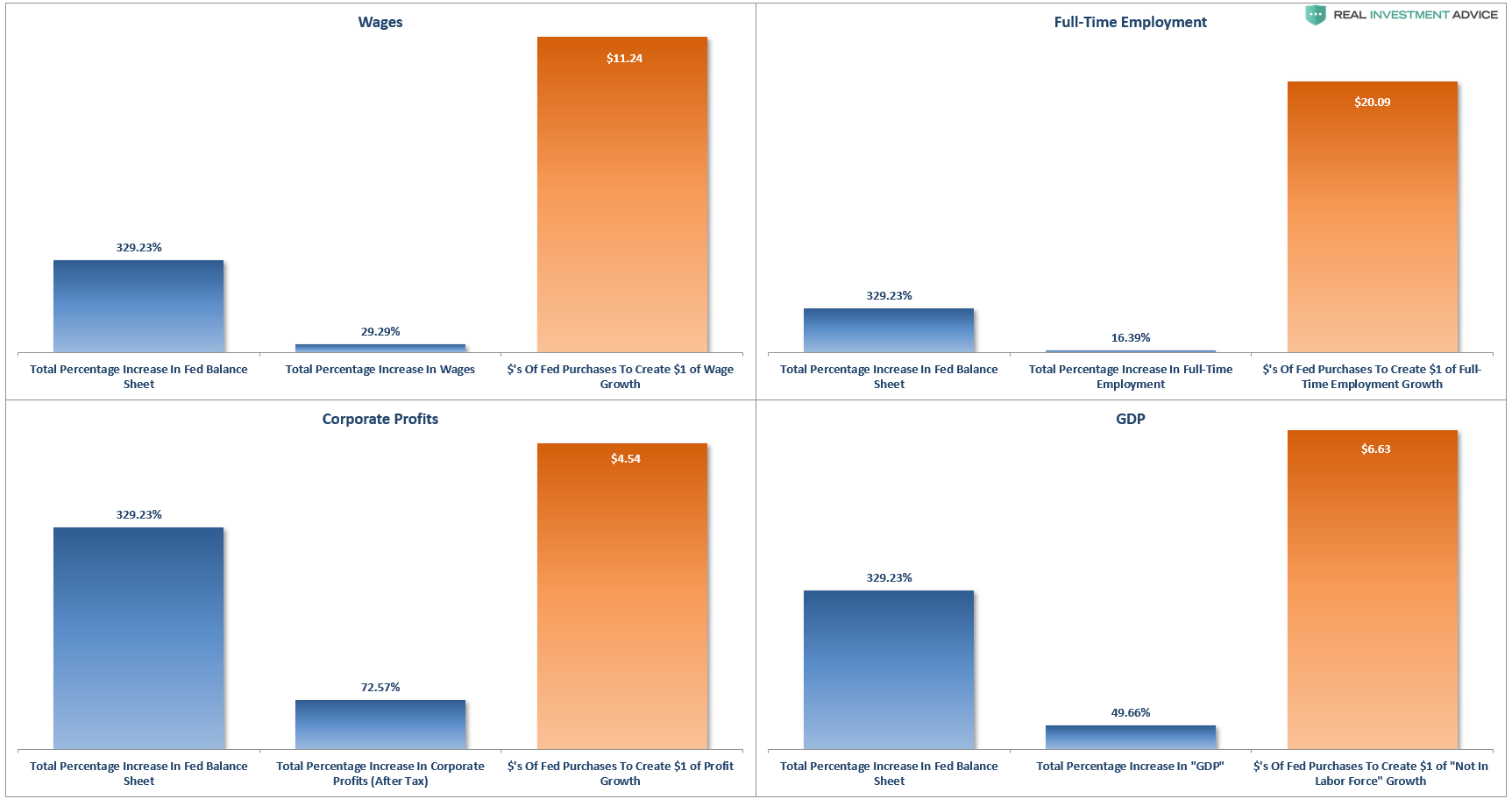

Yes, asset prices surged as liquidity flooded the markets, but as noted above “Q.E.” programs did not translate into economic activity. The two 4-panel charts below shows the entirety of the Fed’s balance sheet expansion program (as a percentage) and its relative impact on various parts of the real economy. (The orange bar shows now many dollars of increase in the Fed’s balance sheet that it took to create an increase in each data point.)

As you can see, it took trillions in “QE” programs, not to mention trillions in a variety of other bailout programs, to create a relatively minimal increase in economic data. Of course, this explains the growing wealth gap, which currently exists as monetary policy lifted asset prices.

