March 13, 2020 headline:

“After Worst Week Since 2008, What’s Next For The Stock Market?” , Benzinga March 13, 2020

Investors became conditioned to buy the dips after the record setting 2008 crash. The S&P 500 made a quick recovery after crashing down by 40% within six months to its lowest level since 1996 after Lehman declared bankruptcy in September 2008.

Those who jumped in the last time the markets had their worst week since 2008, the week ended February 28, 2020, lost 8.2% in 10 days based on the S&P 500’s March 13th close. Secular bear markets are famous for producing one sensational headline after another as a market continues to reach new lows.

February 28, 2020 headline:

“Wall Street has worst week since 2008 as S&P 500 drops 11.5%”, Associated Press February 28, 2020

From September 12, 2008, the last market close prior to Lehman’s bankruptcy to the bottom of the 2000 to 2009 secular bear market which began in 2000 and ended on March 9, 2009:

- Passive buy and hold investors lost 39%

- bullish traders who precisely got in at all bottoms and sold at tops made 136.5%

- bearish traders who precisely sold short at all tops and bought the shares back at all bottoms made 162.3%

What likely happened due to the extreme volatility as depicted in the chart below most non-professional traders lost money. Buy and hold bargain hunters who bought during the first five months after the 2008 crash began lost a minimum of 20%. From February 9, 2009, which was five months after the decline began, to the March 9th final bottom the market declined by an additional 22%.

The table below reinforces the difficulties that anyone but a professional investor had to make money from the 2008 crash. $100 traded from September 12th to March 2009, would have declined to $74.20 at the 2000 secular bear’s final bottom.

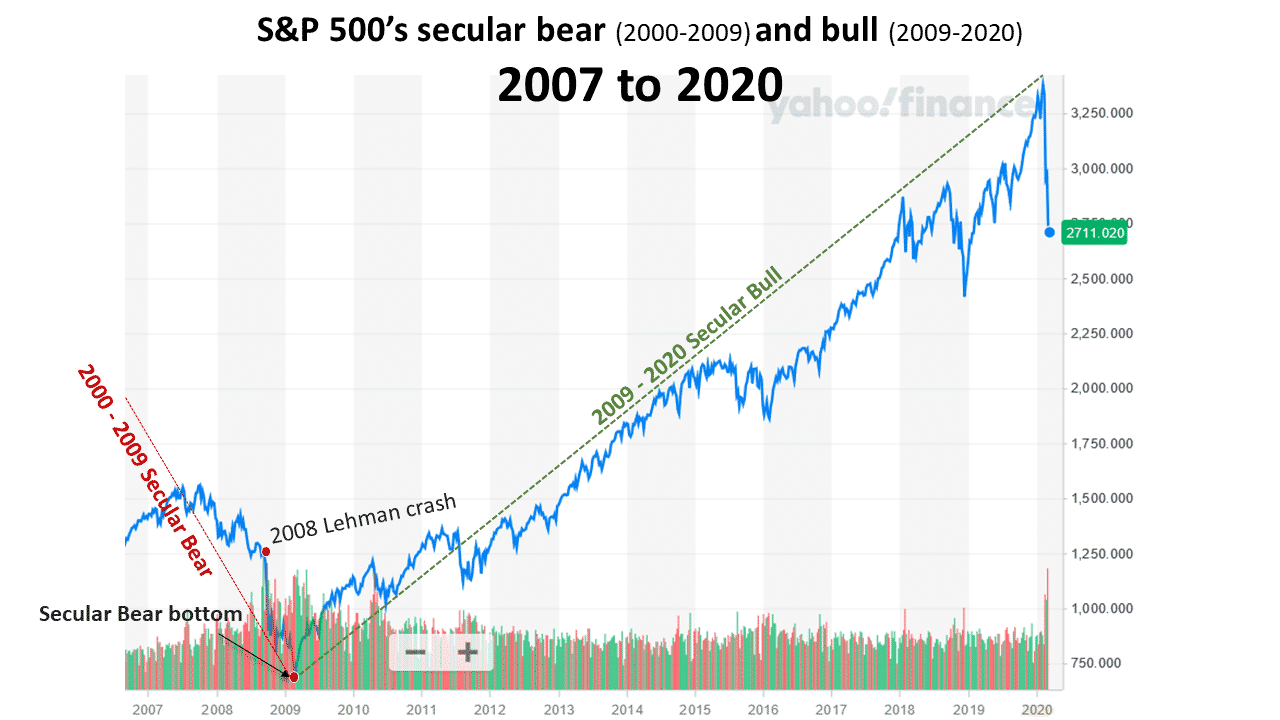

The current market is much riskier than the 2008 market for dip buying. Instead of being at the bottom of secular bear, the chart below depicts that the S&P 500 has been in a secular bull market since 2009. In my March 5th article when the S&P 500 was 10% higher included my prediction that the secular bull likely reached its all-time high on February 19, 2020 and the secular bear began the very next day on February 20, 2020.

Based on my recent empirical research findings from analyzing prior crashes which have similar traits as the crash of 2020, the probability is high that the decline from the top to the bottom will be from 79% to 89%. The final bottom will be reached between October and December of 2022.

BullsNBears.com which covers all of the emerging and declining economic and market trends is an excellent resource site. Click here to view one-minute video about the site.