The question repeatedly asked of us last week is how much more can the stock market fall? We don’t have a crystal ball and we cannot predict the future but we can take steps to prepare for it. Our analysis and understanding of history allow us to use many different fundamental and technical models to create a broad range of possible answers to the question. With that range of potential outcomes we adjust our risk tolerance as appropriate.

For example, in our daily series of RIA Pro charts and the weekly Newsletter, we lay out key technical, sentiment, and momentum measures for many markets, sectors, and stocks. In doing so, we provide a range of potential shorter-term outcomes. We also depend on feedback from other reliable independent services such as Brett Freeze at Global Technical Analysis. His work is exclusively and routinely featured every month in Cartography Corner on RIA Pro.

In this article, we move beyond technical analysis and share a simple fundamental valuation analysis to help provide more guidance as to where the market may trade in the coming months and even years. This analysis can be viewed as bullish or bearish. Our goal is not to persuade you towards one direction or the other, but to open your eyes to the wide range of possibilities.

CAPE

The data employed in this analysis is as of the market close on March 13, 2020.

Shiller’s Cyclically Adjusted Price to Earnings (CAPE 10) is one of our preferred valuation measures. Robert Shiller developed the CAPE 10 model to help investors assess valuations based on dependable, longer-term earnings trends. The most common CAPE analysis uses ten years of earnings data. The period is not too sensitive to transitory gyrations in earnings and it frequently includes a full economic cycle.

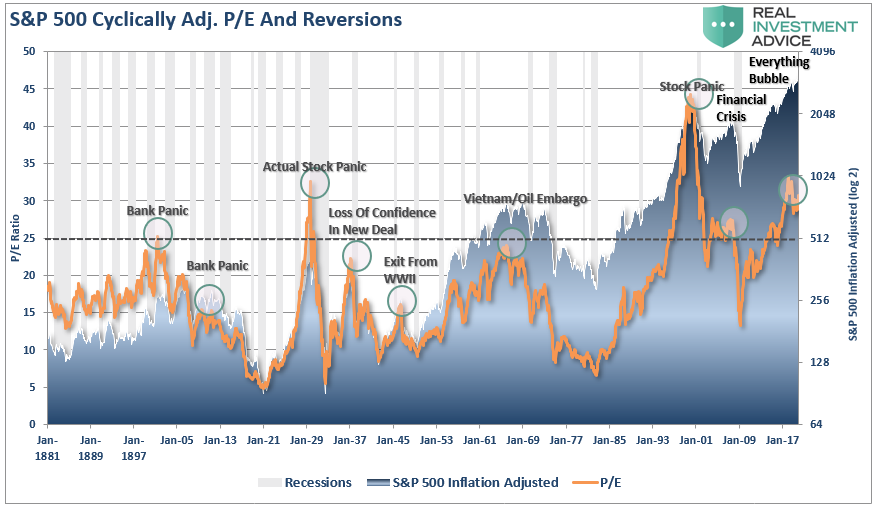

As shown below, monthly readings of CAPE fluctuate around the historical average (dotted line). The variance of valuations around the mean is put into further context with the right side y-axis, which shows how many sigma’s (standard deviations) each reading is from the average. The current CAPE of 25.36, or +1.10 sigma’s from the mean.

Data Courtesy Robert Shiller

The average CAPE over the 120+ years is 17.06, the maximum was 44.20, and the minimum was 4.78.

If we use more recent data, say from 1980 to current, the average CAPE is 22.29. Due to the higher average over the period, which includes the late 90s dot com bubble and the housing bubble, the current reading is only .36 sigma’s above its average.

The following tables, using both time frames, provide price guidance based on where the S&P 500 would need to be if CAPE were to move to its average, maximum, and minimum, as well as plus or minus one sigma from the mean.

The graph below shows the S&P 500 price in relation to that which would occur if the CAPE ratio went to its average, maximum, minimum, and plus or minus one sigma from the last 120 years.

It is important to stress that the denominator, earnings, includes data from March 2010 to February 2020. That ten years did not include a recession, which, over the 120+ years in this analysis, only happened briefly one other time, the late 1990’s.

The Corona Virus will no doubt hurt earnings for at least a few quarters and could push the economy into a recession. Accordingly, the denominator in CAPE will likely be declining. Whether or not CAPE rises for falls depends on the price action of the index.

Summary

Stocks are not cheap. As shown, a reversion to the average of the last 120 years, would result in an additional 33% decline from current levels. While the massive range of outcomes may appear daunting, this analysis is designed to help better understand the bounds of the market.

The S&P 500 certainly has room to trade much lower. It can also double in price and stay within the bounds of history. Lastly, given the unprecedented nature of current circumstances, it may be different this time and write new history.

Market Bubbles: It’s Not The Price, It’s The Mentality.

“Actually, one of the dangers is that people could be throwing risk to the wind and this [market] could be a runaway. We sometimes call that a melt-up and produces prices too high and then if there’s a shock, you come down to Earth and that could impact sentiment. I think this market is fully valued and not undervalued, but I don’t think it’s overvalued,” – Jeremy Siegel

Here is an interesting thing.

“Market bubbles have NOTHING to do with valuations or fundamentals.”

Hold on…don’t start screaming “heretic,” and building gallows just yet.

Let me explain.

I can’t entirely agree with Siegel on the market being “fairly valued.” As shown in the chart below, the S&P 500 is currently trading nearly 90% above its long-term median, which is expensive from a historical perspective.

However, since stock market “bubbles” are a reflection of speculation, greed, emotional biases; valuations are only a reflection of those emotions.

In other words, bubbles can exist even at times when valuations and fundamentals might argue otherwise. Let me show you an elementary example of what I mean. The chart below is the long-term valuation of the S&P 500 going back to 1871.

Notice that with the exception of only 1929, 2000, and 2007, every other major market crash occurred with valuations at levels LOWER than they are currently.

Secondly, all market crashes have been the result of things unrelated to valuation levels such as liquidity issues, government actions, monetary policy mistakes, recessions, or inflationary spikes. Those events were the catalyst, or trigger, that started the “reversion in sentiment” by investors.

For Every Buyer

You will commonly hear that “for every buyer, there must be a seller.”

This is a true statement. The issue becomes at “what price.” What moves prices up and down, in a normal market environment, is the price level at which a buyer and seller complete a transaction.

Market crashes are an “emotionally” driven imbalance in supply and demand.

In a market crash, the number of people wanting to “sell” vastly overwhelms the number of people willing to “buy.” It is at these moments that prices drop precipitously as “sellers” drop the levels at which they are willing to dump their shares in a desperate attempt to find a “buyer.” This has nothing to do with fundamentals. It is strictly an emotional panic, which is ultimately reflected by a sharp devaluation in market fundamentals.