The table above shows that QE1 came immediately following the financial crisis and had an effective ratio of about 1.6:1. In other words, it took a 1.6% increase in the balance sheet to create a 1% advance in the S&P 500. However, once market participants figured out the transmission system, QE2 and QE3 had an almost perfect 1:1 ratio of effectiveness. The ECB’s QE program, which was implemented in 2015 to support concerns of an unruly “Brexit,” had an effective ratio of 1.5:1. Not surprisingly, the latest round of QE, which rang “Pavlov’s bell,” has moved back to a near perfect 1:1 ratio.

Clearly, QE worked well in lifting asset prices, but as shown above, not so much for the economy. In other words, QE was ultimately a massive “wealth transfer” from the middle class to the rich which has created one of the greatest wealth gaps in the history of the U.S., not to mention an asset bubble of historic proportions.

But Will It Work Next Time?

This is the single most important question for investors.

The current belief is that QE will be implemented at the first hint of a more protracted downturn in the market. However, as suggested by the Fed, QE will likely only be employed when rate reductions aren’t enough. This was a point made in 2016 by David Reifschneider, deputy director of the division of research and statistics for the Federal Reserve Board in Washington, D.C., released a staff working paper entitled “Gauging The Ability Of The FOMC To Respond To Future Recessions.”

The conclusion was simply this:

“Simulations of the FRB/US model of a severe recession suggest that large-scale asset purchases and forward guidance about the future path of the federal funds rate should be able to provide enough additional accommodation to fully compensate for a more limited [ability] to cut short-term interest rates in most, but probably not all, circumstances.”

In other words, the Federal Reserve is rapidly becoming aware they have become caught in a liquidity trap keeping them unable to raise interest rates sufficiently to reload that particular policy tool. There are certainly growing indications the U.S. economy maybe be heading towards the next recession.

Interestingly, David compared three policy approaches to offset the next recession.

- Fed funds goes into negative territory but there is no breakdown in the structure of economic relationships.

- Fed funds returns to zero and keeps it there long enough for unemployment to return to baseline.

- Fed funds returns to zero and the FOMC augments it with additional $2-4 Trillion of QE and forward guidance.

In other words, the Fed is already factoring in a scenario in which a shock to the economy leads to additional QE of either $2 trillion, or in a worst case scenario, $4 trillion, effectively doubling the current size of the Fed’s balance sheet.

Does the Fed see a recession on the horizon? Is this why there are concerns about valuations?

Maybe.

But there is a problem with the entire analysis. The effectiveness of QE, and zero interest rates, is based on the point at which you apply these measures.

