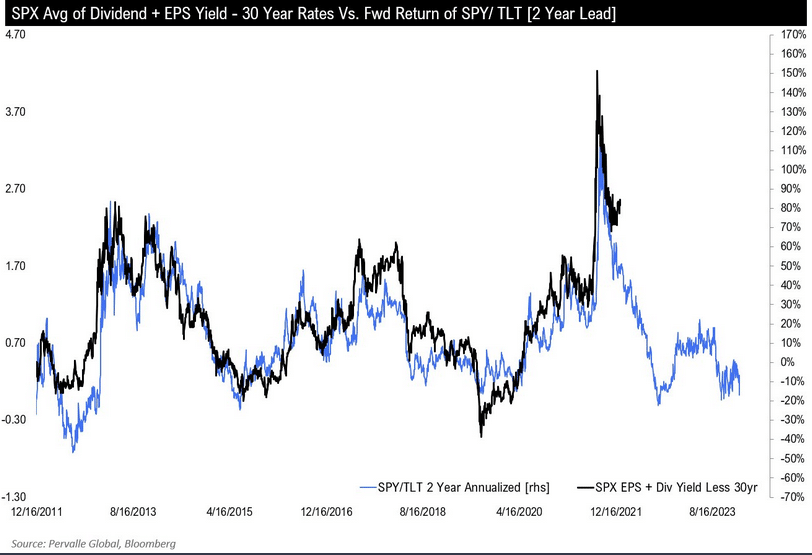

Many investors are frequently reallocating their holdings between stocks and bonds. This year, figuring out the correct ratio of stocks to bonds has been difficult as both have performed similarly poorly. While it is tempting to assume that stocks will outperform bonds as they tend to do over longer periods, the graph below from Pervalle Global provides insight into the relative performance we should expect between stocks and bonds over the next two years.

The graph compares the return of the price ratio of SPY to TLT versus the average of the S&P 500 dividend yield and earnings yield less the thirty-year US Treasury yield. If the correlation holds, TLT may significantly outperform SPY over the coming year.

Per the chart creator, Teddy Vallee: “The regression implies a negative return for stocks relative to bonds 2 years out.“

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Sept. 23 (3.8% prior)

- 8:30 a.m. ET: Advance Goods Trade Balance, August (-$89.0 billion expected, -$89.1 billion prior)

- 8:30 a.m. ET: Wholesale Inventories, month-over-month, August preliminary (0.4% expected, 0.6% prior)

- 8:30 a.m. ET: Retail Inventories, month-over-month, August (1.0% expected, 1.1% prior)

- 10:00 a.m. ET: Pending Home Sales, month-over-month, August (-1.5% expected, -1.0% prior)

- 10:00 a.m. ET: Pending Home Sales NSA, year-over-year, August (-24.5% prior)