Bob Bronson once penned:

“It can be most reasonably assumed that markets are sufficient enough that every bubble is significantly different than the previous one, and even all earlier bubbles. In fact, it’s to be expected that a new bubble will always be different than the previous one(s) since investors will only bid up prices to extreme overvaluation levels if they are sure it is not repeating what led to the last, or previous bubbles. Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular – like now – it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes in the future, even if the previous accident-causing mistakes are avoided.”

Comparing the current market to any previous period in the market is rather pointless. The current market is not like 1995, 1999, or 2007? Valuations, economics, drivers, etc. are all different from cycle to the next. Most importantly, however, the financial markets adapt to the cause of the previous “fatal crashes,” but that adaptation won’t prevent the next one.

It’s All Relative

Last week, in our MacroView, I touched on George Soros’ theory on bubbles, which is worth expanding a bit on in the context of this article.

“Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time. Sometimes it’s quite insignificant, at other times it is quite pronounced. When there is a significant divergence between market prices and the underlying reality, the markets are far from equilibrium conditions.

Every bubble has two components:

An underlying trend that prevails in reality, and;

A misconception relating to that trend.

When positive feedback develops between the trend and the misconception, a boom-bust process is set into motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception will be reinforced. Eventually, market expectations become so far removed from reality that people are forced to recognize that a misconception is involved. A twilight period ensues during which doubts grow, and more people lose faith, but the prevailing trend is sustained by inertia.

As Chuck Prince, former head of Citigroup, said, ‘As long as the music is playing, you’ve got to get up and dance. We are still dancing.’ Eventually, a tipping point is reached when the trend is reversed; it then becomes self-reinforcing in the opposite direction.”

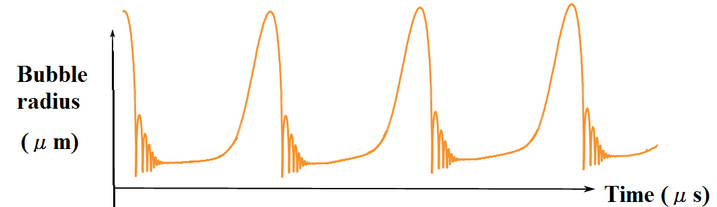

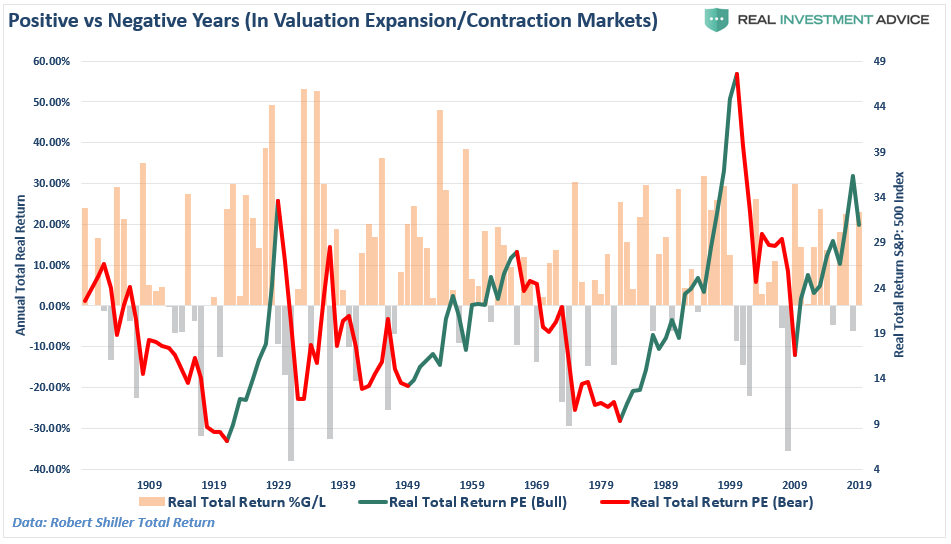

Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.

The chart below is an example of asymmetric bubbles.

The pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market, which can create a feedback loop between the markets and fundamentals.

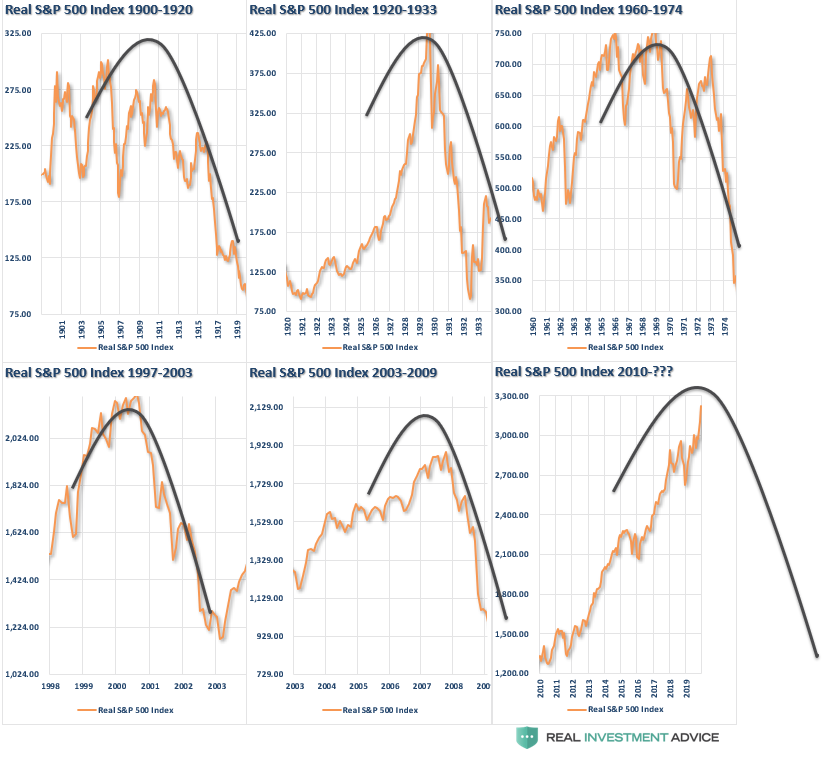

This pattern of bubbles can be seen at every bull market peak in history. The chart below utilizes Dr. Robert Shiller’s stock market data going back to 1900 on an inflation-adjusted basis with an overlay of the asymmetrical bubble shape.

As Soro’s went on to state:

“Financial markets do not play a purely passive role; they can also affect the so-called fundamentals they are supposed to reflect. These two functions, that financial markets perform, work in opposite directions.

In the passive or cognitive function, the fundamentals are supposed to determine market prices.

In the active or manipulative function market, prices find ways of influencing the fundamentals.

When both functions operate at the same time, they interfere with each other. The supposedly independent variable of one function is the dependent variable of the other, so that neither function has a truly independent variable. As a result, neither market prices nor the underlying reality is fully determined. Both suffer from an element of uncertainty that cannot be quantified.”

Currently, there is a strong belief the financial markets are not in a bubble, and the arguments supporting that belief are based on comparisons to past market bubbles.

