Robertson: When “Stuff” Gets Real

We all can be tempted to follow the path of least resistance and in a competitive world there are always incentives to get the most bang for the buck. Often this means taking shortcuts to gain some advantage. In a forgiving world, the penalties for such transgressions tend to be small but the rewards can be significant. When conditions are extremely forgiving, shortcuts can become so pervasive that failing to take them can be a competitive disadvantage.

In a less forgiving world, however, the deal gets completely flipped around and penalties can be significant for those who take shortcuts. This will be important for investors to keep in mind as rapidly weakening economic fundamentals and increasing stress in financial markets make for far less forgiving conditions. When things get real, competence and merit matter again – and this is a crucial lesson for investors.

Leaders of companies and organizations normally receive a lot of attention and rightly so; their decisions and behaviors affect a lot people. In the best of situations, leaders can distinguish themselves by creatively finding a “third” way to resolve difficult challenges. In other situations, however, leaders can reveal all-too-human weakness by taking shortcuts, cheating, and acting excessively in their own self-interest.

One of the situations in which these weaknesses can be spotted is in whistleblower incidents. For example, the Financial Times reported on the illuminating experiences of one HR director who in successive jobs was requested to break rules by a boss:

“Told by a senior manager at a FTSE 100 business to rig a pay review to favour his allies, she refused. ‘After that, he did everything to make my life absolute hell,’ she says. Then, at the first opportunity, he fired her, claiming that she was underperforming. Warned that the company would use its resources to fight her all the way if she took legal action, she accepted a pay-off and left’.”

“Her next employer asked her to manipulate the numbers for a statutory reporting requirement to make its performance look better. She refused, signed another non-disclosure agreement and resigned.”

As unfortunate as these experiences were, they were not isolated events. The HR director described such incidents as happening “left, right and centre”. The fact that such cases are extremely hard to prosecute in any meaningful way helps explain why they are so pervasive. Columbia law professor John Coffee describes: “It’s extremely difficult to make a case against the senior executives because they don’t get Involved in operational issues. But they can put extreme pressure on the lower echelons to cut costs or hit targets.”

Company employees aren’t the only ones who risk facing hostility for standing for what they believe is right. Anjana Ahuja reports in the FT that scientists can fall victim to the same abuses. As she points out, “Some are targeted by industry or fringe groups; others, as the Scholars at Risk network points out, by their own governments. The academic freedom to tell inconvenient truths is being eroded even in supposed strong holds of democracy.”

Ahuja noted that the Canadian pharmacist and blogger, Olivier Bernard, was chastised for “interrogating the claim that vitamin C injections can treat cancer.” As a consequence of his efforts, “He endured death threats” and “opponents demanded his sacking.”

In yet another example, Greece’s former chief statistician Andreas Georgiou “has been repeatedly convicted, and acquitted on appeal, of manipulating data.” The rationale for such a harsh response has nothing to do with merit: “statisticians worldwide insist that Mr Georgiou has been victimised for refusing to massage fiscal numbers.” It is simply a higher profile case of refusing to be complicit in wrongdoing.

The lessons from these anecdotes also play out across the broader population. The FT reports:

“According to the [CIPD human resources survey], 28 per cent of HR personnel perceive a conflict between their professional judgment and what their organisation expects of them; the same proportion feel ‘it’s often necessary to compromise ethical values to succeed in their organisation’.”

Employees are all-too familiar with the reality that such compromises may be required simply to survive in an organization and to continue getting health insurance: “Most HR directors know colleagues who have been fired for standing their ground.”

Yet another arena in which expertise and values get compromised is politics. While political rhetoric nearly always involves exaggerations and simplifications, the cost of such manipulations becomes apparent when important issues of public policy are at stake. Bill Blain highlighted this point on Zerohedge:

“It’s as clear as a bell that Trump had no plan to address the Coronavirus before he was finally forced to say something Monday [March 9, 2020]. Until then it was a ‘fake-news’ distraction. He made a political gamble: that the virus would recede before it became a crisis, making him look smart and a market genius for calling it.”

Blain’s assessment illustrates a point that is common to all these examples: Each involves a calculation as to whether it is worth it or not to do the right thing based on merit or to take a shortcut. Each involves an intentional effort to reject/deny/attack positions that are real and valid. Evidence, expertise and professional judgment are foresworn and replaced by narrative, heuristics, and misinformation. While such tactics undermine the long-term success of organizations and societies, they can yield tremendous personal advantages. The good of the whole is sacrificed for the good of the few.

Another point is that these efforts are absolutely pervasive. They can be found across companies, academia, politics, and beyond. They can also be found in countries all across the world. In an important sense, we have been living in an environment of pervasive tolerance of such decisions.

A third point, and the most important one, is that now it is starting to matter. It appears that the real human impact of the coronavirus has shaken many people out of complacency. The types of narratives and misinformation regarding the market that had been accepted suddenly seem woefully out of place when dealing with a real threat to public health. As Janan Ganesh reports in the FT, “This year provides a far less hospitable atmosphere for such hokum than 2016”. He concludes, “Overnight, competence matters.”