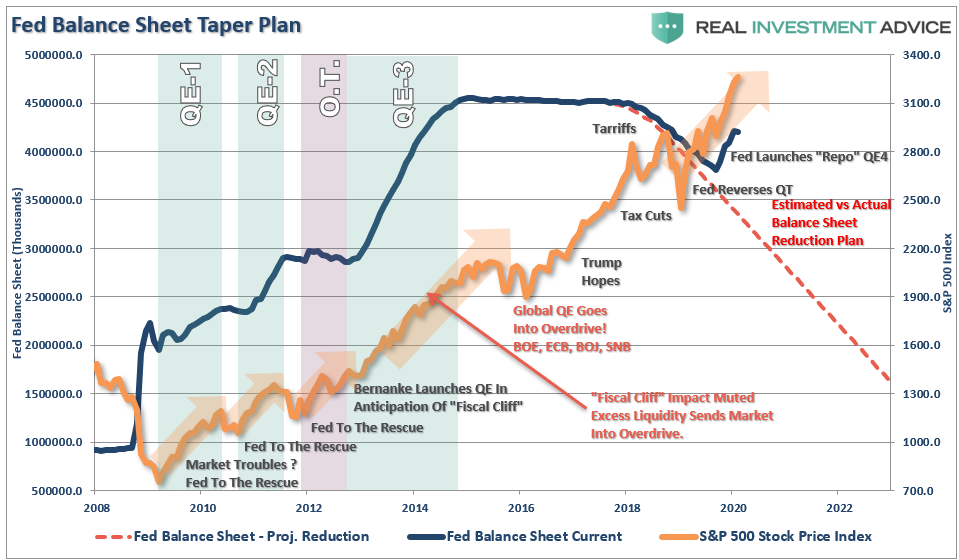

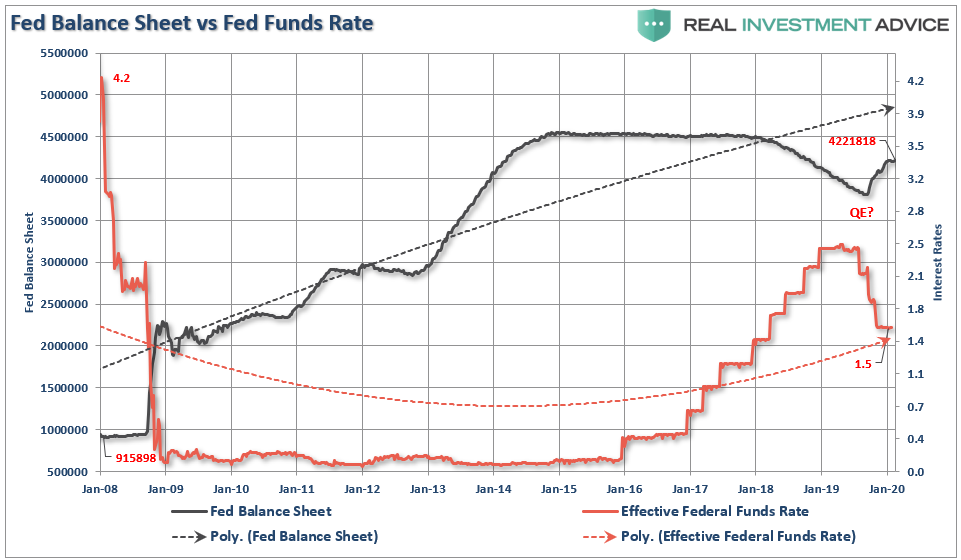

In 2008, when the Fed launched into their “accommodative policy” emergency strategy to bail out the financial markets, the Fed’s balance sheet was running at $915 Billion. The Fed Funds rate was at 4.2%.

If the market fell into a recession tomorrow, the Fed would be starting with a $4.2 Trillion balance sheet with interest rates 3% lower than they were in 2009. In other words, the ability of the Fed to ‘bail out’ the markets today, is much more limited than it was in 2008.”

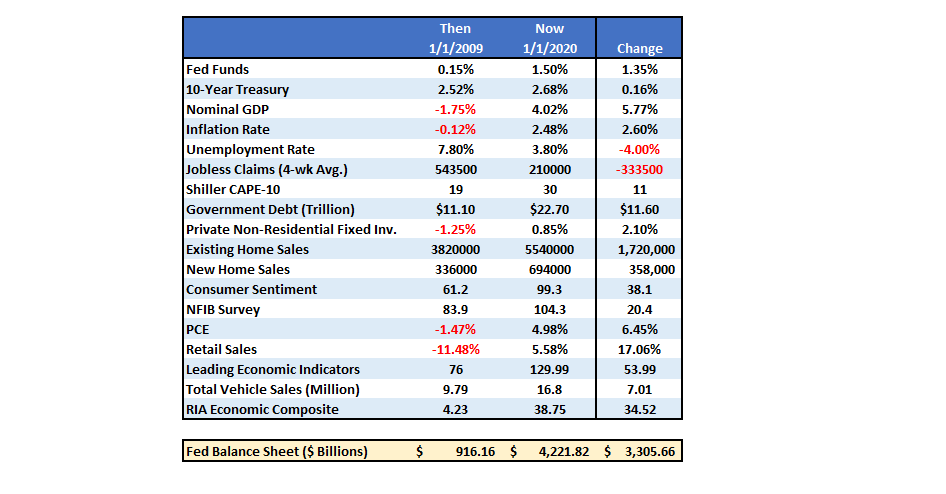

But there is more to the story than just the Fed’s balance sheet and funds rate. The entire backdrop is completely reversed. The table below compares a variety of financial and economic factors from 2009 to present.

Importantly, QE, and rate reductions, have the MOST effect when the economy, markets, and investors are extremely negative.

In other words, there is nowhere to go but up.

Such was the case in 2009. Not today.

This suggests that the Fed’s ability to stem the decline of the next recession, or offset a financial shock to the economy from falling asset prices, may be much more limited than the Fed, and most investors, currently believe.

Summary

It has taken a massive amount of interventions by Central Banks to keep economies afloat globally over the last decade, and there is rising evidence that growth is beginning to decelerate.