It is likely that in a world where there is virtually “no fear” of a market correction, an overwhelming sense of “urgency” to be invested, and a continual drone of “bullish chatter;” the markets are poised for the unexpected, unanticipated, and inevitable event.

Reflections

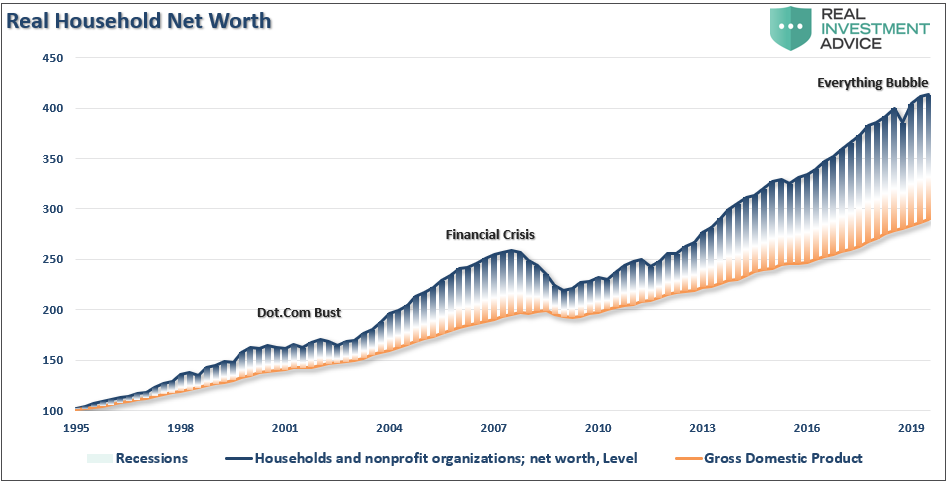

When thinking about excess, it is easy to see the reflections of excess in various places. Not just in asset prices but also in “stuff.” All financial assets are just claims on real wealth, not actual wealth itself. A pile of money has use and utility because you can buy stuff with it. But real wealth is the “stuff” — food, clothes, land, oil, and so forth. If you couldn’t buy anything with your money/stocks/bonds, their worth would revert to the value of the paper they’re printed on (if you’re lucky enough to hold an actual certificate).

But trouble begins when the system gets seriously out of whack.

“GDP” is a measure of the number of goods and services available and financial asset prices represent the claims (it’s not a very accurate measure of real wealth, but it’s the best one we’ve got.) Notice the divergence of asset prices from GDP as excesses develop.

What we see is that the claims on the economy should, quite intuitively, track the economy itself. Excesses occur whenever the claims on the economy, the so-called financial assets (stocks, bonds, and derivatives), get too far ahead of the economy itself.

This is a very important point.

“The claims on the economy are just that: claims. They are not the economy itself!”

Take a step back from the media, and Wall Street commentary, for a moment and make an honest assessment of the financial markets today.

The increase in speculative risks, combined with excess leverage, leave the markets vulnerable to a sizable correction at some point in the future. The only missing ingredient for such a correction is the catalyst to bring “fear” into an overly complacent marketplace.

It is all reminiscent of the market peak of 1929 when Dr. Irving Fisher uttered his now famous words: “Stocks have now reached a permanently high plateau.”

This “time IS different.”

However, “this time” is only different from the standpoint the variables are not exactly the same as they have been previously. The variables never are, but the outcome is always the same.

The Next Decade: Valuations & The Destiny Of Low Returns

Jani Ziedins via Cracked Market recently penned an interesting post:

“As for what comes next, is this bull market tired? Is a crash long overdue? Not if you look at history. Stocks rallied for nearly 20 years between the early 1980s and the late 1990s. By that measure, we could easily see another decade of strong gains before the next “Big One”. Of course, the worst day in stock market history happened during that 20-year bull market in 1987, so we cannot be complacent. But the prognosis for the next 10 years is still good even if we run into a few 20% corrections along the way.”

After a decade of strong, liquidity-driven, post-crisis returns in the financial markets, investors are hopeful the next decade will deliver the same, or better. As Bob Farrell once quipped:

“Bull markets are more fun than bear markets.”

However, from an investment standpoint, the real question is:

“Can the next decade deliver above average returns, or not?”

Lower Returns Ahead?

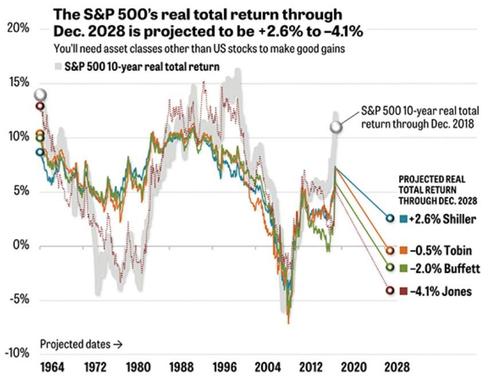

Brian Livingston, via MarketWatch, previously wrote an article on the subject of valuation measures and forward returns.

“Stephen Jones, a financial and economic analyst who works in New York City, tracks the formulas that several market wizards have disclosed. He recently updated his numbers through Dec. 31, 2018, and shared them with me. Buffett, Shiller, and the other boldface names had nothing to do with Jones’s calculations. He crunched the financial celebrities’ formulas himself, based on their public statements.”

“The graph above doesn’t show the S&P 500’s price levels. Instead, it reveals how well the projection methods estimated the market’s 10-year rate of return in the past. The round markers on the right are the forecasts for the 10 years that lie ahead of us. All of the numbers for the S&P 500 include dividends but exclude the consumer-price index’s inflationary effect on stock prices.”