True enough, but Ganesh could have gone further. Suddenly, additional traits such as courage, good judgment, and ethical behavior also matter. Overnight, carelessness and complacency have become much more costly.

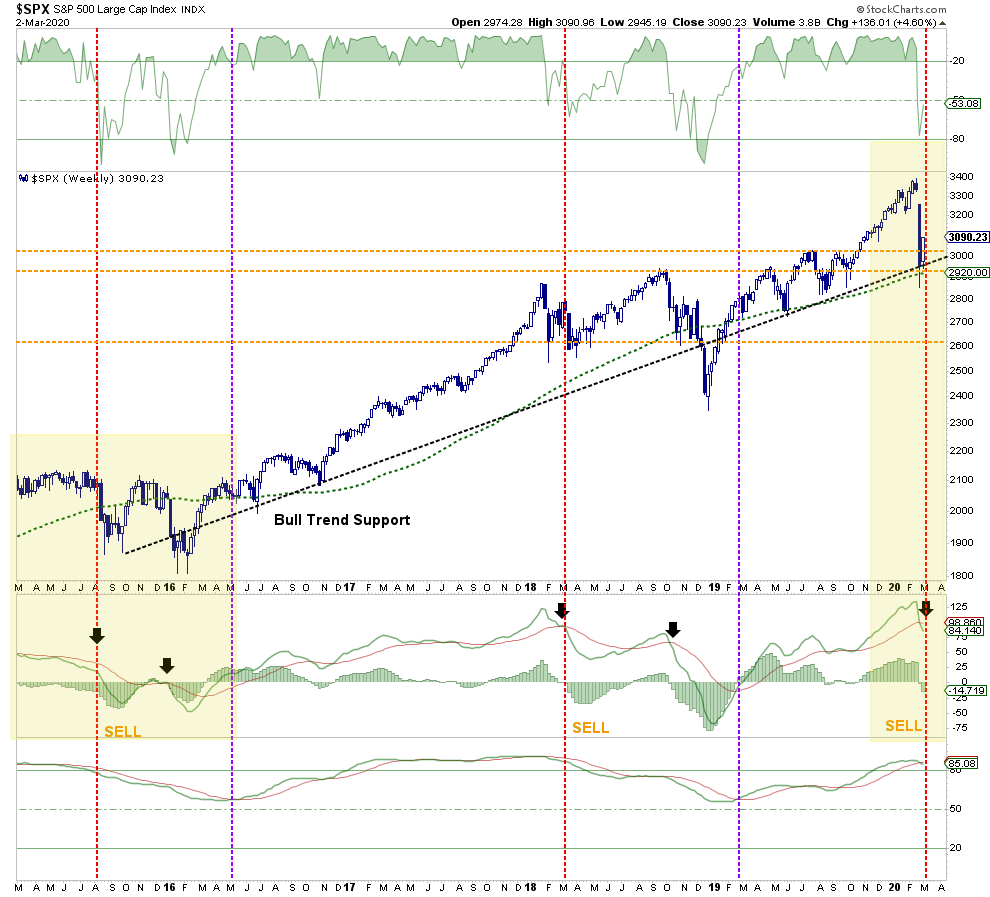

All these things will become extremely important for investors as well. For example, information sources are crucial for early identification of potential problems and for proper diagnosis. Most mainstream news outlets were slow to report on the threat of the coronavirus even though it was clearly a problem in China in January. By far the best sources on this issue have been a handful of independent researchers and bloggers who have shared their insights publicly.

One form of news that will be interesting to monitor is upcoming earnings reports and conference calls. These events can provide an opportunity to learn about companies as well as to learn about management’s philosophy and decision-making.

Which companies are busily responding to the crisis by scrutinizing their supply chains and developing HR policies to ensure the safety of their employees? Which companies already had these measures in place and are simply executing on them now? Which companies are withdrawing guidance while they frantically try to figure out what’s going on? These responses will reveal a great deal about management teams and business models.

In addition, a much higher premium on merit will also place much higher premia on security analysis, valuation, and risk management. Alluring stories about stocks and narratives about the market can be fun to follow and even compelling. At the end of the day, however, what really matters is streams of cash flows.

Finally, a higher premium on merit is likely to significantly re-order the ranks of advisors and money managers. Those ridiculed as “overly cautious” and “perma bears” will emerge as valuable protectors of capital. Conversely, those arguing that there is no alternative (TINA) to equities will be spending a lot of time trying to pacify (and retain) angry clients who suffer big losses. Further, things like education, training, and experience will re-emerge as necessary credentials for investment professionals.

As the coronavirus continues to spread across the US, things are starting to get real for many investors. Suddenly, the world is appearing less forgiving as it is becoming clear that economic growth will slow substantially for some period of time. This especially exposes the many companies who have binged on debt while rates have been so low. Further, it is becoming increasingly obvious that there is very little the Fed can do with monetary policy to stimulate demand.

While the coronavirus will eventually dissipate, the increasing premium on merit is likely to hang around. The bad news is that in many cases it will be too late to avoid the harm caused by leaders and managers and advisors who exploited favorable conditions for personal advantage. The good news is that there are very competent people out there to make the best of things going forward.