Earnings

Market Trading Update

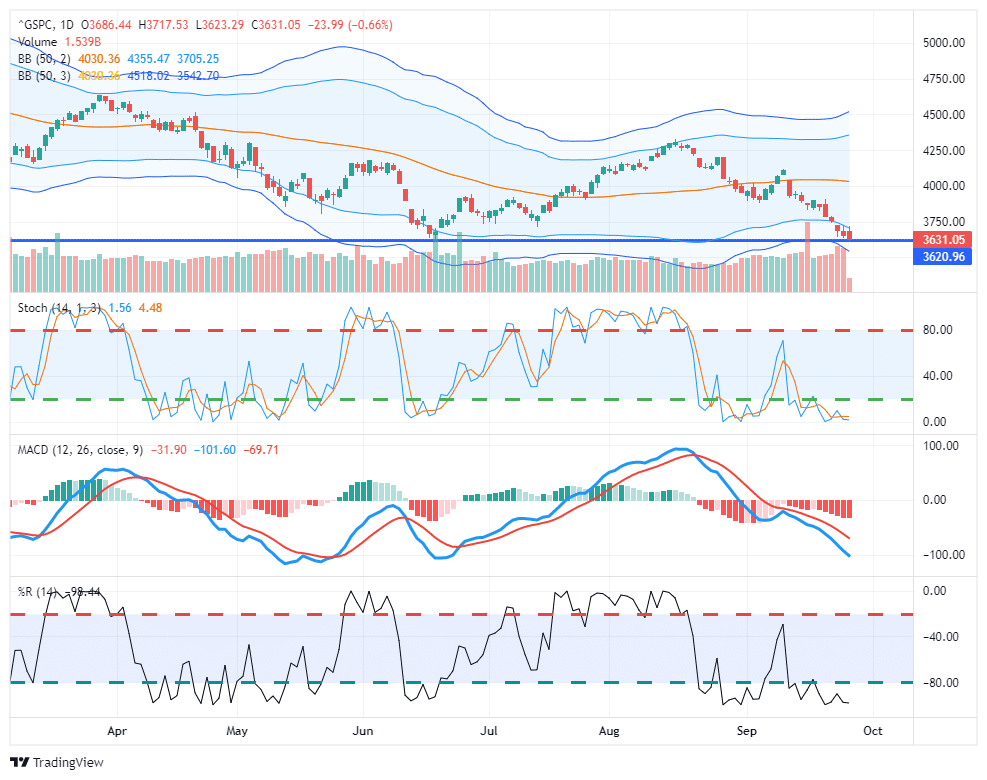

The market tried to rally yesterday morning until St. Louis Fed President, James Bullard, reiterated the Fed’s “hawkish stance” of combatting inflation at all costs. That language sucked the air out of the stock and bond rally, sending yields up and stocks down. Currently, the market is holding support at the June lows and is extremely oversold, pushing well into 3 standard deviations below the 50-dma. As yesterday’s blog post noted, the setup for a relatively strong “short squeeze” is in place. Use that rally to reduce risk and raise cash accordingly.

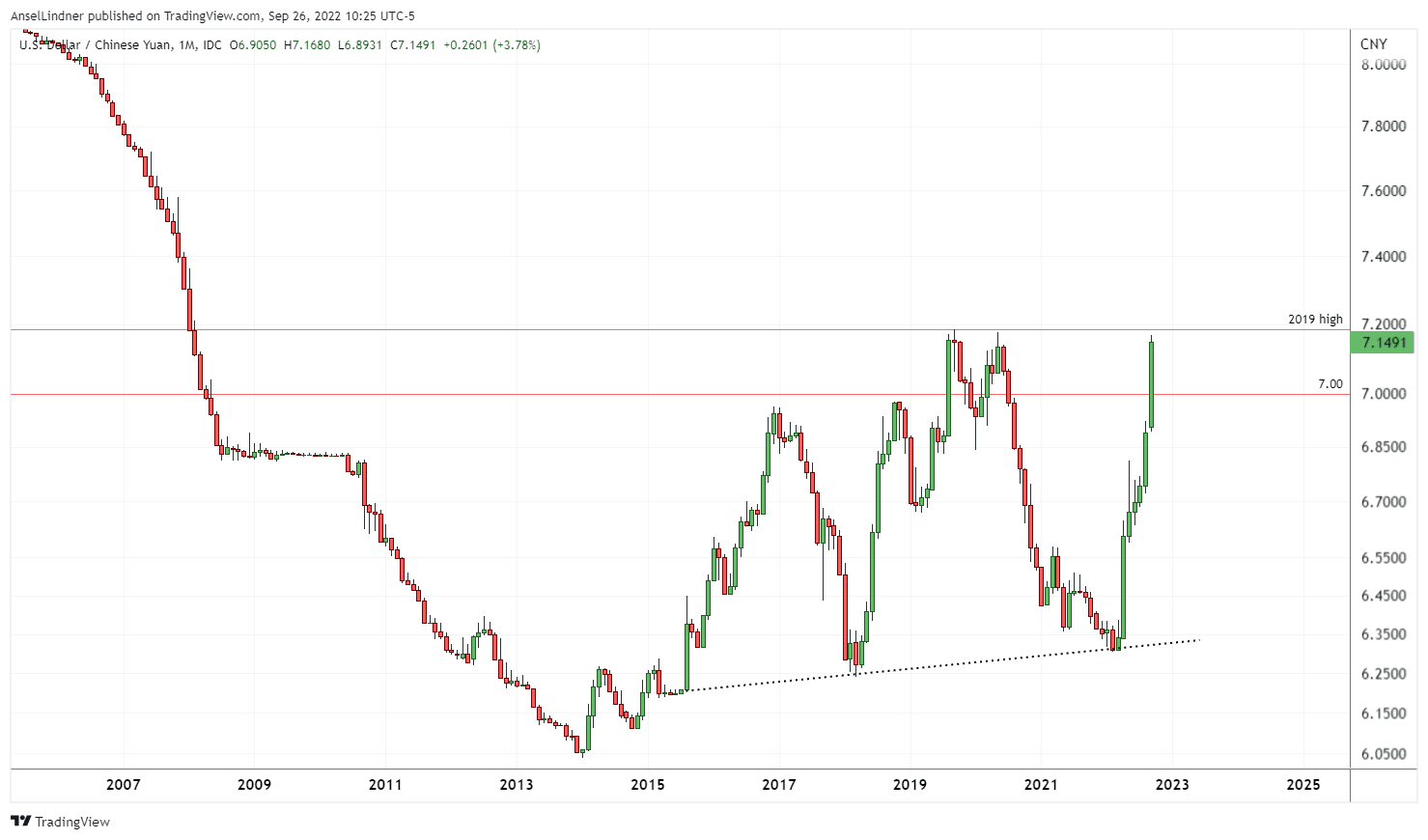

Et Tu China Yuan?