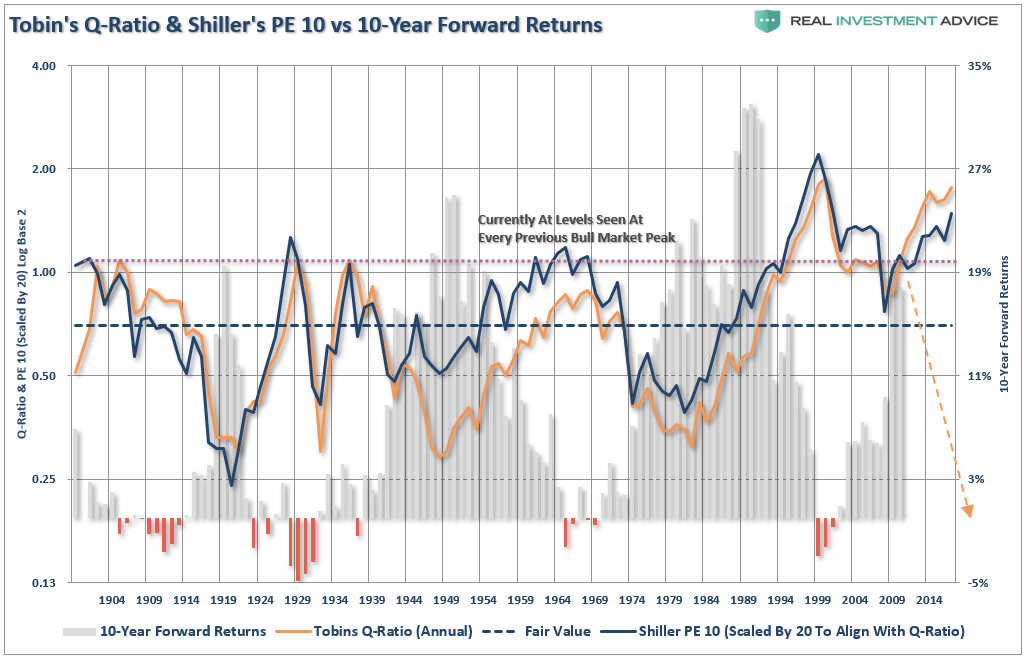

Shiller’s P/E10 predicts a +2.6% annualized real total return.

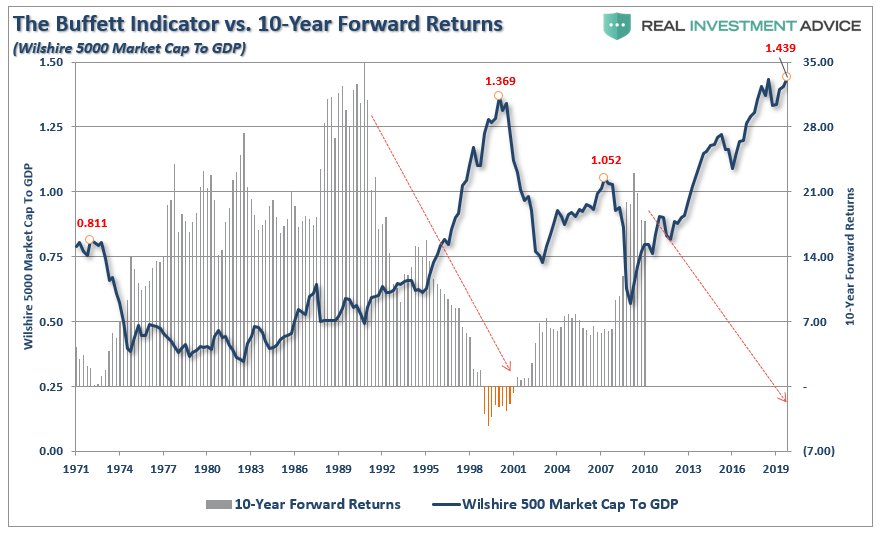

Buffett’s MV/GDP says -2.0%.

Tobin’s “q” ratio indicates -0.5%.

Jones’s Composite says -4.1%.

(Jones uses Buffett’s formula but adjusts for demographic changes.)

Here is the important point:

“The predictions might seem far apart, but they aren’t. The forecasts are all much lower than the S&P 500’s annualized real total return of about 6% from 1964 through 2018.”

While these are not guarantees, and should never be used to try and “time the market,” they are historically strong predictors of future returns.

As Jones notes:

“The market’s return over the past 10 years,” Jones explains, “has outperformed all major forecasts from 10 years prior by more than any other 10-year period.”

Of course, as noted above, this is due to the unprecedented stimulation the Federal Reserve pumped into the financial markets. Regardless, markets have a strong tendency to revert to their average performance over time, which is not nearly as much fun as it sounds.

The late Jack Bogle, founder of Vanguard, also noted some concern from high valuations:

“The valuations of stocks are, by my standards, rather high, butmy standards, however, are high.”

When considering stock valuations, Bogle’s method differs from Wall Street’s. For his price-to-earnings multiple, Bogle uses the past 12-months of reported earnings by corporations, GAAP earnings, which includes “all of the bad stuff.”Wall Street analysts look at operating earnings, “earnings without all that bad stuff,” and come up with a price-to-earnings multiple of something in the range of 17 or 18, versus current real valuations which are pushing nearly 30x earnings.

“If you believe the way we look at it, much more realistically I think, the P/E is relatively high. I believe strongly that [investors] should be realizing valuations are fairly full, and if they are nervous they could easily sell off a portion of their stocks.” – Jack Bogle

These views are vastly different than the optimistic views currently being bantered about for the next decade.

However, this is where an important distinction needs to be made.

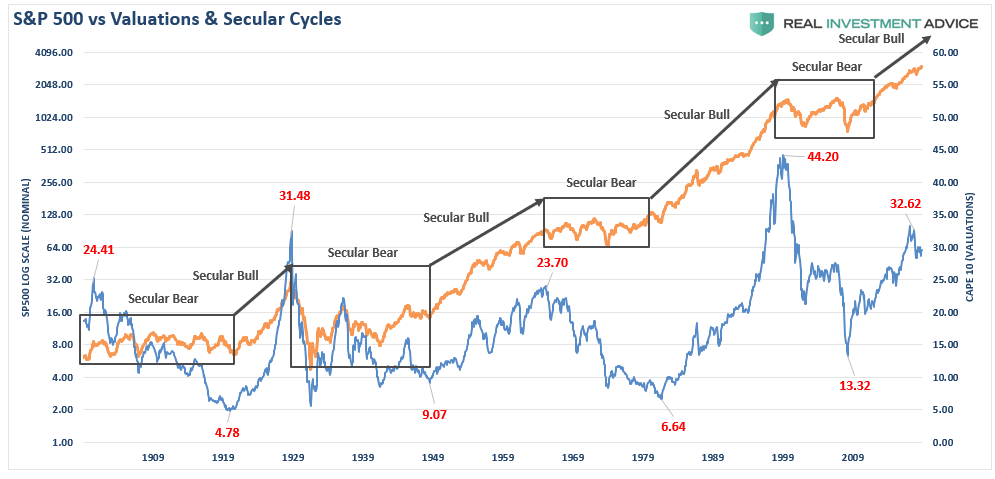

Starting Valuations Matter Most

What Jani Ziedins missed in his observation was the starting level of valuations which preceded those 20-year “secular bull markets.” This was a point I made previously:

“The chart below shows the history of secular bull market periods going back to 1871 using data from Dr. Robert Shiller. One thing you will notice is that secular bull markets tend to begin with CAPE 10 valuations around 10x earnings or even less. They tend to end around 23-25x earnings or greater. (Over the long-term valuations do matter.)”

The two previous 20-year secular bull markets begin with valuations in single digits. At the end of the first decade of those secular advances, valuations were still trading below 20x.

The 1920-1929 secular advance most closely mimics the current 2010 cycle. While valuations started below 5x earnings in 1919, they eclipsed 30x earnings ten-years later in 1929. The rest, as they say, is history. Or rather, maybe “past is prologue” is more fitting.

