Looking Beyond Apple and Microsoft

As the 1970s came to a close, six of the world’s ten largest companies were in the oil exploration, drilling, and services business. Just a few years earlier, on April 1, 1976, Steven Jobs and Steven Wozniak, two college dropouts working out of a garage, formed Apple Computers, Inc. In April 1975, Bill Gates and Paul Allen formed a company called Micro-Soft.

Four decades later, these two technology startups are the world’s largest companies, far surpassing the largest oil companies of the 1970s. In fact, the combined market capitalization of Microsoft and Apple is larger than the aggregate market cap of the domestic oil industry. Even more astounding, the combined market cap of Microsoft and Apple just surpassed the total market cap of the entire German stock market.

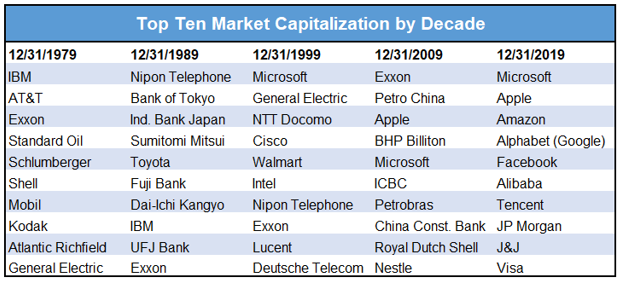

The table below shows the rotation of the world’s largest publically traded companies over the last fifty years. Of the companies shown below only five have been in the top ten for more than one decade.

Throughout history, most of the world’s largest companies are routinely supplanted by new and different companies from decade to decade. Furthermore, different industries tend to dominate each decade and then fade into the next decade as new industries dominate. For instance, in the 1970’s big oil accounted for six of the top ten largest companies. In the 1980’s, Japanese companies held eight of the top ten spots. In the 1990s it was telecom, the 2000s were controlled by banks and commodities, and this past decade was dominated by technology and social media companies.

Throughout history, most of the world’s largest companies are routinely supplanted by new and different companies from decade to decade. Furthermore, different industries tend to dominate each decade and then fade into the next decade as new industries dominate. For instance, in the 1970’s big oil accounted for six of the top ten largest companies. In the 1980’s, Japanese companies held eight of the top ten spots. In the 1990s it was telecom, the 2000s were controlled by banks and commodities, and this past decade was dominated by technology and social media companies.

While table offers several insights, we believe the most important lesson is that our investment strategies must focus on the future and our dependence on past strategies must be carefully considered. Today, two college dropouts in their parent’s basement fooling around with artificial intelligence, block chain, or robotics may prove to be worth more than Apple, Microsoft, or Amazon in just a few decades. The table also emphasizes the importance of selling high and rotating to that which has “value”.

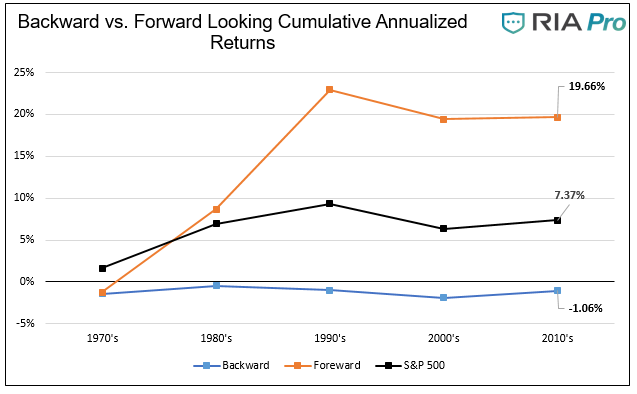

To emphasize that point, we constructed the following graph. Although simple, it effectively illustrates the theme by comparing one stock looking backward and one stock looking forward as an investment strategy. The backward-looking strategy (blue line) buys the largest company at the end of each decade and holds it through the following decade. The forward-looking strategy (orange line), with the gift of 20/20 foresight, buys the company that will be the largest company at the end of the new decade and holds it for that decade. For example, on January 1, 2010, the forward-looking strategy bought Microsoft and held it until December 31, 2019, while the backward-looking strategy bought Exxon and held it over the same period.

Due to the split-up of AT&T and poor price data, we used GM data which had the second largest market capitalization in 1969. For similar reasons, we also replaced Nippon Telephone and Telegraph (NTT) with The Bank of Tokyo. The graph is based on share price returns and is not inclusive of dividends.

The forward strategy beat the S&P 500 by over 12% a year, while the backward-looking strategy grossly underperformed with a negative cumulative annualized price return over the last 50 years. As startling as the differences are, they fail to provide proper context for the value of 50 years of compounding at the annualized rates of return as shown. If all three portfolios started with $100,000, the backward-looking portfolio would be worth $59,000 today, the S&P 500 worth $3,500,000 today, and the forward-looking portfolio would be worth $791,000,000 today.

Summary

Although no one knows what the top ten list will look like on December 31, 2029, we do know that the next ten years will not be like the last ten. The 2000’s brought two recessions and for the first time in recorded history, the 2010s brought NO recessions. Investors need to be opportunistic, flexible, creative and forward-looking in choosing investments. Investing in today’s winners is not likely to yield us the results of yesterday. It is difficult to fathom as Apple and Microsoft drive the entire market higher, but history warns that their breath-taking returns of the last decade should not be expected in the 2020’s. In fact, history and prudence argue one should sell high.