We have been focusing on the rapid depreciation of the British pound, euro, and Japanese yen over the past few months. There is another currency in similar shoes as those well-followed currencies. The Chinese yuan, as shown below, has been depreciating versus the dollar. The yuan now sits at similar levels as its peaks in 2019 and March 2020. Before those peaks, one has to go back to 2008 to find similar levels.

The strong dollar means China must weaken its currency to avoid the yuan appreciating in line with the dollar. Doing so makes its products more expensive for foreign nations. As a substantial exporting nation, it must be careful to retain its pricing edge. While trying to stay competitive by weakening the yuan, such actions spark fears that capital will leave China to avoid depreciation. Accordingly, capital outflows can build on themselves and leave the Chinese government in a precarious position.

Bank Risk Rising

Yesterday’s Commentary showed how CDS (credit default swaps) rates are rising for the United Kingdom. A UK default is not likely. However, investors are hedging bets against such an event. It’s not just the UK or other nations with rising CDS rates, as the graph below shows. In all six instances, the five-year CDS of the major banks and brokers are trading at their highest levels since the pandemic first broke out. The graphs below and the UK graph are not dire by any stretch, but they point to rising risks. Further, if they continue to increase, financial instability will become a concern for the Fed. As we wrote yesterday, the Fed considers financial stability their third mandate. It will do whatever it takes to provide ample liquidity to the financial markets and critical financial institutions well before a “Lehman moment” surfaces.

Easing Housing Fears

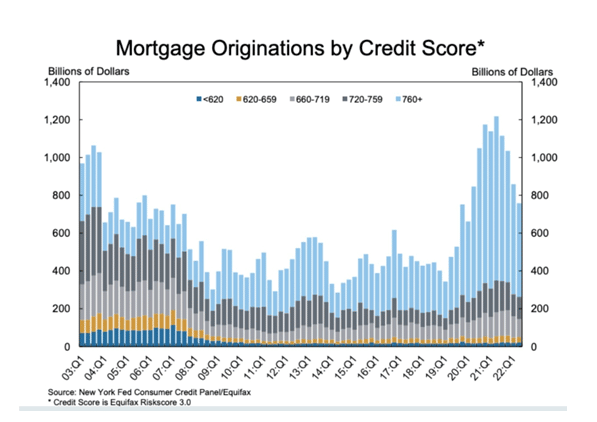

Sam Ro of Yahoo put out an article with a few good graphs to help ease concerns that some similarities, like surging prices and higher mortgage rates that triggered the financial crisis, are occurring today. Per Sam:

“First, lenders have been much more disciplined with their lending practices. According to New York Fed data, the vast majority of new mortgage loans in recent years have gone to prime borrowers with the highest credit scores.“

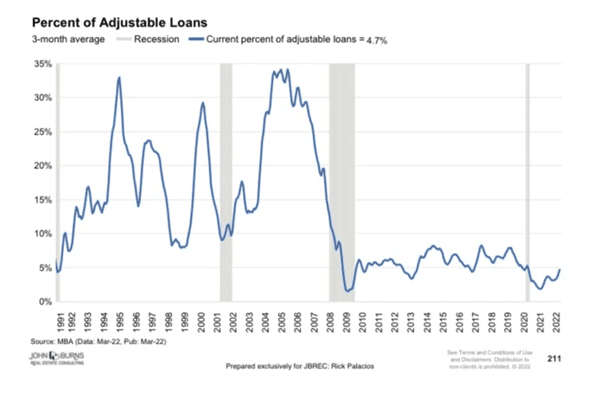

“Second, adjustable rate mortgages are nowhere near as popular as they were during the housing bubble. This means very few new buyers are vulnerable to interest rate volatility.”

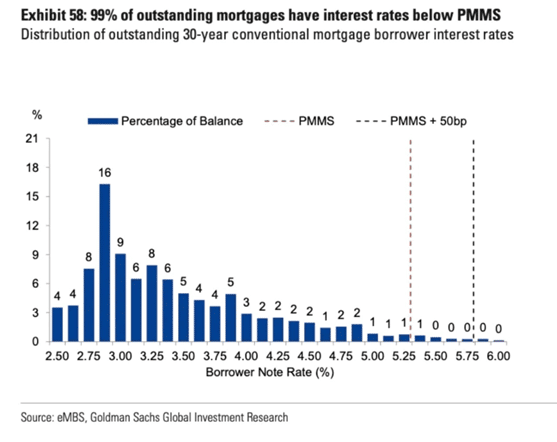

“Third, about 99% of outstanding mortgages have a locked-in rate that’s lower than the current market rate, according to Goldman Sachs analysts. In other words, the vast majority of homeowners are not materially affected by rising mortgage rates.”

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read