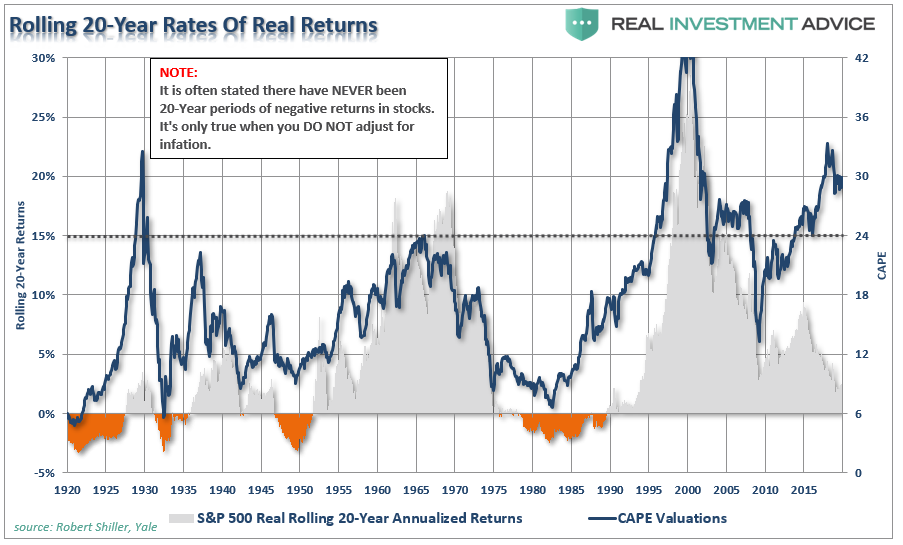

Low Returns Mean High Volatility

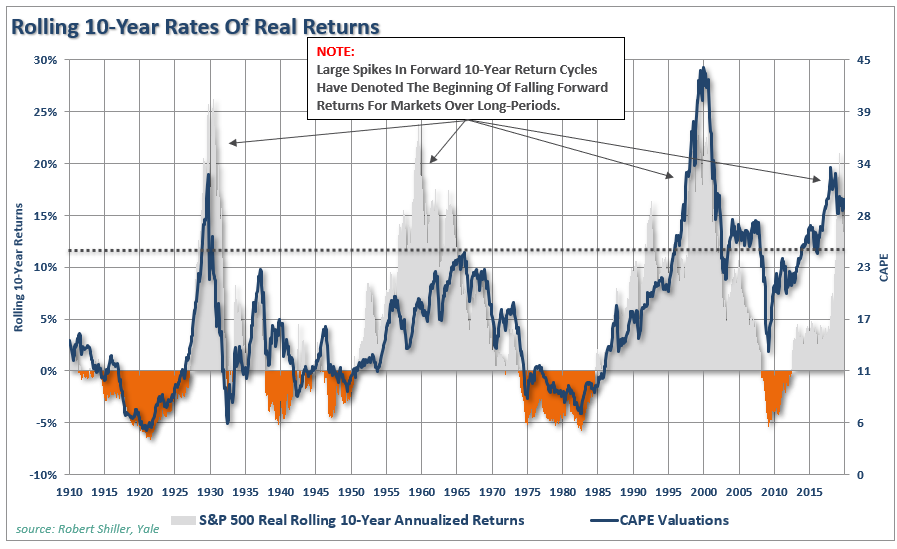

When low future rates of return are discussed, it is not meant that each year will be low, but rather the return for the entire period will be low. The chart below shows 10-year rolling REAL, inflation-adjusted, returns in the markets. (Note: Spikes in 10-year returns, which occurred because the 50% decline in 2008 dropped out of the equation, has previously denoted peaks in forward annual returns.)

(Important note:Many advisers/analysts often pen that the market has never had a 10 or 20-year negative return. That is only on a nominal basis and should be disregarded as inflation must be included in the debate.)

There are two important points to take away from the data.

There are several periods throughout history where market returns were not only low, but negative.(Given that most people only have 20-30 functional years to save for retirement, a 20-year low return period can devastate those plans.)

Periods of low returns follow periods of excessive market valuations and encompass the majority of negative return years. (Read more about this chart here)

“Importantly, it is worth noting that negative returns tend to cluster during periods of declining valuations. These ‘clusters’ of negative returns are what define ‘secular bear markets.’”

While valuations are often dismissed in the short-term because there is not an immediate impact on price returns. Valuations, by their very nature, are HORRIBLE predictors of 12-month returns and should never be used in any investment strategy which has such a focus. However, in the longer term, valuations are strong predictors of expected returns.

The chart below shows Dr. Robert Shiller’s cyclically adjusted P/E ratio combined with Tobin’s Q-ratio. Again, valuations only appear cheap when compared to the peak in 2000. Outside of that exception, the financial markets are, without question, expensive.

Furthermore, note that forward 10-year returns do NOT improve from historically expensive valuations, but decline rather sharply.

Warren Buffett’s favorite valuation measure is also screaming valuation concerns (which may explain why he is sitting on $128 billion in cash.). The following measure is the price of the Wilshire 5000 market capitalization level divided by GDP. Again, as noted above, asset prices should be reflective of underlying economic growth rather than the “irrational exuberance” of investors.

Again, with this indicator at the highest valuation level in history, it is a bit presumptuous to assume that forward returns will continue to remain elevated,.

Bull Now, Pay Later

In the short-term, the bull market continues as the flood of liquidity, and accommodative actions, from global Central Banks, has lulled investors into a state of complacency rarely seen historically. As Richard Thaler, the famous University of Chicago professor who won the Nobel Prize in economics stated:

“We seem to be living in the riskiest moment of our lives, and yet the stock market seems to be napping. I admit to not understanding it.

I don’t know about you, but I’m nervous, and it seems like when investors are nervous, they’re prone to being spooked. Nothing seems to spook the market.”

While market analysts continue to come up with a variety of rationalizations to justify high valuations, none of them hold up under real scrutiny. The problem is the Central Bank interventions boost asset prices in the short-term, in the long-term, there is an inherently negative impact on economic growth. As such, it leads to the repetitive cycle of monetary policy.

Using monetary policy to drag forward future consumption leaves a larger void in the future that must be continually refilled.

Monetary policy does not create self-sustaining economic growth and therefore requires ever larger amounts of monetary policy to maintain the same level of activity.

The filling of the “gap” between fundamentals and reality leads to consumer contraction and ultimately a recession as economic activity recedes.

Job losses rise, wealth effect diminishes and real wealth is destroyed.

Middle class shrinks further.

Central banks act to provide more liquidity to offset recessionary drag and restart economic growth by dragging forward future consumption.

Wash, Rinse, Repeat.

If you don’t believe me, here is the evidence.