Furthermore, we have much more akin with Japan than many would like to believe.

- A decline in savings rates

- An aging demographic

- A heavily indebted economy

- A decline in exports

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

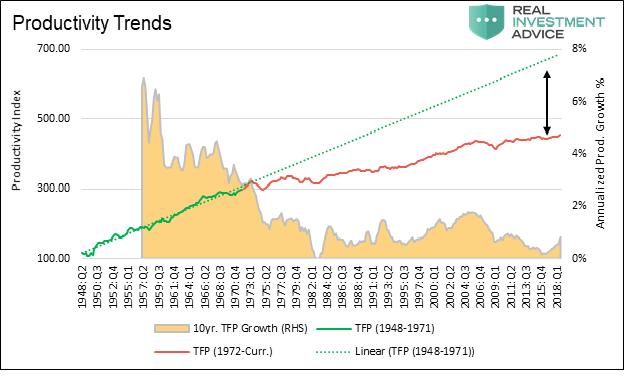

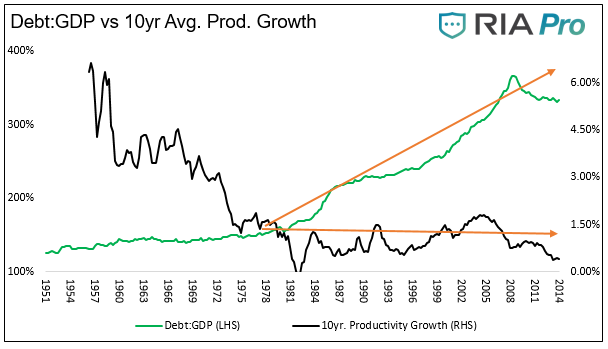

- Dependence on productivity increases

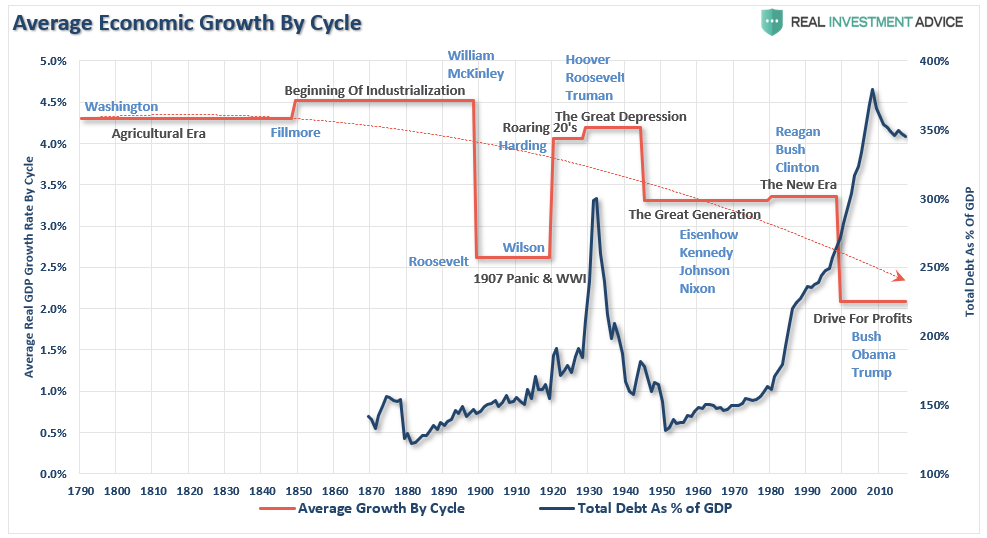

The lynchpin to Japan, and the U.S., remains demographics and interest rates. As the aging population grows becoming a net drag on “savings,” the dependency on the “social welfare net” will continue to expand. The “pension problem” is only the tip of the iceberg.

While another $2-4 Trillion in QE might indeed be successful in keeping the bubble inflated for a while longer, there is a limit to the ability to continue pulling forward future consumption to stimulate economic activity. In other words, there are only so many autos, houses, etc., which can be purchased within a given cycle. There is evidence the cycle peak has been reached.

If the effectiveness of rate reductions and QE are diminished due to the reasons detailed herein, the subsequent destruction to the “wealth effect” will be larger than currently imagined. The Fed’s biggest fear is finding themselves powerless to offset the negative impacts of the next recession.

If more “QE” works, great.

But as investors, with our retirement savings at risk, what if it doesn’t.