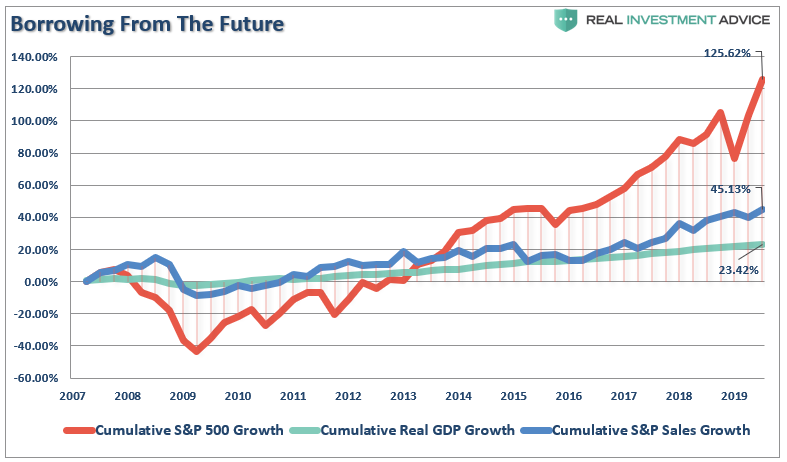

The stock market has returned more than 125% since 2007 peak, which is roughly 3x the growth in corporate sales and 5x more than GDP.

It is critical to remember the stock market is NOT the economy. The stock market should be reflective of underlying economic growth which drives actual revenue growth. Furthermore, GDP growth and stock returns are not highly correlated. In fact, some analysis suggests that they are negatively correlated and perhaps fairly strongly so (-0.40).

However, in the meantime, the promise of another decade of a continued bull market is very enticing as the “fear of missing out” overrides the “fear of loss.”

Let me conclude with this quote from Vitaliy Katsenelson which sums up our investing view:

“Our goal is to win a war, and to do that we may need to lose a few battles in the interim.

Yes, we want to make money, but it is even more important not to lose it. If the market continues to mount even higher, we will likely lag behind. The stocks we own will become fully valued, and we’ll sell them. If our cash balances continue to rise, then they will. We are not going to sacrifice our standards and thus let our portfolio be a byproduct of forced or irrational decisions.

We are willing to lose a few battles, but those losses will be necessary to win the war. Timing the market is an impossible endeavor. We don’t know anyone who has done it successfully on a consistent and repeated basis. In the short run, stock market movements are completely random – as random as you’re trying to guess the next card at the blackjack table.”

For long-term investors, the reality that a clearly overpriced market will eventually mean revert should be a clear warning sign. Given the exceptionally high probability the next decade will be disappointing, gambling your financial future on a 100% stock portfolio is likely not advisable.

Shiller’s CAPE – Is There A Better Measure?

In “Part 1” of this series, I discussed at length whether Dr. Robert Shiller’s 10-year cyclically adjusted price-earnings ratio was indeed just “B.S.” The primary message, of course, was simply:

“Valuation measures are simply just that – a measure of current valuation. If you ‘overpay’ for something today, the future net return will be lower than if you had paid a discount for it.

Valuation models are not, and were never meant to be, ‘market timing indicators.'”

With that said, in this missive I want to address some of the current, and valid, arguments against a long term smoothed price/earnings model:

Beginning in 2009, FASB Rule 157 was “temporarily” repealed in order to allow banks to “value” illiquid assets, such as real estate or mortgage-backed securities, at levels they felt were more appropriate rather than on the last actual “sale price” of a similar asset. This was done to keep banks solvent at the time as they were being forced to write down billions of dollars of assets on their books. This boosted banks profitability and made earnings appear higher than they may have been otherwise. The ‘repeal” of Rule 157 is still in effect today, and the subsequent “mark-to-myth” accounting rule is still inflating earnings.

The heavy use of off-balance sheet vehicles to suppress corporate debt and leverage levels and boost earnings is also a relatively new distortion.

Extensive cost-cutting, productivity enhancements, off-shoring of labor, etc. are all being heavily employed to boost earnings in a relatively weak revenue growth environment. I addressed this issue specifically in this past weekend’s newsletter:

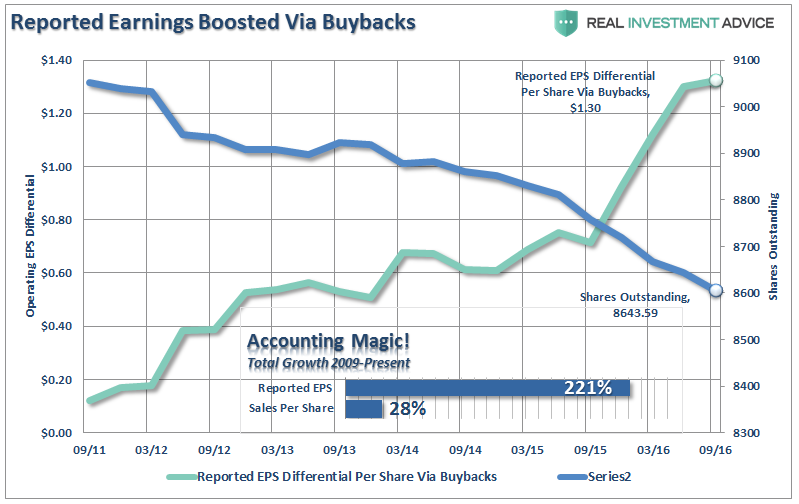

“What has also been stunning is the surge in corporate profitability despite a lack of revenue growth. Since 2009, the reported earnings per share of corporations has increased by a total of 221%. This is the sharpest post-recession rise in reported EPS in history. However, that sharp increase in earnings did not come from revenue which is reported at the top line of the income statement. Revenue from sales of goods and services has only increased by a marginal 28% during the same period.”

The use of share buybacks improves underlying earnings per share which also distorts long-term valuation metrics. AstheWSJ article stated:

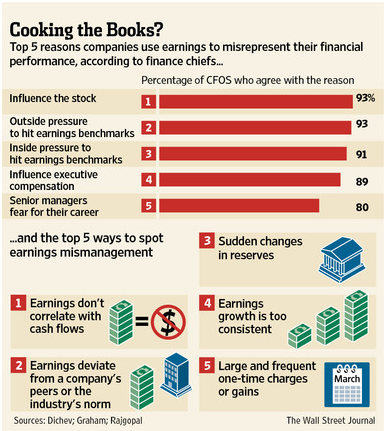

“If you believe a recent academic study, one out of five [20%] U.S. finance chiefs have been scrambling to fiddle with their companies’ earnings.

Not Enron-style, fraudulent fiddles, mind you. More like clever—and legal—exploitations of accounting standards that ‘manage earnings to misrepresent [the company’s] economic performance,’ according to the study’s authors, Ilia Dichev and Shiva Rajgopal of Emory University and John Graham of Duke University. Lightly searing the books rather than cooking them, if you like.”

This should not come as a major surprise as it is a rather “open secret.” Companies manipulate bottom line earnings by utilizing “cookie-jar” reserves, heavy use of accruals, and other accounting instruments to either flatter, or depress, earnings.

“The tricks are well-known: A difficult quarter can be made easier by releasing reserves set aside for a rainy day or recognizing revenues before sales are made, while a good quarter is often the time to hide a big “restructuring charge” that would otherwise stand out like a sore thumb.

What is more surprising though is CFOs’ belief that these practices leave a significant mark on companies’ reported profits and losses. When asked about the magnitude of the earnings misrepresentation, the study’s respondents said it was around 10% of earnings per share.“

As shown, it is not surprising to see that 93% of the respondents pointed to “influence on stock price” and “outside pressure” as the reason for manipulating earnings figures.

The extensive interventions by Central Banks globally are also contributing to the distortion of markets.

Due to these extensive changes to the financial markets since the turn of the century, I do not completely disagree with the argument that using a 10-year average to smooth earnings volatility may be too long of a period.

Duration Mismatch

Think about it this way. When constructing a portfolio that contains fixed income one of the most important risks to consider is a “duration mismatch.” For example, let’s assume an individual buys a 20-year bond, but needs the money in 10-years. Since the purpose of owning a bond was capital preservation and income, the duration mismatch leads to a potential loss of capital if interest rates have risen at the time the bond is sold 10-years prior to maturity.

One could reasonably argue, due to the “speed of movement” in the financial markets, a shortening of business cycles, and increased liquidity, there is a “duration mismatch” between Shiller’s 10-year CAPE and the financial markets currently.

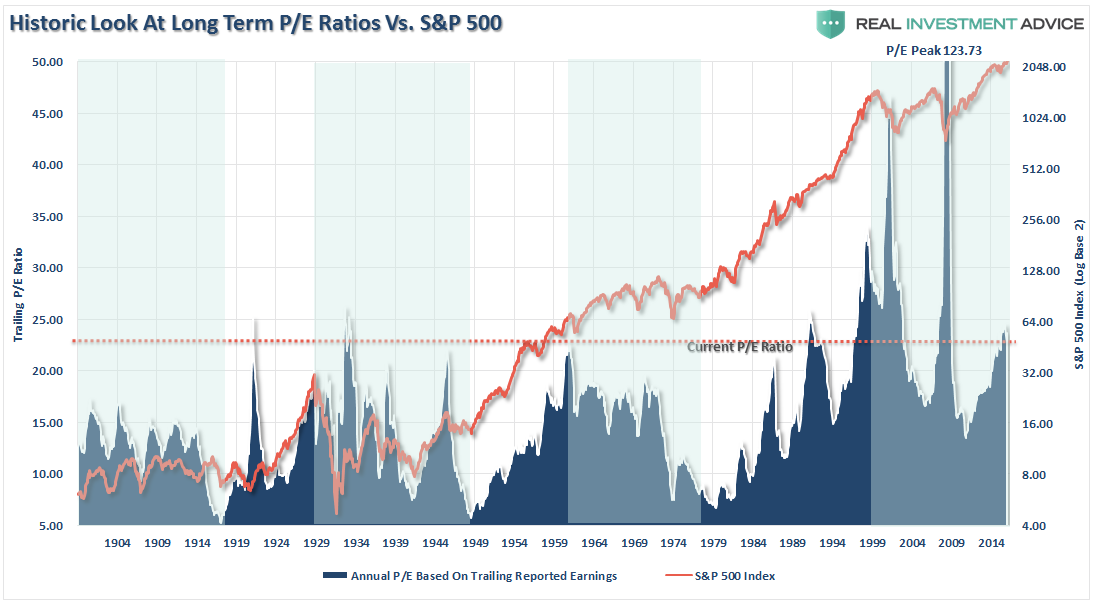

The first chart below shows the annual P/E ratio versus the inflation-adjusted (real) S&P 500 index.

Importantly, you will notice that during secular bear market periods (green shaded areas) the overall trend of P/E ratios is declining. This “valuation compression” is a function of the overall business cycle as “over-valuation” levels are “mean reverted” over time. You will also notice that market prices are generally “sideways” trending during these periods with increased volatility.

You can also see the vastly increased valuation swings since the turn of the century, which is one of the primary arguments against Dr. Shiller’s 10-Year CAPE ratio.

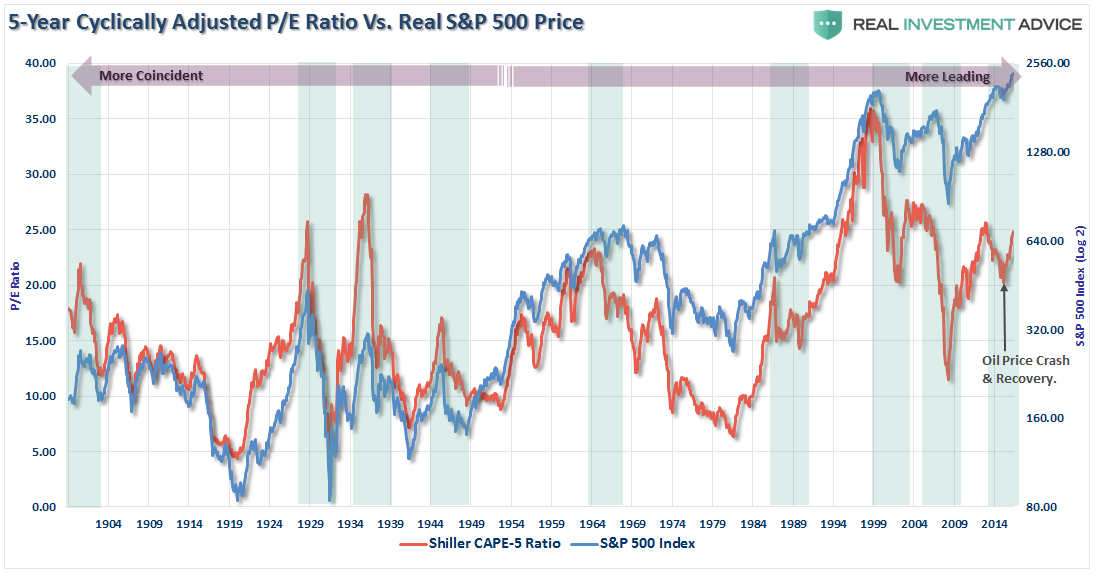

Introducing The CAPE-5 Ratio

The need to smooth earnings volatility is necessary to get a better understanding of what the underlying trend of valuations actually is. For investor’s periods of “valuation expansion” are where the bulk of the gains in the financial markets have been made over the last 116 years. History shows, that during periods of “valuation compression” returns are much more muted and volatile.

Therefore, in order to compensate for the potential “duration mismatch” of a faster moving market environment, I recalculated the CAPE ratio using a 5-year average as shown in the chart below.

There is a high correlation between the movements of the CAPE-5 and the S&P 500 index. However, you will notice that prior to 1950 the movements of valuations were more coincident with the overall index as price movement was a primary driver of the valuation metric. As earnings growth began to advance much more quickly post-1950, price movement became less of a dominating factor. Therefore, you can see that the CAPE-5 ratio began to lead overall price changes.

A key “warning” for investors, since 1950, has been a decline in the CAPE-5 ratio which has tended to lead price declines in the overall market. The recent decline in the CAPE-5, which was directly related to the collapse and recovery in oil prices, has so far been an outlier event. However, complacency “this time is different,” will likely be misplaced as the corrective trend currently remains intact.

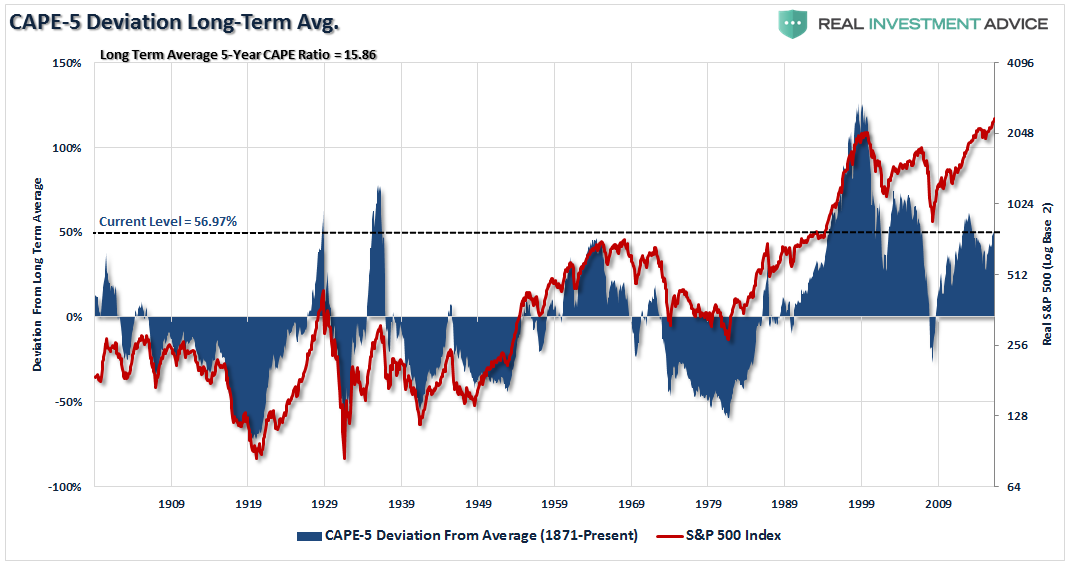

To get a better understanding of where valuations are currently relative to past history, we can look at the deviation between current valuation levels and the long-term average. The importance of deviation is crucial to understand. In order for there to be an “average,” valuations had to be both above and below that “average” over history. These “averages” provide a gravitational pull on valuations over time which is why the further the deviation is away from the “average,” the greater the eventual “mean reversion” will be.

The first chart below is the percentage deviation of the CAPE-5 ratio from its long-term average going back to 1900.

Currently, the 56.97% deviation above the long-term CAPE-5 average of 15.86x earnings puts valuations at levels only witnessed five (5) other times in history. As stated above, while it is hoped “this time will be different,” which were the same words uttered during each of the five previous periods, you can clearly see that the eventual results were much less optimal.

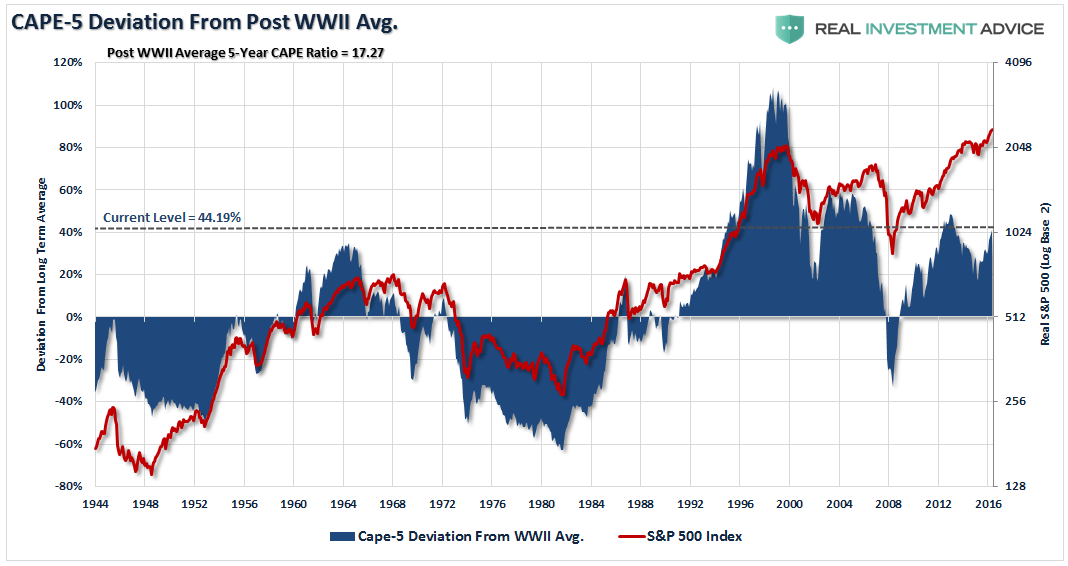

However, as noted, the changes that have occurred Post-WWII in terms of economic prosperity, changes in operational capacity and productivity warrant a look at just the period from 1944-present.

Again, as with the long-term view above, the current deviation is 44.19% above the Post-WWII CAPE-5 average of 17.27x earnings. Such a level of deviation has only been witnessed three times previously over the last 70 years in 1996, 2005 and 2013. Again, as with the long-term view above, the resulting “reversion” was not kind to investors.

Is this a better measure than Shiller’s CAPE-10 ratio?

Maybe, as it adjusts more quickly to a faster moving marketplace. However, I want to reiterate that neither the Shiller’s CAPE-10 ratio or the modified CAPE-5 ratio were ever meant to be “market timing” indicators.

Since valuations determine forward returns, the sole purpose is to denote periods which carry exceptionally high levels of investment risk and resulted in exceptionally poor levels of future returns.

Currently, valuation measures are clearly warning the future market returns are going to be substantially lower than they have been over the past eight years. Therefore,if you are expecting the markets to crank out 10% annualized returns over the next 10 years for you to meet your retirement goals, it is likely that you are going to be very disappointed.

We respect your privacy and will only send you email that is related to what you subscribed to and why you subscribed. You can unsubscribe whenever you want with just a click of your mouse. For more information please see... Disclosure & Privacy Policy.